Abstract

Corporate social responsibility (CSR) reporting is a communication channel between companies and stakeholders. As the literature has largely been confined to exploring privately-owned enterprises, state-owned enterprises (SOEs)—a typical example of public sector organizations—warrant further investigation. This study examines SOEs’ accountability structures and reporting features, which are dominated by state owners and mainly driven by non-financial objectives. Through a content analysis of the CSR reports of 49 SOEs and 111 non-SOEs in China, we analyze the stakeholders and CSR domains involved in the reporting. The findings demonstrate that SOEs disseminate the full coverage of stakeholders and a wider scope of CSR domains in disclosure. We extend the debate on CSR-reporting research by demonstrating how state ownership influences hybrid organizations’ self-expression and accountability frame through our finding of a distinctive specialized sub-organization with strong ties to the state that drives CSR internally.

Keywords

As stakeholders have become more interested in actions taken by companies to become socially responsible, corporate social responsibility (CSR) communication has become a vital corporate self-expression tool to demonstrate accountability (Merkl-Davies & Brennan, 2017). While most business communication research has examined the format, scope, issues, and the stakeholders involved in CSR reporting with a focus on companies with an explicit financial goal (e.g., O’Connor et al., 2017), many researchers are shifting their attention to the public sector, bringing organizations with both commercial and non-profit motivations into the CSR-reporting debate (Ervits, 2021).

State-owned enterprises (SOEs) are a typical example of public sector organizations and refer to “any corporate entity recognized by national law as an enterprise, and in which the state exercises ownership” (OECD, 2018, p. 12). As a pivotal part of many economies, SOEs contribute 10% to the global gross domestic product and generate revenues equivalent to 19% of world trade (Florio et al., 2018). Although the terminology often differs, the existence of SOEs is commonplace (Roper & Schoenberger-Orgad, 2011). Owned by the state wholly or partially, they receive a dominant shareholding power from the state and experience stricter pressures toward accountability (Argento et al., 2019). Additionally, the hybrid characteristic of SOEs arising from state ownership has attracted communication scholars. Here, hybridity implies that organizations exist in the intersectional sphere of the public and private, combining public goals with a market orientation (Yetano & Sorrentino, 2023).

As a hybrid of institutional logic and multiple targets, SOEs are typified by citizens as distant stakeholders, with public value taking a prominent position (Argento et al., 2019). When reporting CSR to wholescale stakeholders with diverse interests, accountability issues regarding the stakeholders involved and the responsibilities that SOEs are preferentially liable for should be clarified. Recently, SOEs’ CSR reporting in the accounting realm has increased. Further, based on results from quantitative scoring, scholars have demonstrated that state ownership impacts the disclosure level and quality of CSR reporting (e.g., Dragomir et al., 2022; Garde Sánchez et al., 2017; Guo et al., 2019). However, limited research has explored the reporting features of SOEs, and their inherently ambiguous accountability structure caused by hybridity has seldom been discussed in the business communication literature (Montecalvo et al., 2018).

To fill these gaps, we aim to answer the question: what are the features of SOEs’ CSR reporting? This study focuses on China, where rapid economic growth has been accompanied by serious social and environmental problems. Owing to a shift in policy calling for a balance of social and environmental development in China (See, 2009), substantial authoritative guidance from state and quasi-state organizations promotes the dramatic growth of CSR reporting (Patten et al., 2015). Moreover, China provides a typical scenario for investigating SOEs. China’s marketization reform in 1978, SOEs have grown dramatically and now play a significant role in China’s economy.

This study considers a corpus of CSR reports of 49 SOEs and 111 non-SOEs in China, analyzed with content analytic methods. The overarching contribution of this study lies in demonstrating how state ownership influences the accountability structure of SOEs’ CSR reporting, going beyond a single scoring perspective toward CSR reports. The results suggest that, with the exception of disclosure level or quality, the scope of accountability could be a vital indicator in evaluating CSR reports of hybrid organizations, such as SOEs. Second, we contribute to comparative CSR-reporting research by pointing to the detailed difference of stakeholders and CSR domains involved in companies of heterogeneous ownership. The results confirm and complement discussions on potential isomorphic patterns for beneficiaries between SOEs and non-SOEs (e.g., Ervits, 2021). Third, by exploring the Chinese context, we consider a specified internal sub-organization type that promotes CSR in SOEs. This sub-organization may work with weak regulations and unsound external market systems to boost CSR development in China, thus expanding our understanding of the complex relationship between the state and business unit in developing countries.

To advance our inquiry, we first review the pertinent literature and present our research question. Next, we outline research procedure and methods. After considering the findings, we conclude with a discussion of the study’s contributions and limitations and provide avenues for future research.

Background on CSR Reporting and SOE

Literature on CSR Reporting

Although there is still no overarching definition of CSR, the conceptualization by Carroll (1991) is one of the most widely accepted definitions, encompassing economic, legal, ethical, and discretionary responsibilities. CSR can also be seen as an organization’s initiatives beyond profit-making or compliance with the law (Hamid et al., 2020). Companies have voluntarily reported their CSR—including CSR policies, progress, and results—to respond to ongoing stakeholder and societal scrutiny (Chiu & Sharfman, 2011). Compared with financial reports that are mainly designed for investment targets and require consistent financial information disclosure, CSR reports are written to address the demands of multiple stakeholders, resulting in a multiplicity of frames that companies can follow at their discretion (Tschopp & Huefner, 2015).

Various communication studies have considered CSR reporting, including the scope, issues, and stakeholders involved. For instance, companies in a given industry tend to frame CSR reporting related to specific issues and common stakeholders (O’Connor et al., 2017). Based on different supply chain positions, companies focus on particular stakeholders as prime targets and lean toward relevant CSR practices to ensure communication effectiveness (O’Connor & Shumate, 2010). The efficiency and effectiveness of stakeholder-specific communication are vital features for profit-making companies (Knebel & Seele, 2015). However, business communication research has focused on examining companies with explicit financial goals, especially large and multinational enterprises; thus, literature on companies in the public sector is limited.

SOEs and CSR Reporting

An SOE is a typical example of a public sector organization. In some cases, SOEs are controlled by state owners in a sophisticated ownership structure that combines the private sector; in this way, the state can still exert influence over SOEs through a whole, majority, or minority shareholding, known as “golden shares” (Argento et al., 2019). State ownership creates the hybridity characteristic of SOEs, meaning that multifaceted goals (both financial and public policy targets) combined with incompatible institutional logic, including market (responsive to profitability and effectiveness) and state (focusing on public value creation) logic (Yetano & Sorrentino, 2023). SOEs should integrate both types of logic because of the need to meet societal expectations and prove that their provision is efficient and effective in promoting social and ecological targets (Dragomir et al., 2022).

Unlike non-SOEs, which are only accountable to core stakeholders, SOEs must take on broader duties toward stakeholders nationally. A mixture of social value concerns and financial objectives make SOEs face ambiguous accountability, creating the reporting features of hybrid organizations; this has yet to be fully explored in the business communication field. Prior studies have focused on whether state owners alter the disclosure level and quality of CSR disclosure, reporting a positive (Guo et al., 2019), neutral (Garde Sánchez et al., 2017), or negative (Argento et al., 2019) influence of state ownership in different contexts. Several studies have indicated that SOEs have a stronger incentive to initiate CSR reports and increase the reporting amount (Guo et al., 2019). Other empirical evidence has demonstrated the opposite—that state ownership leads to a lower quality of CSR information (Dragomir et al., 2022). Accounting research along these lines is quantitative and based on results from measurements such as CSR indices and ratings (Fatemi et al., 2018).

Nevertheless, scoring CSR reports generates potential problems because of the multidimensional nature of CSR (Setó-Pamies, 2015), and numerical indices are often deficient in offering detailed information on accountability structures that are inherently ambiguous and created by hybridity. Recent research has begun to identify the reporting content reflected in the SOEs’ CSR reporting, demonstrating the communication difference in a specific field and an isomorphic pattern between SOEs and non-SOEs (Ervits, 2021). Although Ervitz (2021) did not emphasize the hybridity and accountability related to SOEs, the qualitative findings indicated that SOEs have a set of priorities in addressing social problems toward multiple stakeholders, paving the way for further explorations of SOEs’ reporting features. When communicating CSR information to various stakeholders with heterogeneous (even conflicting) interests, SOEs share the same reporting issues: who are they accountable to? For what are they accountable? And what levels of accountability can each stakeholder expect from their collectively owned organizations?

Effect of State Ownership on Framing Issues of CSR Reporting

Companies orient themselves to stakeholder groups through CSR reporting— communicating the people, places, and practices comprising CSR commitments and thereby clarifying for whom and what they accept responsibility (O’Connor & Shumate, 2010). Although the information contained in CSR reporting varies owing to the lack of an enforced framework (Campopiano & De Massis, 2015), most CSR reports include information about (a) stakeholders for whom companies are socially responsible, and (b) CSR domains which CSR activities are conducted for each stakeholder. SOEs are run according to market principles but inevitably carry much of the state’s will. Therefore, they are driven by non-economic goals and unique internal value systems, and thus may involve distinct stakeholders and CSR domains compared with the traditional reporting paradigm.

Stakeholders Involved in SOEs’ CSR Reporting

Traditionally, primary stakeholders who can directly influence business operations include suppliers, employees, and shareholders—who provide the basic resources for business; customers who consume the products and services and create profit for the firm; communities who belong to the area in which the company operates; and government with direct legal authority over companies (e.g., Clarkson, 1995; Freeman, 2010). Frequently, secondary stakeholders indirectly influence or are influenced by the company without legal duties; such stakeholders include environmentalists, NGOs, and the media (e.g., Clarkson, 1995; Freeman, 2010). As an organization straddling the public sector and market, SOEs involve more complex stakes.

First, even while SOEs experience managerial issues and market challenges akin to those faced by companies operating in the private sector, they are unique because of their vital societal function (Argento et al., 2019). SOEs—whose management teams usually have a formal status equivalent to government officials and embody the government’s ideology (Li et al., 2022)—need to supplement the government in fulfilling some of its political and social functions. The advantages of resource acquisition and wider networks from such political legitimacy inspire companies to disclose CSR more widely for legitimacy building. Lin et al. (2020) argue that such shareholding rights have led to over-diversifying attention or accountability toward various parties, including the state, financiers, citizens, clients, and other national actors, all of whom may have competing interests. Subsequently, a distinction may arise between for whom SOE prioritizes its accountability and to what extent SOE covers a wider scope of stakeholders in reporting.

Second, prior research focusing on non-SOEs has seldom discussed the stakeholders within companies or the idea that shareholders and employees appear to be the only internal groups for which companies have accountabilities by default. However, within SOEs, there are unique internal institutions that are often directly affiliated with the state (Ennser-Jedenastik, 2014). Extant literature suggests that the most effective strategy to align business actions with the state owner’s preferences is to staff the party affiliates inside, such as SOEs under the European parliamentary system (Ennser-Jedenastik, 2014). That is, the role of the state-related department may be emphasized or emerge in SOE information disclosure.

Based on the above, in order to understand the features of SOE CSR reporting, it is vital to grasp a wider scope of external stakeholders and divide internal actors:

What are the reporting features when SOEs describe stakeholders in CSR reports?

Domains Covered in SOEs’ Reporting

The dominant control power of state ownership means that the state’s demands and interests are reflected in corporate activities (Ervits, 2021). State-owned entities concentrate more on non-financial goals and thus involve a full-scale social benefit nationally for stakeholders—and even non-stakeholders. Stakeholder relevance should be represented in CSR reporting through the provision of documents containing specific events that stakeholders engage with (Schlegelmilch & Pollach, 2005). We can thus suggest that SOEs may emphasize the social benefit for overall stakeholders in reporting and may be more proactive in disclosing various CSR practices. However, controversy exists in CSR reporting of SOEs with congenital advantages of legitimacy building, strong political ties, and a favorable position for state subsidies, national projects, and resource acquisitions (Li et al., 2022). Several studies in the accounting literature reveal that non-SOEs have higher disclosure levels than SOEs, especially when the political status attaches legitimacy to SOEs (Lee et al., 2017). These findings indicate that SOEs can pursue disclosure efficiency toward specific groups rather than assert the whole-scale accountability at their disposal in CSR reporting.

In considering national interests, the question arises of whether SOEs declare an all-around social benefit creation for a broader scope of stakeholders or even non-stakeholders nationwide. Or, do SOEs take advantage of the innate resources that come with political rationality to narrow the scope of their CSR domains in reporting? In such situations, SOEs create meaningful issues for organizational communication scholars. Thus, we propose the second question:

What are the reporting features when SOEs report on CSR domains?

Contextualizing the Research Objective

In the last three decades, China’s GDP has increased substantially, but this burgeoning growth has led to social and environmental problems. As a result, there has been increased governmental emphasis and guidance on the CSR disclosure offered. Thus, the practice of CSR reporting grew dramatically in the mid-2000s (Patten et al., 2015). SOEs in China are especially influential business units. For example, China’s National Petroleum is the largest integrated energy group worldwide according to the Fortune Global 500 list. Some Chinese SOEs are governed by the State-Owned Assets Supervision and Administration Commission of the State Council at the national level, containing the appointment of top executives, drafting guidelines, and so on. Regional governments own the others (See, 2009). The legacy of central planning is the structure of remuneration that encourages SOEs to utilize government assistance in exchange for increased civic engagement and charitable giving (Ervits, 2021). Before the privatization reforms, Chinese SOEs carried a significant social burden, including daycare centers, residences, recreation centers, and employment commitments.

Since the 1990s, many SOEs relieved from social tasks are listed on the stock markets through ownership reconfiguration; however, the government has retained a sizable stake (Ervits, 2021). To address social issues, governments desire expanded engagement from relevant companies; CSR thus becomes a practicable instrument for alleviating the ramifications of a neoliberal economy (Tan-Mullins & Hofman, 2014). SOEs are expected to provide social services similarly in other nations, but the scope of this expectation may vary (Ervits, 2021). In China, the mission of SOEs is to behave as a conduit for social and economic policies in China; on many occasions, they resolve public issues or preserve social stability (Bai et al., 2006). Non-financial goals are stipulated in their CEO agreements and are viewed as vehicles of governmental policy to promote CSR (See, 2009).

Method

Sample and Data Collection

We relied on a sample of companies from a trans-industry list offered by Cninfo, an official website designated by the China Securities Regulatory Commission for securities information disclosure. Because SOEs concentrate in particular sectors and industrial characteristics may affect the results, we conducted stratified random sampling to ensure that each industry received proper representation across eight economic sectors (food, pharmaceutical, machinery manufacturing, information communication technology, chemical, energy, real estate, and financial services). We extracted 182 companies and downloaded their 2019 financial reports from the website of the Shanghai Stock Exchange and Shenzhen Stock Exchange to check their basic information, including ownership and integrity records. We further confirmed the status of their CSR disclosure on the Shanghai Stock Exchange and Shenzhen Stock Exchange.

We retained a sample of 160 companies as they met the following criteria: (1) the company continuously engaged in and posted CSR in official CSR reports; (2) the company provided a detailed description of stakeholders and CSR activities information; and (3) the company had not been involved in any scandal in the research period to deliberately exclude reporting aimed at image recovery. The 160 companies included 49 SOEs and 111 non-SOEs. Moreover, the 49 SOEs included wholly and partially state-owned shareholdings, whose ultimate dominant shareholder is the State-owned Assets Supervision and Administration Commission (national level) or local governments (regional level). The CSR reports collected ranged from 2 to 95 pages.

Research Procedure and Data Analysis

While critics of CSR reports point to the discrepancy between social disclosure and actual performance (Sweeney & Coughlan, 2008), we did not use them as a measure of CSR substantiality but as an indicator of the communication topics and issues in reporting; we followed Krippendorff’s (1980) assumption that the extent of the disclosure could be taken as some indication of the importance of an issue to the reporting entity. We employed a quantitative content analysis to code all the CSR reports, following a qualitative examination to identify the reporting features. The quantitative approach deals mostly with frequencies of specific words or themes, while a descriptive analysis is context-dependent and might reveal latent meanings not easily discernible by word count.

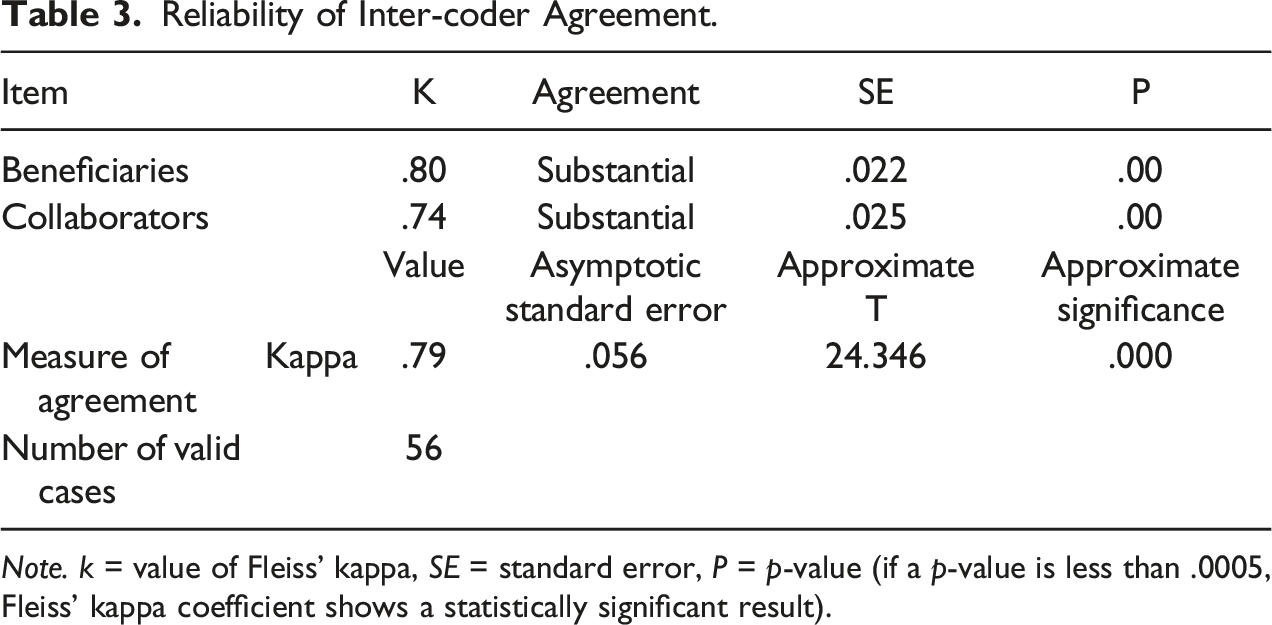

Content analysis techniques are used to codify textual content into multiple groups or categories according to predetermined criteria (Krippendorff, 2018). These techniques eliminate overly subjective analyses and generally offers improved dependability and reproducibility (Krippendorff, 2018). We used MAXQDA 2020 to deal with our extensive qualitative data set. We first conducted a pilot analysis of the CSR reports to familiarize ourselves with the process and classification rules of the coding process; this also tested whether our coding scheme could effectively correspond to the stakeholders and CSR domains that emerged in the paragraphs when coding. We increased reliability using several assessors (Bernard et al., 2016).

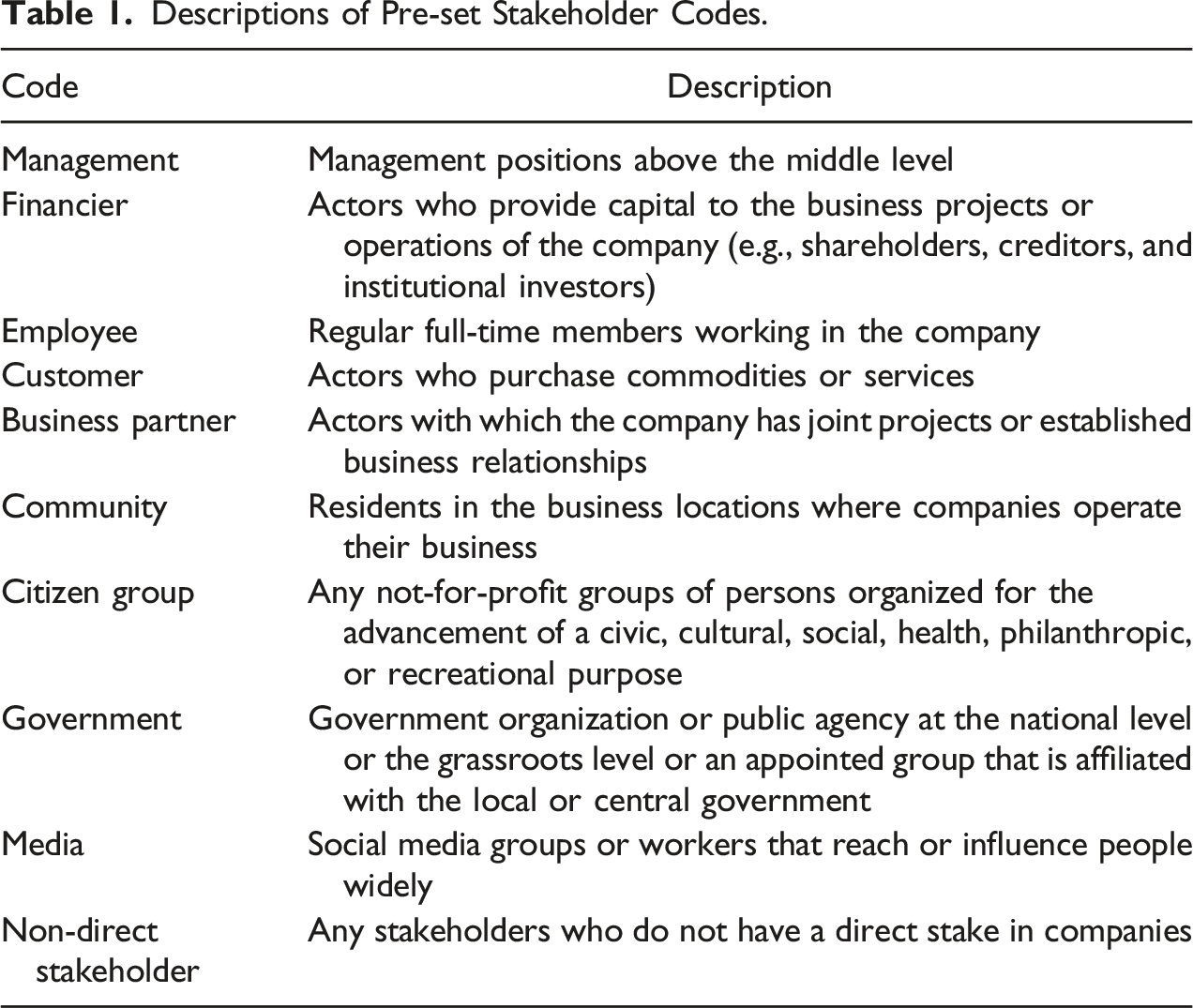

Pre-Set Stakeholder Codes and Coding Framework of CSR Domains

Descriptions of Pre-set Stakeholder Codes.

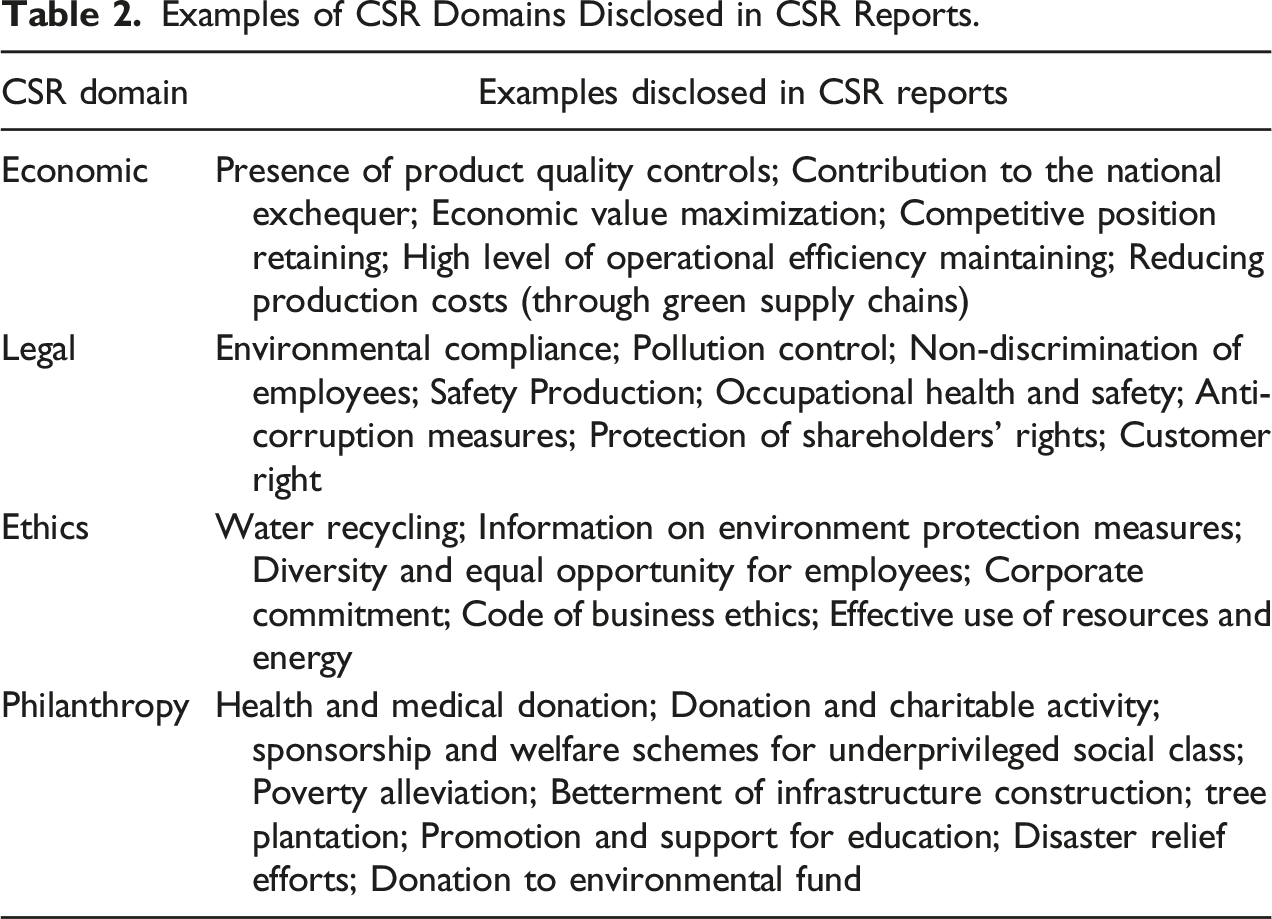

To address the second research question, we borrowed the conceptual framework of Carroll’s (1991) pyramid to ascertain the CSR domains covered in the SOEs’ reporting. First, Carroll considered the CSR domain in a pragmatic and more comprehensive way, taking into consideration the altruistic characteristics of a firm without ignoring the basic economic responsibility of a company (Dusuki, 2008). As such, this approach is appropriate to analyze the information disclosure of SOEs with whole-scale responsibilities and functions. Second, many studies have used Carroll’s classification to examine CSR in different contexts. As a widely accepted CSR concept in exploring the context of developing countries (Hamid et al., 2020), it is suitable for analyzing China.

In this pyramid, Carroll framed the four-part CSR domain. Economic responsibility refers to the primary economic role, including maximizing economic value, retaining a competitive position, and maintaining high operational efficiency. Legal responsibility reflects the basic concepts of fair business practices established by law and legal institutions. Ethical responsibility is broader and includes practices strongly expected by society, even if not codified in law, reflecting society’s various values and norms. Philanthropic responsibility is not strongly expected ethically or morally, referring to discretionary or voluntary social value-creation activities. Table 2 provideds several examples of CSR domains disclosed in the reports. To explain how SOEs frame the scope of the CSR domain toward each stakeholder in reporting, we integrated the above-assumed stakeholders into the CSR pyramid to conduct further analyses.

Coding Process and Reliability of Agreement of Code Integration

We conducted a third-step content analysis procedure using MAXQDA. In the first phase, we split texts into paragraphs, and the people involved in the activities (the subjects and objects of the texts) were extracted. Referring to O’Connor et al. (2017), we classified all individuals who emerged in the text into two categories—those identified as participating in CSR (i.e., Participant category) and those identified as benefiting from CSR (i.e., Beneficiary category). We subdivided the Participant category, identifying internal stakeholders participating in CSR as a “Contributor” and external stakeholders who assisted the company in CSR as a “Collaborator.” Similarly, the paragraphs related to CSR activities were assigned to the “CSR domain” category.

In the second phase, we reviewed the “Contributor” category and gave the words under this category-specific code names. For any word that could not be classified into the Pre-code, we assigned a new code name through discussions. We re-examined all the reports each time a new code emerged and ascertained whether the codes had overlapping concepts. Then, we reviewed the “Collaborators” and “Beneficiaries” categories and assigned all the people-related words to our pre-set ten stakeholder codes. Further, based on the coding framework, all the paragraphs related to CSR domains were given specific code names. During this phase, the authors independently took part in code assignment and met regularly to review the results. To improve credibility, we invited additional coders in the same field to code independently (Bernard et al., 2016). Eventually, we identified five types of “contributors” inside the company, eight types of “collaborators,” eight types of “beneficiaries,” and 16 types of “CSR domains.” We provide a final coded example below: Our employee groups (Contributor category: Employee) worked with Dalian Charitable Foundations (Collaborator category: Citizen group) in 2019, donating a total value of 400,000 yuan for children living in poverty in mountainous areas (Beneficiary category: non-direct stakeholder) in Guizhou (CSR domain: Philanthropic). (HaiXin Corporation)

Examples of CSR Domains Disclosed in CSR Reports.

Coding framework.

Reliability of Inter-coder Agreement.

Note. k = value of Fleiss’ kappa, SE = standard error, P = p-value (if a p-value is less than .0005, Fleiss’ kappa coefficient shows a statistically significant result).

Results

In this section, we offer insights into the stakeholders involved in CSR reporting, providing detailed information on the contributors participating in CSR internally, collaborators assisting companies in CSR externally, and beneficiaries for which companies are responsible.

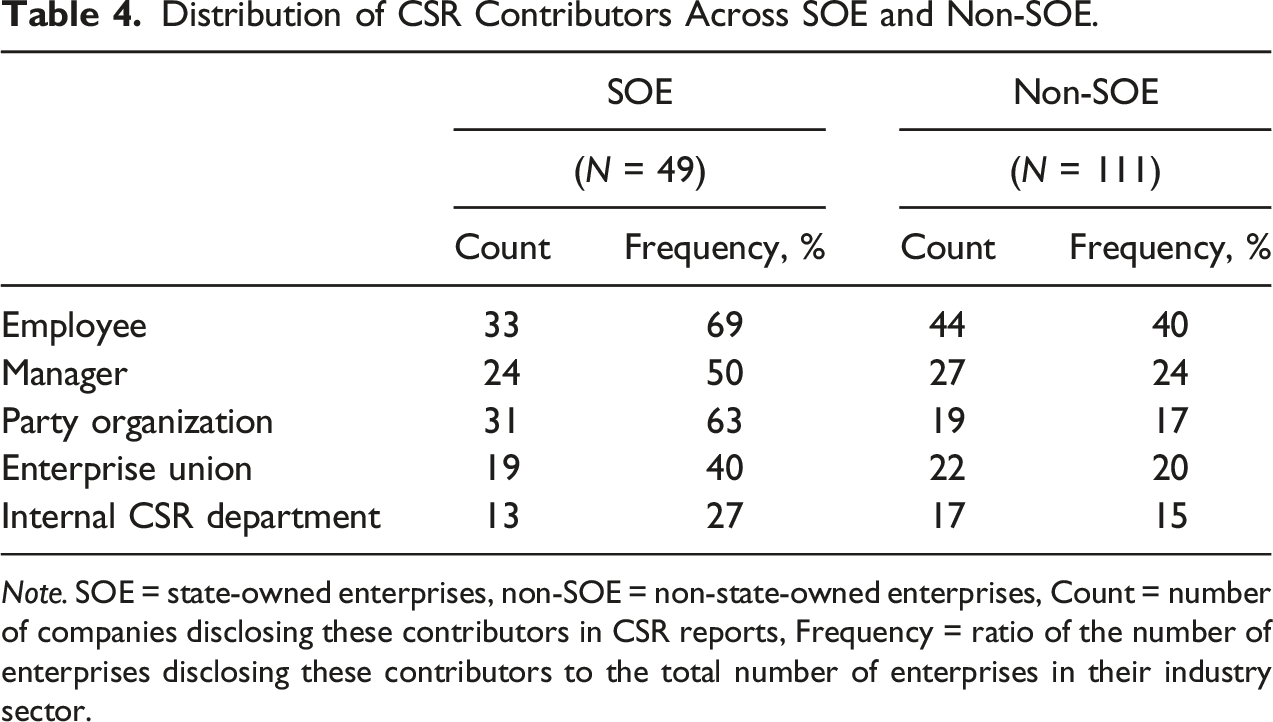

Contributor: Distinctive Internal Party Affiliates Inside the SOEs

Distribution of CSR Contributors Across SOE and Non-SOE.

Note. SOE = state-owned enterprises, non-SOE = non-state-owned enterprises, Count = number of companies disclosing these contributors in CSR reports, Frequency = ratio of the number of enterprises disclosing these contributors to the total number of enterprises in their industry sector.

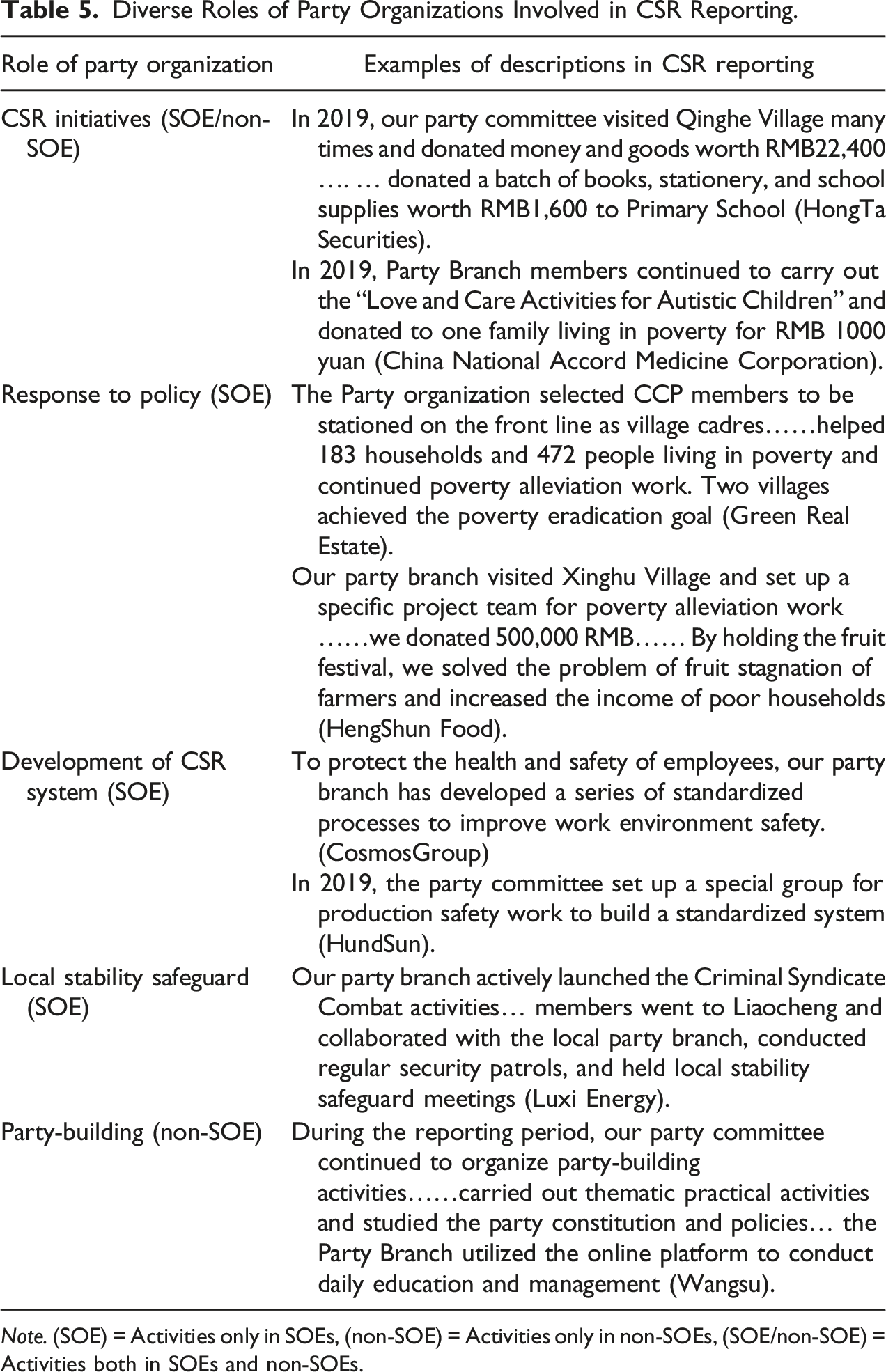

Our results demonstrate that most SOEs emphasize the role of party organization—a specialized internal unit functioning independently within the company—in CSR reports. This indicates the existence of two parallel systems in Chinese SOEs: the regular corporate system and the party system (Lin & Milhaupt, 2021). In China, companies must establish a party organization if they employ more than three employees of the Communist Party of China (CPC) (Beck & Brødsgaard, 2022). The company must provide the necessary conditions and resources for party organization activities, and the party organization participates in decision-making and social responsibility fulfillment inside the company. Through the effort of employees with CPC membership, the party’s work can be integrated into the company’s CSR routine. Although the number of non-SOEs affiliated with party organizations is small, they are still susceptible to party-state influence and are eager to respond to the institutional environment in their pursuit of close ties with the party.

Diverse Roles of Party Organizations Involved in CSR Reporting.

Note. (SOE) = Activities only in SOEs, (non-SOE) = Activities only in non-SOEs, (SOE/non-SOE) = Activities both in SOEs and non-SOEs.

The unique roles of party organizations in SOEs were classified as (a) responding to the national policy, (b) promoting the institutionalization of CSR within the company, and (c) participating in safeguarding local stability. First, most of the SOEs’ reports recorded detailed information regarding the operations and performances of party organizations in “poverty alleviation,” a nationwide campaign launched by the central government in 2016. 1 Promoting the internal institutionalization of CSR practices is the second unique function of the party organization embodied in SOEs’ CSR reporting. Jamali and Karam (2018) have argued that in emerging countries where market mechanisms and legal institutions are not in place and there is a complex national business system, other CSR mechanisms may exist. The current findings indicate the potential existence of alternative mechanisms in China wherein party organizations established by employees with CPC memberships may guide companies to engage in CSR. Moreover, party organization safeguards local stability, implying that SOEs may undertakes social functions such as maintaining public order.

Unlike SOEs that emphasize the diverse roles of party organizations in CSR reports, non-SOEs affiliated with party organizations mainly provided detailed information on the effective functions of their party branches in party-building initiatives (i.e., the introduction of party policies and the promotion of awareness of state affairs).

Collaborator: Collaborations with Multiple Stakeholders

Distribution of CSR Collaborators Across SOE and Non-SOE.

Note. SOE = state-owned enterprises, non-SOE = non-state-owned enterprises, Count = number of companies disclosing these collaborators in CSR reports, Frequency = ratio of the number of enterprises disclosing these collaborators to the total number of enterprises in their industry sector.

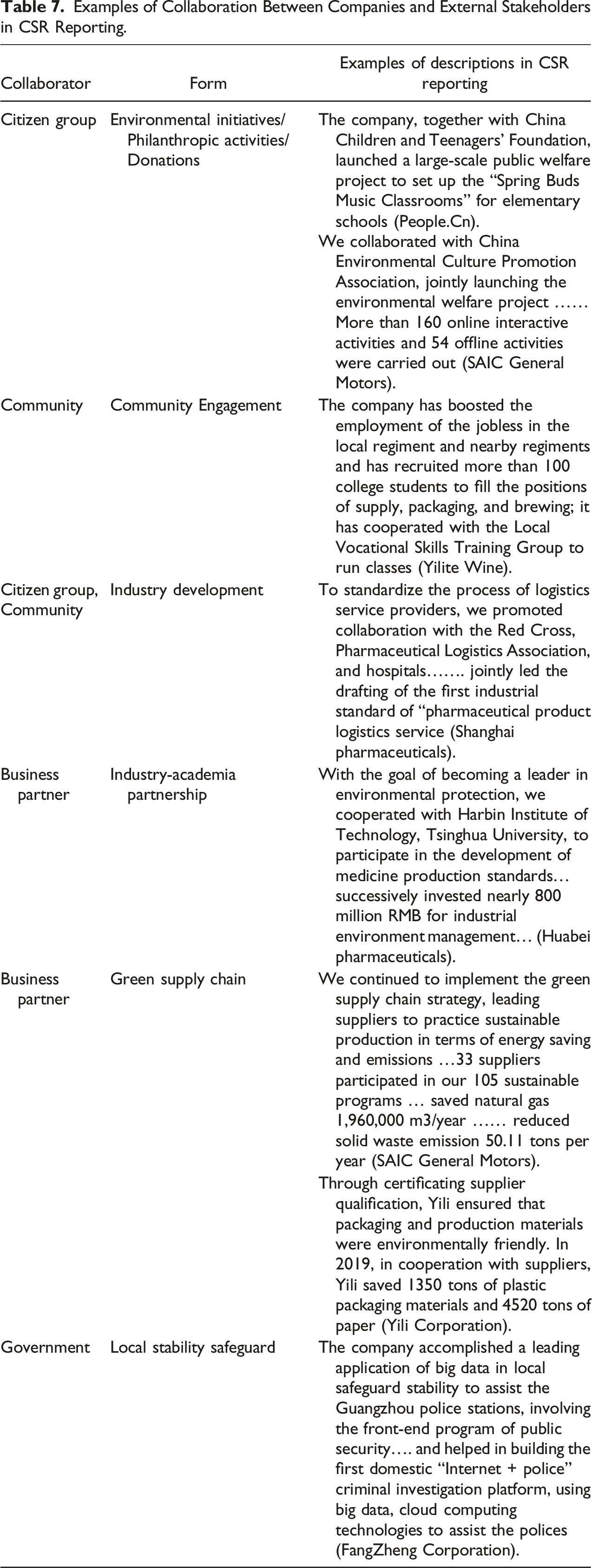

Examples of Collaboration Between Companies and External Stakeholders in CSR Reporting.

Further, the SOEs in our sample had a wider range of business partners cited in CSR reports (freq = 43%) than non-SOEs did (freq = 26%), such as universities in industry-academia partnerships. The cooperation between SOE and supplier is mainly reflected in the specific column named “construction of green supply chain” in reports. In our study, SOEs (freq = 41%) disclosed their relationships with local government and administrative agencies, indicating their increased attention to political legitimacy. There was also a linkage with the community (freq = 35%) and non-direct stakeholders (freq = 33%) for SOEs, whereas non-SOEs tended to solely emphasize the relationship with the community. The frequency of customers and media being emphasized as collaborators was minimal in SOEs and non-SOEs.

Beneficiary: Extended Range of Beneficiaries

Distribution of CSR Beneficiaries Across SOE and Non-SOE.

Note. SOE = state-owned enterprises, non-SOE = non-state-owned enterprises, Count = number of companies disclosing these beneficiaries in CSR reports, Frequency = ratio of the number of enterprises disclosing these CSR beneficiaries to the total number of enterprises in their industry sector.

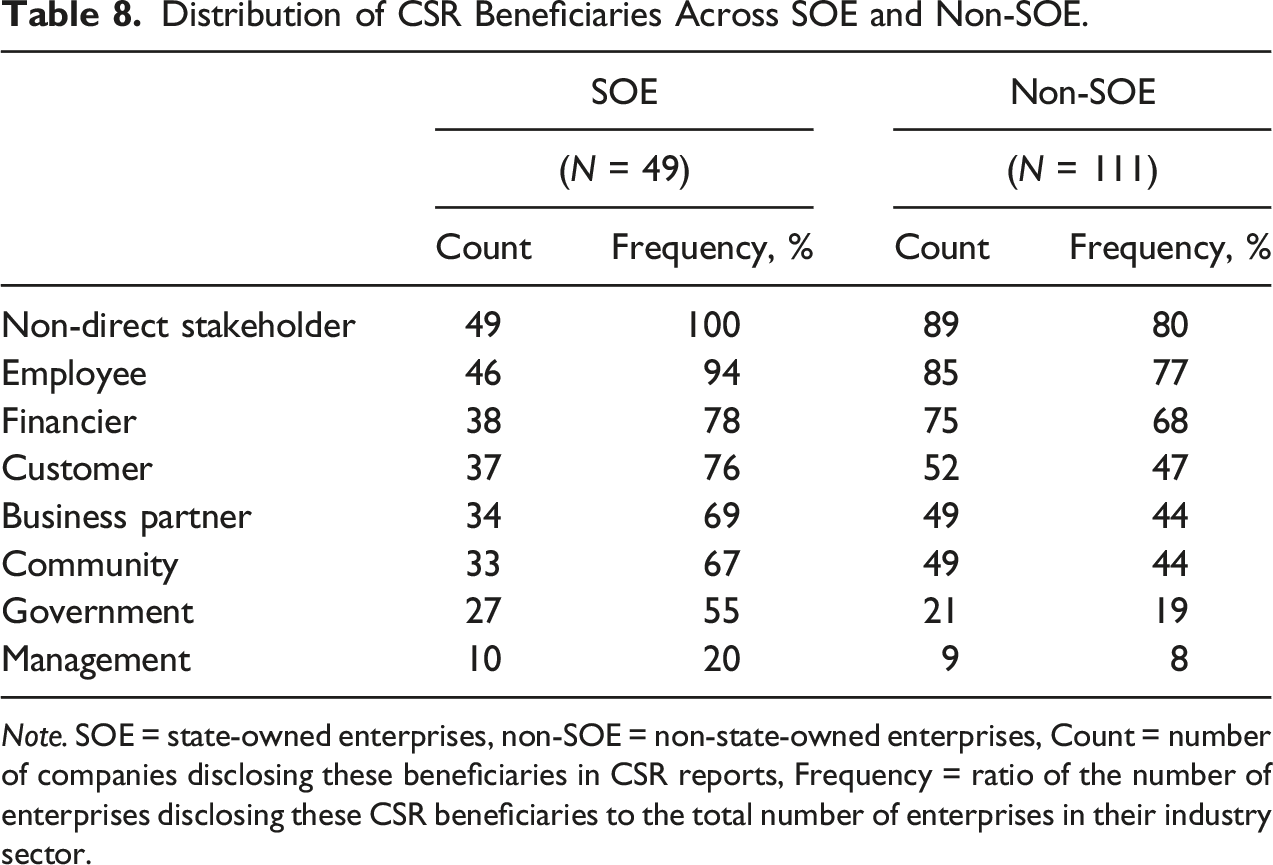

In SOE reporting, the second highest emphasized stakeholder was the employee (freq = 94%). Before transforming into a market economy, Chinese state-controlled economic units functioned as the service center of a specified region where employees were citizens. In our research, most SOEs emphasized the company building a protection system and openly disclosing the information regarding providing social insurance and a housing fund for employees. The willingness and ability to address CSR issues have been found to differ significantly between SOEs and non-SOEs; in our research, this is demonstrated by the difference in reporting CSR toward customers (SOEs freq = 76%, non-SOEs freq = 47%). Further, SOEs (freq = 69%) placed a high value on business partners, thereby differing from non-SOEs (freq = 44%).

Another gap was reflected in the emphasis on local communities. SOEs are under intense pressure to prove the goal achievement of a variety of non-financial objectives, such as infrastructure development and solving local fiscal or unemployment problems for the community (freq = 67%). Although there is no particular need to communicate their business justification or fulfillment of responsibility to the government, more than half of SOEs in our study (freq = 55%) directly conducted CSR, mainly through direct cash and material donations to local grassroots governments. Finally, SOEs (freq = 20%) mentioned support for managers and protecting their fundamental rights, a higher mention rate than non-SOEs (freq = 8%). The difference in the mentioning rate between SOEs and non-SOEs was the smallest for financiers, such as shareholders and investors.

Wider Scope of CSR Domain

Distribution of CSR Domain Across SOE and Non-SOE.

Note. SOE = state-owned enterprises, non-SOE = non-state-owned enterprises, Count = Number of companies disclosing these CSR practices in CSR reports, Frequency = ratio of the number of enterprises disclosing these CSR practices to the total number of enterprises in their industry sector.

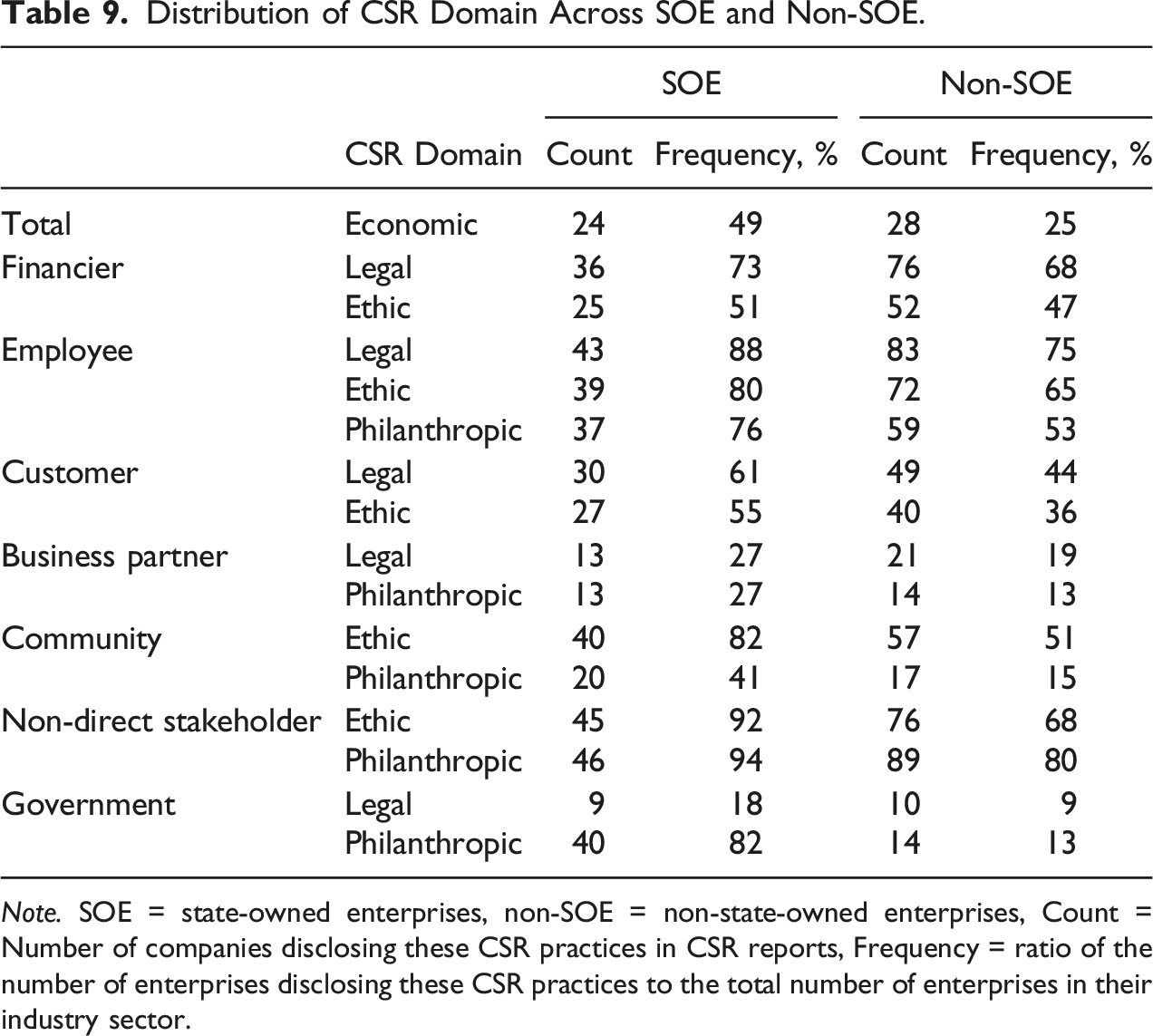

Most SOEs (freq = 88%) emphasized legal CSR to protect employees’ basic rights and interests (e.g., clarification of employees’ rights under the Labor Law, the guarantee of the salary distribution system, and establishment of welfare system). Ethical responsibilities for employees, such as improving working conditions and developing training programs, were mentioned frequently (freq = 80%). SOEs also stressed “employee-philanthropic” CSR, including organizing entertainment and cultural events for and donations to retired employees in poverty (freq = 76%). As for customers, more than half of the SOEs highlighted a legal responsibility to establish a protection system for consumers’ basic rights (freq = 61%), whereas non-SOE concerns for consumers demonstrated room for improvement (freq = 44%). Because activities such as humanized services delivery and consumption environment improvement are not legally governed, we classified them as “customer-ethical” CSR, which SOEs (freq = 55%) mentioned more frequently than non-SOEs did (freq = 36%).

Most SOEs (freq = 82%) declared ethical responsibilities toward communities in CSR reporting, including stability safeguards and solving employment problems for those with disabilities and impoverished minorities. Half of the non-SOEs (freq = 51%) were also interested in providing local employment opportunities. However, less than half frequently mentioned philanthropy for local areas regardless of capital ownership. In our study, Chinese companies emphasize philanthropic activities in a wider world context rather than specific regions. Moreover, SOEs paid the most attention to social value creation for the non-direct stakeholders, as they described “non-direct stakeholder philanthropy” most frequently. More SOEs (freq = 92%) also emphasized ethical responsibilities toward non-direct stakeholders, such as human rights issues, compared with non-SOEs (freq = 68%).

As for government-related stakeholders, CSR practices in philanthropic and legal responsibility reports were found in descending order of frequency. Activities such as party building, development of special economic zones, and support for grassroots government agencies were formulated as “government-philanthropic.” Law compliance, such as corruption eradication, was formulated as “government-legal.” Among them, philanthropy for government differs significantly between SOEs (freq = 82%) and non-SOEs (freq = 13%).

Like non-SOEs (freq = 19%), SOEs accepting the legal responsibility to protect partners’ rights was still limited (freq = 27%). Only a few SOEs clarified their legal responsibilities, such as protecting the basic rights of partners, preventing fraud in transactions, and establishing fair procurement and a supply system free of bribes. The results demonstrated an urgent need to implement a rights protection system for partners in China. For business partners with financial difficulty, a few SOEs (freq = 27%) provided direct donations, support in the form of human and material resources, and the free provision of technology and equipment through “business-philanthropic” CSR relatively more actively than non-SOEs (freq = 13%). However, the priority of business partners in SOEs’ reporting was not as high as that of other core beneficiaries with a direct stake. Less than half of the SOEs identified economic responsibility (freq = 49%), such as maximizing earnings per share, maintaining a strong competitive advantage, and increasing operational efficiency.

Discussion

Given the prevalence of SOEs and their critical role globally, we analyzed SOEs to move beyond the discussion limited to the private sector in the CSR communication field; the findings revealed several characteristics of SOEs in CSR reporting.

Multiple Stakeholders Involved in CSR Reporting

First, compared with non-SOEs, SOEs mentioned the contributions of diverse internal stakeholders, revealing multipurpose considerations in a systematic reporting system. Moreover, we identified a new type of internal stakeholder, an internal body with political involvement inside the SOEs, one that plays a vital role in driving CSR: party organization. Further, we demonstrated the multiple roles of party organizations mentioned by SOEs, including response to national policy, social stability safeguarding, and development of an internal CSR system, whereas only a few non-SOEs have set up party organizations and mainly disclosed information regarding party building activities.

Second, SOEs cited more multiple partnerships than non-SOEs in CSR reporting. With a network of political contacts and business legitimacy, SOEs build multilateral cooperation with citizen groups, business partners, government, and local communities (Guo et al., 2018). In our study, SOEs reported long-term partnerships involving philanthropic activities with citizen groups and emphasized their duty to collaborate with business partners to improve the industry and work with local communities to address livelihood and employment issues.

Third, SOEs emphasized social benefits for a whole scale of beneficiaries than non-SOEs, owing to the government’s impact and the requirement for higher-level accountability. SOEs attach particular importance to protecting and creating social value toward employees and non-direct stakeholders. Labor in state-controlled economic units is highly prioritized—a pattern following other post-communist countries (Kuznetsov et al., 2009). However, the concern for non-direct stakeholders demonstrates the influence of institutional ideology and the non-financial goals of state owners, which should harmonize the interests nationwide (Lin et al., 2020).

Scope of CSR Domains in Reporting

This study elucidated the CSR domain closely toward each stakeholder in reporting, suggesting that SOEs emphasize CSR in wider domains more than non-SOEs. We also revealed that the domain reported differs depending on the stakeholder type in SOEs—SOEs placed the highest value on the responsibilities toward employees and non-direct stakeholders through the disclosure of total CSR domains. While companies with different ownership exhibit visible distinctions, they also reveal a concern for common stakeholders (Ervits, 2021), meaning that a homogenizing behavior of non-SOEs imitating SOEs may exist. Interestingly, both SOEs and non-SOEs in our study targeted non-direct stakeholders, which can be identified as core beneficiaries. Such an extension of the scope of core stakeholders results from a poverty alleviation event triggered by the government (Li et al., 2016), which most companies mentioned. Companies cannot be divorced from the political context, even among non-SOEs (Li et al., 2022). This indicates a need to explore the non-regulatory aspects of company-government interaction over legal compliance, such as proactive policy response.

Conclusion

Hybrid organizations—such as SOEs, social enterprises and community-based organizations—are increasing worldwide. Taking China as a case study, we present a CSR-reporting model of SOEs to clarify their features of accountability, thus benefiting the CSR communication field. The results demonstrate that, on the one hand, when competing institutional logic exists, SOEs in China prioritize the benefit and service of society as a whole. Below the state logic, the state and SOEs are in a symbiotic relationship, allowing the scope of their core focus to encompass the nationwide populace (Lin et al., 2020). The greatest concern for non-stakeholders regarding SOEs is a message of conformity and allegiance—in our research, SOEs did not mention the state when they mentioned benefiting the public, but its significance is implied. By contrast, SOEs in our study gave a second place to their accountability with specific stakeholders (e.g., employee, financier, and customer) who require the disclosure of CSR to maintain market logic. Companies dominated by a single market logic highlight targeted transmission and efficiency (Knebel & Seele, 2015). Hybrid organizations, however, have competing logic and emphasize full coverage in their CSR disclosure. Therefore, rather than the disclosure level or quality of reporting, understanding the scope of accountability is a vital indicator in evaluating the CSR reports of such organizations.

This study reveals the reporting features and issues of SOEs, going beyond a single rating perspective. We found that SOEs and non-SOEs have a similar prioritization of beneficiaries, which is in line with the findings of Ervits (2021). From our observations of SOE communication, we further see a wider collaborative network, and that the scope of stakeholders and CSR domains involved in CSR reporting of SOEs is broader than those of non-SOEs. Specifically, a specialized internal organization is uniquely affiliated with the state frequently emerged in SOEs’ CSR communication, with different roles in the discourse between SOEs and non-SOEs, with the former emphasizing policy response and socio-political functions while the latter highlights political legitimacy.

Our study also provides theoretical insights that could be of benefit to researchers in the SOE and CSR field. Prior studies have argued for the difference in disclosure level and the quality of CSR reports under state ownership (e.g., Dragomir et al., 2022; Guo et al., 2019), and we take this a step further to elaborate on these differences from the perspective of the stakeholders and CSR domains. We complement comparative CSR studies by providing a cross-sectoral analysis of different ownership types. The existence of internal affiliation related to the state in SOEs is implied in prior studies (Ennser-Jedenastik, 2014); however, how it works in the corporate setting has not been investigated. This finding indirectly provides empirical evidence of how such internal state-related organizations inside the SOEs influence CSR.

Finally, this study can be extrapolated as a reference for specific emerging countries because it examines the Chinese situation in a non-Western context. Prior research has suggested that other mechanisms to promote CSR may exist in developing countries where market mechanisms and legal institutions are not in place (Jamali & Karam, 2018). Our findings indicate that, in China, party organizations formed by employees with CPC memberships may guide companies to engage in CSR. Regarding the role of government in shaping CSR, we infer that, aside from external constraint and guidance, the government may exert its influence through staff in SOEs, where party affiliations act as an internal penetration (see Beck & Brødsgaard, 2022). Nevertheless, our findings should not be generalized without taking into consideration the complex national business system of China, alongside the nuances of the specific country in question.

Our study has certain limitations, which provide opportunities for further research. First, our sample was derived from listed companies; the samples focus on large and medium-sized companies, whereas the examination of small and micro-companies was limited (i.e., governmental constraints may affect micro-companies). Second, this study analyzed a single year’s CSR reports. Cross-sectional data do not allow for causal and temporal exploration, whereas a longitudinal investigation would offer a more dynamic perspective. Third, our sample was limited to a single-country context. We encourage future research to analyze CSR reporting by SOEs of other countries to verify whether the findings can be applied to other institutional contexts that may exhibit different effects of state ownership on information disclosure. As CSR efforts are highly dependent on context, we suggest adding comparative investigations of SOEs across countries to provide fresh evidence.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported in part by grants from Fee Assistance Program for Academic Reviewing of Research Papers of Hitotsubashi University.