Abstract

Much of the large literature on precarious work has largely tended to assume that precarity is shaped by job quality: that precarious work leads to precarious lives. This paper adds to the literature by questioning this line of causality and highlighting the broader range of influences shaping the lives of older workers who enter precarious work after retrenchment from secure, long-term careers. Drawing on a study of Australia’s automotive manufacturing industry, which closed in 2017, this article finds that for older retrenched workers, exposure to precarious employment sharpened life precarity for some but did not lead to precarious lives for others. Instead of a uniform transition from security to precarity, these workers’ life trajectories diverged depending on their household-scale financial security. Key issues influencing the likelihood of older workers’ lives becoming precarious were enterprise benefits and asset wealth accumulated through their previous careers.

Keywords

Introduction

Much of the vast literature on precarious work has emphasised the forging of precarious lives through the experience of work and employment. Assumptions of a direct correlation between the characteristics of poor-quality jobs and the precarity of workers’ lives underlie this emphasis; that is, precarious work leads to precarious lives (Kalleberg, 2011; Lewchuk et al., 2008; Standing, 2011). But there have also been critical accounts that modify or challenge this predominant approach by reversing the line of causality – that is, precarious lives lead to precarious work (Anderson, 2010; McDowell et al., 2009) – or, alternatively, rethinking cause-and-effect logics in the reproduction of precarity (Gallie, 2009; Kalleberg, 2018).

These insights have received attention among key groups of workers exposed to precarious work, including young, tertiary-educated workers who struggle to find secure employment and immigrant workers whose precarity in employment is sharpened by the absence of citizenship rights. In contrast, the group that is the focus of this article – older or established workers who are expelled from relatively stable, long-term careers through downsizing, plant closures and retrenchment – has received less attention. This leaves a residual assumption among researchers that retrenched workers’ lives will gradually but predictably become precarious due to the increasingly pervasive influence of precarious work.

In response to this problem, this article reframes precarity among older retrenched workers as a relational and temporal process – one in which the experience of work is mediated by prevailing regulatory regimes and household-scale financial arrangements – rather than an outcome with direct causal antecedents in job quality. In this reframing, precarious work becomes one determinant rather than the determinant of precarisation among retrenched workers. This means that, in some scenarios, the experience of precarious work does not have a negative impact upon workers’ life trajectories while, in others, a prevailing sense of precarity is sharpened by the experience of insecure, post-retrenchment jobs.

This article deploys a case study of the collapse of Australia’s automotive manufacturing industry in 2017 to demonstrate this argument. While exposure to precarious work became widespread among workers retrenched in the wake of the collapse, the extent to which their lives could be accurately described as precarious depended upon a broader range of determinants, including redundancy pay, alternative household income sources and assets-based wealth through home ownership and private pensions. These factors tended to consolidate divergent life trajectories among workers that were already prevalent at the point of retrenchment.

The article proceeds as follows: first, a literature review explores recent contributions on precarity in order to foreshadow our discussion of divergent life trajectories. Second, we outline our case study, data and methods. Third, an empirical section outlines the process of precarisation among retrenched auto workers in Australia to identify the factors that have contributed to these different pathways. Fourth, a discussion section argues that these factors can be understood through the lens of divergent life trajectories.

Precarious Work and Precarious Lives

The idea that precarious work leads to precarious lives has become a common refrain within the interdisciplinary field of precarious work studies. It is now widely understood that dependence upon precarious work has a negative impact on an individual’s mental and physical health and well-being (Kalleberg 2011, 2018; Lewchuk et al., 2008). A dominant line of causality has been established, which begins with the character of jobs, work and employment and which finishes with the state of the individual. As Kalleberg (2009: 1) has written, a ‘focus on employment relations forms the foundation of theories of the institutions and structures that generate precarious work and the cultural and individual factors that influence people’s responses to uncertainty’.

Standing (2011, 2014) has gone further in suggesting that the rise of precarious work has produced an emerging but distinctive social class – the ‘precariat’. The concern is this article is less about Standing’s claims about social class – which have been widely and vigorously debated elsewhere (see, inter alia, Jørgensen, 2016; Paret, 2016; Alberti et al., 2018; Pang, 2019) – and more on his emphasis on precarious work as the driving force for precarious life. Arguably the most attention in Standing’s work has been on the negative definition of precarious work as an absence of ‘forms of labor-related security’, which set standards for decent employment in previous decades, including adequate opportunities to earn wage income, protection against arbitrary dismissal and collective voice in the workplace (also see Vosko, 2010; Kalleberg, 2011). Although Standing discusses other factors, the core of his argument is that the decline in social protection linked to standard employment has driven the contemporary tendency towards precarity.

However, there have long been alternative approaches to those studies that draw a direct causal line from job quality and employment attributes to individual precarity. One alternative has been to focus on the ways in which individuals’ social or embodied attributes, especially their gender or ethnicity, align with sectoral and occupational divisions of labour in order to sharpen their vulnerability (McDowell et al., 2009). Such studies effectively reverse the line of causality in precarious work research; that is, precarious work roles are socially and institutionally allocated for individuals with attributes that give them a higher probability of experiencing precarious lives or, in short, precarious lives lead to precarious work (Anderson, 2010).

Other alternatives have shifted attention to the institutional arrangements that mediate the relationship between individual workers and precarious work scenarios. In these studies, some regulatory regimes play a role in facilitating or enhancing the precariousness of work while others can alleviate or cushion the negative impacts of precarious work. To demonstrate this, some studies have focused on the household scale (Campbell and Price, 2016; Clement et al., 2009) while others have focused on national institutional regimes in which international diversity in welfare and employment policies leads to different outcomes for individuals exposed to precarious work in different countries (Gallie, 2009; Kalleberg, 2018).

While these approaches question dominant conceptualisations of causality in precarious work studies, they are yet to elicit a large response through research on older workers. Among those older workers whose livelihoods have been upended by retrenchment, most recent studies have tended to follow the predominant logic by focusing on the impact of lower wages, less secure jobs and non-standard work (Bailey and de Ruyter, 2015; Varga, 2013). The lingering assumption is that retrenched workers’ lives are likely to become more precarious and that this can be deduced by ‘reading off’ the characteristics of their poorer-quality post-retrenchment jobs.

Sometimes this is true but, as we contend, not in all cases. One recent alternative is provided by Lain et al. (2019) who, following Millar (2017), argue that what matters is workers’ ‘ontological precarity’ – that is, the extent to which they ‘view their reality as being precarious’ (Lain et al., 2019: 2222) – rather the ‘labor condition’ that derives from the experience of work. Thus, ‘the extent to which an individual feels precarious will also depend on whether or not their wider life circumstances provide security’ (Lain et al., 2019: 2222). Standing has partly recognised this problem among older workers by drawing a contrast between ‘grinners’ who have ‘adequate pension and healthcare coverage. . . who can do odd jobs for the pleasure of activity or to earn money for extras’ (Standing, 2011: 59) and ‘groaners’ who ‘have no pension to write home about, have a residual mortgage or have nothing to write home about because they have no home’ (Standing, 2011: 84).

However, such observations are only a beginning. This article extends these insights in two main ways. First, by rejecting the idea that precarity can be deduced by analysing a list of job quality characteristics, it adopts a relational understanding of precarity in which workers are positioned within a ‘triadic configuration of relations’ between states, markets and civil society (Pang, 2019). For example, the relative precarity of retrenched workers is shaped by their relations with labour markets, including their capacity to locate and access new employment. However, it is also shaped by their relations with state institutions, including policies that facilitate (or undermine) the social protection of unemployed workers like unemployment insurance or legally sanctioned redundancy payments, or relations with civil society organisations like trade unions.

To demonstrate these relations, the article utilises a study of retrenched workers who experienced precarious work following the closure of the automotive manufacturing industry in Australia in 2017. In terms of relations to civil society, this case study is instructive because of Australia’s tradition of relatively strong historical protections for workers vis-à-vis unionisation in manufacturing occupations and union-negotiated redundancy pay. In terms of relations to the state, the study is also relevant because of Australia’s distinctive tradition of asset-based welfare for older workers based on compulsory saving into private pension accounts (alongside a public means-tested age pension) and incentives for private home ownership.

The policy of compulsory private pension accumulation – known in Australia as superannuation – was designed to reduce dependence on the age pension among the working classes. Since 1992, all employers have been required by law to pay a minimum of 9 per cent of workers’ ordinary time earnings – raised to 9.5 per cent in 2014 – into a superannuation fund or retirement savings account. Employees can begin to access income from superannuation once they reach their ‘preservation age’, which is 55 for those retirees born before 1960, gradually increasing to 60 for those born later. Furthermore, the home ownership rate among older people is around 80 per cent. Among older homeowners, 77 per cent owned their home outright by 2006 – that is, they had paid off all mortgage debt on their primary residence enabling them to boost discretionary income in retirement in the absence of ongoing housing costs (Yates and Bradbury, 2010).

The second way in which the article extends insights into precarity among retrenched older workers is by emphasising the temporal, as well as the relational, dimension of precarity. We understand precarity as a process of precarisation whereby risks are shifted, in multiple ways, from employers or state institutions onto individuals and households (Alberti et al., 2018). Retrenchment involves multiple stages, from the announcement of job loss, to the period of retrenchment, to the experience of job searching, to the acceptance of new jobs or withdrawal from the labour market. For workers retrenched from long-term careers, their relations with states, markets and civil society therefore go through a process of transition. For example, the relational impacts of labour markets change as workers move from relatively secure to relatively precarious jobs. Similarly, relations with civil society change if, for example, workers move from jobs with relatively strong union protection to jobs with lower union density and strength.

In temporal terms, the key missing issue in studies of precarious work among retrenched older workers, we argue, is the extent to which retrenched workers are already on a particular life trajectory at the time of their retrenchment, one which is tied to the economic securities and benefits they have accrued (or been denied) through their long careers – that is, through their previous relations with markets, states and civil society. These benefits can include the wealth impacts of private savings and asset ownership, especially equity value held in private housing. Post-retrenchment experiences can enhance or erode these prevailing life trajectories.

For older workers in Australia who move from previously secure long-term employment into precarious jobs, therefore, the question becomes: to what extent are retrenched workers shielded from the negative impacts of precarious work by asset-based welfare, such as the atrophy of housing costs through private home ownership? Conversely, to what extent are once-protected workers exposed to these impacts? The evidence we present in this paper suggests factors like superannuation savings and home ownership, as well as redundancy payments and spousal income, interact with the dynamics of precarious work to generate a process of precarisation which is highly uneven. Before returning to this argument, the following section outlines the nature of our case study, data and methods.

Case Study, Data and Methods

To address our research questions, we use data gathered from semi-structured interviews with retrenched auto workers. In 2016 and 2017, Australia’s last three carmakers – Toyota, General Motors Holden (GMH) and Ford – progressively closed their vehicle manufacturing plants. Historically, the auto industry has been a trendsetter for advanced manufacturing technology and innovation, as well as wages, employment conditions and union rights. Therefore, the loss of domestic manufacturing was lamented by a wide range of civic and political actors (Beer, 2018). Recently, the Federal Government estimated that close to 14,000 direct job losses among carmakers and supply chain companies had occurred 12 months since the final closures (Australian Government, 2019).

Australia has undergone a long process of manufacturing decline driven by forces of trade liberalisation, government-sponsored restructuring and rising demand for service sector employment in major cities. In more recent times, the restructuring of the global auto industry after the Great Recession of 2008–2010 and mineral resource expansion during the 2000s and 2010s, which drove a sharp appreciation of the Australian dollar, further undermined domestic manufacturing.

After the closure of manufacturing facilities, a fundamental issue for most workers was the lack of occupationally appropriate employment with working conditions comparable to their previous careers. Almost all employees were employed on a permanent full-time basis prior to the closures – 96 per cent according to workers’ unions. In Australia, a permanent work contract means that an employee has a range of paid leave entitlements, such as annual leave and sick leave. By comparison to the automotive workforce, only half (50 per cent) of all Australian workers in paid employment in 2017 had full-time jobs with leave entitlements (Carney and Stanford, 2018).

The average tenure in automotive jobs was 23 years. Eighty-five per cent had been employed for 10 years or more, compared to 25 per cent for the working age population (ABS, 2018). Auto plants were also bastions of union membership. Although union density had fallen to just 15 per cent of the Australian workforce by 2016 – and only 9 per cent of private sector workers – density within the auto industry remained unusually high. Within the three carmakers and among the industry’s larger suppliers, union density was generally above 80 per cent. Several workshops operated effectively as ‘closed shops’ with close to 100 per cent union membership.

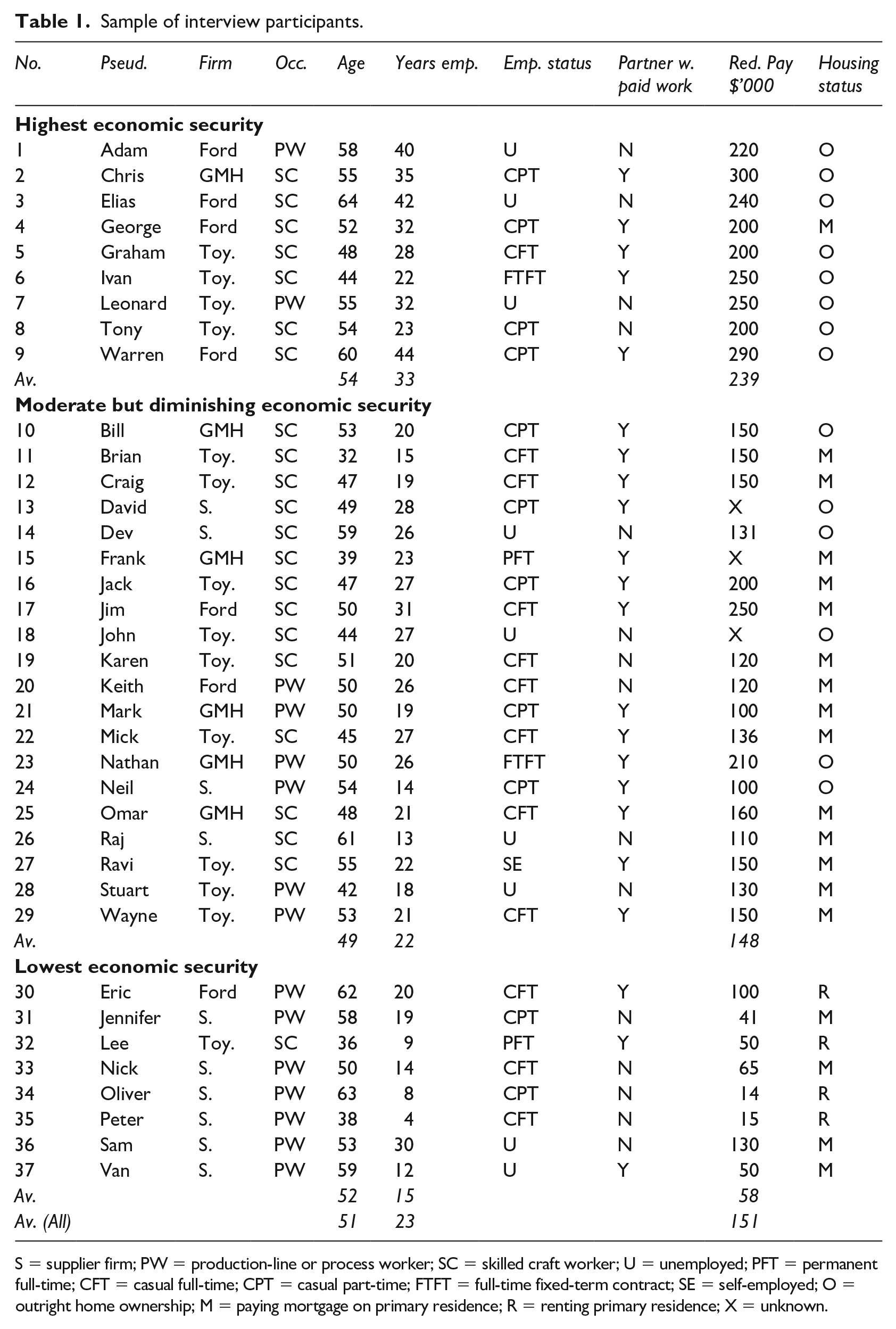

Our data was gathered as part of a three-year study into the closure of auto manufacturing plants in Australia. This study included sample surveys with over 400 union members in the Australian state of Victoria, where most retrenched auto workers are located, interviews with policy-makers and trade unions and analysis of company and government documents. However, in order to address the research questions for this article, we analysed data from interviews with 37 retrenched workers in the Australian state of Victoria. These interviewees were selected from the sample surveys. The full sample of interview participants in listed in Table 1, which includes basic data on workers’ broad occupational group, age, employment duration and employment status, as well as additional information such as the size of redundancy payments, the presence of a partner/spouse in paid work and whether or not they were paying off a mortgage, owned a home outright or renting. Interviews were conducted in Melbourne and the regional city of Geelong, which lies 75 km to the southwest of Melbourne. Pseudonyms have been used to protect anonymity.

Sample of interview participants.

S = supplier firm; PW = production-line or process worker; SC = skilled craft worker; U = unemployed; PFT = permanent full-time; CFT = casual full-time; CPT = casual part-time; FTFT = full-time fixed-term contract; SE = self-employed; O = outright home ownership; M = paying mortgage on primary residence; R = renting primary residence; X = unknown.

Each of the 37 participants desired new paid work after retrenchment. A minority of workers who wanted to retire or take an extended break from paid work were excluded from our sample. Among the interviewees, 27 worked for car assembly manufacturers and 10 worked for auto supply firms.

In order to analyse the temporality of precarisation, participants were interviewed in two stages: before and after retrenchment. The first round was conducted in March–May 2017, prior to the final closure of the industry in October 2017. The second round was conducted 12 months later – in March–May 2018 – or around 6 months after the closures. In the empirical section below, these two time periods are denoted as ‘Interview A’ and ‘Interview B’ whenever we use direct quotations.

The first round of interviews aimed to capture workers’ sense of their employment status and careers and their expectations for the future. At this point, we also collected basic data about workers’ financial security, including their household income and home ownership status. In the second round, we focused on workers’ employment situation post-retrenchment and their perceptions about changing work, financial and personal circumstances. Primary data from our interviews was triangulated with baseline data collected through the auto unions on their members’ pre-retrenchment employment conditions which were made available to the authors. While this is not intended as a representative data sample, the analysis aims to draw on qualitative data from the case study in order to outline the nature of the precarisation process as one which produces differentiated outcomes based upon multiple social and economic factors which include, but are not reducible to, job quality.

Interviews were digitally recorded and transcribed. Data was coded using Strauss’ approach (Strauss and Corbin, 1998). Key themes were identified using open coding. These themes were then broken down with axial coding to match with the core research questions concerning household income, home ownership and redundancy pay. Coding was used to categorise workers into groups based on subjective attitudes to new work and workers’ sense of their own security/insecurity. The following section draws on observations and quotations from selected participants in the study in order to demonstrate the linkages between workers’ subjective perceptions of insecurity and their overall financial security.

The Process of Precarisation

This section discusses the journey of a group of older workers who lost their jobs after the Australian auto manufacturing industry closed in October 2017. Thirty-five of the 37 interviewees were men. Their average age was 51 years (with ages ranging from 36 to 64 years). On average, workers had a further nine years before becoming eligible to access superannuation savings. Union workforce data showed that average weekly earnings (AWE) were $1256 at the time of the closures in October 2017. 1 Although this was below average AWE for all Australian workers, it was significantly higher than high-employing sectors such as retail trade (10 per cent higher) and accommodation and food services (13 per cent higher) (ABS, 2018). As argued above, these wages were earned in jobs with exceptionally high stability and predictability prior to the closure announcements.

Strong union membership was reflected in redundancy payments for retrenched workers. Although the minimum redundancy entitlement for permanent workers with over 10 years of service was 12 weeks’ wages under the Fair Work Act 2009, auto workers could access significantly more generous entitlements through union-negotiated enterprise agreements in each firm. Most workers who had been employed by leading carmaker firms finished with up to four weeks’ redundancy pay for every year of continuous service – generally capped at 90 weeks’ wages.

Due to their exceptionally long job tenure, most workers received close to this cap under each firm’s enterprise agreement and many received the full 90-week allowance. Payments were higher still because most enterprise agreements allowed workers to ‘cash out’ a range of extra-wage benefits like sick leave, annual leave and long service leave. According to union workforce data, the average expected redundancy payment prior to closure was $137,280 or around two years’ average wages. In our sample, the average redundancy payment was 10 per cent higher than this ($151,000) (see Table 1).

In summary, data gathered prior to the final closures in 2017 suggests that workers’ experiences were shaped by standard, protected and decent wage employment with high union representation and exceptionally long employment duration. For the majority of retrenched workers who desired re-employment, this picture of workplace stability changed radically after the closure of the industry.

Precarious Work after Retrenchment

While most workers who needed to work were able to find employment, only a minority were able to obtain permanent full-time jobs. According to union workforce data, about three quarters of retrenched workers who remained in the paid labour force (i.e. excluding those who had fully or temporarily retired) had paid work 12 months after the closure of the industry. But fewer than half of these workers (45 per cent) had a permanent full-time job, representing a major decline in standard employment. A further 11 per cent had a permanent part-time job, 30 per cent were casuals and 14 per cent had fixed-term contracts with an expiry date.

‘Casual’ is the main form of non-standard employment arrangement in Australia and refers to category of workers who do not have a commitment about the duration of their employment or about regular or minimum working hours. It also includes most types of agency or labour-hire employment in which workers are hired by a third-party intermediary. Casual workers are not entitled to any form of paid leave or redundancy pay (Campbell et al., 2009).

There was a high incidence of casual, intermittent and short-term work in our sample. Although nine out of the 37 workers were unemployed at the time of their second interview, all had undertaken at least one paid job in the period since their retrenchment. Only two out of the 37 had a permanent full-time job. Twenty-three had casual jobs, including 12 with casual full-time jobs and 11 with casual part-time jobs. A further two workers had fixed-term contracts and one was self-employed (see Table 1).

All the people in this cohort of casual and fixed-term workers stated that their new jobs had inferior conditions compared to their previous careers in the auto industry. Many complained about a lack of job security. For example, after 14 years as a process worker in an auto parts supplier in Melbourne’s north, Nick had begun working evening shifts at a kitchen parts manufacturer: I’m working [under] probation for six months and that is the hard thing. . . The problem is you don’t know [if] they [will] keep you or not. . . They push you to your limit and then when you finish. . . [the] next question is if they reject me from there (Nick, aged 50, Interview B, 28 March 2018).

Such a fear of job loss forced many workers to accept inferior working conditions. For example, Mark expressed his frustration at being forced to accept unpredictable casual shifts as a bus driver after 19 years as a production-line worker employed on regular day-shifts at GMH: ‘I’m not happy but I need a job. That’s why I’m doing [this]. [I have] no choice’ (Mark, aged 50, Interview B, 12 May 2018).

Impact of Seniority, Employment Tenure and Redundancy Pay

The incidence of precarious work and concerns about job insecurity were high among retrenched auto workers. These concerns stood in contrast to the benefits of their previous jobs. However, these past benefits also flowed into workers’ redundancy pay in ways that shaped present-day labour market experiences. The size of redundancy payments varied between firms and between workers on the basis of occupation, seniority and employment duration. Older workers in skilled trade occupations with above-average job tenure – that is, longer than 23 years – tended to receive the largest redundancy payments.

The highest single payment in our sample was $300,000 paid to Chris, a skilled craft worker who had spent 35 years working for GMH in Port Melbourne. Chris was able to use part of his payment to pay-off the remainder of his household’s mortgage debt: [Finishing] with [GMH]. . . enabled us to pay off the house, pay off the credit cards. . . put some money in the bank, have a bit of a top up in [superannuation], bought a new car. . . [We will] jump in the caravan next week, and go up to Queensland for a working holiday. . . [We] can only afford to do this now obviously because of the payout from [GMH]. I’m happy. I’m in the twilight of my working career. . . [We’ve] still got another two or three years where we’ll probably need to work, you know, maybe full time but preferably casual or part-time, utilising some of the payout money and then when I hit 57 I think I’m pretty much going to go into full retirement mode, yeah, and just survive off my super and my wife’s super until we get to the aged pension and then. . . it’s early retirement for me (Chris, aged 55, Interview B, 3 May, 2018).

At the other end of the spectrum were lower-paid, lower-skill production-line workers and younger workers with more limited job tenure and significantly lower redundancy payments. For example, Peter was a process worker from a supply chain company in Melbourne’s western suburbs. His career had been a series of modestly paid manual jobs until his most recent job in the auto industry, where he had worked for four years. This left him with a $15,000 redundancy payment, which was too little to enable him to stay out of paid employment for long: My [previous] pay level. . . [was] pretty much my budget. . . I have very little money left over after the end of the month. . . Um, so yeah, I wouldn’t be able to go too much lower. . . But there is only agency work that I can see. I mean, I look in the [newspapers] and [job-search websites] all of that, but nine times out of 10, they’re going to be through agencies (Peter, aged 38, Interview A, 7 May 2017).

His dependence on finding jobs through employment agencies was a source of anxiety: I reckon I’ll be alright, but I’ll. . . yeah. I’m a little worried. I’m a little worried. Probably more because there’s going to be so many people out of work and trying to find the same jobs. . . I’ve pretty much always worked through agencies, and most of the time, you know, they’ll call you up for a job on the other side of the city, and you say, ‘No, I don’t particularly want to take that’ and they don’t call you back. . . (Peter, aged 38, Interview A, 7 May 2017).

In between the two poles represented by Chris and Peter, the majority of workers in our sample received redundancy payments, which provided them with a measure of immediate protection after their retrenchment. Thirteen out of the 37 workers in the sample received above-average redundancy payments. David, who had spent a 28-year career as a fitter and turner at a major supplier in southeast Melbourne, summarised the perspective of these workers: ‘I don’t need to go straight into a new job. Oh, no, because they’re going to give us severance pay. . . [It’s] a bit of a buffer’ (David, aged 49, Interview A, 13 April 2017).

However, David was aware that a precarious situation could gradually emerge if he failed to find secure employment: ‘I’m not stressed out at the moment, but ah. . . yeah. A little bit unsure of what’s going to happen’ (David, aged 49, Interview A, 13 April 2017). By the time of his second interview, David was employed in a casual part-time role. Those workers who, like David, were forced to spend down their payment as a primary source of day-to-day income were under greater pressure to take whatever employment was available. As the following sections show, the degree to which workers used their redundancy payments as a de facto wage income was shaped by underlying financial factors at a household level.

Role of Households, Home Ownership and Housing Costs

Apart from variations in redundancy pay, there were several household-level factors that influenced workers’ exposure to precarious work. First, workers who lived in households with more than one contributing source of income were under less pressure to settle for precarious jobs. In our interview sample, the majority of workers – 22 out of 37 – had a partner or spouse in paid employment. A further impact was the extent of superannuation and workers’ eligibility to access these savings. Finally, household security also reflected levels of home ownership.

In our sample, 14 workers owned, or co-owned, their main residence outright and had settled all mortgage debt, 19 workers were still paying off their mortgage and four workers were renting. Chris, the recipient of the largest redundancy payment in our sample, had used part of his payment to pay off the remainder of his household’s mortgage debt: ‘You know, it wasn’t a big mortgage, it was probably $50,000 [left to pay]. . . [We live] in a 4-bedroom home. . . where the property prices are booming’ (Chris, aged 55, Interview B, 3 May, 2018).

Chris’ date of birth also meant that he could begin to access his superannuation within three years. Household disposable income was further boosted by his wife’s wage income – she continued to work in a permanent part-time job in retail services – as well as her accumulated superannuation. Although Chris had been working casually in small business as a truck driver and was earning a wage approximately 30 per cent lower than his salary at GMH, he was entirely protected from the negative impacts of precarious work: ‘Ah, it hasn’t been too difficult in terms of work, you know…. It’s just been driving the [truck] around doing deliveries. . . [It] hasn’t been too draining’ (Chris, aged 55, Interview B, 3 May, 2018).

Warren was in a similarly secure position. In his household, income was comprised of his wife’s permanent part-time job as a schoolteacher, superannuation payments from his 44-year career at Ford’s Geelong facility and wages from his new job as a casual bus driver for a local school. Even before receiving his $290,000 redundancy payment, his mortgage debt had been paid off in full. His motivation for working was to ‘keep myself busy’ rather than due to any immediate financial pressure: ‘It’s really just a fill-in job when someone else can’t do it. . . The little bit of [casual] work I’ve done [since leaving Ford], it’s just sort of like “beer money”, but it’s good for me’ (Warren, aged 60, Interview B, 3 April 2018).

Other workers with sizeable redundancy payments, superannuation savings and equity in housing had a degree of protection even though they were in a less enviable position than workers like Chris and Warren. For example, Stuart had done some casual truck driving but was unemployed at the time of his second interview, after an 18-year career as a production-line worker at Toyota. He did not have a partner or spouse and had to meet his mortgage repayments from his $130,000 redundancy payment until he found new work: I feel financially okay. I’m all right because of the redundancy package. If I didn’t have that I would be pretty concerned with how I was going to get by. . . [If] I was out of work for this long without any income. . . I would be really concerned, you know. I wouldn’t like to be in that situation (Stuart, aged 42, Interview B, 28 March 2018).

Similarly, John received an above-average redundancy payment after his 27-year career as a fitter and turner at Toyota. Although he had little mortgage debt leftover, he was a single divorced father and did not have a spouse or partner to provide additional household income. While John’s situation was not precarious in the short term, he was increasingly vulnerable in absence of ongoing, well-paid work. He was unemployed at the time of his second interview, having worked in two casual jobs in the previous six months: At the moment, I still have to work. . . Within another 12 months from now if nothing happens I’ll be in dire straits. . . I’ve been living off [my redundancy payment], you know? I reckon my package. . . keeps [me] secure for [another] 12 months without working (John, aged 44, Interview B, 18 March 2018).

Workers like John and Stuart had some immediate protections, including above-average redundancy payments accumulated from decades as skilled craft workers and equity in mortgaged homes. However, their need to sustain wage incomes for decades before reaching their preservation age – and longer before reaching retirement age – meant that long-term exposure to insecure work could potentially generate a slide into precarity.

Other workers were in a much weaker position financially and, therefore, already in a precarious position at the time of their retrenchment. Although he had an average redundancy payment after 30 years working as a process worker in a parts supplier in southeast Melbourne, Sam needed ongoing work to meet his mortgage and other household commitments. He was unemployed at the time of his second interview, had no partner or spouse and had caring commitments for his elderly mother. Sam had only been through one temporary warehouse job in the previous 12 months and continued to spend down his redundancy payment in order to meet his week-to-week expenses: I need a job. I can’t stay the way I am. . . I’ve got some money in the bank but in another year or two I’ll be all run out. . . I don’t know what I’m going to do. . . I don’t know what will happen to me. . . I don’t know [tips head back]. . . Every day I’m thinking well, you know, what am I - what am I to do? I’m having to pay, electricity, gas, you know, water, phone, internet. . . It all adds up. . . I mean, I’ve got my superannuation but. . . then again is that enough? No. Not going to be enough. So I’ve got to think of trying to adjust; trying to get myself a job now if I can. Whether it’s part time or full time, either way I’ll take it, you know? (Sam, aged 53, Interview B, 26 April 2018).

Sam’s situation summed up the exposure of the worst-positioned older workers to the negative effects of precarious work. A likely future of income poverty meant that Sam was prepared to accept any kind of employment. However, his age and his three decades in secure, protected employment with few marketable skills outside manufacturing put him in a weak position to compete against younger jobseekers for poorer-quality entry-level jobs.

Discussion: Precarisation and Life Trajectory

Evidence from our interviews on the process of precarisation shows that ex-auto workers were exposed to a higher incidence of precarious work after their retrenchment. This exposure stood in contrast to their prior experience of long-term, secure employment in well-paid, stable and predictable jobs. However, retrenched workers’ experiences also diverged on the basis of key financial influences like redundancy payments, household income and asset wealth in the form of superannuation savings and home ownership. In this section, we compare the statements of interview participants discussed in the previous section with the summary data presented earlier in Table 1. In doing so, we suggest that these different experiences represent divergent life trajectories.

The first life trajectory was represented by those retrenched workers with relatively high economic security. These workers’ interviews were characterised by statements that revealed a relaxed attitude to post-retrenchment life and a sense of contentment with household financial arrangements. Workers in this group include Chris and Warren, both of whom were mentioned in the previous section and who exemplified this optimistic outlook. Although all workers in this group had only been through casual or fixed-term jobs, none complained about lower wages, insufficient working hours or a lack of employment security. Each worker in this group framed insecure jobs as fulfilling temporary needs. Most saw these jobs as peripheral arrangements, which provided a bridge between their working lives and retirement in the foreseeable future.

Furthermore, most of these workers (seven out of nine) came from skilled craft-based occupations, which had enabled them to accumulate significant superannuation savings and to maximise their redundancy entitlements. These workers were more likely to be older and the closest to retirement age. The average age of these workers was 54 and their average employment duration in the auto industry was 33 years. All but one co-owned their homes outright (see Table 1). These workers had a very limited dependence on ongoing wage income and, therefore, on precarious jobs. In terms of a ‘triadic and relational understanding of precarity’ (Pang, 2019: 560), these workers were thus insulated from the risks of unpredictable labour markets and precarious post-retrenchment jobs by the financial benefits they had accrued through prior relations with long-term employers, unions and state institutions, in the form of accumulated superannuation, asset wealth in housing and union-negotiated redundancy pay.

The second life trajectory was represented by those with moderate but diminishing economic security. Interviews with these workers were characterised by statements about opposing forces; on one hand, long careers and enterprise benefits that had provided a significant degree of protection after retrenchment and, on the other hand, a concern about the capacity to maintain living standards in the longer term and anxiety about the future. This view was exemplified by the statements of David, John and Stuart. Although they were more likely to be younger than those workers in the high-security group (with an average age of 49) and generally desired another decade or more of full-time paid work before retirement, only one of these workers had a permanent job at the time of their second interview. While these workers had accumulated sizeable redundancy payments and equity in housing assets, their household wealth was not as impressive as workers in the high-security group. Their average redundancy payment was $148,000 – much lower than the $239,000 paid on average to workers in the high-security group. Fourteen out of these 19 workers were still paying off mortgages.

Although most had a spouse or partner in paid work (13 out of 19), these workers had a higher vulnerability to the negative effects of precarious work and were at longer-term risk of sliding into precarity. Generous redundancy payments and financial equity in home ownership promised to, potentially, consolidate a pre-existing sense of security but long-term exposure to precarious work threatened to disrupt this trajectory and to unravel previously secure lives.

The third life trajectory is based upon those workers with low economic security. Interviews with workers from this group were characterised by a high degree of stress and anxiety when asked about their employment and financial circumstances. Underlying fears of destitution and marginalisation were exemplified by interviews with Nick, Peter and Sam. These workers’ lives could already be described as precarious. Seven of these eight workers had held long-term careers as lower-paid production-line or manual process workers and lacked formal qualifications.

Like most other workers in the sample, casual employment was the new norm. Only one of these workers had a permanent job. Most (five out of eight) did not have a partner or spouse in paid work to assist with household expenses. Half of these workers were renting and had no asset wealth in housing. The average redundancy payment in this low-security group was $58,000, or less than a quarter of the average for workers in the high-security group. These workers were the most vulnerable to accepting whatever work was available, including temporary and short-term jobs. With relatively few assets, few alternative income sources and ongoing housing costs, they were on a pathway of precarious life which was becoming increasingly difficult to reverse or dislodge.

Thus, instead of a uniform transition into precarity, we find a picture of diverse life trajectories. At one end of the spectrum, there was a relatively privileged group of workers who were shielded from market volatility and who could not be described as precarious in any meaningful way despite their exposure to insecure jobs. At the opposite end of the spectrum was a group of workers who were already in a precarious situation after the closure announcements. In between these two groups was the majority of retrenched workers, who had sufficient alternative income sources and a measure of asset wealth to provide short-term protection alongside ongoing exposure to precarious work. The fact that most workers in this intermediate group were years or decades away from their preservation and retirement ages mean that its members may splinter in the longer-term between those able to accumulate sufficient wealth to maintain living standards in retirement and those threatened with a long-term slide into precarity.

Conclusion

The unevenness of experiences after the closure of auto manufacturing in Australia stands in contrast with the ubiquitous character of precarious work encountered by retrenched workers. Most workers who sought re-employment experienced jobs that were insecure and poorly protected in comparison to their previous careers. Yet, while precarious work was the norm, only in some cases did it sharpen the precariousness of workers’ lives. Trajectories of growing precarity (or, alternatively, growing economic security) were not contingent upon any single facet of the post-retrenchment experience such as job quality but, rather, upon the interaction of precarious work experiences with household-scale financial security.

Under institutional regimes with widespread asset-based welfare such as Australia’s, it is especially important to understand the distinctive economic benefits accrued by workers through long careers in protected occupations and the ways in which these benefits push workers onto life pathways that are already present at the time of retrenchment. These trajectories can be further enhanced or eroded by the experience of new jobs.

Findings from this case illustrate that precarisation can be a differentiating process among workers previously accustomed to secure, standard employment. However, they do not represent the experience of all workers retrenched from long-term careers. Of particular note is the strength of workplace conditions, epitomised by generous redundancy entitlements, which flowed from the historical strength of unionism in the auto industry. The benefits of these conditions are less apparent in many other industries where workers are the victims of large-scale retrenchment events.

For example, most workers in sectors such as warehousing or retail trade, where many retrenched auto workers found re-employment, do not have access to the same levels of union protection, redundancy entitlements and historical income and employment security. Consequently, the trajectories of retrenched workers from these industries are likely to be less positive overall than the experiences of retrenched auto workers. For these reasons, future research will need to compare the process of retrenchment for workers from industries with relatively high levels of security with workers from industries with lower levels of security. In this way, the extent to which the process of precarisation is differentiated along the lines of the ex-auto manufacturing workforce can be more fully analysed and understood.

Footnotes

Acknowledgements

We thank the participants of the 2018 Seminar on Precarity, organised by The Australian Sociological Association’s (TASA) Thematic Group on Work, Labour and Economy, for their comments on a previous version of this paper, especially Helen Forbes-Mewett, Ben Spies-Butcher and Claire Parfitt.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Australian Research Council [Grant DE170100735].