Abstract

In this study we explore how the institutions of kinship and commerce are integrated within family businesses. Previous research shows that family firms’ characteristic synthesis of institutional logics often unravels during intergenerational successions; however, it remains unclear how this process can be arrested, or by whom. Through inductive analysis, we offer a novel insight: outside advisors can act as surrogates for family in this integrative role. Specifically, we identify fiduciaries—professionals with special client obligations—as key actors in preserving family firms’ viability as commercial enterprises and kinship groups. Our findings contribute to theories of family businesses, professions, and institutions.

Introduction

How are the core social institutions of family and commerce integrated within family businesses? The institutional logics perspective has identified entrepreneurial founders as originating the distinctive blend of commercial and kinship logics known as “family capitalism” (Fairclough & Micelotta, 2013, p. 75). That institutional integration, along with continuity of leadership and control by members of the kin group, sets family business apart from other enterprises. An emergent research stream has shown how this integration is created by adjudicating among the demands of the kin group and the economic best interests of the firm (Miller, Le Breton-Miller, Amore, Minichilli, & Corbetta, 2017; Miller, Le Breton-Miller, & Lester, 2011). Through synthesis of the competing institutional logics, a distinctive hybrid emerges with competitive advantages over purely commercial enterprises (Pache & Santos, 2013). Ideally, kin group members in subsequent generations maintain this balance, but previous research has shown that this is not always the case (Miller & Le Breton-Miller, 2006; Stalk & Foley, 2012). This leaves key theoretical and empirical questions unanswered, such as: What happens when family firm leaders fail to integrate the logics of kinship and commerce?

Recent empirical research suggests that the institutional integration of many family firms begins unravelling from the inside during intergenerational leadership successions, including the departure of the founder. As one study summarized the recent findings, “Families’ commitment to entrepreneurship declines precipitously once control is passed from the founding to later generations” (Jaskiewicz, Combs, & Rau, 2015, p. 30). The kin group members who succeed to leadership often treat the firm as an extension of family relations, neglecting commercial considerations (Miller et al., 2011). This suggests that in familial succession processes, the logic of commerce becomes less tightly integrated into the family firm as one generation of kin group leadership succeeds another.

This leaves family business research with a gap in knowledge concerning how some firms continue to thrive as succession processes weaken the integration of institutional logics. Some studies have suggested that second, third, and subsequent generations of a business family can be taught an entrepreneurial ethic (Eddleston & Kellermanns, 2007), which could enable them to step into the integrative role and steward their family firms into the future. However, the practitioner literature indicates that such achievements are infrequent in the real world because such training is costly and time-consuming, and often fails (Colclough, 2009; Hughes, 1997).

This article’s distinctive contribution lies in identifying another group of actors, from outside the family, who can assume the integrative responsibilities and authority of successful kin group business leaders. Specifically, the study proposes that trusted family advisors (Strike, 2013; Strike & Rerup, 2016) can take on a task previous research has ascribed uniquely to family members: synthesizing the institutional logics of kinship and commerce. To make this argument, the article links the research stream on family business advising (Strike, 2012) to the broader domain of institutional scholarship on organizations. The latter includes a handful of studies that identify a subset of professional advisors, known as fiduciaries, whose distinctive characteristics may enable them to straddle the domains of family and business (Fairclough & Micelotta, 2013; Thornton, Jones, & Kury, 2005). However, that research has not yet moved beyond case studies examining individual professional groups within a single country. Given the increasingly multifaceted and transnational character of family business advising (Su & Dou, 2013), a broader inquiry into the role of fiduciaries is warranted.

This article’s analytical focus on fiduciary advisors points up another contribution to family business scholarship: Our study responds to calls for closer specification of individual agency, as opposed to interorganizational dynamics (Pache & Santos, 2010; Reay, Jaskiewicz, & Hinings, 2015), in “the blending of family and market logics” (Miller et al., 2011, p. 21). To this end, the article offers a grounded model of fiduciaries’ work in integrating the logics of family and commerce within family firms. The analysis identifies two sets of tasks that fiduciaries perform in family businesses where the competing institutional logics are beginning to disintegrate: rationalization and stabilization. Rationalization reorients the firm and its members so that the firm’s commercial viability and robustness are given appropriate consideration alongside the relational considerations of the kin group. Stabilization involves creating structures to ensure that integration will endure through challenges such as leadership transitions. This analysis extends recent work on the destabilization and restabilization of family firms (Carr, Chrisman, Chua, & Steier, 2016); to those findings, we add new insight on the significance of interventions by fiduciaries.

Finally, this article addresses calls to specify more closely the roles of third-party advisors in business families (Strike, 2013), and to integrate family business research more tightly with the literatures of other disciplines. The article does so by specifying a model of fiduciary advising to family firms, linking scholarship on family business advising to the institutional theory literature in organization studies. By drawing these two research streams together, this study makes a novel contribution: it identifies fiduciary advisors as key actors in creating the blend of commercial and kinship logics that underpin family firms, and models how this integration work is done. The analysis draws from multiple data sources, including interviews with 65 fiduciaries advising family firms in 18 countries; these interviews, along with a large trove of supporting archival data, were collected as part of an 8-year participant observation study by the first author. The unique data set permits an unusually broad global perspective on advising family businesses, attending to the “how, when, and why” questions that theory building must address.

The remainder of this article will review the relevant literature on family firms and institutional logics, the debates in institutional theory around integration and agency, and the role of fiduciaries. The methods section outlines the unusual empirical case, along with the multiple data sources and the analytical strategy used to develop the grounded process model. The findings section details the ways in which the logics of commerce and family begin to disintegrate within family firms, and how fiduciaries respond with actions designed to rationalize and stabilize the enterprises they advise. The discussion outlines the article’s key contributions, as well its limitations and the directions it suggests for future research.

Literature Review

Institutional Logics and the Family Firm

A long-standing theoretical question in organizational research has become increasingly important in family business scholarship: How do firms adjudicate conflicts among the multiple, often conflicting, institutional logics in their environments? Institutional logics are collections of rules, norms, practices, and “the deeply held and often unexamined assumptions by which reasoning takes place” (Thornton et al., 2005, p. 128). As organizing principles for thoughts, emotions, and actions (Fairclough & Micelotta, 2013; Friedland & Alford, 1991), logics influence both individuals and the organizations of which they are a part.

Social actors at all levels contend with multiple institutional logics in their environments (Thornton, Ocasio, & Lounsbury, 2012). This includes family businesses (Miller et al., 2017; Reay et al., 2015), which straddle two of the institutional sectors that organize societies the world over: the realm of family and that of commerce (Friedland & Alford, 1991). We define a family as a kinship group distinctive for the significance it accords to reputation and shared identity (Thornton, 2004), as well as to emotional bonds, traditions, reproduction, and paternalistic authority. A family business, in turn, is a hybrid formation in which a commercial enterprise is structured to benefit and “perpetuate the influence of a restricted group of relatives” (Fairclough & Micelotta, 2013, p. 75). It thus represents a “fusion” (Carney & Nason, 2016, p. 2) of commerce and kinship.

Yet we know little of how such firms find and maintain their position at the intersection of “family and capitalism” (Friedland, 2012). As one recent study described the current status of institutional logics research in the family business literature, “theory on how family firms approach multiple logics is currently fragmented and incomplete” (Jaskiewicz, Heinrichs, Rau, & Reay, 2016, p. 786). This fragmentation has contributed to the multitude of conflicting findings on the viability of family firms as business enterprises.

On one hand, the logic of commerce impels individuals and organizations to pursue profit, market dominance, rationalization, and efficiency; competition and meritocracy are assumed, as are opportunism and short-term contracting (Reay et al., 2015). On the other hand, the logic of family foregrounds emotional needs, social cohesion, and tradition; its core premises are loyalty, altruism, and the stability of long-term interactions among “kin and kin-like associates” (Fairclough & Micelotta, 2013, p. 88). In institutional theory, the two logics are often defined in opposition, as in a recent article that contrasts “the conventions and feelings of family . . . versus the objectified impersonality of business” (Friedland, 2018, p. 518).

Empirically, some studies indicate that the logics can be successfully blended (Miller et al., 2011); many others find that “family goals are regularly in conflict with commercial goals” (Jaskiewicz et al., 2016, p. 784). This is not just the interpretation of scholars but the experience of the kin group itself. For example, one study of Portuguese family enterprises found that individuals reported feeling “a profound sense of contradiction” (de Lima, 2000, p. 152) between the imperatives and assumptions of their business and kinship relations. This may contribute to the high failure rate of family firms, such that only 10% remain in family control through the third generation (Stalk & Foley, 2012).

In practice, the two institutional logics may conflict over issues of governance and strategy, where choices must be made between the well-being of the business as an economic enterprise and the well-being of the family as a social unit (Pérez-González, 2006). This includes issues such as nepotism or the use of business capital to fund personal consumption by family members. Similarly, the clash between family and commercial logics may play out in decisions about risks that could grow the business in the long run but jeopardize payouts to family members in the short run (Miller et al., 2017). Such clashes can create “devastating conflicts” that threaten family firms’ survival, particularly at times of generational transition (Jaskiewicz et al., 2016, p. 782).

Individual Agency and Institutional Integration in Family Business

Scholars have thus far taken a highly selective view of the actors positioned to manage this clash of institutional logics. This is part of a more general challenge faced by institutional research, which has historically neglected individuals and their role as agents of change and innovation (Friedland, 2018; Hallet & Ventresca, 2006). Within the family business literature, research has focused exclusively on family members empowered to act as the “man in the middle” (Miller et al., 2011, p. 9), blending the family and commercial logics. Furthermore, scholarship in this area has only developed far enough to consider how heirs diverge from the founder’s initial enactment of the integrative role.

Findings from those studies suggest that integration is not the dominant approach of a founder’s heirs. Instead, second- and third-generation CEOs often abandon the founder’s integration project. Some opt for detachment or segmentation (Jaskiewicz et al., 2016), so that commercial and family logics separately affect different aspects of family firm. Still others simply choose one logic or the other to dominate the firm going forward: Those who favor the commercial logic turn the firm over to nonfamily management or sell it outright to nonfamily owners; those who “did not think strategically about the business but instead made decisions based on family preferences” turned their firms into “lifestyle” accessories (Reay et al., 2015, p. 303). While these findings have considerably advanced theory on the multiple logics facing family businesses, it remains unclear how well the resulting models can generalize outside the domain of small, local enterprises—such as pharmacy or artisanal winemaking—on which they were based.

In medium- and larger sized enterprises, the logic of commerce may not be so easily banished or quarantined through segmentation, detachment, or prioritization of the family logic. In such businesses, higher capitalization and complexity (e.g., public trading of the firm’s stock) means that market forces play a much more significant role (Miller et al., 2011). Furthermore, firms doing business in more than one region or country are often under particular pressure to blend and hybridize institutional logics in order to solve problems and function effectively on a day-to-day basis: Clients and the market demand an integrated, customized approach (Smets, Morris, & Greenwood, 2012). Thus, for many family businesses, remaining a going concern under family control requires blending of competing logics.

This returns us to the question of who can play the “man in the middle” for business families. This article addresses the gap in knowledge by proposing that nonfamily members may also take on that role. In this way, the article answers a call that has not yet been fully addressed—one that demands more research on “the blending of family and market logics,” particularly “at the level of the individual actor” rather than at the level of organizational fields (Miller et al., 2011, p. 21). Since agency has been neglected in institutional research (Smets et al., 2012), making it a focal area here represents a distinctive contribution in comparison to other studies— which have primarily examined interorganizational dynamics (Pache & Santos, 2010; Reay et al., 2015)—and aligns this article with the original aims of institutional logics scholarship (Friedland & Alford, 1991).

The Fiduciary and Integration of Institutional Logics

Outside the literature on family business, a broader research stream on organizations offers insights on actors who can integrate competing institutional logics. These actors, known generally as “institutional entrepreneurs,” mobilize conflicts (Friedland & Alford, 1991) and work “across societal sectors” (Thornton & Ocasio, 2008, p. 129). In practice, that means institutional entrepreneurs create hybrids out of institutions that are otherwise “incompatible” (Sewell, 1992, p. 17) or discontinuous. One such hybrid is “family capitalism” (Fairclough & Micelotta, 2013, p. 75).

These actors are central figures in organizational theorizing because they link multiple levels of analysis, driving change in macro-level social institutions through micro-level problem solving; such efforts are often catalyzed by novel problems and crises in their everyday work tasks (Smets et al., 2012). This research has largely been overlooked in family business studies (Reay et al., 2015), yet it provides valuable insights for developing theory where we currently lack knowledge. Building on this work and linking it to the literature in family business can help address recent calls for more fine-grained attention to micro-level processes underlying change in institutional logics and business family relationships (Miller et al., 2011; Smets et al., 2012).

Of particular relevance is research on a special type of institutional entrepreneurs known as fiduciaries—a subset of professionals who help family firms thrive and endure as both kinship groups and profitable businesses (Thornton et al., 2005). Examples of fiduciaries include accountants, lawyers, corporate directors, and trustees. They are distinguished from other professionals by a special set of obligations to their clients. In addition to the baseline professional demands of expert authority, they are required to act with loyalty, honesty, and good faith toward their clients and to avoid any conflicts of interest (Parkinson, 2005). The law regards this role as akin to a sacred trust: Thus, breaches of fiduciary duty are punished more harshly than other types of professional misconduct (Boxx, 2012).

The neglect of fiduciaries in family business scholarship is particularly surprising since owners of family firms themselves are defined legally as having “a fiduciary duty to the business” (Daugherty, 2013, p. 66). This includes family business founders, as well as relatives who are majority shareholders; the courts have applied fiduciary standards to these individuals specifically to prevent any interpersonal conflicts among them from tainting the management of their common business enterprises (Osi, 2009). Most interestingly, the two defining features of the fiduciary standard are care and loyalty: terms that also characterize the idealized family relation (Thornton et al., 2012). In this context, care means prudence in business dealings, and loyalty means “unselfishness [and] the duty to refrain from exploiting the relationship for personal gain” (Boxx, 2012, p. 239)—qualities readily transferrable to kinship settings.

This suggests that fiduciaries may be uniquely positioned among professional advisors to play the “man in the middle” role for family business clients. This is based on the close fit between fiduciaries’ norms and practices and the institutional logic of the family. The connection is literally spelled out in the law: Some jurisdictions define a fiduciary as a professional who must “observe the utmost good faith and act en bon père de famille” (Guernsey Trusts Law, 2007; http://hautevilletrustees.com/wp-content/uploads/2014/07/The-Trusts-Guernsey-Law-2007.pdf)—a French phrase that translates as “good father of a family.” The global impact of this norm is suggested by scholarly research from decades earlier in North America showing that in family businesses, “the fiduciary occupies, after the death of the family founder, the place of abstract patriarchal authority in a family” (Marcus & Hall, 1992, p. 70).

Thus, fiduciaries’ behavioral norms and special obligations as professionals position them at the boundary between the logics of kinship and commerce. While other professions have become dominated by the logic of commerce (Spence & Carter, 2014), fiduciaries represent an earlier era of professionalism, when integrity and reputation were paramount and expertise was used to assist clients rather than exploit them for profit. While their expert authority is compatible with the logic of commerce—being based on competence and a performance track record—their special obligations of loyalty, care, and selfless service align fiduciaries closely with the family logic. One recent study of fiduciary lawyers advising family businesses suggests that this alignment goes even farther, showing that fiduciaries advising family business in Italy become “quasi-family” members who “share their clients’ emotive, personal concerns and develop . . . affective commitment” (Fairclough & Micelotta, 2013, p. 81). These fiduciaries are linked to their clients not merely by a sense of professional obligation or dependence on payment for services but also by affective ties akin to that of relatives.

These findings are highly suggestive, but research on fiduciaries remains very narrow in focus—limited to case studies of individual professions in individual countries, such as American accountants (Thornton et al., 2005) and Italian lawyers (Fairclough & Micelotta, 2013). It remains unclear whether these findings can be generalized. By extending inquiry to other kinds of fiduciaries, across multiple national settings, this study will contribute to theory in this area, in addition to its primary objective of analyzing the actors and mechanisms underlying the integration of kinship and commercial logics in family firms.

Method

Research Setting

The theorizing in this article is based on a longitudinal study of wealth managers: fiduciaries who specialize in protecting business families’ wealth. These professionals serve the world’s “upper crust” of 15.4 million individuals with US$1 million or more in net worth (Cap-Gemini, 2016). The clients derive most of this wealth from ownership and management of their family firms (Carney & Nason, 2016). Such families typically call on fiduciaries when the institutional integration of the firm begins to decline, such as when family business members “overemphasize relationship concerns at the expense of business concerns” (Gómez-Mejia, Cruz, Berrone, & de Castro, 2011, p. 690). This sometimes occurs when the founder steps down (Marcus & Hall, 1992; Miller et al., 2011), while in other cases the problem does not become critical until the second or third generation (Le Breton-Miller, Miller, & Steier, 2004; Miller & Le Breton-Miller, 2006).

Because of their clients’ wealth, these fiduciaries constitute an elite subset of business advisory professionals. Between the relatively small numbers of practitioners, and the formidable barriers to accessing them for research purposes, scholarship on fiduciary wealth managers is rare. While their services would not be accessible to many family firms, the profession represents one of the “unconventional contexts [that] are useful for examining understudied processes and phenomena” (Strike & Rerup, 2016, p. 901).

Specifically, fiduciary wealth managers’ work sheds light on the dynamics of business families operating in a global environment. Client families are typically residents and citizens of multiple countries, with business interests and assets spread across the world (Beaverstock, Hubbard, & Short, 2004). Fiduciary wealth managers provide such families with a global strategy for preserving and protecting those assets; this usually involves using offshore financial centers to create trusts, holding companies, and foundations to shelter family firms from taxation, bankruptcy claims, divorce settlements, and disputes over inheritance and succession (Harrington, 2016). Most practitioners are trained as lawyers or accountants; what distinguishes fiduciaries is not just what they know—a particular skill set relevant to elite business families—but how they practice, with honesty, loyalty, and the fiduciary duty to put clients’ interests above their own. These fiduciary demands contribute to the unusual mix of socio-emotional skills and technical expertise that characterizes wealth managers’ work (Harrington, 2017).

Data Collection and Analysis

Data collection for this study extended over almost 8 years, beginning in November 2007 and ending in July 2015. Multiple data sources from complementary perspectives were used in order to reduce bias, enhance validity, and triangulate findings. The reliability and robustness of the analysis are further supported by the first author’s “prolonged engagement” (Creswell & Miller, 2000) with fiduciaries, over nearly a decade of participant observation and interviews. As part of a larger study of the profession, the first author spent 2 years training to gain formal certification as a wealth manager, followed by the first author’s participation in three international professional society meetings, each attended by hundreds of practitioners. The events took place in San Francisco (focused on business families in North and South America), Hong Kong (focused on Asian business families), and Johannesburg (focused on African and Indian business families). Enrolment in or completion of the wealth management credential course was a formal prerequisite for attending the professional society meetings.

The courses and professional society meetings were organized by the London-based Society for Trust and Estate Practitioners (STEP). STEP is the main professional body for wealth managers worldwide, representing 20,000 members in 95 countries, and its certification course (leading to the TEP credential obtained by the first author) is the global standard in the profession. The program involves about 500 course hours and generally takes about 2 years to complete for individuals in full-time employment. The first author’s coursework took place in Switzerland, Liechtenstein, and the Cayman Islands. Each of the five courses involved different groups of students: in attendance were 10 to 15 practicing wealth managers from various firms. Though all were established in their fields, with 2 to 15 years of experience as fiduciaries, they were enrolled in the credentialing course at the request and expense of their employer firms. While fiduciary wealth management has a centuries-long history (Harrington, 2012), the formal credential is a relatively recent innovation. Many wealth management firms consider it a signal of professional respectability to employ fiduciaries who have earned the industry standard credential; therefore, many made it mandatory for practitioners to enroll in the STEP courses.

The first author’s strategy of immersion in the professional training and development of fiduciaries was necessary to overcome the considerable barriers to access surrounding elite professionals generally, and advisors to wealthy business families in particular. Recent studies of family business advisors have noted the difficulty of accessing these professionals and their extreme reticence in the face of outsiders’ inquiries (Strike, 2013; Strike & Rerup, 2016). As part of their special responsibilities, fiduciaries are required to maintain tight discretion (Marcus, 1983); in some jurisdictions, they may face civil and criminal penalties for breaching client confidentiality (Parkinson, 2004). To avoid running afoul of these obligations, most wealth managers simply refuse to speak with researchers, journalists, or other outsiders. Most will not name their clients, even to other wealth managers (Strike & Rerup, 2016); this foreclosed the possibility of gathering data from practitioners’ client families. The profession has thus acquired a reputation for being “tight-lipped” and “gun-shy” (“Shells and Shelves,” 2012). Long-term ethnographic immersion is often the only method available for gaining access to such guarded and wary groups (e.g., van Maanen, 1973).

While the first author never practiced as a fiduciary family advisor, obtaining the credential and attending professional society meetings provided access to highly detailed information on the family business advisory process that was not available through other means. The first author’s extended engagement with the world of fiduciary work was, like other accounts informed by insider experience, “invaluable in capturing subtle, often confidential relational and psychological issues” within professional practice that would otherwise remain inaccessible to researchers (Salvato & Corbetta, 2013, p. 238). Thus, while the data set obtained was one-sided—representing only the perspective of the fiduciaries—it was also exceptionally rich, illuminating the experiences of practitioners in a wide variety of cultural and business settings.

The first author was able to probe the nature and challenges of fiduciary family business advising both through interviews and by observing the questions and challenges that conference and course participants shared with each other. The courses and meetings provided three mechanisms of data collection: 65 interviews with practitioners in 18 countries, which produced 645 pages of transcripts; participant observation in the meetings and training courses, the latter of which yielded more than 3,000 pages of course texts for analysis; and archival materials, including over 1,200 pages of content from the meetings in San Francisco, Hong Kong, and Johannesburg. To this was added another rich source of archival material on business families: 8 years’ worth of the STEP Journal, ranging from 2007 through 2015; this data trove contained more than 5,500 pages of articles, focused largely on family business issues.

Semistructured Interviews

The practitioner interviews represent the primary data source for this article. The cross-national research design was driven by the multiterritoriality (Beaverstock et al., 2004) of wealthy business families, which was linked to institutional variation in the logics of commerce and family. All participants in this study were fiduciaries specializing in advising wealthy, multinational business families. The interviews were conducted with the fiduciaries’ knowledge of the researcher’s identity and institutional affiliation, as well as their consent to participate in a research project.

The 18 interview sites included most of the world’s major financial centers, including Switzerland, Liechtenstein, Hong Kong, Singapore, Mauritius, and the following British Crown Dependencies and Overseas Territories: Guernsey, Jersey, the British Virgin Islands, and the Cayman Islands. Some interviews were also conducted in the newer, up-and-coming financial centers such as the Seychelles, which serve clients in Asia and Africa. None of the participants consented to be taped during the interviews, so their responses were recorded by the first author typing on a laptop, at the rate of approximately 75 words per minute. Interviews typically lasted 90 minutes, with a range of 30 minutes to over 3 hours. This yielded 645 pages of interview transcripts. Since the aims of the study were inductive, the interview questions sought to elicit variation and consistency in areas such as the challenges of working with wealthy, multinational families, as well as the kinds of services fiduciaries provide and the nature of their relationships with clients. The interviews did not seek to explore institutional logics in the family firm; the role of fiduciary advisors in relation to those logics emerged as part of our analysis, detailed below.

As Table 1 indicates, the sample was unusually diverse. Participants ranged in age from late 20s to late 60s, and included five major racio-ethnic groups drawn from 19 nationalities. In terms of gender, women were very well represented in this sample compared to similar studies (e.g., Strike, 2013) but still remained in the minority at 29%. Like most elite professions, the demographic composition of wealth management is mostly White and male.

Characteristics of Interview Sample (N = 65).

This study acknowledges the problematic nature of classifying people by race and ethnicity. For example, the category “Black” in this context includes people who identify as African American, Afro-Caribbean, Seychellois, Mauritian, and bi- or multiracial. In this sense, grouping interview participants is bound to be inaccurate and reductive as a means of capturing their multifaceted identities. However, within the context of the broader demographic information provided here, information about race and ethnicity may be helpful—particularly since a majority of interview participants mentioned that culture and identification play a significant role in the establishment of trust between professionals and their clients.

Data Analysis

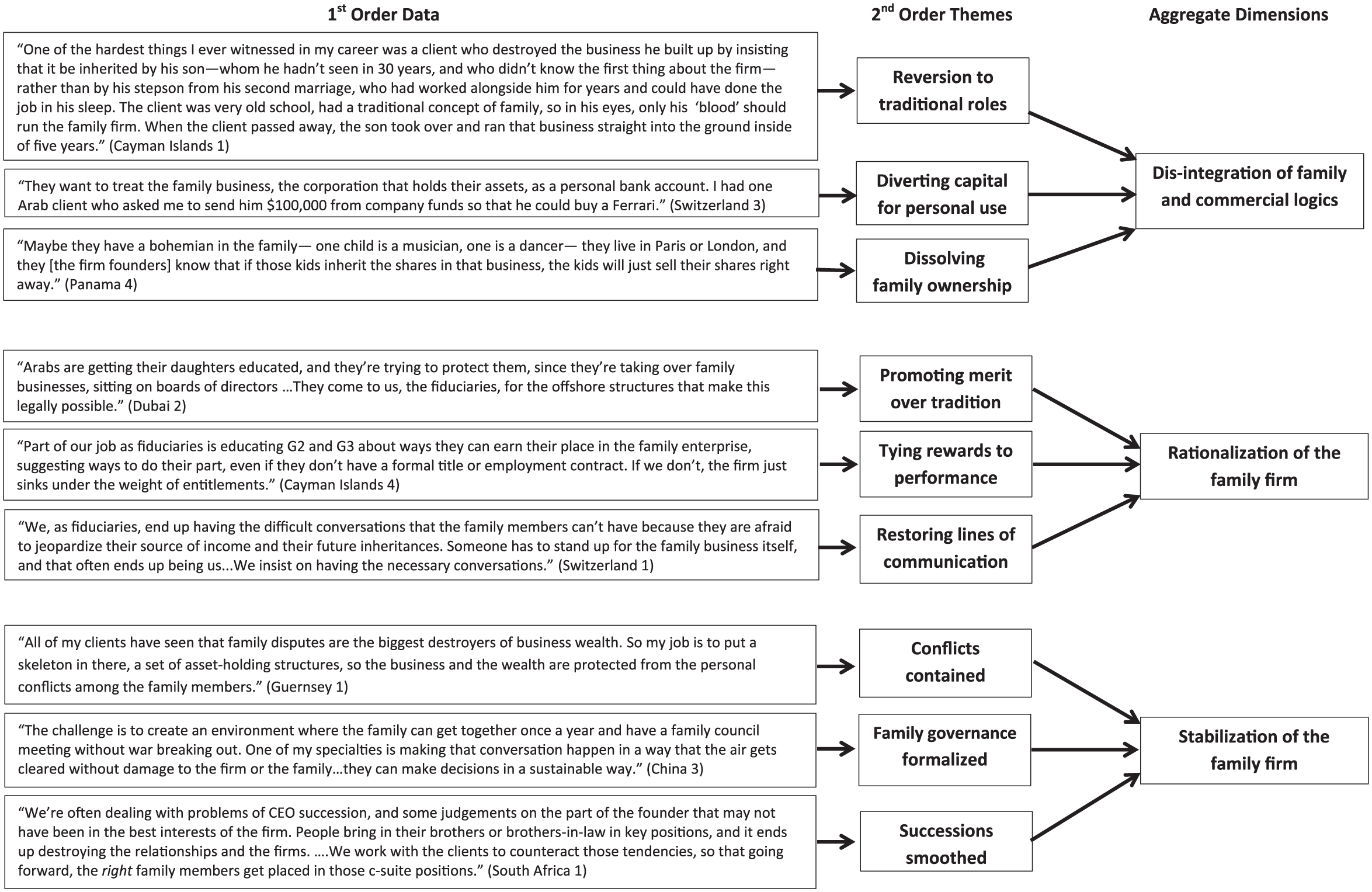

We chose a discovery-oriented interpretive approach (Locke, 2011), in which the “insider” perspective of the first author and the interview participants was countered by the second author acting as a critical outsider and devil’s advocate. We analyzed the data inductively: The goal was not to develop hypotheses but rather to interpret processes and meanings created by fiduciaries adjudicating institutional logics in their advisory work (Gioia, 2004). Step 1 was a first-order analysis that brought together the fiduciaries’ accounts to create a highly detailed, textured view of the family and commercial logics in the business families they advised. The analysis was also sensitive to the ways fiduciaries developed their understandings of these logics, and used them as guidance in forming their own lines of action. This addresses recent calls for methodology that sheds light on “how specific people take specific actions” (Strike & Rerup, 2016, p. 888).

Next, we developed a second-order analysis, in which we searched for major themes in the data and compared them with concepts from the literature. In particular, we searched the data for themes linked to the family and commercial logics that governed fiduciaries’ work with client families. Thus, from the first-order raw interview data, we drew out patterns of regularity and variation to lift the data to the level of theory. This led to the development of aggregate dimensions in Step 3.

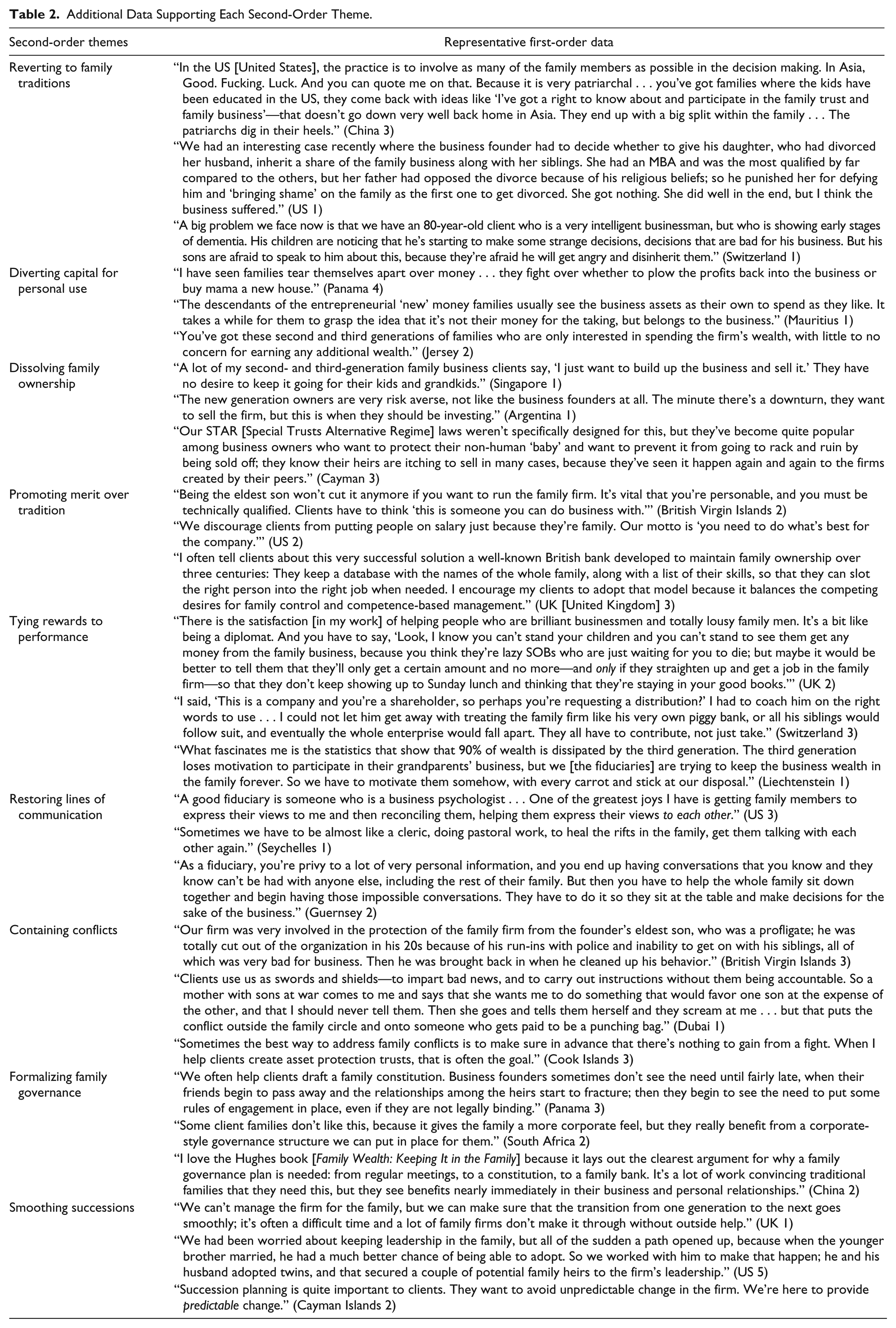

Figure 1 illustrates the relationship among the three parts of the analysis, using examples to show how we moved from the first-order data provided by fiduciaries to the second-order themes we developed, and ultimately to the aggregate dimensions. Further substantiating evidence for the second-order themes we identified can be found in Table 2. While Figure 1 does not represent a causal model, the relationship of the themes we discovered in iterating through the data analysis led to the development of the grounded model specified in the next section.

Data structure.

Additional Data Supporting Each Second-Order Theme.

Our analysis was subjected to member checks: Three participants commented on and critiqued the analysis, pointing out flaws and suggesting new insights. While all qualitative research involves an irreducible element of subjectivity, this research process offers some reason for confidence in the findings, despite the study’s limitations.

Findings

The findings are organized around the specification of three processes: the disintegration of the family and commercial logics in family firms, catalyzed by intergenerational succession processes; efforts at rationalization of the family firm by the advisors; and finally, stabilization of the family firm by the advisors.

Dimension 1: Disintegration of Family and Commercial Logics

Intergenerational successions often precipitate the unravelling of integrated institutional logics in the firm (e.g., Miller et al., 2011). While it was never described in the scholarly language of institutional logics, the theme of disintegration arose throughout the interview data, as well as in the STEP Journal and STEP professional development programs. Speakers at professional society meetings repeatedly brought up the challenge of families in which a kin group leader stepped down, leading heirs to orient the business away from commerce and toward serving the personal agendas of the family members. The fiduciaries interviewed for this study highlighted three activities they observed among their business family clients that seemed to hasten the internal disintegration process: reversion to traditional family roles, diverting capital for personal use, and dissolving family ownership of the firm. These become central challenges for the professionals to address.

Reversion to Traditional Family Roles

Many of the fiduciaries interviewed for this study said that generational transitions in leadership often led to a change in the relationships among a business family’s heirs: Their interactions centered more on their ties as relatives than as partners in a firm. This could mean reverting to patterns of deference based on traditional authority, rather than competence: Thus, male relatives and older members of the family acquired outsized significance in decision making, regardless of their knowledge and experience. As one New York-based fiduciary described what he’d seen in 30 years of practice,

As soon as a leadership vacuum emerges at the top, the eldest sons and uncles—who may have been off doing their own thing for years—come out of the woodwork to tell the rest of the family how to run the business, despite having zero claim except their membership in the “lucky gene club.” And it almost never ends well. (US 2)

Sometimes the process begins with the very first leadership transition, initiated by the family business founder himself or herself. Several participants in this study indicated that they had watched as founders became more tradition-oriented on reaching the end of their working lives. This led, in some cases, to decisions that seemed to undermine the founder’s own work of integrating the family and business logics. As a fiduciary working in Hong Kong explained,

One of my clients in China is an 84-year-old man whose daughter has worked with him for decades in the family business. This in itself is unusual. Men of his generation don’t usually bring their daughters into that kind of authority position. But what’s really strange is that he arranged to completely exclude her from inheriting anything of that business when he dies; only his sons will get shares. And he asked me recently what I thought of this. Of course I think it’s a terrible idea, and I have been trying to convince him to give his daughter an equal share—she’s earned it, and she knows more than any of the boys do. But I had to answer him very diplomatically and say that while his decision was not consistent with my culture, I understood why he had done it, because traditionally Chinese daughters were always the financial responsibility of their husbands; women never stayed unmarried and self-supporting, so there was no tradition of women inheriting. So now it’s me versus Chinese culture! (China 1)

By bringing his daughter into a senior leadership position, the founder established a way to integrate the logics of commerce and family: employing a close relative but on the basis of her competence rather than as a result of sheer nepotism. Yet the founder’s own succession plan would undo this integration, aligning the business firmly with the logic of family by passing ownership exclusively to males, in conformity with Chinese tradition.

Although this was a source of both puzzlement and alarm to the fiduciary, the professional literature we used as a secondary source for this study indicates that such behavior is neither uncommon nor unique to family firms in China. These data suggest that founders may put new emphasis on their family roles as a way of asserting traditional authority over a firm’s future. As a STEP Journal article explained,

It is particularly difficult for first-generation entrepreneurs to give up “their baby.” They are often scared that their children might destroy the business. Sometimes the founder may see a rival in their offspring, and sometimes pure ego and the desire for power drives them to stay on too long. Sometimes the founder hands the management to the next generation, but retains ownership control . . . Unfortunately, this ownership control is often used as a tool to steer, control or influence the next generation. The greatest fear of parents is the loss of power. (Hillerström, 2012, p. 35)

When founders begin to see a firm primarily as “their baby,” rather than as a business enterprise, their own relationship to institutional logics changes. Rather than taking a “man in the middle” position, family firm leaders of the first and subsequent generations may opt to accentuate their role as parents—and the traditional, unquestionable parental authority that comes with that role—rather than considering the best interests of the firm. This creates a problem for the fiduciary to solve.

Diverting Capital for Personal Use

While reversion to traditional family roles may occur while the founder of a firm is still alive and in charge, several other threats to the integration of institutional logics are distinctly more common in the later generations of a family business. This includes the propensity of some kin group members to derive their income exclusively from the proceeds of their relatives’ work in the family firm. A specialist in Latin American business families described this as one of the biggest challenges he faces in his day-to-day work:

One of the other issues that comes up regularly is where you’ve got family members who have been used to living from trust funds or family foundations [which hold profits from the family firm] and don’t have any other purpose or “raison d’être.” (Uruguay 1)

This is such a common problem that it merits several mentions in the TEP training course textbooks. For example, one passage alerts fiduciaries to the threat posed by clients “using a company in the manner of a money box, or as a glorified bank account for the personal use of the client” (Parkinson, 2006, p. 35).

The reasons for concern were elaborated in the interviews, which made clear that excessive diversion of capital from the family firm for personal use created both economic and social problems. Economically, family members’ demands for a share of the firm’s profits may damage a company’s competitiveness by limiting funds available to invest in the business; the more capital paid out to support family, particularly those not working in the firm, the less can be applied to growth and innovation. In addition, cash-strapped enterprises are more vulnerable to dissolution following economic downturns or other external shocks. One fiduciary in Johannesburg described the challenge as one in which “there are really two classes of family members: one set that builds the firm and the other that bleeds it dry—and often the latter group wins” (South Africa 4).

Socially, the “idlers” are often resented by the “workers” supporting them; at the same time, those not involved in the family business may become suspicious that their working relatives are purposefully withholding proceeds from the firm. As reported in a recent STEP Journal article,

In one family, many members were concerned that their family enterprise seemed to generate no profit to distribute to the family members; they distrusted the competence of the third-generation family leaders. . . . Since family members often depend for all or part of their livelihood on family resources, their lack of knowledge can lead them to feel anxious and unsafe, leading to conflict. (Hauser & Jaffe, 2015, p. 75)

As that case illustrates, the disintegration of institutional logics in a family firm may not create a crisis until the third generation or later. This often catalyzes the decision to bring in external experts to mediate the family feud. In other words, to the extent that family firms are treated as sources of capital for private use by the kin group, the business is decreasingly integrated with the logic of commerce. Such events create the boundary conditions for outsiders like fiduciaries to enter as advisors to the family firm.

Dissolving Family Ownership

An even greater existential threat to the family business lies in the prospect of it relinquishing family control. Though it is not always normative or desirable to maintain family ownership, its loss represents a definitive dissolution of the integrated commercial and kinship logics. The fiduciaries interviewed for this study suggested that the desire for continuity of family firm ownership is widely shared among their clients who are entrepreneurs. At the same time, a variety of forces work against this cohesion over time.

Lack of interest in the family business is a common driver of heirs’ impulse to sell. A practitioner in one of the leading Caribbean offshore financial centers explained,

I’ve had clients, entrepreneurs, tell me “This firm will never be up for sale—it will still be around for my grandchildren’s grandchildren.” They love the idea of dynasty. And generally, their immediate family humor them about it. But once that founder is gone, all bets are off. The heirs generally can’t wait to cash out and play golf. (Cayman 3)

In other words, the heirs are not engaged at all with the logic of commerce or keeping their family in business. Their interest begins and ends with making the firm serve their needs as a kin group.

In addition to lack of interest in the business, there may be a question of aptitude: Not everyone is able to engage in the risk-taking and long-term planning necessary for entrepreneurial success. As a recent STEP Journal article pointed out, some heirs simply “are less financially astute” than others and “might be forced to sell their share” as a result (FitzGerald, 2016). The STEP Journal, along with TEP course textbooks, is replete with advice on how breakup of family ownership can be avoided, particularly through the use of special legal and financial tools, such as offshore purpose trusts (Parkinson, 2005). But such tools are of little use without the cooperation of family members who perceive the risk accurately. A fiduciary in Channel Islands related the case of a family business leader:

He didn’t want the four children knowing how much the firm was worth. “There will be chaos,” he said. He had built up quite a bit of wealth and he didn’t want them to know. So he died, and now there is chaos, because they [the children] are fighting with each other. They want to sell the business now, rather than keep it running. They’ve been to court twice now, and they are depleting the firm’s money. (Guernsey 2)

Such lack of anticipation that heirs may not share current leaders’ interests or aptitude for business creates a third major challenge for fiduciaries employed by family enterprises.

Dimension 2: Rationalizing the Family Firm

As the previous section indicated, the dissolving integration of institutional logics in family firms frequently produces a lopsided outcome: dominance of the family logic in those firms, and declining commercial viability. To counteract this, fiduciaries sought to rationalize their clients’ businesses. This meant making the firms less family-like and more corporation-like in three ways: by promoting merit over tradition in hiring and promotion, by tying rewards to performance, and by restoring clear lines of communication that had been obstructed by interpersonal conflict. These activities offset the increasing hold of the family logic on these businesses, moving them back toward integration with the logic of commerce.

Promoting Merit Over Tradition

Even when family businesses want to operate in a businesslike way, cultural and legal impediments may make it difficult for them to do so. Several participants in this study mentioned that clients from countries with strong traditional cultures wanted to run their firms on a more contemporary commercial basis but were often frustrated by local meanings and practices linked to the institutions of business and family. In some Latin American countries, for example, tradition dictates that family business ownership and management roles be passed to the next generation regardless of their interests or qualifications. This is the case even when, as one Panama City practitioner put it, “The kids may not want to ‘asuciar los manos’ [dirty their hands] with the family business, especially if it’s grown up around something like agriculture” (Panama 4).

To reassert the influence of the commercial logic in such cases, fiduciaries are brought in to create legal structures that ensure that merit and motivation trump traditional family entitlements:

They want to keep the firm in the family, but it has to be a business, not just a toy for their kids to play with. I am brought in to realize this vision—to make sure only the kids with the interest and qualifications inherit the business. (Panama 4)

Fiduciaries can protect the business through means that are not readily available to a business family’s members—for example, fiduciaries can establish offshore trusts and foundations that put restrictions on the ways that ownership changes hands. Ultimately, these put legal limits on the degree to which the logic of family can influence the family business.

Fiduciaries’ ability to use the law as a tool for imposing meritocracy is particularly important when the family business is based in countries governed by legal regimes that prioritize a traditional family hierarchy of entitlement. The problem is particularly acute in regions governed by Shari’a law, where billions in family business wealth are allocated after the founder’s death by religious courts that give nearly all inheritance rights to male heirs; not only are female heirs severely disadvantaged but all males inherit equally, regardless of age, qualifications, or contributions. According to a fiduciary working with clients in the region:

The eldest son of a family, who helps build the family business, may be resentful of his baby brother—son of wife number four or something—who, under Shari’a law, will get an equal share of the family fortune, and an equal decision-making role, despite having done nothing to build the company. So I talk with the family members, including the founder when possible, to create a solution. That often means putting the whole company in an offshore trust, so that management and shares can pass to the most qualified of the children, rather than the traditional heirs. We just take the traditions out of the picture by moving offshore. (Switzerland 2)

In some settings, law and tradition can draw family firms more deeply into the institutional logic of family, even against the wishes of some family members. The fiduciary in this case must draw the firm back into the realm of commerce, whose logic—as the STEP Journal puts it—holds that ownership and management “should be awarded based on competence and merit rather than emotion” and that “a chip off the old block isn’t always the best solution” (Evans, 2012).

Tying Rewards to Performance

Many fiduciaries interviewed for this study identified as one of the biggest challenges the process of setting conditions for access to the monetary rewards of family firms. The fiduciaries saw their role in these situations not as controlling the purse strings but as inducing a shift in the attitudes and behavior of family members. As one fiduciary put it,

You do get kids who are driving around in Lamborghinis who are being supported by the entrepreneurial efforts of other family members. . . . I tell them that if they want access to the family business resources, they have to have a role as a contributor to that business. It doesn’t even have to be a full-time job, but they actually have to show up to family meetings and act like responsible owners. (China 4)

In essence, this fiduciary is asking the younger members of the business family to reframe their relationship to the firm in terms of the logic of commerce, rather than the logic of family. This alters the basis on which family members feel “entitled” to the proceeds of the business, so that they must integrate the firms’ commercial interests into their thinking, alongside their own personal needs.

As we discovered in the analytical process, the reasons fiduciaries give for promoting such a shift include both relational and economic benefits to the family firm. On one hand, linking business rewards to performance can avert interpersonal conflicts and resentments within the family by better aligning the logics that animate the Lamborghini drivers with those governing relatives actively involved in management of the firm. In addition, this contributes to the long-term economic survival of the business. As a fiduciary in the Channel Islands explained,

The most tax-advantageous position for a family firm is often to employ family members rather than just handing out distributions. That can sometimes create fights among beneficiaries, because those not involved in the family business may complain that their interests are being compromised by family wealth being paid out as salary to those who are employed in the family business, so that those funds don’t flow into the trust, but get “diverted” into salaries. But that’s what’s best for the business; it’s not a charity. (Jersey 1)

Taking these long-term considerations of economic viability into account is another distinctive contribution of fiduciaries to the family businesses they advise. Family members, especially those not involved in the day-to-day workings of the firm, may never consider the tax implications of their decisions. By looking out for the best interests of the firm itself, by positioning it as favorably as possible in relation to tax laws and other economic opportunities, the fiduciary reasserts the integration of the logic of commerce into the firm’s activities.

Restoring Lines of Communication

Within business families, relationship considerations—such as sibling rivalries or traditional hierarchies—can impede communications necessary to the effective management of the firm. Rationalization in this context means restoring the family’s ability to exchange information and work together; this task often falls to the fiduciary. In this sense, the fiduciary’s status as an outsider can be an advantage, allowing him or her to take a nonpartisan stance in conflicts and advocate for the best interests of the business itself.

In some cases, our analysis found that fiduciaries had to initiate difficult conversations that challenged traditional authority relations. For example, one fiduciary found it necessary to push back on the decision of one of his oldest and wealthiest clients, insisting on reopening a line of communication that the client wanted to shut down:

One 82-year-old guy decided to disinherit his son because the son asked for a bit of his inheritance ahead of time; the father said “My son doesn’t want to work anymore.” That was his only child, so we had to have a long talk to help him understand what this would mean for the firm, and reopen the dialogue . . . there was going to be civil war in the family, and the whole future of the company’s management would be up for grabs. (Panama 1)

The fiduciary in this case took no position on the justice or the emotions invoked by the client’s decision but instead approached the issue by reorienting the client to the logic of commerce.

Other participants in the study reported that rationalization and restoring communication within the business inevitably required a component of emotional work. In fact, several fiduciaries independently used the term social worker to describe their relationship to some business family clients. As a practitioner in London explained,

Part of my job is social worker—I do deal with some tricky families . . . I was working with a family that was very complicated: several marriages, several children, including a suicide. One of the kids was pretty flaky and not in a position to engage in management, but the other two were already managing the firm. I advised the two in management positions to have a frank talk with the third one about his status, which prompted the excluded one to have a cry-on-the-shoulder talk with his mother, and aired out long-standing issues in the family, resulting in the excluded one dropping his plans for a massive lawsuit against his siblings. I kept them out of court and a ruinous battle for the firm. (UK 3)

In this, as in other cases we analyzed, the business interests of the family were put at risk due to communication breakdowns. Things left unsaid as a result of relational hierarchies or other emotional issues conflicted with the commercial aspect of the family firm, in which open exchange of information was essential. The fiduciary in this case was able to reassert the influence of the commercial logic by persuading the family to break the communication impasse, averting a destructive legal-financial problem for the business.

Based on the archival material we analyzed, these examples from the interview data reflect a common challenge for fiduciaries serving family firms. A STEP Journal article attributed this to traditional family hierarchies that make it difficult, or even taboo, to express certain ideas:

There is often a very large communication gap between the first generation founder (in particular the father) and the children. In practice it is very common to hear second generation family members explaining they are not able to talk to their father (or mother) about succession . . . They want to maintain family harmony and avoid conflict, so the third party advisor is brought in to say what they cannot say themselves. (Stewart, 2010, p. 29)

As the “third party advisor,” the fiduciary has enough distance from culture and family tradition to initiate difficult conversations, while also being enough of a trusted intimate to be heard and taken seriously. She or he can thus catalyze a restoration of communication by turning the attention of client families back to their common interests in the economic viability of their firm. This reasserts the influence of the commercial logic and contributes to its reintegration with the logic of family.

Dimension 3: Stabilizing the Family Firm

Once a fiduciary rationalizes a family business through the three means discussed above, the question of robustness arises: how long can the improvements to the firm’s functioning endure? The goal is to create a more robust and enduring integration, less vulnerable to changes in leadership, and—according to the fiduciaries interviewed for this study—less easily disrupted from within. Thus, we defined this dimension of the data by its focus on stability, which meant putting structures and processes in place to maintain the blend of institutional logics that allowed the business to go forward as both a social unit and a functional economic enterprise. The fiduciaries’ key stabilization activities were containing conflicts, formalizing family governance, and smoothing family firm succession processes.

Containing Conflicts

Our analysis showed that, in the eyes of fiduciaries, family firms are highly susceptible to destructive interpersonal conflicts among kin group members. Dimension 1 of Figure 1 lists three of the major sources of such conflicts. Numerous articles in the STEP Journal are devoted to discussing these issues and how best to manage them. One representative essay explains that in addition to the many external challenges facing any business, in family firms “the ‘enemy within’ needs to be considered. Putting it bluntly: how you can stop the family from pushing the self-destruct button?” (Colclough, 2009, p. 51).

Most of the fiduciaries interviewed for this study took a containment approach. That is, as long as lines of communication among family group members remained open enough to permit the business to function and avoid acute flare-ups of conflict (see Dimension 2), the fiduciaries did not seek to intervene in or resolve interpersonal disputes. Instead, they used their legal-financial expertise to contain or head off conflict whenever possible. As a fiduciary in Johannesburg put it,

The thing I really enjoy is mediation between family members—particularly between family members who have gone to war with each other . . . that’s where the creation and management of complicated family structures made up of layers of trusts and offshore corporations come in, to structure those relationships and contain the conflicts. You can’t quarantine the business from the interpersonal nastiness, but you can render the conflicts harmless to the firm. (South Africa 2)

Although this fiduciary used the term mediation, which implies helping the family members talk through their differences, his actions were in fact oriented toward structural solutions. He prompted enough dialogue within the family to learn the contours of their disputes, then set up offshore trusts and corporations to protect the firm from them. Though not empowered to resolve the familial conflicts himself, what this fiduciary found satisfying was the way in which the structures he created could prevent the client family from further harming itself, relationally and economically.

This echoes the pragmatic orientation of other fiduciaries interviewed for the study, as well as of the advice offered in professional society publications. For example, a STEP Journal article echoed the view of many practitioners that conflict in family firms is inevitable because of the intimate link between personal relationships on one hand, and money on the other:

There are instances where it is necessary to contemplate how the family business might need protecting from the consequences of unhappy marriages in the family, or from beneficiaries in other difficulties. We know that a trust may have some asset-protection value on divorce . . . A prenuptial agreement can be another line of defense. (Washington, 2013, p. 31)

In this article, as in the interview data, the fiduciaries’ focus was consistently on harm prevention and stability for the long term, rather than on conflict resolution or emotional closure. There is no suggestion that the fiduciary can prevent family members from divorcing or falling into financial difficulties, only the intention that the family business can be preserved in the face of such threats by careful containment strategies. As a fiduciary in Singapore put it, she concluded after 20 years of practice that “there was no substitute for iron-clad prenups and purpose trusts to ensure that a family business survives its own family” (Singapore 2).

Formalizing Family Governance

Given the frequency of conflict in business families, a related challenge is getting those families to agree on ground rules for decision making and action—particularly concerning highly charged issues surrounding management control, allocation of resources, and risk. Stabilizing the firm, in this case, means helping the family create a set of procedures and rules that members can accept as legitimate, and provide regularity to family business interactions. This can be done through very simple agreements that catalyze problem solving by the client families themselves, as described by a fiduciary in the Channel Islands:

I’m trying to build consensus by having regular meetings, then I encourage clients to develop family governance arrangements that can be implemented by subsequent generations. (Jersey 2)

The key phrase here is “by subsequent generations,” since the goal is a long-term, predictable order to family business relations.

The task is particularly urgent with clients who have created successful businesses quickly, disrupting family dynamics with a sudden influx of wealth and new responsibilities. According to a practitioner in Dubai,

For the super-wealthy, the only thing that drives them to make a plan is that their wealth is usually tied up in a business they created. They want to see it—along with their name and reputation—survive into the future . . . they see what happens to families that try to improvise, to get along without any governance plan, and how easily their enterprises come crumbling down. Suddenly they get very interested in wonky bureaucratic things like having a family constitution or having someone take minutes at family meetings. (Dubai 3)

As this comment suggests, formalizing governance in family firms means inserting elements of bureaucracy. When a fiduciary helps a family business client implement regular meetings, or a family constitution, kin relations are put on a more corporate or commercial basis.

In other words, facilitating the creation of family governance structures entrenches the logic of commerce in a context of family relations; this stabilizes the integration of the two logics by making rules and procedures do the work, rather than a specific leader, who will eventually step down. A STEP Journal article makes this connection more explicitly:

Good governance is just as pertinent in the family world as it is in the corporate world . . . Implement a formalized governance structure. Centralize and create a streamlined reporting structure . . . [to] ensure the family continues to own and control the family business. (Colclough, 2009, p. 51)

In this sense, what the fiduciary achieves through formalizing governance in client firms is a kind of “corporatization” of the family. While this does not override kinship bonds, it overlays them with some structural features normally considered distinctive to bureaucracies, creating a blend of logics that can remain robust across generational transitions.

Successions Smoothed

Our analysis found near-universal concern about the vulnerabilities created by generational successions within family businesses. Succession planning is the topic of over 800 STEP publications. So essential is this task that, as one fiduciary in New York put it, “A good fiduciary must by definition by a good succession planner” (US 4).

As with conflict containment and family governance, fiduciaries’ emphasis was on making legal and financial structures do the work, rather than making processes dependent on individual leadership. As a STEP Journal article concluded, “Structure can help make succession seamless” (Evans, 2012). But the selection and creation of these structures foreground the added value of the fiduciary’s expertise, since solutions are not one-size-fits-all. For example, family business leaders may decide that only some heirs should succeed to ownership and management of the firm, while others may be entitled only to its proceeds. This requires a careful selection of legal and financial strategies, as a fiduciary in Mauritius explained,

If you’re looking at passing wealth over several generations, then more often than not, a trust would be more suitable than a corporate structure. But if you want to have a structure for transferring management of a trading enterprise, you’d be better off with a corporate structure. So with a family business, we take the trading enterprise and wrap it in a trust, so you get the best of both worlds. (Mauritius 3)

Making these selections and combinations among alternative structures is a key way in which fiduciaries add value for business families, particularly when assets and kin group members are dispersed across multiple countries and legal systems.

Another aspect of the succession process to which fiduciaries must be attentive is the complexity involved in choosing which family members succeed to the firm’s leadership. Such decisions are embedded in a context of particular interpersonal ties with their own histories; this makes it difficult to generalize or apply standardized solutions. A fiduciary in London explained that legal and financial expertise alone are insufficient to address succession challenges because

all of this is about families. If you were just a rich businessman without a family, you wouldn’t have any issues: You wouldn’t care about inheritance taxes or trusts. But when they have kids, all of the sudden, they care a lot about passing their business to their kids—and protecting it from their spouses. Then they start hiring people like me to make sure the firm will endure for the long term: that the right family member gets put in the CEO chair, that the person is well prepared to take on that responsibility. (UK 4)

This combination of technical expertise with consideration of interpersonal issues lends fiduciary work its special character and its ability to integrate competing institutional logics of commerce and family. This blend of skills allows fiduciaries to do what most other professionals cannot: step into a role usually occupied by family members. As a fiduciary in Dubai summarized her relationship to clients, “You have to be very business-like, but also family-like” (Dubai 2).

Discussion

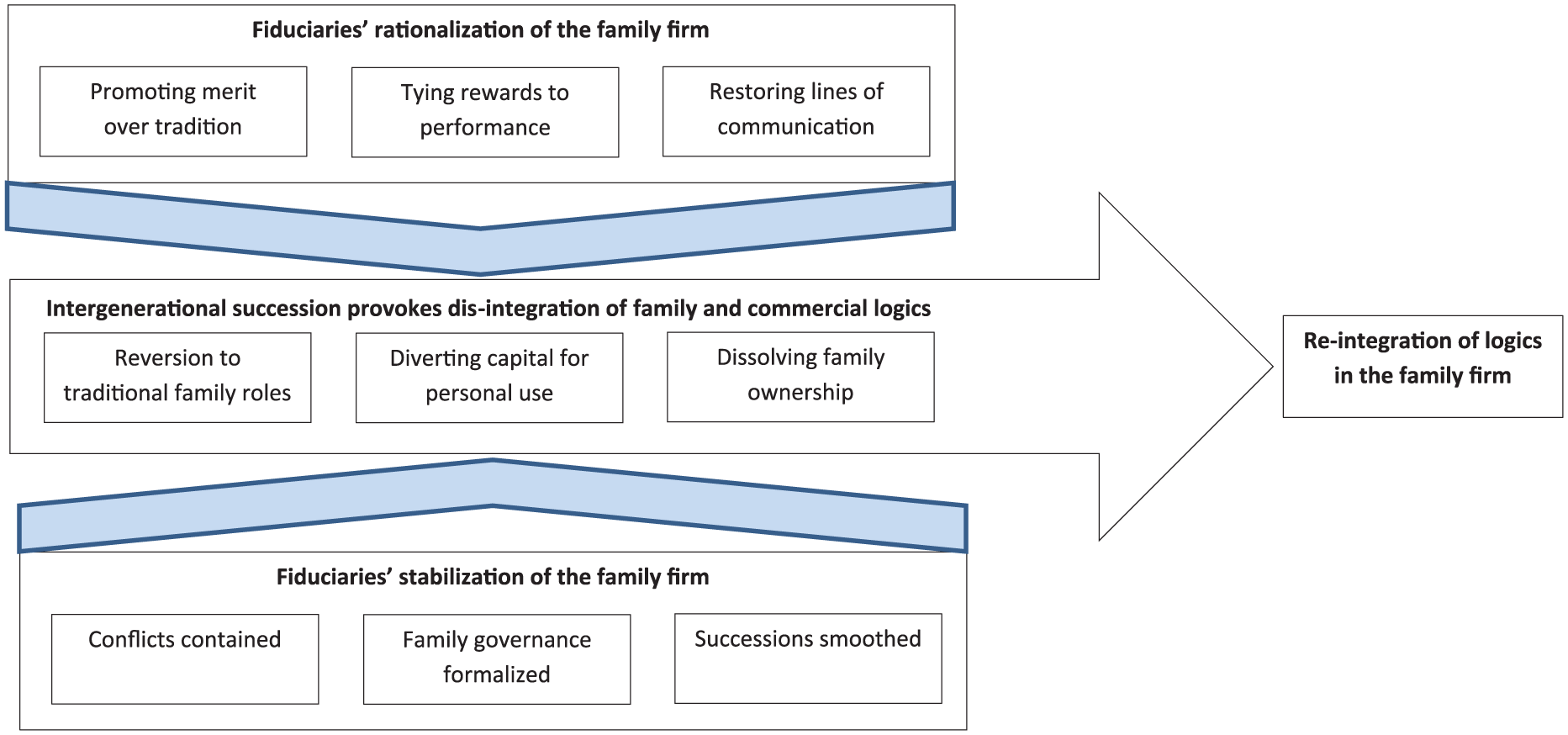

Based on the analysis offered above, we brought together the three aggregate dimensions of our analysis into a grounded causal model, as shown in Figure 2. The model shows how fiduciaries reestablish the integration of family and commercial logics, enabling firms to remain economically viable. In the center of the model (Dimension 1 in Figure 1), business families make decisions and engage in activities that weaken the integration of logics; this represents the independent variable in the model. At the top and bottom of the model, fiduciaries take actions to rationalize the family firm (Dimension 2 in Figure 1) and stabilize it (Dimension 3 in Figure 1); these represent the intervening processes in the model. The dual action by fiduciaries results in reintegration of the family and commercial logics, representing the model’s dependent variable.

An emergent model of fiduciaries’ reintegration of family and commercial logics in family businesses.

As our analysis showed, many family firms begin unraveling from the inside at times of intergenerational succession—including, but not limited to, the founder stepping down. This is consistent with findings of previous studies, such as those showing second- and third-generation kin group members treating the business as a personal “money box,” or liquidating their ownership stake altogether due to lack of interest or skills (Jaskiewicz et al., 2016). In addition, we found that family firms can begin disintegrating through reversion to traditional family roles and hierarchies, which often run counter to the commercial interests of the business. Our findings here align closely with earlier research showing that family firm leaders can find it difficult to get past traditional parent–child interaction norms with a son or daughter who is also an employee; this research also illustrates how sibling rivalries and other “dysfunctional behaviors of family members” can cause family firms to “fail or incur performance problems and corporate scandal” (Kidwell, Kellermanns, & Eddleston, 2012, p. 504). For example, a classic sibling rivalry between the Gucci brothers nearly bankrupted the famed Italian fashion company (Gordon & Nicholson, 2008). Such intrafamilial dynamics can dissolve the synthesis of institutional logics that made the firm viable.

Our model shows how integration can be restored to fractured family firms through the intervention of expert advisors. We found that their work puts family firms on a more businesslike basis, and stabilizes them through the use of legal and financial structures that make the firms less dependent on the actions of any particular leader. This occurs in part through the process of “rationalization” (Weber, 1949), which involves helping family firms adopt characteristics ordinarily associated with rationalized nonfamily corporations. To help family firms operate more like commercial enterprises, trusted advisors emphasize efficiency, meritocracy, and bureaucratic structures; they also supplant traditional forms of kin group relations with formal governance mechanisms for promotion, remuneration, and communication.

In addition, these trusted advisors stabilize the integration of institutional logics so that firms will be less dependent on a “man in the middle” and less vulnerable to changes in leadership. Our findings in this area are consistent with previous research on the destabilization and restabilization of family firms, particularly around leadership transitions (Carr et al., 2016). To these findings, we contribute new insight by specifying the role of the fiduciary and the component actions involved in the restabilization process. Our data show professional advisors stabilizing family firms with structures created to contain conflict, formalize family governance, and smooth succession.

In other words, fiduciary wealth managers use their expertise and position of trust to create structures—such as offshore corporations—that substitute for and mimic the integrative role of successful kin group leaders in the family firm. Such strategies have been credited with the long-term preservation of many well-known family enterprises. For example, the endurance of the Rockefeller family business, which began with oil and is now primarily in financial services (Morrell, 2017), has been attributed to structures set up by fiduciary wealth managers, such as the family office.

Contributions to Knowledge and Practice

Our inductive model is the product of an analysis that innovates by linking research on family business advising to the broader field of institutional scholarship on organizations; in this respect, we answer calls to integrate family business research better with the literatures of other disciplines. Specifically, we bring in institutional logics (Jaskiewicz et al., 2016; Miller et al., 2017; Reay et al., 2015) and analyze how an elite subgroup of professionals integrate them. We show that these professionals, known as fiduciaries, can step into the “man in the middle” role identified in previous research (Miller et al., 2011) as responsible for producing the distinctive blend of institutional logics that characterize family businesses. This finding represents a novel contribution to theory, since it shows for the first time that nonfamily members can take on this key aspect of a successful family business leader’s authority (Miller et al., 2017). In addition, our model advances scholarship by specifying how fiduciaries enact the integration of institutional logics, maintaining the commercial viability of the family firm while simultaneously facilitating its coherence as a social unit. Thus, it responds to calls in previous research to analyze and substantiate the relationship between family businesses and their most trusted advisors (Strike, 2013).

This article also represents the first attempt to examine fiduciary professionals’ role in family businesses outside the realm of a single profession or national context (Fairclough & Micelotta, 2013; Thornton et al., 2005). The findings of the study suggest how the concept of fiduciary duty can be useful in linking the analytical contexts of family business scholarship and institutional research. This is because fiduciary work by definition straddles the realms of family and commerce. As a result of their special obligations, fiduciaries create a kind of “personal capitalism,” as opposed to the purely “managerial capitalism” of the commercial domain (Thornton et al., 2005, p. 135; see also Marcus & Hall, 1992).

In addition to the implications for scholarly research, these insights on fiduciaries suggest some “best practices” for family business advising. For example, when faced with destructive interpersonal conflicts among family members—whether as a result of traditional family roles (Kidwell et al., 2012) or because of disagreements over control (Jaskiewicz et al., 2016)—participants in this study found it most effective to pursue a containment strategy. That is, they did not mediate familial conflicts or seek resolution of them, perhaps because to do so might have given the appearance of partiality. Instead, in keeping with the fiduciary ethic, they focused on the best interests of the firm, both as an economic enterprise and a kinship group.

The practitioners’ favored practices for achieving this objective can be clustered into two sets of structural mechanisms. The first consist of structures external to the family firm—such as offshore trusts—that serve to decouple or distance potentially destructive issues from the day-to-day workings of the business. The second set of structures were placed inside the firm to create a businesslike accountability and regularity among kin group members; common approaches, mentioned both by participants in this study and in the practitioner literature (e.g., Hughes, 1997), included creating a family constitution and instituting formal criteria for employment and promotion. Somewhat surprisingly, these “best practices” were consistent across the many national and cultural settings in which this study’s participants worked.

Limitations and Directions for Future Research

As a study that draws on an unconventional context to shed light on neglected aspects of family business (Strike & Rerup, 2016), this article has a number of limitations, some of which point up avenues for further investigation. The main limitations concern the interview data: The 65 interviews with fiduciaries represent one side of a complex relationship, captured in onetime “snapshots.” Although our data set is very rich, encompassing perspectives from an unusually diverse range of practitioners in 18 countries, it has been affected by the problems of secrecy and access that obtain in studies of elites—particularly those connected with the ultra-wealthy and their advisors (Strike, 2013). The client perspective is not available to us, nor are the long-term data that would allow us to observe change over time in the relational dynamics between fiduciaries and family firms. By sacrificing depth for breadth of data collection, we may also have missed the impact of other institutional logics (Friedland, 2012) on family firms—a possibility implied by the effects of religion and culture in our data from the Middle East and Asia.