Abstract

Ever since scholars recognized that family firms are heterogeneous, many studies have attempted to compare different types of family firms without ensuring that the source of heterogeneity is unique to family firms. When the source of heterogeneity among family firms resembles the source of heterogeneity among nonfamily firms, the problem of counterfactual indeterminacy bias can lead to misleading or irrelevant findings that fail to distinguish the effects of family influence from factors that affect all firms. We delineate common forms of this bias and offer recommendations to prevent it in research on family firm behavior and performance.

Research Questions

What is counterfactual indeterminacy bias, and why are explicit family–nonfamily comparisons essential?

How does the omission, oversimplification, or static treatment of nonfamily firms distort inferences about family firm behavior and performance?

What practical steps can family business scholars take to specify, justify, and theorize about nonfamily reference groups so that comparative claims are theoretically and empirically robust?

Implications for Practice

Findings drawn from family-firm-only samples can produce misleading narratives, and patterns attributed to “family influence” (e.g., founder superiority over successors) may simply reflect dynamics common to all firms.

Treat “nonfamily firms” as a heterogeneous category. State-owned enterprises, founder-led startups, venture-backed firms, and widely held corporations operate under very different logics; advisors and owners should align comparison groups with their firm’s actual context rather than rely on generic “nonfamily” benchmarks.

Demand comparative grounding from research-based advice. Educators, consultants, and family business institutes should ensure that recommendations rest on properly specified family–nonfamily comparisons; otherwise, prescriptions may overstate family firm exceptionalism and lead owners and successors astray.

Policymakers and institutions that support family enterprises should avoid treating family firms as a uniform or inherently distinct category. Policies related to succession, governance, taxation, or small-and medium-sized enterprise (SME) support should be grounded in comparative evidence that distinguishes genuinely family-specific dynamics from broader organizational patterns.

Introduction

In family firm research, nonfamily firms are frequently employed explicitly or implicitly as the reference group against which family firms are compared (Chua et al., 1999; Sharma, 2004). This is necessary because the theoretical foundation of the field rests on the premise that family firms exhibit unique characteristics and behaviors that distinguish them from nonfamily firms. These include, among others, long-term orientation (Chua et al., 2025; Lumpkin & Brigham, 2011; Zellweger, 2007), family governance (Le Breton-Miller & Miller, 2009; Miller & Le Breton-Miller, 2006; Villalonga & Amit, 2006), familiness resources (Habbershon & Williams, 1999), and prioritization of family-centered noneconomic (FCN) goals that generate socioemotional wealth (Berrone et al., 2012; Gómez-Mejía et al., 2007). These theoretical assumptions have spurred a large and growing body of studies comparing family and nonfamily firms (Chrisman & Patel, 2012; Miller et al., 2007).

More recently, however, the literature has shifted toward investigating heterogeneity among family firms, to unpack how, when, and why certain family firms differ from others in strategic behavior, governance, or performance outcomes (Chua et al., 2012; Daspit et al., 2021; Neubaum et al., 2019; Nordqvist et al., 2014; Steier et al., 2015). This shift has deepened our understanding of family firm complexity. Yet, alongside this progress, a critical theoretical misconception has emerged: that heterogeneity among family firms alone provides a sufficient basis for their study, on the assumption that such heterogeneity either does not exist in nonfamily firms or is not comparable to that observed among family firms. This misconception overlooks a fundamental point: because heterogeneity among family firms is typically attributed to family involvement and influence, any claim about what distinguishes one type of family firm from another carries an implicit assumption about how nonfamily firms behave, an assumption that should be theoretically grounded rather than taken for granted.

By contrast, we argue that investigating the differences between family and nonfamily firms remains a fundamental concern of family business studies, and even studies of family firm heterogeneity must be based on characteristics that theoretically distinguish family and nonfamily firms. Otherwise, comparisons of family firms will devolve into comparisons of firms, with the family component only serving as a sampling frame. 1

We refer to this issue as counterfactual indeterminacy bias, a situation in which researchers examine how a focal variable (e.g., family ownership) affects outcomes while implicitly assuming its counterpart (e.g., nonfamily ownership) lacks analogous characteristics that are comparatively important. Unlike discussions of endogeneity or selection bias, counterfactual indeterminacy bias is concerned with whether the theoretical comparison of family and nonfamily firms along the dimension(s) analyzed is meaningful. If it is not, then the theoretical value in comparing different types of family firms along those dimensions is minimal. The problem of counterfactual indeterminacy bias bears a conceptual resemblance to the control-group issue in experimental sciences, where the absence or misspecification of a control group undermines the ability to isolate treatment effects from background noise (Campbell & Stanley, 2015; Rubin, 1974; Shadish et al., 2002). This logic has been extended to observational research through the potential outcomes framework, which holds that causal claims require a plausible counterfactual, that is, a credible estimate of what would have occurred in the absence of the treatment (Imbens & Rubin, 2015; Morgan & Winship, 2015). The omission, misspecification, or static treatment of reference groups in family business studies parallels design flaws in uncontrolled or contaminated experiments. Integrating the control-group logic from the hard sciences offers not only a powerful methodological analogy but also a practical blueprint for improving causal inference, enhancing theoretical precision, and strengthening the cumulative validity of family business research. However, this does not mean that every study requires a nonfamily control group. 2 It only means that every study that compares different types of family firms should be based on characteristics or behaviors that distinguish family firms and nonfamily firms or are unique to family firms. Otherwise, again, the study will theoretically devolve into a comparison of firms using a family business sample, not a comparison of family firms.

It is important to distinguish counterfactual indeterminacy bias from methodological concerns that are already well recognized in organizational research. Endogeneity corrections (e.g., instrumental variables, Heckman selection models) address whether a coefficient estimate is unbiased given the model specification. Control variables absorb variance attributable to observed confounders to sharpen the focal estimate. Both operate within a given research design and assume that the comparison of interest is itself meaningful. Counterfactual indeterminacy bias, by contrast, is concerned with whether the variables being examined are likely to vary in type or level between family firms and the nonfamily reference group. A study can be econometrically well-identified, free of endogeneity concerns and equipped with a comprehensive set of controls, yet still produce misleading or irrelevant conclusions if the nonfamily reference group is omitted, poorly theorized, or assumed to be homogeneous and stable. In this sense, counterfactual indeterminacy bias is a theoretical and research design problem related to the population examined, not merely a statistical estimation problem. Addressing it requires conceptual scrutiny of the comparative logic that precedes model specification.

We make two contributions to the literature. First, we introduce counterfactual indeterminacy bias as a distinct lens for evaluating the comparative logic that underpins family business research, elaborating its forms and potential solutions. Second, we offer concrete guidance on how reference groups should be specified, matched to theoretical assumptions, and modeled across contingent conditions. In the sections that follow, we discuss the parallel between counterfactual indeterminacy bias and the control-group principle in experimental science and then identify three recurring forms of this bias (neglecting the reference group, assuming homogeneity within it, and assuming stability across contingent conditions). We conclude by offering recommendations for addressing each form of bias.

Counterfactual Indeterminacy Bias: A Parallel to the Control-Group Principle

As outlined above, counterfactual indeterminacy bias parallels the control-group problem in experimental design, where a missing or misspecified control condition threatens the isolation of treatment effects (Campbell & Stanley, 2015; Rubin, 1974; Shadish et al., 2002). When the nonfamily reference group is theoretically or empirically omitted, misspecified, or treated as static, the unique effects of family involvement become difficult to distinguish from background factors common to all firms. Thus, even when a comparative study of family firms is not conducted as an experiment, the same inferential logic applies. In studies of family firms, the reference group, typically nonfamily firms, serves a function analogous to the control condition in experiments. As in experimental settings where control contamination or non-concurrent controls bias the treatment effect (Pocock, 2013), poorly theorized or unstable reference groups in family business research can distort causal interpretation and threaten construct validity. Although this problem rarely occurs when the sample includes both family and nonfamily firms, the problem is very likely to occur in studies that only compare family firms with different characteristics unless care is taken to ensure that the characteristics examined theoretically distinguish family firms from nonfamily firms.

Recognizing this parallel indicates that counterfactual indeterminacy bias is not merely a technical oversight but a structural inference problem. It comprises three confounds to validity emphasized in experimental methodology: misattributing causal mechanisms which can act as a confound to internal validity; defining the wrong comparative baseline, which can serve to confound construct validity; and generating context-insensitive generalizations, which confound external validity. In the language of causal inference (Imbens & Rubin, 2015; Morgan & Winship, 2015), comparisons of family and nonfamily firms represent observational analogues to treatment–control contrasts, and the rigor of conclusions depends on the plausibility of the assumed counterfactual. In the following section, we discuss three recurring forms of counterfactual indeterminacy bias that together illustrate how this form of bias distorts theory building and empirical inference in family business research.

Types of Counterfactual Indeterminacy Bias in Family Business Studies

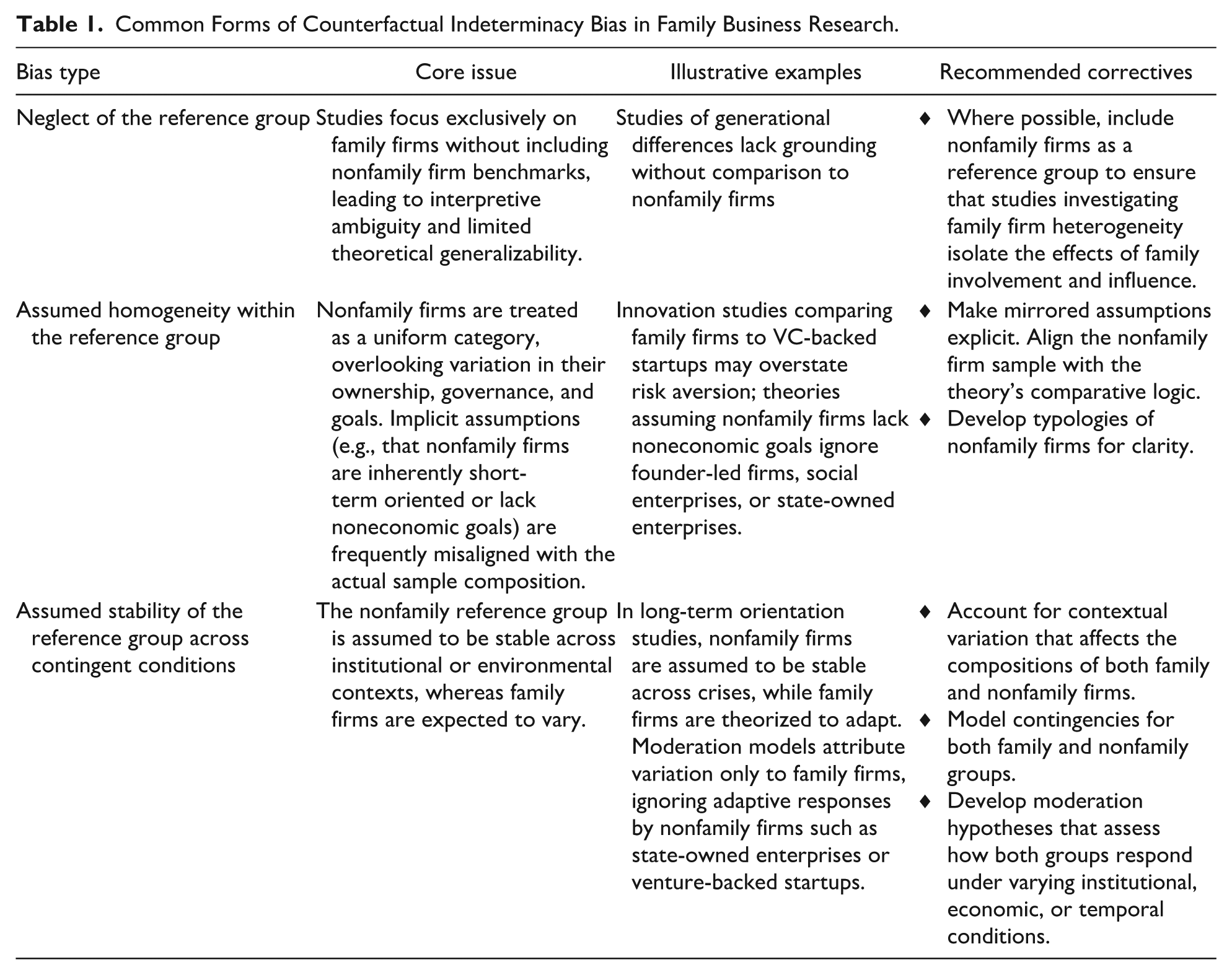

Counterfactual indeterminacy bias introduces several threats to the integrity of research design and inference, which are related to (a) the failure to include a reference group, (b) including the wrong reference group, or (c) misinterpreting the characteristics of the reference group in the theory and research design. These threats are based on the assumptions, implicit or explicit, that there is no need for comparison with the behavior of nonfamily firms because the behavior of family firms can only be due to family involvement and influence rather than business necessity, that the reference group is homogeneous and therefore acts like a constant having no effect on the relationships of interest, or that the reference group is stable across contingent conditions with no influence on the relative behavior or performance of family firms in comparison with nonfamily firms (see Table 1). These assumptions systematically distort comparative logics by obscuring the characteristics of the reference group, leading to misattribution of observed effects and flawed theoretical generalizations (Bruton et al., 2010; Miller et al., 2011). Thus, addressing and avoiding counterfactual indeterminacy bias is essential for producing reliable and generalizable insights on family firms.

Common Forms of Counterfactual Indeterminacy Bias in Family Business Research.

Neglect of the Reference Group

A serious error in family firm research is the tendency to neglect the reference group altogether by focusing exclusively on family firm heterogeneity without providing a theoretical justification for not making comparisons with nonfamily firms (Dyer, 2006). The problem is especially consequential in research designs that draw comparative inferences, whether explicitly or implicitly, without carefully considering and explaining why the source of heterogeneity under examination distinguishes family firms not only from one another but also from nonfamily firms (Chua et al., 2012; Daspit et al., 2021). 3

Interpretative Ambiguity: The Risk of Biased Narratives

When nonfamily firms are excluded from empirical analyses, research findings may lack a meaningful interpretive baseline, making it difficult to determine whether observed patterns within family firms are truly distinctive or simply reflective of general differences among all organizations (Chrisman et al., 2005; Sharma, 2004). Without a clearly specified comparison group or theoretical rationale that explains the differences between family and nonfamily firms, researchers risk misattributing outcomes to family involvement that may instead arise from structural or contextual factors that also characterize nonfamily firms (Welter, 2011).

Take, for example, a study examining firm performance across generational transitions within family firms. Suppose that the analysis is based solely on a family business sample, using generational status (e.g., founder-led = 1; successor-led = 0) as the key explanatory variable. Also, assume that the results show that first-generation family firms outperform later-generation firms, a finding that suggests successors weaken family firm performance. Such an inference can easily produce oversimplified and potentially biased narratives that portray founders as visionary leaders, while depicting successors as lacking capability or commitment (Lansberg, 1999; Stewart & Hitt, 2012). However, without including nonfamily firms run by their founding versus succeeding leaders, we are unable to tell if the performance advantages of founder-leadership are unique to family firms or a characteristic of firms in general. Besides addressing that question, incorporating nonfamily firms into the analysis may reveal alternative comparative patterns that yield a more nuanced and complete, context-sensitive view of generational transitions. The three hypothetical patterns below illustrate how introducing a reference group can fundamentally reshape theoretical interpretation. 4

Firm Performance, Case 1: Nonfamily Firms > First Generation > Second Generation

This scenario suggests that while first-generation family firms perform better than successor-led family firms, their performance still lags behind the performance of nonfamily firms. If this is the case, family involvement itself may not be a performance-enhancing factor, implying that even at their peak in the first generation, family firms are at a disadvantage compared with professionally managed nonfamily firms.

Firm Performance, Case 2: First Generation > Nonfamily Firms > Second Generation

Here, first-generation family firms outperform nonfamily firms, but the advantage dissipates in the next generation. This pattern aligns with theories suggesting that founders bring entrepreneurial vision, agility, and commitment that both nonfamily firms and second-generation family firms find difficult to replicate (Miller et al., 2007). This scenario suggests that, if the family values firm performance more than family control or socioemotional wealth (SEW), founders should consider selling the firm or hiring a nonfamily successor rather than appointing a second-generation family leader (cf., De Massis et al., 2008).

Firm Performance, Case 3: First Generation > Second Generation > Nonfamily Firms

This pattern suggests that family firms outperform nonfamily firms across generations, even though performance declines following succession. It provides support for the view that family firms possess enduring capabilities that extend beyond the founding generation, or that lower agency costs stemming from the combination of family ownership and management outweigh the superior ability that is often attributed to nonfamily managers (Habbershon & Williams, 1999; Le Breton-Miller & Miller, 2006). If so, the dominant narrative that succession is a liability would shift toward understanding how second-generation leaders sustain a performance advantage over nonfamily firms, even if they do not fully match their predecessors. Again, without including nonfamily firms we are unable to tell if the performance advantages of family firms become stronger or weaker or stay the same over time.

Each alternative scenario suggests fundamentally different conclusions about generational transitions in family firms. If nonfamily firms are excluded from the analysis, research will be unable to distinguish which conclusion is valid and may choose an overly simplistic and biased narrative regarding the performance of first- and second-generation family firms.

The consequences of these possibilities illustrated by our admittedly contrived example would have practical implications if true. If intra-family succession is an inferior option to selling out (e.g., through management buy-outs, buy-ins, or initial public offerings), family business owners may become reluctant to pass on the firm to their offspring fearing that their successors will dissipate the family’s wealth or even fail outright (Morris et al., 2010). A perception that intra-family succession is unlikely to create value for the family could lead family owners to underinvest in the firm compared with what they might have been willing to invest if they thought their children could effectively manage the business (Parker, 2016). Moreover, underinvestment may constrain the strategic options of successors, leading to a self-fulfilling prophecy that later-generation leaders will underperform. It might also lead to other counterproductive decisions such as leader entrenchment, resistance to professionalization, and bypassing opportunities for renewal and strategic change (König et al., 2013; Stewart & Hitt, 2012). Furthermore, if the message that emerges is that only family control can drive superior firm performance, later-generation family members may feel pressured to emulate founder behaviors, even when the business environment has changed (De Massis et al., 2008; Sharma et al., 2003). As a consequence, successors may resist delegation, ignore the need for external talent, or cling to outdated strategies that might lead to firm stagnation rather than growth (Davis & Harveston, 1999; Zellweger et al., 2011).

Disconnect Between Theory and Empirical Analysis

The exclusion of nonfamily firms from empirical analyses creates a critical disconnect between theoretical constructs and empirical validation, especially when the independent variable is not uniquely or inherently tied to the owning family. For example, consider a study examining the relationship between family ownership and firm performance using a sample exclusively composed of family firms. If the analysis reveals a positive association, i.e., that higher levels of family ownership correlate with superior performance, this finding may be interpreted as evidence of distinctive governance mechanisms, patient capital, or stewardship-driven leadership (Le Breton-Miller & Miller, 2006). However, without including nonfamily firms as a reference group, it is impossible to determine whether the observed effect is truly a consequence of family ownership or simply a reflection of a more general effect of concentrated ownership or founder control, which may also be present in nonfamily contexts (Anderson & Reeb, 2003; Dyer, 2006; Miller et al., 2007; Villalonga & Amit, 2006).

While family ownership serves as an illustrative example, this issue can extend to other commonly studied constructs. The central question becomes whether the presence or level of an independent variable is unique to family firms, or whether it also manifests in other organizational forms such as founder-led startups, social enterprises, or private equity-owned firms (Bruton et al., 2010; Zahra, 2005). If such distinctions are not made explicit, researchers risk misattributing causal effects, blurring the line between family-driven mechanisms and general organizational properties (Krasikova & LeBreton, 2012). Without a comparative framework that incorporates nonfamily firms, researchers risk conflating general organizational principles with family-specific phenomena. Indeed, Dyer (2006) suggests that this sort of problem can occur even in comparative studies that fail to fully isolate the family effect from the firm effect.

Recommendations

The reliance on family-business-only samples creates a methodological disconnect by isolating empirical findings from the comparative theoretical frameworks that were originally developed to explain differences between family and nonfamily firms. This disconnect limits the external validity and interpretive clarity of research conclusions. To bridge this gap, scholars should incorporate nonfamily firms as a reference group whenever theoretically justified and empirically feasible. Doing so enables more accurate assessments of how family-specific dynamics interact with, reinforce, or diverge from broader organizational processes (Chua et al., 1999, 2012).

This requires more than simply adding nonfamily firms to the sample. Researchers must first articulate the theoretical distinctions between family and nonfamily firms that their study presupposes, and then ensure that the research design, including sample composition, variable operationalization, and comparative logic, allows those distinctions to be isolated and tested.

Miller et al. (2007) provide a useful benchmark for how such comparative logic can be applied effectively. By explicitly incorporating nonfamily firms and carefully distinguishing family firms from founder-led firms, their study demonstrates how theorizing and specifying the nature of the counterfactual reference group strengthens inferences about family firm performance. Thus, subsequent research on family firm heterogeneity would benefit from making the reference group explicit, aligning it with the theoretical contrast of interest, and treating comparative design as a core element of theory development rather than a secondary empirical choice.

Assumed Homogeneity Within the Reference Group

When scholars develop family business theories, they not only make explicit assumptions about the nature and behavior of family firms but also implicit assumptions about nonfamily firms (Chrisman et al., 2025). These assumptions are embedded in the comparative logic of theory building, wherein nonfamily firms are often treated as the conceptual foil to highlight the distinctiveness of family firms (Chua et al., 1999). For example, when a theory posits that family firms benefit from unique governance advantages, such as long-term orientation, relational control, or stewardship-driven leadership, it typically implies that nonfamily firms are short-term oriented, contractually governed, or dominated by principal-agent logic (Chrisman et al., 2004; Miller & Le Breton-Miller, 2006; Schulze et al., 2001).

This implicit comparative logic extends well beyond governance-related constructs. Many foundational theories in the family business field, spanning topics such as professionalization (Stewart & Hitt, 2012), succession (De Massis et al., 2008), innovation (Chrisman & Patel, 2012), risk-taking (Fang et al., 2021), and stakeholder relationships (Zellweger & Nason, 2008), rely on unstated assumptions about the differences between family firms and nonfamily firms. This logic becomes problematic when the empirical reference group fails to match those assumptions. For instance, if the comparison group fails to include founder-led firms, mission-driven social enterprises, or hybrid ownership organizations, which exhibit different but overlapping behavioral and structural traits (Bruneel et al., 2020; Randolph et al., 2019), the conceptual contrast is weakened, and the empirical conclusions risk being ambiguous.

This issue has direct implications for research design and validity. When researchers fail to ensure alignment between the assumptions embedded in their theoretical framework and the characteristics of the nonfamily firm sample, they risk confounding family-specific effects with broader organizational phenomena. In other words, observed differences may stem from factors such as founder centrality, stakeholder orientation, or ownership concentration, which are not unique to family firms. To avoid such misattribution, researchers must be as deliberate and rigorous in defining and selecting the nonfamily comparison group as they are in conceptualizing the family firm itself. This is especially important in situations where several different types of nonfamily firms, such as state-owned enterprises (SOEs), lone-founder firms, and widely held corporations coexist (Markin et al., 2022).

Heterogeneity in Nonfamily Firms

Even when nonfamily firms are included in research, they are often treated as a uniform category with shared characteristics. However, this oversimplification ignores the wide diversity of ownership structures and strategic orientations found among nonfamily firms. For instance, some nonfamily firms are SOEs that attempt to balance commercial success with public policy objectives (Liang et al., 2015). Others are venture-backed startups, where decision-making is driven by high-growth expectations from external investors (Amit et al., 1998). In addition, professionally managed partnerships and hybrid-ownership firms function under governance structures that differ from traditional publicly traded corporations (Mair et al., 2015; Nguyen et al., 2021). The failure to account for these variations can lead to differences between family and nonfamily firms that are overstated or understated due to the oversimplified representation of the nonfamily business category, which can vary widely in strategic behavior and performance. For example, Markin et al. (2022) find that in China, family firms significantly underperform lone-founder firms, achieve performance that is statistically equal or marginally superior to that of widely held nonfamily firms, and significantly outperform SOEs. Thus, it is important to determine which type(s) of nonfamily firms to use for comparisons with family firms.

Recommendations

To avoid the pitfalls discussed above, scholars must ensure consistency between their theoretical assumptions about family and nonfamily firms and the empirical strategies they use to assess those theories. This begins with making implicit assumptions explicit. When developing or applying family firm theories, researchers should clearly articulate not only what is assumed about family firms but also what is presupposed about the nonfamily reference group. Both sides of the comparison must be treated as theoretically meaningful, not as empirical conveniences.

Equally important is aligning the composition of the nonfamily firm sample with the assumptions embedded in the theory. If the theory implicitly contrasts family firms with professionally managed, shareholder-driven organizations, including founder-led, mission-oriented, or SOE firms in the reference group risks undermining the intended comparison unless the characteristics of those types of firms are considered. In such cases, the empirical findings may conflate differences in organizational form or mission with family involvement, leading to inaccurate conclusions.

Assumed Stability of the Reference Group Across Contingent Conditions

One of the critical issues associated with counterfactual indeterminacy bias is the assumption that the nonfamily firm reference group remains stable across different external conditions. Many studies implicitly treat nonfamily firms as a homogeneous and unchanging benchmark against which family firms can be measured. However, this assumption may be problematic for two reasons. First, contingent conditions can lead to heterogeneity among nonfamily firms. Second, the impact of external factors on firm behavior or performance is not exclusive to family firms but extends to their nonfamily counterparts as well.

Variation in Nonfamily Firm Composition

A straightforward and obvious way to reduce the possibility of mismatched comparisons is to ensure that family and nonfamily firms are drawn from the same database or population. This avoids noticeable biases, such as comparing family-owned SMEs from one dataset with publicly traded corporations from another (Kofford et al., 2025). Yet even when researchers use a single database, the composition of the family and nonfamily firm sample may vary substantially. This creates a dynamic baseline problem that potentially undermines comparative inferences.

Variation Over Time

The composition of both family and nonfamily firms within a given database can shift across periods, meaning that the groups at Time 1 are not equivalent to those at Time 2. For example, in China, the nonfamily category was historically dominated by SOEs, but recently, the prevalence of privately held corporations and venture-backed startups has risen (Liang et al., 2015; Markin et al., 2022). In Western contexts, the mix of firms also changes cyclically: during boom periods, venture-backed firms may dominate, while in downturns, family firms may become relatively more prevalent (Amit et al., 1998; Chang et al., 2008; Puri & Zarutskie, 2012; Yilmaz et al., 2024). Likewise, the composition of family firms themselves evolves across time. Succession transitions alter ownership and governance logics, institutional reforms can change the criteria for operationalizing family firm variables, and the relative share of multi-generational family firms versus founder-led firms may vary with survival dynamics (Cucculelli & Micucci, 2008). In such cases, an observed change in family versus nonfamily performance across time may partly reflect shifting baselines in either or both groups, rather than true changes in underlying family firm behavior. Although shifting baselines are beyond researchers’ control, it is important to be aware of the possibility so that sample selection can be done in a way that minimizes such noise, and analyses can be conducted to determine the extent to which changes in family versus nonfamily firm performance are a function of endogenous or exogenous factors.

Variation Across Contexts

A similar issue arises in cross-national or cross-industry studies (Berrone et al., 2022), where the category of “nonfamily firms” can take vastly different forms depending on the institutional and economic environment. In China, nonfamily firms could include SOEs driven by long-term, political objectives favored by the Communist Party. In Western economies they are more likely to be publicly traded corporations with dispersed ownership driven by wealth creation, or entrepreneurial ventures financed by venture capital and driven by growth objectives (Anderson & Reeb, 2003; Bruton et al., 2015; Lumpkin & Brigham, 2011). Likewise, in sectors such as health care or education, nonfamily organizations may include mission-driven cooperatives or nonprofits, creating very different benchmarks than in capital-intensive industries dominated by shareholder-oriented corporations. These cross-context differences mean that a “nonfamily” comparison group in one setting is not functionally equivalent to that in another, complicating the interpretation of family–nonfamily contrasts. This is less problematic in studies that analyze only one country, industry, or dataset, where comparative analysis is rather straightforward. However, explicit comparisons across contexts that fail to account for these differences risk attributing observed variation to “family versus nonfamily” effects when they may instead reflect underlying contextual heterogeneity in the composition of the nonfamily group.

Contextual Variation in Nonfamily Firm Behavior

A frequent practice in family business research is to use moderation hypotheses to examine how contextual conditions influence the relationship between family involvement and firm outcomes. In these models, scholars typically argue that under Condition A (e.g., economic stability), family firms behave in one way, whereas under Condition B (e.g., economic crisis), they behave differently. The underlying theoretical logic is that contingent conditions interact with the distinctive characteristics of family firms to produce different strategic behaviors or performance outcomes. These moderation-based arguments often rely on the implicit and problematic assumption that the behavior and performance of nonfamily firms remain stable. In other words, the counterfactual reference group against which family firms are compared is treated as context-invariant, even though contextual shifts are likely to affect all firms, regardless of ownership type. This oversight can lead to biased inferences about the distinctiveness of family firms, especially when changes in behavior are attributed exclusively to family involvement, while similar adaptive responses among nonfamily firms are overlooked.

Consider the case of firm behavior during economic downturns. Family firms, motivated by factors associated with loss aversion such as preserving family control, protecting the firm’s legacy, or safeguarding socioemotional wealth, are typically risk-averse under stable conditions and risk-tolerant in periods of adversity (Chrisman & Patel, 2012; Gomez–Mejia et al., 2014). These firms might pursue bold actions such as counter-cyclical investments, strategic acquisitions, or diversification to reverse declining performance. Such moves are often interpreted as a unique feature of family firms’ long-term commitment and strategic flexibility. Yet nonfamily firms also tend to be loss averse and likely to adjust their behavior in response to contextual pressures, though their motivations, mechanisms, and degree of adjustments may differ. Publicly traded corporations may reduce discretionary spending or delay innovation projects to meet short-term earnings expectations from institutional investors (Bushee, 1998). Venture-backed startups, which emphasize rapid growth during boom cycles, may pivot toward cost containment and liquidity preservation during downturns (Puri & Zarutskie, 2012). SOEs may realign strategic priorities based on shifting government directives (Bruton et al., 2015).

If researchers sample family and nonfamily firms from the same population, observable differences in behavior will naturally emerge if they exist. However, the risk lies not in detecting these differences but in interpreting them, especially if the comparisons are made only among different family firms. Too often, theoretical arguments attribute strategic variation solely to family-specific characteristics while assuming the nonfamily benchmark remains static across contexts. This assumption is problematic because, as suggested above, nonfamily firms also adapt to contextual shifts (Bruton et al., 2015; Bushee, 1998). When such adaptations are overlooked, scholars risk overstating or mischaracterizing the distinctiveness of family firm responses.

Recommendations

To avoid this bias, theory development must move beyond simply explaining how contextual conditions shape family firm behavior. Instead, the focus should be on how contextual conditions influence the relative differences between family and nonfamily firms. Put differently, the task is not merely to argue whether, how, and how much family firms change under Condition A versus Condition B, but to theorize and assess the adaptations of both family and nonfamily firms to understand how their responses diverge, converge, or evolve over time.

The assumption that nonfamily firms remain stable and uniform across different contingent conditions presents significant methodological and theoretical challenges. If researchers fail to consider how nonfamily firms respond to changing conditions and how the responses of family firms differ, they risk drawing misleading conclusions about family firms. Similarly, if studies assume that contingent conditions influence only family firms while leaving nonfamily firms unchanged, they may overstate the uniqueness of family business responses.

To advance the field, researchers must develop theories and test hypotheses that emphasize differences in the responses of family and nonfamily firms to changing circumstances, rather than focusing solely on how changing conditions affect family firms. In particular, family business scholars should: (a) recognize that the diversity within nonfamily firms may also be shaped by contingent conditions; (b) ensure that external contingencies are modeled for both family and nonfamily firms, rather than assuming that only family firms adapt to external changes; and (c) develop moderation hypotheses that examine how contingent conditions influence changes in family and nonfamily firms, rather than focusing solely on family firms.

Contributions and Final Thoughts

We have introduced counterfactual indeterminacy bias as a structural inference problem in family business research, analogous to the control-group problem in experimental science, and have identified three core manifestations: the absence of a reference group, the assumption of homogeneity, and the assumption of stability across contingent conditions.

This paper contributes to the literature by discussing the dangers of counterfactual indeterminacy bias and how to avoid them. We highlight the importance of making implicit assumptions explicit, particularly the mirrored assumptions about nonfamily firms that underpin theoretical claims, and foster alignment between theory and research design (Suddaby et al., 2011). In doing so, we set a pragmatic agenda for the field: researchers should pre-specify and justify reference groups, report the heterogeneity within those groups, and employ designs (e.g., stratified sampling, multilevel and configurational analyses) that can disentangle family effects from broader organizational mechanisms. Substantively, our examination invites re-evaluation of influential findings (e.g., on performance, succession, risk, and governance) by testing whether “family effects” persist once appropriate nonfamily comparators are introduced. Methodologically, it encourages the use of replication studies, matching methods, and meta-analytic partitioning by reference group.

Addressing counterfactual indeterminacy bias is significant for both research and practice. For researchers, adopting diverse reference groups, modeling heterogeneity, and accounting for contingent conditions enhance the validity of causal inferences and theoretical claims, ensuring that findings about family firms are not artifacts of oversimplified baselines (Certo et al., 2016). For practitioners, nuanced insights into how firms navigate economic, institutional, or competitive challenges can inform more effective strategies and avoid misleading narratives that overemphasize family firm exceptionalism (George et al., 2016).

We see three priorities for future research. First, replication studies should re-examine influential findings in the family business literature on performance, succession, risk-taking, and governance using properly specified nonfamily comparison groups to assess whether established “family effects” hold once the reference group is made explicit. Second, scholars should develop classifications of types of nonfamily firms (e.g., state-owned enterprises, lone-founder firms, venture-backed startups, widely held corporations) that can serve as a basis for more precise matching in comparative studies. Third, the field would benefit from further methodological guidance on when and how to incorporate nonfamily reference groups. Not every study requires a nonfamily comparison: studies of phenomena that are exclusively tied to individuals or the family and lack a meaningful nonfamily analogue (e.g., family altruism, intra-family succession dynamics, family identity transmission) may appropriately rely on family-only samples. The key criterion is whether the theoretical claims being advanced depend, explicitly or implicitly, on a family–nonfamily contrast.

Footnotes

Acknowledgements

The authors thank Evelyn Micelotta, Benjamin D. McLarty, Erik Markin, and Weiwen Li for their comments and suggestions on earlier drafts of this piece.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.