Abstract

This study investigates whether family owners consider the stages of CEO tenure in their use of firm performance to assess CEOs. Integrating insights on family owners’ long-term orientation and stages of CEO tenure, we theorize that family owners rely more on firm performance to make CEO replacement decisions during the mid-stage of CEO tenure than during the early and late stages. Moreover, we predict that they hold nonfamily CEOs more accountable for firm performance than family CEOs only during the mid-stage of CEO tenure. Using data from family-controlled firms in Taiwan, we found empirical evidence supportive of our theoretical predictions.

Introduction

Many publicly traded firms around the world are still controlled by their founding families, and these controlling families may either appoint a family member or a professional manager who is not a family member as the CEO (Anderson & Reeb, 2003; Berrone et al., 2012). Compared to having a family member as the CEO, appointing a nonfamily member enables a controlling family to access the broad managerial labor market for capable talents (Chua et al., 2009; Sirmon & Hitt, 2003; Zellweger et al., 2012). Meanwhile, because it gives away the CEO position to a nonfamily member whose interest may not align with the family, it can potentially undermine the controlling family’s socioemotional wealth (SEW), which refers to the nonfinancial aspects of the firm that meet the family’s affective needs such as family pride and reputation (Gomez-Mejia et al., 2007, p. 106).

Given the tradeoffs involved in the appointments of family versus nonfamily CEOs, prior research has examined whether controlling families treat family and nonfamily CEOs the same or differently in holding them accountable for firm performance. Some scholars argue that there is a clear difference in controlling families’ treatment of family versus nonfamily CEOs because of the presence or absence of family ties (Gomez-Mejia et al., 2001; Schulze et al., 2001). Others suggest that controlling families may treat nonfamily CEOs like extended family members and de-emphasize firm performance in their assessment of both family and nonfamily CEOs (Bassanini et al., 2013; Christensen-Salem et al., 2021). The empirical findings are largely consistent with the differential treatment argument, showing that the likelihood of turnover for nonfamily CEOs is not only higher than for family CEOs but also is more strongly tied to firm performance in family-controlled firms (Chen et al., 2013; Crossland & Chen, 2013; Gomez-Mejia et al., 2001; Li, 2018; Neckebrouck et al., 2018).

Our study attempts to contribute to the literature on agency contracts in family firms by investigating whether controlling families treat family CEOs more favorably than nonfamily CEOs across different stages of CEO tenure. The existing studies took a largely static view of the agency relationship between controlling families and CEOs, as they implicitly assumed that controlling families’ relationships with family versus nonfamily CEOs stayed the same throughout CEO tenure. Empirically, they only examined whether firm performance had a differential negative effect on the turnover of family versus nonfamily CEOs, but whether such a differential effect exists during each stage of CEO tenure has remained uninvestigated and thus unclear. As a result, the existing literature leaves an impression that differential contracts for family versus nonfamily CEOs remain constant throughout CEO tenure. To contribute to the understanding of agency contracts in family firms during different stages of CEO tenure, our study examines this issue from a more dynamic perspective that integrates insights from research on family owners’ concern for SEW and long-term orientation (Berrone et al., 2010; Gomez-Mejia et al., 2011; Le Breton-Miller et al., 2011) with insights from research on the stages of CEO tenure (Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001; Shen, 2003).

Specifically, we examine first whether family owners consider the stages of CEO tenure in their use of firm performance to make CEO replacement decisions, and then whether they treat family and nonfamily CEOs differently during each stage in terms of holding them accountable for firm performance. Prior research suggests that family owners tend to have a long-term orientation in decision-making because their SEW is tied to the long-term survival of their firms (Berrone et al., 2010; Gomez-Mejia et al., 2011; Le Breton-Miller et al., 2011). We argue that such a long-term orientation makes controlling families consider the stages of CEO tenure in their assessments of CEOs. Given that it generally takes at least a couple of years for new CEOs’ strategies to show a significant impact on firm performance (Gabarro, 1987; Miller & Shamsie, 2001), we theorize that controlling families focus less on firm performance in their assessments during the early stage of CEO tenure when CEOs are still working on formulating and implementing their strategies (Hambrick & Fukutomi, 1991), but more during the mid-stage of CEO tenure when the CEOs’ strategies start to significantly impact firm performance (Miller & Shamsie, 2001; Shen, 2003). For CEOs who survive the mid-stage by delivering satisfactory performance, we argue that controlling families will again focus less on firm performance in their assessments as they have gained significant knowledge about these CEOs’ competence (Hermalin & Weisbach, 1998; Murphy, 1986). Thus, we predict that the negative effect of firm performance on CEO turnover in family-controlled firms is stronger during the mid-stage of CEO tenure than during the early and late stages.

We further theorize that controlling families hold nonfamily CEOs more accountable than family CEOs for firm performance only during the mid-stage of CEO tenure. During the early stage, because both family and nonfamily CEOs are working on formulating and implementing their strategies, family owners are less likely to expect nonfamily CEOs to have a stronger impact on firm performance than family CEOs. Consequently, they do not hold nonfamily CEOs more accountable for firm performance. During the mid-stage, because firm performance is significantly influenced by CEOs and their strategies (Miller & Shamsie, 2001; Shen, 2003), family owners will expect nonfamily CEOs to deliver stronger firm performance to compensate for the family’s SEW loss that results from the appointment of nonfamily CEOs (Gomez-Mejia et al., 2011). They will thus hold nonfamily CEOs more accountable than family CEOs for firm performance. During the late stage, in addition to focusing less on firm performance in their assessments of CEOs as we argued above, family owners may have developed a stronger relationship with nonfamily CEOs over time that makes them treat nonfamily CEOs more like extended family members (Bassanini et al., 2013; Berrone et al., 2022). Therefore, we predict that firm performance has a stronger negative effect on the turnover of nonfamily CEOs than on the turnover of family CEOs only during the mid-stage of CEO tenure, but not during the early or late stage. Using data on a sample of 326 family-controlled firms in Taiwan between 1999 and 2015, we found empirical support for our theoretical predictions.

By investigating whether and how the effect of firm performance on CEO turnover changes during the early, mid-, and late stages of CEO tenure in family-controlled firms, our study makes two major contributions to the family business literature. First, it contributes to the understanding of agency contracts in family firms in terms of whether or to what degree family owners hold CEOs accountable for firm performance during different stages of CEO tenure. While prior research has extensively examined the impact of firm performance on CEO turnover in family firms (e.g., Gomez-Mejia et al., 2001; Li, 2018), our study advances a more dynamic perspective to suggest that family owners take into account the stages of CEO tenure in their use of firm performance to make CEO replacement decisions. Second and more importantly, our study contributes to the understanding of agency contracts in family firms in terms of family owners’ relationships with family versus nonfamily CEOs, specifically, whether family owners treat family and nonfamily CEOs differently throughout CEO tenure. In contrast to existing research that takes a static view of family owners’ relationships with family versus nonfamily CEOs throughout CEO tenure (Bassanini et al., 2013; Gomez-Mejia et al., 2001; Hall & Nordqvist, 2008; Nason et al., 2018), our theory and supportive findings suggest a more dynamic relationship in that family owners hold nonfamily CEOs more accountable for firm performance than family CEOs only during the mid-stage of CEO tenure, but not during the early or late stage. In sum, our study shed new light on agency contracts in family firms, particularly regarding family owners’ relationships with family versus nonfamily CEOs at different stages of CEO tenure.

Theory and Hypotheses

Many publicly traded firms around the world have their founding families as controlling shareholders (La Porta et al., 1999; Peng et al., 2018). By keeping a significant proportion of firm ownership, the founding families can retain control and effectively influence managerial decisions at these firms (Blumentritt et al., 2007; Nelson, 2003; Young et al., 2008). As a result, the controlling families are able to cater to and protect family values, reputation, and pride beyond financial gains in firm decisions (Berrone et al., 2010; Schulze et al., 2003; Strike et al., 2015). Gomez-Mejia and colleagues (2007) introduced the concept of SEW to describe the “non-financial aspects of the firm that meet the family’s affective needs” (p. 106), such as the preservation of family pride and the perpetuation of family values.

Because CEOs can significantly influence firm decisions and performance (Finkelstein et al., 2009; Quigley & Hambrick, 2015), organizational scholars have been long interested in how family owners’ consideration of SEW influences the decision of CEO replacement. Because having a family member as the CEO gives family owners a strong sense of control in protecting family values and identity, the dominant view is that family owners not only prefer appointing a family member as the CEO to maintain their SEW but also they are more willing to tolerate financial losses caused by the appointment of a family CEO (Gomez-Mejia et al., 2001, 2011; Li, 2018). In contrast, because appointing a nonfamily CEO can undermine family control and SEW, family owners tend to expect nonfamily CEOs to deliver superior financial performance to compensate for their losses in SEW caused by the appointment of a nonfamily CEO (Bennedsen et al., 2007; Gomez-Mejia et al., 2011; Gu et al., 2019; Villalonga & Amit, 2006). Consequently, the dominant view suggests that family owners have different agency contracts with family and nonfamily CEOs, as they hold nonfamily CEOs more accountable for firm performance (Schulze et al., 2001). Consistent with this view, the existing research finds that firm performance has a stronger negative effect on the turnover of nonfamily CEOs than the turnover of family CEOs (X. Chen et al., 2013; Dasgupta et al., 2018; Gomez-Mejia et al., 2001; Rizzotti et al., 2017; Schulze et al., 2001).

While the existing research provides insight about how family owners’ concern with SEW may impact their agency contracts with family versus nonfamily CEOs, it implicitly assumes that this impact remains constant throughout CEO tenure. Research on the seasons of CEO tenure suggests that the degree to which firm performance reflects CEOs’ competence varies at different stages of CEO tenure (Hambrick & Fukutomi, 1991; Hermalin & Weisbach, 1998; Miller & Shamsie, 2001; Shen, 2003). We believe that an integration of this insight with family owners’ concern for SEW can shed new light on agency contracts in family firms, particularly regarding family owners’ use of firm performance to make CEO replacement decisions at different stages of CEO tenure and whether they treat family and nonfamily CEOs differently during each stage.

Impact of Firm Performance on CEO Turnover at Different Stages of CEO Tenure

Research on the seasons of CEO tenure suggests that firm performance often does not fully reflect CEOs’ competence until after they have been in the office for a few years. There are several reasons why firm performance hardly reflects CEOs’ competence during the early stage of their tenure. First, new CEOs need to spend a significant amount of effort to better understand their firms’ internal and external environments, including both the challenges and the opportunities (Gabarro, 1987; Gu et al., 2024; Vancil, 1987). Such learning is important for all new CEOs, regardless of whether they are promoted from inside or hired from outside (Shen, 2003). Even CEOs appointed to address a specific strategic mandate need some time to familiarize themselves with the new job before figuring out how to respond to the mandate (Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001). Second, the strategy implementation process takes time, given that it involves allocations of resources and changes in organizational structures, systems, and procedures (Gabarro, 1987). Finally, as firm performance is highly path-dependent (Hannan & Freeman, 1984), it tends to be heavily influenced by the prior CEO’s strategic decisions during the first few years of a CEO’s tenure (Graffin et al., 2013; Shen & Cannella, 2002). Taken together, the above arguments suggest that firm performance does not serve as a good indicator of CEOs’ competence during the early stage of CEO tenure.

While research on the seasons of CEO tenure does not focus specifically on CEOs in family businesses, it has important implications for family owners and CEOs in family-controlled firms, particularly regarding the extent to which family owners use firm performance to assess CEOs. Concerned with their SEW, we argue that family owners likely focus less on firm performance when assessing CEOs during the early stage of CEO tenure. Prior research suggested and found that because family owners’ SEW is tied to their firms’ long-term survival (Martin & Gomez-Mejia, 2016), they tend to have a long-term orientation and prefer to develop long-term relationships with key stakeholders such as employees, customers, and the communities they are embedded in (Berrone et al., 2010; Gomez-Mejia et al., 2011; Le Breton-Miller et al., 2011). Given the importance of CEOs to their firms’ long-term survival, family owners are likely to have a long-term orientation in their relations with new CEOs as well, giving the latter time to formulate and implement their strategies. As it takes a few years for new CEOs’ strategies to impact firm performance (Graffin et al., 2013; Miller & Shamsie, 2001), family owners are likely to focus less on firm performance in their assessment of new CEOs.

Meanwhile, we would like to note that our argument does not suggest that family owners do not hold new CEOs accountable. In contrast, family owners are likely to closely monitor new CEOs during this stage because both their long-term financial wealth and SEW are influenced by new CEOs’ decisions and actions during this stage (Martin & Gomez-Mejia, 2016). Instead of emphasizing firm performance, family owners may focus more on monitoring and assessing new CEOs’ strategic decisions and actions, such as resource allocation and investment decisions (Baysinger & Hoskisson, 1990; Eisenhardt, 1989). In other words, family owners may rely more on behavior-based strategic control than outcome-based financial control in corporate governance during the early stage of CEO tenure, as their strong ownership position gives them both incentives and power to engage in strategic control. Thus, our arguments suggest that family owners rely more on evaluating CEOs’ strategic decisions and actions, but less on firm performance to assess CEO competence and make CEO replacement decisions during the early stage of CEO tenure.

As CEOs go through the early stage and enter the mid-stage of tenure, family owners are likely to focus more on firm performance in their assessments and hold CEOs accountable for poor firm performance. While family owners are concerned with SEW (Gomez-Mejia et al., 2007), they also care about firm performance because it is critical to their firm’s long-term survival, which influences both the family’s financial wealth and SEW (Crossland & Chen, 2013; Gomez-Mejia et al., 2011; Martin & Gomez-Mejia, 2016). After CEOs have been in the office for a few years, their strategic decisions and actions during the early stage are expected to show a significant impact on firm performance (Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001). Thus, family owners will focus more on firm performance in their assessments of CEOs after the early stage of CEO tenure, and they will continue this practice for several years to ensure that their CEOs are competent to deliver good firm performance (Hermalin & Weisbach, 1998; Shen, 2003). If firm performance remains good compared to industry peers’ during this period, it gives family owners confidence in their CEOs’ competence. However, if firm performance becomes poor, family owners may raise questions about their CEOs’ competence and consider making a change. The significant ownership possessed by family owners gives them the power to hold CEOs accountable for firm performance (Gomez-Mejia et al., 1987; Tosi & Gomez-Mejia, 1989). Thus, we predict that firm performance has a strong negative effect on CEO turnover during the mid-stage of CEO tenure, when CEOs are expected to deliver good firm performance to prove their competence.

If CEOs can prove their competence by delivering good firm performance and survive the mid-stage, family owners may focus less on firm performance in their assessments of CEOs afterwards, similar to what happens in boards’ assessments of CEO competence at nonfamily firms (Murphy, 1986). The primary reason is that family owners are likely to have accumulated significant knowledge about the CEOs over the years and become more confident in their competence (Hermalin & Weisbach, 1998; Murphy, 1986). In this situation, a decline in firm performance may no longer have the same impact on family owners’ assessments of these CEOs’ competence as during the mid-stage of CEO tenure, when family owners expect CEOs to prove competence by delivering good firm performance. In addition, concerned with their firms’ long-term survival, family owners may encourage these proven competent CEOs to explore new strategic initiatives, rather than to continue focusing on exploiting proven strategies. Prior research suggests that CEOs tend to continue their earlier proven strategies during the late stage of tenure, which can result in a mismatch with evolving environmental demands over time (Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001). To prevent such a tendency, family owners may focus less on firm performance but more on new strategic initiatives and actions in their assessments of CEOs who have demonstrated competence by delivering good firm performance and survived the mid-stage. For example, they may pay greater attention to the CEOs’ decisions and efforts in promoting new product launches or new market entries that can have important implications for their firms’ long-term survival. Thus, we expect the impact of firm performance on CEO turnover to be weakened during the late stage of CEO tenure relative to the mid-stage of CEO tenure.

Taken together, the above arguments suggest that family owners may not constantly rely on firm performance to assess CEOs’ competence; instead, they are most likely to do it during the mid-stage of CEO tenure, but less likely during the early and late stages. Thus, we predict that the negative impact of firm performance on CEO turnover is stronger during the mid-stage than during the early and late stages in family-controlled firms. Compared to prior studies that did not consider CEO tenure and those that focused only on the early stage (Graffin et al., 2013; Shen & Cannella, 2002) or the late stage (Ocasio, 1994), our theory provides a more systematic prediction of how the impact of firm performance on CEO turnover varies across the early, mid-, and late stages of CEO tenure.

Impact of Firm Performance on the Turnover of Family Versus Nonfamily CEOs

Research on the stages of CEO tenure also has implications for family owners’ agency contracts with family versus nonfamily CEOs, particularly regarding whether they hold nonfamily CEOs more accountable for firm performance than family CEOs. The existing family business literature suggests that, because the appointments of nonfamily CEOs can undermine family control and SEW, family owners expect nonfamily CEOs to deliver higher performance than family CEOs to compensate for the families’ losses in SEW (Bennedsen et al., 2007; Gomez-Mejia et al., 2011; Villalonga & Amit, 2006). While we agree that family owners tend to have higher performance expectations toward nonfamily CEOs than toward family CEOs, they may not demand nonfamily CEOs to deliver superior firm performance more than they demand family CEOs during every stage of CEO tenure.

As we explained earlier, family owners’ long-term orientation makes them focus less on firm performance in their assessments of new CEOs because they understand that it takes time for new CEOs’ strategies to impact firm performance. Thus, although family owners expect nonfamily CEOs to be more competent than family members, they are less likely to demand nonfamily CEOs to deliver superior firm performance immediately after taking the CEO job. Instead, they are likely to rely less on firm performance in the assessments of both family CEOs and nonfamily CEOs during the early stage of CEO tenure, giving them time to formulate and implement strategies to ensure the firms’ long-term survival. Although family owners may treat family and nonfamily differently in the use of behavior-based strategic control (e.g., they may assess family CEOs’ strategic decisions and actions more favorably than nonfamily CEOs’), it does not necessarily mean that they would hold nonfamily CEOs more accountable for firm performance than family CEOs. Therefore, we do not expect firm performance to have a stronger negative effect on the turnover of nonfamily CEOs than family CEOs during the early stage of CEO tenure.

As CEOs enter the mid-stage of tenure, their strategic decisions and actions during the early stage start to impact firm performance significantly (Miller & Shamsie, 2001; Shen, 2003). Because firm performance becomes a stronger indicator of CEO competence, family owners focus more on firm performance in their CEO assessment and replacement decisions during this stage, regardless of whether the CEOs are family members, to ensure family firms’ long-term survival. It is also likely when family owners expect nonfamily CEOs to deliver superior firm performance to compensate for the family’s loss in SEW resulting from the appointment of a nonfamily member as the CEO. When firm performance becomes poor, it will have a stronger impact on nonfamily CEOs, making them more likely to be replaced than family CEOs (Crossland & Chen, 2013; Gomez-Mejia et al., 2001). Thus, we predict that firm performance has a stronger negative effect on the turnover of nonfamily CEOs than the turnover of family CEOs during the mid-stage of CEO tenure.

For CEOs who have proven their competence and survived the mid-stage, family owners will focus less on firm performance in their assessments of CEOs as they have become quite confident about these CEOs’ competence. This is especially true for nonfamily CEOs, who have met family owners’ expectations of delivering superior firm performance during the mid-stage. As we have argued earlier, during the late stage of CEO tenure, family owners will focus more on CEOs’ strategic decisions and actions to ensure that these CEOs continue to work for the families’ long-term interests. This shift in focus reduces the impact of firm performance on CEO turnover. In addition, family owners’ relationships with nonfamily CEOs may have evolved into more “family-like” over the years (Berrone et al., 2022). Although our theory has so far focused on family owners’ assessments of CEOs’ competence to deliver satisfactory firm performance, prior research suggests that family owners also care about nonfamily CEOs’ dedication to the socioemotional aspects of family interests beyond firm performance, such as family value, pride, and reputation (Hall & Nordqvist, 2008; Nason et al., 2018). When they find that a nonfamily CEO is not dedicated to the socioemotional aspects of family interests, they may decide to replace the CEO regardless of the latter’s competence (Martin & Gomez-Mejia, 2016). Meanwhile, nonfamily CEOs may also evaluate their fit and relationship with the family owners to decide their own career path. After working as the CEO for several years, they are likely to have gained a good understanding of the family owners and their expectations. Nonfamily CEOs who no longer feel comfortable working for the family owners or perceive potential for serious conflicts with the family owners may decide to “jump ship” before the conflicts materialize. Such a decision will help them avoid being forced out for “undisclosed” reasons and lower the risk of tarnishing their reputation in the external managerial labor market (Semadeni et al., 2008).

Because of the mutual selection between family owners and nonfamily CEOs over time, nonfamily CEOs who survive the early and mid-stages are not only likely to have gained the confidence of family owners in terms of competence and dedication. They may also feel comfortable working for and with the family owners (Grubman & Jaffe, 2010; Miller et al., 2011). Recognizing these nonfamily CEOs’ competence and dedication, family owners may reciprocate by treating them more like extended family members (Berrone et al., 2022). In this situation, family owners may no longer hold nonfamily CEOs more accountable for firm performance than family CEOs. Therefore, we do not expect firm performance to have a stronger effect on the turnover of nonfamily CEOs than the turnover of family CEOs during the late stage of CEO tenure.

Taken together, the above arguments suggest that family owners tend to hold nonfamily CEOs more accountable for firm performance than family CEOs only during the mid-stage of CEO tenure, but not during the early or late stages. Thus, we propose the following:

Method

Sample

We tested the above hypotheses using data from a sample of family-controlled firms listed in the Taiwan stock market from 1999 to 2015. Family-controlled firms are prevalent in Taiwan, as approximately 80% of the listed firms are controlled by the founding families (Claessens et al., 2000; Gu et al., 2019; Li, 2018). Moreover, many family-controlled firms have professional managers who are not members of the controlling families as CEOs (Chung & Luo, 2008; Li, 2018). The large number of nonfamily CEOs at family-controlled firms in Taiwan presents an ideal context to test our dynamic perspective on the impacts of firm performance on CEO turnover and the turnover of family versus nonfamily CEOs during different stages of CEO tenure.

Our primary data source is the Taiwan Economic Journal (TEJ) database, which is the most authoritative database covering publicly listed firms in Taiwan and has been commonly used in previous studies of family firms (e.g., Li, 2018; Luo & Chung, 2013). The TEJ identifies a listed firm as family-controlled if a family (a) owns at least 5% of firm shares and (2) has at least two family members on the board of directors or top management team (Huang et al., 2012). Furthermore, the TEJ classifies a CEO as a family or nonfamily CEO based on whether the CEO has a blood or marital relationship with the controlling family, consistent with the conception of family versus nonfamily CEO used in the literature (Li, 2018). We also used company annual reports and various news portals to complement the TEJ database in collecting information about CEOs’ backgrounds and the causes of their turnovers. After deleting observations with missing data, the final sample consists of 532 family-controlled firms, 680 professional CEOs, 674 family CEOs, and 7,384 firm-year observations.

Measures

Dependent Variable

In line with prior studies (Shen & Cannella, 2002; Wiersema & Zhang, 2011), we tracked each CEO’s employment status at a firm every year during the sample period and measured the dependent variable CEO turnover annually as a dummy. Because our theory focuses on forced or involuntary CEO exit, we coded CEO turnover as 1 if the CEO stepped down during the year and it was not caused by retirement, death, health issues, or acceptance of a similar or higher position such as vice board chair or board chair at the focal firm or another firm owned by the same controlling family (Hubbard et al., 2017; Shen & Cannella, 2002; Wang et al., 2017). We further checked the causes of CEO turnover using various news portals, including the authoritative Taiwanese Market Observation Post System, to confirm the coding based on the information provided in the TEJ database. When a CEO turnover was stated as being caused by any of the reasons listed above, we treated it as right censored and coded it as 0 (Allison, 1984). We also coded CEO turnover as 0 when the CEO remained in the position at the end of the year (i.e., no turnover happened during the year).

Independent Variables

We measured firm performance using industry-adjusted returns on assets (ROAs). Industry-adjusted ROA takes into account the influence of industry trends and has been commonly found to have a significant effect on CEO turnover, including in family firms (Crossland & Chen, 2013; Finkelstein et al., 2009; Li, 2018). We first calculated firm ROA as the percentage of the net operating profits divided by the firm’s total assets, and industry ROA as the average ROA of all the listed firms in the focal firm’s primary two-digit Standard Industry Code (SIC) category. We then measured firm performance by subtracting the industry ROA from the focal firm’s ROA (Ocasio, 1994; Zhang & Rajagopalan, 2010).

We used a dummy variable to measure whether a CEO was a family or nonfamily CEO. Specifically, we coded nonfamily CEO as 1 if the CEO has no blood or marital relationship with the controlling family and 0 otherwise. The mean of nonfamily CEO is 0.408, suggesting that 40.8% of the CEOs in our sample were classified as nonfamily CEOs. To measure the three stages of CEO tenure, we first recorded CEO tenure as the number of years the CEO had served in the position at the focal family-controlled firm. We then divided CEO tenure into early stage, mid-stage, and late stage based on the number of years the CEO had been in the position. Research on the stages of CEO tenure suggests that new CEOs often spend the first 2–3 years developing and implementing their strategies (Gabarro, 1987). Given that it may take an additional year for new CEOs’ strategies to impact firm performance (Miller & Shamsie, 2001), we decided to code early stage as 1 for the year of succession (year 0) and the first 3 full years of a CEO’s tenure (year 1 to year 3), and as 0 otherwise. Our theory suggests that family owners focus on firm performance in their assessments of CEOs after the early stage of CEO tenure and continue this practice for several years to ensure that their CEOs are competent to deliver good firm performance. Accordingly, we coded mid-stage as 1 for the next 6 years of CEO tenure (e.g., from year 4 to year 9), and 0 otherwise. We then coded late stage as 1 for all the years afterwards. We also coded mid-stage using a shorter 5-year window (from year 4 to year 8) and a longer 7-year window (from year 4 to year 10) as robustness checks and obtained similar findings.

Control Variables

We included a number of control variables to account for the potential effects of other CEO factors, corporate governance factors, and firm factors on CEO turnover. First, we controlled for the effect of CEO power. We collected data on CEOs’ ownership, duality, education, insider status, initial public offering (IPO) experience, and new director appointment that have been widely used as indicators of CEO power (Chang & Shim, 2015; Shen & Cannella, 2002; Zhang & Rajagopalan, 2010). We measured CEO ownership as the proportion of the firm’s stocks owned by the CEO, CEO duality as 1 if the CEO simultaneously served as the board chair and as 0 otherwise, CEO education as 1 if the CEO had a college degree or above and as 0 otherwise, and CEO insider as 1 if the CEO joined the focal firm before becoming the CEO. We also created a variable, CEO IPO experience, to capture whether the CEO was appointed before the family-controlled firm’s IPO, and coded it as 1 if yes and 0 otherwise. On one hand, leading a firm through the IPO process may help strengthen the CEO’s relationship with the controlling family. On the other hand, because the firm is exposed to various new demands from outside investors and regulatory agencies after the IPO (Fischer & Pollock, 2004; Leitterstorf & Rau, 2014), the controlling family may monitor the CEO closely to ensure that his or her competence meets the new demands. Thus, it is important to control whether a CEO was appointed before or after the firm’s IPO. We further constructed a variable, proportion of new directors, to capture the percentage of new directors who joined the board after the CEO took office, because these new directors tend to be beholden to the CEO for their directorship and may weaken board monitoring (Coles et al., 2014; Shivdasani & Yermack, 1999).

Next, we included three commonly used variables to account for the controlling family’s influence in corporate governance: family ownership, family directorship, and nonfamily block ownership (La Porta et al., 1999; Young et al., 2008). We traced both direct and indirect equity owned by the controlling family based on information in the TEJ database and company annual reports and calculated family ownership as the proportion of shares collectively held by all family members. We calculated family directorship as the proportion of directors who were family members on the board. The average family ownership was 30.9%, and the average family directorship was 63.3%. Such high levels of family ownership and family directorship gave us great confidence that the controlling families in the sample had both the incentive to monitor CEOs and the power to hold them accountable for firm performance. We constructed nonfamily block ownership to control their influences on corporate governance (Li, 2018). It was measured by the accumulated ownership held by the top 10 nonfamily shareholders (Denis et al., 1997).

At the firm level, we included firm size, firm age, and leverage as controls. Firm size and firm age may influence the level of formalization in CEO succession (Ocasio, 1999; Wiersema & Zhang, 2011). Firm size was measured as the natural logarithm of the family firm’s total assets, and firm age was the natural logarithm of the number of years since the founding of the firm. We controlled for leverage as it may affect the likelihood of bankruptcy and financial distress, thereby influencing the likelihood of CEO turnover (Daily & Dalton, 1995; Lehn & Zhao, 2006). We calculated leverage as the percentage of a firm’s total debt to its equity. We also added a set of industry and year dummy variables to control for industry and temporal effects on CEO turnover.

Statistical Analyses

Because our dependent variable CEO turnover is dichotomous and our research focus is on the effect of firm performance during different stages of CEO tenure, we used maximum-likelihood logistic regression to test our theory and hypotheses. The logistic regression model is fitted by the logit transformation of the probability of the event of interest (i.e., Pr (y = 1| X)), where y is the event of interest (CEO turnover in our study), and X is a vector of independent and control variables, as illustrated as follows:

The above equations suggest that the coefficients B in a logit model can be interpreted similarly to those in an ordinary least squares (OLS) regression. Specifically, a positive (negative) β i means that xi has a positive (negative) impact on the occurrence of the dependent variable, although the impact is not linear (Hoetker, 2007; Wiersema & Bowen, 2009). Logistic regression has been widely used in prior studies of CEO turnover, including CEO turnover in family-controlled firms (e.g., Goyal & Park, 2002; Lehn & Zhao, 2006; Li, 2018). Because we had a panel data set with each CEO having multiple yearly observations, we grouped the observations at the CEO level and conducted logistic regression analysis using xtlogit provided in Stata. Given that firm performance could be influenced by CEO turnover (Finkelstein et al., 2009), we followed prior studies (Shen & Cannella, 2002; Wiersema & Zhang, 2011) and examined the effect of firm performance in year t−1, instead of firm performance in year t, on the likelihood of CEO turnover in year t to minimize the impact of simultaneous causality between firm performance and CEO turnover in year t on the results.

Results

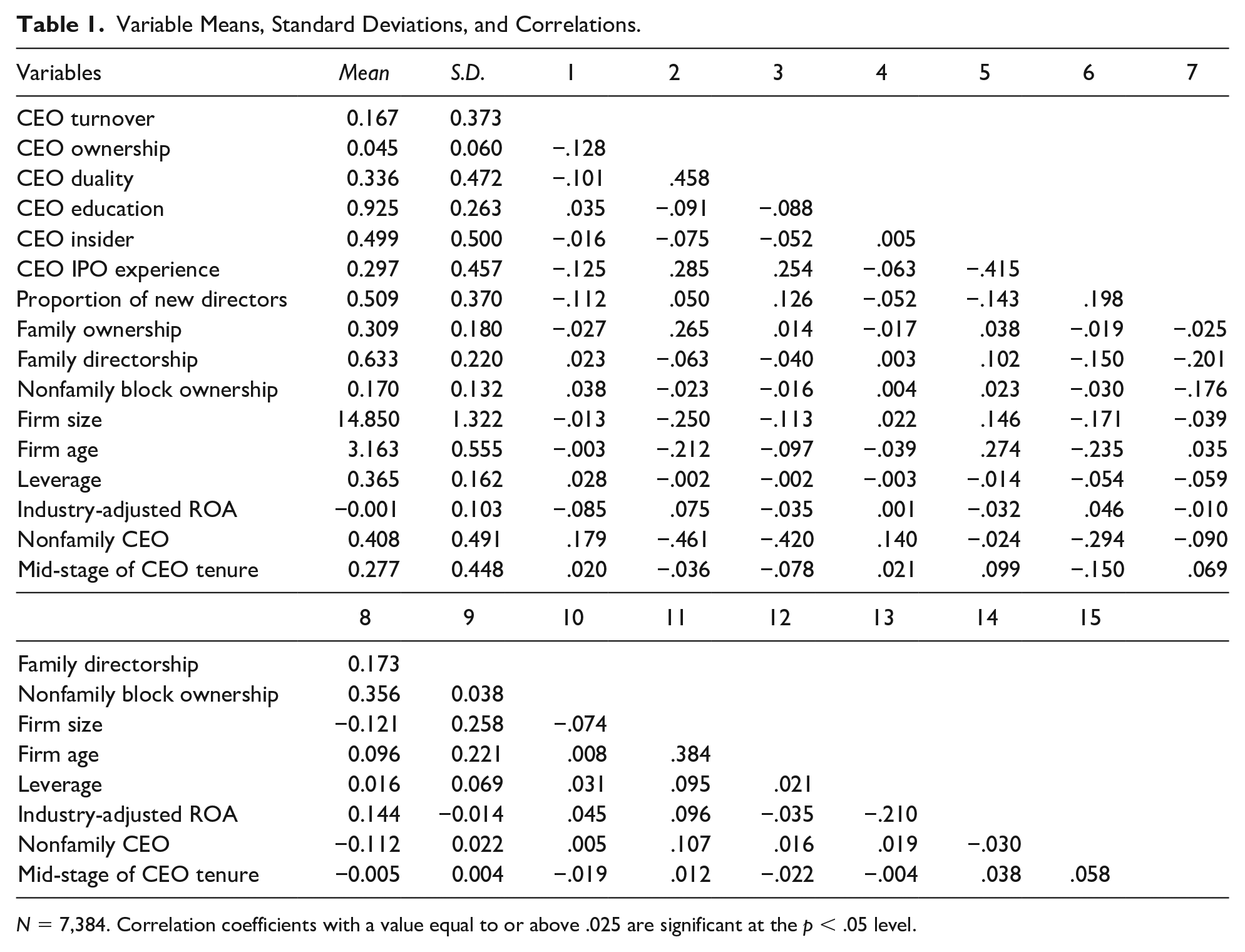

Table 1 reports variable means, standard deviations, and correlation coefficients. Table 2 reports results from the full sample logistic regression analysis. Model 1 includes control variables only, Model 2 adds industry-adjusted ROA, and Model 3 is the full model with the interaction between industry-adjusted ROA and mid-stage CEO tenure. While we did not propose a formal hypothesis about the negative effect of firm performance on CEO turnover that has been well-established in prior research on family firms (G. Chen et al., 2015; Li, 2018), we wanted to confirm its presence in our sample so that our findings would be comparable to previous. The coefficient of industry-adjusted ROA (b = −2.410, p = .000) is negative and statistically significant in Model 2. Our further analysis of the marginal effects revealed that a decrease of one standard deviation in industry-adjusted ROA from the mean increased the probability of CEO turnover by 6.18 percentage points. These results are consistent with previous findings, giving us confidence in the quality of our data. In addition, they provided us the foundation to examine whether the negative effect of firm performance on CEO turnover varies at different stages of CEO tenure.

Variable Means, Standard Deviations, and Correlations.

N = 7,384. Correlation coefficients with a value equal to or above .025 are significant at the p < .05 level.

Logit Model of CEO Turnover Across Different Stages of CEO Tenure (Full Sample).

Robust standard errors are in the parentheses, and p-values are in italics.

H1 predicts that the negative effect of firm performance on CEO turnover is stronger during the mid-stage of CEO tenure than during the early and late stages. We tested in Model 3. The results show that the interaction between industry-adjusted ROA and mid-stage CEO tenure is negative and statistically significant (b = −2.002, p = .080). Our further analysis of the marginal effects revealed that when industry-adjusted ROA decreased one standard deviation from the mean, the probability of CEO turnover increased by 9.63 percentage points during the mid-stage of CEO tenure, but only by 4.72 percentage points during the early and late stages. These findings provide support for H1.

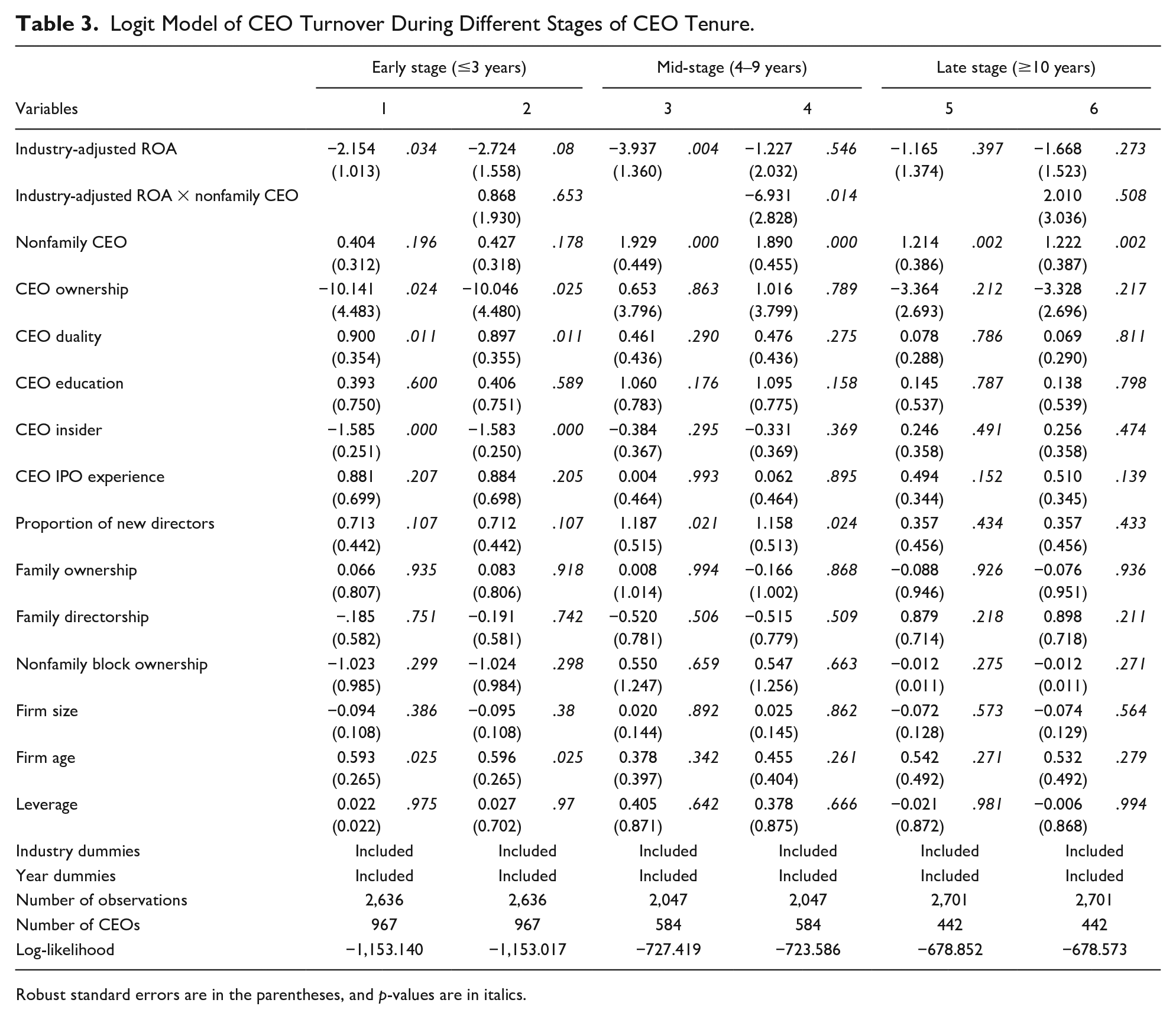

H2 predicts that the negative effect of firm performance on CEO turnover is stronger for nonfamily CEOs than for family CEOs only during the mid-stage of CEO tenure. We tested it by examining the effects of firm performance on CEO turnover during the early, mid-, and late stages of CEO tenure, respectively, and reported the results in Table 3. For each stage, we first examined the main effect of industry-adjusted ROA and then its interaction with nonfamily CEO on CEO turnover. Models 1 and 2 report results for the early stage, the first 3 years of CEO tenure. While Model 1 shows that industry-adjusted ROA has a significant negative effect (b = −2.154, p = .034), Model 2 shows that its interaction with nonfamily CEO does not have a significant effect on CEO turnover (b = 0.868, p = .653). Models 3 and 4 report results for the mid-stage, from year 4 to year 9 of CEO tenure. Model 3 shows that industry-adjusted ROA has a significant negative effect (b = −3.937, p = .004), and Model 4 shows that its interaction with nonfamily CEO also has a significant negative effect on CEO turnover (b = −6.931, p = .014). Models 5 and 6 report results for the late stage, starting from year 10 of CEO tenure. Model 5 shows that industry-adjusted ROA does not have a significant negative effect (b = −1.165, p = .397), and Model 6 shows that its interaction with nonfamily CEO does not have a significant negative effect on CEO turnover (b = 2.010, p = .508). Taken together, these results suggest that firm performance has a stronger negative effect on the turnover of nonfamily CEOs than on the turnover of family CEOs only during the mid-stage of CEO tenure, providing support for H2.

Logit Model of CEO Turnover During Different Stages of CEO Tenure.

Robust standard errors are in the parentheses, and p-values are in italics.

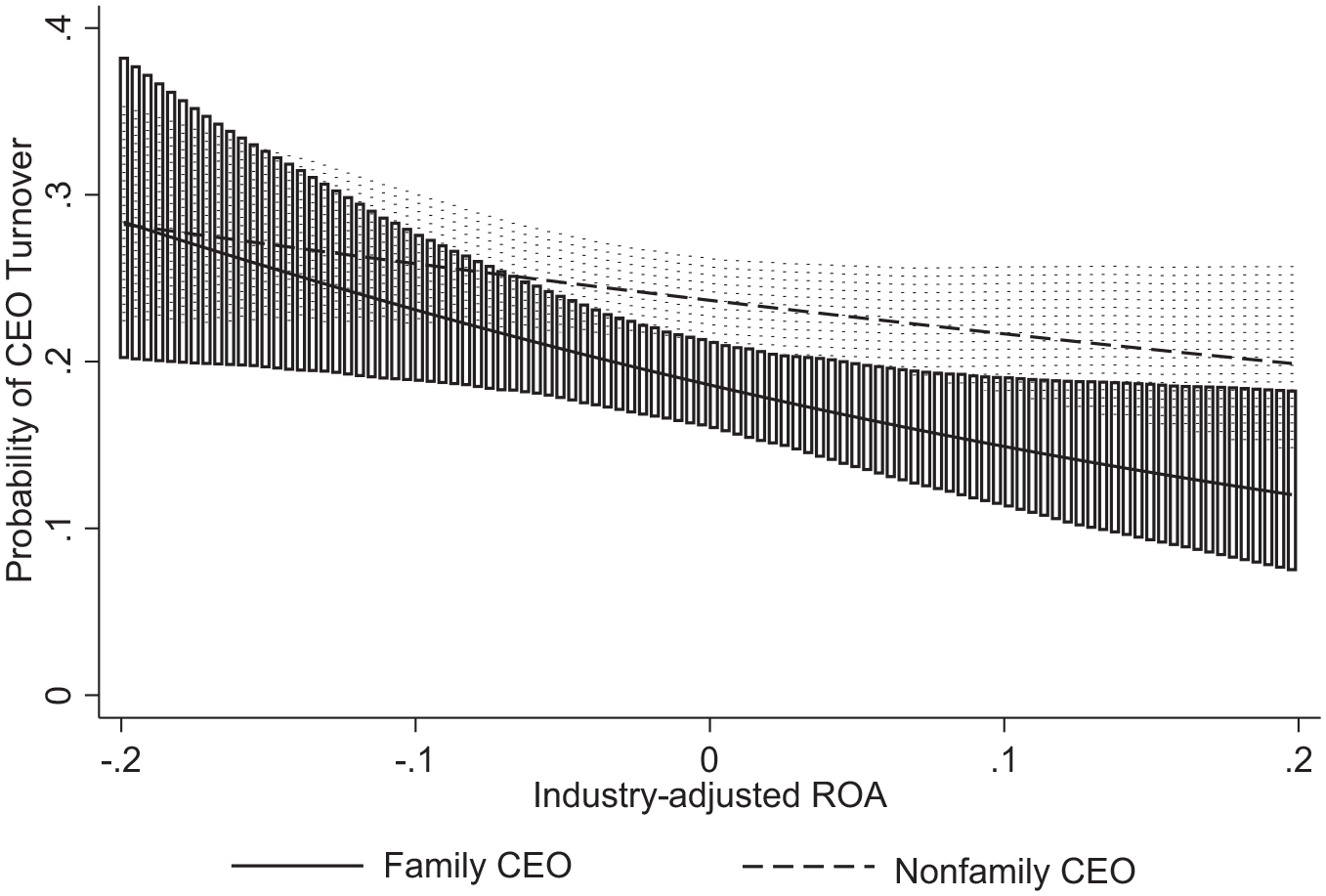

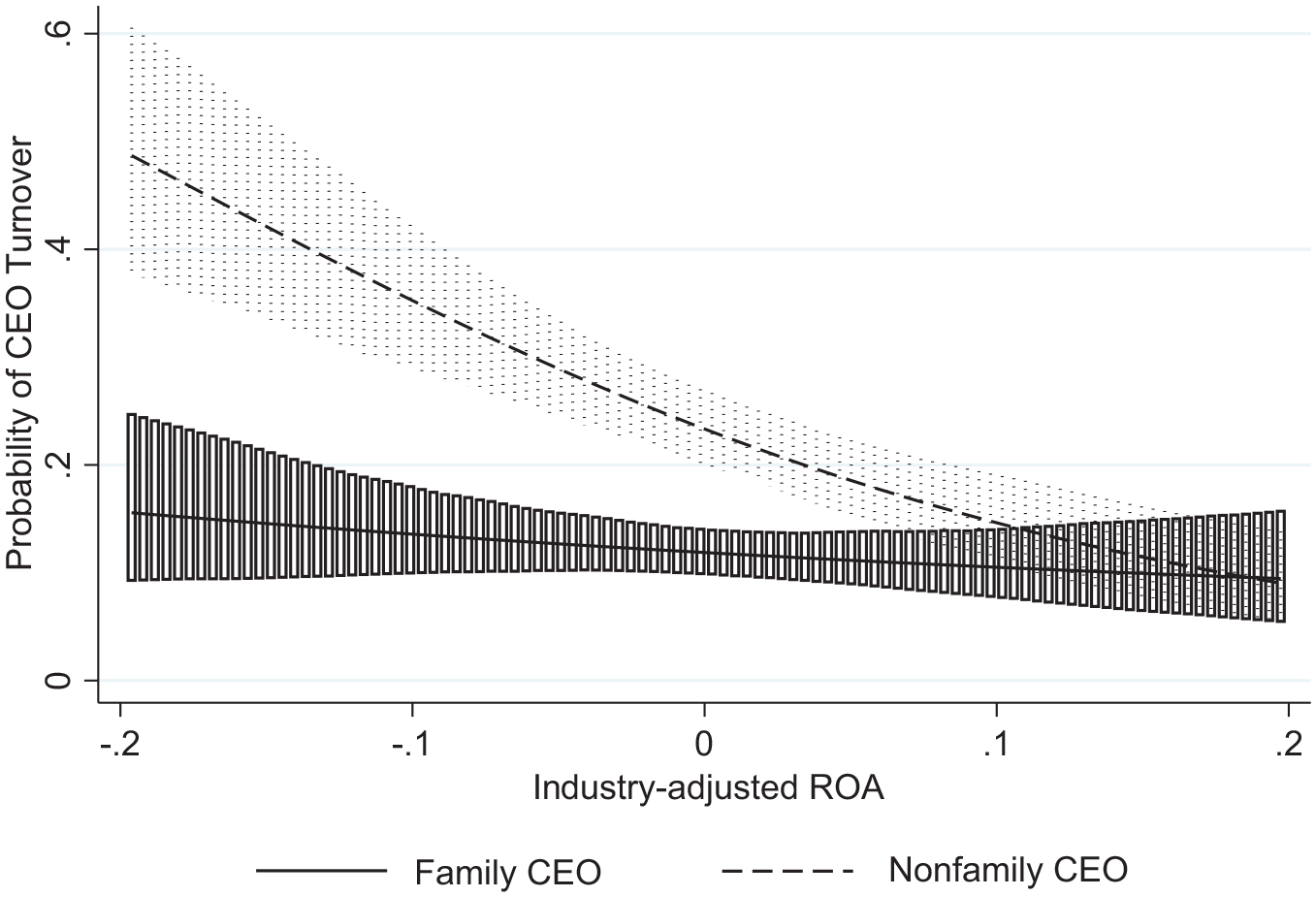

To ensure that the above interpretation of the nonlinear interaction effects was correct, we plotted the marginal effects of industry-adjusted ROA on the probability of CEO turnover during each stage of CEO tenure using a simulation-based logistic estimator with robust standard errors. This simulation-based approach derives the robust standard errors of the marginal effects for each observation based on repeated simulations from the multivariate normal distribution and thus produces more accurate estimates (Zelner, 2009). We used the results from Models 2, 4, and 6 of Table 3 to derive the estimated marginal effects of industry-adjusted ROA on the probability of CEO turnover for family and nonfamily CEOs separately, while holding all the other continuous explanatory variables at their means and significant binary variables at 1. Figures 1 to 3 present the estimated marginal effects with 95% confidence intervals during the early, mid-, and late stages of CEO tenure, respectively.

Effects of Firm Performance on CEO Turnover During the Early Stage of CEO Tenure.

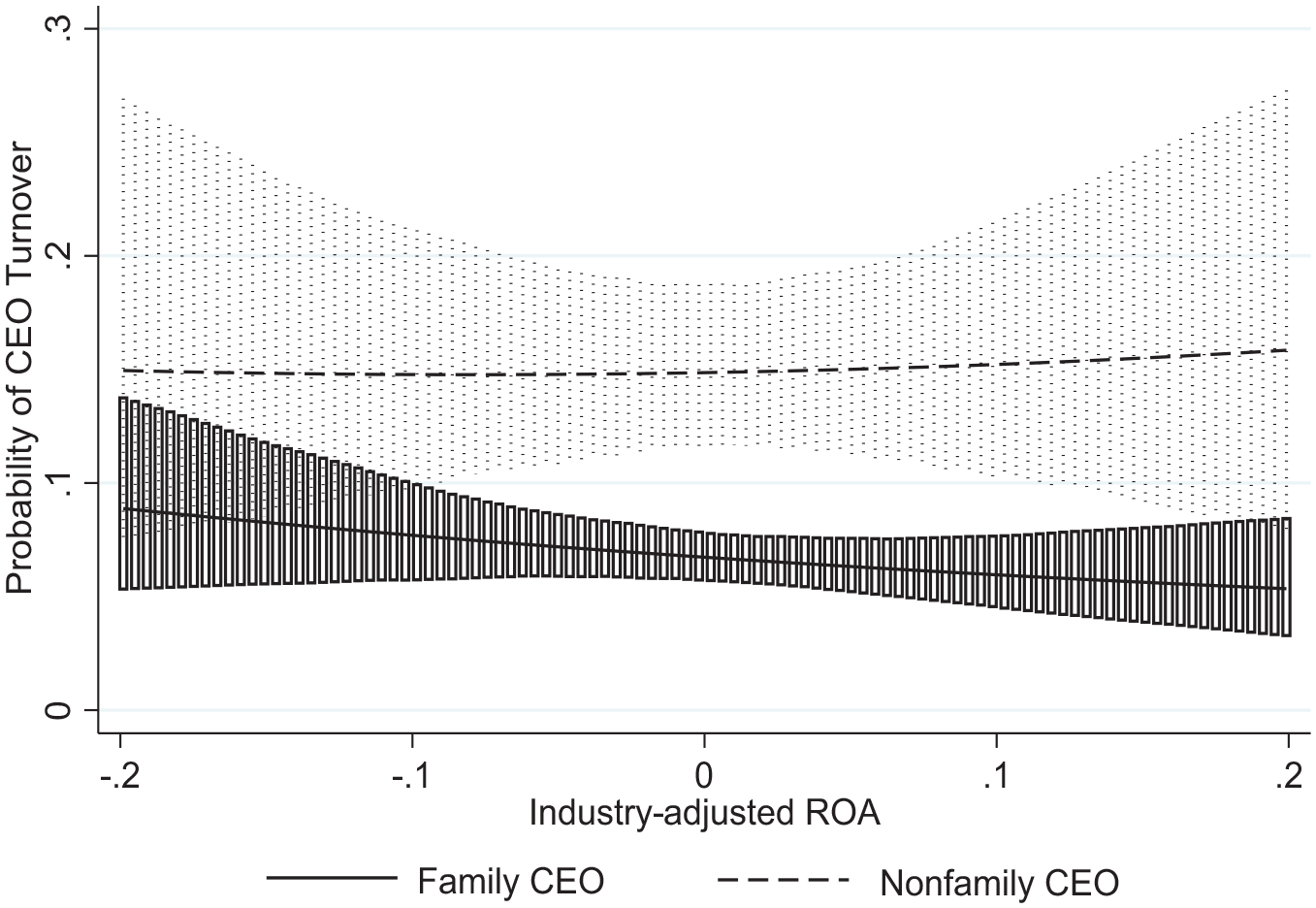

Effects of Firm Performance on CEO Turnover During the Mid-Stage of CEO Tenure.

Effects of Firm Performance on CEO Turnover During the Late-Stage of CEO Tenure.

Figure 1 shows a significant overlap in the marginal effects of industry-adjusted ROA on the turnover of family CEOs and nonfamily CEOs, indicating that the negative effect of firm performance on family CEO turnover is not significantly different from nonfamily CEO turnover during the early stage of CEO tenure. 1 Figure 2 shows that industry-adjusted ROA’s marginal effects on nonfamily CEO turnover are far above its effects on family CEO turnover when it is below zero, suggesting that poor firm performance has a stronger effect on the turnover of nonfamily CEOs than on the turnover of family CEOs. Figure 3 shows that the marginal effects of industry-adjusted ROA on CEO turnover remain almost constant for both family and nonfamily CEOs, and they overlap at both the low and the high end of industry-adjusted ROA. This finding suggests that firm performance does not have a significant negative effect on CEO turnover during the late stage of CEO tenure nor a stronger negative effect on the turnover of nonfamily CEOs than on the turnover of family CEOs. Taken together, Figures 1 to 3 provide further support for H2.

Supplementary Analyses

We conducted seven sets of supplementary analyses to check the robustness of the findings. First, we conducted analyses using alternative measures of firm performance, a key variable in our study. In the primary analysis, we used ROA to measure firm performance. To evaluate the robustness of our results, we used earnings per share (EPS) as an alternative measure. We also used a 2-year window to calculate the 2-year moving average of firm performance (during years t−2 and t−1) and examined its effect on CEO turnover in year t. These additional analyses generated consistent results as those in the primary analysis, providing greater confidence in our findings about how the effect of firm performance on CEO turnover changes over CEO tenure in family-controlled firms.

Second, we conducted analyses using an alternative measure of CEO turnover that included only turnovers caused by factors that are unrelated to CEO competence, such as routine retirement, death, and health issues. Our theory suggests that the negative impact of firm performance on CEO turnover changes across CEO tenure because family owners’ reliance on firm performance to assess CEO competence varies at different stages of CEO tenure. Thus, our prediction of the negative relationship between firm performance and CEO turnover focuses on forced or involuntary CEO exits caused by family owners’ assessment of CEO competence based on firm performance. When we replaced the measure with turnovers caused by factors that were unrelated to CEO competence, the negative effect of firm performance that we found in the primary analysis would weaken or disappear. The results are consistent with this expectation, showing that firm performance does not have a statistically significant negative effect on the alternative measure of CEO turnover (b = −3.268, p = .224). This finding gave us greater confidence in our theory that highlights how family owners use firm performance as a competence signal to make CEO replacement decisions at different stages of CEO tenure.

Third, we conducted analyses to check whether the weakened effect of firm performance on CEO turnover was caused by an increase in CEOs’ structural power over time (Ocasio, 1994; Shen, 2003). Although we included many variables, such as CEO ownership, duality, education, insider status, and new directors appointed after the CEO, to control the effect of CEO power, it is still important to rule out this alternative explanation. Given that CEO duality is widely considered the most significant structural arrangement that promotes CEO entrenchment (Finkelstein & D’Aveni, 1994; Young et al., 2008), we analyzed the likelihood of turnover for CEOs who did not hold the board chair position. We also conducted robustness checks among family firms with over 50% family presence on the board (i.e., family-dominated firms). Results from these analyses are consistent with those reported in Tables 2 and 3. This finding suggests that the weakened effect of firm performance on CEO turnover during the late stage of CEO tenure was unlikely driven by powerful CEOs who held the board chair position or family firms where family owners did not have a dominant presence on the board.

Fourth, we examined whether our theory and findings would apply to inside CEOs who have been working in the firm for a while. Research on the stages of CEO tenure suggests that inside CEOs also need time to learn about their firms and the external environment because the CEO’s job demands are significantly different from those of their prior positions within the firm (Gabarro, 1987; Miller & Shamsie, 2001; Shen, 2003). However, one might argue that family owners would expect inside CEOs to impact firm performance sooner or immediately because of their existing firm-specific knowledge. To examine this possibility, we conducted analyses on the subsample of inside CEOs and found that (a) the negative effect of industry-adjusted ROA on CEO turnover is stronger during the mid-stage of CEO tenure and that (b) neither industry-adjusted ROA nor its interaction with nonfamily CEO has a significant effect on CEO turnover during the early stage of CEO tenure. These findings do not support the argument that family owners hold inside CEOs accountable for firm performance soon after they take office. Instead, they suggest that family owners also give inside CEOs time to formulate and implement their strategies.

Fifth, we examined whether firm performance had a stronger effect on CEO turnover during the mid-stage than during the early stage. Results in Model 1 and Model 3 of Table 3 show that industry-adjusted ROA is negatively associated with CEO turnover during both the early stage (b = −2.154, p = .034) and the mid-stage (b = −3.937, p = .004), raising the question of whether family owners hold CEOs more accountable for firm performance during the mid-stage than during the early stage. We thus created a subsample by combining observations during the early and mid-stages of CEO tenure and conducted analysis to directly address this issue. The results are reported in Appendix A. Model 1 shows that industry-adjusted ROA has a negative effect (b = −2.822, p = .000) and mid-stage has a positive effect (b = 0.540, p = .001) on CEO turnover. Model 2 shows that their interaction has a negative effect (b = −2.591, p = .043), while their respective main effects remain the same as in Model 1. These results suggest that industry-adjusted ROA has a stronger negative effect on CEO turnover during the mid-stage than during the early stage, providing further support for our theory that family owners hold CEO more accountable for firm performance during the mid-stage of CEO tenure.

Sixth, we tested whether our results suffered from potential endogeneity caused by omitted variables (Hill et al., 2021; Semadeni et al., 2014). Although we included many control variables to rule out potential confounding effects, we could still have omitted some important variables. Following Busenbark et al. (2022), we used the robustness of inference to replacement (RIR) to address this issue. The results suggest that to invalidate our inference about the effects of firm performance and mid-stage tenure on CEO turnover, 48.9% and 53.8% of the estimates in Table 2 would have to be due to omitted variable bias (i.e., 3,611 and 3,972 of the 7,384 observations would have to be replaced by observations with zero effect). Moreover, to invalidate our inference about the differential effect of firm performance on family versus nonfamily CEO turnover during the mid-stage of CEO tenure, 32.3% of the estimates in Model 4 of Table 3 would have to be due to omitted variable bias (i.e., 661 of the 2,047 observations during the mid-stage would have to be replaced by observations with zero effect). Although absolute standards for impact thresholds are difficult to establish as the contexts of estimates differ, the above findings give us confidence that our results are unlikely to suffer from omitted variable bias to such an extent that would alter our conclusions.

Finally, we examined whether the negative effect of firm performance on CEO turnover we found was driven by CEO tenure. Our primary analysis used firm performance in year t−1 to predict CEO turnover in year t to minimize the impact of simultaneous causality between firm performance and CEO turnover in year t on the results and explicitly accounted for the effect of CEO tenure stage on CEO turnover. However, one may still argue that CEO tenure can simultaneously influence both firm performance and CEO turnover and thus lead to a spurious correlation between them. To address this issue, we conducted a two-stage analysis (Gu et al., 2024; Zhu et al., 2020). Specifically, we first regressed firm performance on CEO tenure and then used the residuals of firm performance unexplained by CEO tenure in year t–1 to predict CEO turnover in year t. The first-stage analysis shows that the mid-stage of CEO tenure has a significant positive effect on firm performance (b = 0.007, p = .008). The second-stage analysis shows that the residuals of firm performance have a negative effect on CEO turnover (b = −2.454, p = .000) and that this negative effect is stronger during the mid-stage of CEO tenure (b = −2.203, p = .057), consistent with findings of the primary analysis. Taken together, results of all the above supplementary analyses, available upon request, provide further support for our theoretical predictions about the negative effect of firm performance on CEO turnover in family firms.

Discussion

Integrating insights from research on family owners’ SEW and long-term orientation (Gomez-Mejia et al., 2007, 2011; Le Breton-Miller et al., 2011) and research on the seasons of CEO tenure (Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001; Shen, 2003), this study proposed a dynamic perspective about the impact of firm performance on CEO turnover in family firms. We theorized that family owners take into account the impact of CEOs on firm performance in their use of firm performance to make CEO replacement decisions at different stages of CEO tenure. Using data from a sample of family-controlled firms in Taiwan, we found that the negative effect of firm performance on CEO turnover was stronger during the mid-stage of CEO tenure than during the early and late stages. Moreover, we found that firm performance had a stronger negative effect on the turnover of nonfamily CEOs than on the turnover of family CEOs only during the mid-stage of CEO tenure. These findings supported our dynamic perspective about the impact of firm performance on CEO turnover at different stages of CEO tenure in family firms.

Contributions

Our study makes several contributions to the literature on CEO assessment and agency contracts in family businesses. First, it contributes to the understanding of the impact of firm performance on CEO assessment and turnover during the early, mid-, and late stages of CEO tenure in family-controlled firms. While prior studies consistently found that firm performance has a negative effect on CEO turnover in family firms (e.g., X. Chen et al., 2013; Gomez-Mejia et al., 2001; Li, 2018), they did not investigate whether this negative effect varied over CEO tenure. We predicted and found that it was stronger during the mid-stage of CEO tenure than during the early and late stages. This finding supports our theory that family owners consider the impact of CEOs on firm performance at different stages of CEO tenure in their use of firm performance to assess CEO competence and make CEO replacement decisions. Compared to prior research that did not consider CEO tenure (e.g., X. Chen et al., 2013; Li, 2018) and that focused only on the early stage (Graffin et al., 2013; Shen & Cannella, 2002) or the late stage (Ocasio, 1994), our study provides a more systematic investigation of the variation in the impact of firm performance on CEO turnover during the early, mid-, and late stages of CEO tenure in family firms. Moreover, it introduces a novel dynamic perspective to predict and explain this variation by integrating insights on family owners’ long-term orientation (Gomez-Mejia et al., 2007, 2011; Le Breton-Miller et al., 2011) and the stages of CEO tenure (Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001).

Second, our theory and supportive findings contribute to the understanding of agency contracts and corporate governance in family businesses, particularly regarding the extent to which family owners rely on firm performance to assess CEO competence during the different stages of CEO tenure. The impact of firm performance on CEO turnover has long been considered to reflect an important aspect of agency contracts and corporate governance, that is, holding CEOs accountable for firm performance (Fama & Jensen, 1983). Meanwhile, scholars recognize that firm performance may not be a good indicator of CEO competence during the early stage of CEO tenure (Graffin et al., 2013; Shen, 2003) and that boards rely less on firm performance to assess CEOs after they gain significant knowledge of the CEOs’ competence over time (Hermalin & Weisbach, 1998; Murphy, 1986). Our study suggests that family owners also recognize that firm performance is not always a good indicator of CEO competence throughout the entire CEO tenure. They thus adjust agency contracts with CEOs accordingly regarding the extent to which they rely on firm performance to assess and replace CEOs. Specifically, they rely on firm performance more during the mid-stage of CEO tenure than during the early and late stages to make CEO replacement decisions. Therefore, our theory and supportive findings advance the understanding of the role of firm performance in agency contracts at family firms during different stages of CEO tenure.

Third, our study contributes to the literature on family owners’ relationships with family versus nonfamily CEOs in terms of whether family owners always treat them differently. The existing studies took a largely static view and suggested the existence of differential agency contracts for family and nonfamily CEOs throughout CEO tenure, as demonstrated by the different impacts of firm performance on their pay and turnover (Bassanini et al., 2013; Gomez-Mejia et al., 2001; Li, 2018; Nason et al., 2018). In contrast, our study took a more dynamic view and revealed that firm performance has a stronger negative effect on the turnover of nonfamily CEOs than family CEOs only during the mid-stage of CEO tenure, but not during the early or late stage. This finding does not support the argument that family owners always hold nonfamily CEOs more accountable than family CEOs for firm performance; instead, it suggests that family owners adjust agency contracts for family and nonfamily CEOs based on the stage of CEO tenure. In this regard, our study contributes to the literature on family owners’ relationships with family versus nonfamily CEOs by advancing a dynamic perspective that explains how and why the relationships change over different stages of CEO tenure.

Directions for Future Research

Our study points out several directions for future research on family businesses. First, future research may investigate how family owners assess CEOs during the early stage of CEO tenure. Our theory and findings suggest that family owners rely less on firm performance to assess new CEOs and do not treat nonfamily CEOs differently from family CEOs during this stage. While we argued that family owners likely rely more on behavior-based strategic control (i.e., monitoring new CEOs’ strategic decisions and actions) to ensure their long-term financial wealth and SEW, it was beyond the scope of the current study to investigate how family owners assess new CEOs’ strategic decisions and actions or what other factors family owners also consider in deciding whether to retain or replace a new CEO. The results in Model 1 of Table 3 are noteworthy in two aspects in addition to the insignificant coefficient for nonfamily CEO. The first is the negative coefficient for industry-adjusted ROA (b = −2.154, p = .034), suggesting that family owners do use firm performance to make CEO replacement decisions during the early stage of CEO tenure (although they rely more on firm performance to assess CEOs during the mid-stage, as indicated by the results in Model 2 of Appendix A). The second is the negative coefficient for CEO insider (b = −1.585, p = .000), suggesting that family owners treat inside and outside CEOs differently during the early stage of CEO tenure. Moreover, the results of our supplementary analyses on inside CEOs do not suggest that family owners hold inside CEOs accountable for firm performance immediately after they take office. Thus, future research may investigate whether family owners treat inside and outside CEOs differently in performance assessment during the early stage of CEO tenure. For example, given the prevalence of intergroup bias in social evaluations (Zhu et al., 2014), one may examine whether family owners exhibit ingroup favoritism toward inside CEOs and assess their strategic actions and performance more favorably than outside CEOs.’

Second, researchers may investigate how family owners assess CEOs during the late stage of CEO tenure. Our study suggests that family owners rely less on firm performance to assess CEOs who have survived the mid-stage by proving their competence. Because CEOs tend to rest on their past strategies during the late stage (Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001), it becomes imperative for family owners to ensure that these CEOs engage in strategic exploration for long-term firm success (Shen, 2003). Future research may examine how family owners motivate and assess CEOs during the late stage of CEO tenure. While we argued that family owners would rely more on behavior-based strategic control (i.e., actively monitoring CEOs’ strategic decisions), they may also use long-term–oriented incentives and outcomes such as stock ownership and patent applications, or a combination of them in corporate governance. Future research may investigate how the practices vary across countries or cultures (Berrone et al., 2022). In addition, although we did not find firm performance to significantly impact CEO turnover during the late stage, the results in Models 5 and 6 of Table 3 show that nonfamily CEOs had a higher risk of turnover than family CEOs. Investigating what caused this difference can further enhance the understanding of family owners’ relationships with family CEOs and nonfamily CEOs during the late stage of CEO tenure.

Relatedly, future research can investigate how family owners’ relationships with CEOs during the late stage of CEO tenure influence firm strategies and performance. Prior research showed that CEOs tend to resist strategic change during the late stage of their tenure, which can lead to a mismatch between firm strategies and environmental demands and eventually hurt firm performance (Miller, 1991; Miller & Shamsie, 2001; Shen, 2003). It would be interesting and important to examine whether such a tendency also exists in the context of family firms and what family owners do to reduce the chance for it to happen. For example, our study suggests that family owners focus more on strategic decisions and less on firm performance in CEO assessment during the late stage to encourage CEOs to engage in strategic exploration for long-term success. Future research can thus examine whether family owners’ reduced focus on firm performance in CEO assessment helps to promote strategic exploration and reduce strategic persistence, whether the effect differs between family and nonfamily CEOs, and how it influences family firms’ long-term performance and survival.

Conclusion

By advancing a dynamic perspective, our study revealed two novel findings about the negative effect of firm performance on CEO turnover in family-controlled firms. First, it is stronger during the mid-stage of CEO tenure than during the early and late stages. Second, it is stronger for nonfamily CEOs than for family CEOs only during the mid-stage, but not during the early or late stage. Our dynamic perspective and supportive findings contribute to the understanding of agency contracts for CEOs at family firms, including for both family CEOs and nonfamily CEOs, at different stages of CEO tenure. They also have important implications for future research on family businesses. We hope that our study will encourage scholars to pay more attention to the stages of CEO tenure in their study of agency contracts in family firms, as well as the dynamic relationships family owners have with family versus nonfamily CEOs during each stage.

Footnotes

Appendix

Logit Model of CEO Turnover During Early and Mid-Stages of CEO Tenure.

| Variables | 1 | 2 | ||

|---|---|---|---|---|

| Industry-adjusted ROA | −2.822 (0.747) |

.000 | −1.901 (0.906) |

.036 |

| Mid-stage | 0.540 (0.158) |

.001 | 0.509 (0.156) |

.001 |

| Industry-adjusted ROA × mid-stage | −2.591 |

.043 | ||

| Nonfamily CEO | 1.019 |

.000 | 1.015 |

.000 |

| CEO ownership | −6.440 |

.050 | −6.482 |

.048 |

| CEO duality | 0.592 |

.031 | 0.615 |

.025 |

| CEO education | 0.878 |

.138 | 0.879 |

.136 |

| CEO insider | −1.238 |

.000 | −1.258 |

.000 |

| CEO IPO experience | −0.346 |

.294 | −0.330 |

.323 |

| Proportion of new directors | 1.041 |

.001 | 1.027 |

.001 |

| Family ownership | 0.516 |

.418 | 0.455 |

.476 |

| Family directorship | −0.266 |

.574 | −0.250 |

.597 |

| Nonfamily block ownership | −0.320 |

.659 | −0.327 |

.652 |

| Firm size | −0.035 |

.659 | −0.037 |

.680 |

| Firm age | 0.521 |

.023 | 0.529 |

.021 |

| Leverage | 0.400 |

.447 | 0.388 |

.460 |

| Industry dummies | Included | Included | ||

| Year dummies | Included | Included | ||

| Number of observations | 4,683 | 4,683 | ||

| Number of CEOs | 1,121 | 1,121 | ||

| Log-likelihood | −1,809.56 | −1,807.417 | ||

Robust standard errors are in the parentheses, and p-values are in italics.

Acknowledgements

The authors thank Associate Editor Alfredo De Massis and two anonymous reviewers for their helpful comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.