Abstract

We draw upon the mixed gamble perspective to investigate the entry timing decisions made by family firms in the context of cross-border acquisition (CBA) waves. We argue that family-controlled firms trade-off short-term SEW and financial losses in favor of long-term SEW and financial gains, while moving early in CBA waves. Findings suggest that family-controlled firms have a higher preference for early movement compared with nonfamily-controlled firms. Further, we show that founder’s presence on the board and acquirer’s superior performance amplifies the mixed gamble trade-offs, thereby strengthening the relationship between family control and early movement within CBA waves.

Keywords

Introduction

Extant literature highlights that family firms conduct strategic decisions by considering not only financial but also nonfinancial aspects, which are referred to as socioemotional wealth (SEW; Chrisman & Patel, 2012; Gomez-Mejia et al., 2007; Zellweger et al., 2012). According to the SEW perspective, family firms are considered loss averse (Gomez-Mejia et al., 2007), which explains their reluctance toward cross-border acquisitions (CBAs; Chen et al., 2009; Geppert et al., 2013). But how does this fit with the established literature that family firms have a long-term orientation (Chrisman et al., 2012; Sirmon & Hitt, 2003), which may motivate them to conduct acquisitions and gain long-term financial and SEW benefits (Gomez-Mejia et al., 2018; Hussinger & Issah, 2019)? This calls for reconciling the decision-making criteria of family firms by incorporating both SEW loss aversion and long-term orientation when explaining their acquisitive behavior. This theoretical challenge is particularly salient in the context of CBA waves, where the potential for SEW and financial gains/losses are associated with entry timing decisions.

CBA waves are defined as periods of intense acquisition activity which cluster in time and industry and are characterized by higher uncertainty and risks compared with domestic acquisition waves (Xu, 2017). These CBA waves provide a short window to acquire targets and attain a fit with the environment (Fuad & Gaur, 2019). Specifically, within waves, early movers have the opportunity to select the best targets, which not only leads to superior long-term financial performance (Fuad & Sinha, 2018) but may also provide SEW benefits to family firms. In contrast, studies show that CBA waves are associated with uncertainty and risks on account of institutional differences between the countries, and therefore early movers may experience financial (Xu, 2017) and SEW losses. Such mixed findings create a dilemma for family firms when deciding their entry timing strategies. While there is a burgeoning body of research on family firms’ acquisition behavior (Worek, 2017), we lack an adequate understanding of the trade-offs associated with short and long-term SEW and financial gains/losses encountered by family firms during entry timing decisions within CBA waves. In this study, we attempt to address this research gap.

Prior studies explain the acquisitive behavior of family firms by focusing on both SEW and financial wealth (Gomez-Mejia et al., 2018). This is because SEW and financial wealth dimensions are not fully fungible and often interact, which creates a dilemma for family firms to consider both their anticipated losses and potential gains while conducting acquisitions. Accordingly, scholars theorize a mixed gamble approach in which family firms consider a trade-off between potential gains and losses to SEW and financial wealth in their decision-making criteria (Gomez-Mejia et al., 2014). Family firms differ based on their levels of ownership and management in the business (Boellis et al., 2016; Liang et al., 2014; Ray et al., 2018). In line with prior studies, we classify family firms into two types—family-controlled and nonfamily-controlled firms. We refer to family-controlled firms as those where family members are involved in both the ownership and management of the organization, whereas nonfamily-controlled firms have family involvement limited to the ownership level (Alessandri et al., 2018; Dau et al., 2020; Schmid et al., 2015).

We argue that entry timing decisions within CBA waves are a mixed gamble strategy adopted by family-controlled firms by considering both short-term and long-term trade-offs in SEW and financial wealth. Early moving firms may benefit from selecting superior targets, which provides greater organizational fit and synergies between the target and the acquirer (McNamara et al., 2008), leading to long-term financial gains (Fuad & Sinha, 2018). Higher fit with the core family business results in long-term SEW gains related to family control, preservation of family routines, and transgenerational sustainability (Hussinger & Issah, 2019; Zellweger et al., 2012). However, while moving early in CBA waves, there may be some short-term SEW losses such as managerial diversion from the core business and disruption of existing routines due to integration processes (Hussinger & Issah, 2019). Additionally, CBAs involve high costs and resource commitments to overcome information challenges and integration issues between the target and the acquirer (Chari & Chang, 2009; Lebedev et al., 2015), which may lead to short-term financial wealth reduction. Hence, family-controlled firms’ long-term orientation may motivate them to trade-off short-term losses in favor of long-term SEW and financial gains and prioritize early movement in a CBA wave. In contrast, nonfamily-controlled firms attach lower importance to SEW and have a short-term orientation compared with family-controlled firms (Alessandri et al., 2018; Chrisman et al., 2012; Liang et al., 2014). This is because nonfamily-controlled firms are managed by professional executives, who have relatively short-term financial focus (Jaskiewicz & Luchak, 2013), and their compensation and tenure are linked to the financial performance of the firm (Block, 2011). Hence nonfamily-controlled firms would have a relatively greater focus on short-term financial wealth in their decision-making criteria. Given that there are short-term financial losses in moving early due to the costs involved in CBAs, nonfamily-controlled firms may have a lower preference for early movement compared with family-controlled firms.

Further, we investigate the moderating effect of founder’s presence and prior performance on entry timing decisions of family-controlled firms. Within family firms, corporate-level decisions such as acquisitions are strongly influenced by the behavioral motives of family principals (Defrancq et al., 2016; Feito-Ruiz & Menendez-Requejo, 2010; Miller et al., 2010). Founders are emotionally attached to family firms and are committed to their long-term growth objectives, thereby fundamentally influencing firms’ decision making (Brune et al., 2019; Gu et al., 2019; Le Breton-Miller & Miller, 2013). Hence, we argue that founder’s presence on the board shifts the decision frame in favor of moving early, where substantial SEW and financial gains exist, compared with family-controlled firms without a founder. Furthermore, prior performance has an important bearing on the strategic decision making of family principals on account of their strong focus toward ensuring firm survival (Berrone et al., 2012; Chrisman & Patel, 2012). When the performance of a family firm is better, the reference point shifts in favor of SEW gains (Gomez-Mejia et al., 2018), and firms may want to avoid the high risks of failure associated with CBAs, thereby amplifying the need for early movement. Hence, better performing family-controlled firms may have a stronger preference for early movement compared with poor-performing family-controlled firms.

We make three significant contributions to family firms’ literature. First, we explain the decision-making behavior of family firms by reconciling the short-term SEW loss aversion and the long-term orientation perspective in the context of CBA waves (Chrisman & Patel, 2012; Gomez-Mejia et al., 2014; Hussinger & Issah, 2019). We enlarge the mixed gamble approach by including the time orientation of SEW and financial gains/losses in the decision-making criteria of family firms while conducting CBAs. Our study thus provides a nuanced understanding of mixed gamble by examining financial and socioemotional trade-offs encountered by family firms while timing their entry in CBA waves.

Second, our study shows that the founder’s presence on the board of family-controlled firms may amplify their willingness to trade-off the short-term SEW losses for potential long-term SEW and financial gains. The commitment of founder towards transgenerational control and long-term financial well-being of the family business is associated with a higher preference for long-term SEW and financial gains over short-term losses (Kotlar et al., 2018), thereby accentuating the need to move early in CBA waves. This strengthens the early movement preference of family-controlled firms having a founder on their board compared with family-controlled firms without a founder.

Finally, we show that family-controlled firms with superior performance move early in a CBA wave compared with family-controlled firms with poor performance. This is because, in high-performing family firms, the potential financial gains become less attractive, and SEW considerations become important (Hussinger & Issah, 2019), especially in the case of risk-prone CBAs. Our finding attests prior studies on mixed gambles (Gomez-Mejia et al., 2018) and shows that superior performance shifts the decision frame of family-controlled firms from economic benefits towards SEW considerations, thereby strengthening their preference for early movement in CBA waves.

Theory and Hypotheses

Acquisitions and the Mixed Gamble Perspective

Prior research drawing on the behavioral agency model highlights the loss-aversion character of family firms, which makes them risk-averse while undertaking strategic decisions (Chrisman & Patel, 2012; Gomez-Mejia et al., 2007). Family firms exhibit a lower propensity towards acquisitions due to their desire to preserve SEW, such as family control and influence over the business, compared with nonfamily firms (L. Caprio et al., 2011; Chen et al., 2009; Geppert et al., 2013; Gomez-Mejia et al., 2018; Shim & Okamuro, 2011). This is because family involvement in the firm reinforces SEW considerations over financial benefits (Alessandri et al., 2018; Liang et al., 2014). Complementing the SEW loss aversion aspect, studies highlight that family managers also have a strong long-term orientation compared with nonfamily managers (Block, 2011; Jaskiewicz & Luchak, 2013; Sirmon & Hitt, 2003). Therefore, not conducting acquisitions may result in a missed opportunity for long-term SEW advantages. Acquisition literature provides evidence that family firms are active acquirers and have superior performance (Worek, 2017). Scholars also note that family firms may be myopic in their decision making and focus on short-term goals (Chrisman et al., 2012). However, their preference toward long-term strategic goals such as future well-being of the family and transgenerational control over the business may overcome their short-term focus (Gu et al., 2019; Sirmon & Hitt, 2003; Zellweger et al., 2012). Family firms with longer horizons, therefore, may prefer to undertake risky strategic decisions like R&D investments and acquisitions (Chrisman & Patel, 2012; Schierstedt et al., 2020). Hence, this juxtaposition of loss aversion and long-term orientation presents a dilemma to family firms, and may therefore consider not only affective but also financial implications of their decisions (Kotlar et al., 2018).

Scholars argue that the strategic decisions conducted by family firms should not be viewed as a choice between pure loss or pure gain (i.e., pure gamble) because these decisions entail both losses and gains simultaneously (Chrisman & Patel, 2012; Gomez-Mejia et al., 2014; Martin et al., 2013). Since a specific decision scenario involves the possibility of a trade-off between gain and loss, it is referred to as a mixed gamble approach (Cruz & Justo, 2017). Alessandri et al. (2018) show that the mixed gambles approach may not only be applied across family and nonfamily firms but is also applicable to study family firm heterogeneity based on different levels of family involvement in ownership and management. They show that family management and level of ownership influence the risk to SEW, thereby affecting their internationalization strategies. Accordingly, we argue that family-controlled and nonfamily-controlled firms may assign varying levels of priority to SEW and financial gains/losses while conducting CBAs.

Recent studies on acquisitions show that family-controlled firms trade-off short-term financial and SEW losses for long-term financial gains and transgenerational sustainability (Hussinger & Issah, 2019). Due to their long-term orientation and desire to preserve SEW, family-controlled firms want to pursue strategies having long-term benefits even at the cost of short-term sacrifices (Alessandri et al., 2018; Liang et al., 2014). Thus, family-controlled firms adopt a mixed gamble approach while conducting acquisitions. Extant literature highlights that when family-controlled firms decide to acquire, they tend to conduct related acquisitions and benefit from long-term financial and SEW gains (Hussinger & Issah, 2019). However, when family firm’s performance is below aspiration level, it lowers the likelihood of conducting related acquisitions (Gomez-Mejia et al., 2018). In this scenario, when the survival of the firm is at stake, family principals may prefer risk diversification through unrelated acquisitions. In contrast, nonfamily-controlled firms have a relatively short-term orientation which shifts the decision making in favor of short-term financial benefits (Alessandri et al., 2018). This is because managers in nonfamily-controlled firms primarily focus on short-term incentives such as bonuses (Jaskiewicz & Luchak, 2013), which are linked with the financial performance of the firm (Block, 2011). Moreover, the influence of the family on protecting SEW is reduced if they have only ownership stake in the firm and do not occupy decision-making leadership positions on the board (Alessandri et al., 2018). Therefore, nonfamily-controlled firms assign a relatively lower importance to SEW interests compared with family-controlled firms (Gomez-Mejia et al., 2014) and may behave differently while conducting CBAs.

Entry Timing in CBA Waves as a Mixed Gamble

We theorize that family-controlled firms and nonfamily-controlled firms may show divergent behavior while timing their acquisitions within CBA waves. Family-controlled firms decide their entry timing strategies by considering both SEW and financial gains/losses in their decision frame (Gomez-Mejia et al., 2014). Given their long-term orientation (Block, 2011; Sirmon & Hitt, 2003), family-controlled firms will prefer to move early in a CBA wave to gain both long-term SEW and financial benefits. Early movers in CBA waves have the opportunity to cherry-pick the best combination of targets compared with late movers, which provides greater synergies and better organizational fit (McNamara et al., 2008). Greater fit with the family-controlled firm’s existing core business is associated with greater SEW gains and fewer SEW losses (Hussinger & Issah, 2019). Also, family-controlled firms have an emotional attachment for their core businesses, technologies, and products (Gomez-Mejia et al., 2010). Participating early in a CBA wave helps family managers to select targets aligned to their core businesses, thereby increasing the firm’s SEW. Further, acquiring targets of choice in the early phase of the CBA wave also maintains family control and influence over the business in the long-term. Due to a higher fit, there will be a lower need to hire external managers, which maintains family control post the integration process (Gomez-Mejia et al., 2018). Hence, early moving family-controlled firms benefit from not only preserving their affective endowments on account of acquiring synergistic targets but also gain long-term SEW benefits due to greater organizational fit and transgenerational control.

However, despite moving early, there may be some short-term SEW losses in CBAs, such as diversion of family managers’ attention from their core business and temporary disruption to their existing business processes and routines due to restructuring and integration activities (Hussinger & Issah, 2019). This is because CBAs may involve acquiring targets in institutionally different countries, which may increase the need to realign and restructure businesses in line with the host country’s environment. CBAs may also require handling cross-cultural integration issues which may disrupt existing business routines. CBAs also require greater managerial attention in order to implement postacquisition activities in a culturally and institutionally different target country (Chari & Chang, 2009). This may put greater pressure on family managers and divert their attention from the existing family business. Also, external capital usage for conducting acquisitions may increase family firm’s dependence on outside entities and influence their decision making (Requejo et al., 2018). Hence, moving early in a CBA wave results in short-term SEW losses, which may be offset by the higher long-term SEW gains in terms of maintaining family control and influence, preservation of existing knowledge and routines, core business continuity, and transgenerational sustainability (Berrone et al., 2012; Zellweger et al., 2012).

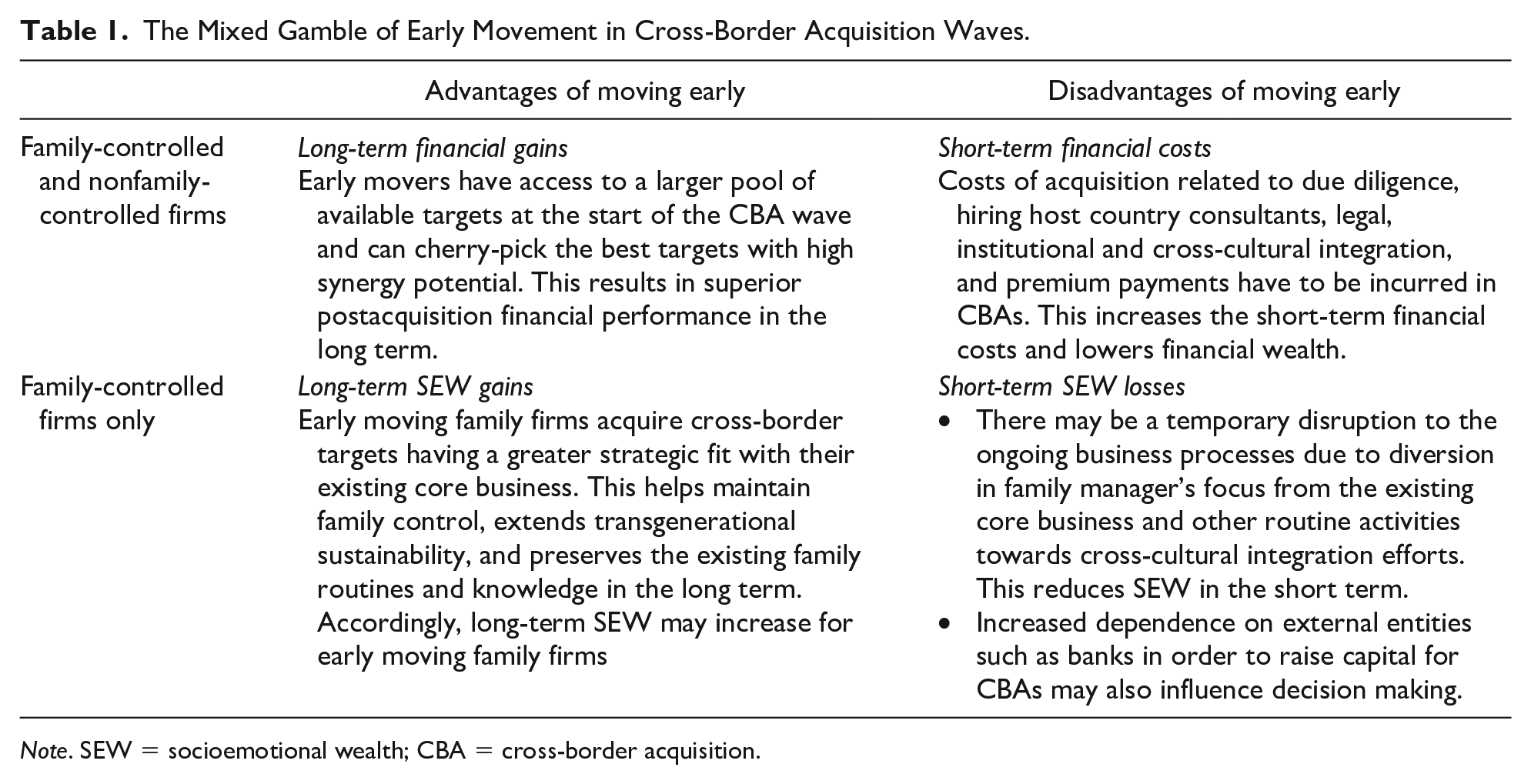

In addition, apart from the SEW gains and losses, there are financial benefits and costs involved in the long and short terms when participating in the CBA wave. Cherry-picking targets early in the wave lead to greater synergistic gains, which provide long-term financial benefits (Fuad & Sinha, 2018). However, there are some short-term financial costs involved in the CBA process, which may lower the financial wealth of the acquirer. These costs are related to the due diligence process, postacquisition integration, hiring of foreign consultants, and paying a premium to the target shareholders (Graebner et al., 2017; Welch et al., 2020). These costs become important while conducting CBAs because of increased information asymmetry and risks of adverse selection compared with domestic acquisitions (Xu, 2017). Such short-term financial costs are likely to be overcome in the long term when the financial synergies begin to accrue to the acquiring firm. We depict the SEW and financial gains/losses associated with the timing decisions in CBA waves in Table 1.

The Mixed Gamble of Early Movement in Cross-Border Acquisition Waves.

Note. SEW = socioemotional wealth; CBA = cross-border acquisition.

Taken together, acquiring targets in the early phase of the CBA wave would simultaneously increase SEW and financial wealth in the long term, yet there may be short-term SEW and financial losses. For family-controlled firms, the long-term SEW and financial gains due to greater synergies may outweigh the short-term losses in SEW and financial wealth, thereby motivating them to move early. In contrast, nonfamily-controlled firms would have a lower preference for SEW preservation along with a greater focus on short-term orientation (Alessandri et al., 2018; Liang et al., 2014). This is because external managers in nonfamily-controlled firms are less motivated by long-term SEW gains compared with short-term financial outcomes, as their compensation is tied to the financial performance of the firm (Block, 2011). As argued earlier, despite some potential long-term financial synergies from moving early, firms also face substantial CBA costs that are likely to reduce their financial wealth in the short term. On account of nonfamily involvement in management, the decision-making criteria of nonfamily-controlled firms is based on short-term financial wealth considerations, and a lower preference for SEW gains, compared with family-controlled firms. Hence, we argue that family-controlled firms would move early in a CBA wave relative to nonfamily-controlled firms.

Family-Controlled Firms and the Influence of the Founder

Founders play an important role in guiding the strategic behavior of family-controlled firms and are more committed to long-term growth objectives compared with later generations (Kelly et al., 2000; Schierstedt et al., 2020). Values and beliefs established by founders become institutionalized over time in the form of long-term goals, which may last across generations (Athanassiou et al., 2002; Lee et al., 2019; Schein, 1995). Due to their affective attachment to the family business, founders tend to preserve SEW in CBAs compared with successive generations (Brune et al., 2019; Haider et al., 2020). However, studies also show that the transgenerational orientation of founders results in a preference for long-term SEW and financial gains over short-term losses (Kotlar et al., 2018).

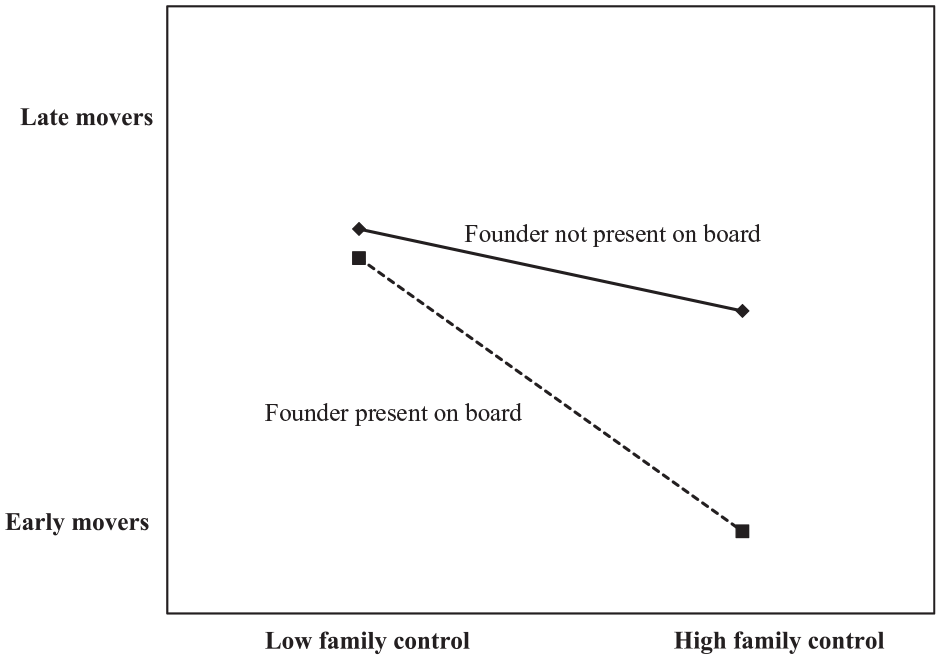

We argue that having a founder on the board would positively moderate and strengthen the preference of family-controlled firms to move early in the CBA wave compared with family-controlled firms without a founder due to the following reasons. First, founder’s presence on the board of family firms amplifies the need for long-term SEW and financial gains compared with family firms without a founder on board. This is because founders are more committed and motivated to ensure the survival and growth of family firms compared with later generations (Gu et al., 2019; Zellweger et al., 2012). The long-term orientation of the founder prompts them to look for opportunities that ensure transgenerational control (Chrisman & Patel, 2012; Le Breton-Miller & Miller, 2013). Thus, a founder on the board of family-controlled firms would prefer to conduct CBAs in order to supplement the need for long-term SEW gains such as the sustainability of the family business for future generations.

Second, apart from the long-term SEW focus, founders want their business to survive, grow and act as a source to provide for future generations (James, 1999; Miller & Le Breton-Miller, 2014). In this context, firm internationalization and entry into foreign markets by way of CBAs may be an important strategy for transgenerational sustainability. Founder’s presence strengthens the strategic preferences of family firms for long-term financial well-being and transgenerational control (Kotlar et al., 2018), thereby accentuating the need to move early. This pronounced preference for both long-term financial and SEW gains on account of founder’s presence would result in a greater tendency for family firms to move early in a CBA wave compared with family firms without a founder on their board. In contrast, the absence of the founder from the board of family-controlled firms may attenuate their preference for long-term affective and financial goals, such as transgenerational control and business sustainability, resulting in a lower inclination for early movement, compared with family firms having a founder on board.

Third, founder’s presence on the board mitigates the short-term loss aversion behavior of family-controlled firms compared with family-controlled firms without a founder on board. This is because an acquisition leads to temporary disruption to existing business routines on account of diversion in family manager’s attention from existing core business (Hussinger & Issah, 2019). Disruption of business processes in the case of CBAs may be pronounced due to greater changes in the cultural and institutional environment of the target firm compared with domestic acquisitions. Founders possess superior firm-specific knowledge and routines compared with descendants (Brune et al., 2019; Morck et al., 1988), which may help overcome the short-term SEW losses associated with early movement in CBA waves. Founders may utilize their superior firm-specific knowledge and skills to minimize the disruption related to acquisition activities while conducting CBAs, thereby mitigating short-term SEW losses. Furthermore, founders provide a greater business continuity (Gu et al., 2019) to the family business, which would attenuate the disruption to the existing business routines, compared with family firms without a founder. In contrast, family-controlled firms not having a founder on board may lack firm-specific knowledge possessed by the founder (Block, 2012) and find it challenging to integrate CBAs. Therefore, they may find it difficult to mitigate their short-term SEW losses during the CBA process.

Taken together, we argue that the founder’s presence on the board is likely to amplify the need for long-term SEW and financial gains while mitigating the short-term SEW and financial losses in the case of CBAs, thereby strengthening the inclination for early movement. Hence, from a mixed gamble perspective, family-controlled firms with their founder on board will have a higher motivation to trade-off long-term financial and SEW gains over short-term SEW losses, thereby strengthening their preference for early movement in CBA waves, compared with family firms without a founder on board:

Family-Controlled Firms and Financial Performance

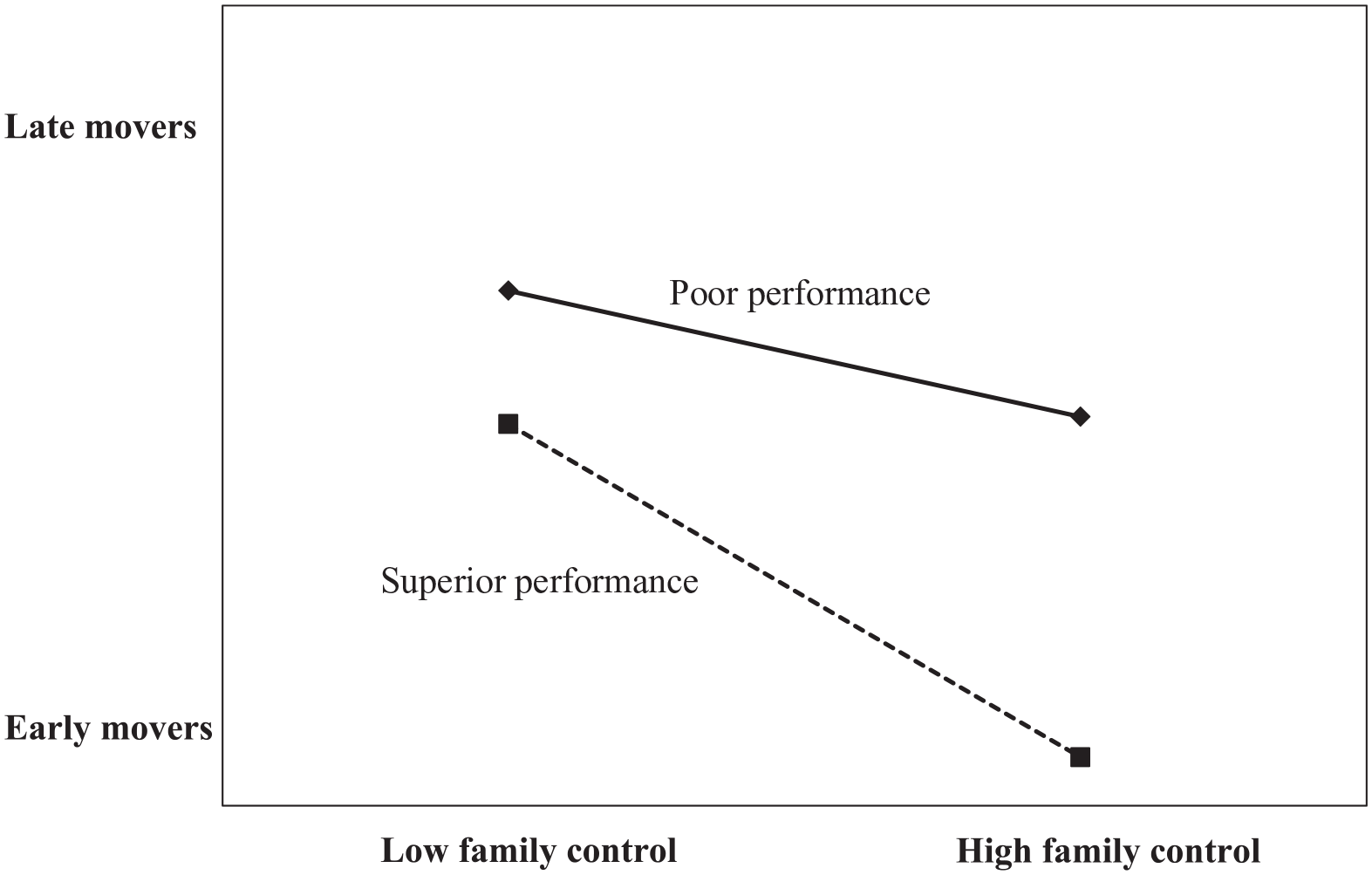

We argue that family-controlled firms with superior performance would have a stronger preference for moving early in a CBA wave compared with family firms with poor performance. When family firms are financially steady, their threat of survival is low, and therefore their preference remains towards maintaining SEW (Gomez-Mejia et al., 2018). Further, superior performance strengthens the willingness and ability of firms to undertake risky acquisitions and move early in the wave (Haleblian et al., 2012). Given that the risks of adverse selection and failure are high in CBAs compared with domestic firms, financial superior firms may have the resources and the motivation to undertake CBAs within waves. Accordingly, financially stable family-controlled firms may prefer to move early and benefit from long-term SEW gains related to family control and continuity of core business. Also, family firms with superior performance would have a greater ability to bear the acquisition costs, especially related to due diligence and postmerger integration activities, which are substantial in the CBA context. This ability enables cherry-picking and identifying targets with better fit (McNamara et al., 2008), leading to long-term SEW and financial gains. Accordingly, this would strengthen the preference to move early in CBA waves for financially stable family firms.

In contrast, family-controlled firms with poor performance may have a lower preference for early movement in CBA waves compared with financially stable family-controlled firms. This is because poorly performing firms may find it difficult to finance their CBAs while moving early (Haleblian et al., 2012). Lack of finances would lead to poor due diligence activities in CBAs, resulting in a greater likelihood of adverse selection and poor fit. This would result in lower financial and SEW gains for poor-performing family firms. Further, such firms may also encounter reduced family influence and control in undertaking strategic decisions on account of raising external capital to fund such acquisitions (Gomez-Mejia et al., 2018). Accordingly, family-controlled firms with poor performance may experience lower SEW and financial gains along with higher SEW losses compared with high-performing family-controlled firms. Therefore, we argue that better performing family-controlled firms prefer to move early in the CBA wave compared with family-controlled firms with poor performance:

Method

Study Context

The Indian context provides a unique and interesting opportunity to study family firms’ behavior in CBA waves. Family firms play a dominant role in various economies, including emerging markets like India (La Porta et al., 1999; Ray et al., 2018). CBAs conducted by Indian firms provide an important context to apply the mixed gamble approach due to the SEW and financial gains and costs associated with the acquisition process (Gomez-Mejia et al., 2018). CBA waves are riskier compared with domestic acquisitions on account of differences in the cultural, legal, and institutional environments of the acquirer and the target (Feito-Ruiz & Menéndez-Requejo, 2010; Xu, 2017). Furthermore, institutional reforms and liberalization policies implemented by the Government of India in the past two decades have led to changes in foreign approval processes and relaxation in repatriations. This resulted in an increased outward foreign direct investment and CBA waves. Fuad and Gaur (2019) note that the easing of funding and regulations related to automatic route policies acted as a trigger and led to CBAs by Indian firms. For example, by 2003, Indian firms could finance up to 100% of their net worth, and it was further relaxed up to 200% in 2005. Such relaxations acted as exogenous shocks in triggering CBA waves. Further, waves propagate until there is the availability of capital liquidity (Harford, 2005), and therefore a reason why waves ended around 2009 may be due to the economic crisis around 2008-2009 period. This crisis impacted the access to capital liquidity and thereby may have halted the wave propagation with a dip around 2008. Accordingly, we study CBA waves against the backdrop of these reforms catered towards outward foreign direct investments.

Data and Sample

Identifying CBA Waves

We retrieved all completed CBAs by Indian firms between 2000 and 2018 from the SDC database and acquirers’ financial data from the PROWESS database. In line with prior studies, we identify CBA waves at the two-digit SIC (Standard Industrial Classification) codes (Fuad & Gaur, 2019; Popli & Sinha, 2014). In the first step, we ascertain the year, which has the maximum number of wave deals and refer to it as the peak year of the wave. We then move backward and identify the year in which the CBA activity falls to half of the peak year activity. This year marks the beginning of the CBA wave. We conduct a similar exercise and move forward from the peak year and identify the drop in acquisition activity to half. This marks the end year of the wave. Through this manual process, we identified a total of 13 potential waves.

In the second step, in order to establish waves with greater rigor, we subjected these potential CBA waves to a simulation-based screening (Haleblian et al., 2012; Harford, 2005). This step is a robust methodology of wave identification and ensures that the potential waves did not happen due to chance. Accordingly, we take the total number of deals within the study period and randomly assigned them to each year of the potential wave. The peak years were then identified, and deal volumes were matched to waves identified in the first step. Waves that exceeded the 95th percentile were classified as final CBA waves.

Our initial CBA wave data set comprised 310 wave deals between 2003 and 2009, which had promoter’s equity data. Since we focus on family firms, we select firms that have a minimum of 20% equity ownership by the family (Ashwin et al., 2015; Ray et al., 2018). This resulted in 253 data points. Furthermore, we could not map some CBA deals and faced data issues related to few variables. Thus, our final sample comprised 221 CBA deals. We conducted t tests and chi-square tests on the initial and final data sets to test for sample selection bias. These tests included wave data and variables related to timing, prior performance, and firm size and indicate that the final sample represents the initial data set.

Measures

Dependent Variable

The entry timing variable represents the order of entry within a CBA wave. Prior studies have measured it using a binary variable to classify first movers (Xu, 2017). We use a continuous measure by calculating the duration in days between the first deal and the focal deal in the wave scaled by the wave duration (Haleblian et al., 2012). Thus, the first mover has a value of 0, whereas the last mover is assigned a value of 1.

Independent Variables

Our key independent variable is a family-controlled firm. Our sample comprises family firms with a minimum of 20% equity ownership by the founding family (Ashwin et al., 2015; Ray et al., 2018). Further, we classify family-controlled firms as those where the family member is either a CEO or a managing director (Alessandri et al., 2018; Dau et al., 2020). Firms that match the above criteria are coded as 1 and classified as family-controlled firms, while others are assigned a value of 0 and referred to as a nonfamily-controlled firm. We retrieved equity ownership information of the promoter family from the PROWESS database and verified the same with annual reports and shareholding information available on company websites. The presence of family members at the CEO or managing director position is manually coded through annual reports, company websites, and directors’ information available at the website of the Ministry of Corporate Affairs, Government of India (Ray et al., 2018).

Other hypothesized variables are founder on board and prior performance. We operationalize founder on board as a dummy variable with a value of 1 if the founder is present on the board, else 0. Finally, in line with prior studies (Cerrato et al., 2016; Kyriazopoulos & Drymbetas, 2015), we control for prior performance based on return on equity (ROE) prior to the focal acquisition and log transform the variable. This is important because our sample includes services companies that are asset-light. However, as a robustness test, we replace ROE with return on assets (ROA) and find the results to be consistent in both cases.

Control Variables

We include various firm-, deal-, industry-, and country-level variables, which may influence the timing within a CBA wave. The acquirer’s Firm size is measured as the logarithmic transformation of the acquirer’s sales (G. Caprio et al., 2014). Firm’s international sales are operationalized as the ratio of foreign sales to total sales (FSTS; Ray et al., 2018). We also controlled for the acquirer’s affiliation to a business group, foreign institutional investment, age, prior performance, marketing expenses, and debt to equity. Business group affiliation variable is assigned as 1 if the firm is a part of the business group, else assigned a value of 0. Firm age is measured as the number of years since incorporating the firm and the focal year of CBA (Kotlar et al., 2018). Marketing intensity is measured as the sum of marketing and advertising expenses divided by sales, whereas the debt-to-equity ratio controls for the slack resources in a firm. Foreign institutional investor (FII) ownership was operationalized as the percentage of common shareholdings by foreign institutional investors (Ashwin et al., 2015; Ray et al., 2018). Finally, we control for an acquirer’s propensity to conduct multiple acquisitions by incorporating a dummy variable with a value equal to 1 if the firm is conducting multiple CBAs in a wave and 0 otherwise.

Moreover, we also control for the percentage sought in the deal and the listing status of the target and acquirer. We tried to control for various deal-level variables such as the consideration offered, relative size, and deal premium in our models. However, we faced considerable data loss issues since our study has both listed and nonlisted firms. We, however, incorporate the listing status of the acquirer and the target firms. Acquirer listing status and Target listing status variables are dummy variables with a value of 1 if the firm is public listed else 0 (Dikova et al., 2010). Finally, to control for industry-related effects, industry dummies are included in all the models. We also include industry relatedness of the CBA based on the two-digit SIC similarity between target and acquirer. As the majority of CBAs by Indian firms were conducted in the United States, United Kingdom, and Germany, we control for these countries’ fixed effects in our analyses.

Method

Our dependent variable, Entry timing, is a continuous variable censored between 0 and 1. OLS regression in such scenarios may provide an inaccurate estimation (Maddala, 1983). We, therefore, conduct a tobit regression analysis to test the hypothesized relationships. Further, to control for sample selection bias and endogeneity issues, we conduct a two-stage Heckman regression and discuss those results under the robustness tests section.

Results

Table 2 shows the descriptive statistics of the variables under study, whereas Table 3 shows the results of tobit regression. All variance inflation factors were less than 10. Model 1 reflects the control variables, whereas Models 2 to 4 show the results for the hypothesized variables.

Means, Standard Deviations, and Correlations.

Note. CBA = cross-border acquisition; FII = foreign institutional investor ownership; FSTS = foreign sales to total sales.

p < .05. **p < .01.

Tobit Regression—Entry Timing in a Cross-Border Acquisition Wave.

Note. Estimates are shown with robust errors in parentheses. CBA = cross-border acquisition; FII = foreign institutional investor ownership; FSTS = foreign sales to total sales.

p < .10. **p < .05. ***p < .01. ****p < .001.

Model 1 of Table 3 shows that Target listing status, Firm size, percentage sought, and Foreign institutional ownership lead to late movement in CBA waves. We also find that Firm age, Prior performance, and Business group affiliation variables are associated with an early movement in a wave.

Model 4 of Table 3 shows that family-controlled firm variable is negative and significant (β = −0.11, p < .05). This suggests that firms with higher family control have a higher likelihood of moving early in a CBA wave than low family-controlled firms, thereby supporting Hypothesis 1. Hypothesis 2 argues that family-controlled firms having a founder on board would strengthen the relationship between family control and early movement in CBA waves. The interaction term is negative and significant (β = −0.27, p < .01) in Model 4 of Table 3. This supports Hypothesis 2. Finally, the interaction effect between prior performance and family-controlled firm variable is negative and significant (β = −0.11, p < .10), implying support for Hypothesis 3. Figures 1 and 2 show the interaction effect of family-controlled firm variable with founder on the board and prior performance variables.

Interaction effect of family control with founder on board.

Interaction effect of family control with prior performance.

Robustness Tests

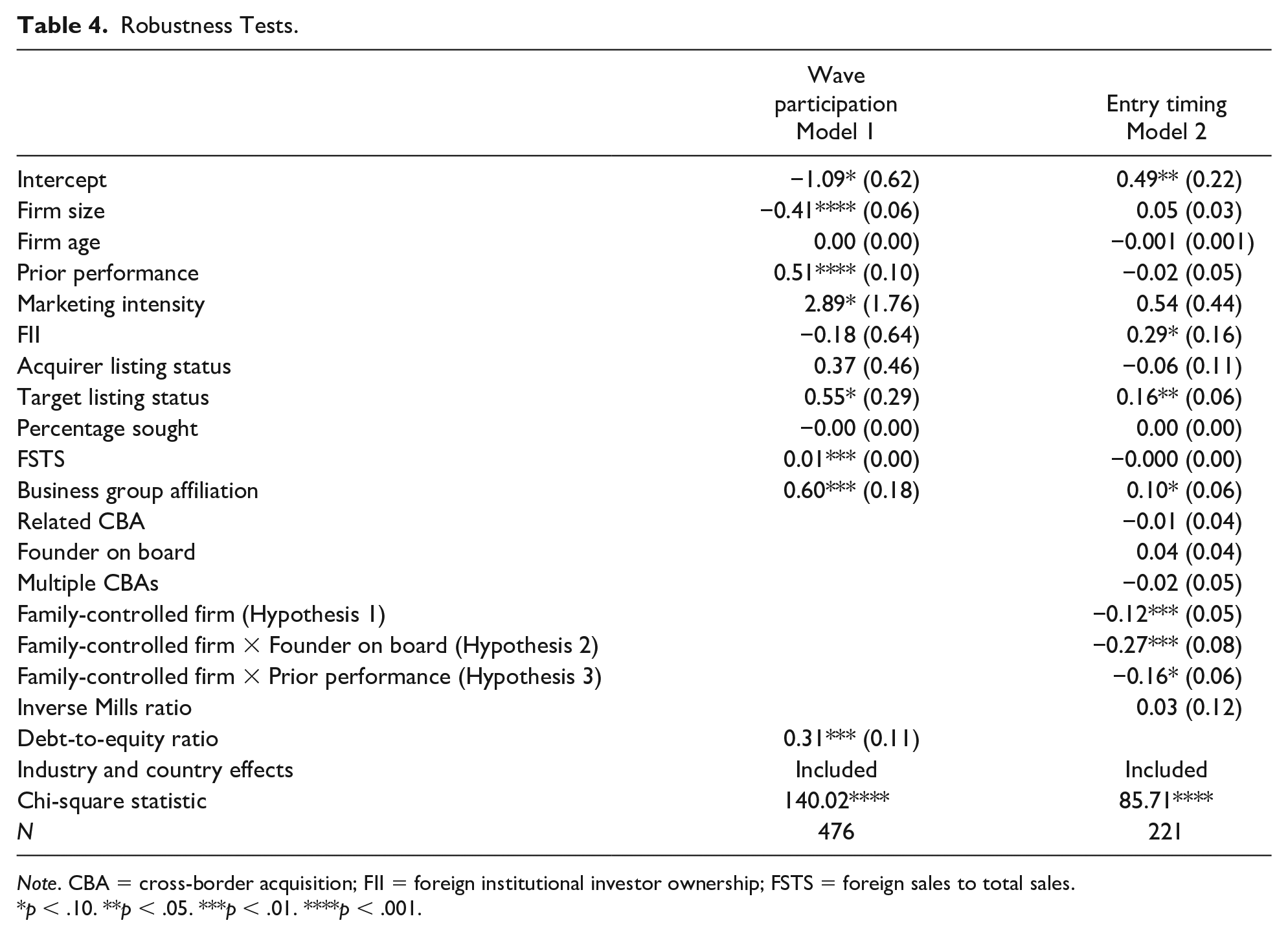

We ran multiple robustness checks to test the sensitivity of our findings and reported them in Tables 4 and 5, respectively. First, we conducted a two-stage Heckman (1979) regression analysis to control for possible self-selection bias in our models. This is because the decision to participate in waves may not be random but based on the choice of family managers. Hence, in the first stage, we conducted a probit regression to predict the likelihood of participating in a wave. We used the debt-to-equity ratio as the instrument variable associated with the firm’s financial slack (Haleblian et al., 2012) and may influence firm’s participation in the CBA wave. The inverse Mills ratio from the first stage probit model is then used in the second stage regression. However, we found that the inverse Mills ratio is not significant, suggesting that selection bias is not present in our models. These results are shown in Table 4, and all hypotheses are supported.

Robustness Tests.

Note. CBA = cross-border acquisition; FII = foreign institutional investor ownership; FSTS = foreign sales to total sales.

p < .10. **p < .05. ***p < .01. ****p < .001.

Robustness Tests.

Note. Estimates are shown with robust errors in parentheses. CBA = cross-border acquisition; FII = foreign institutional investor ownership; FSTS = foreign sales to total sales.

p < .10. **p < .05. ***p < .01. ****p < .001.

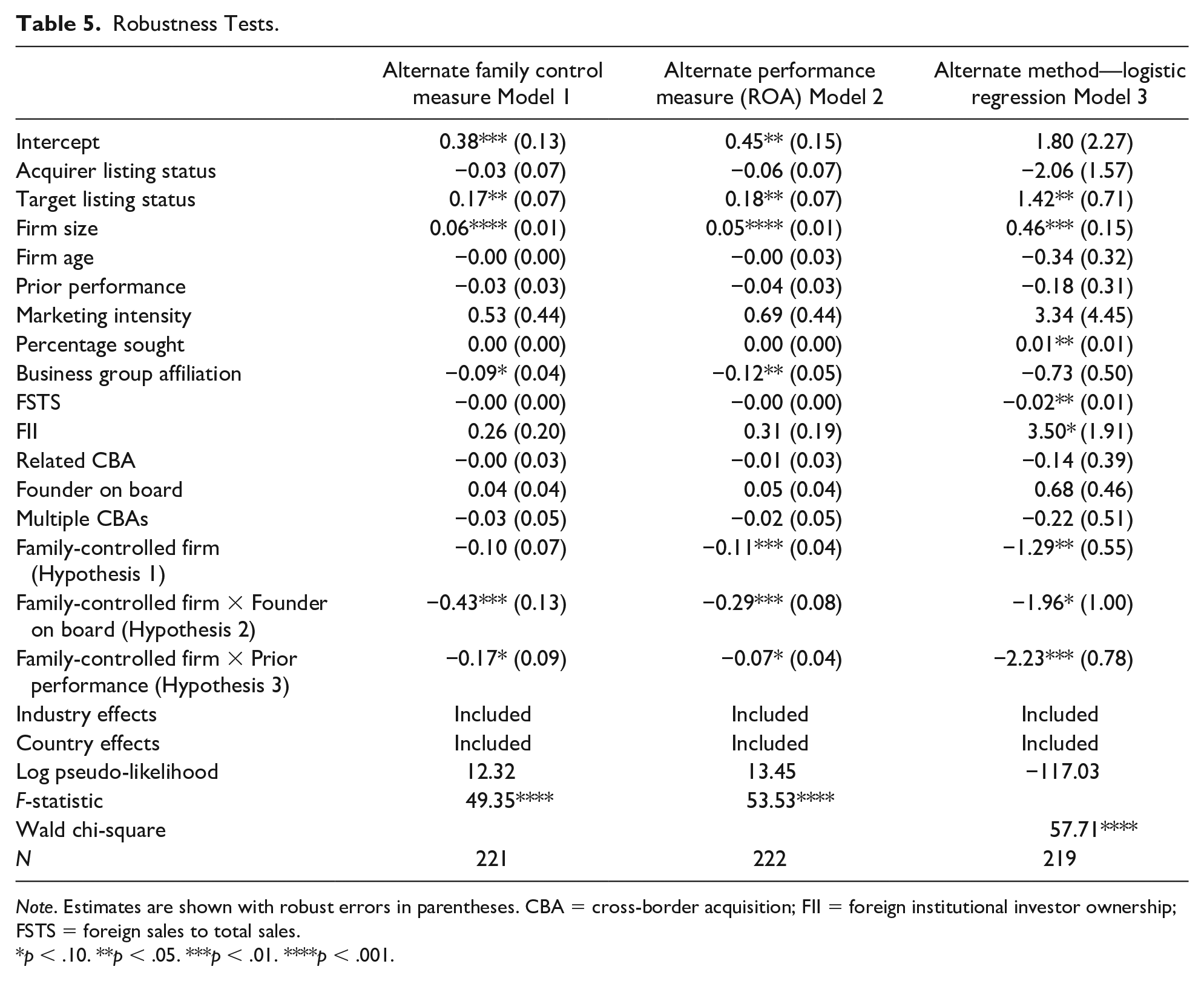

Second, we operationalized family-controlled firms as a continuous variable rather than a dummy variable. All family-controlled firms are assigned an actual value of shareholdings and nonfamily-controlled firms are assigned a value of 0 (Gomez-Mejia et al., 2018). This provides us an assessment of family control and incorporates heterogeneity within family firms. We found that all our hypotheses are supported except Hypothesis 1. The results are shown in Model 1 of Table 5. Second, we replaced the prior performance variable (ROE) with ROA and log transformed the age variable. We conducted a tobit regression and the results are shown in Model 2 of Table 5. We found the results to be robust and consistent. Third, we split the entry timing variable into a dummy variable with a value of 0 for early movers having a value of entry timing variable below 0.5 and 1 for late movers. We also log transformed the age variable and ran a logistic regression analysis. The results are shown in Model 3 of Table 5. In addition, we replaced logistic regression with probit regression in the above analysis and found the results to be consistent.

Fourth, in line with prior studies (Gomez-Mejia et al., 2018; Iyer & Miller, 2008), we checked for sensitivity of the prior performance of the firm by operationalizing performance below aspiration levels variable. It is computed as the difference of return on total assets in Years t − 1 and t − 2. Wherever the differences are negative, we take the absolute values of difference and assign a value of 0 to others. We find that the interaction effect of performance above aspirations with the family control variable is nonsignificant. Finally, since the business group affiliation variable and firm size have a correlation of 0.59, we removed the business group affiliation variable from our models and checked for the results. All hypotheses are supported.

Discussion and Conclusion

In this article, we draw upon the mixed gamble approach and explain the entry timing behavior of family-controlled firms within CBA waves by considering the trade-offs between SEW and financial wealth. Further, we study the boundary conditions associated with the founder’s presence on the board and firm’s prior performance on the entry timing decisions. We test our arguments on a sample of 221 CBA wave deals between 2003 and 2009 conducted by Indian firms.

Anchored in the mixed gamble perspective (Gomez-Mejia et al., 2014; Martin et al., 2013), our study highlights the trade-offs between affective and financial endowments undertaken by family-controlled and nonfamily-controlled firms while participating in CBA waves. Findings suggest that family-controlled firms move early in a CBA wave compared with nonfamily-controlled firms. Moving early in a wave helps family-controlled firms to cherry-pick superior assets from a larger pool of available targets (McNamara et al., 2008), which not only provides SEW benefits such as family control, continuity of core business, and transgenerational sustainability but is also associated with long-term financial gains. Accordingly, within CBA waves, early moving family-controlled firms select targets that are more aligned to their business. This results in lower short-term SEW losses arising from the temporary disruption of existing routines. Further, there are short-term financial costs related to due diligence activities, hiring of foreign consultants, paying premiums, and cross-cultural integration (Chari & Chang, 2009; Dikova & Sahib, 2013; Lebedev et al., 2015), leading to reduced financial wealth in the CBA context. Nonfamily-controlled firms due to the presence of external managers prefer short-term financial gains (Hussinger & Issah, 2019) and may be deterred by the short-term financial costs while participating in CBA waves. Therefore, despite nonfamily-controlled firms benefitting from potential long-term cherry-picking advantages, the short-term CBA costs would lower their preference for early movement compared with family-controlled firms.

Theoretical Contributions

Our study contributes to the scholarly understanding of family firms in multiple ways. First, we reconcile the decision-making behavior of family-controlled firms by incorporating both SEW loss aversion and long-term orientation when participating in CBA waves (Chrisman & Patel, 2012; Gomez-Mejia et al., 2014). According to the loss aversion perspective, family firms are risk-averse and focus on preserving their SEW, and at times foregoing financial gains (Berrone et al., 2012; Gomez-Mejia et al., 2007), which leads to a lower preference to conduct acquisitions (G. Caprio et al., 2014; Shim & Okamuro, 2011). Complementing the loss aversion view, other studies document that family firms prefer to conduct acquisitions with the aim to attain long-term financial and SEW benefits (Hussinger & Issah, 2019). We argue that the long-term SEW and financial gains while conducting early CBAs outweigh the short-term SEW and financial losses. Therefore, family-controlled firms would prefer to move early in CBA waves compared with nonfamily-controlled firms. This view aligns with the burgeoning body of research on family firms which considers the mixed gamble implications on firm behavior (Eddleston & Mulki, 2021; Gomez-Mejia et al., 2018). Thus, we extend the mixed gamble approach by including the temporal aspects of SEW and financial considerations in the entry timing decisions of family firms during CBAs.

Some scholars argue that family firms are inertial in nature, and hence, their decision making is delayed. Sharma and Manikutty (2005) argue that family structure and culture influence the time lag between the leader’s realization of the need to divest and actual divestment and may lead to inertial pressures against resource shedding. In contrast, studies also highlight the agile behavior of family firms on account of quicker decision making (Abetti & Phan, 2004; Gast et al., 2018). In the case of merger waves, early moving firms have lower inertial tendencies due to greater awareness, motivation, and capability to respond to environmental changes (Haleblian et al., 2012). Our findings suggest that family-controlled firms move early in CBA waves compared with nonfamily-controlled firms, which may be due to their higher motivation for long-term gains. This agile response of family firms in the context of CBA waves is in sharp contrast to their inertia-prone characterization in the family business literature (Sharma & Manikutty, 2005).

Second, we highlight that family-controlled firms with a founder on the board have a higher preference for early movement in CBA waves compared with family-controlled firms without a founder. Founder’s long-term orientation reinforces the transgenerational sustainability of family firms (Le Breton-Miller & Miller, 2013; Zellweger et al., 2012), which motivates them to conduct CBAs (Schierstedt et al., 2020). We show that the founder on the board of family-controlled firm amplifies the need for long-term SEW and financial gains over short-term SEW and financial losses, thereby reinforcing early movement in CBA waves.

Third, family-controlled firms with superior performance have a higher preference for early movement in the wave compared with family-controlled firms with poor performance. This is because when family-controlled firms have better performance, their threat of survival is low, thereby shifting their preference toward SEW benefits (Gomez-Mejia et al., 2018). Further, well-performing firms would be able to finance their CBAs with much ease and conduct a better due diligence process, thereby selecting better synergy targets while moving early. In contrast, firms with poor performance would find it difficult to finance their acquisitions (Haleblian et al., 2012), leading to poor due diligence process, greater risk of adverse selection, and lower strategic fit with their family business. Accordingly, better performing family firms would gain both higher SEW and financial benefits by moving early compared with poor-performing family firms, which may encounter lower SEW and financial gains. Hence, the preference to move early in CBA waves is higher in family-controlled firms with superior performance than poor-performing family-controlled firms.

Finally, our study contributes to the strategic management literature on internationalization of family firms (Alessandri et al., 2018; Lahiri et al., 2020; Pukall, & Calabro, 2014; Singla et al., 2014). Prior studies highlight mixed findings related to family involvement in management and its influence on internationalization (Liang et al., 2014). Similarly, in the context of CBA waves, studies show mixed findings in regard to early movement and firm performance, which creates a dilemma for firms deciding to participate in acquisition waves (Fuad & Sinha, 2018; McNamara et al., 2008; Xu, 2017). In this study, we utilize the mixed gamble perspective (Gomez-Mejia et al., 2014) in explaining the entry timing decision of family-controlled firms compared with nonfamily-controlled firms in the CBA context.

Managerial Implications

Our study has implications for family managers. Family-controlled firms are mainly focused on fulfilling family goals and therefore are averse to conducting CBAs (Chen et al., 2009; Geppert et al., 2013). Conducting CBAs within waves may have implications for both SEW and financial wealth. Hence, family managers should consider the potential financial and SEW gains in the long term by weighing them against the short-term SEW and financial losses incurred in the wave. Our results suggest that family-controlled firms move early in the CBA waves in order to benefit from long-term financial and SEW gains compared with nonfamily-controlled firms. Thus, entry timing strategies within CBA waves may be duly considered by weighing the long-term SEW and financial gains with the short-term SEW and financial losses.

Limitations and Directions for Future Research

Our study has several limitations that provide opportunities for future research. First, we have studied the entry timing behavior of family-controlled and nonfamily-controlled firms which participate in CBA waves. Future research may study other aspects of heterogeneity within family firms on account of the multidimensional SEW construct (Swab et al., 2020) and the role of nonfamily members (Tabor et al., 2018) in entry timing decisions of CBAs and other modes of diversification such as strategic alliances. Second, we could not include the target’s financial information and some of the deal-level variables due to a reduction in sample size. This is because we have both listed and nonlisted target firms in our sample. Future research may also study the characteristics of targets and their impact on the mixed gamble perspective. Third, our sample is limited to the Indian context, and scholars may examine the generalizability of our findings across other emerging and developed economies, especially in the context of CBA waves. Finally, qualitative studies may be conducted to study the family firms’ risk-taking behavior and decision making within CBA waves. This may provide us with a more nuanced understanding of the various mechanisms involved in the decision-making process of family-controlled firms from a mixed gamble perspective.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.