Abstract

Local jurisdictions across the country continue to adopt alternative financing options, although the effects of these remain uncertain. There are two views of impact fees: (a) an old view, that fees are a tax on development increasing prices and reducing quantity and (b) a new view, that fees provide services and reduce future taxes, thus increasing demand and prices. The research presented in this study, based on data from Florida counties, finds that the relationship between fees on commercial development and fees on employment differs across different categories of economic activity. The use of fees is positively related to service-sector employment growth and negatively related to manufacturing employment growth. This result suggests that different sectors realize different levels of benefits from infrastructure provided through fee revenue and that policy decisions based on total employment may suffer from overaggregations and lead to unintended consequences.

Over the past several decades, local governments have diversified their revenue sources, increasing the variation between jurisdictions, yet the relationships between these newer funding mechanisms, employment levels, and the composition of that employment are not yet fully understood. Traditional property taxes spread the burden across asset owners, whereas fees, sales taxes, and other alternative financing mechanisms can to some extent allocate the costs to specific benefit recipients, future generations, and visiting consumers. One such alternative to the property tax is development impact fees: large fees whose revenues are earmarked for infrastructure to support new development. Casual observation reveals that many existing residents balk at taxes used to finance the construction of additional infrastructure to support new development and benefit new residents. Yet more targeted revenue mechanisms may have distortionary effects. Impact fees are one solution that potentially satisfies the political constraints of requiring that new development pay its own way and the pragmatic requirement that infrastructure service levels be maintained to at least some minimum level. Although the use of fees is not new, their effects on development, incidence, and employment distortions remain somewhat open for discussion.

In theory, fees are a Pigouvian-style tax on development, forcing developers to consider their social costs. Anderson (2004) and Brueckner (1997) suggest that fees are a theoretically efficient way of paying for infrastructure for a single jurisdiction; how these fees affect employment is an issue yet to be settled. Although it could be argued that the fees are another cost and therefore reduce employment, it could also be argued that they are the purchase of publicly provided inputs and therefore positively contribute to employment. One possible resolution to the differing conclusions is that the effect of fees differs across categories of economic activity of employment. For example, it may be more difficult for geographically constrained service industries to avoid fees than for manufacturing or other industrial activities to do so; thus, fees potentially affect the composition of employment.

Background/Literature Review

Among the alternatives to traditional property taxes are sales taxes, user fees, and development impact fees. Impact fees are politically popular for two reasons: (a) the fees are charged to developers, which placates existing residents and voters who object to paying for additional infrastructure to support new development, as suggested by Anderson (2005), although how much of the burden developers actually bear is the subject of much research, and (b) the fees are popular with policy wonks because the fees move infrastructure financing closer to marginal cost pricing for development and are often seen as corrective taxes, an idea popularized by Turnbull (1988). Critics argue that fees are an excise tax that makes housing more expensive, thus limiting affordable housing and pushing economic development to other jurisdictions. Developers also often argue, albeit privately and not publicly, that the fees break a social contract where residents are provided infrastructure by existing and prior residents and implicitly agree to provide funding for the construction of future infrastructure to serve additional residents.

Whereas there is a growing literature examining the effect of impact fees on residential home prices, the empirical literature on their effect on economic development is relatively thin. The notable exceptions are Nelson and Moody (2003), who find a positive correlation between fees per building permit and job growth, and Jeong and Feiock (2006), who find that counties with fees grow at a faster rate. However, the more recent literature, such as G. Burge and Ihlanfeldt (2009), has raised questions about the causality of the relationship. G. Burge and Ihlanfeldt find that an increase in the amount of fees required leads to a reduction in employment levels over a 2-year time period. This research expands on G. Burge and Ihlanfeldt’s work to examine the effect of fees on different categories of employment.

Although a full literature review of the research on how fees affect residential development is beyond the scope of this study, it is instructive to frame the analysis of fees’ effect on economic development using theory developed in the residential literature. Altshuler, Gómez-Ibáñez, and Howitt (1993) give an excellent history of the evolution of development exactions into a system of fees. Initially, jurisdictions negotiated exactions of in-kind donations for development approval; that is, land for a school or right-of-way. However, these exactions were often land that was not usable or poorly located for its intended purpose. Over time, a system of fees evolved that had benefits for both local officials and developers. Developers preferred the fees to exactions because they were more predictable, and politicians preferred the fees instead of having to defend every exaction to a constituency that believed the officials were outmaneuvered by the developers (Altshuler et al., 1993). Ihlanfeldt and Shaughnessy (2004) provide a summary of how the theory of fees has evolved over time to incorporate infrastructure services and model fees as more than simply a tax. For a more in-depth review of the residential literature, Burge, Nelson, and Matthews (2007) give an excellent overview of price effects, housing construction effects, and economic development.

There are two schools of thought in the housing literature, for which Ihlanfeldt and Shaughnessy (2004) coined the terms “the old view” and “the new view.” The old view considers a system of fees to be an excise tax on development resulting in lower land prices, reduced developer profits, higher home prices, and a decrease in the quantity of new homes supplied. This view implicitly assumes that the revenues from the fees are used for purposes that provide little to no benefit to the development assessed the fee. The new view, as explained by Ihlanfeldt and Shaughnessy (2004), who base it on Yinger (1998), broadens the model to consider the benefits of the additional infrastructure and allows for a structural break in the social contract of infrastructure provision. Home purchasers capitalize the reduction of future property tax liabilities in the form of higher home prices, following the switch from property tax financing to fee financing of infrastructure to serve new development. This more general model suggests that both old and new home prices will increase by the same amount and allows for the possibility that prices may increase by an amount greater than the fee and that land prices may either increase or decrease following the imposition of a fee system.

Using their “new view” model, Ihlanfeldt and Shaughnessy (2004) find that home prices increase by more than the amount of the fee, indicating that home buyers recognize the value of the services provided and are capitalizing the reduction of future taxes into home prices. However, Ihlanfeldt and Shaughnessy also find that land values fall by approximately the same amount as the fee, a result inconsistent with their theory. They suggest that this finding could be the result of developers “pricing in” the risk that fees increase between the time when the land is purchased and the time of building permit issuance, when the fee is paid. Evans-Cowley, Forgey, and Rutherford’s (2005) findings support Ihlanfedlt and Shaughnessy’s (2004) assertion of a negative effect on land prices owing to uncertainty regarding fee levels. Using municipal data from Texas, Evans-Cowley et al. (2005) break land into two categories: (a) land and (b) lots. They find that fees have a negative but minimal effect on land but a positive effect on the price of lots. Because fees are often paid at the time of platting in Texas, as opposed to the time of building-permit issuance in most other states, their results are consistent with Ihlanfeldt and Shaughnessy’s (2004) suggestion that the fall in land values is due to uncertainty; once the fee is paid and the uncertainty removed, the price should increase, as Evans-Cowley et al. (2005) find.

The theory developed and presented in the residential literature is instructive for framing the analysis presented in this study, as firms also derive value from infrastructure constructed with fee revenue and are forward-looking in their decision-making process. However, the degree to which they capitalize in or realize benefits from the infrastructure may be different from that of a resident. Although fees are not assessed directly on business expansion and subsequent employment growth, they are assessed on new construction, which is assumed to be correlated with employment expansion. Assuming firms wish to maintain the ratio between labor and capital, charging fees on construction could be construed as indirectly assessing fees on employment growth.

The Firm’s Location Problem

Firms weigh many different factors, including taxes and fees, before ultimately deciding on a location. The relative ability of a firm to avoid fees and still serve its intended market is a major factor in determining the incidence and employment effects of any fee system. Incorporating transport costs into a stylized profit maximization problem is one way to conceptualize a firm’s ability to serve a market from outside the jurisdiction and is instructive for considering a firm’s location choice under a system of fees. Obviously a firm would choose not to pay fees if it could still realize the benefits and suffer no other losses. For example, consider a firm that can avoid the fees by locating across the street from an alternative location and would realize the benefits of having access to the road regardless of which location is chosen. However, because of differing firm strategies, customer preferences, and other factors, not all firms will locate outside a jurisdiction to avoid fees. Nevertheless, with a system of fees in place, it is likely that some firms will choose to locate outside the fee-charging jurisdiction.

Suppose the firm has a choice between two jurisdictions separated by one unit of distance. One jurisdiction contains the firm’s customers and charges fees, and the other jurisdiction has no fees and is void of customers. Thus the firm maximizes profits, π, so that

where q is the quantity of the good sold, p is the price of each unit, c is the unit cost, t represents a per-unit distance transport cost, d is a unit of distance such that the firm is just able to avoid the fees, and f is the amount of the fee. A firm choosing the distance from its customers to maximize profits yields

Thus, if the transport costs associated with locating outside the jurisdiction containing the firm’s customers is equal to the fee charged to locate in the customer-containing jurisdiction,

Data

Assuming firms maximize profits leads one to believe that firms make location, size, and quantity decisions based on the markets they are looking to serve. The questions addressed in this study are whether fees are related to employment growth and whether the relationship differs across firm categories. Thirty years of employment and demographic data for counties in Florida are used to analyze the relationship between fees and employment. Florida and California are the two states where impact fees are most prevalent. Burge (2005) suggests that Florida data lend themselves to countywide analysis because counties, not municipalities, largely handle the impact fee collections countywide. Municipalities in Florida may also charge fees for services not provided by the county, but these cases are relatively insignificant when compared in size and prevalence with the county fee systems. 1

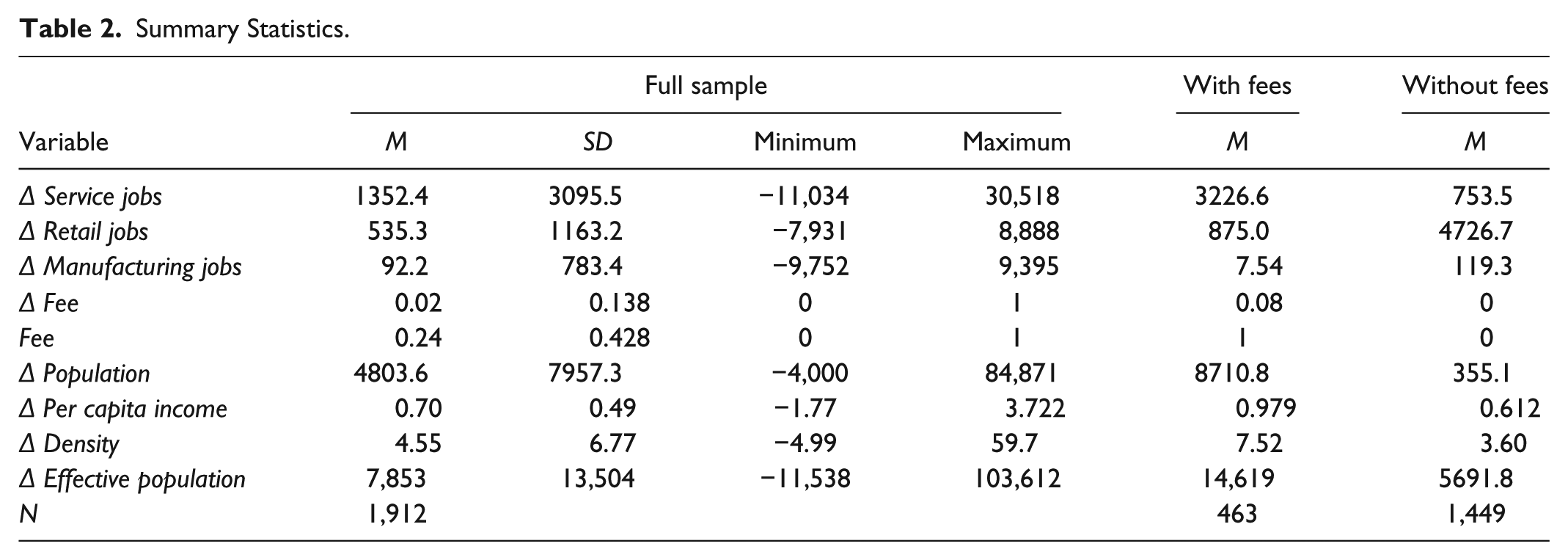

Employment data come from the Bureau of Economic Analysis’s (BEA) Local Areas Personal Income and Employment data sets spanning 1970 through 2000. The data are based on standard industrial classification (SIC) codes for consistency and overlaps the time period in which most counties adopted fees. Table 1 lists impact fee adoption dates by county as reported by Jeong (2006). Annual estimates of county population and changes in population (Δ population) come from the U.S. Census Bureau and are presented in Table 2 along with other sample statistics. Changes in annual per capita income (Δ per capita income) were calculated using income data from the BEA’s Personal Income Summary. Effective population and changes in effective population (Δ effective population) are based on the sum of population plus total employment across all categories and reflect the fact that firms serve more than just the residents of a particular jurisdiction.

Year of Impact Fee Adoption.

Source. Jeong (2006); G. Burge and Ihlanfeldt (2006).

Summary Statistics.

Table 2 gives sample statistics including county means for counties with and without fees. Of note is that counties without fees experienced larger increases in retail and manufacturing employment, but that counties with fees experienced larger increases in service employment, population, and income. Employment figures come from the BEA’s Local Areas Personal Income and Employment data and are divided according to their definitions. Manufacturing includes “establishments engaged in the mechanical or chemical transformation of materials or substances into new products.” 2 Retail employment includes “establishments engaged in selling merchandise for personal or household consumption and rendering services incidental to the sale of the goods.” Service employment includes “establishments primarily engaged in providing a wide variety of services for individuals, business and government establishments, and other organizations.”

Model

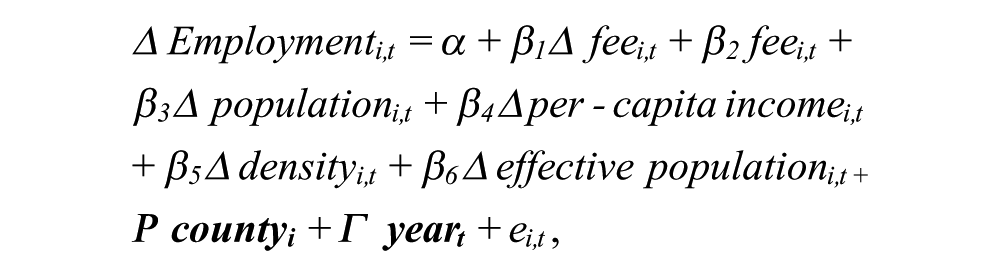

The firm’s location and employment decision is based on market factors and cost factors. The number of jobs available in a jurisdiction is dependent on many factors, some of which are relatively stable over time, such as geographic factors, and some that change, such as demographics. Although it is nearly impossible to collect data on all factors, the stable determinants, both observable and nonobservable, are removed from consideration by first differencing the data. To examine the relationship between impact fees and employment growth, the following equation is estimated using ordinary least squares:

where Δ employment is the annual change in employment, Δ fee is a binary variable indicating a county switched to fees during that year, and fee is a binary variable indicating a county has a fee system in place. The inclusion of Δ fee is to account for uncertainty during the transition to a fee system as opposed to the recurring relationship between fees and employment growth. If fees are correlated with reduced employment levels but not employment growth, then Δ fee is important. However, if the relationship is between the use of fees and employment growth, then fee is the important variable. For the sake of completeness, both are included. The other variables, Δ population, Δ per capita income, Δ density, and Δ effective population are included to control for changes in market size. Effective population is equal to the sum of population and employment and is included as a measure of market size. The data have been differenced to remove the effect of size and focus on changes as well as to remove any constant unobservable factors. County and year fixed effects are included as vectors county and year to control for county and time-specific factors such as local governance or changes in the national economy, but are omitted from the reported results for ease of presentation.

In the preceding model, there is no a priori expectation about the relationship between impact fees and employment growth, as the “old view” suggests they should have a negative effect on employment growth and the “new view” suggests it could be positive. Furthermore, there is no expectation that the relationship be the same for all categories of employment. The question in this study is twofold: (a) how is the use of fees related to employment growth and (b) does the relationship vary across employment types? To answer these questions, the model is estimated using ordinary least squares with change in employment for three different sectors—(a) services, (b) retail, and (c) manufacturing—serving as the dependent variable.

It is expected that changes in population and changes in per capita income will be positively related to changes in employment, as a faster growing market should facilitate faster growth in employment. Change in effective population is anticipated to be positively related to changes in sectoral employment for service and retail but unrelated to manufacturing, as the customer base of firms classified as manufacturing most likely extends well beyond the county limits. For example, a restaurant serves not only residents but also employees of other local firms, whereas a golf ball manufacturer serves national or global markets. Density is often considered to be a positive factor for employment. However, there is no a priori expectation about the relationship between a change in density and a change in employment. Whereas an increase in density increases the number of customers, it may also increase congestion and the costs of land and transport; thus, it could have either a positive or a negative effect.

Estimation Results

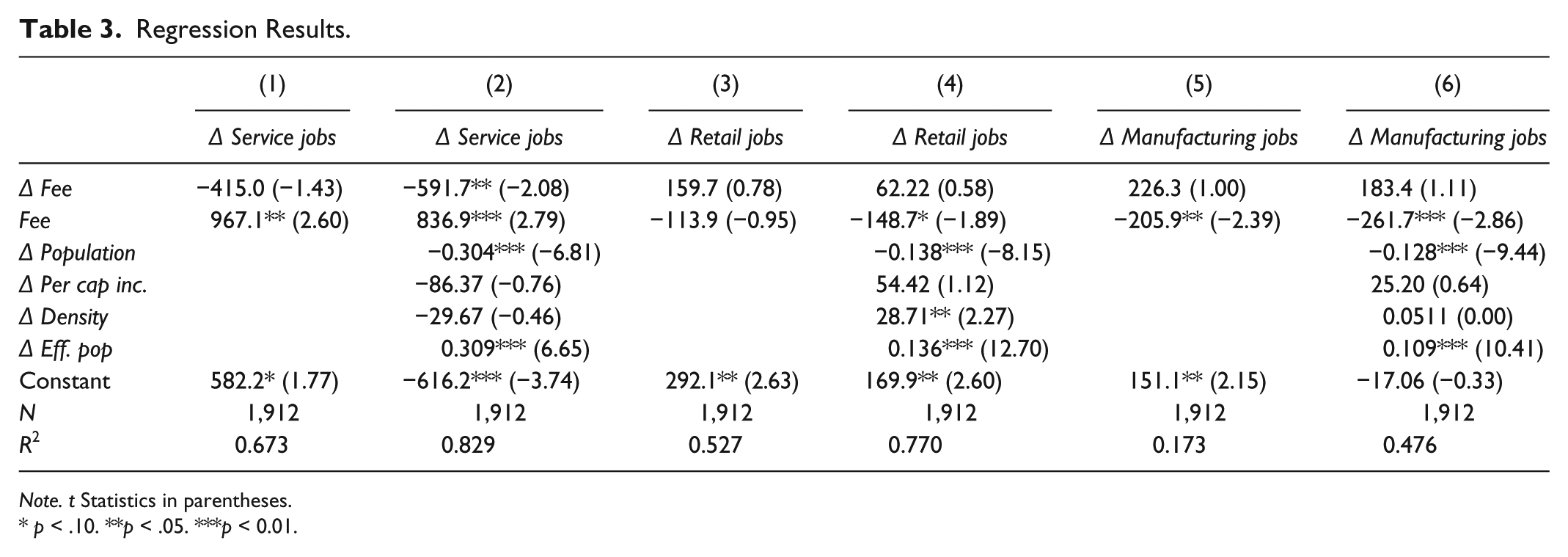

Table 3 provides estimation results. The dependent variables in these regressions are changes in three different measures of employment: (a) change in service employment (Columns 1 and 2), (b) change in retail employment (Columns 3 and 4), and (c) change in manufacturing employment (Columns 5 and 6). The first column for each measure is a simple regression that includes a binary variable for switching to fees (Δ fee), a binary variable for fees (fee), and county and time fixed effects; these regressions do not include the market size control variables. The model is estimated with cluster robust standard errors allowing correlation between errors for each county. The differenced binary variable (Δ fee) is included to pick up changes in the level of employment resulting from a switch to fees, and the binary variable for use of fees (fee) captures how fees are related to changes in employment.

Regression Results.

Note. t Statistics in parentheses.

p < .10. **p < .05. ***p < 0.01.

Of particular interest is the mixed relationship between the use of impact fees (fee) and changes in employment. Note that a negative coefficient does not mean that counties with fees are losing jobs, only that employment is growing more slowly than in a similar county without fees. A negative coefficient on fee is consistent with the “old view” of impact fees (that fees are a tax and do not provide compensatory benefits to the payer) and a positive result is consistent with the “new view” (fees provide infrastructure and future tax benefits and these benefits are recognized by firms). The difference in the relationship across sectors is an interesting result. Whereas fees are positively related to service-sector employment growth, they are negatively related to manufacturing and have a small or insignificant relationship with retail employment changes. These mixed results suggest that there is likely some validity to both the old view and the new view of fees when it comes to nonresidential development. A possible explanation for the differing relationship may be that service firms put a larger premium on increased infrastructure services or lower future taxes than do manufacturing firms. Different industries may view fees from different perspectives: either as a tax with little to no benefit or, potentially, as the purchase of infrastructure services and future tax benefits. Future research should further examine these relationships using firm-level surveys and data analyses.

It is surprising that population growth (Δ population) is negatively related to employment, but this could be explained by the possibility that residential development has bid up land prices. The positive relationship between changes in effective population (Δ effective population) and changes in employment is consistent with the theory that firms make location and expansion decisions based on their market. This finding would suggest that changes in income (Δ per capita income) should also be positively related to changes in employment, but the coefficient estimates in this analysis are insignificant.

Conclusion

There are two views of impact fees when it comes to residential development: (a) an “old view” that fees are a tax on development increasing prices and reducing quantity and (b) a “new view” suggesting that fees provide services and reduce future taxes, increasing development demand and prices. Building on this dichotomy using research on residential fees, this study finds that the relationship between fees and changes in employment differs across industries and is potentially evidence in favor of the new view for service industries, but evidence in favor of the old view when it comes to manufacturing. These results suggest that policy makers need to consider that fees may have positive effects in the residential and service sectors of the local economy and negative effects on industrial development. Whereas fees are theoretically an efficient way of financing infrastructure, they cannot be considered in a vacuum, as other jurisdictions that serve as substitutes may be attractive places for some firms to locate to avoid fees, while still enabling them to serve the fee-charging market. To the extent that firms face low transportation costs, they can easily avoid the fees by choosing these substitute locations.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.