Abstract

This article tests an integrated model of financial planning for retirement (FPR), with 948 Spanish workers aged between 30 and 63. Overall, the three model dimensions—capacity, willingness, and opportunities to plan and save—show a significant association with financial planning for retirement. The moderator role of age in the relationships between antecedents and financial planning was tested. Consistent with our hypothesis, younger participants showed a greater level of FPR if they were characterized by a high level of education. The interaction between both age and psychological preparation for retirement and retirement goals clarity failed to reach statistical significance. We discuss how financial planning effectiveness could be increased based on the results of importance-performance map analyses.

Keywords

Ten years ago, Taylor and Geldhauser (2007) underlined the urgency of an economic imperative to study financial planning for retirement (FPR), specifically among low-income workers, due to the questioning of the strength of social security systems. Today, FPR continues to deserve empirical attention because it is a task which has become ever more necessary but, at the same time, increasingly complex for both individuals and institutions. FPR consists of the series of activities involved in the accumulation of wealth to cover needs in the postretirement stage of life. It is complex because success means anticipating needs and saving to meet them at a time of life when personal income inevitably decreases.

Furthermore, poor financial planning has long-term negative effects, because many people opt to retire when their pensions are still insufficient, only to suffer difficulties later on (Annink, Gorgievski, & Den Dulk, 2016; Khan et al., 2016; Whitley, Benzeval, & Popham, 2016). Specifically, in Spain, the reforms of the Public Pensions System during 2011 and 2013 postponed the legal retirement ages and adopted a pension revaluation index to improve the sustainability of the system. But these changes led to a progressive reduction of the average pension value, which has been estimated as 30% less between 2010 and 2050 (Sánchez-Martín, 2014). Considering the high welfare costs for households implied by these reforms, it seems be crucial to investigate the factors associated with FPR among Spanish workers aged between 30 and 63.

The model proposed by Hershey, Jacobs-Lawson, and Austin (2013) is the only one so far to have integrated the key variables found in partial empirical studies (e.g., Hershey, Jacobs-Lawson, McArdle, & Hamagami, 2007; Hershey & Mowen, 2000) from a theoretical standpoint. Three dimensions—capacity, willingness, and opportunity to plan for retirement—were proposed by Hershey and his colleagues. Moreover, the model holds a main assumption related to the continuity and strengthening of FPR during the course of adulthood. As Hershey et al. stated, “This developmental aspect of the model is designed to convey the notion that, for most individuals, a predisposition early in adulthood—say, a positive attitude toward planning—would be expected to be maintained over time” (p. 408). However, this pattern of continuity is not immutable, and some influences could lead to changes. Consequently, it would be relevant to test both the stability pattern of influences on FPR across adulthood and the specific changes in this pattern related to age groups. To sum up, this article aims to provide general empirical support for Hershey’s FPR model in Spanish worker population. To this end, we operationalized the three dimensions described and we analyzed their predictive power for FPR, controlling for the effects of age, to test the stability of the pattern. We also examined the specific moderator role of workers’ age (below 40, between 40 and 55, and older than 55) in the relationships between planning antecedents and FPR, to further explore changes associated with the age groups. Then, we discuss areas for improvement of FPR based on importance-performance map analyses (IPMAs), carried out for age groups.

Financial Planning for Retirement

Retirement involves numerous emotional, physical, social, and financial changes, and the financial aspects of retirement are legion. Hence, an adequate planning therefore involves deciding how limited resources are to be distributed, given that achieving one goal may sometimes mean sacrificing others. When workers start planning for retirement early, adjustment and adaptation is generally experienced as highly positive (Topa, Depolo, & Alcover, 2018; Topa, Moriano, Depolo, Alcover, & Morales, 2009). In this light, a key aspect of efforts to improve the current situation should include investigation of ways to boost personal saving and encourage effective financial preparation (Topa, Lunceford, & Boyatzis, 2018).

Hershey and colleagues’ model (2013), called the “Capacity–Willingness–Opportunity Model,” was developed as a conceptual framework for understanding a wide range of influences on FPR. As a foundation, authors adapted Blumberg and Pringle’s (1982) model on work performance, which proposed three main antecedents that contribute to individual performance: capacity, willingness, and opportunity. Unlike the original model, where the dimensions were conceived as additive, in Hershey’s model, potential interactions among the dimensions were acknowledged. Previous research, conducted by Hershey’s group since 2000, empirically supported the individual parts of the model, as challenges of training preretirees in financial decisions. Later, a more psychological perspective was developed, including psychological predispositions that could be associated with financial planning behavior (e.g., personality factors, perceptions of task relevance, and motivational factors), and it was tested in separated studies (Hershey & Mowen, 2000; Hershey et al., 2007; Jacobs-Lawson & Hershey, 2005), adding financial inhibitors and emotional factors (Neukam & Hershey, 2003). Finally, it was tested cross-culturally.

Other models have been proposed on financial-related behaviors, such as Huston’s model (2010) regarding cognitive, motivational, and environmental influences on financial management behavior or Hodges’s model (2004) on immigrants’ process of financial planning, as well as more general models connecting intention and behavior (e.g., theory of planned action), but Hershey’s model is the only one specifically focused on retirement. This specific focus on FPR was the main reason for selecting this model over the others.

Capacity to Plan and Save for Retirement

The first dimension includes the abilities, knowledge, and skills which contribute to differences in people’s cognitive and intellectual capacity to plan and save for retirement effectively. Among others, one’s knowledge, skills, intelligence, and level of training and education would likely contribute to the ability to plan and save. Hence, financial literacy and the level of training and education were included in the study as indicators following Hershey and colleagues (2013).

The association of an individual’s understanding of retail financial transactions on FPR is a matter that has received considerable attention. Initially, it was observed that training in financial literacy improved retirement planning among people approaching retirement (Hershey & Mowen, 2000) and that accurately predicted saving behavior (Jacobs-Lawson & Hershey, 2005). Such domain-specific knowledge is associated with a tendency to plan ahead for retirement with the positive intention of saving (Hershey et al., 2007) and actively seeking out relevant financial information and investment strategies.

It has been shown empirically that a better education helps people seek relevant information for retirement planning, and at the same time, educational level is a significant factor influencing enrollment in financial education programs and it may motivate retirement planning. Based on this literature, we postulate:

Willingness to Plan and Save for Retirement

The second dimension includes the motivational forces and the psychological and emotional factors that determine the likelihood that a given individual will begin planning and will sustain the activity over time. Among others, clarity and nature of one’s financial goals, retirement-related fear and anxiety, perceived social norms, and self-image could be linked to the tendency to plan and save. Psychological preparation for retirement is a mental process which includes thinking ahead and discussion and the search for information about retirement, and some recent studies have considered this variable, finding it to be significantly related with FPR (Guyla, 2007; Stephen, 2012). Goals provide direction, coherence, and meaning to behaviors. Goal clarity improves functioning not only because it guides conduct but also because it provides a frame of reference within which future efforts can be situated. In terms of FPR, retirement goals are necessarily related with saving for retirement (Neukam & Hershey, 2003), and it has been shown that goal specification is a predictor of financial planning and saving activities. Hence, we posit:

Opportunity to Plan and Save for Retirement

Finally, certain external influences exist, including environmental facilitators and constraints affecting effective financial tasking. Among others, availability of voluntary retirement saving programs, tax incentives for saving, and availability of financial advisors in the proximal environment would be associated with the tendency to plan and save. Financial professionals provide advice and information on the best investment products available based on their clients’ needs. In fact, many people today seek investment information and advice from numerous sources, including stock brokers, financial advisers, books, magazines, and online forums in an effort to acquire some level of financial expertise and achieve better outcomes, and ever more of them use such advisory services specifically to address the financial aspects of retirement.

The ability to generate income from a range of sources including salaries, pension schemes, and investments has been posited as a predictor of FPR (Hershey & Mowen, 2000). However, significantly indebted households tend to accord greater priority to the repayment of loans than to saving for retirement (Bernstein, 2004). In this light, we postulate:

Retirement Planning and Age

The role of age in Hershey’s model is a bit complex. On the one hand, a relevant characteristic of the conceptual model is continuity. This implies that a stable pattern of entrenchment of capacity, willingness, and opportunities to plan and save could be expected. The best option would, of course, be to begin saving from the very start of working life, but most people do not actually take up financial planning for their retirement until the later stages of adulthood. Because of this, age is the most widely studied demographic indicator in relation to FPR (Topa et al., 2009).

On the other hand, the proposition of continuity does not imply that the pattern is immutable. At least three types of influences could lead to changes in FPR: normative age-related influences, normative history-related influences, and nonnormative life events. Based on normative age-related influences, workers around 50 years become more interested in financial planning than younger workers. Empirical studies support that savings and FPR significantly differ as a function of age (Barnhoorn, Döhring, Van Asseldonk, & Verwey, 2016). For instance, it has been observed that older people are much more likely to be involved in FPR (Hershey et al., 2007). In Spain, history-related influences could be exemplified by the pensions system reform conducted in 2011 and 2013, which increased the population’s awareness about the sustainability of future pensions (Budowski, Schief, & Sieber, 2016), or by differences in formal education among cohorts (O’Shea, Monaghan, & Ritchie, 2014), which provide them with different skills in order to handle financial information. Finally, nonnormative life events, such as major health problems (Assari & Lankarani, 2016), could interfere with FPR, and empirical support has recently been found for this assertion (Han, Boyle, James, Yu, & Bennett, 2015). To sum up, Hershey’s model suggested that age differences matter in FPR. Because of the stability pattern proposed by the model, age will be included first as control variable in our analyses, in order to exclude its association with FPR. Further, to test the proposed changes derived from the three sources of influences explained above, age will be treated as a moderator in the relationship between antecedents and FPR. Based on Martín (2005), we grouped our participants as young adults (below 40 years), middle adults (between 40 and 55 years), and mature adults. This classification seems to be in agreement with more recent findings. For example, employment rates among highly educated Europeans (International Standard Clasification of Education [ISCED] 5 and 6) was more frequent for those aged under 39 years than for the group aged 40 and over (Eurydice, 2009). Moreover, the Eurobarometer survey in 2012 showed that 45% of European believed that age-based discrimination against people over 55 years was widespread, while “54% of Europeans cite being over 55 as a factor that puts job applicants at a disadvantage” (Davies, 2014, p. 2). Accordingly, Scherbov and Sanderson (2016) recommended considering age-specific characteristics to better understand patterns of aging. Since both social perceptions and job opportunities seem to change abruptly about 55 years, we have taken this age as the beginning of the mature adults group. In this study, we posit:

Specifically, these variations are defined as follows:

Finally, we included some variables as controls since previous empirical evidence supports their relationships with FPR. Sociodemographic characteristics, such as job seniority or number of children financially dependent at home, have been shown to be associated with retirement planning and decision-making in general, and more specifically with the financial aspects of retirement, as stated by Alcover, Topa, Parry, and Depolo (2014). Related to perceived health, a meta-analysis showed that poor health has negative and significant relationships both with incomes, objectively assessed before retirement, and with income satisfaction after retirement (Topa, Moriano, Depolo, Alcover, & Moreno, 2011). Due to this mixed pattern of influences between these variables and retirement planning, they were controlled in our further regression analyses.

Method

Data and Procedure

The sample consisted of N = 948 Spanish workers aged 30–63 years, employed full time in various Spanish firms operating in health care, education, services, and the telecommunications industry. The sample included 51.8% women and 48.2% men. The average age of participants was 46.3 (SD = 11.8). We contacted employers’ human resource departments to inform them about our research and request their cooperation. A total of 1,800 envelopes were distributed, each set containing a cover letter, a questionnaire, and a prepaid envelope. One month later, a reminder was sent and 1,080 were eventually returned (response rate of 60%). After eliminating questionnaires affected by more than 10% of missing data, the final sample for the study comprised 948 usable responses. Considering that socioeconomic status is a critical variable when saving for retirement, our participants reported that 71% had a cell phone, 85.7% a personal computer, 63% central heating, 83.4% some type of insurance, 80.3% takes holidays once in a year, 447% travels abroad for holidays once in a year, and 67.4% dines out in a restaurant at least once in a month.

Instruments

Demographic information and control variables

Age, gender, level of training and education, number of dependents at home, and number of years worked were collected. The control variable self-perceived health was assessed with the self-perceived health scale from the Survey of Health, Ageing and Retirement in Europe (Kalwij & van Soest, 2005), where 1 = excellent and 5 = poor. This survey question has been widely used in health surveys, such as the Health Retirement Survey in the United States and the English Longitudinal Study of Ageing in the United Kingdom, and is meant to reflect overall health status. The inclusion of this item in the Survey of Health, Aging and Retirement in Europe study since 2004 allows for easier comparisons between European and North Americans.

Financial literacy

A 6-item scale designed by Hershey and Mowen (2000) was used to assess individuals’ general knowledge about the topic. A sample item from this scale is “I am very knowledgeable about financial planning for retirement” or “When I have a need for financial services; I know exactly where to obtain information on what to do.” The response scale was Likert-type ranging from (1) strongly disagree to (5) strongly agree. Mean scores have been computed, with high values representing better financial knowledge. This measure has demonstrated high internal consistency and reliability in the past (α = .94; Jacobs-Lawson & Hershey, 2005). The original study revealed satisfactory fit statistics in the confirmatory factor analysis (Tucker–Lewis index = .90, comparative fit index = .91, and root mean square error of approximation = .052), as well as its moderate to high Pearson correlations with retirement relevance (r = .23) and retirement affect (r = .13; Hershey & Mowen, 2000).

Level of training and education

The ISCED-97 classification from the Survey of Health, Ageing and Retirement in Europe (Kalwij & van Soest, 2005) was used, in which 1 = primary education or first stage of basic education and 6 = second stage of tertiary education. The participants were asked to report the highest school leaving certificate or university qualification they had obtained.

Psychological preparation for retirement

This variable was assessed using 38 statements developed by Guyla (2007) as later used by Stephen (2012). Examples of items are “I discuss my retirement plans with my spouse and my family” and “I seek and read articles, books and other literature on retirement.” High scores indicate better psychological preparation for retirement. This measure has shown high internal consistency and reliability in the past (α = .92; Stephen, 2012). Construct validity evidence was reported by Guyla (2007) based on its relationships with the Preretirement Involvement Scale (Evans, Ekerdt, & Bosse, 1985; r = .40, p < .001) and with the Scale of Retirement Planning proposed by Mutran, Reitzes, and Fernandez (1997; with r = .32, p < .001). The response scale was Likert-type for psychological preparation ranged from (1) always without fail to (5) never to less than a quarter of the time. The responses have been recoded and mean values calculated where high values represent better preparation.

Retirement goal clarity

The variable was assessed using five statements (Stawski, Hershey, & Jacobs-Lawson, 2007), asking respondents to focus in the preceding 12 months. Therefore, high scores indicate clearer retirement goals. Examples of items include “I set specific goals for how much will need to be saved for retirement” and “I thought a great deal about quality of life in retirement.” This measure has shown high internal consistency and reliability in the past (α = .90; Stawski et al., 2007). Later, empirical evidence showed strong relationships with financial knowledge (r = .48; Koposko & Hershey, 2014). The response options ranged from (1) strongly disagree to (5) strongly agree. The high score represented clearer retirement goals.

Investment advice

The Investment Advice Use Scale (Li, Lee, & Cude, 2002) was used, which measures a person’s use of investment advice through 9 items. Examples of these items include “Using my financial institution as a sounding board of ideas about my finances is important to me” and “I need help selecting savings and investment products that are best suited to meet my financial goals,” “I do not need advice on investment options,” and “I prefer to consult a specialist when I make financial decisions.” Additionally, Li, Lee, and Cude (2002) conducted a factor analysis which showed that the scale items adequately weighted on a single factor, with item loadings higher than .50, and this factor explained 18.6% of the intention to adopt online trading. The response scale was Likert-type for investment advice and FPR, ranging from (1) strongly disagree to (5) strongly agree, with the high values representing stronger preferences for use of investment advisor services. Reliability for this scale was adequate in other study (Topa, Hernández, & Zappalà, 2018) reaching α = .77.

Financial resources

Four items were used from the Financial Resources subscale of the Retirement Resources Inventory (RRI; Leung & Earl, 2012). Examples include “I possess ___ income to support my/my family’s living expenses” and “I have __ financial support from my investments.” Leung and Earl (2012) supported the RRI validity by using the Subject Matter Experts procedure. Therefore, 17 experts allocated the items in randomized order to the appropriate subscales of the questionnaire on 82.5% of the times. Finally, test–retest reliability has been provided as α = .82 (Leung & Earl, 2012). The response scale was Likert-type for financial resources ranged from (1) very little to (5) excess. Highest values represented better financial resources accumulation.

FPR

The outcome variable of the model was assessed using the financial planning for retirement scale, with nine statements (Stawski et al., 2007), focusing their attention in the preceding 12 months. Examples of items include “I identified specific spending plans for the future” and “I made voluntary contributions to a retirement savings plan.” This measure has shown high internal consistency and reliability in the past (α = .87; Stawski et al., 2007). In order to provide construct validity evidence, Hershey, Jacobs-Lawson, McArdle, and Hamagami (2007) showed Pearson correlations with voluntary saving contributions (r = .32) in a sample of 265 middle-aged working adults. The response scale was Likert-type for FPR, ranging from (1) strongly disagree to (5) strongly agree, and providing us a result where high values represented better financial planning for retirement.

Analytic Strategy

First, to handle missing data, several decisions were taken. Previously, questionnaires with more than 10% of nonresponses were excluded from the final sample. Second, cases of missing data were screened. Our missing values were less than 5%, and Little’s missing completely at random (MCAR) test has been applied. This analysis showed that missing values were completely at random (χ2 = 34.05; df = 30, p = .28). And then, in the regression analyses, missing data were replaced by the common point imputation method using the most commonly chosen value.

A sequential multiple linear regression analysis was performed using SPSS Version 24 to test Hypotheses 1, 2, and 3, beginning with the control variables (number of dependents at home, seniority at work, and self-perceived health and age) and going on to capacity to save and plan (financial literacy and level of training and education), willingness to save and plan (psychological preparation for retirement and retirement goal clarity), and opportunity to save and plan (investment advice and financial resources), which were added in four separate steps. Both changes in F and R 2 statistics were considered to establish the significance of each model, along with the standardized regression coefficients (βs) and the associated probability levels, with a 95% confidence interval. Finally, to test Hypothesis 4, moderation analyses were conducted with the PROCESS macros for SPSS (Hayes, 2013). The simple moderating effect analysis aims to show when the predictor is associated with the criterion variable.

In particular, the hypothesized relationships were assessed using Model 1, which estimates the moderating role played by M (age-group) in the X → Y (antecedent → FPR) relationship. The moderation hypothesis is supported when the process varies according to different values assumed by the moderating variable. This procedure was based on 5,000 bootstrap resamples as well as estimates of the direct effect and associated confidence intervals conditional on three specific levels of the moderator (below 40, between 40 and 55, and more than 55). When zero is not included in the 95% bias-corrected confidence interval, it may be concluded that the parameter is significantly different from zero at p < .05. Moreover, in each moderation analysis, all the other predictor variables were included as covariates.

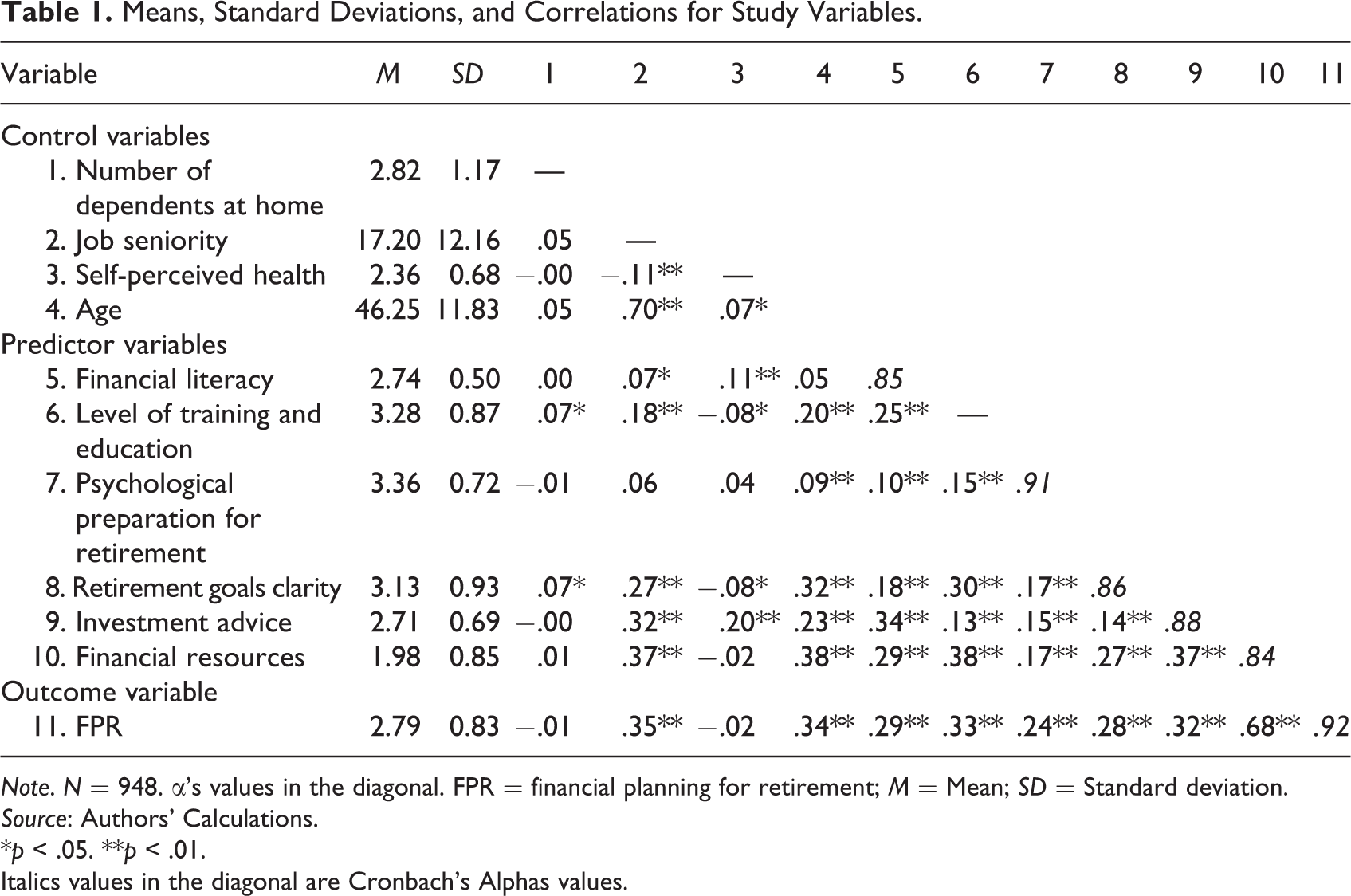

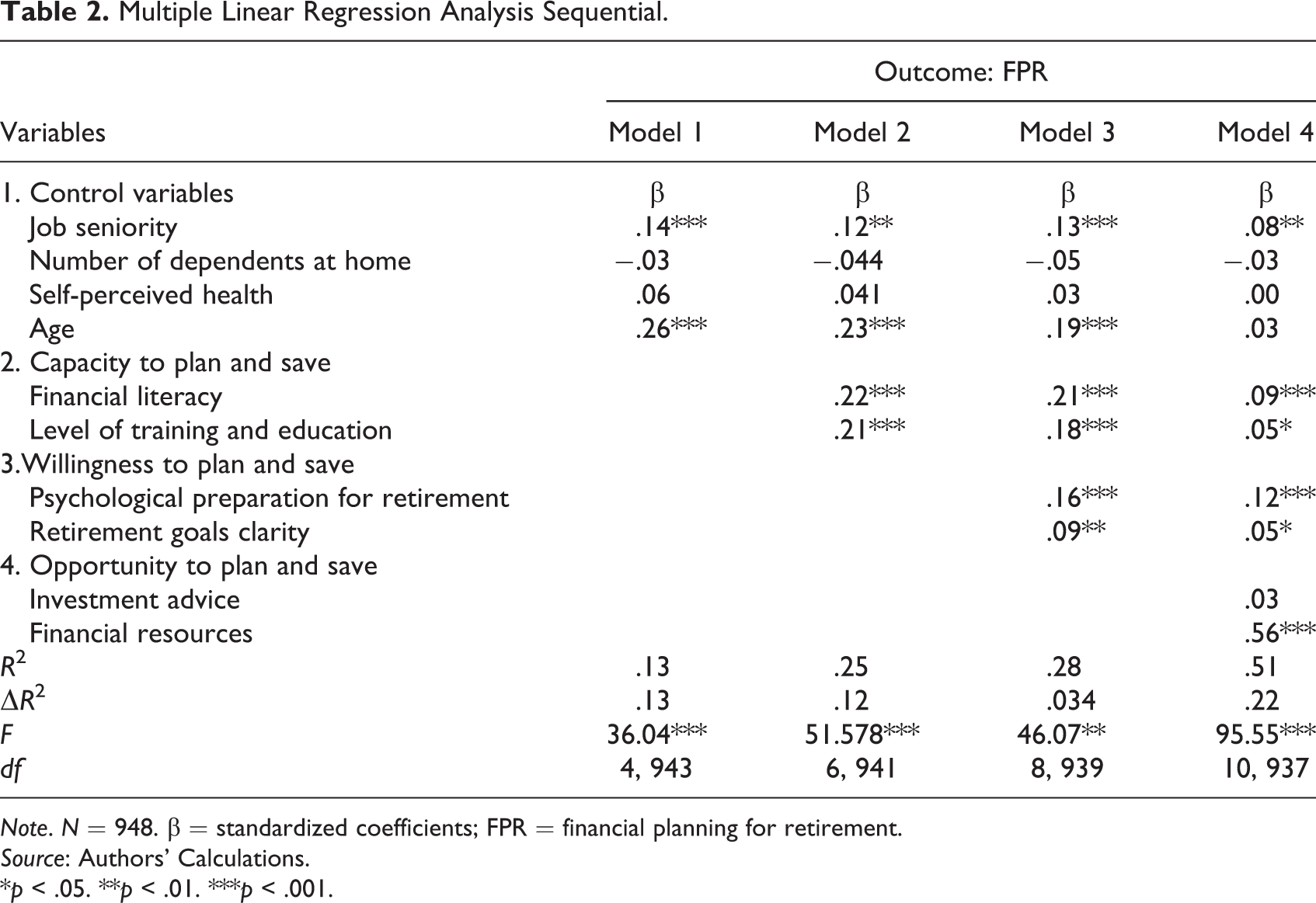

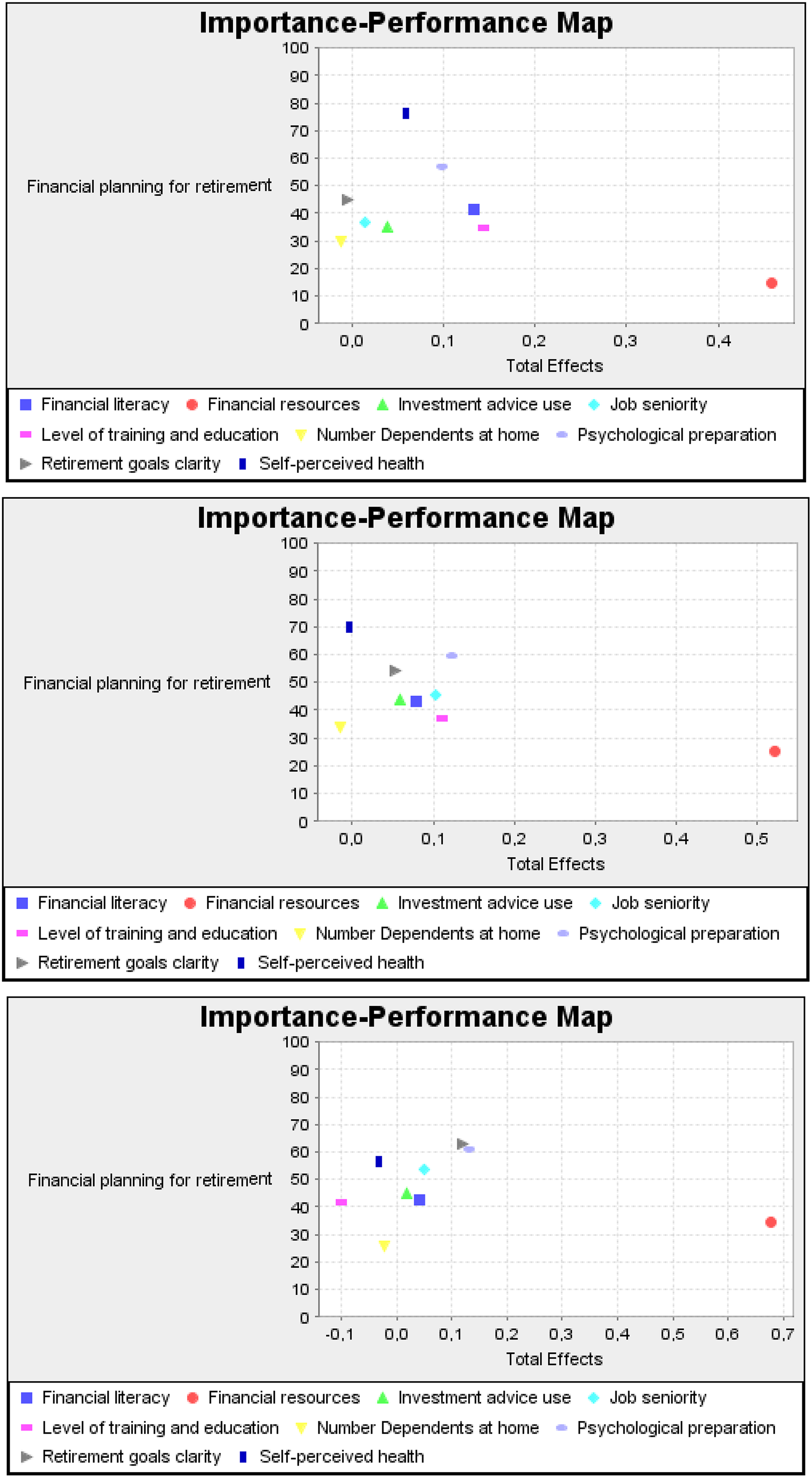

To better understand which are the areas for improvement, we conducted an IPMA for each age-group, with Smart PLS 3.0 (Ringle, Wende, & Becker, 2015). This analysis provides information on the relative importance of constructs in explaining other constructs. The IPMA provides performance scores on a scale from 0 to 100. As a result, interventions could aim at primarily focusing on improving the performance of constructs that exhibit a high importance but, at the same time, have a relatively low performance.

Results

Before testing our model, a correlation analysis was conducted among the study variables. These results are reported in Table 1. Pearson’s correlations indicated that all significant relationships between the variables were in the expected direction. When the sequential multiple linear regression analysis was performed, four separated models emerged. In Model 1, age and seniority at work were positively and significantly associated with FPR, but the number of dependents at home and self-perceived health were not. In Model 2, both financial literacy (β = .22, p < .001) and the level of training and education (β = .21, p< .001) were positively and significantly related to FPR as predicted by Hypothesis 1. In Model 3, both psychological preparation for retirement (β = .16, p < .001) and retirement goals clarity (β = .09, p < .01) were positively and significantly associated with FPR, in line with Hypothesis 2. In Model 4, investment advice was not significantly associated with FPR (β = .03), whereas financial resources were positively and significantly associated with FPR (β = .56, p < .001), which partially supported Hypothesis 3 (Table 2). Taken together, the capacity, willingness, and opportunity dimensions provide a positive and meaningful prediction of FPR, even though investment advice, in the opportunity dimension, showed a positive but nonsignificant standardized regression weight. Furthermore, all the dimensions increased the explained variance, most notably in the cases of capacity and opportunity to plan and save (ΔR 2 = .12 and .22, respectively).

Means, Standard Deviations, and Correlations for Study Variables.

Note. N = 948. α’s values in the diagonal. FPR = financial planning for retirement; M = Mean; SD = Standard deviation. Source: Authors’ Calculations.

*p < .05. **p < .01.

Italics values in the diagonal are Cronbach's Alphas values.

Multiple Linear Regression Analysis Sequential.

Note. N = 948. β = standardized coefficients; FPR = financial planning for retirement. Source: Authors’ Calculations.

*p < .05. **p < .01. ***p < .001.

To test Hypothesis 4, the second analysis was aimed at exploring the moderating effect of age on the association between antecedents and FPR. Regarding Hypothesis 4a, the analysis tested the moderating role of M (age) on X (Level of training and education) → Y (FPR), with job seniority, number of dependents at home, self-perceived health, financial literacy, psychological preparation for retirement, retirement goals clarity, investment advice, and financial resources as covariates. The overall model was significant, F(11, 936) = 88.50, p < .001, R 2 = .51. The main effects of both level of education (B = .35, SE = .09, 95% confidence interval [CI] [.155, .537], p < .001) and age (B = .348, SE = .10, 95% CI [.135, .562], p < .01) were significant, as was the interaction term (B = −.133, SE = .04, p < .01, ΔR 2 = .005). Specifically, results indicated that the association between level of education on FPR decreased in magnitude from low (younger than 40; B = .196, SE = .05, p < .001) to moderate (between 40 and 55; B = .090, SE = .04, p < .05) to high (older than 55; B = −.016, SE = .05, p = .75) age levels. Consistent with our expectations, younger participants showed a greater level of FPR if they were characterized by a high level of education.

Regarding Hypothesis 4b, the first analysis tested the moderating role of M (age) on X (psychological preparation for retirement) → Y (FPR), with job seniority, number of dependents at home, self-perceived health, financial literacy, level of education, retirement goals clarity, investment advice, and financial resources as covariates.

The overall model was significant, F(11, 936) = 86.85, p < .001, R 2 = .50, but the main effects of both psychological preparation for retirement (B = .10, SE = .07, 95% CI [−.036, .244], p = .14) and age (B = −.01, SE = .12, 95% CI [−.23, .21], p = .92), as well as the interaction term (B = .01, SE = .03, p = .66, ΔR 2 = .0001) were nonsignificant. The second analysis related to Hypothesis 4b tested the moderating role of M (age) in X (retirement goals clarity) → Y (FPR), with job seniority, number of dependents at home, self-perceived health, financial literacy, level of education, psychological preparation for retirement, investment advice, and financial resources as covariates. The overall model was significant, F(11, 936) = 87.48, p < .001, R 2 = .50, but the main effects of both retirement goals clarity (B = −.05, SE = .05, 95% CI [−.15, .05], p = .37) and age (B = −.12, SE = .09, 95% CI [−.30, .05], p = .17), as well as the interaction term (B = .05, SE = .03, p = .06, ΔR 2 = .001) were nonsignificant. Both analyses fully rejected Hypothesis 4b.

To better understand which are the areas for improvement, we conducted IPMA analyses for each age-group, and the results are displayed in Figure 1. Specifically, financial resources showed a strong association with FPR in all groups. As shown in Figure 1, the IPMA of FPR reveals that financial resources have main importance for all the groups, even though relative differences in their performance when younger and older groups were compared. Moreover, the remaining variables showed similar importance for all groups, but their performance values were different. First, considering the young group, level of education and financial literacy showed medium importance, but relative low performance. Their importance was even negative when we the older workers group are considered. Consequently, interventions with young workers should be aimed to improve both variables. Second, for participants aged between 40–55 years and aged over 55, psychological preparation for retirement showed similar importance values and also it had relative high performance. This suggested that improvement on FPR could be focused on this construct. Third, considering those participants aged over 55 years, goals showed high performance compared with other groups, and it suggested that it would be an additional avenue to improve FPR among other groups. Finally, investment advice showed similar importance for all groups, but it performance increases slowly as a function of participant’s age, showing that earlier interventions to increase FPR should focus on this construct (Figure 1).

Importance-performance map analysis results for the three groups of participants. Source: Authors’ Calculations.

Discussion

The goal of the present study was to provide an initial empirical support for the FPR model proposed by Hershey et al. (2013), which is based on the three dimensions of capacity, willingness, and opportunity to plan and save for retirement, establishing age-based differences. FPR is a pressing issue today, given that the literature points to “unrealistic financial optimism” with regard to the availability of resources during retirement and the adequacy of future income streams (Hershey & Mowen, 2000). As argued by Taylor and Geldhauser (2007), anyone seeking to design measures to improve FPR must first understand why people decide to save and why they so often fail to commit to financial planning.

Perceived health does not emerge from among the sociodemographic factors analyzed as a key predictor of FPR. This finding is opposite to various previous meta-analytic reviews, which underscored the importance of health for retirement income and retirement income satisfaction (Topa et al., 2011). As retirement involves decisions with very relevant health implications, it is reasonable to assume that this factor will grow in importance as a predictor of FPR. However, the relationships between health and FPR may be complex and deserve further exploration.

The present study shows that age is positively and significantly related with FPR, in line with other researchers (Ekici & Koydemir, 2016). Moreover, age may act as a proxy measure for other factors like the increase in disposable income afforded by declining expenditures, as many people aged over 55 have no dependent children or elderly parents living at home, allowing them more easily to align the level of their spending with their incomes and manage financial constraints more easily. In any event, it seems clear that further research is needed to clarify these issues.

The second reason why people do not engage in FPR would be simply because they do not know how to plan (Taylor & Geldhauser, 2007). Our findings on capacity to plan and save for retirement revealed that both financial literacy and levels of training and education were positively and significantly related with FPR (Han et al., 2015). Meanwhile, psychological preparation for retirement would be considered as a proxy, which conceals the influences of other variables, as financial self-efficacy, that have an explanatory role in finance behavior, specifically for women, as has been recently stated (Zyphur, Li, Zhang, Arvey, & Barsky, 2015). While professional advice may be associated with higher levels of FPR, our findings in this regard are more complex. In the present study, this variable has a positive relationship but do not show any association with FPR when financial resources were included. This finding supports Taylor and Geldhauser’s (2007) assertion that the third reason why we do not see more FPR, specifically among low-income workers, is that they lack the money to save. Our study shows that financial resources are positively and significantly related with FPR, but the existing evidence on this score is controversial. Previously, certain other studies point in the opposite direction (e.g., Jacobs-Lawson & Hershey, 2005), suggesting that financial resources do not determine retirement saving because people often do not save despite having sufficient financial resources to do so. Given that the patterns identified could be influenced by methodological issues, more research is needed to clarify these relationships. Be this as it may, the measure of available financial resources used in this article was self-reported and therefore not objective, conditioning the reliability of our findings in this regard given the enormous variability in self-reported measures caused the phrasing of questions, the measurement scales employed to collect data, and the comparability of the indicators obtained in countries with widely differing currencies, income and employment parameters, tax systems, and financial conditions (Whitley et al., 2016). Moreover, self-reported measures are also affected by participants’ ability to make exact estimations of their annual income and total assets, not to mention the frankness of their responses. Indeed, responses may even conceal implicit comparisons with peers from the same socioeconomic group (Wang et al., 2016; Yu & Chen, 2016). According to various theories, such implicit comparisons in self-assessments affect not only responses but also income satisfaction per se (Ekici & Koydemir, 2016).

The main aim of this study, to provide an overall assessment of Hershey’s model (2013), has been met, despite some minor differences in the relevance of the relationships between age groups. As the authors of the model stated, the dimensions were not orthogonal, and its interactions allow us to explain the complex picture of financial planning and decision-making. In this study, we also found differences in the importance and performance of the model variables between the three age groups. First, financial resources are more significant for the older age-group, but not investment advice. This may be because there is a link between the use of financial advisory services and the level of education and training, given that it has been shown that better educated people are more likely to seek professional advice (Hirschi, Jaensch, & Herrmann, 2017). Thus, people plan the financial aspects of their retirement more diligently as they grow older (Van der Velde, Jansen, Bal, & Van Erp, 2017). However, both psychological preparation for retirement and goal clarity have a greater association with FPR among older workers, as might be expected in view of the proximity of retirement for this group. In light of the foregoing, researchers interested in facilitating adjustment to retirement via FPR will need to explore age-based differences in the causal relationships between psychosocial antecedents and financial planning behaviors more thoroughly.

Limitations and Suggestions for Future Research

Generalization of the findings from this study is complicated in the first place by its cross-sectional nature. There can be little doubt that the performance of longitudinal studies of FPR would enrich our knowledge of the process. In the second place, all of the participants in the study were Spanish. Hence, our findings need to be treated with some caution, despite the proven power of the variables normally used in the literature to predict FPR in different cultural contexts (Teerawichitchainan & Knodel, 2015; Trzcińska & Goszczyńska, 2015). The study is subject to obvious limitations in terms of the size and representativeness of the sample and of the sampling procedure used. The other major limitation concerns the self-report data collection procedure used, which can be a source of uncontrolled common variance error. Additionally, we have collected limited data related to socioeconomic status. Hence, future studies could use best practices to assess and integrate this information into FPR, as recommended (Diemer, Mistry, Wadsworth, López, & Reimers, 2013).

At the theoretical level, we would recall that the factors influencing the saving and planning behaviors of older people are very diverse, and the nature of the relations between psychological, financial, and contextual variables is likewise enormously complex (Rahimi, Hall, & Pychyl, 2016). It has recently become clear that holistic approaches are needed if we are to understand financial planning for retirement more fully (Dolinski, Dolinska, & Bar-Tal, 2016). Nevertheless, few scholars have successfully advanced in this way (Harkin, 2017). Several directions could be taken to develop the model. First, wider research into external constraints, such as the influence of household debt on levels of engagement with FPR (Bernstein, 2004), would be recommended. Second, positive psychological capital could be explored as an antecedent, based on research positing this dimension as an important set of resources which could affect more general retirement planning and, in turn, impact on FPR (Topa, Jiménez, Valero, & Ovejero, 2017). Finally, in certain cognitive variables, including needs for cognitive closure (Dolinski et al., 2016), procrastination may be associated with attitudes toward FPR (Rahimi et al., 2016).

Practical Implications

In addition to the new avenues of research mentioned above, this article has various practical implications. To begin with, our findings using the proposed model show that greater emphasis should be placed on the development of financial retirement plans designed to attract younger savers in order to assure their financial security upon reaching the age of retirement. Several studies have repeatedly drawn the attention to the impact of workplace financial education on FPR outcomes, providing both quasi-experimental evidence and evidence from panel surveys (McWhirter, Luginbuhl, & Brown, 2014). Also, initiatives to improve financial education have been proposed, applying innovative methodologies like contemplation (Harkin, 2017). To sum up, career counselors and practitioners could help improve individual competence in investment matters through the implementation of financial education programs focusing on the most prominent factors of the Hershey model (Resende & Zeidan, 2015). Given researchers’ insistence on the relevance of personal optimism (Zyphur et al., 2015) and perceived mastery in FPR, it would be recommendable to propose interventions aimed at boosting these specific variables. Moreover, research consistently focused on the gender differences in FPR (Heilman & Kusev, 2017), which would be also associated with smaller spouse participation in retirement saving. In view of the long-term implications of the gender gap for retirement savings, workplace programs should be directly designed to increase women’s engagement with FPR (Fabre, Causse, Pesciarelli, & Cacciari, 2016).

Furthermore, financial advisers could help themselves and the wider population by performing periodic evaluations of FPR to identify changes in savings trends over time and achieve a better understanding of their clients as a basis for the design of individual FPR proposals tailored to individual needs, given the relevance of personal priorities and the meanings individuals attach to goals on levels of FPR engagement (Süssenbach, Gollwitzer, Mieth, Buchner, & Bell, 2016). Finally, it has been argued that the motivational processes underlying financial behavior in general, and specifically FPR practices, are crucial to achieving the desired outcomes (Martínez-Ruiz, Izquierdo-Yusta, Olarte-Pascual, & Reinares-Lara, 2016). Hence, government should actively promote political initiatives to create tax incentives to encourage saving for life after retirement. This article represents a further step along the way toward more integrated and comprehensive approaches to FPR, given that the study of retirement planning has now begun to include ever more financial, psychological, and social dimensions. At the same time, it will be crucial to progress with research into the FPR process in view of the wave of retirement policy reforms undertaken in numerous countries, most of them intended to shift some of the responsibility for financial planning for old age onto individuals.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.