Abstract

Building on a longitudinal case study, this article describes the entrepreneurial behavior of a multinational family firm over generations. The study inductively raises the theoretic level to fill gaps in the literature about the family role in entrepreneurial behavior and addresses the singular count of the two- and three-circle models. The data analysis shows that entrepreneurial behavior emerges not only in response to business challenges but also and predominantly to family challenges. The cluster model is suggested as a necessary extension of the circle models, positing the family as the relevant level of analysis when considering entrepreneurial behavior and introducing the distinction between organic and portfolio, core and peripheral firms.

When looking at entrepreneurship in family firms, “very little attention has been paid to how family dynamics affect fundamental entrepreneurial processes” (Aldrich & Cliff, 2003, pp. 573-574). Although some earlier scholars used the term entrepreneurial family (e.g., Heck, 1998; Rosenblatt, de Mik, Anderson, & Johnson, 1985) and by this referred to the family as the driving force of entrepreneurial behavior in family firms, literature reviews on entrepreneurship show that the firm, and not the family, has been the dominant level of analysis (Davidsson & Wiklund, 2001; Martinez, Yang, & Aldrich, 2011).

A recent rising interest in the family role in entrepreneurship has been manifested, especially when relating to family firm’s generational continuity (Habbershon, Nordqvist, & Zellweger, 2010; Habbershon & Pistrui, 2002; Zellweger, Nason, & Nordqvist, 2012). Several constructs have been suggested to understand the family’s contribution in pursuing firm longevity, such as transgenerational entrepreneurship (Habbershon et al., 2010), family social capital (Dyck, Mauws, Starke, & Mischke, 2002), transgenerational family effect (Morris & Peng, 1994), transgenerational wealth (Habbershon & Pistrui, 2002), family entrepreneurial orientation (Zellweger et al., 2012), and family socioemotional wealth preservation (Gomez-Mejia, Cruz, Berrone, & De-Castro, 2011). Habbershon et al.’s (2010) definition of transgenerational entrepreneurship captures the main ideas in these constructs: “the processes through which a family uses and develops entrepreneurial mindsets and family influenced capabilities to create new streams of entrepreneurial, financial and social value among generations” (p. 7). However, as stated clearly by Schjoedt, Monsen, Pearson, Barnett, and Chrisman (2013), “there is still much we do not know, and there has been lack of concerted effort to develop a theory that applies to the specific circumstances and contingencies facing entrepreneurial or family business teams” (p. 3). In addition, “the realization that there is not necessarily just one family business, but a group of family businesses, many of which are the result of entrepreneurial family activities and processes, is one whose implications are fundamental, but yet to be fully conceptualized and investigated” (Rosa, Howorth, & Cruz, 2014, p. 367).

Moving to the family and team levels of analysis adds two separate and new sources of complexity referring (a) to entrepreneurship as a social process with diverse participants and (b) to a mechanism through which the entrepreneurial vision is translated via action, control, and resource mobilization of multiple firms in order to extract value and accumulate assets. Recent studies try to understand these two processes: (a) looking at the group of owners by studying the number (Kellermanns, Eddleston, Barnett, & Pearson, 2008; Sciascia, Mazzola, & Chirico, 2013) and identity of family generations involved in entrepreneurial behavior (Kellermanns & Eddleston, 2006), or the different nature of family relationships that influence new venture’s outcomes (Brannon, Wiklund, & Haynie, 2013; Danes, 2011, 2013). (b) Others study the second process, by focusing on portfolio family firms (e.g., Discua-Cruz, Howorth, & Hamilton, 2013; Mäkimattila, Rautiainen, & Pihkala, 2013; Sieger, Zellweger, Nason, & Clinton, 2011). However, there is only a small number of empirical and theoretical studies on these issues with no theory that explains them (Gomez-Mejia et al., 2011; Iacobucci & Rosa, 2010; Schjoedt et al., 2013). Furthermore, the studies focus solely on entrepreneurs and new firms rather than looking at families over long sweeps of time (Aldrich & Cliff, 2003; Chang, Memili, Chrisman, Kellermanns, & Chua, 2009). Therefore, scholars aspire for more nuanced and longitudinally oriented research methodologies, which are able to appreciate the inherently complex, and often idiosyncratic, nature of performance in both family and firm, along with frameworks and methods to be deployed in engaging a more diverse set of topics and international contexts (Litz, Pearson, & Litchfield, 2012, pp. 27-28). Specifically, to understand how families engage in entrepreneurial behavior, more longitudinal (Brockhaus, 1994; Kellermanns & Eddleston, 2006; Steier, 2007; Zahra & Covin, 1995) and archival studies (Martinez et al., 2011) are needed.

In order to address these gaps, our general research question is inspired by Aldrich and Cliff’s (2003, p. 591) call for answers to the question of “to what extent do changes in family system characteristics affect the timing and pacing of venture creation processes?”. Our research question is therefore twofold in nature: (a) how major events of change in the family system and the business system are translated into entrepreneurial moves in the family business and (b) whether family-based or business-based antecedents play the utmost role over time in terms of entrepreneurial behavior in the family business. Building inductively on a qualitative case study, this article presents an enlarged perspective that gives voice to those living an experience (Corley & Gioia, 2004; Plate, Schiede, & von-Schlippe, 2010). This perspective focuses on building an emergent theory from an interpretive qualitative illustration (Nordqvist & Zellweger, 2010). The longitudinal case study presented in this article explores the Pery family firm where the family has behaved entrepreneurially over three generations. The organizational context of the family managing its assets is thoroughly described and analyzed to suggest a series of propositions.

By enfolding the extant literature as an essential feature of an inductive approach (Eisenhardt, 1989), the predominance of the family level of analysis in explaining entrepreneurial behavior over time and the business portfolio evolution suggests a necessary update and extension of the Two- and Three-Circle Models (Gersick, Davis, McCollom Hampton, & Lansberg, 1997; Tagiuri & Davis, 1996) accordingly. Several limitations have already been attributed to these models, such as pushing into dualistic dichotomies (Habbershon & Pistrui, 2002; Whiteside & Brown, 1991), not accounting for the variations in the circles given the boundary considerations (Distelberg & Blow, 2011; Labaki, Michael-Tsabari, & Zachary, 2013; Sundaramurthy & Kreiner, 2008; Zody, Sprenkle, MacDermid, & Schrank, 2006), and lacking nonlinear or time considerations in the family firm evolution (Habbershon & Pistrui, 2002).

This article suggests the cluster model to update the three-circle models by embracing the family-level constructs of transgenerational entrepreneurship while providing a more exhaustive picture of the circles’ evolution over time. While the original bivalent two-circle model appropriately describes a family that owns a firm (Tagiuri & Davis, 1996), this article addresses the inappropriateness of the circle models when it comes to describing a family that owns more than one firm. Simply put, the cluster model is offered as an extension of the three-circle model that is an oversimplification of the two-circle model in which the fundamental building blocks are the family system and business system.

The article is organized as follows: We start with a literature review highlighting the need to view the family as the driving force of entrepreneurial activity within the family firm. The case study follows to describe the entrepreneurial behavior and its elicitors in the Pery family firm with a series of propositions. The cluster model is then introduced as a major update and extension of the circles models. The study limitations and future research directions are finally presented.

Previous Research

Family as a Unit of Study in Family Firms

A fundamental problem in studying the family as a unit of analysis is that even family researchers admit that “we lack a generally agreed-upon definition of what exactly a family is” (Greenstein & Davis, 2013, p. 8). Families have been studied extensively by social scientists (e.g., Elder, 1985; Moen, 1998) while businesses have been, for the most part, the focus of business scholars. Successfully combining the two fields of study is challenging (James, Jennings, & Breitkreuz, 2012). Many family business scholars see only one system, that is, the business. As Aldrich and Cliff (2003) note, “To some extent, this oversight is understandable. After all, business and families are commonly considered to be distinct social institutions and, as such, are typically investigated by scholars in separate faculties” (2003, p. 574). Yet some researchers posit the simultaneous consideration of both the family system and the business system (Zachary, 2011; Zachary, Danes, & Stafford, 2013). Lately, Chrisman, Chua, Pearson, and Barnett (2012) aim at having a more nuanced understanding of how exactly does the family influence the business while demonstrating the different roles of family involvement and family essence.

The Family as the Driving Force of Entrepreneurial Behavior in Family Firms

The fields of entrepreneurship and family business have to a great extent developed independently, but they have been moving closer to each other over the past decade (Anderson, Jack, & Drakopoulou-Dodd, 2005; Nordqvist & Melin, 2010). Two different topics rise when examining the nexus of entrepreneurship and family businesses: one is the unique features of the family institution’s role in the processes and outcomes of entrepreneurship, termed as the entrepreneurial family, and the second is the significance of entrepreneurship in the type of organization represented by family firms, termed as the entrepreneurial family business (Nordqvist & Melin, 2010, p. 214). Entrepreneurial family was used earlier by Rosenblatt et al. (1985) followed by other researchers (e.g., Heck, 1998; Zachary, 2011). Aldrich and Cliff (2003) admit that “very little attention has been paid to how family dynamics affect fundamental entrepreneurial processes” (pp. 573-574). More recently, other scholars made similar calls for the study of the family’s influence on entrepreneurship (e.g., Chang et al., 2009; Irava & Moores, 2010).

Looking at the entrepreneurial family means moving from the firm to the owners’ level of analysis. However, in the existing literature on entrepreneurship, two reviews (Davidsson & Wiklund, 2001; Martinez et al., 2011) show that the firm has been the dominant level of analysis. According to Davidsson and Wiklund (2001), the conventional levels of analysis dominate the field because researchers have a preference to collecting data that are easily obtainable rather than important. As noted earlier by Brockhaus (1994), “field studies . . . are difficult to achieve because of the entrepreneurs’ and family business owners’ disinterest in participating in such studies” (1994, p. 26). The limits of firm-level analysis of entrepreneurship have been raised by several scholars (Carter & Ram, 2003; Scott & Rosa, 1996). When the firm is the only fundamental unit of definition and analysis, part of the wider entrepreneurial reality of capital utilization and accumulation process is missed. As Scott and Rosa (1996) sum it up: “if all you study is small firms, that is all you will ever see” (p. 82).

Moving to the stakeholders’ level of analysis adds two separate and new sources of complexity referring to (a) entrepreneurship as a social process with diverse participants (Coase & Wang, 2011; Danes, 2013; Iacobucci & Rosa, 2010; Martinez et al., 2011) and (b) the mechanism through which the entrepreneurial vision is translated via action, control, and resource mobilization of multiple firms in order to extract value and accumulate assets (Habbershon et al., 2010; Scott & Rosa, 1996). Therefore, moving to the family’s level of analysis when studying entrepreneurship allows us to look at how a group of individuals may own a group of firms.

Entrepreneurship as a Social Process: “A Group of Individuals”

Coase, a Nobel Laureate, and Wang (2011) offer a more comprehensive view of entrepreneurship by referring to it as a “social process” among many entities and individuals, suggesting that a single disciplinary view of the firm is myopic and incomplete. The predominance of the firm as the unit of analysis in entrepreneurship research is particularly obscuring for family firms: “Contrary to popular images of the entrepreneur as a lone wolf, it might “take a village” to create a new firm, and the relationships between those involved in the initial entrepreneurial efforts affect the firm for many years after its founding . . . The internal dynamics of both firms and families are key to understanding their success or failure” (Martinez et al., 2011, p. 21). The use of the individual entrepreneur as the main unit of analysis may be equally misleading since evidence shows that the individual behavior results from complex interactions among all stakeholders (Carter & Ram, 2003). The new venture’s creation act by itself can be the product of changing emotional relationships within the family, as showed by Cramton (1993), who was among the pioneering and rare scholars to closely examine the family group from which the venture emerged. The use of the business–family as the unit of analysis recognizes the important role of family resources and capabilities and reflects more accurately the strategic priorities and influences manifested in the activities of the enterprise (Cliff & Jennings, 2005; Danes, 2013; Habbershon et al., 2010).

Starting to look at the identity and relationships among the group of family owners, findings show that the highest level of entrepreneurial orientation is achieved when two generations of the family are involved in the firm, rather than one (Kellermanns et al., 2008; Sciascia et al., 2013). Danes (2011, 2013) focuses on the entrepreneur as part of a couple while Brannon et al. (2013) analyze distinct types of family relationships and show that couples are more likely to achieve first sales than teams with blood relations. Nonetheless, there continues to be little focus on the inside dynamics of the family itself (Zachary, 2011; Zachary et al., 2013).

Entrepreneurship as a Process With Multiple Firms: “A Group of Firms”

Studying the owners of organizations may provide better answers to questions, such as how and why firms are created, grow and die (Carter & Ram, 2003; Scott & Rosa, 1996). Comparing novice and habitual founders, Birley and Westhead (1993) conclude,

If the business is the sole unit of analysis, there is a threat that the value of the new venturing event will be underestimated. It also indicates that future attempts to explain business growth should incorporate the possibility that owner-managers may attempt to resolve their personal materialistic aspirations through the growth of further multiple business operations, which may not be directly related to the single unit of analysis being studied. (p. 57)

Moreover, looking only at the firm level may hide the wider picture: if an entrepreneur chooses to start a new venture in a new organization that he also owns and prefers to manage a cluster of firms instead of only a single one, an individual firm may not grow but the cluster itself does, through the addition of “new” businesses (Carter & Ram, 2003; Scott & Rosa, 1996). Yet until recently, there was no systematic assessment of the frequency of multiple business owners in different economies (Scott & Rosa, 1996; Sieger et al., 2011; Westhead & Wright, 1998). Westhead and Wright (1998) define a portfolio founder as one who “retains his/her original business and inherits, establishes, and/or purchases another business” (p. 176). Although little is known about the underlying motivations and processes, it is likely that portfolio ownership has different forms and functions for owners in different circumstances and contexts (Carter & Ram, 2003).

By stressing the centrality of the family in social and economic wealth creation, Habbershon and Pistrui (2002) suggest the construct of ‘transgenerational wealth,’ defined as “a continuous stream of wealth that spans generations” (p. 223). With this construct, they aim at encompassing the traditional family and business relationship as well as the conditions under which a family diversifies its interests beyond a particular entity, while explaining that the strategic activity of the family unifies and drives its wealth creation intents. Habbershon et al. (2010) adopt a longitudinal perspective and term this family capability ‘transgenerational entrepreneurship’ that goes beyond how to grow and pass on a business organization to the next generation, to deal with the question of how families create new streams of value among generations. Zellweger et al. (2012) introduce the ‘Family Entrepreneurial Orientation’ (FEO) to study longevity in family firms and outline a conceptual approach taking the family as the unit of analysis, rather than the firm. However, it is important to recognize that FEO only looks at the ownership behavior and ignores the family system and its internal dynamics (Zachary, 2011; Zellweger et al., 2012). In their sample of family firms, Zellweger et al. (2012) find that only 10.6% of the firms control a single firm, while the mean number of firms currently controlled by the family is 3.4. Over time and the family’s history, family firms on average controlled 6.1 firms, created 5.4 firms, added 2.7 firms through merger and acquisitions, spun off 1.5 firms, and shifted industry focus 2.1 times. These findings portray a much more complex reality of evolution for family firms: a family may keep and hold its original core business but as time passes by a family may also choose to sell, cash-out, invest, and buy business units, and as a result manage a much more complicated portfolio of assets. As a comparative study, Heck and Trent (1999) found that 14% of a national U.S. sample of households who owned family businesses, actually owned two or more businesses and that this represented about 2% of the U.S. population overall. In the absence of a clearly guiding family firm theory on the topic, we wish to address these two issues of complexity, related to the group of family members who own a group of firms, in a longitudinal case study that can capture the evolution and dynamism of entrepreneurial behavior over time.

The Pery Family Business Case

Research Methodology

Scholars from the entrepreneurship and family firm field argue that more in-depth, qualitative research is needed to better understand how entrepreneurship in the family firm context relates to important social and economic value creation (Anderson et al., 2005; Litz et al., 2012). Although there is no accepted “boilerplate” for writing up qualitative methods (Pratt, 2009), we follow an inductive process in building theories from case studies as recommended by Eisenhardt (1989). Qualitative research can provide the basis for understanding the social processes that underlie management and memorable examples of important management issues in order to build theory (Gephart, 2004). Pery 1 is a large publicly listed and multigenerational family firm operating mainly in the food industry. This family firm was selected for our investigation as a highly illustrative case that lends itself as a qualitative study of “phenomena in the environments in which they naturally occur” and as description of “the actual human interactions, meanings, and processes that constitute real-life organizational settings” (Eisenhardt & Graebner, 2007, p. 25). In addition, the analysis of descriptive longitudinal data allows us to illustrate how a phenomenon changes over time (Ployhart & Vandenberg, 2010, p. 99). While operating over three generations and 75 years, Pery has founded several new businesses, sold parts of the business units, bought companies, and conducted one of the biggest inter-units mergers in the country.

Data Collection and Analysis

The Pery case describes how entrepreneurial behavior over time occurs in a family context. Having access to the family level of analysis is difficult, as noted by family researchers:

Records kept by individuals and private organizations are not usually part of the public record and are not generally kept continuously or over long periods of time. However, they may still represent a valuable source of research materials for the researcher who can gain access to them. (Greenstein & Davis, 2013, pp. 96-97)

A similar difficulty is expressed by entrepreneurship and family business researchers (e.g., Brockhaus, 1994). Following Yin’s (2009) case study approach, we analyze the Pery family in business by carrying out a triangulation of different sources of data. Our data are collected from various sources, including company website, press articles, massive media coverage, external and internal company and family documents (i.e., family’s private history book), and interviews. 2 Content analysis of texts tends to avoid recall biases and is a highly utilized means of obtaining otherwise unavailable information (e.g., Kabanoff, Waldersee, & Cohen, 1995; Short, Payne, Brigham, Lumpkin, & Broberg, 2009). Since we want to shed light on the possible antecedents of entrepreneurial behavior at the family level of analysis, the content analysis of text offers considerable potential in gaining key insights into the thinking of top decision makers and in “following the choices they make” (Short et al., 2009, p. 15). Data triangulation makes it possible to acquire a wider perspective of the development of the family business portfolio over time and to highlight the family role. The evolution of the business and family systems over a period of 75 years from 1936 to 2011 as well as of the environment implied a series of strategic, financial, and family challenges, which were essential in determining the path of development of the family business portfolio.

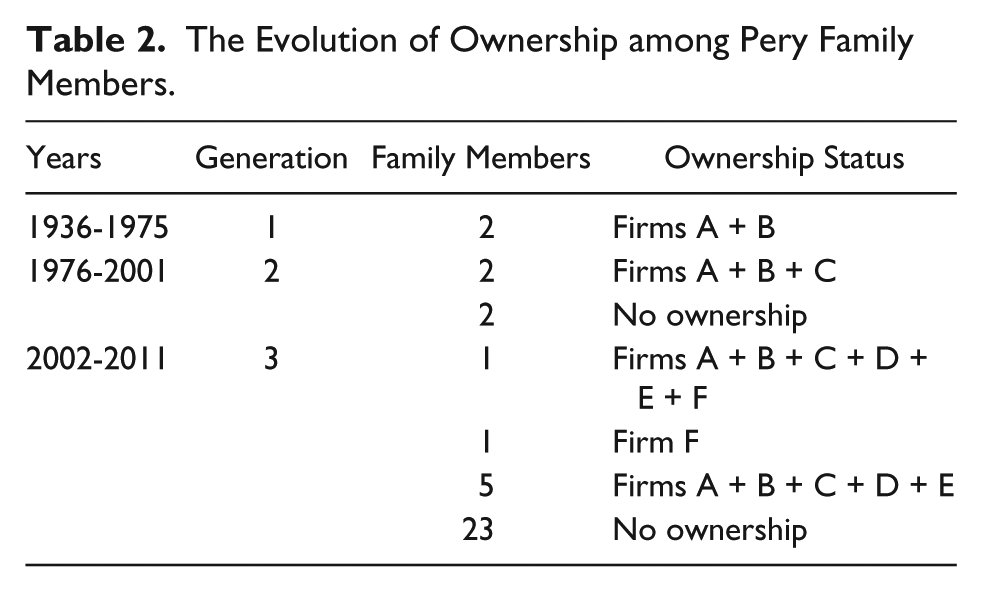

Established in 1936, Pery became the second-largest food and beverage company in its country of origin. It is currently an international corporation with approximately 13,500 employees operating in 25 production sites in 21 countries around the world. The family in business is at the third-generation’s stage. In order to look at the entrepreneurial behavior and its antecedents over time, we listed the main changes that occurred in the family and business over 75 years. We documented the major family-related events, such as marriages and divorces, entries to and exits of family members from the business, showing whether they coincide or not with business-related events, such as venture creation or divestments (Table 1) as well as the subsequent family ownership evolution (Table 2).

The Family and Business Events Chart.

The Evolution of Ownership among Pery Family Members.

In line with Harvey and Evans (1994), we agree that the “organizational change is a multidimensional construct that needs to be carefully defined to ensure that the constructs of this complex issue are fully delineated” (p. 333). We suggest identifying the changes as all attempts that have modified the structure of the family business as it was progressing from one stage of development to another. Each event of change was documented along with the relevant written testimonies provided by family members in the family’s history book, in the official family firm website and/or descriptions in business newspapers. The main events refer to changes in the business level, including founding firms, buying, selling, or merging firms, as well as ownership and management changes. Based on the collected data, we specify whether the event of change was originated within the family or the business systems. Following the recommendation of Pratt (2008), we present data both in the body of the article and in the tables in the form of “power quotes” and “proof quotes.”

For example, the following text was coded as a business reason for the family to buy back the shares of the Boro Dairy Pery (Firm A): “[O]ne fine day Famous Star sent a message saying it wanted to dissolve our partnership due to pressure from foreign customers boycotting products from USA . . . The termination of the agreement was signed . . . Pery later sold back its shares under better conditions”. The reason for this transaction to buy back 28% of Firm A’s shares stemmed out of the political environment of the businesses, thus was coded as a firm-level antecedent. Another event of change, the decision to buy a salad firm and to merge it into Firm A, was initiated by the family while thinking about the risk in the existing firm. The family was the source for this business decision based on its wish to divide the risks between several industries as documented in their private history book: “The thinking behind this decision was the fact that a potential sum of money has been accumulated, which had to be invested and made use of.

“In order not to leave all our eggs in one basket,” says Peter, in the spirit of strategic thinking, it was decided to enter the field of products which are not to be found on the refrigerator shelf. The decision was to enter a field which was still underdeveloped, from an industrial point of view—salads and frozen goods.

For the theory to gradually emerge, we need to go beyond the process of coding and classifying data into concepts by making the connections between these concepts clear (Dey, 2003), as will be exposed in the upcoming section.

Findings and Propositions

Given the accounts of events in Pery’s both family and business systems, we identified 25 events of change between 1936 and 2011. These events happened within 75 years and among three generations. The essence of the findings from the Pery family business data analysis is presented in Table 3, Section A.

Entrepreneurial Behavior in the Pery Family Business (Section A) Illustrated by the Cluster Model (Section B a ).

Red = family; green = core business; blue = peripheral business.

Based on the analysis of the data, we make several observations revolving around (a) the prevalence of the family elicitors in entrepreneurial behavior over time, (b) the necessary distinction between organic and portfolio firms, (c) and between core and peripheral businesses. These observations are translated into propositions and confronted with existing literatures.

Antecedents of Entrepreneurial Behavior

Adding the family level of analysis when looking at entrepreneurial processes opens the possibility to track the antecedents of entrepreneurial decisions in a wider perspective. When previous research has analyzed entrepreneurship in family firms mainly within the context of the firm, this has led not only to a partial picture but also to an implicit assumption that entrepreneurial decisions stem out of the business and its environment solely. Looking at both systems of family and firm, we tried to understand the antecedents of each of the 25 events of change identified. Thus, each entrepreneurial event could be the result of antecedents that come from the family or from the firm.

We defined the family as the antecedent of an event of change when the family needs were the major drivers of the decision and/or when the testimonials clearly pointed into this direction. Therefore, we considered, for example, that divesting the family risks or helping a friend are family-driven decisions whereas purchasing other firms in the same industry as an initiative of the board of directors in response to the competitive environment are business-driven decisions. Most of the events were clearly identified as family- based or business-based. Some events, however, were not easily identified as such because the boundaries between the two systems were not clear. The difficulty to pinpoint some of the events as to their origin is part of the diffused boundaries between the family and business systems (e.g., Zody et al., 2006). Since the family holds major positions in the board of directors and management, even decisions that originate in these forums are not always pure business decisions. In addition, the proposals relative to business opportunities were submitted to the owning family who had to consider them and take action. To cite but one example that illustrates this practice, one family member observed, “You don’t look for opportunities, but you grab them when they come along”. Even when opportunities rise in the business environment, it is the family’s responsibility to “grab them” and materialize them into business events. We chose to rely on the information disclosed, that is to consider an event as being business driven when the existing accounts relating to the business origin of the decision are predominantly salient and when the accounts on the family origin of the decision are rather insignificant and vice versa. The logic behind determining the source of each instigated change (family or business) is summarized in Table 4.

Antecedents of Entrepreneurial Behavior in the Pery Family.

More events were defined as stemming out of the family (60%) than the business (40%). Therefore, not to include the family level of analysis along with the firm level when looking at entrepreneurial behavior in family firms seems to lead to an extremely biased and partial description of the phenomena. The evolution of the Pery family firm illustrates how the owning family pursued entrepreneurial activities by responding to changes in the environment (such as business opportunities) and in the family (such as succession challenges) to maintain the continuity of the family business system. Bennedsen, Nielsen, Perez-Gonzalez, and Wolfenzon (2007) already point at a family event as a source for a strategic decision by studying the influence of the gender of a departing CEO’s firstborn child, as male first-child firms are more likely to pass on control to a family CEO than are female first-child firms. Recent research also suggests that antecedents of entrepreneurial behavior may stem out of family reasoning since the formation of new family firms is triggered by succession crises and the growing need to find positions for the extended family members (Cruz, Justo, & Gomez-Mejia, 2011; Discua-Cruz et al., 2013). The full discussion of the criteria for determining the exact source for an entrepreneurial behavior in the family or business systems along with the possible difficulties to reach clear decisions when the antecedents rise in both systems is beyond the scope of this study. Nevertheless, we point here at the two systems as different sources. Given these considerations, we suggest the following proposition:

Organic Versus Portfolio Family Firms

The Pery family starts at the first generation with Firm A, which could be described by the two- and three-circle models (Gersick et al., 1997; Tagiuri & Davis, 1996) that represent the basic structure of a family and a firm. However, our analysis shows that the evolution over time is more complex, and therefore neither well- represented nor captured in these models. In later stages, the Pery structure of a family and a firm evolves into a portfolio of assets described as Firm B and Firm C. Then, it progressively evolves into other firms with the subsequent generations, such as Firms D, E, and F. To better capture the evolution of these business systems around the family system, we need to go beyond the structure of the two- and three-circle models by introducing a new analogy that we will term clusters. The cluster analogy refers to the multiple business entities owned by the family and to the central part played by the family in organizing the various business activities “around” it. The figures represented in Table 3, Section B allow us to convey a more exhaustive picture of the Pery family evolution by drawing these clusters.

For more clarity, we also need to introduce a distinction between organic and portfolio firms (Schneider, 2010) that translates into different types of entrepreneurial behaviors in family firms. When a family holds a firm, we term it as organic; when a family owns more than one firm, it is a portfolio family firm. The first firm added to the family business in the Pery case is the ice cream factory. The move to establishUnpublished manuscript this new business is explained by the story of Elsa Pery, reading a book describing American dairies that gave her the idea for expanding the summer activities. According to our interviews, the ice cream factory is built in another city, not very far from the dairy. The local government at the time had subsidies for dairy products and not for ice cream. This was one of the reasons to separate the new initiative into a new sister company.

Discua-Cruz et al. (2013) find that the formation of portfolio family firms is triggered also by succession crises and expanding families that necessitated providing more opportunities. As a family business matures, it is most likely to build portfolios of related businesses with the extended family filling key positions (Cruz et al., 2011). In the Pery case, the first firm to be added to the core business was in order for Elsa Pery to carry out her vision of Ice Cream. Creation of new businesses in established firms are also often aimed at finding suitable positions for as many family members as possible by launching new ventures or divisions in the business (Miller, Steier, & Le Breton-Miller, 2003). The full range of reasons to develop from one firm into a portfolio of firms should be part of future studies. Nevertheless, these considerations lead to our second proposition:

Core Versus Peripheral Businesses

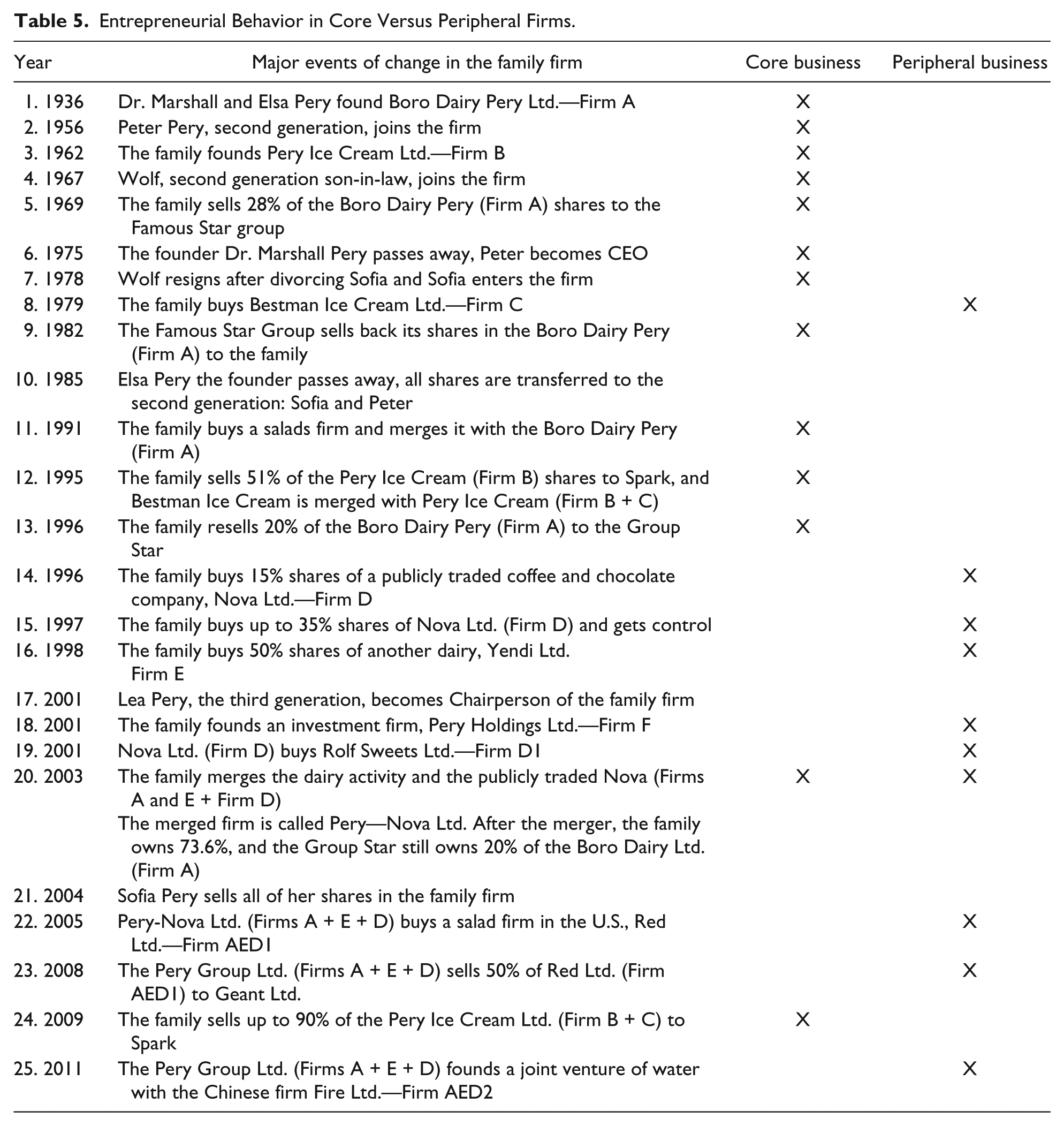

A portfolio of firms, as described in the previous section, is made of several businesses. When a family owns more than one firm, there could be obvious differences between these companies, such as age and size. Looking at possible differences among a portfolio of non-family firms, Kotler and Keller (2009, p. 179) define a firm as a core business when it functions as “the primary area or activity that a company was founded on or focuses on in its business operations.” This definition is based on primacy and the initial founding time as definers. Applying this definition to family firms suggests that a core business is the primary activity a family firm is founded on in the first generation. In our case of the Pery family, the core businesses are the dairy and ice cream firms, Firms A and B. The other firms founded or added at later generations are therefore peripheral businesses. We mark the core firms in a green color in Table 3 and the peripheral firms in blue. As can be noticed, the current activity after eight decades includes mainly peripheral firms. The identification of entrepreneurial events as involving core or peripheral firms is summed up in Table 5.

Entrepreneurial Behavior in Core Versus Peripheral Firms.

The Pery family considered coffee and salads as different business activities than the core dairy firm. This may be an issue of definitions and perceptions as for an outsider, these activities may be viewed as close activities within the food industry. The case study shows how the family considers each entrepreneurial creation of a new firm by referring to the first historical dairy. The distinction between core and peripheral firms owned by one family may shed more light on the research area that looks at the unique bond of families to their firms. The attachment between a family and its core business may be stronger than other peripheral businesses. When scholars try to explain the special relationship between owners and family firms, one multidimensional construct currently prevails: socioemotional wealth (Gomez-Mejia et al., 2011; Gomez-Mejia, Haynes, Nunez-Nickel, Jacobson, & Moyano-Fuentes, 2007). Among its dimensions, the family members’ identification with the firm is particularly relevant in the Pery case. This dimension addresses the close identification of the family with the firm and its emotional underpinnings, suggesting that the family business may have a great deal of personal meaning for family members, who may feel a strong sense of belonging to the business, especially when it holds the family’s name (Berrone, Cruz, & Gomez-Mejia, 2012). Although this dimension of socioemotional wealth refers to the oversimplified one-family-one-firm descriptions of a family firm, it can be extended to account for the more complex reality that is uncovered in the Pery case. Owning multiple firms and having multiple family members allows for a more nuanced and refined description of the special relationship between family firm owners and their firm or firms.

The following examples from the Pery case can demonstrate different levels of socioemotional wealth when it comes to the dimension of identification of family members with the firm. In the Pery case, the first firm identified as a peripheral business is the one following the purchase of Bestman Ice Cream Ltd. Firm C in 1979, few years after the death of the founder Dr. Marshall Pery, and few years before the death of his wife, Elsa. The younger generation decided to buy another ice cream factory, which we define as a peripheral firm compared with the primary two firms founded by the first generation. As reported by the former CFO who describes the event, Elsa Pery had difficulties to adjust emotionally:

When we decided to buy Bestman Ice Cream we had a very big task of how to persuade Mrs. Pery. We knew that this was an obstacle . . . Because it was a big step, a step that would risk Pery to a certain degree. Pery firm was relatively small then . . . It was risky and I also think that older people look more at the risk and maybe less at the opportunity . . . And (after the purchase) for Mrs. Pery it was always “them” and “us”, and I would tell her, “It’s also us, it’s the same pocket” and she would say “Yes, I understand, but” . . . I think that logically the brain would understand, she was aware of it, she was a business woman, but the heart never accepted it, I think.

Later, when Peter Pery himself became older and the family sold part of the core Pery Ice Cream, the duality of older versus younger family members dealing differently with different firms, and the special emotions attached to a core business repeated themselves. The following analysis is made by a financial reporter referring to the Pery’s sale of up to 90% of the Pery Ice Cream Ltd. (Firm B + C) to Spark:

Peter Pery has nostalgic feelings toward Pery Ice Cream because he finds it hard to forget the sights of his mother preparing ice cream with a manual machine and selling this strawberry ice cream from her home balcony . . . Lea Pery and Eddy Vigodman (the current CEO) have long forgotten those historic days and their new management style includes international thinking and rational strategies. Their connection to the past is weaker than Peter Pery’s.

In this example, Peter Pery is seen as having a greater emotional bond to the core firm established by his mother than toward other later firms. The citation also refers to different levels of emotional ties that are supposed to be attached to the original core Firm B by the third generation (Lea Pery) compared with the second generation (Peter Pery). These differences demonstrate our examination of different group members who refer differently to various units in a group of firms. The core business of ice cream is treated differently than other peripheral firms considering the socioemotional wealth logic attached to it in terms of family identification, notwithstanding that members from different generations may vary in their behavior. Zellweger et al. (2012) find in their study that the core company on average makes up roughly three quarter of total sales of the family-owned business activity. This highlights another perspective on the core business as the main supplier of stability and cash for the portfolio, which could also be part of the socioemotional wealth considerations of the family. Based on these ideas, the following propositions are suggested:

Another phenomenon that could be studied in this focus is the conflicted evidence about entrepreneurial behavior in family firms: some scholars stress the strong entrepreneurial characteristics of this type of businesses (e.g., Astrachan, Zahra, & Sharma, 2003) while others argue that the family firm context can be a distinct liability for entrepreneurial behavior (e.g., Schulze, Lubatkin, Dino, & Buchholtz, 2001). This conflict is summed up by the argument that “perhaps the greatest concern is that in order to protect the firm over the long run, family leaders may become too strategically conservative, thereby minimizing entrepreneurial behaviors” (Kellermanns et al., 2008, p. 2). The following example from the case study echoes Kellermanns et al.’s (2008) thought. The Pery family decides to buy up to 35% shares of Nova Ltd. (Firm D), which later led to the merger between Nova and the historic core business of Pery Dairy. This entrepreneurial move, transferring the family firm to the next generation, almost did not happen, because Peter Pery was already close to retirement, as he recalls,

“I was sure that this was the end of the road for us in Nova,” says Peter, “I said to Sofia and Lea. We’ll go home, take a vacation and try to calm down after the affair.” To his great surprise, Peter found himself in the minority. “Sofia, Lea and the advisors all said we should buy Nova, that it was an opportunity we should not let ourselves miss. I was most surprised . . . Peter found himself in the minority even against his own grandchildren.” . . “and my indecision was not easy. I understood that from a strategic point of view, this was a great opportunity. I asked myself what I would be telling myself five years from now. Was it right to oppose such a good opportunity for purely selfish reasons, a desire for peace and quiet? Should Pery give up such a good opportunity just because I did not want to burden myself too much? In the end, I came to the conclusion that since my sister, the children and the managers all support the purchase of Nova, I would support them and go with them on the long journey, which, as far as I am concerned, is another postponement of my retirement from Pery”. This conservative and protective concern could be more related to a core business within a portfolio (like the Pery Ice Cream) or to an organic family firm than to a new initiative that is carried out in a new firm within a portfolio (like the Nova company), which leads to the following propositions:

Following up with our inductive approach, the last step consists of raising the theoretical level and sharpening the constructs that were derived from our data analysis (Eisenhardt, 1989). As noted by Shepherd and Sutcliffe (2011), a bottom-up approach requires the comparison of the emerging theory with existing theories published in the literature to determine and delineate its contributions.

The Cluster Model as a Necessary Theoretical Extension

The Family and Business Antecedents of Entrepreneurial Behavior

The currently accepted models of family firms, viewed under the label of paradigm in Kuhnian terms, do not provide an exhaustive picture of family entrepreneurship (Moores, 2009; Tagiuri & Davis, 1996). Our findings derived from the Pery case echo some literature acknowledging that the family system and its vast resources, including its intangible resources, such as human capital and social capital, are ignored for the most part when studying the formation of the family firm and its continuity over time (Danes, Stafford, Haynes, & Amarapurker, 2009; Heck, 1998; Rogoff & Heck, 2003; Zachary, 2011; Zachary et al., 2013).

The three-circle model is in fact an oversimplification of the family firm considered as consisting only of a single business entity. While this could be mainly true at the first stage, at later stages a family firm can control a portfolio of multiple firms (Habbershon et al., 2010; Habbershon & Pistrui, 2002; Sieger et al., 2011; Zellweger et al., 2012). Building on the description of our qualitative longitudinal case study, we propose the cluster model (Figure 1) as a theoretical attempt to convey a more exhaustive, dynamic, and realistic view of the family business entrepreneurial behavior over time.

The cluster model: An illustration based on the Pery family business case.

We posit the cluster model as an extension for the three-circle model as well as a major enhancement of the two-circle model in which the fundamental building blocks are the family system and business system. Using the three-circle model, many scholars addressed the type of relationships between the systems (e.g., Carlock & Ward, 2001; Davis & Stern, 1988; Lansberg, 1983; Weigel & Ballard-Reish, 1997) without acknowledging the need to go beyond the singular count of the circles by describing a family that may own more than one firm. The cluster model better describes an owning family that holds more than one firm. This description graphically demonstrates the implications of the different constructs that have been suggested at the family level to capture transgenerational survival. These constructs (e.g., transgenerational wealth, transgenerational family effect, family entrepreneurial orientation) raise the understanding of how family businesses employ financial assets to create business continuity (Pistrui, Murphy, & Deprez-Sims, 2010). According to the cluster model, a family starts at the first generation with Firm A. In later stages, this basic structure of a family and a firm may evolve into a portfolio of assets, described in Figure 1 as Firm B and Firm C.

Evidence of Organic Versus Portfolio Family Firms

The Cluster Model also responds to the calls that claim that family businesses do not represent a monolithic group in terms of organizational and behavioral characteristics (Chua, Chrisman, Steier, & Rau, 2012; Corbetta & Salvato, 2004; Sharma, Chrisman, & Chua, 1997). Several typologies of family businesses have been suggested, the most commonly used are based on the criteria of life cycle, recognizing different ownership structures, stages of business growth, and family experiences in the business (Gersick et al., 1997). We contribute to the typology efforts by characterizing family firms using the cluster model and the way by which these firms manage their assets entrepreneurially. Building on the organic and portfolio terminologies, we suggest that family firms can be characterized by the number of firms they hold and distinguished as such when it comes to the study of their entrepreneurial behavior: a family that owns a firm would be referred to as “organic” as compared with a family that owns several firms referred to as “portfolio” family firm. The Pery case shows how the two-circle model describes the first stage of founding the family firm, when indeed one family owns one firm. The family has a simple structure at this grounding point, of only one couple. They both own one firm, a dairy, for the first 26 years of the family firm. Then, this couple decides to found another business, an ice cream factory, thereby moving the family to the next stage of owning two firms. In later years and generations, the family has grown as more members are born and children marry, but also the firms have grown into a portfolio of businesses. This portfolio includes six different businesses at the current point in time. The family’s entrepreneurial behavior is therefore described by the cluster model: a family that acts entrepreneurially by founding, selling, merging, and buying several firms.

Our distinction between an organic or portfolio family firm complies with previous suggestions: Habbershon and Pistrui’s (2002) maintain that the “family-in-business” mindset differs from a “family-as-investor.” The first includes a particular business that is the focus of managerial efforts that leads a family “to think of itself as a particular type of a family (a “brewery family” or a “manufacturing family”), which in turn locks it into path-dependent corporate strategies and family traditions that dictate its capital asset strategies” (Habbershon & Pistrui, 2002, p. 231). This mindset of one family and one circle of firm may describe initial stages during the first generation and the founder’s era. But this mindset may also describe family firms at later stages and among generations, such as Zildjian in the United States and Kikkoman in Japan, where the family mainly owns one firm over generations. In Habbershon and Pistrui’s (2002) terminology, these families would be called the “music percussion family” and the “soy family,” respectfully. We termed this type an organic family firm.

The second mindset described by Habbershon and Pistrui (2002) is the family-as-investor type, when a family is committed to wealth creation pursuing capital allocation strategies and structures that are responsive to the market. This mindset leads family members “to be stewards of their resources and capabilities and not necessarily of a particular business entity or legacy asset” (Habbershon & Pistrui, 2002, p. 231). When a family owns more than one firm, we term this type a portfolio family firm. An example for this type is the Haniel family firm, which is more than 250 years old and operates in 50 countries. This family spun off several firms during its history and has changed industries of operation: from trading to industry, then mining and shipping, and today consumer goods and pharmaceuticals (Haniel, 2008). When a next generation leader has changed the business focus for the first time after 50 years of the family firm’s existence, “this was the most important step that the Haniels had ventured up to that time—the merchants had turned into industrialists” (Haniel, 2008, p. 8). This shift between firms and industries would happen several times in later generations and keep this family of more than 600 members as private owners of a large group of international firms.

The Delineation of Core Versus Peripheral Businesses

Our distinction between a core business that is the central activity during the first generation and other peripheral businesses that evolve later is a theoretic extension to define the differences in the importance and centrality of firms within a portfolio. Changing the core business is a major step for a family firm. Having a portfolio of firms with various definitions of centrality and emotional ties attached to them opens new ways of understanding the complexity of entrepreneurial behavior among generations. The evolution of a family firm can thus be summed up as follows: the firm starts as a bivalent “one family–one firm” in the first generation. While some family firms keep this form into later generations as organic family firms, others may evolve into a cluster structure of “one family holding more than one firm,” with multiple firms that may include the original core one but not necessarily so. This structure of portfolio family firms describes the changes over time in later generations. As in the Pery case, the major events become centered on the peripheral business and less around the core business (Table 5). It is interesting that this shift somewhat coincides with the simultaneous shift from family to business antecedents (Table 4). This observation may be connected to family members who feel that the current firm is “less a family business today,” a view shared by a reporter and Sofia Pery in a recent interview:

Sofia left the Pery family firm founded by her parents after “slamming the door behind her,” about 8 years ago, because she was against the merger initiated by her niece, Lea Pery. Senior Sofia wanted to keep the traditional and familial character of “Pery” and opposed to make it into a public firm, but she has lost the battle to the third generation current leader of the dynasty. “Looking back, did you make a mistake by insisting that Pery should stay a family firm?” asked the reporter. Sofia answers: “To become a publicly traded firm is the way to grow, I knew it already then. But I thought that it is not the right thing for me.

Based on these considerations, the cluster model is suggested as a theoretical model that captures the complex picture of family firms and extends the simplistic description of the bivalent-circle model and the three-circle model.

Conclusions, Limitations, and Future Directions

Our study contributes to the literature in three ways. First, it reveals the critical role played by the family system in the evolution of businesses over time. By showing the entrepreneurial activity as driven by the family, it asserts that not only that the family system needs to be included, but that the analysis of the family firm among generations needs to be conducted at the family level. Therefore, adding the family’s perspective to entrepreneurial behavior over time not only better describes reality but also enriches the understanding of the family firm’s complexity (Litz, 1995). Second, the identification and analysis of the reasons that drive family entrepreneurial activity, which combine strategic planned moves, responses to environmental changes, and complying with family needs, better describe the uniqueness of the firm that is owned by a family. Third, the case study inductively introduces the cluster model as a necessary extension of the Circles Models to better capture the family-level activity and the growing complexity over generations.

The emergence of the cluster model and its myriad forms of delineations significantly change the family business research terrain. Such a conceptualization allows the presentation of multiple firms owned by the same family over time. The cluster model approach represents a new and significant conceptualization for future family business research while at the same time calls into question the oversimplicity of previous research. This study contributes in two main additional ways: by introducing necessary distinctions between “organic” versus “portfolio” family firms and between “core” and “peripheral” businesses, and by opening several new theoretic trajectories as a result. First, the cluster model develops and transforms the traditional circles models by proposing a basic typology of organic versus portfolio types of a family owning one or more firms. This change may occur as an evolution within the next generations, but it is not a necessary linear development since family firms may hold only one business and still survive through generations. When family firms hold a portfolio of firms, we introduce the necessary distinction between a core business and other peripheral businesses. These contributions apply to types of entrepreneurial families as well as to types of entrepreneurial family firms: we point out at families that own one firm compared with families that own more firms, and at firms that are sole businesses compared with firms that are part of a cluster. Second, the theoretical contribution comes from the Cluster Model’s potential to capture constructs, such as socioemotional wealth and entrepreneurial behavior, which may vary in intensity in organic firms as compared with portfolio firms and between a core business and peripheral ones. The duration within which a family holds an asset in a portfolio may also influence these constructs. The Cluster Model presented herein holds great promise as a conceptualization of rather complex family business systems. Nonetheless, limitations of the research exist and are, at a minimum, fivefold. By acknowledging them, we wish to open avenues for future research directions.

Methodological considerations: The suggested cluster model stems out of one historical case study. Further research effort is warranted to examine a broader set of observations or national contexts. Simply put, this case study approach and its findings, as an important first step, have yet to be applied and tested using more comprehensive research designs. In addition, those future explorations need to go beyond the sources of information that we relied on, which were the business as well as the family documents. The documented history available in public accounts can be biased since it focuses on individual and economic issues while ignoring the role of emotional relationships and family members who may have a central role in entrepreneurship, whereas they lie in the shadow of the key persons highlighted on the spot. In her analysis of new ventures creation, Cramton (1993) shows how the public accounts of events differ from the private accounts, hiding important underlying issues about the connection between the business and the efforts to maintain the family togetherness.

Ownership as a separate circle/system: We studied the Pery family firm from two perspectives: the family and the business/businesses. The original presentation of ownership as a separate system is expressed in the three-circle model, while the cluster model does not account for this perspective. Among the three generations of the Pery family, there is an evolution in the ownership diversity, as described in Table 2: While the first generation includes a couple that owns all firms, and thus demonstrates the overlap between ownership and family systems as theorized by scholars (Gersick et al., 1997), this overlap diminishes in the next generations. Currently, the Pery family consists of 30 members, with four different groups of ownership status: only one family member holds ownership shares in all firms while 23 members do not hold any shares. The complexity of ownership at the family level is beyond the scope of the current article but should be accounted for in future studies.

Beyond the “snapshot” view of the cluster model: A limitation of the circle model is its description of a family firm in a static way, like a snapshot taken at one point in time. The cluster model suffers from the same limitation although it is a snapshot taken at a later stage of the family firm life cycle. The two models are descriptive at one point in time, and they do not describe what happens before or after they have been taken. Nevertheless, part of the cluster model’s contribution is acknowledging that it is only a partial and incomplete picture to look at the nascent first-generation family business.

The circles as parameters of size or importance: In our description of the different entrepreneurial steps of the Pery family, we drew one circle for the family and different circles for each business entity. Obviously, not all the business units are of the same size when considering sales or number of employees. These characteristics could be described by different sizes attributed to the circles. We had a different color for the core firm to describe it in a special way in order to assess its unique importance in the cluster. 3

5.The family as a group of individuals with dynamics in play: We looked at a group of individuals that owns a group of firms. According to Martinez et al. (2011), only 7% of entrepreneurship articles include “teams” as one of their units of analysis. We show that the Pery family as a group evolves over time into a heterogeneous team regarding ownership status. Moreover, the growing complexity of the business side, manifested in multiple sales, acquisitions, foundations, and mergers of firms, is echoed by a growing complexity in the family’s structure and size. Even Table 1 cannot fully describe the full scope of complexity of second marriages and stepchildren that were not included in the table, but bring more considerations to the family’s side. The dynamics between all these individuals who make up the family group and their influence on entrepreneurship and strategic decisions should be part of future studies.

Overall, research best practices are necessitated by the cluster model view. The family system must be recognized along with the business system. Our research must model the family and the business as well as their interactions over time. No longer is the case that family business research seeks to only provide knowledge on the business. Researchers can no longer ignore or diminish the family system; instead, the research investigations must be inclusive of the family system and all its dynamics and complexities. Both the family system and business system endure and change over time with varying degrees of interdependence, resulting in a vibrant and complex configuration of the family firm over time.

Footnotes

Acknowledgements

We gratefully thank Allison Pearson and Pramodita Sharma as well as the anonymous reviewers for their helpful comments and support. We also acknowledge the support of FFI with the Award of the Best Unpublished Research Paper that was received in 2012 for an earlier version of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.