Abstract

Drawing on the affect infusion model from cognitive psychology, the authors develop a conceptual framework that explains how affect related to corporate ownership influences the formation of socioemotional wealth perceptions among family firm owners, reflected in altered subjective value perceptions for the ownership stake. The authors explore target, personal, and situational features in the subjective valuation process for the ownership stake and explain how these factors mediate the relationship between affect and socioemotional wealth perceptions. They further the understanding about the level of bias in family owners’ subjective firm value assessments and offer new approaches for socioemotional wealth research.

Introduction

Entrepreneurship research has long emphasized that owner-managers often consider more than financial utility in their possession of privately held firms (e.g., Levesque, Shepherd, & Douglas, 2002; Penrose, 1959; Schumpeter, 1934). These nonfinancial benefits from ownership are particularly prominent in the family firm literature. In fact, the observation that family firm owners are motivated by more than financial goals is one of the most prominent assertions in family business research (Sharma, Chrisman, & Chua, 1997). It is argued that family owners receive utility from exercising authority, acting altruistically regarding family members, or conserving the family firm’s social capital (Arregle, Hitt, Sirmon, & Very, 2007; Schulze, Lubatkin, & Dino, 2003).

Recently, a stream of literature on the socioemotional wealth (SEW) of organizational ownership has started examining the noneconomic utility that owning family members derive from corporate control (Berrone, Cruz, Gomez-Mejia, & Larraza-Kintana, 2010; Gomez-Mejia, Haynes, Nunez-Nickel, Jacobson, & Moyano-Fuentes, 2007; Zellweger & Astrachan, 2008). Gomez-Mejia et al. (2007) suggest that SEW should be seen as the “non-financial aspects of the firm that meet the family’s affective needs” (p. 106). Building on these initial SEW writings and the insights from behavioral theories, such as prospect theory (Kahneman & Tversky, 1979), we contend that owners are willing to sell their ownership stakes only if they are compensated commensurately with the perceived loss of SEW (Ariely, Huber, & Wertenbroch, 2005; Arkes & Blumer, 1985; Thaler, 1980; Tversky & Kahneman, 1981, 1991; Wiseman & Gomez-Mejia, 1998). In other words, SEW is reflected in the perceived value for the ownership stake and, more precisely, is that part of a business value (as perceived by the owner) that is unexplained by financial considerations (Astrachan & Jaskiewicz, 2008; Zellweger & Astrachan, 2008). These authors show that SEW considerations lead to biased value considerations, hence, to values that deviate from an objective market price, when owners have to indicate an acceptable sale price for the ownership stake (Zellweger, Kellermanns, Chrisman, & Chua, 2011).

Current SEW literature, however, is unable to explain how and under which conditions affect, that is, feelings and emotions (Baron, 2008), influences the formation of SEW and hence drives family owners’ value perceptions. This dearth of insight is striking in light of the relevance of affect for SEW (e.g., Gomez-Mejia et al., 2007) and the observation that family firm ownership represents a particularly affect-dense setting (Kellermanns & Eddleston, 2004; Schulze, Lubatkin, Dino, & Buchholtz, 2001). Moreover, failing to account for affect in our progress toward a theory of SEW is unfortunate, since affect infusion theory provides critical insights into cognitive processes in general and the subjective valuation of possessions in particular (Chung, Cohen, & Monroe, 2008; Forgas & Ciarrochi, 2001; Hirshleifer & Shumway, 2003).

Along this line of thinking, therefore, this article draws on cognitive psychology literature (Forgas, 1995; Forgas & Ciarrochi, 2001) to answer the question as to why some family owners are more biased in assigning a value to their ownership stake than others. We develop a conceptual framework that introduces target, personal, and situational features in value perception processes as mediators in the relationship between affect related to corporate ownership and subjective value perceptions of the ownership stake. Thereby we understand the level of bias in these subjective value assessment, and hence the absolute difference between the subjective and objective value assessment, as an indicator of SEW (Astrachan & Jaskiewicz, 2008). Whereas present SEW research considers family firm ownership to be homogenous in its ability to create SEW, we suggest that there is heterogeneity among family firm owners in their SEW perceptions and that such heterogeneity is related to the presence or absence of the mediating effect of target, personal, and situational features in the value perception process for the ownership stake.

Our study attempts to make four contributions to the literature. First, we respond to the prominent call in family business research to examine why and how family firm owners value nonfinancial utility related to corporate ownership (Sharma et al., 1997). Previous research has proposed an idiosyncratic goal-based rationale (Gomez-Mejia et al., 2007), whereby particularistic utility functions are enabled by the extended power of controlling families (Carney, 2005) and family and firm reputation concerns (Zellweger, Nason, Nordqvist, & Brush, 2011). By focusing on the affect infusion model (AIM), we introduce an overlooked theoretical rationale rooted in cognitive psychology (Forgas, 1995). Second, we contribute to SEW theory by exploring under which conditions and to what degree affect biases owners’ subjective value perceptions for private family firm ownership and hence drives SEW. Here, the AIM is able to open the black box between affect and SEW (Berrone et al., 2010; Zellweger & Astrachan, 2008). Therefore, we accommodate calls to consider the differing degree of emotional attachment among family firm owners (Sharma & Manikutty, 2005). Third, we contribute to behavioral theories, such as prospect theory, and the role of affect in shaping reference levels by arguing that the endowment effect can be explained, at least partly, by affective elements. More specifically, affect-infused information processing can create biased value estimates, directly influencing the formation of SEW (Greve, 1998). Even though this claim has been made before (Lerner, Small, & Loewenstein, 2004; Zhang & Fishbach, 2005), we are among the first to reveal a model that shows that affect infusion in reference point creation should also hold for assets that are held for seemingly purely financial reasons such as corporate ownership. Finally, our findings speak to the subjectivist perspective of entrepreneurship, since we account for the fact that individuals hold different preferences and expectations; more specifically, the presupposition that the contents of the human mind, and, hence, decision making and value perceptions, are not rigidly determined by external events (Foss, Klein, Kor, & Mahoney, 2008; Hayek, 1948; Penrose, 1959).

First, we review SEW literature in the context of family firm ownership and introduce the AIM. Then, we discuss how affect infuses SEW perceptions and biases the acceptable sale price of ownership stakes. To this end, we develop testable propositions and discuss the implications of our research for theory and practice.

Socioemotional Wealth Among Family Firm Owners

A standard assumption in traditional agency writings is that owners are driven solely by financial motivations, in particular the financial value of the ownership stake (Fama & Jensen, 1983). However, there is widespread consensus among entrepreneurship (Schumpeter, 1934) and, especially, family firm scholars (Sharma et al., 1997) that owner-managers are also driven by nonfinancial considerations. In their study of the largest firms in Europe, Thomsen and Pedersen (2000) show that the type of owner (e.g., members of the founding family, banks, institutional investors, other nonfinancial companies, governments) has implications for firms’ objectives. Key findings include that shareholder value is not a universal goal for some owner types and that trade-off effects against the creation of shareholder value are particularly prominent in family firms. To explain this effect, strategy and family business scholars suggest that families should be seen as principals having the institutional power to reinterpret and manipulate the goal set in their firms (Scott, 2008; Thornton & Ocasio, 1999) and replace calculative decision criteria with particularistic goals, whereby nonfinancial considerations of the owning family play a critical role (Carney, 2005). Alternatively, it has been argued that depending on the degree of identity overlap between family and firm, family firm owners are seen as inclined to seek nonfinancial utility (Zellweger et al., 2011). Although the firm often becomes an integral and inescapable part of life for family firm owners, the relationship to the firm is more distant, transitory, and utilitarian for nonfamily shareholders (Lubatkin, Schulze, Ling, & Dino, 2005).

Most recently, and under the umbrella of SEW, researchers have started investigating the sources and components of the nonfinancial utility of family firm owners (Berrone et al., 2010; Gomez-Mejia et al., 2007; Gomez-Mejia, Larraza-Kintana, & Makri, 2003; Gomez-Mejia, Nunez-Nickel, & Gutierrez, 2001; Zellweger & Astrachan, 2008). Topics include family relationship contracting that produces agency contracts departing from economic rationality (Gomez-Mejia et al., 2001); lower family CEO salary in exchange for job security and emotional attachment (Gomez-Mejia et al., 2003); maintaining control over the firm, which engenders risk taking or creative earnings management to assure SEW (Gomez-Mejia et al., 2007; Stockmans, Lybaert, & Voordeckers, 2010); low levels of diversification to tightly control investments (Gomez-Mejia, Makri, & Larraza-Kintana, 2010); and better compliance with institutional pressures to alley family reputation concerns (Berrone et al., 2010). Therefore, SEW is defined as the “non-financial aspects of the firm that meet the family’s affective needs, such as identity, the ability to exercise family influence, and the perpetuation of the family dynasty” (Gomez-Mejia et al., 2007, p. 106) and also as the “stock of affect-related value that the family has invested in the firm” (Berrone et al., 2010, p. 82).

SEW writings argue that socioemotional utility enters an owner’s value appraisal when the owner assesses the value for the ownership stake (Astrachan & Jaskiewicz, 2008; Zellweger & Astrachan, 2008). In the presence of socioemotional utility, owners tend to indicate biased value perceptions, that is, their value perceptions deviate from market value as calculated based only on financial information (Zellweger & Astrachan, 2008). According to the SEW perspective rooted in the behavioral theory of the firm, prospect theory, and the behavioral agency model (Cyert & March, 1963; Gomez-Mejia et al., 2007; Wiseman & Gomez-Mejia, 1998), socioemotional utilities related to family firm ownership are endowed by owners and form a reference point from which owners are willing to part only if they are compensated commensurately with the perceived loss of SEW (Ariely et al., 2005; Arkes & Blumer, 1985; Thaler, 1980; Tversky & Kahneman, 1981, 1991; Wiseman & Gomez-Mejia, 1998). Following this line of argumentation, we conceptualize SEW as the absolute difference between an owner’s subjective value assessment and the objective market value for the ownership stake of a firm. SEW with negative valence indicates an inclination to withdraw from the firm and to sell out, whereas SEW with positive valence indicates an inclination to be attached to the ownership and to invest the self into it. In both cases we suggest that affect biases subjective value perceptions and hence shapes SEW perceptions.

This theoretical approach is guided by the perception that SEW literature’s progress is largely dependent on researchers’ ability to theoretically untangle the processes through which various dimensions of SEW shape a reference point and thus bias family owners’ value perceptions and ultimately firm-level behavior. Whereas control considerations and identity concerns have been discussed elsewhere (Chrisman, Chua, Pearson, & Barnett, 2011; Zellweger et al., 2011), affect and its relationship to SEW has gathered surprisingly little attention. This is unfortunate, for at least three reasons.

First, family firms are often considered as an affect-rich organizational context. Scholars see the intermingling of emotional factors originating from family involvement with business factors as a distinct attribute of family firms (Tagiuri & Davis, 1982, 1992). Such affective experiences at the ownership level may consist, for example, of satisfaction regarding achievements of the firm, trust and harmony among family members, or pride in long-term and continuous control over the firm (Kets de Vries, 1993). Family firm owners often display emotional attachment to their firms; loss of the firm represents a highly emotional event for most owners (Salvato, Chirico, & Sharma, 2010; Sharma & Manikutty, 2005; Shepherd, Wiklund, & Haynie, 2009).

Second, despite the relevance of affect for SEW and its prevalence in the family firm setting, it is important to acknowledge heterogeneity among family firms and their owners (Melin & Nordqvist, 2007). Unfortunately, however, current SEW research assumes that family firms are homogeneous in their emphasis of SEW considerations; often, family firm status is used as a proxy for the existence of SEW (Berrone et al., 2010; Gomez-Mejia et al., 2007; Gomez-Mejia et al., 2010; Jones, Makri, & Gomez-Mejia, 2008; Miller, Le Breton-Miller, & Lester, 2010). This frontal approach is unlucky, since it falls short of contributing beyond the theoretically uninspiring observation that family firms are different from nonfamily firms, and that family owners value socioemotional dimensions of corporate ownership whereas nonfamily owners are unaffected by such biases. SEW literature must reach beyond this oversimplification and explain the varying sources and degrees of SEW, thereby acknowledging family firm heterogeneity (Melin & Nordqvist, 2007). Some family-controlled firms closely resemble nonfamily firms, for example, investment vehicles in which the family point of view is limited to that of a passive shareholder (Pearson, Carr, & Shaw, 2008; Sorenson, Goodpaster, Hedberg, & Yu, 2009). In these situations, SEW considerations induced, for example, by affect may be limited or nonexistent. Therefore, exploring how various elements of ownership infuse affect and, hence, SEW, which ultimately biases the perception of corporate value, holds promise to render the heterogeneous reality of family firm ownership more realistically.

Third, through affect infusion literature, in particular the AIM (Forgas, 1995), cognitive psychology offers sound theoretical ways to untangle the link between affect, appraisal processes of affect, and the cognitive process of subjective value assessment of a possession. Conceptualized as an explanation for affect infusion in numerous information-processing contexts, this theory has been successfully applied in the entrepreneurship context of opportunity recognition and exploitation (e.g., Baron, 2008; Foo, 2011; Foo, Uy, & Baron, 2009) and for individual valuation of possessions (Chung et al., 2008; Forgas & Ciarrochi, 2001; Hirshleifer & Shumway, 2003). We suggest, therefore, that the AIM holds valuable insights into the processes through which affect infuses family owners’ value considerations and hence leads to SEW.

The Affect Infusion Model

Affect infusion theory sheds light on the psychological processes through which affect primes cognitive judgments, including evaluations of personal efficacy and social performance (see Forgas & Bower, 1987, for a review). Possessions may have an affective dimension, since to a large degree they can become symbolic extensions of the self, thus taking on a significance well beyond their economic value (Forgas & Ciarrochi, 2001). Affect infusion theory suggests that merely owning an object increases its value to owners (Beggan, 1992; Kahneman, Knetsch, & Thaler, 1991); put differently, affective feelings about ownership play a key role in generating the endowment effect (Bower, 1981; Chung et al., 2008; Forgas & Ciarrochi, 2001; Hirshleifer & Shumway, 2003; Keltner, Ellsworth, & Edwards, 1993; Lerner et al., 2004; Pham, 2007; Shiv, Loewenstein, Bechara, Damasio, & Damasio, 2005).

Introducing the AIM, Forgas (1995) laid the theoretical foundation to explain the processes through which affectively loaded information influences and becomes incorporated into a judge’s deliberations and colors judgmental outcomes. The AIM suggests that depending on target, personal, and situational features, the individual chooses between four information-processing strategies: direct access, motivated, heuristic, and substantive, which differ in magnitude of required effort and level of affect infusion (see, e.g., Chung et al., 2008; Hills, Hill, Mamone, & Dickerson, 2001; Hirshleifer & Shumway, 2003). Direct-access processing (a low-affect strategy) is applied when the target (i.e., the possession) is highly familiar, the individual is not personally involved, and circumstances require little effort; individuals routinely avail themselves of stored information and experience in processing activities, eliminating emotionality (Forgas, 2001). For instance, we consider the value assessment of fungible commodities that are held for exchange as a prototypical example of this processing style. In motivated processing (also low affect), in turn, individuals adopt a highly targeted, selective thinking style (Forgas & George, 2001), whereby a bounded or narrow-minded information search naturally constrains the influence of affective states on judgments (Forgas, 2001). A strong motivational goal (e.g., to sell a possession) limits the power of affective states to guide information processing through specific access to prior experience or knowledge (Forgas & George, 2001). Such low affect-infusing processing may be at play, for instance, when a merchant sells products to the market. Because those transactions are highly routine based, the merchant tends to be very familiar with the process. Furthermore, the motivation for the merchant is straightforward: She or he simply wants to generate income. We suggest, then, that affect infusion in the merchant’s information processing is limited or nonexistent.

Turning to affect-infusing processing styles, heuristic information processing is chosen if the information is simple, information is not personally relevant for the individual, and the situation is not demanding in terms of accuracy or detailed considerations (Forgas, 1995). Heuristic processing of information relies on emotions and mood; affect is explicitly used as input to minimize the level of effort. Appraisals are then undertaken based solely on how the owner feels about the possession, allowing affect to minimize effort. For instance, consider a garage sale. When there is a potential buyer, the seller is likely to indicate a price according to her or his instinct, rather than expending much effort to weigh the costs against the benefits of a sale or to research prices of comparables.

In the context of value assessments of private family firm ownership, we expect these three processing strategies to be minimally relevant. Rather, we expect value assessments to be affect infused along the lines of substantive processing, the fourth information-processing strategy in the AIM. This strategy is seen as demanding the most effort, requiring individuals to carefully handle information using their own memories, associations, and comparisons (Forgas & Ciarrochi, 2001). Substantive processing will likely be chosen if there is no alternative that requires less effort (Forgas, 2001). The mechanism through which affect enters the cognitive process in substantive processing follows the affect-priming principle: The affective state grants access to certain categories of interpretations (Bower, 1981).

This affect-infusing processing choice seems likely to be at play in our context of interest because the private firm ownership stake is in most cases not tradable on a liquid market for corporate control, which implies the absence of less effortful value appraisal processes. Value assessments, which often imply interpretations and comparisons that require extensive information processing, make affect infusion more likely. Moreover, since ownership in family firms is often held with transgenerational sustainability intentions (Chua, Chrisman, & Sharma, 1999), the asset is originally not held for exchange, thus increasing the novelty of the value assessment task and the likelihood of affect infusion (Forgas, 1995). Similarly, because the ownership stake is most often personally relevant to the owner, both in financial and nonfinancial terms (Sharma et al., 1997), affect infusion through substantive processing is highly probable, given the necessity to carefully assess the change in asset position.

Affect Infusion and Family Owners’ Ownership Value Perceptions

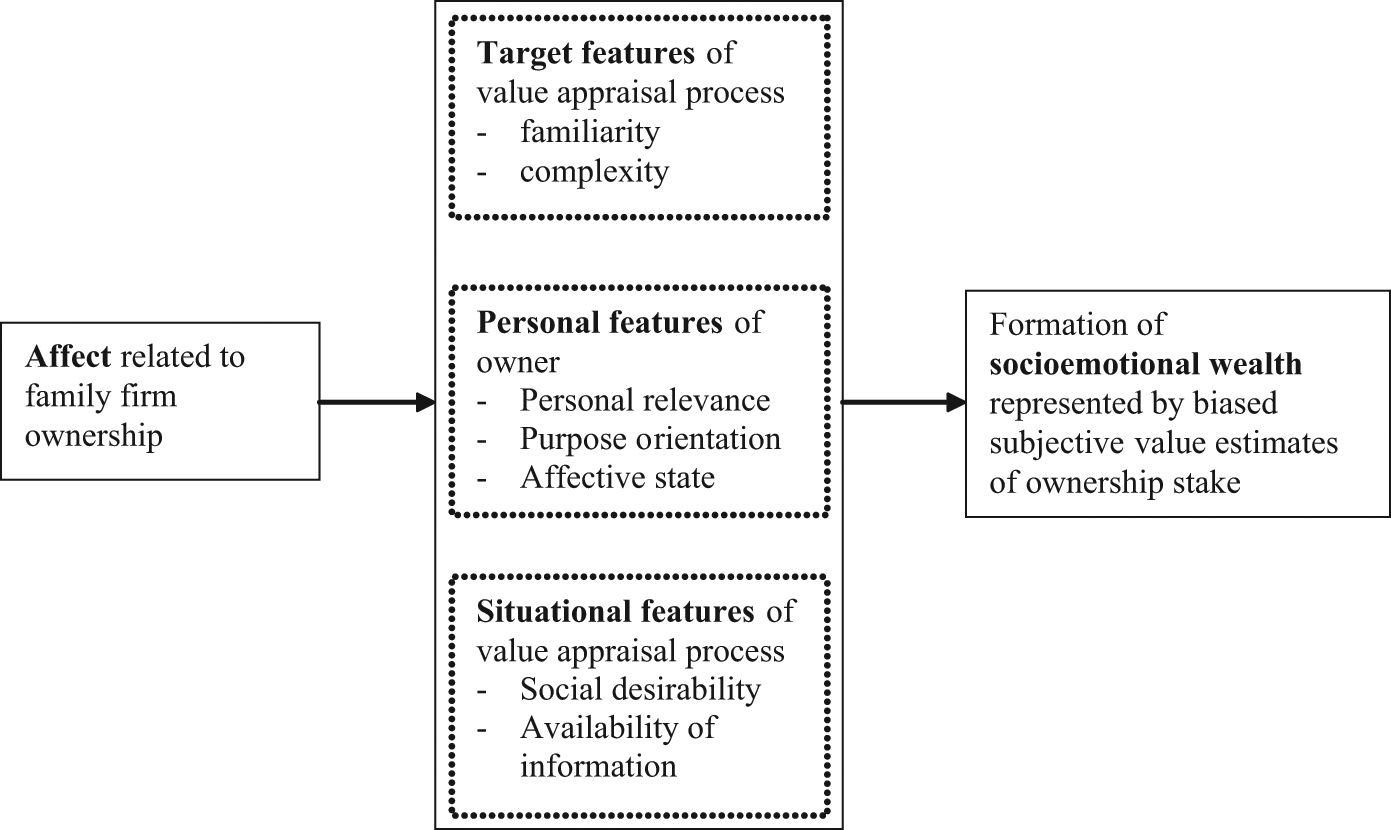

In line with the AIM and acknowledging heterogeneity among family firms as well as their owners (Melin & Nordqvist, 2007), we suggest that the degree of substantive processing, that is, the degree of affect infusion in the formation of owners’ subjective ownership value assessments, is dependent on (a) the target features of the value assessment process, (b) the personal features of the owner assessing the value, and (c) the situational features under which the value is determined (Forgas, 1995). In other words, building on both SEW literature (Gomez-Mejia et al., 2007) and affect infusion theory (Forgas, 1995), our model suggests that affect exerts an influence on value perceptions and hence SEW through target, personal, and situational features of the value assessment process. Accordingly, we see target, personal, and situational features of the value assessment process as mediators linking affect related to ownership on one hand and SEW on the other hand. This logic is represented in below Figure 1 and is further explored in the next sections.

Relationship between affect related to family firm ownership and socioemotional wealth mediated by target, personal, and situational features

Target Features in Determining Family Owners’ Ownership Value Perceptions

The AIM suggests that target features (i.e., features of the owner’s utility evaluation process of the ownership stake) influence the choice of information-processing strategy. It is argued that the more familiar the target, the more likely a non-affect-infused processing strategy (i.e., low affect infusion) will be pursued (Forgas, 1995). Familiarity with value appraisals, as argued in the AIM, means that the owner (as judge) possesses detailed and extensive information about the value of the ownership stake in question, for example, when acquisitions and divestments of corporate ownership are executed regularly and necessary information is readily available. In large, family-controlled holding companies where owners regularly adjust the firm’s portfolio, owners possess expertise in value assessment. As do experienced venture capitalists, family firm owners rely in that particular case on various routines and mental shortcuts that increase efficiency and minimize intensive processing (Shepherd, Zacharakis, & Baron, 2003). This allows them to make decisions in a more habitual manner—that is, through automatic processing rather than through more conscious, step-by-step systematic processing (Logan, 1990; Zacharakis & Shepherd, 2001).

However, if the owner is inexperienced in value assessments, the task likely becomes challenging, thus slowing considerations of firm value (Shepherd & Haynie, 2009) and making it more likely that affect will infuse the unfamiliar cognitive process. For example, when owners are inexperienced with assessing objective business performance data that facilitates the value appraisal process or have limited experience with corporate control transactions, they will compensate by using an extended and elaborate processing strategy when determining the value of a firm. In sum, unfamiliarity with value assessment of the ownership stake should heighten affect infusion and increase SEW considerations, thereby biasing corporate value perceptions.

The AIM further predicts that task complexity is positively correlated with the choice of substantive information-processing strategies and, thus, with the degree to which affect biases individual value perceptions. Experimental studies have shown that complex tasks require elaborate processing strategies to generate a coherent impression, with greater availability of affect-primed information influencing the judgment or decision (Forgas, 1992). In accordance with this explanation, the impact of mood effects is expected to be greater if the value appraisal process of the ownership stake is difficult, since this leads to more extensive processing. Although the stock market eliminates such complexities through the value-revealing pricing mechanism, the challenge is considerable in privately held firms. Beyond the limited fungibility of ownership stakes, complexity of value assessments may be exacerbated when an ownership stake is vested with extended control mechanisms, such as pyramidal groups that separate ownership from control, the entrenchment of controlling families, and non-arm’s-length transactions (i.e., “tunneling”) between related companies (Morck & Yeung, 2003). In these cases, the ultimate value of the ownership stake may be particularly complicated to assess, given the various ways through which funds can be extracted from controlled firms and minority shareholders and accumulated at the apex of the family-controlled corporate structure (Johnson, La Porta, Lopez-de-Silanes, & Shleifer, 2000).

The complexity of subjective value assessments of corporate ownership may be even more challenging when business finances are interwoven with owners’ personal finances (Haynes, Walker, Rowe, & Hong, 1999). The owner then must carefully handle private information, which likely demands substantial effort, given the absence of comparable cases against which the task could be benchmarked. In turn, complexity of the value assessment task should heighten affect infusion and increase SEW considerations, which ultimately biases corporate value perceptions.

These considerations on unfamiliarity with and complexity of the value assessment task are summarized as follows:

Proposition 1a: Affect from corporate ownership exerts an influence on an owner’s value perception for the ownership stake through the owner’s experiences in assessing the value of corporate ownership stakes and the transfer of corporate control. That is, the less experienced the owner, the more likely is affect infusion and hence SEW.

Proposition 1b: Affect from corporate ownership exerts an influence on an owner’s value perception for the ownership stake through the complexity of the corporate value assessment, measured through the complexity of the business structure and the intermingling of personal and business finances. That is, the higher the complexity, the more likely is affect infusion and hence SEW.

Personal Features in Determining Family Owners’ Ownership Value Perceptions

Beside target features of the value assessment process, the AIM accounts for personal features of the individual who assesses the value of a possession. For example, the owner pursues substantive processing of information and, hence, exhibits affect infusion when the task is of high personal relevance (Forgas, 1995). Personal relevance of ownership stakes may arise from both financial and nonfinancial sources in the context of family firm owners. Clearly, the level of embeddedness of the firm experienced by the owner depends on the fraction the ownership stake represents within the owner’s total wealth (Miller et al., 2010). When that fraction is high, personal relevance is high, given that changes in the possession’s worth have a strong impact on the global financial circumstances and, potentially, lifestyle choices of the owner. However, personal relevance may also be nurtured by nonfinancial elements such as identification with the asset, because affiliation with the firm increases the owner’s self-distinctiveness, self-awareness, and self-enhancement (Albert & Whetten, 1985; Dukerich, Golden, & Shortell, 2002). Some family firm owners may strongly identify with the controlled firm, for example, if the asset represents a family legacy, thereby contributing to the owner’s self-awareness. In turn, the more personally relevant the asset is to the owner, the more likely becomes affect infusion in value appraisal, thus increasing the likelihood of SEW considerations, which ultimately biases corporate value perceptions.

In addition, the AIM argues that an individual’s strong purpose orientation leads to low affect infusion processing strategies (Forgas, 2001). When the owner who assigns a value to her or his ownership stake is influenced by a strong, preexisting motivation, little open and constructive processing is used in interpreting the detailed features of the target, limiting the scope of affect infusion into the value judgment. For example, family firm owners with a strong motivation to realize the value of their ownership stake and an imminent motivation to sell may, therefore, exhibit low levels of affect infusion when assessing the ownership stake’s value. They are then more likely to benchmark their value perceptions against a comparable company and a reasonable economic value at which it can be traded on the market for corporate control. In the absence of an imminent purpose to sell, owners are more likely to focus on perceived personal importance of ownership and their sentiment toward surrendering the asset (Carmon & Ariely, 2000; Kahneman & Knetsch, 1992; Kahneman & Miller, 1986). Consequently, when owners have no specific motivation to assess the value of the ownership stake for selling purposes, it is more likely that affect should motivate family owners to assign biased value perceptions (Ariely et al., 2005).

Moreover, the AIM suggests that the affective state of the judge should influence the choice of affect-infusing processing strategies. A target-specific or context-dependent mood is believed to induce substantive processing, with positive mood eliciting more positive value assessments and negative mood more negative assessments. Mood-congruent judgments in cases of substantive processing have been confirmed in a wide series of psychological studies (Clore & Parrott, 1991; Erber & Erber, 1994; Parrott & Sabini, 1990; Salovey, O’Leary, Stretton, Fishkin, & Drake, 1991; Schwarz & Clore, 1983; Sedikides, 1994). Judges may use their mood as a point of contrast against which other information is retrieved or evaluated; in addition, mood facilitates the recall of memories congruent with the mood during substantive processing. Good mood, in a sense, indicates that the situation is favorable and that little monitoring and processing effort is required. This may lead to low affect infusion information-processing strategies for goods to which owners are indifferent. However, positive mood in the corporate context (e.g., harmony among owners and enjoyment of exercising control) is likely to instill substantive processing and raise compensation considerations for the forgone emotional benefits caused by the loss of the asset (Douglas & Shepherd, 2000). Such mood-congruent judgments for positive moods have been confirmed even for highly analytical tasks, such as the pricing of public stock ownership (Hirshleifer & Shumway, 2003) or the valuation of inventories by auditors (Chung et al., 2008).

These considerations on personal relevance, purpose orientation, and positive affective state are summarized as follows:

Proposition 2a: Affect from corporate ownership exerts an influence on an owner’s value perception for the ownership stake through the personal relevance of the ownership stake for the owner, measured as the asset’s value in relation to the owner’s total wealth and the level of identification of the owner with the firm. That is, the stronger the personal relevance of the asset, the more likely is affect infusion and hence SEW.

Proposition 2b: Affect from corporate ownership exerts an influence on an owner’s value perception for the ownership stake through purpose orientation of the owner, measured in terms of the owner’s intention to assess corporate ownership value with the aim of an imminent sale. That is, the stronger the purpose orientation, the less likely is affect infusion and hence SEW.

Proposition 2c: Affect from corporate ownership exerts an influence on an owner’s value perception for the ownership stake through the owner’s general affective state. That is, the more positive the affect state, the more likely is affect infusion and hence SEW.

Situational Features in Determining Family Owners’ Ownership Value Perceptions

The last category within the AIM that influences information-processing types is that of situation (Forgas, 1995). Social desirability is one such situational determinant on individual choices of information-processing strategies, which leads to more thorough and substantive information processing because the meaning of the possession depends on assessment by others (Forgas, 1995). Given that social desirability concerns depend on the norms of the social context and the power of social actors to enforce these norms (Mann, 1986), the impact of social desirability on value appraisal is context specific. In a social context with salient stakeholders who also value noneconomic goals, it is more likely that nonfinancial utility considerations and affect flood the owner’s value appraisal process, resulting in biased corporate value perceptions (Villanueva & Sapienza, 2009). For instance, co-investors from the same family with a goal set that includes noneconomic elements, and firms with strong employee representation and concerns about public perception, shape a context where value perception in pure economic terms may find limited social acceptance. This is then likely to be reflected in an affect-infused value appraisal, which is most likely reflected in biased perceived ownership values.

Although these considerations may be representative of the prototypical case of the locally rooted, closely held family firm, social desirability norms are expected to differ widely for salient stakeholders with pure financial goals. For example, for institutional co-investors or for firms that consider venture capital funds as owners, the social norm likely shifts to a more economic rationale (Villanueva & Sapienza, 2009). The norms of these actors and the power they hold are more likely to crowd out affect in the assessment of corporate value perceptions. Owners, therefore, are persuaded to “face the facts” and reduce sentimentality, which raises owner awareness of affect infusion and resets affect priming (Erber & Erber, 1994). Accordingly, to the extent the goal set of the most salient stakeholders of the firm coincides with a pure economic logic, social desirability concerns about the consideration of the largest co-investor leads to low affect infusion in the ownership value assessment process.

In addition, affect infusion literature purports that the availability of information for evaluation of a task biases information-processing strategies. The AIM assumes that affective states interact with and inform cognition and judgments by influencing the availability of cognitive constructs used in the processing of information (Forgas, 1995). In the presence of detailed information required for the task, individuals will be inclined to use low affect infusion processing strategies. In the absence of such information, however, shortcuts or simplifications are unavailable (Paulhus & Lim, 1994) and the evaluation process requires more effort. Extending this line of thinking to the availability of information to assess the value of a corporate ownership stake, literature rooted in the entrenchment hypothesis of organizational ownership (Morck, Shleifer, & Vishny, 1988) finds that certain family firms practice lower quality accounting methods to protect the family’s interests at the expense of nonfamily shareholders (Schulze et al., 2003). Firms with concentrated family ownership, therefore, have fewer incentives to engage in high-quality accounting methods; they tend to withhold such information because the perceived benefits of sharing private information with outside parties are modest (Fan & Wong, 2002). Even internally, detailed and objective information (e.g., on business performance) may be scarce, given the complexity of diversified corporate structures in which business units are cross-subsidized (Morck & Yeung, 2003). Also, a family firm owner can face incentives not to develop such information, given the efficiency benefits of trust-based approaches among board members, the managerial team, and representatives of family owners. Thus, owners are spared from expensive collection and analysis of business information used to monitor and align interests (Anderson & Reeb, 2003). The negative side of these relational-based approaches is that family firm owners may be inclined to conceal objective business information to protect underperforming family members.

Based on this reasoning, many family firms tend to edit lower quality accounting information (Cascino, Pugliese, Mussolino, & Sansone, 2010; Stockmans et al., 2010; Wang, Keswani, & Taylor, 2006). Accordingly, we expect that in the presence of such opaqueness, value assessments of corporate ownership are particularly challenging. Along the precepts of affect infusion theory, we argue that with decreasing availability of business-related data required to assess the value of the firm, the level of affect infusion rises, given the need for substantive information processing. In consequence, this will result in biased ownership values.

These considerations of social desirability and availability of data are summarized as follows:

Proposition 3a: Affect from corporate ownership exerts an influence on an owner’s value perception for the ownership stake through the nonfinancial motivations of salient stakeholders. That is, the more salient stakeholders are motivated by nonfinancial goals, the more likely is affect infusion and hence SEW.

Proposition 3b: Affect from corporate ownership exerts an influence on an owner’s value perception for the ownership stake through the availability of business performance data and quality of reporting systems. That is, the more available such data and the more developed reporting systems, the less likely is affect infusion and hence SEW.

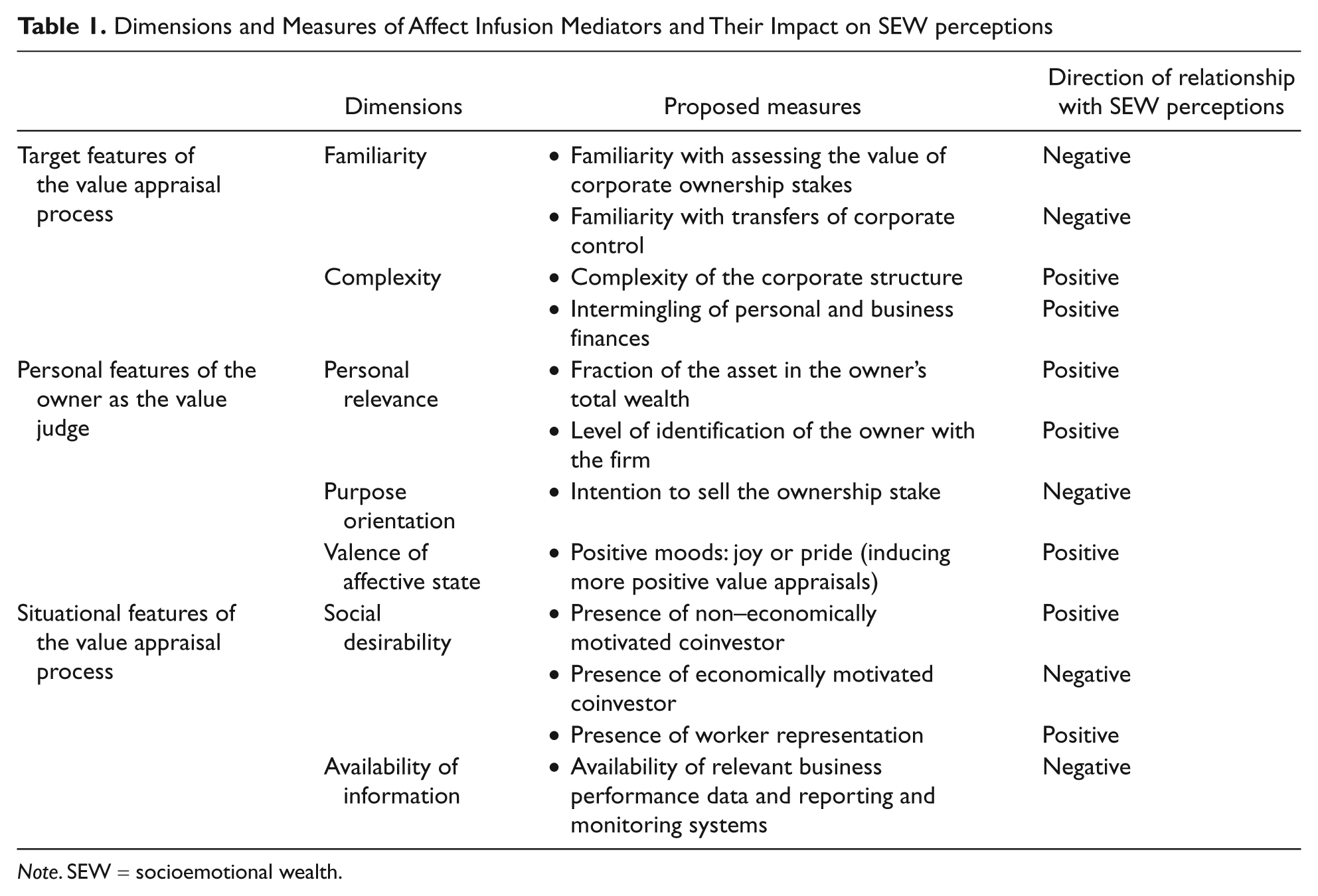

In sum, we propose a model predicting the influence of affect related to corporate ownership on owners’ value perceptions through target, judge, and situational elements related to the value assessment task for the corporate ownership stake. Our reasoning for such a mediating effect for AIM variables just as the proposed measurement of the variables mentioned in our propositions are depicted in Table 1.

Dimensions and Measures of Affect Infusion Mediators and Their Impact on SEW perceptions

Note. SEW = socioemotional wealth.

Illustrative Case: Ingvar Kamprad From IKEA

To illustrate our rationale it seems helpful to apply our thinking to a concrete example. We chose the case of Ingvar Kamprad who controls IKEA, a multinational furniture chain with annual revenues of more than €20 billion, officially headquartered in Sweden (Schwarzer, 2011), and contend that SEW considerations as reflected in biased value estimates should be very prevalent for Ingvar Kamprad.

For the case of personal features, the firm’s name IKEA, which stands for Ingvar Kamprad Elmatryd, the name of his parents’ farm, and Agunnaryd, the name of his home municipality (Mourkogiannis, Unger, & Vogelsang, 2007), can be seen as a symbol for the owner’s sense of identification with the firm. Furthermore, Kamprad explicitly has no intention to sell his firm. To protect his entrepreneurial legacy against a possible sale, Kamprad has introduced a sophisticated legal structure using multiple foundations to control the ownership rights (Schwarzer, 2011). Moreover, Ingvar Kamprad has expressed his intention not to sell out but to keep the firm under family control by appointing his sons Peter, Jonas, and Mathias to top management positions.

Regarding target features of the firm, through the aforementioned governance mechanisms the firm exhibits a highly complex organizational structure, motivated not only by concerns to preserve power but also by tax considerations. This complexity is also reflected in the geographical spread of the top management bodies of Kamprad’s empire, which are located in the Netherlands, Sweden, and Lichtenstein. Moreover, functional divisions are separated between a “blue,” a “red,” and a “green” group, which are responsible for the management of IKEA operations, brand/franchise management, and private wealth management, respectively (Schwarzer, 2011), thereby leading to an intermingling of business and private finances.

Regarding situational features, because the firm is privately held and because the Kamprad family is sole owner of the firm, there is no salient co-investor who could eventually limit affective influences and induce a more rational point of view.

Taken together, and based on these personal, target, and situational features, it will be likely that Kamprad experiences affect infusion when considering an acceptable sale price and hence display heightened SEW perceptions.

Discussion

Building on behavioral theories, such as prospect theory, the behavioral theory of the firm, and the behavioral agency model, we argued that owners are willing to part with an asset only if they are compensated commensurately with the perceived loss of SEW (Ariely et al., 2005; Tversky & Kahneman, 1991; Wiseman & Gomez-Mejia, 1998). Put differently, in the presence of SEW considerations, perceived values for ownership stakes are biased and deviate from economic value since owners strive for compensation of the loss of SEW. Hence, SEW is reflected in biased subjective value appraisal for the ownership stake. Whereas power- and identity-related reasons for the formation of SEW and acceptable sale prices have been discussed elsewhere (Zellweger et al., 2011), the present article draws on cognitive psychology literature, more specifically the AIM (Forgas, 1995) to develop a conceptual framework exploring the role of affect in these processes. Based on this theoretical strand, we introduce target, personal, and situational features in the subjective value appraisal process as mediators in the relationship between affect related to corporate ownership and subjective value perceptions of ownership stakes.

Our article makes several important contributions to the literature. First, by using the AIM to explain under which conditions affect biases corporate value perceptions, we shed light on the impact of an underexplored source of SEW. Recent studies have examined social dimensions of SEW such as identity concerns, community status, and transgenerational sustainability intentions (Berrone et al., 2010; Gomez-Mejia et al., 2007; Zellweger et al., 2011). By failing to acknowledge affect infusion theory (especially given the context of socioemotional wealth), current SEW literature risks overlooking a rich stream of psychology research that holds promise for the further advancement of a SEW theory (Forgas & Bower, 1987; Forgas & Ciarrochi, 2001; Forgas & George, 2001; Hirshleifer & Shumway, 2003). In our attempt to advance toward a theory of SEW, we thus outline the individual-level psychological processes that lead to SEW perceptions.

Building on the AIM, we explain how target features of the value appraisal process, such as unfamiliarity with value assessments of corporate ownership stakes or complexity of the value appraisal task, induced, for example, by a complex corporate structure, make it more likely that owners are affect infused when attributing a value to their ownership stake; thus, they indicate values for their ownership stake that significantly deviate from objective market values determined by financial considerations only. We also suggest that the more personally relevant the asset is, for example, as the firm represents a high fraction of the owner’s total wealth or the family firm has an important personal meaning to the owner, the more likely the owner is affect infused when determining the asset’s value and develops SEW leading to biased value perceptions. Similarly, we suggest that the stronger the purpose orientation of the owner to imminently realize the value of the asset (i.e., to sell), the less likely the owner uses affect-priming processing strategies, thus reducing the relevance of SEW considerations that would bias value considerations.

With regard to affective state, we theorize that the more positive the general affective state, the more likely the owner uses substantive information processing, thereby exhibiting mood-congruent value appraisals and, hence, heightened SEW and biased value perceptions for the ownership stake in the family firm. Only partly in line with the AIM, we suggest that social desirability concerns should lead to affect infusion and SEW perceptions in a context that values noneconomic utility arising from corporate ownership. However, in a context in which economic rationality prevails (e.g., when strong co-investors have pure financial interests), social desirability should eliminate affect infusion. Finally, we argue that in the absence of detailed information needed to judge the value of the firm, shortcuts or simplifications are unavailable; therefore, the evaluation process requires more effort and an affect-infused analysis. In turn, SEW considerations emerge, which bias corporate value perceptions.

Our considerations about the creation of SEW reaches well beyond existing research that has chiefly considered family firm owners as homogeneous in their SEW perceptions (Berrone et al., 2010; Gomez-Mejia et al., 2007; Gomez-Mejia et al., 2010; Jones et al., 2008; Miller et al., 2010). We challenge this homogeneity assumption by exploring the varying salience of aspects of the value assessment process, aspects of the owner, and aspects of the owned asset in framing the valuation process and, ultimately, endowing owners with SEW.

As a second contribution, our study adds to the prominent call in family business and mainstream management research to address the reasons why certain types of owners, and family firm owners in particular, are expected to value nonfinancial goals (Sharma et al., 1997; Thomsen & Pedersen, 2000). By focusing on the AIM, we provide a theory-based rationale to this observation that may not be limited in its application to family firms.

Also, our study builds on a recent development in the area of behavioral theories, which considers the role of affect in shaping reference points (e.g., Greve, 1998). We argue that the biased valuation of ownership stakes can be explained, at least partly, by affective elements. Even though this claim has been made before (Lerner et al., 2004; Zhang & Fishbach, 2005), we are among the first to show that affect infusion in the process of reference point formation should also hold for assets that are held for seemingly purely financial reasons.

Finally, these findings also speak to the subjectivist perspective of entrepreneurship, since we account for the fact that individuals hold different preferences and expectations: more specifically, that the contents of the human mind and, hence, decision making, are not rigidly determined by external events (Foss et al., 2008; Hayek, 1948; Penrose, 1959).

Limitations and Opportunities for Future Research

We would be remiss not to note the limitations to our study. Our considerations of affect infusion and SEW perceptions are not equally relevant for all types of corporate owners. Although the spillover of affect in the context of publicly quoted ownership stakes may be limited given the permanent availability of an objective price (albeit affect infusion has been found to persist even in this particular setting; see Hirshleifer & Shumway, 2003), our considerations may be particularly relevant but not limited to owners of privately held family firms, especially owners who not only hold a financial stake but also work in the controlled firm (Schulze & Gedajlovic, 2010).

Also, we have to acknowledge that the AIM is an individual-level theory. Therefore, we are hesitant to extend our arguments to the family group level. Our arguments seem particularly applicable to the case of a sole owner or to the case where the actors experience a shared sentiment toward the firm. Such a perspective of treating a family as a unitary actor with a common view and sentiment toward ownership in the firm is in line with a common practice among social scientists to attribute properties and opinions of an individual to those of a group (Nordqvist & Melin, 2010). For example, researchers often take a key informant approach to explore organizational behavior. Bourdieu (1996) even contends that the family acts as a collective subject even more than internally weaker institutions such as firms. Hence, even family firms with a dispersed ownership structure, through the social norms for harmony and mutual support, not to mention the factual inability to leave one’s family, will have various types of family governance mechanisms that should lead to a common point of view and affect toward the ownership, which then suggests that family can be treated as a collective subject.

We hasten to add that we did not examine all factors that are part of the AIM (Forgas, 1995). For example, it seems arduous to us to apply predictions on situational features, such as task publicity or need for accuracy, which should lead to affect infusion (Forgas, 1995), to the corporate context. Our decision not to include these features in our theorizing is based on the argument that publicity of, or need for, accuracy in the value appraisal process may result in more rational and affect-free information processing, which is anathema to the predictions of the AIM. We theorize that task publicity and need for accuracy force owners to accept economic rationality in a “fact-based” corporate world. In a similar way, we have explored limitations of the standard precepts of the AIM regarding social desirability, which suggests that social desirability should always leads to more affect infusion. As demonstrated through Proposition 3a, we take a more nuanced stance on this relationship.

Also, we excluded a potential reciprocal relationship between SEW and affect. Although we argued for a causal relationship between affect and SEW via affect infusion variables, it may be possible that SEW concerns nurture certain emotions, suggesting reverse causality. For example, “seeing more than the money” in a firm may nurture feelings of joy and pride. However, in an effort to stick to the causal direction as argued in the AIM and to sustain the parsimony of our article, we refrained from introducing such reciprocal or moderating relationships into our model (Whetten, 1989).

It is important to note that SEW considerations and corporate value perceptions may not always move in parallel. We suggest that depending on the presence of the factors outlined above, affect infusion in value appraisals creates a reference point from which owners are willing to part only if they are compensated commensurately with the loss of SEW. Therefore, one may implicitly assume a positive relationship between SEW and acceptable sale price, an argument that corresponds to the underlying rationale in current SEW literature (Gomez-Mejia et al., 2007) and improves the parsimony of our article (Whetten, 1989). However, in the presence of negative utility (e.g., negative moods), the relationship can be less straightforward, since negative mood can cause both mood congruent and incongruent, hence, reduced, but also heightened, value appraisals (DeSteno, Petty, Wegener, & Rucker, 2000; Foo, 2011; Forgas, 1995; Keltner et al., 1993; Lerner & Keltner, 2000; Lerner et al., 2004). Whereas certain negative moods (e.g., sadness) may instill withdrawal behavior and reduced value perceptions (Lerner et al., 2004), other negative moods (e.g., anger) may induce people to “repair” their moods (Forgas, 1995) by pricing the associated sunk costs (Arkes & Blumer, 1985); thus, value perceptions are heightened by negative feelings. In fact, it is even conceivable that in the presence of positive emotional environments of firm ownership (e.g., feelings of accomplishment and happiness), owners may be willing to sell for lower corporate value perceptions, since they may perceive that they have reached their financial and nonfinancial goals and are satisfied with their achievements. This seems to be an area ripe for future research.

Future research could empirically investigate the predictive power of our propositions. Moreover, and although we position our ideas in an ongoing ownership context, it seems fruitful to test our predictions in the context of actual transfers of corporate control. Scholars could, for example, investigate how the proposed measures depicted in Table 1 can help explain transactions likelihoods or the length of negotiation periods, assuming that strong positive SEW perceptions and hence overvaluation of the equity stake reduce the likelihood of transactions and extend negotiation periods.

More broadly, the AIM holds promise in explaining how affect biases cognitive processes beyond value perceptions. Within the family firm context, it seems interesting to examine whether the AIM variables introduced in Table 1 are able to elucidate family firm behavior that has been attributed to SEW considerations (up to this date measured mainly through family ownership), such as the reluctance of family firms to internationalize, to diversify or to enter less risky governance forms (Gomez-Mejia et al., 2007; Gomez-Mejia et al., 2010; Miller et al., 2010). Beyond the family firm context, introducing the AIM variables as mediators in analyses between individual-level features of decision makers and firm-level behavior may add additional clarity to the root causes of organizational behavior.

Finally, we see an opportunity to examine the linkages between the institutional setting as an unexplored situational variable, level of affect infusion, and the creation of SEW. Building on recent findings on the link between the institutional environment and entrepreneurial cognitions (Lim, Morse, Mitchell, & Seawright, 2010), we propose that the institutional setting, in particular the protection of property rights, should be considered as a situational feature for affect infusion. With strong protection of property rights, assets tend to be allocated more efficiently, since secure possession of physical and intellectual assets eases their transfer to the most efficient use (McMullen, Bagby, & Palich, 2008; Whitley, 1999). In such a context, possessions are more likely to be traded and held for exchange, making value appraisals less affect infused. In contrast, when property rights’ protection is low, assets will more likely be held for use and ongoing ownership, which makes it more likely that assets are imbued with personal meaning (Strahilevitz & Loewenstein, 1998).

Implications for Practitioners

Our study has important implications for practitioners. If owners consider more than the monetary value of the firm, they may persist with marginal activities, delay a sale, or hold on to an underperforming business, which raises the economic cost in case of bankruptcy (Shepherd et al., 2009). By exploring sources of SEW, we make owners aware of potential sources of economic costs. These costs, however, accrue not only at the level of the individual owner but also at the societal level, since SEW perceptions restrict or impede the efficient allocation of capital. Given that in many cases SEW considerations make a transfer of corporate control less likely, being aware of these affect-based drivers may encourage owners to distance themselves from their firms to enable timely succession (Miller, Steier, & Le Breton-Miller, 2003). Therefore, raising awareness of the sources of affect infusion seems critical, since it resets these biases and helps avoid undesired effects (Erber & Erber, 1994).

Although SEW considerations may have detrimental effects on controlled firms, it is important to acknowledge their potential benefits. By lowering the impact on threshold levels of performance (Gimeno, Folta, Cooper, & Woo, 1997) and costs of owner-provided capital, SEW provides the necessary leeway for entrepreneurial activity to succeed, which may be particularly beneficial when others are unable to assess or may underestimate the value of ownership, such as in founding, innovation, and turnaround processes. Taken together, practitioners need to be aware not only of the drawbacks but also of the potential benefits of SEW.

Conclusion

The claim that family firms (the majority of firms) should be motivated by both financial and nonfinancial value perceptions challenges some of the most fundamental assumptions of economic theory. Our article, which explores affect as a source of such nonfinancial value perceptions, contributes to the further establishment of SEW theory regarding family firm ownership. This is a fascinating area of research that deals with the most fundamental assumptions of corporate ownership.

Footnotes

Acknowledgements

We would like to thank Maw der Foo, Eric Gedajlovic, Paul Shrivastava, the participants of the Family Business Research Workshop at the Concordia University -John Molson School of Business, Montreal, and the three anonymous reviewers of Family Business Review. We would also like to thank Pramodita Sharma and Michael Carney for their valuable comments on earlier versions of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Bios

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.