Abstract

This article examines the effects of family involvement on dividend policy in closely held firms that face agency problems involving majority–minority shareholders. We argue that minority shareholders press for dividends when they perceive situations fostering wealth expropriation. Looking at 458 Colombian companies, we find that family involvement in management does not affect dividend policy; family involvement in both ownership and control through pyramids affects dividend policy negatively; and family involvement in control through disproportionate board representation affects dividend policy positively. Thus, family influence on agency problems, and hence on dividend policy as a mitigating mechanism, varies depending on family involvement.

Introduction

The current literature on corporate governance and agency theory highlights how ownership structures affect corporate finance decisions. Ownership concentration might increase oversight of firm management and generate shared benefits of control for minority shareholders, but it might also facilitate the acquisition of private benefits of control at the expense of minority shareholders (Barclay & Holderness, 1989; McConnell & Servaes, 1990; Villalonga & Amit, 2010). Family firms are not immune to agency conflict and may exacerbate it in certain circumstances (Schulze, Lubatkin, Dino, & Buchholtz, 2001; Songini & Gnan, 2013; Uhlaner, Wright, & Huse, 2007). Moreover,

As the separation of ownership from control in widely held firms drives a wedge between the interests of principal and agent, the dispersion of ownership in family-held firms drives a wedge between the interest of those who lead a firm—and often own a controlling interest—and other family owners. (Schulze, Lubatkin, & Dino, 2003, p. 181)

Dividends can be used to mitigate several types of agency problems. Theoretical arguments by Rozeff (1982), Easterbrook (1984), and Jensen (1986) suggest that dividends reduce the free cash flow controlled by insiders, thus reducing agency conflicts between management/owners, debt-holders/shareholders, and majority/minority shareholders. A vast amount of empirical literature deals with these issues in the context of large listed firms (see Michaely & Roberts, 2012). However, little is known about how dividends alleviate agency problems in closely held family firms that face potential conflict between majority and minority shareholders.

Using a database of 458 Colombian companies spanning the 1996 to 2006 period, we examine the effects of family involvement on dividend policy in closely held firms with some level of ownership dispersion. Our main argument is that minority shareholders press for dividends, and therefore increase the likelihood of dividend payments and their level to prevent misuse of assets by insiders.

We find that family influence on these agency conflicts differs according to the type of family involvement. Our main findings can be summarized as follows: First, family involvement in management (FIM) had no statistical significance in explaining dividend policy as a mechanism for mitigating agency conflicts, which suggests that family CEOs neither alleviate nor worsen agency problems between majority and minority shareholders.

Second, family involvement in ownership (FIO) increases the likelihood of supervision over the CEO and reduces the probability of opportunistic behavior, creating shared benefits of control for minority shareholders. Furthermore, these benefits exceed other agency costs generated by ownership concentration. Consistent with this idea, we find that FIO has a significant negative effect on the firm’s dividend policy.

Third, we find that family involvement in control (FIC) through pyramidal structures affects dividend policy negatively. Although pyramids, as a control-enhancing mechanism, allow families to extract pecuniary and nonpecuniary private benefits, contestability among majority and minority shareholders within pyramids might mitigate agency problems, counterbalancing the negative effects. This is possible in our context because minority shareholders in Colombian closely held firms are generally sophisticated investors (e.g., wealthy families, equity and pension funds, international investors, and other large private firms) and is consistent with findings and arguments of Villalonga and Amit (2009). Finally, we find that FIC through disproportionate family representation on the board of directors increases the amount and likelihood of dividend payment significantly. According to Villalonga and Amit (2009), this kind of involvement could elicit the adverse effects associated with a pure control-enhancing mechanism; hence, minority shareholders try to remove free cash flow from the CEO’s ready access to avoid misuse or wealth expropriation.

This study contributes to the current empirical literature on corporate finance, governance, and family firms in several ways. It is among the few that deal with dividends as mitigating mechanisms for agency tensions between majority and minority shareholders within the context of closely held family firms. The results contribute to the growing literature on agency problems inside family firms (Block, 2012; Clarysse, Knockaert, & Lockett, 2007; Martín de Holan & Sanz, 2006; Schulze et al., 2001, Schulze et al., 2003).

Family firms are the most widespread form of organizational structure (La Porta, López de Silanes, & Shleifer, 1999). Although they have received considerable attention in the financial and management literature, most of the empirical findings are based on listed firms (Anderson & Reeb, 2003; Kowalewski, Talavera, & Stetsyuk, 2010; Sacristán-Navarro & Gómez-Ansón, 2007; Villalonga & Amit, 2006, 2009) and conclusions from these samples may not apply to closely held firms (Bettinelli, 2011). Our work contributes to a better understanding of such firms, an important but understudied subject.

Research on family firms usually views them as a single unit, ignoring the different ways families may influence corporate finance and governance decisions. This study follows the approach of Villalonga and Amit (2006, 2009) by considering family involvement in three dimensions: management, ownership, and control (pyramids and disproportionate board representation).

Even though the sample is restricted to Colombia, this context contributes to a better understanding of family firms not only in Latin America but also in other emerging markets with low investor protection, family involvement, high ownership concentration, and pyramidal structures through business groups aimed at enhancing firm control. Family firms in emerging markets are an important yet highly understudied subject, as noted in recent surveys of the state of research on corporate governance in emerging markets (Claessens & Yurtoglu, 2013; Fan, Wei, & Xu, 2011).

The remainder of this article is organized as follows: In the next section we present the theoretical framework within the agency context and develop our hypotheses. We then discuss the empirical design concerning data and methodology. Next we present the main results and robustness checks. And finally we discuss our findings and conclude.

Theoretical Framework and Hypotheses

Agency Cost and Dividends: An Overview

Dividend policy is one of the most thoroughly researched subjects in modern corporate finance. M. Miller and Modigliani (1961) show that in a world of perfect information and frictionless capital markets, dividend policy is irrelevant for a firm’s market value. However, in the real world firms operate in an environment of asymmetric information and multiple agency conflicts, and dividends play a key role. Jensen (1986) and others examine dividends as a mechanism to mitigate agency problems. In his “free cash flow problem” Jensen notes that insiders can increase their perks consumption only to the extent that the firm has sufficient free cash flow.

A number of empirical studies show that agency problems associated with free cash flow are significant in the United States and elsewhere (Denis & McConnell, 2003; Durnev, Morck, & Yeung, 2004). Higher dividend payments imply lower agency costs and improved corporate governance. Nonetheless, a country’s level of investor protection affects the relationship between dividends and agency costs. La Porta, López de Silanes, Shleifer, and Vishny (2000) suggest that legal mechanisms supporting good governance lead to high dividends.

These empirical findings are drawn from large listed firms, but little is known about the role of dividends to alleviate agency tensions in the context of closely held family firms. Clarysse et al. (2007) examine the tensions between the founders and other stakeholders in the context of closely held Belgian firms. In a review of several articles dealing with closely held family firms, Uhlaner et al. (2007, p. 232) hold that “it is too simplistic to presume that all family firms are necessarily less vulnerable to the agency principles.” Songini and Gnan (2013) highlight several conflicts of interest and agency problems within the family business context. Moreover, Schulze et al. (2003) claim that controlling owners can extract resources from the firm at the expense of nonfamily shareholders or other family factions, but this is possible only if the controlling owner has enough free cash flow on hand.

Latin American companies generally and Colombian firms in particular are a favorable context for studying the influence of family involvement on dividend policy. Low levels of investor protection and the prevalence of closely held firms affiliated with business groups make for a setting that allows examination of how minority shareholders in family firms deal with the potential agency conflicts that this type of firm generates, and how these problems affect dividend policy.

Drawing on a sample of Asian firms, Claessens, Djankov, and Lang (2000) show that the possibility of expropriation is especially high when a company is affiliated with a business group. Moreover, Faccio, Lang, and Young (2001) find expropriation of outside shareholders by the controlling shareholder to be the leading agency problem in countries with highly concentrated family ownership and control, where families almost always choose the firm’s CEO. Empirical data from Latin America show that dividends play a key role in limiting expropriation by insiders; both Garay and González (2008) and Chong and López-de-Silanes (2007) report a positive relation between good corporate governance and a high level of dividends.

The hypotheses we propose test the relation between the three dimensions of family involvement (management, ownership and control) and dividend policy, as a mitigating mechanism of majority–minority agency tension in closely held family firms.

Family Involvement in Management

In the context of the above discussion, alignment of interest favors either no dividends or lower dividends. Classical agency theory assumes that a family CEO solves agency problems and eliminates the need for dividends, and Fama and Jensen (1983) argue that family management reduces agency cost because the incentives of owners and managers are fully aligned.

De Massis, Kotlar, Campopiano, and Cassia (2013) show that increasing degrees of FIM may be expected to decrease the moral hazard associated with the incentives of managers to behave opportunistically at the expense of minority shareholders. Several researchers show that family CEOs are significantly and positively related to financial performance, which could imply less agency conflict (Anderson & Reeb, 2003; Dyer, 2006; Kowalewski et al., 2010; Villalonga & Amit, 2006). However, we cannot assume that a family manager will always act in favor of minority shareholders (whether these are other family members or nonfamily shareholders) and FIM may either reduce or increase agency problems.

Sciascia and Mazzola (2008) suggest that the positive effects linked to FIM are not strong enough to compensate for its disadvantages. Morck and Yeung (2003) state that FIM does not necessarily mitigate agency problems and that families may indeed extract private benefits at the expense of minority shareholders (Sacristán-Navarro, Gómez-Ansón, & Cabeza-García, 2011) leading to managerial entrenchment (Demsetz, 1983). Morck, Shleifer, and Vishny (1988) assert that CEOs can achieve considerable entrenchment by belonging to the founding family.

Schulze et al. (2003) argue that a sense of entitlement among founding family members can encourage a family CEO to use the firm’s resources to provide family members with employment, perquisites, and privileges they would not otherwise receive. Accordingly, the presence of noneconomic preferences creates potentially serious agency problems in family firms. Even though both family and nonfamily minority shareholders share common economic interests in profitability, growth, and market share, there is no reason to believe they share noneconomic preferences (Schulze et al., 2001). Lee and Rogoff (1996) and Bertrand and Schoar (2006) argue that the goals of family firms may include such nonfinancial interests as family independence, satisfaction, nepotism, and family legacy, among others. Burkart, Panunzi, and Shleifer (2003) note that family CEOs, in contrast to nonfamily CEOs, perceive intangible benefits from their position as firm managers.

Zwiebel (1996) shows that dividend policy may be viewed as the optimal response of partially entrenched managers. Such managers might lower their empire-building ambitions to prevent control challenges. Although privately held family firms can be free from the discipline imposed by the corporate market, they increase the agency threat posed by “self-control” (Jensen, 1998); hence, a control challenge could stem from minority shareholders, including other family factions. Hu and Kumar (2004) find the likelihood of dividend payments, and their amount, is significantly and positively related to factors that increase CEO entrenchment.

Considering the above arguments, we assume that a partially entrenched family CEO derives both monetary and nonmonetary benefits and that given the majority-minority shareholder agency tension, minority shareholders (whether other family members or nonfamily shareholders) will press for more dividends. Accordingly, we put forward the following hypothesis:

Family Involvement in Ownership

Next, we discuss the relationship between FIO and dividend policy when the family firm has minority shareholders. Agency theory suggests that concentrated ownership could be a strong governance mechanism. Indeed, the concentrated nature of family ownership, the usually undiversified equity holdings, and control of management should lower agency costs (Fama & Jensen, 1983; Jensen & Meckling, 1976). Shleifer and Vishny (1986) state that large shareholders have enough wealth invested in a firm to compensate for the cost of monitoring the CEO. In short, controlling shareholders have both the ability and the monetary incentive to supervise managers and mitigate agency costs (De Massis et al., 2013; Demsetz & Lehn, 1985; Shleifer & Vishny, 1997). A controlling family can remove managers who do not follow a value-maximizing strategy (Bjuggren & Palmberg, 2010). Both Villalonga and Amit (2006) and Sciascia and Mazzola (2008) found that FIO has a positive effect on firm performance, and hence on firm value. Because of the lower agency costs with ownership concentration, having no dividends or lower dividends should be acceptable to minority shareholders.

However, there are also arguments that FIO could give rise to agency conflicts. For example, Sacristán-Navarro et al. (2011) posit that conflicts of interest between shareholders may appear when families protect their own interests as owners. Conflicts of interest could arise even between family shareholders in different roles, fostering misunderstanding among majority and minority shareholders (Boles, 1996; E. J. Miller & Rice, 1988; Swartz, 1989). Additionally, Morck et al. (1988) argue that agency costs that bear minority shareholders could increase with an entrenched dominant shareholder. In the framework of our discussion, this could motivate minority shareholders to press for more dividends to mitigate agency problems.

In sum, FIO may mitigate agency conflicts attributable to managerial misbehavior and, at the same time, may accentuate agency conflicts among shareholders. The context determines whether the net effect is positive or negative for minority shareholders. Kowalewski et al. (2010), among others, argue that concentrated ownership may be effective in solving agency problems in countries with weak corporate governance institutions because of its potential to lower monitoring costs.

Like other Latin American and emerging countries, Colombia ranks low in terms of corporate governance. For example, according to the revised anti-director right index reported by Djankov, La Porta, Lopez-de-Silanes, and Shleifer (2008), it scores 3 points out of a maximum of 5. This measurement is close to the average for countries of French legal origin but below the average for common law countries. In emerging markets one should expect the presence of a majority shareholder to increase the likelihood of supervision over the CEO and reduce the probability of opportunistic behavior, whether the CEO is a family member or not, creating shared benefits of control for minority shareholders that exceed other agency costs generated by ownership concentration. In this context, dividend policy should not play a crucial role in controlling agency problems associated with the CEO. Hence, we propose the following hypothesis:

Family Involvement in Control

FIC happens when families use various control-enhancing mechanisms that enable a family’s voting rights to exceed its cash flow rights. These structures include multiple share classes, pyramids, cross-holdings, voting agreements, and disproportionate board representation (Villalonga & Amit, 2006, 2009). The following hypotheses concern the two most common control-enhancing mechanisms used in Colombia: pyramidal family control and disproportionate board representation. Several studies (Sacristán-Navarro & Gómez-Ansón, 2007; Villalonga & Amit, 2009) note that these mechanisms are often used in family firms, but we currently do not know what their effect is on the dividend policy of private family firms with minority shareholders.

Pyramids allow shareholders to control a firm through one or more intermediate firms they do not fully own. Pyramids organized to exercise controlling power that exceeds cash flow rights are not uncommon in family firms (Almeida & Wolfenzon, 2006; Claessens, Djankov, Fan, & Lang, 2002; La Porta et al., 1999; La Porta et al., 2000; Sacristán-Navarro & Gómez-Ansón, 2007). They allow families to extract pecuniary and nonpecuniary private benefits, such as high compensation, related-party transactions, empire building, social status and societal power, recognition as successful entrepreneurs, and appointment of family members to management positions (Bjuggren & Palmberg, 2010; Dyck & Zingales, 2004). Several studies summarized by Morck, Wolfenzon, and Yeung (2005) illustrate governance problems within pyramidal business groups. If pyramids exacerbate conflicts between majority and minority shareholders, as stated in Bebchuk, Kraakman, and Triantis (2000), then minority shareholders should press for more dividends to mitigate wealth expropriation.

Almeida and Wolfenzon (2006) and Villalonga and Amit (2009), among others, argue that pyramids can serve purposes other than pure control enhancement; hence, their net effect on value may not always be negative. For example,

Privately held intermediate entities in pyramids may also serve as investment vehicles for sophisticated investors like private equity funds, pension funds, and other institutional investors. Such investors may play a monitoring role with respect to the founding family and, unlike retail investors in publicly traded corporations, are vigilant in preventing tunneling. (Villalonga & Amit, 2009, pp. 3050-3051)

Other large shareholders in pyramids may mitigate wealth expropriation by monitoring managers and moderating family influence (Maury & Pajuste, 2005). In Spain, where pyramidal family structures are prevalent, the existence of an additional significant shareholder can counterbalance the potential extraction of private benefits (Sacristán-Navarro, et al., 2011).

This positive argument may apply to private family firms in Colombia, where minority shareholders are indeed generally more sophisticated and unlike ordinary “retail investors,” they represent other wealthy families, equity and pension funds, international investors and other large private firms. In sum, this positive effect of contestability among majority and minority shareholders within pyramids will likely mitigate agency problems so that dividend policy need not play so crucial a role. Therefore, if tunneling has a negative effect while potential blockholder contestability has a positive effect on agency costs, considering our context, the net expected result can be stated in the following hypothesis:

A final hypothesis concerns the impact on dividend policy of disproportionate family representation on the board of directors. Considerable theoretical and empirical evidence drawn from the economics and finance literature posits that free cash flow not paid to shareholders may be diverted by insiders (Hart & Moore, 1974; Gomes, 2000; Jensen, 1986; Myers, 2000; Zwiebel, 1996). Hence, minority shareholders should press for more dividends. We argue that this tension is present in closely held family firms.

Potential benefits of family board representation include a long-term perspective or longer investment horizon, less managerial myopia, and better management supervision (Fama & Jensen, 1983; James, 1999; Stein, 1988, 1989; Sciascia & Mazzola, 2008). Family representation can also generate shared benefits and mitigate agency conflicts with minority shareholders by establishing long-term relationships with customers, suppliers, and capital providers (Anderson, Mansi, & Reeb, 2003; Sacristán-Navarro et al., 2011). However, a disproportionate representation (i.e., when the percentage of family members on the board exceeds their cash flow rights) could elicit the adverse effects associated with a pure control-enhancing mechanism.

Villalonga and Amit (2009, p. 3054) state, “This can be an important form of corporate control because, by having the right to elect a large fraction of the board, families can control the firm’s management, strategic direction, and voting agenda.” This could be especially important when financial and nonfinancial goals are in conflict and family objectives are in conflict with business objectives (Sciascia & Mazzola, 2008).

As Sacristán-Navarro et al. (2011) argue, families that control the board may extract private benefits at the expense of minority shareholders. Consistent with this point, Filatotchev, Lien, and Piesse (2005) found a negative relationship between the percentage of directors linked to a family and a number of measures of profitability and firm value. In line with the classical view of dividends’ role in mitigating agency problems (Jensen, 1986), we expect minority shareholders to try to remove free cash flow from the CEO to avoid misuse. These arguments support the following hypothesis:

Method

Description of the Database

Our sample is based on a unique data set that combines firm-level information for closely held companies affiliated with business groups, a feature not commonly found in current research on corporate finance, governance, or family firms. Financial, ownership, and board-related information are drawn largely from two Colombian government agencies, the Financial Superintendence (Superintendencia Financiera, SFIN) and the Superintendence for Commercial Societies (Superintendencia de Sociedades, SSOC).

SFIN is the financial regulator for all security issuers of stocks and bonds; SSOC supervises and monitors corporate restructuring and bankruptcy processes. Additionally, SSOC maintains financial records and notes for medium-sized and large privately owned firms. Notes to financial statements are subject to statistical confidentiality and include 16 appendices per company, sometimes listing major shareholders, appointments to the board, the CEO, auditing firms, and parent–subsidiary commercial relations. We drew additional information relating to directorships and CEOs from the Chambers of Commerce where companies are registered.

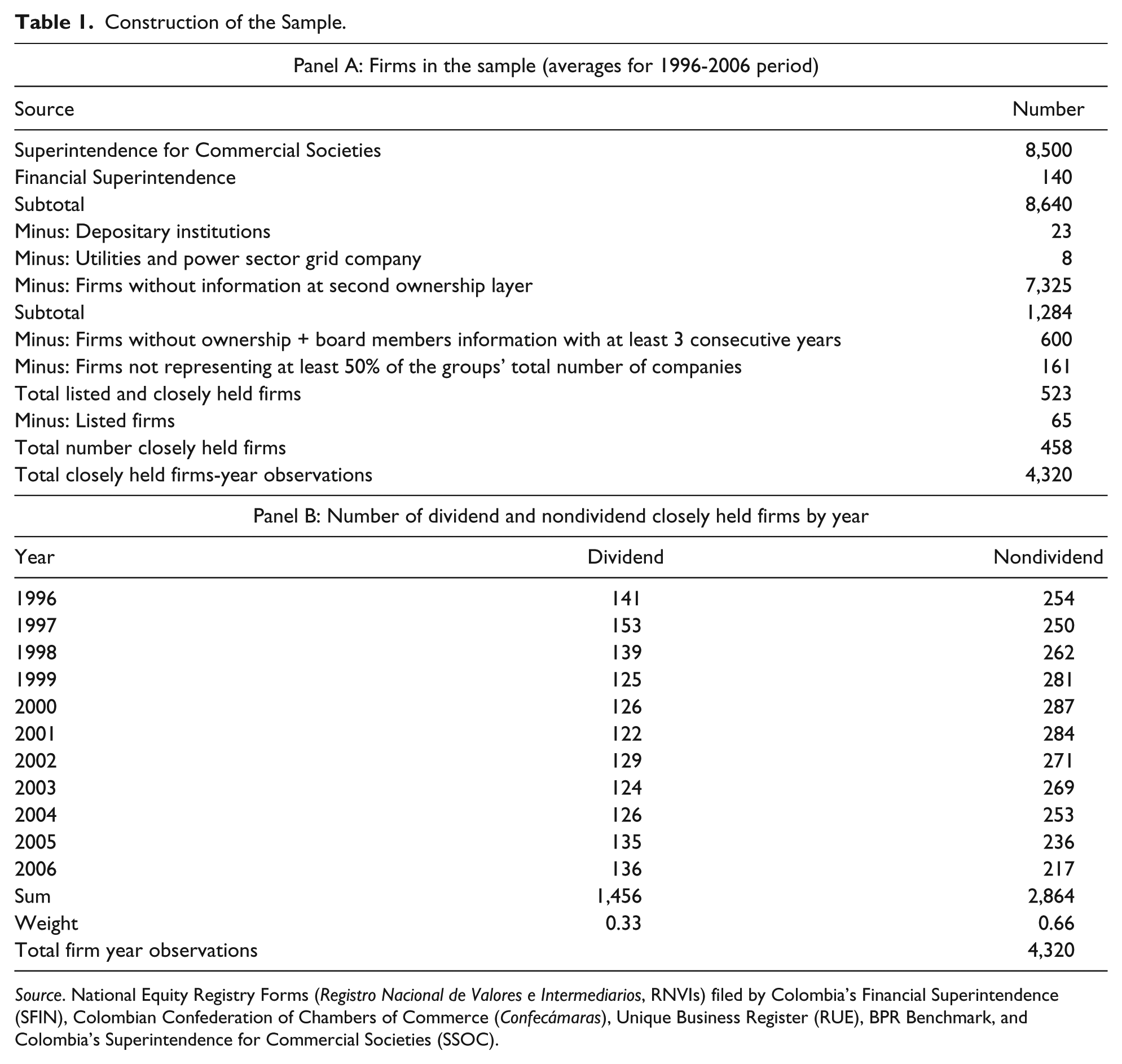

Table 1, Panel A, summarizes the construction of the sample. The original population of 8,640 companies with financial records collected by SSOC and SFIN during 1996 to 2006 were considered. We first eliminated those subject to special regulation: 23 depositary institutions—mostly commercial banks—and 8 electric utilities, all former state-owned enterprises. All these firms were security issuers registered at SFIN. The next filter excluded 7,325 firms without information at the second ownership layer. This restricts consideration to firms with majority and minority shareholders and firms within pyramids where we can identify the ultimate owner. We imposed two additional filters to the 1,284 companies remaining in the sample: (a) they must have reported complete information of ownership and board composition for at least 3 consecutive years (600 firms excluded) and (b) firms affiliated with an economic group must represent at least 50% of the group’s total number of companies (161 firms excluded). The latter constraint means that a firm in a given business group formed by 20 firms must be affiliated with at least ten or more companies to that group to remain in the sample. This allows us to build more accurate information regarding pyramidal control within the group, that is, to identify with more precision the ultimate ownership and determine if there is family control through pyramidal ownership.

Construction of the Sample.

Source. National Equity Registry Forms (Registro Nacional de Valores e Intermediarios, RNVIs) filed by Colombia’s Financial Superintendence (SFIN), Colombian Confederation of Chambers of Commerce (Confecámaras), Unique Business Register (RUE), BPR Benchmark, and Colombia’s Superintendence for Commercial Societies (SSOC).

After allowing for all restrictions, the data sources yielded 523 firms. We then excluded the listed firms from the sample and focused on those closely held. The final size of the sample comprises 458 closely held firms for the analyzed period; 414 of them are affiliated with 28 business groups (of which 25 remained family controlled in 2006) and 44 are independent firms. The majority of the affiliated firms in the sample belong to one of the five largest conglomerates in Colombia. Total data set length is 4,320 firm-year observations, with 33.7% of firm observations from companies that pay dividends (Panel B). Sample firms represent, in terms of asset value, almost 40% of all firms that report financial information to the SSOC.

Dividend and Family Involvement Variables

This study employs two dependent variables to analyze dividend policies. The first is a dividend dummy, which takes the value of 1 when firms decide to pay a dividend, and zero otherwise. This variable captures a firm’s ex ante decision to distribute net earnings. The second variable is the dividend ratio, defined as the amount of dividend payout divided by total assets. We divide dividend payout by assets rather than sales, because holding companies included in the sample do not report sales but usually pay high dividends. Lipson, Maquieira, and Megginson (1998) and Lee (2010) also employ dividend to assets as dependent variable.

We use several variables to gauge family involvement. Family CEO is a dummy variable that takes the value of 1 if a family member serves as CEO and zero otherwise; it captures the impact of family involvement on firm management. Admittedly, this is a very limited assessment of FIM; for example, we do not consider several cases where a nonfamily CEO works closely with a top management team comprised of family members. The closely held nature of our sample and limited information regarding top executives makes it impossible to analyze other types of family involvement.

Family Ownership is a dummy variable that takes the value of 1 when the founding family is the largest shareholder and zero otherwise. Pyramidal Family Control equals 1 when the family has pyramidal control over the firm through indirect ownership. And finally, Majority Family Board dummy is a dummy variable that takes the value of 1 if the participation of family members on the board is more than 50%. This is a good proxy for disproportionate family board representation because, in our sample, families that are the largest shareholder own 33.22% of the firm’s equity on average (median of 27.45%). Following Villalonga and Amit (2009), we want this variable to capture how families using this control-enhancing mechanism can appoint a disproportionate number of directors in excess of their ownership rights.

Control Variables

Econometric analysis takes into account 15 variables to control for firm characteristics. The first five are financial variables that are correlated with the firm’s dividend policy, namely, return on assets (ROA), leverage, and growth opportunities (three for the current values plus two for the lagged values of ROA and leverage). The second set of controls is composed of four idiosyncratic variables that may affect the dividend decision and that are also used extensively in empirical research on dividends and ownership: firm age, firm size, business group affiliation, and diversification. 1 Five controls relate to corporate governance, including board size, the fraction of nonfamily external directors, and the turnover among board members. Inclusion of these controls is consistent with empirical research on family firms (Anderson & Reeb, 2003; González, Guzmán, Pombo, & Trujillo, 2012; González, Guzmán, Pombo, & Trujillo, 2013; King & Santor, 2008; Villalonga & Amit, 2006). Similarly, participation of the CEO on the board and the presence of an external auditing firm were also included. Last, we include contestability as a variable that captures the power of other shareholders to challenge the largest shareholder (Maury & Pajuste, 2005). Definitions and methodology for all indicators and variables included in the econometric analysis are presented in the appendix.

Empirical Model

The estimating equation models the partial effects of family involvement through management, ownership, and control over dividend ratios. Because the sample includes several firms that paid no dividends during the years analyzed, estimations follow a Tobit model. Notably, the empirical model is left truncated at zero, meaning that the variable under analysis is not empirically observed at this value. The empirical regression is specified as an unobserved latent variable y*, one that is not always observed, as follows:

where

The observed variable yi follows an observation rule, in this case:

Thus, the estimating equation of the dividend payout ratio when data is censored can be written as

where

The model also controls for dummies by year, YEAR, and industrial sector, IND. Hence, estimating Equation 1 follows a classical Tobit cross-section regression. 2 From a corporate governance view, dividend policy in a weak institutional environment becomes a market mechanism for investor protection (La Porta et al., 2000). Therefore, we also consider the probability of dividends using a Probit-panel regression model:

where Yit is the dividend dummy, which indicates whether a given firm paid dividends for a particular year and all repressors are the same as those used in the estimating Equation 1.

Results

Descriptive Statistics

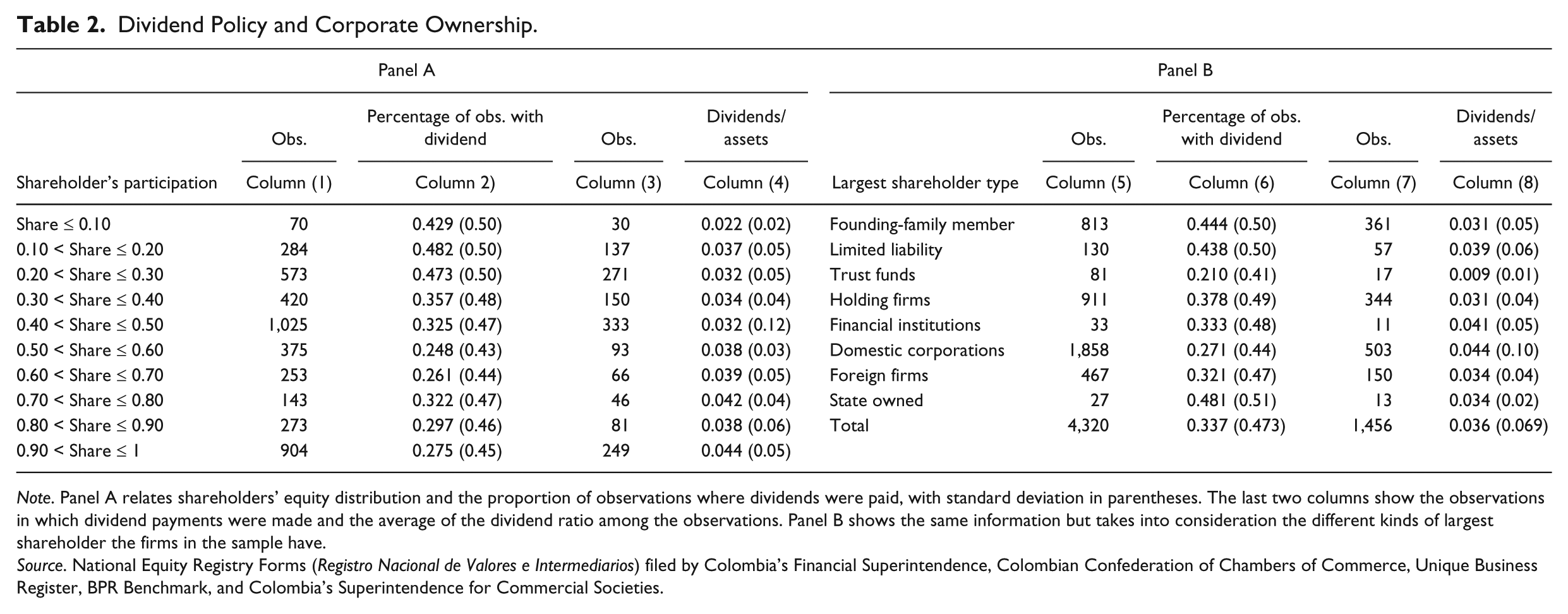

Table 2 reports the dividend ratio and corporate ownership by largest shareholder (Panel A) and shareholder type (Panel B). In Panel A, we report the total number of observations for each shareholder’s participation percentile (column 1), the percentage (column 2), the number of observations that feature dividends (column 3), and the mean and standard deviation of the dividend ratio among dividend observations (column 4). A higher equity fraction for the largest shareholders, as shown, seems to imply a lower likelihood of dividend payout (column 2); the dividend ratio tends to increase with the equity fraction for the largest shareholders, and stabilizes once participation rises more than 50% (column 4). This pattern is consistent with the notion that the largest shareholders who control the firm prefer earnings retentions to dividend payouts.

Dividend Policy and Corporate Ownership.

Note. Panel A relates shareholders’ equity distribution and the proportion of observations where dividends were paid, with standard deviation in parentheses. The last two columns show the observations in which dividend payments were made and the average of the dividend ratio among the observations. Panel B shows the same information but takes into consideration the different kinds of largest shareholder the firms in the sample have.

Source. National Equity Registry Forms (Registro Nacional de Valores e Intermediarios) filed by Colombia’s Financial Superintendence, Colombian Confederation of Chambers of Commerce, Unique Business Register, BPR Benchmark, and Colombia’s Superintendence for Commercial Societies.

Panel B shows the largest shareholder type, with dividend ratio and its frequency. This univariate analysis suggests that direct ownership by the state or by families implies a higher likelihood of dividend payout (column 6); however, it is not possible to argue any kind of causality among these variables without a robust econometric model. There are no clear differences among the remaining types of shareholders, but trust funds, often used by families as legal vehicles to control firms with pyramidal ownership structures, show a lower likelihood of dividend payout. Accordingly, dividend payments seem to be lower inside pyramids.

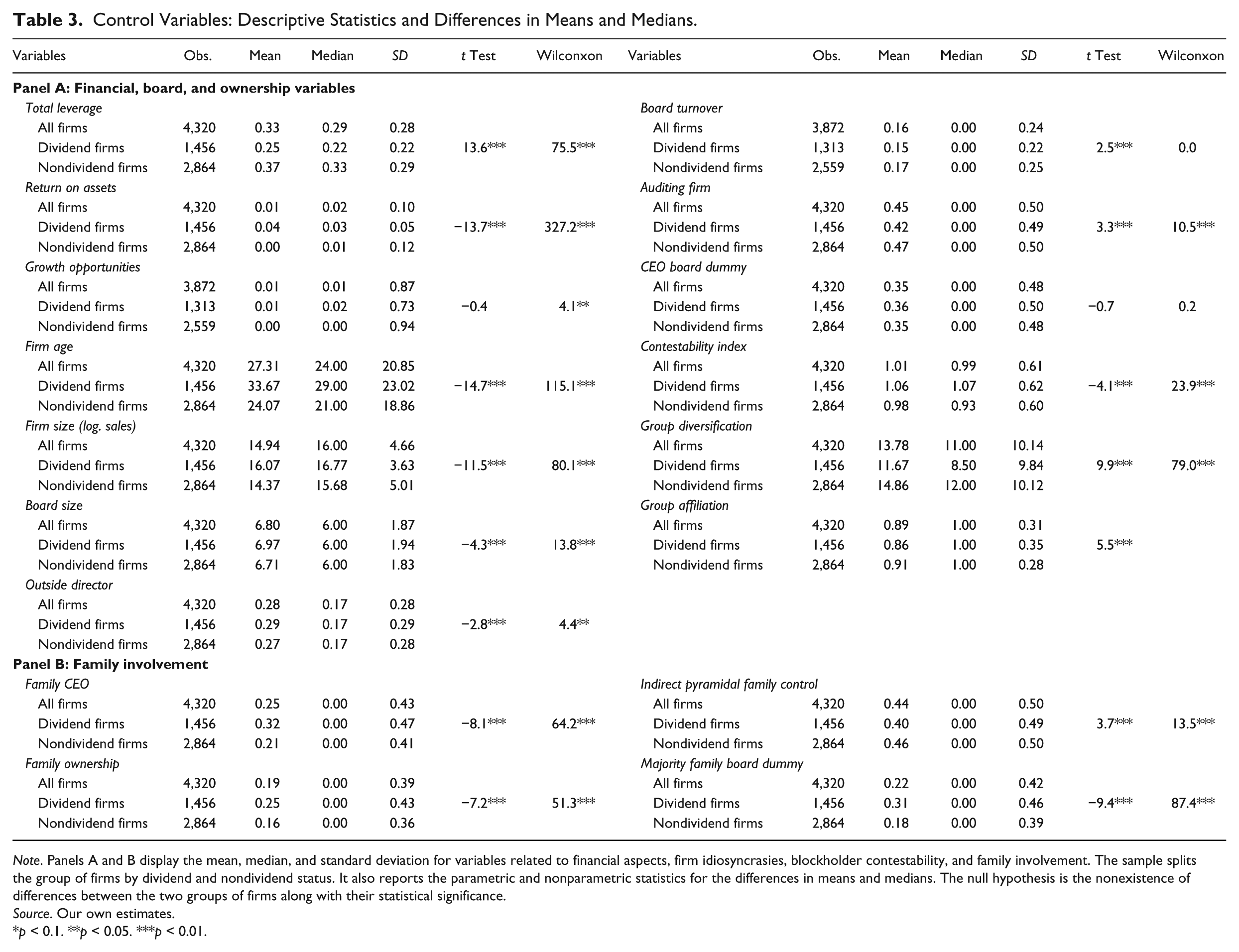

Table 3 presents a statistical summary of all variables. The last two columns display the test of differences of means and medians by two-tailed t tests and the nonparametric rank sum test for all control variables classed by dividend and nondividend firms. Panel A shows financial, idiosyncratic, board structure, and blockholder contestability controls. Panel B considers all family involvement variables. These data show that dividend-paying firms are older, larger, less leveraged, and more profitable than nonpaying firms. Furthermore, dividend-paying firms have larger boards on average, a higher participation of outside directors, and higher contestability across blockholders. Finally, the mean (median) for group diversification shows that dividend-paying firms belong, on average, to less diversified groups and exhibit slightly fewer affiliations with business groups. Hence, a firm seems to be more likely to pay dividends when it is either unaffiliated or it belongs to less diversified business groups.

Control Variables: Descriptive Statistics and Differences in Means and Medians.

Note. Panels A and B display the mean, median, and standard deviation for variables related to financial aspects, firm idiosyncrasies, blockholder contestability, and family involvement. The sample splits the group of firms by dividend and nondividend status. It also reports the parametric and nonparametric statistics for the differences in means and medians. The null hypothesis is the nonexistence of differences between the two groups of firms along with their statistical significance.

Source. Our own estimates.

p < 0.1. **p < 0.05. ***p < 0.01.

Regarding family involvement, Panel B shows that about 25% of firms in the overall sample feature a family CEO, but this percentage is higher for companies that pay dividends. The largest blockholder is related to the founding family in 19% of the companies, but involvement is higher for the subsample of dividend firms. In terms of control through pyramidal structures, dividend-paying firms show less involvement, which seems to indicate that pyramidal family control results in lower dividend payments. Regarding disproportionate board representation (majority family board dummy) about 22% of firms in the overall sample feature this kind of family involvement, but the percentage is higher for companies that pay dividends (31%). All the above differences are statistically significant at the 1% level. We now analyze how different types of family involvement affect firms’ dividend policy.

Family Involvement and Level of Dividend

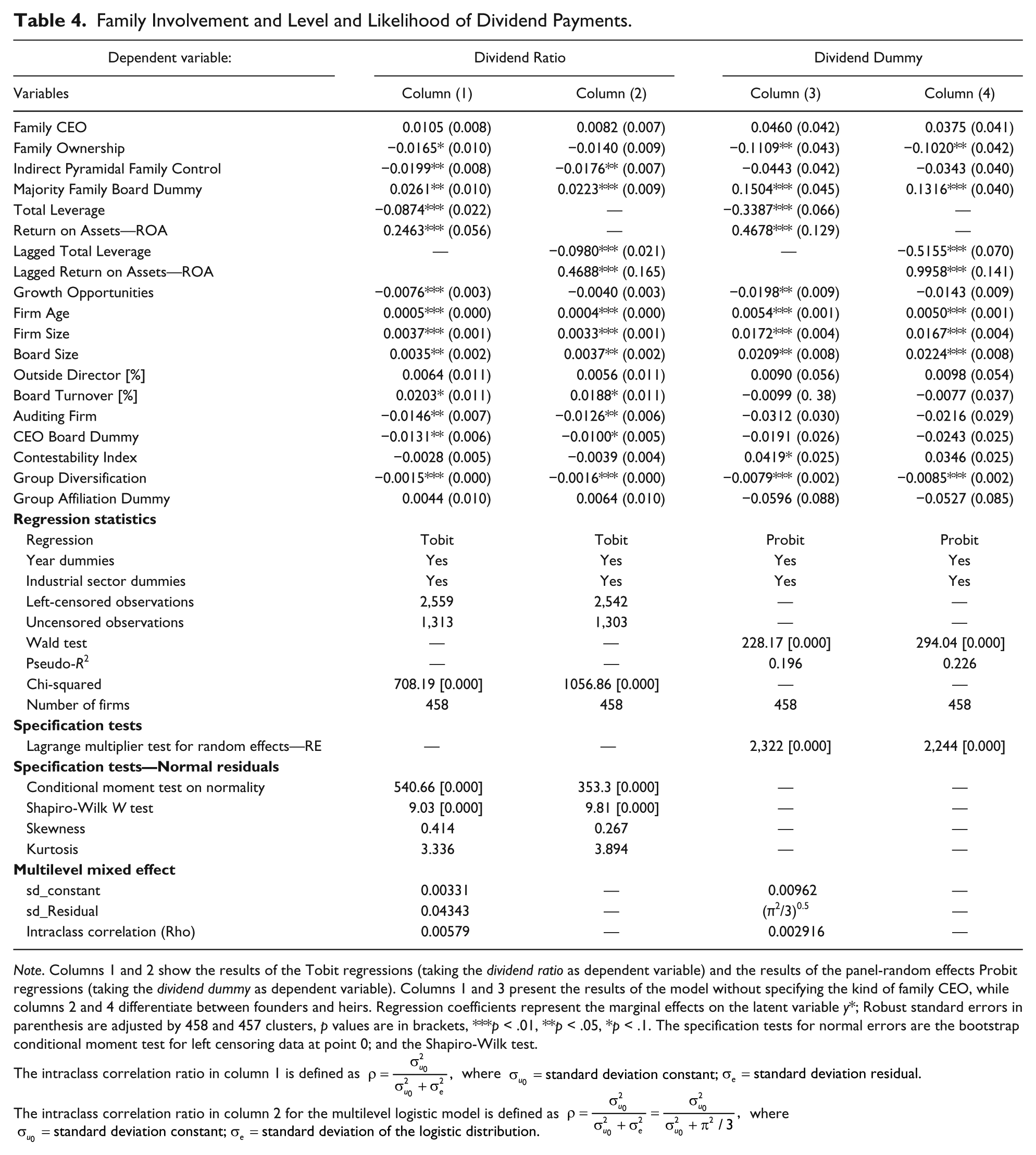

The core results of the Tobit regressions are reported in Table 4, columns 1 and 2, which specify the dividend ratio as the dependent variable. Note that there is no statistical evidence to support Hypothesis 1 (H1), which predicted that a family CEO would lead to increased dividend payments. According to regressions in columns 1 (current values of control variables) and 2 (lagged values of control variables) FIM had no statistical effect on the level of dividend payment.

Family Involvement and Level and Likelihood of Dividend Payments.

Note. Columns 1 and 2 show the results of the Tobit regressions (taking the dividend ratio as dependent variable) and the results of the panel-random effects Probit regressions (taking the dividend dummy as dependent variable). Columns 1 and 3 present the results of the model without specifying the kind of family CEO, while columns 2 and 4 differentiate between founders and heirs. Regression coefficients represent the marginal effects on the latent variable y*; Robust standard errors in parenthesis are adjusted by 458 and 457 clusters, p values are in brackets, ***p < .01, **p < .05, *p < .1. The specification tests for normal errors are the bootstrap conditional moment test for left censoring data at point 0; and the Shapiro-Wilk test.

The intraclass correlation ratio in column 1 is defined as

The intraclass correlation ratio in column 2 for the multilevel logistic model is defined as

Regression results support Hypothesis 2 (H2), which predicts that family involvement through ownership, as the largest shareholder, would lead to lower dividend levels. Family ownership reduces the level of dividend payment by 1.65%. Similarly, supporting Hypothesis 3a (H3a), when the family controls the firm through pyramidal structures, the impact on dividend payout is also negative and reduces the level of dividend payment by 1.99%. Disproportionate family board representation (majority family board dummy) increases dividend ratios by 2.61%, as predicted by Hypothesis 3b (H3b).

Certain important determinants of the payout ratio besides family involvement are worth highlighting. First, financial indicators affect dividend ratios, as expected. Total leverage and growth opportunities are negatively related to dividend ratio, while return on assets is positively related. These effects hold (except for growth opportunities) even after taking one lag period for leverage and return on assets (column 2). Second, the regression coefficients of idiosyncratic variables, such as firm size and age, are positive and significant. These are expected results, consistent with previous dividend studies (Chen, Cheung, Stouraitis, & Wong, 2005; Fama & French, 2001; Hu & Kumar, 2004).

Third, corporate governance variables affect dividend ratios. Having the CEO also serve on the board implies a negative premium of 1.3% on dividend ratios. Moreover, the presence of an auditing firm also reduces dividend ratios, by 1.46%. Board turnover affects dividend payment positively. One standard deviation change (0.25) in directorate composition during a given year raises payout ratio by 51 basis points. In contrast, the presence of outside directors has no effect, since this variable is statistically not significant. Blockholder contestability also has no effect on dividend payout. Fourth, the level of business group diversification exerts a significant and negative impact on dividend payments.

Last, diagnostic tests of Tobit regressions show that the overall model is significant according to chi-square tests, and the reported standard errors of regression coefficients are robust. The variance covariance matrix follows a robust cluster-weighted estimate under the assumption that observations are independent across clusters. 3

Family Involvement and the Likelihood of Dividend Payments

Columns 3 and 4 in Table 4 present the results of the panel regressions for the random effects Probit model following the empirical specification in Equation 2. Again, there is no statistical support for the claim in H1 that a family CEO has a positive influence on the probability of dividend payments. However, there is statistical support for H2; FIO has a negative impact. Regarding FIC through pyramidal control (H3a), the regression coefficients are not statistically significant. FIC through disproportionate board representation (majority family board dummy) increases the likelihood of dividends by 15.04% (column 3), which supports H3b. Hence, the econometric results of the Probit random effects model are in the same direction as those for the level of payout ratio.

Multilevel Effects

As noted, the majority of firms in the sample are affiliated with the five largest conglomerates in Colombia. This raises the question of whether dividend policy is driven by affiliation to a specific conglomerate. In that regard, we estimate the intraclass correlations (ICC) defined as the proportion of the group-level variance to total variance for two dependent variables (dividend ratio and dividend dummy). We take into account the business group affiliation as the highest level dimension; that is, considering that firms are nested within business groups. We used seven groups: the top five conglomerates, the group of unaffiliated firms, and the group of the remaining 23 business groups. A high ICC (close to 1) implies that one additional firm in a business group provides little valuable information. Hence, high ICC suggest the need for multilevel regressions.

The ICC ratios are displayed at the bottom of Table 4 (columns 1 and 3) with the full regressions equations. For the full Tobit regression, the ICC ratio is 0.006; for the Probit model, 0.002, which leads us to disregard multilevel regressions associated with business group affiliation. These low ICCs seem puzzling because it could be expected that dividend policy is decided at the business group level. However, they could be explained by different levels of family involvement across firms in the same business group. Members of the same family have differentiated involvement in the firms belonging to that business group. In some, the family is involved in management, ownership, and the board of directors, but in others, the same family may be involved in control through pyramids. Therefore, the family effect on dividend policy differs even within the same business group.

Robustness Tests

This section presents an instrumental variable analysis to control for endogeneity and double causality among the independent variables. The empirical literature in corporate governance stresses the potential endogeneity between corporate governance fundamentals and firm managerial choices, such as those regarding capital structure, investment, or dividend policies. We tackle endogeneity issues in the empirical model by including robustness checks based on instrumental variables estimations. Two variables—firm leverage and family ownership—are considered to have a circular relationship with either the dividend payout ratio or the likelihood of dividend payments. The discussion that follows focuses on the endogeneity between dividend policy and family ownership. However, families can decide to maintain ownership in firms expected to make low dividend payments in order to control higher free cash flow levels. 4

Following the arguments of Demsetz and Lehn (1985), extended by Himmelberg, Hubbard, and Palia (1999), our regressions use firm size (measured by asset tangibility) and volatility as key instruments for family ownership. The arguments behind the first instrument is that the larger the firm, the greater the value of a given fraction of ownership. Therefore,

The higher price of a given fraction of the firm should, in itself, reduce the degree to which ownership is concentrated. Moreover, a given degree of control generally requires a smaller share of the firm, the larger is the firm. (Demsetz & Lehn, 1985, p. 1158)

This argument implies greater diffuseness of ownership in larger firms (measured as a firm’s assets tangibility).

These authors give an additional argument for expecting an inverse relation between ownership and size: “An attempt to preserve effective and concentrated ownership in the face of larger capital needs requires a small group of owners to commit more wealth to a single enterprise” (Demsetz & Lehn, 1985, p. 1158). This suggests that risk-averse owners will demand a higher risk-adjusted cost of capital, discouraging owners of larger firms from attempting to maintain highly concentrated ownership.

The second instrument, firm cash flow volatility (measured as the standard deviation of the operating margin for the previous 3 years) is a proxy for firm idiosyncratic risk, and all else being equal, might induce blockholders to rebalance their equity shares, for which firm control is most useful. Following the arguments of Demsetz and Lehn (1985, p. 1159): “The noisier a firm’s environment the greater the payoff to owners in maintaining tighter control.” Therefore, high volatility environments should give rise to more concentrated family ownership structures.

In a comparative study between public and privately held firms, Michaely and Roberts (2012) show that private firms smooth dividends significantly less than their public counterparts, but no empirical evidence links asset tangibility and profit volatility with dividends in private firms. Brav, Graham, Harvey, and Michaely (2005) show evidence that private firms are more likely to pay dividends in response to temporary changes in earnings, suggesting that private firms’ dividend policies are more erratic, but again, there is no relation that links our instruments with family firm dividend policy.

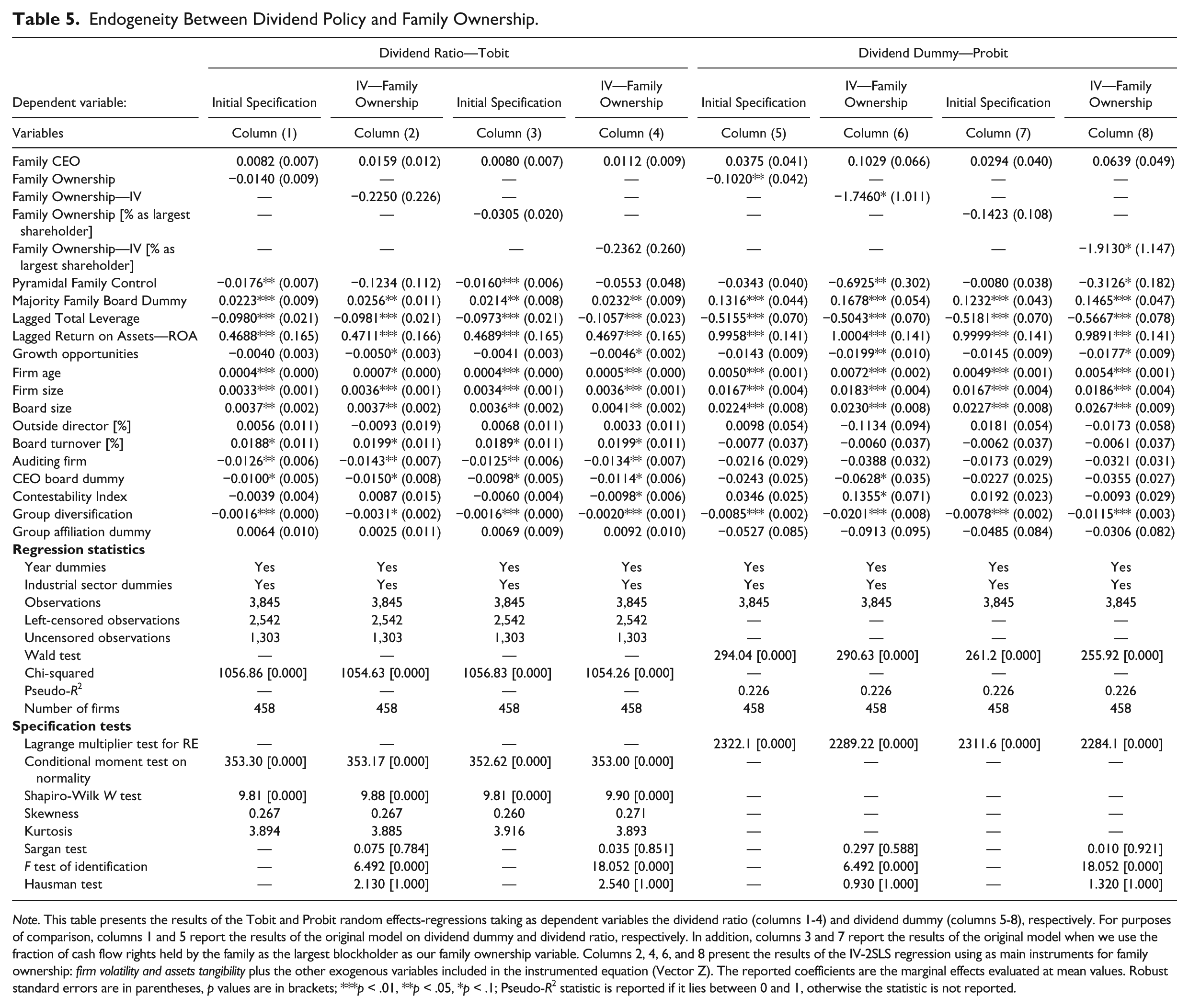

Table 5 presents the estimated results of instrumental variables Tobit and panel-Probit regressions when family ownership uses size and firm volatility as the main instruments. For purposes of comparison, columns 1 and 5 report the results of the original model for the dividend dummy and dividend ratio, respectively. In addition, columns 3 and 7 report the results of the original model when the family ownership variable is the fraction of cash flow rights held by a family as the largest blockholder. Columns 2, 4, 6, and 8 include the instrumented equations. In most cases, regression coefficients keep the sign, magnitude and significance of the original regressions, showing similar marginal effects of family ownership on dividend policy. An F test of the validity of the instruments show a value of 6.5 and 18, which suggests the use of valid instruments (Stock, Wright, & Yogo, 2002); Sargan tests show that it cannot be rejected that the instrumental variables are uncorrelated to some set of residuals, and therefore they are acceptable instruments. Finally, Hausman tests suggest that the original model’s results are preferable on the grounds of efficiency.

Endogeneity Between Dividend Policy and Family Ownership.

Note. This table presents the results of the Tobit and Probit random effects-regressions taking as dependent variables the dividend ratio (columns 1-4) and dividend dummy (columns 5-8), respectively. For purposes of comparison, columns 1 and 5 report the results of the original model on dividend dummy and dividend ratio, respectively. In addition, columns 3 and 7 report the results of the original model when we use the fraction of cash flow rights held by the family as the largest blockholder as our family ownership variable. Columns 2, 4, 6, and 8 present the results of the IV-2SLS regression using as main instruments for family ownership: firm volatility and assets tangibility plus the other exogenous variables included in the instrumented equation (Vector Z). The reported coefficients are the marginal effects evaluated at mean values. Robust standard errors are in parentheses, p values are in brackets; ***p < .01, **p < .05, *p < .1; Pseudo-R2 statistic is reported if it lies between 0 and 1, otherwise the statistic is not reported.

Additional consistency tests were performed on the above econometric results. We first look at the decision power of family blocks within boards, using an alternative measure for disproportionate family board representation. The variable Family Board Participation measures the percentage of board directors who are family members. Results show that family board participation increases dividend ratios and the likelihood of dividend payments, consistent with our results. Higher levels of family involvement on the board increases the agency tension between majority and minority shareholders, and minority shareholders press for more dividends.

Following Villalonga and Amit (2009), we also constructed a variable called Disproportionate board representation, a dummy that takes the value of 1 when the proportion of family directors on the board is greater than the percentage of shares in hands of the family as the largest shareholder, and zero otherwise. In most cases, regression coefficients keep the sign, magnitude and significance of the original results.

A second analysis examines the possibility that the largest family shareholder is not necessarily the controlling one because of the separation between equity and voting rights. Accordingly, the family ownership variable was broken into two categories: Family Ownership with equity share greater than 50% (i.e., a dummy variable that takes the value of 1 if the largest shareholder is a family with 50% or more of the firm’s shares, and 0 otherwise) and Family Ownership with equity share less than 50%. Regressions show similar results in terms of signs, statistical significance and magnitude.

Third, we test the influence of holding firms and trust funds on our results since families are usually behind these legal entities, which can be used to control firms, and so can bias the results. Leaving those that are not working companies out of the analysis, our main results remained. Finally, other econometric specifications were analyzed to check consistency. In particular, random effect estimates of the dividend ratio yielded similar, although weaker, results. 5

Discussion and Conclusions

This article analyzes how FIM, FIO, and FIC influence agency problems between majority and minority shareholders, and how the level and likelihood of dividend payment serve as mitigating mechanisms. Our sample of closely held Colombian firms departs from the traditional emphasis on listed firms in developed countries.

Colombian firms share several characteristics with other emerging markets, for example, high ownership concentration, family business groups, and low investor protection. Our findings show that family influence in relation to the level and likelihood of dividend payments differs significantly according to the type of family involvement.

FIM does not have significant effects on dividend policy. H1, which was not upheld, states that a partially entrenched family CEO derives both monetary and nonmonetary benefits and that minority shareholders (whether family members or nonfamily shareholders) will press for more dividends in response to agency tension. We found that family CEOs had no impact on the amount or likelihood of dividend payments. It seems that family CEOs neither alleviate nor worsen agency problems between majority and minority shareholders. This suggests that benefits associated with family CEOs, such as reduction of agency costs because of the alignment of interests between owners and managers (Fama & Jensen, 1983), longer investment horizon and less managerial myopia (James, 1999; Stein, 1988, 1989), among other benefits, compensate for any disadvantages deriving from a nonmonetary goal orientation (Bertrand & Schoar, 2006; Lee & Rogoff, 1996), nepotism (Pérez-González, 2006), and other agency threats (Kowalewski et al., 2010; Schulze et al., 2001).

As argued in H2, FIO reduces the amount and likelihood of dividend payout. Families affect dividend policy through the supervision they exert as majority shareholders, which reduces management agency problems and the need to use dividends to mitigate them (Fama & Jensen, 1983; Jensen & Meckling, 1976). However, FIO can give rise to agency conflicts between majority and minority shareholders when family members pursue their own interests (Sacristán-Navarro et al., 2011), sometimes even within the family (Boles, 1996; E. J. Miller & Rice, 1988; Swartz, 1989). Hence, FIO may mitigate management agency costs and at the same time accentuate agency conflicts between majority and minority shareholders. If the net effect is mediated by the context, this could explain the varying results when studying the effect of FIO on agency problems. Our results suggest that in a country like Colombia with weak legal protection for minority shareholders, FIO creates shared benefits of control for minority shareholders, and these benefits exceed other agency costs generated by ownership concentration.

In terms of FIC through the use of pyramidal structures (H3a), and in opposition to the traditional view of this control-enhancing mechanism, our results suggest fewer agency costs between majority and minority shareholders inside pyramids. Hence, dividend policy is affected negatively. This result is consistent with Villalonga and Amit (2009) who argue that pyramids can serve purposes beyond that of pure control enhancement.

Most of literature in corporate governance asserts that pyramids promote wealth extraction through tunneling, budget misallocation, empire building, nepotism, related-party transactions and high compensation, all of which harms minority shareholders (Almeida & Wolfenzon, 2006; Bjuggren & Palmberg, 2010; Dyck & Zingales, 2004; Morck et al., 2005; Sacristán-Navarro & Gómez-Ansón, 2007). However, in line with Villalonga and Amit (2009), we argue that in the Colombian context, unlike ordinary “retail investors,” minority shareholders are generally more sophisticated investors, such as wealthy families, equity and pension funds, international investors and other large private firms. This sophisticated kind of minority shareholder is vigilant in preventing tunneling, and the contestability among majority and minority shareholders within pyramids seems to mitigate agency problems and counterbalance any negative effects. Although the contestability variable was not significant in our regressions, the power exerted by these types of investors is not necessarily related to their percentage of ownership in the firm.

Regarding FIC through disproportionate board representation, we find the expected positive and significant effect on both the level and likelihood of dividends (H3b). This is consistent with the classical role played by dividends in mitigating agency problems. Disproportionate board representation creates incentives for majority shareholders to pursue the interests of the family or different family factions (Block, 2012; Martín de Holan & Sanz, 2006; Schulze et al., 2003) at the expense of minority shareholders, who then seek dividends.

This article contributes to the current empirical literature on corporate finance, governance, and family firms in several ways. First, it deals with dividends as mitigating mechanisms in the context of closely held family firms. In contrast, most empirical findings for family firms are based on listed firms (Anderson & Reeb, 2003; Kowalewski et al., 2010; Sacristán-Navarro & Gómez-Ansón, 2007; Villalonga & Amit, 2006, 2009) and little is known about closely held family firms, an understudied organizational form. This matters because some results for samples of listed firms are not directly applicable to closely held firms.

Second, our findings contribute to the growing literature on agency problems within family firms. Our interest is in how minority shareholders in a family firm view potential agency tensions, which will be reflected in dividend policy. Research on family firms usually views a family business as a single unit, ignoring the different ways families may influence corporate finance and governance decisions. This study follows the approach of Villalonga and Amit (2006, 2009) by considering family involvement in three dimensions: management, ownership, and control (pyramids and disproportionate board representation). Omitting any one of these dimensions could lead to misleading results and overlook the multidimensional family effects on firm outcomes.

Third, even though the sample is restricted to Colombia, this context contributes to a better understanding of family firms in emerging markets and to the scant stock of empirical literature on corporate finance, governance and family firms in Latin America and other understudied regions that are gaining relevance for the world economy.

Not addressed in this study is the role of a family CEO working with a majority of nonfamily managers or a nonfamily CEO leading a team of family managers. Accordingly, more research is needed on the structure of top management teams in family firms and the implications for dividend policy in particular and firm performance in general. Similarly, empirical studies are required regarding changes in dividend policy across family generations. Last, the influence of family and nonfamily minority shareholders on dividend policy and the contestability issues they must deal with merit further analysis.

Footnotes

Appendix

Acknowledgements

We want to especially thank the associated editor Wim Voordeckers for his helpful guidance and support in the review process, the comments of three anonymous referees, Randall Morck, Vikas Mehrotra, Belén Villalonga, Luis-Fernando Melo, and Andrés García. We also thank the Superintendence for Commercial Societies (Superintendencia de Sociedades) and the Colombian Confederation of Chambers of Commerce (Confecámaras) for their help in accessing the raw micro-data on boards, ownership, and notes to the financial statements for the nonlisted corporations in the data set.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funding from the University of the Andes School of Management Research Committee and CESA School of Business is fully acknowledged.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.