Abstract

In this article, we introduce socioemotional selectivity theory (SEST) from psychology to the family business literature. Applying the theory to family businesses, we argue that a family business’s age influences whether it trusts family or professional business advisors most. Consistent with SEST, we find that business age relates to whether the family business emphasizes financial or socioemotional wealth more and that this wealth emphasis relates to whether family members or professional business advisors are trusted most. Based on these findings, we believe that SEST has much to offer to the study of family and nonfamily businesses.

Keywords

Which type of business advisors do family businesses trust most? In particular, does a family business’s age influence which type of advisors it trusts most—family or professional advisors? The type of advisors that family businesses trust matters because business advice can affect a business’s performance. Research has found that business leaders who seek advice from a narrow range of advisors like themselves are less capable of successfully addressing poor performance in their organizations than business leaders who seek advice from advisors who are less familiar (McDonald & Westphal, 2003). When confronted with poor performance, business leaders who seek advice from a narrow range of advisors like themselves are unable to significantly change their organization’s strategy because they do not have access to different perspectives. As a result, organizational performance often worsens. This suggests that family business leaders should strive to have a heterogeneous circle of business advisors. But research findings suggest that family businesses often develop homogeneous social networks as they age (Yeung, 2000). We seek to better understand how and why this homogeneity occurs and what effect this has on the selection of advisors for family firms over time.

Business advising refers to a variety of services provided to the owners or managers of a business. These services include accounting services, management consulting, strategic consulting, financial planning, moral counseling, and others. Trust matters in business advising because to receive advice, a business needs to interact closely with an advisor (Bennett & Robson, 2004). Close interaction can mean physically spending time together, being collocated, and sharing extensive information. This close interaction is required so that information asymmetries between the business and advisor may be diminished, accurate assessments may be made, and relevant and valuable advice may be provided. Because businesses often share some of their most valuable information with business advisors in an attempt to facilitate valuable advice, businesses risk exposing this information to outsiders (the advisors). The trust that the business places in the advisor is meant to mitigate the business’s risk exposure. Despite the importance of trust in business advising, few researchers have examined trust in family business advising relationships (Strike, 2012; Upton, Vinton, Seaman, & Moore, 1993; Ward, 1990). We believe that the selection of advisors may hinge on whether or not family business leaders perceive they can trust particular advisors and that this perception will differ as family businesses age.

Psychology researchers have found that as people age, they tend to narrow their social circles to friends and family. Socioemotional selectivity theory (SEST) explains that as people age, they tend to prioritize having positive social interactions rather than trying to meet new people. This leads them to narrow their social circles. In this article, we examine if family businesses behave similarly. Because family businesses are often dominated by a group of individuals from the same family who possess simultaneous goals for the family and business (Chrisman, Sharma, Steier, & Chua, 2013), we believe that SEST may explain family business social behavior in some cases. Applying SEST to family businesses, we hypothesize that as family businesses age, they will emphasize nonfinancial wealth more than financial wealth, and as they emphasize nonfinancial wealth more, they will tend to trust family members for business advice more than professional advisors. The study’s findings support these hypotheses, although we do not find a direct link between family business age and the type of advisors trusted most.

In the remainder of this article, we begin by introducing and reviewing the SEST literature. Next we apply SEST to family businesses and create testable hypotheses. We then describe the sample that we use to test the hypotheses, explain the study’s methods, and report and discuss the results. Finally we offer our thoughts on the study’s contributions and limitations and suggest directions for future research.

Theory Development

SEST was originally designed as a way of explaining the tendency for individuals to focus their social interactions on familiar people as the age. As individuals’ time horizons shorten, they generally become less focused on the future and more focused on the present. The theory states that individuals can be motivated by knowledge-related goals or emotion-related goals (Carstensen, Isaacowitz, & Charles, 1999). Knowledge-related goals aim at knowledge acquisition, career planning, and development of new social relationships. These goals provide information and connections that may prove useful in the future. Emotion-related goals aim at emotion regulation and the pursuit of emotionally gratifying interactions with social partners. These goals provide immediate satisfaction. When individuals are motivated by emotion-related goals, they become selective about the individuals with whom they interact. In particular, they choose to spend their time with familiar people with whom they share a positive relationship. Selecting to spend time with these people increases the individual’s positive emotional experiences, which is consistent with their emotion-related goals (Carstensen et al., 1999). Figure 1 depicts the theory.

Socioemotional selectivity theoretical model.

The theory makes three assumptions about human nature (Carstensen, 1993). First, social interaction is necessary for survival. Second, individuals are goal oriented. They choose to engage in behaviors that they believe will lead to the realization of their goals. Third, individuals often hold multiple (sometimes conflicting) goals. Therefore they need to select among goals before they act. Engaging in social interaction allows individuals to acquire information and regulate emotional states. Information acquisition includes gathering data and making connections that may be instrumental to satisfying an individual’s long-term goals. Emotional regulation includes seeking to avoid negative emotional states and eliciting positive states.

SEST states that when an individual has competing knowledge- and emotion-related goals, the relative importance of the different types of goals is assessed and the individual will then act (or not act) based on which goal is more important at the time (Carstensen, 1993; Carstensen et al., 1999). When individuals assess their knowledge- and emotion-related goals, they instinctively take into account “their time.” If they perceive that their future is not constrained, they will prioritize knowledge goals. Prioritizing knowledge goals causes them to engage in social interaction that allows them to acquire information or contacts that are new to them. Because those people to whom they are closest usually possess knowledge that is redundant with their knowledge, individuals often engage in social interaction with people with whom they are less familiar when motivated by knowledge-related goals.

Alternatively when individuals perceive their future as constrained, they will prioritize emotion-related goals. Individuals see their futures as constrained when they perceive an impending ending. Examples of impending endings include the end of one’s life or a life stage and the end of a dream or a possibility. These perceived endings cause individuals distress, which heightens the importance of their emotional goals (Carstensen et al., 1999). Prioritizing emotional goals will cause individuals to engage in social interaction that allows them to mitigate their distress and/or elicit positive emotions. Because those people to whom individuals are closest usually care most about their emotional state, individuals will often engage in social interaction with those to whom they are closest when motivated by emotion-related goals. SEST states this happens more often as individuals age.

Most SEST research has examined how age influences individuals’ choice of social partners. Although aging is a main reason why individuals may perceive endings, from the first descriptions of SEST, Carstensen (1993) suggested that there should be other conditions that make endings salient for individuals and that this saliency would influence individuals to choose social partners who help elicit positive emotions. Researchers have subsequently found that SEST explains social partner selection among patients who have been diagnosed as HIV-positive or -negative (Carstensen & Fredrickson, 1998), young cancer patients (Kin & Fung, 2004), adolescent gang members who perceive shortened time horizons (Liu & Fung, 2005), the citizens of Hong Kong in the days before the handover of the city from Great Britain to China (Fung, Cartstensen, & Lutz, 1999), residents of Hong Kong in the days before and after the 2001 American terrorist attacks and the 2003 SARS outbreak (Fung & Carstensen, 2006), and college seniors who are nearing the end of their college days (Pruzan & Isaacowitz, 2006). Taken together, this empirical research shows that individuals in three cases (those who are in their older years, those facing endings in the near future, and those facing situations that limit their abilities to fulfill an important objective) were motivated more by emotion-related goals than by knowledge-related goals and subsequently expressed a preference to spend time with people to whom they were emotionally close. Their motivations for preferring to spend time with friends and family, however, differed depending on whether they perceived that they were facing a shortened time horizon or whether they perceived they were facing a blocked goal (Fung & Carstensen, 2004). In this study, we are interested in family business leaders’ perceived goal constraints and how these constraints affect their relationships with their business advisors. We define a family business as an enterprise in which the members of one or more families wield significant control over the enterprise.

Although SEST is an individual-level theory, we believe that the theory can explain organization-level behavior in family businesses—in particular, advisor selection behavior. Advising is an interpersonal service. In family businesses, a controlling family has a significant amount of influence on the business’s strategic choices. As a result, understanding the demographic and psychometric characteristics of the controlling family members can provide insight into the business’s decisions (Ensley & Pearson, 2005; Felin & Foss, 2005; Hambrick & Mason, 1984). We assume that for the most trusted advising relationships, a family business’s leaders are involved, and these are often family members or individuals who may be “considered family,” as compared to other employees. If this is the case, then we believe that applying a psychological theory like SEST to family business advising relationships is appropriate.

Socioemotional Selectivity Theory Applied to Family Business Advisor Selection

SEST predicts that as individuals age, they will prioritize emotional goals over knowledge goals. Prioritizing emotional goals means that they will seek to minimize negative emotions and elicit positive emotions in their social interactions. Therefore, for their social interaction, they will select friends and family members as social partners more often and unfamiliar individuals less often. For the first part of the SEST model (see Figure 1), for family businesses, an analogy to individual age is “business age” and an analogy to prioritizing emotional goals over knowledge goals is emphasizing “socioemotional wealth” over “financial wealth.”

Business age refers to the age of a business. Although family businesses do not age like individuals, they do age and pass through life stages (Gersick, Davis, Hampton, & Lansberg, 1997). A family business’s age can be measured in years, generations, or family events. As age lengthens in a business, the business becomes less likely to fail (Evans, 1987), growth slows (Evans, 1987), and the rate of innovation slows (Fligstein, 1985). As age lengthens in a family business, the number of family members involved often grows (Gersick et al., 1997), leadership styles often change from paternalistic to professional (Lussier & Sonfield, 2004; Mussolino & Calabro, 2014), and strategies become more conservative (James, 1999). Note that most of the world’s oldest businesses are family businesses (Ekta, 2012; Kothari & Tobwala, 2010).

Financial wealth refers to the monetary capital that an individual or group possesses, and socioemotional wealth refers to the collective, affective capital that a group possesses (Berrone, Cruz, & Gómez-Mejia, 2012). For the controlling family of a family business, socioemotional wealth includes the abilities to further family goals and perpetuate family values within the business and to use the business as a means of maintaining intrafamily intimacy (Berrone et al., 2012; Gómez-Mejia, Cruz, Berrone, & De Castro., 2011; Gómez-Mejia, Haynes, Núňez-Nickel, Jacobson, & Moyano-Fuentes, 2007).

In family business research, socioemotional wealth and financial wealth have been contrasted (Berrone et al., 2012; Gómez-Mejia et al., 2011; Zellweger & Astrachan, 2008). But the different forms of wealth are not necessarily opposed. To further family goals, family businesses may pursue financial wealth goals in service of socioemotional wealth goals. For family businesses that emphasize socioemotional wealth, however, their “primary reference point is the [potential] loss of their socioemotional wealth” (Gómez-Mejia et al., 2007, p. 106). For these family businesses, “any threat to socioemotional wealth means that the family is in a ‘loss mode’” (Berrone et al., 2012, p. 260). These researchers have found, therefore, that family businesses that strongly emphasize socioemotional wealth are willing to sacrifice financial wealth to preserve their socioemotional wealth, or at least not suffer socioemotional wealth losses. Other family businesses may be different. We submit that family businesses differ in the type of wealth they emphasize. They generally have a wealth emphasis that tends toward financial wealth or socioemotional wealth.

Financial wealth emphasis is the priority that a family business places on goals meant to increase the business’s financial capital. Although increasing financial wealth may increase a family business’s socioemotional wealth, a business with a high financial wealth emphasis seeks to increase financial capital without regard for the family’s socioemotional wealth. Conversely, socioemotional wealth emphasis is the priority that a family business places on goals meant to preserve and enhance intrafamily intimacy, without regard for the family’s financial capital. Taken together, these definitions suggest that financial and socioemotional wealth emphases represent two ends of a spectrum. When a family business strongly emphasizes financial wealth, there will be less emphasis on socioemotional wealth, and vice versa.

Applying SEST, we argue that as family businesses age, they are likely to look more like the family businesses described above. That is, they are likely to look like family businesses that have the potential loss of their socioemotional wealth as their primary reference point. This means that the family business’s leaders are motivated by the threat of the loss of their family’s socioemotional wealth. Their identities, the family legacy, and the family’s sense of intimacy are all important, salient factors for the leaders of these old family businesses. But these factors probably matter less for the leaders of young family businesses. Applying SEST to family businesses, the threat of the loss of socioemotional wealth for the leaders of older family business will lead them to emphasize socioemotional wealth; the lack of threat for the leaders of younger family businesses will lead them to emphasize financial wealth. Therefore we hypothesize the following:

For the second part of the SEST model (see Figure 1), for family businesses, a component of an individual’s social circle may be a family business’s “most trusted advisors.” In two studies of small- to medium-sized enterprise (SME) owners and managers, Bennett and Robson (2004, 2005) examined the difference in trust between different types of business advisors. The studies used the same sample. After identifying their most important type of business advisors, the 200 SME respondents in the sample were asked to indicate whether their relationship with the advisor during consultations was “founded largely on personal trust of the supplier [advisor] without written contract, more on a written contract with targets between you and your supplier, or both” (Bennett & Robson, 2004, p. 478). The researchers found that all of the relationships that the SME leaders had with friends and family advisors was based completely on personal trust. All other advice relationships were based on a combination of personal trust and a written contract.

The finding from Bennett and Robson (2004) that SME leaders’ relationships with their family advisors were based on trust is not surprising when considering the activities in which a family advisor may be involved. Because family business leaders play multiple roles in their families and businesses—for example, as family members, managers, and owners (Gersick et al., 1997)—family advisors are often more familiar with issues in the family and business and can therefore provide advice on a wider scope of topics than can professional, nonfamily advisors. Family advisors can knowledgably provide advice to their relatives related to ownership, management, and family issues. Professional advisors often are not as knowledgeable about all three types of issues. This means that they might not understand the business’s priorities and subtleties as well as a family advisor might. On the other hand, professional advisors, because they are not family members, are less likely to be overattached to the family. They are more likely to hold different perspectives than family members. They are more likely to have different backgrounds, and they may be more likely to offer information and ideas that are new to family business leaders (Nicholson, 2008). Nevertheless, whether family business leaders seek advice from family or nonfamily members, they are generally counseled to develop relationships with parties outside the business, including advising relationships. These advising relationships can enhance a business’s ability to accomplish its goals (Street & Cameron, 2007). But family business should be aware of advisors’ interests.

Family and professional advisors differ in the interests they have in the business with which they consult. Accountants and financial advisors are often primarily interested in maximizing a business’s financial wealth position. Moral counselors and coaches are interested in individual leaders’ personal development. A marketing specialist’s interest may be in maximizing the family business’s brand, and a family advisor’s interest is often in supporting and maximizing the family’s wealth (socioemotional and financial wealth).

We submit that like older individuals who seek to minimize negative emotions and elicit positive emotions, family businesses that emphasize socioemotional wealth will select business advisors who do not threaten the family’s shared identity, legacy, or sense of intimacy. Instead, they will select advisors who respect and value the family’s socioemotional wealth as the family business leaders do. Professional advisors’ interests may be seen as threatening or not supportive of a socioemotional wealth emphasis. For example, an accountant’s interest in maximizing the family business’s financial position may result in the accountant suggesting that an unprofitable division be eliminated, with the implication that family members would have to seek employment elsewhere. This advice, if taken, would reduce the family business’s socioemotional wealth. Family advisors’ interest, on the other hand, may be seen as less threatening to the leaders of a family business that emphasizes socioemotional wealth.

Although family businesses with a socioemotional wealth emphasis will have a variety of advisors for different purposes, their most trusted advisors will be family members. Conversely, for family businesses that emphasize financial wealth, we predict that although they will have a variety of advisors, their most trusted advisors will be professional advisors. Therefore we hypothesize the following:

As described above, SEST was developed to explain the tendency of individuals to focus their social interactions on friends and family as they age. The prioritization of emotional goals over knowledge goals is the mediating construct that links an individual’s age to the tendency to include friends and family, or unfamiliar individuals, in his or her social circle. Continuing the analogy begun above for family businesses would mean that family businesses would trust family advisors most as they age (compared to professional advisors), and this relationship should be mediated by a socioemotional wealth emphasis (compared to a financial wealth emphasis). Therefore we hypothesize the following:

Figure 2 depicts the family business SEST model that we examine in this study.

Family business socioemotional selectivity theoretical model for identification of the most trusted advisor.

Method

To test our hypotheses, we used data from the publicly available 2007 American Family Business Survey (AFBS). The 2007 AFBS was a telephone survey conducted within the United States by the Family Firm Institute that asked family business owners questions about their business’s strategy, succession plans, company characteristics, governance structures, and performance. Of the 2,500+ family business leaders who were contacted to participate in the survey, 1,035 (41%) indicated they were willing to participate. The survey respondents were men and women who (a) were at least 18 years old at the time of the survey, (b) reported 2006 federal tax returns for a family business, and (c) had the primary knowledge or a good deal of knowledge about the business. Seventy-one percent of the respondents were the CEO or highest ranking person in the business. Because the AFBS was interested in established companies, respondents were limited to family business leaders who had a business with annual revenues of at least $250,000 and whose family business was at least 10 years old. After determining whether a company met these criteria, the AFBS collected data from 650 members of separate family businesses.

One hundred six respondents listed their business’s primary industry as business/professional services (16.3%). Ninety-three were in a retail trade or distribution industry (14.3%), 6 in a communications industry (0.9%), 50 in a wholesale trade or distribution industry (7.7%), 6 in an energy industry (0.9%), 39 in a travel or transportation industry (6.0%), 17 in an insurance industry (2.6%), 8 in a telecommunications/utility industry (1.2%), 20 in a finance or securities industry (3.1%), 22 in a technology industry (3.4%), 61 in a manufacturing industry (9.4%), 38 in a health care industry (5.8%), 5 in an education industry (0.8%), 43 in a real estate industry (6.6%), and 136 in an “other” industry (20.9%).

Note that all of the data used in this study were derived from the AFBS, and all the AFBS data were self-reported by family business leaders. Although data from multiple sources are often desirable, self-report data are appropriate for measuring perceptual constructs (Conway & Lance, 2010). Two of the main constructs examined in this study (financial vs. socioemotional wealth emphasis, and the degree to which family business leaders trust an advisor) are perceptual data. Therefore self-report data are appropriate. The third main construct examined is business age, which can be gathered equally well from family business leaders or archival sources (if the data are publically available). Additionally, because all the data used in this study derive from a single source (the AFBS respondents), the study may be prone to a common methods bias. Like Schulze, Lubatkin, and Dino (2003) who examined the 2002 AFBS, we believe that the structure of the AFBS questionnaire and the data that we selected to examine mitigate the threat of common methods bias. Several of the data we examine are descriptive data (e.g., business age, industry), which are often not prone to the threats posed by common methods variance (e.g., social desirability). The common methods threat in the other data we examine (e.g., wealth emphasis, most trusted advisors) are mitigated because they do not relate to obvious types of social desirability or other sources of bias, are measured using different question and scale formats, and are located in different parts of the survey (Podsakoff, MacKenzie, Lee, & Podsakoff, 2003).

Measures

Dependent and Independent Variables

Most trusted advisor

Previous business advice research “asked respondents for a complete list of their significant external advisors used in the past 3 years, from which they were asked to nominate the top three preferred suppliers of advice or consulting services” (Bennett & Robson, 2004, p. 478). The authors then categorized the advisors into nine categories: friends and relatives, business associates, accountants, solicitors, banks, customers, consultants, Business Link (a government counseling service), Training and Enterprise Councils (local, government-funded training programs), and the U.K.’s Department of Trade and Industry.

Building on this research in the United States, the AFBS asked, “In general, who are your most trusted business advisors? Please rank your top three.” Each respondent, therefore, listed responses for three advisors regardless of how many advisors the respondent had. The options for categories of business advisors were Accountant, Banker, Business peer, Child, Clergy, Financial services, Friend, Insurance agent, Lawyer, Parent, Spouse, Employees, Family, Me/myself, Partner, Sibling, Miscellaneous, and None. Therefore there were 18 categories of advisors. To measure the degree to which family business leaders trust advisors, we noted their three rankings. For the most trusted advisor, we assigned a trust value of 3. For the second most trusted advisor, we assigned a value of 2. For the third most trusted advisor, we assigned a value of 1, and for the unranked advisors, we assigned a value of 0. Therefore, for each respondent, there was 1 advisor with a trust value of 3, 1 advisor with a value of 2, 1 advisor with a value of 1, and 15 advisors with a value of 0. Because trust requires familiarity and a positive assessment, this method allowed us to distinguish between advisors with whom the respondent was more or less familiar and advisors toward whom the respondent was positive, neutral, or negative.

Studies that have used ranked data similar to the most trusted advisor AFBS data have combined the rankings into categories and summed the rankings within the categories for analysis purposes. These studies include examinations of individual moral values data (Rosenberg, 1987), organization-level environmental threat data (Jauch, Osborn, & Martin, 1980), and nation-level stakeholder salience data (Duncan & Moores, 2014). Following the lead of these studies, to measure the degree to which family business leaders trust family advisors most, we summed the trust values of the family advisors; and to measure the degree to which family business leaders trust professional advisors most, we summed the trust values of the professional advisors. Rather than considering only the single most trusted advisor, we considered the three most trusted advisors. Like the upper echelons literature that suggests that an organization’s management can be better understood by examining multiple top managers rather than only the CEO (Hambrick & Mason, 1984), we reasoned that examining the three most trusted advisors would provide a better representation of a family business’s level of trust than only examining the single, most trusted advisor. We considered the following categories to be family advisors: Child, Parent, Spouse, Family, and Sibling. Therefore the family advisor most trusted measure could be as high as 6 if all of the three most trusted advisors are family members, and the measure could be as low as 0 if none of the three most trusted advisors are family members. Similarly, the professional advisor most trusted measure could range from 0 to 6.

In terms of the family advisor classification, note that the advisor titles unfortunately may not entirely reflect the familial relationship between the survey respondent and the advisor. For example, a brother who is an accountant can be a professional advisor. But we do not know how a respondent might have categorized him. He could be classified as a sibling or as an accountant. Therefore, we opted to be conservative in our classification of family advisors to include only those advisor titles that were familial titles.

Wealth emphasis

In terms of the study’s independent variables, we also used items from the AFBS. In terms of the degree to which a family business emphasized financial versus socioemotional wealth, we noted the leaders’ responses to an item that asked them to assign a score of between 1 and 7 that positioned their firm between a pair of statements. The statements were “We primarily get financial and professional satisfaction from this business; working with family is a bonus” and “We primarily get satisfaction from working with family members; the financial rewards from the firm are a bonus.” If respondents agreed completely with the first statement, they assigned a score of 1 to the item. If respondents agreed completely with the second statement, they assigned a score of 7 to the item. This meant that higher scores were associated with a socioemotional wealth emphasis, lower scores with a financial wealth emphasis, and scores in the middle (a score of 4) were associated with a balanced emphasis on financial and socioemotional wealth. Therefore, we used this score as a measure of wealth emphasis.

Family business age

In terms of a family business’s age, the AFBS asked respondents, “In what year was the business founded?” To compute the age, we subtracted the year from 2007 (the year in which the survey was conducted). Businesses ranged in age from 10 to 207 years old. The mean age was 28.01 years old. Because the age distribution was skewed (skewness = 2.83, kurtosis = 12.69), we normalized the measure by taking the square root of the business age.

Control Variables

In addition to a family business’s wealth emphasis, we reasoned that the level of trust that a family business places in advisors may be influenced by other factors. In particular, the business’s industry, size, and the gender of the business’s CEO might influence the level of trust. In terms of industry, we reasoned that there may be industry characteristics (e.g., industry maturity, task-related characteristics) that might lend themselves more readily to consultation with advisors with more technical expertise than general expertise. In terms of business size, as businesses grow in size, they often become increasingly more professionalized and therefore may use more contracted business advisors. Bennett and Robson (1999a, 1999b) found that SMEs tended to seek advice more from contracted advisors as company size increased. Last, in terms of CEO gender, following research that found that women business owners were more likely than male owners to seek advice from friends and family compared to other advisors (Robson, Jack, & Freel, 2008), we reasoned that female family business leaders may trust family advisors more than male leaders.

Industry

To measure industry, we noted family business leaders’ response to the question “What industry group best describes your company’s activity—Business/professional services, Retail trade or distribution, Communications, Wholesale trade or distribution, Energy, Travel or transportation, Insurance, Telecommunications/utilities, Finance or securities, Technology, Manufacturing, Government, Health care, Education, Real Estate, Other.” Because there were no government industry businesses, we used 14 binary industry dummy variables to represent the business’s industry.

Business size and CEO gender

To measure business size, we used two items. We measured number of employees using the respondent’s answer to the question “About how many full-time equivalent employees does the company have today,” and we measured sales revenue using the respondent’s answer to the question “Approximately what was the sales revenue last year?” Last, to measure CEO gender, we collected the gender of the business’s chief decision maker. We coded the item as “1” if the chief decision maker was male, and we coded the item as “0” if the chief decision maker was female.

Research Method

To test the hypotheses, we adopted a research design that allowed us to test for the existence of relationships between variables in a nonlaboratory setting. Because we were not concerned with determining causality, we used a one-shot case study design (Campbell & Stanley, 1963). The one-shot case study design allows researchers to observe relationships between a treatment (e.g., the degree to which financial or socioemotional wealth is emphasized) and an observation (e.g., the degree to which family or professional advisors are trusted most). To analyze the data collected for the study, we used linear and ordinal regression. We used linear regression for testing Hypothesis 1 because financial versus socioemotional wealth emphasis was measured using a 7-point interval scale. We used ordinal regression to test Hypothesis 2 because the advisor trust–level variables were computed from ordinal measures of trust, and we used linear and ordinal regression to test Hypothesis 3 because both linear and ordinal dependent variables needed to be used. Overall we also used regression because this method allows control variables to be entered with the independent variables.

Results

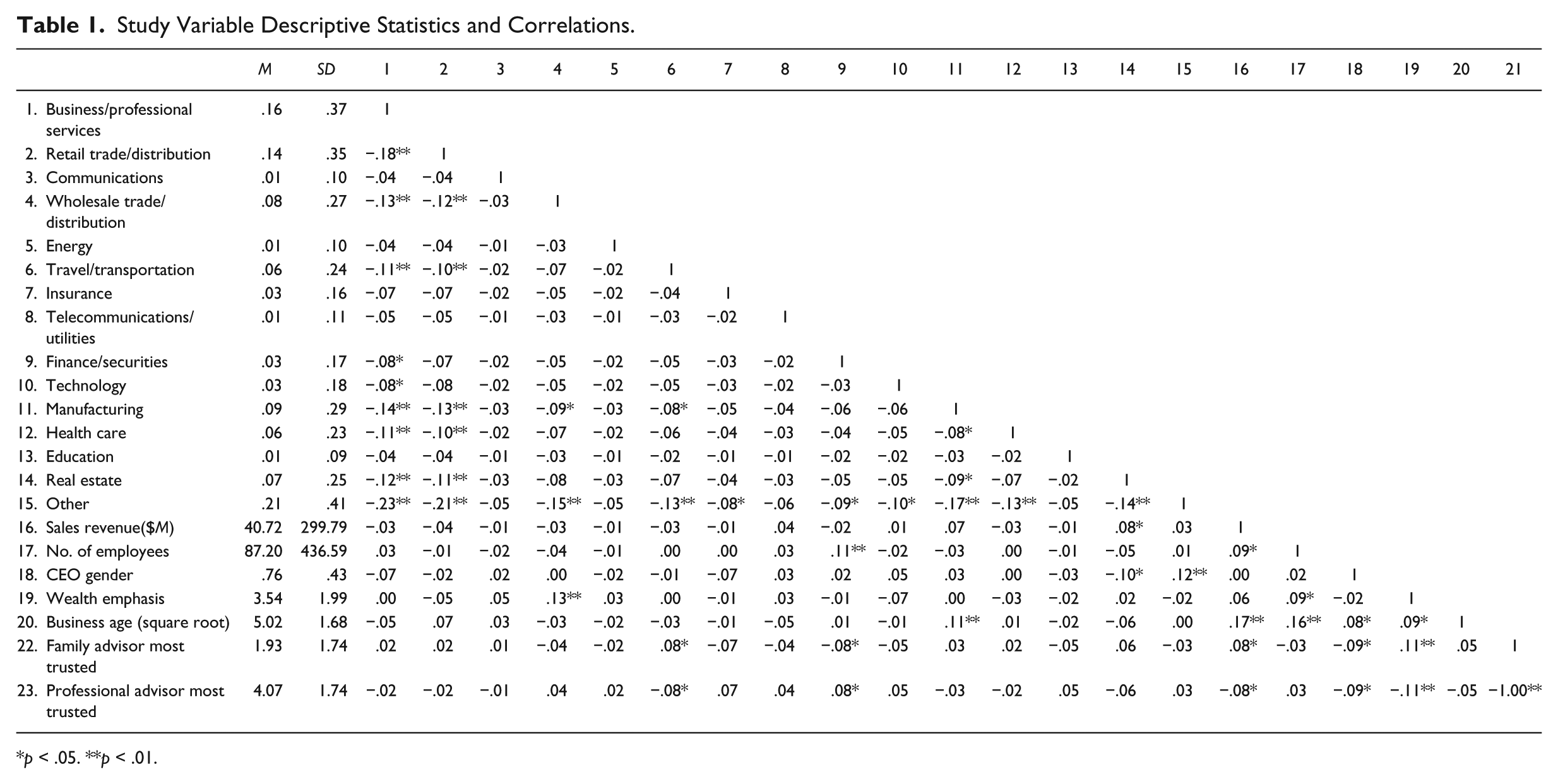

Descriptive statistics and correlations of the study variables are displayed in Table 1. The descriptive statistics show that the industries most represented in the sample were the “business/professional services” industry (16%) and the “other” industry (21%). The mean company size in terms of sales revenue was $40 million, and the mean company size in terms of headcount was 87 full-time employees. Also, 76% of the businesses in the sample were led by a male chief decision maker.

Study Variable Descriptive Statistics and Correlations.

p < .05. **p < .01.

In terms of wealth emphasis, the mean value for the 650 businesses in the sample was 3.54. Therefore the mean score showed that the sample leaned a little toward an emphasis on financial wealth rather than on socioemotional wealth. In terms of business age, the mean value was 5.02 (which is the square root of the business age). In terms of the correlations between the independent and dependent variables, Table 1 shows the correlation between business age and wealth emphasis is significant and in the hypothesized direction (r = .09). The correlations between wealth emphasis and the advisor most trusted variables are also significant and in the hypothesized directions (r = .11 for family advisor most trusted, and r = −.11 for professional advisor most trusted). The correlation between business age and the advisor most trusted variables were not significant (r = .05 for family advisor most trusted, and r = −.05 for professional advisor most trusted). In terms of the dependent variable, the descriptive statistics show that the mean family advisor most trusted level was 1.93, and the mean professional advisor most trusted level was 4.07. Therefore, overall the family business leaders trusted nonfamily business leaders more. Table 2 shows wealth emphasis and family most trusted levels when regressed on the independent and control variables.

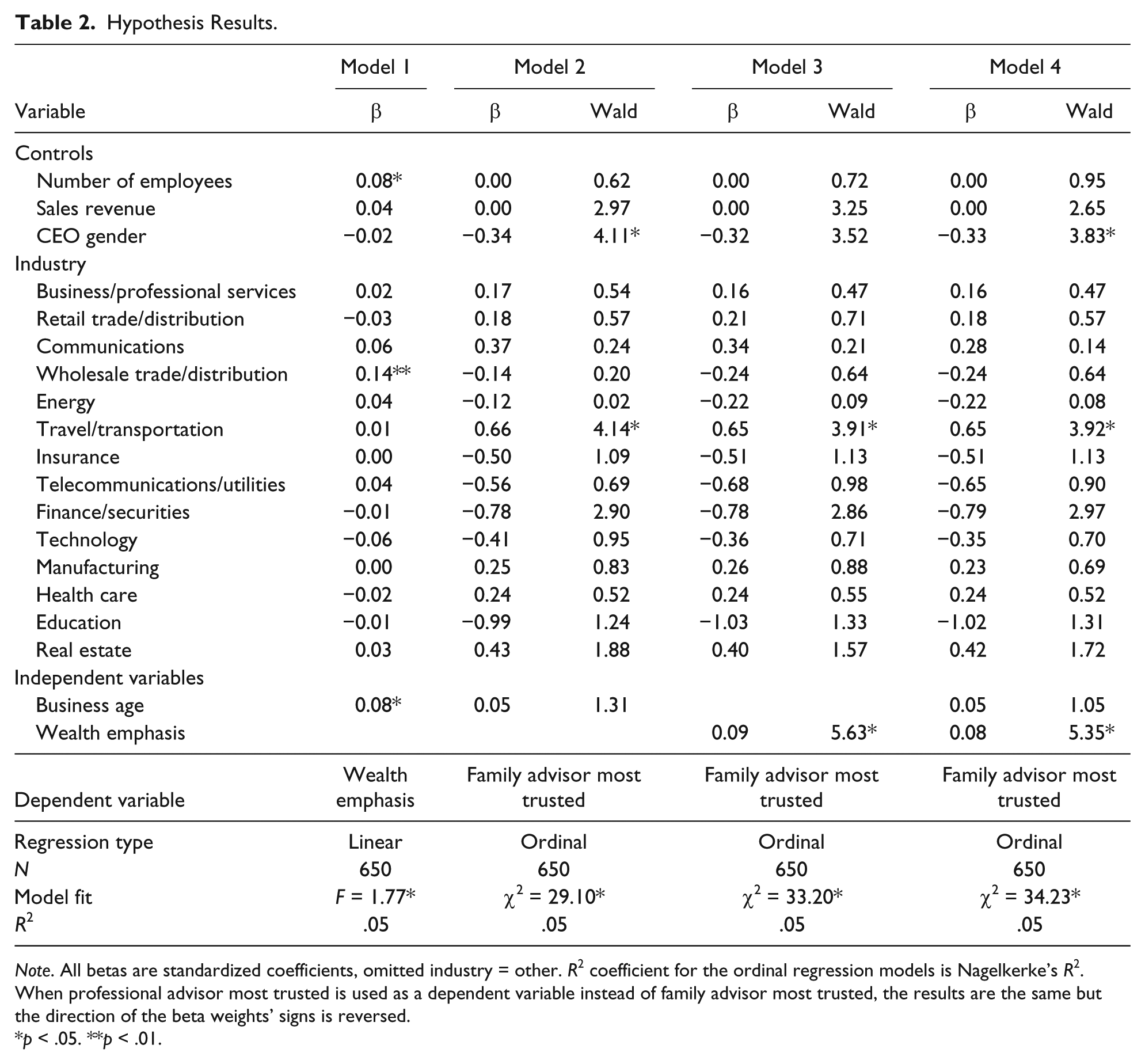

Hypothesis Results.

Note. All betas are standardized coefficients, omitted industry = other. R2 coefficient for the ordinal regression models is Nagelkerke’s R2. When professional advisor most trusted is used as a dependent variable instead of family advisor most trusted, the results are the same but the direction of the beta weights’ signs is reversed.

p < .05. **p < .01.

In Table 2, Model 1 represents the test of Hypothesis 1. This hypothesis states that in a family business, the business’s age will be positively related to socioemotional wealth emphasis and negatively related to financial wealth emphasis. The results show that business age is positively and significantly related to wealth emphasis (β = 0.08, p < .05). Because lower wealth emphasis values are associated with a financial wealth emphasis and higher values are associated with a socioemotional wealth emphasis, this suggests that as a family business’s age increases, it places greater emphasis on socioemotional wealth and less emphasis on financial wealth. Therefore this finding supports Hypothesis 1.

In Table 2, Model 3 represents the test of hypothesis 2. This hypothesis states that in a family business, the level of socioemotional wealth emphasis will be positively related to trusting family advisors most, and the level of financial wealth emphasis will be positively related to trusting professional advisors most. The results show that wealth emphasis is positively and significantly related to family advisor most trusted (β = .09, Wald = 5.63, p < .05). Because lower wealth emphasis values are associated with a financial wealth emphasis and higher values are associated with a socioemotional wealth emphasis, this suggests that when a family business emphasizes socioemotional wealth more, it is more likely to select family members as the most trusted advisors. Conversely, as a family business emphasizes financial wealth more, it is more likely to select professional advisors as the most trusted advisors. Therefore this finding supports Hypothesis 2.

In Table 2, Models 1 to 4 represent the test of Hypothesis 3, the mediation hypothesis. This hypothesis states that in a family business, the level of financial versus socioemotional wealth emphasis will mediate the relationship between the business’s age and the type of advisors who are most trusted. Following guidance of how to test for mediation (Baron & Kenny, 1986), we first regressed the final variable (advisor most trusted) on the initial variable (business age). The results are shown in Model 2. Then we regressed the mediating variable (wealth emphasis) on the initial variable (business age). The results are shown in Model 1. Then we regressed the final variable (advisor most trusted) on the mediating variable (wealth emphasis). The results are shown in Model 3. Finally we regressed the final variable (advisor most trusted) on the initial and mediating variables (business age and wealth emphasis). The results are show in Model 4. For mediation to occur, there should be a significant relationship between business age and the most trusted advisor variable that disappears or diminishes when wealth emphasis is entered into the equation. Because Model 2 shows that there is not a significant relationship between business age and the most trusted advisor variable (β = .05, Wald = 1.31, p > .05), there is no relationship to mediate. Therefore this finding does not support Hypothesis 3.

Discussion

This study addressed the question “Does a family business’s age influence which type of advisors it trusts more—family or professional advisors?” We developed three hypotheses based on SEST to address this research question. The results did not support a direct relationship between a family business’s age and the type of advisors who are trusted most. But, the results did support the hypothesized relationships between a family business’s age and wealth emphasis, and wealth emphasis and the type of advisors who are most trusted. Two out of three hypotheses were supported. In terms of the unsupported hypothesis (that the level of financial vs. socioemotional wealth emphasis would mediate the relationship between the business’s age and the type of advisors who are most trusted), this study’s lack of support may be a result of a distal relationship between business age and the type of advisors who are most trusted, and the lack of sufficient control variables used. Although the direct relationship that was proposed between business age and the type of advisors who are most trusted was not found, we are encouraged that the proposed indirect relationship based on SEST was found. In consideration of these findings, this study makes three contributions.

Contributions

First, this study makes a contribution by introducing SEST to the family business literature. In preparing for this study, we read the foundational SEST literature and we searched for papers that mentioned SEST or cited the main SEST articles. We found no mentions of SEST in the family business or general business journals. Owing to the growing recognition of the importance of socioemotional wealth in family business, we believe that SEST has much to offer to the study of family businesses. In particular, we believe that SEST might help explain how socioemotional wealth in family businesses relates to family member decision making and behavior. We also believe that SEST could explain many decisions that family business leaders make during ownership and management successions. For example, the use of nonfamily CEOs in family businesses has been examined and explained using various theories (e.g., agency theory, resource-based theory, stewardship theory). But the prioritization of emotion- or knowledge-related goals that SEST predicts has not been considered as a determining factor for family business leaders in decision-making processes. Given the recent attention paid to the importance of socioemotional wealth in family businesses, we believe that it may be fruitful to revisit studies that seek to explain particular behaviors by family business leaders to better understand how time and/or goal constraints may have affected their decisions (e.g., succession decisions, employee selection and promotion decisions, financing decisions, business growth decisions). When family business members face goal constraints, particularly socioemotional wealth-related constraints, SEST may help explain how they make decisions. Examples of such constraints might include when a family business leader who wants his or her business to continue learns that none of his or her children want to enter the business, and when sales losses threaten the continued existence of the business.

Second, this study makes a contribution to the SEST literature by extending the theory from the individual to the organizational level. In our search of the SEST literature, we found no articles that applied or discussed SEST as a group- or organization-level theory. The main premise of the upper echelons literature is that businesses are made of individuals, and the strategic choices of the individuals are reflected in, and attributable to, their businesses (Hambrick & Mason, 1984). In writing about the importance of understanding individuals within organizations, Felin and Foss (2005) wrote, “To fully explicate organizational anything—whether identity, learning, knowledge or capabilities—one must fundamentally begin with and understand the individuals that compose the who, specifically their underlying nature, choices, abilities, propensities, heterogeneity, purposes, expectations, and motivations” (p. 441). We agree, and believe that because SEST predicts individual behavior based on motivations, further examination of SEST at the organizational level is warranted.

Third, this study also contributes to the family business advising literature by highlighting factors that may influence the selection of the most trusted advisor. By categorizing advisors as family or nonfamily members, the study shows that psychological factors and time-related factors may dissuade family business owners and managers from following the best practice of using outsiders when attempting to professionalize their businesses (e.g., Songini, 2006). To make a family business more professional, owners and managers are advised to hire outside advisors who can help them create more professional governance and human resource policies and practices (Yildirim-Öktem & Üsdiken, 2010). This functionalist perspective of professionalization suggests that outsiders will expand the diversity of perspectives for the family business’s dominant coalition, and will increase the business’s ability to compete in the marketplace. This study shows that as family businesses age, an emphasis on socioemotional wealth increases; as socioemotional wealth emphasis increases, family businesses tend to place greater trust in family advisors. Considering the family business professionalization best practices (Songini, 2006; Yildirim-Öktem & Üsdiken, 2010), it seems that this trust in family advisors could reduce the likelihood that professionalization processes will be successful.

Limitations and Future Research

The findings of this study should be interpreted in light of several limitations. First, we note that interpersonal trust may be context specific in terms of tasks (Johnson & Grayson, 2003). For example, regarding an issue relating to pollution control and regulatory compliance, a business leader may trust individuals associated with a government agency more than family members who do not have knowledge of regulations. Therefore who is most trusted may depend on the context. Additionally, although we controlled for industry at a broad level, we did not consider differences in tasks that might influence the type of advisors that family businesses most trust. For example, a software development business that uses contracted information systems consulting might trust consultants most. Future research could examine differences between family businesses’ most trusted advisors depending on the nature of the business’s main tasks. In other words, the industry could be a deciding factor.

Second, we did not examine the level of trust that family businesses place in family business specialty consultants. The number of consultants who specialize in advising family businesses has grown as accountants, lawyers, and others have recognized that family businesses often have different goals and values than nonfamily businesses (Strike, 2012). If these specialty consultants recognize and value the nonfinancial goals of family businesses, these consultants might well be among the most trusted advisors. Future family business advisor research, therefore, should take family business specialty consultants into account.

Third, there may be error in how we measured the dependent variable. The level of trust placed in family advisors, was based on respondents’ replies to the item, “Who are your most trusted business advisors? Please rank your top three.” Although we assigned ordinal values of 3, 2, and 1 to the highest, second-highest, and third-highest ranked advisor categories, these values may not capture the relative values that respondents would have placed on their trust levels with their advisors. Moreover, the AFBS item may have been misleading. Respondents might have answered differently if they had been asked, “To whom do you go for advice most often?”

Fourth, we used several one-item scales in this exploratory study, which may have reduced variables’ content validity and led to low R2 values. For example, we measured wealth emphasis with respondents’ answers to a single question. Berrone et al. (2012), however, proposed a measure of socioemotional wealth that is formed by five subconstructs, which are each measured by several items. Therefore our one-item measure of wealth emphasis may have neglected many of the facets of what wealth emphasis truly entails. Future researchers who examine socioemotional wealth emphasis may wish to use more robust operationalizations than we have used in this study.

In terms of future research, we suggest four areas that build on this study. First we note that there are a number of factors business leaders consider when evaluating business advisors. These factors include the price of the advice, the amount of interaction time required, the advisor’s communication style, the nature of the task for which advice is being sought, and the degree to which the business leader is comfortable having his or her norms challenged (Bennett & Robson, 2004). Future research could examine how these factors affect the usage rates and expectations that family business leaders have when consulting with advisors. Do these factors and expectations, in turn, affect the level of trust that the leaders place in the advisors? Additional factors could be added to our model that may increase explanatory power in future research. Beyond the factors that business leaders consider when evaluating business advisors, bifurcation bias (Verbeke & Kano, 2012) and the strength of the family vision (Barnett, Long, & Marler, 2012) may also be of interest to researchers who want to build on this study.

Bifurcation bias refers to the default treatment of nonfamily members as agents and family members as stewards (Verbeke & Kano, 2012). When families have a strong bifurcation bias, it has the potential to create heterogeneous performance results because the labor pool is smaller and family members may take advantage of perquisites. A bifurcation bias may also alter the perceptions of family business leaders when selecting a family advisor (steward) versus a nonfamily advisor (agent). Coupling SEST with a bifurcation bias would seem to increase the likelihood of a family member being chosen as the most trusted advisor.

Additionally, the strength of the family vision may also play a role in the selection of family versus nonfamily advisors. Barnett, Long, and Marler (2012) indicate that a family business’s dominant coalition has a strong family vision when the members have a shared goal of transgenerational sustainability and a strong commitment to the family’s values. When a strong family vision exists, the leaders are more likely to select and implement socioemotional wealth goals (Barnett et al., 2012). We believe that future research should investigate how the strength of a family vision affects family business leaders’ willingness to trust nonfamily advisors who may not understand or appreciate the family’s vision. It may be that the strength of the family vision moderates the relationship between firm age and wealth emphasis.

Second, we note that in our sample, the CEO’s gender was negatively related to the level of trust placed in family advisors. This means that female CEOs were more likely than male CEOs to place high trust in family advisors. Cruz, Justo, and De Castro (2012), using a social embeddedness argument, found that family employment in family businesses led by women leaders was positively related to company performance. Combined, these findings seem to run counter to the social network finding that company leaders who sought advice from a narrow range of advisors like themselves were less capable of successfully addressing poor performance in their organizations (McDonald & Westphal, 2003). This contradiction would seem to provide an interesting area to study.

Third, we wish that we had access to financial and nonfinancial performance measures of the businesses in our study. We relied on previous research (McDonald & Westphal, 2003) to address the consequences of selection of a family or a nonfamily advisor. But it would have been better if we had been able to examine relationships between the amount of trust that family business leaders placed in family advisors and their companies’ performance. It would be interesting to know if categories of business advisors within the overall group of nonfamily advisors have a tendency to change nonfinancial performance results. For example, does trusting professional advisors the most reduce nonfinancial performance such as family harmony?

Fourth, one of the results of this study, that family businesses place more emphasis on socioemotional wealth and less on financial wealth as they age, begs the questions of whether family businesses experience other changes in preferences over time, and whether this change in emphasis occurs gradually over time or as the result of critical events. Researchers have recently called for more studies of the temporal dimensions of family businesses (Sharma, Salvato, & Reay, 2014). Based on this article’s findings that age influences emotional goals (i.e., socioemotional wealth), SEST may prove useful in explaining other family business behaviors over time. Specifically, we believe that investigating how the change in financial versus socioemotional wealth emphasis occurs over time in family businesses, and what other preference changes may occur with age, would be fruitful avenues of exploration for future researchers. The potential changes in age may also be important to consider at the individual level.

From the perspective of SEST, the age of the founder, length of tenure in the business, and the amount of time left prior to succession or retirement could shift his or her goals. This shift could then alter the family business’s decision-making process for a number of critical activities, including succession decisions. For example, the selection of a family versus a nonfamily member to become the next CEO may be partly explainable by SEST; and the length of time prior to the succession event may change the perceptions and goals of the current CEO when considering who would be the most likely successor to the position. Furthermore, the length of a CEO’s tenure may affect his or her choice of goals.

Conclusion

This study explored factors that influence the selection of a family business’s most trusted advisor. To explain these relationships, we applied SEST and suggested that business age influences the types of goals a family business perceives as most salient. We discovered that business age relates to a socioemotional wealth emphasis within family businesses and that a socioemotional wealth emphasis relates to a family member being viewed as the most trusted among the business’s advisors. In all, these findings suggest that family business research may benefit from applying SEST to other family business research questions.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.