Abstract

Credit unions, nonprofit mutual associations also called financial cooperatives, have a lengthy history. The World Council of Credit Unions reports that credit unions are found in 101 countries representing 56,000 credit unions, more than 200 million members, and $1.7 trillion in assets. This study, following earlier research in Canada that found that credit unions are more prevalent in rural communities and small towns relative to the general population and to banks, examines credit union and bank branches in three U.S. states (Arizona, New Hampshire, and Wisconsin). We find that credit union branches are strongly represented in sizable urban communities, and are more likely to be located in low-income zip code areas than banks. The data show not only evidence of a credit union niche market but also a tension between social and economic objectives, and that credit unions accommodate themselves to profit norms, what we refer to as market accommodation.

Introduction

Informal savings and lending associations have been around for centuries. Members make contributions to a pool, and this accumulation of wealth is distributed in the form of loans as members have need (MacPherson, 1999). A more formalized version of this phenomenon are credit unions, member-based associations originating in Germany in the mid-19th century, at that time to provide financial services to rural populations and to urban artisans and masters (Aschhoff, 1982; MacPherson, 2012; Prinz, 2002). The credit union model spread quickly to other parts of Europe, including to Austria, Italy, Belgium, the Netherlands, and France. By the beginning of the 20th century, it had also spread internationally to Canada and the United States (MacPherson, 1999).

In many countries throughout the world, variations of the credit union model have been created. These include cooperative banks found in Europe and many other countries. Cooperative banks are variations of the basic credit union structure that also serve a membership, but like banks in general they serve a broader clientele, may have ownership arrangements that involve external equity investors, and may participate in capital markets in ways that credit unions are not allowed to. The European Association of Co-operative Banks (2013) represents 4,000 banks, 56 million members, and 215 million customers. Internationally, the most celebrated example of a type of cooperative bank is the Grameen Bank of Bangladesh, the members of whom are the borrowers, much as in a credit union. Grameen and its founder Muhammad Yunus were awarded the Nobel Peace Prize in 2006.

While not the mainstream of modern finance, credit unions clearly have a significant role, their members being a substantial part of the population around the world in many developed countries (e.g., Ireland, 73%; United states, 45%; Canada, 43%; Australia, 30%) and in many developing countries (St. Vincent and the Grenadines, 86%; St. Lucia, 75%; Barbados, 72%; Belize, 70%; World Council of Credit Unions [WOCCU], 2012). The WOCCU, a global trade association for credit unions and financial cooperatives, reports that credit unions can be found in 101 countries, representing 56,000 credit unions, more than 200 million members, and $1.7 trillion in assets (WOCCU, 2012). Together, these credit unions have $1.3 trillion of savings and shares, $1.1 trillion of loans, and $161 hundred billion of reserves.

The Credit Union Social Mission

Although credit unions have economic significance, they were associations born of a social mission to provide credit or loans to people who could not access them from other financial institutions and to provide them at affordable interest rates (MacPherson, 1999). While this mission may not seem of great significance among developed countries in the modern world, in the 19th century when credit unions were founded, the availability of credit at affordable rates of interest was an important accomplishment and remains an important feature in many parts of the world. Indeed, credit unions typically offer higher interest rates on savings accounts, lower interest rates on loans, and lower fees as compared with banks (Deller & Sundaram-Stukel, 2012).

Unlike financial institutions owned by shareholders, credit unions either are nonprofit organizations, as in the United States, or operate in the spirit of nonprofit organizations, as is the norm internationally. Their surplus or positive net income at year end is utilized to improve services, reduce the cost of services, or to give rebates to members in the form of dividends. Unlike dividends in a capitalist corporation that are rewards to shareholders for their investment, credit union dividends are based on patronage or use of the service (McKillop & Wilson, 2011; U.S. Department of the Treasury, 1997).

As nonprofit corporations, credit unions have an ownership arrangement that differs from other financial institutions. The members own the credit union, not as individuals, but in common, and as such the credit union is beholden to its members. This is distinct from most other forms of financial institutions that have to answer to their shareholders. Members of a credit union have one vote each at the annual general meeting that elects the board of directors, normally from among the members, and members may participate in committees that form the governance of the organization.

In spite of their distinct structure, questions have been raised about whether credit unions fulfill a social mission that is distinct from banks, particularly as credit unions have grown in scale into larger corporations and may be losing their connection to the communities that founded them and that originally required their service. Since 1970, many federally registered credit unions in the United States have been certified as low-income or community development credit unions (U.S. Department of the Treasury, 1997). However, some research questions whether U.S. credit unions better serve lower income communities than other financial institutions (McKillop & Wilson, 2011; White, 2011). Also, research in the United Kingdom suggests that larger credit unions operating in relatively affluent areas (“wards”) are more successful than those that are smaller and operating in economically less affluent areas (Ward & McKillop, 2005). That study is of particular interest because its unit of analysis was the ward or the area that the credit union served, not simply individual income.

Our study adds to this literature by examining the prevalence of credit union and bank branches in rural and urban communities, and in areas of low, medium, and high median household income (MHI). The context of the study is the United States, which has arguably the strongest credit union sector in the world (WOCCU, 2012).

U.S. Credit Unions

The first U.S. credit union–—St. Mary’s Cooperative Credit Association—was founded in 1909 in the St. Mary’s parish in Manchester, New Hampshire (Pierce, 2011) by Alphonse and Dormène Desjardins, who were the founders of Canada’s credit union movement in 1900 (MacPherson, 1979, 2012). Shortly after that, Massachusetts became the first state to enact credit union legislation. Today, credit unions can be chartered federally or by the state. 1

In 2012, more than 100 years later, there were 7,070 credit unions with 95.7 million members (about 45% of the population 18 years and over; Credit Union National Association [CUNA], 2012b). Although credit unions are by no means the mainstream of the U.S. financial market, their share should not be trivialized. Their total assets are just more than $1 trillion, about 6.7% of the U.S. financial market, and their total deposits are $877.7 billion (CUNA, 2012b).

U.S. credit unions have undergone major changes over the past 50 years. Supported by consolidation, they have become larger, with more members and more assets per credit union. As evidence of this consolidation, there were 21,050 credit unions registered in 1962 (Clarke, 1963), nearly triple the 2012 figure of 7,070 (CUNA, 2012b). However, this growing consolidation has been offset by an increased number of branches and, more recently, electronic banking. Fifty years ago, credit unions had 13.8 million members or 7.5% of the population, about one quarter of 2012. Their assets 50 years ago were only $7.2 billion (approximately $54 billion in 2012 dollars) compared with excess of $1 trillion in 2012.

Previous Research

Mook, Hann, and Quarter (2012) also looked at credit unions in relation to where people live in Canada. That study found that credit unions (referred to as caisses populaires in francophone Canada) have greater representation compared with the population in rural communities and small towns, and are underrepresented in major urban centers. This was true of every Canadian province, but most so in Quebec and Saskatchewan, which interestingly have the strongest credit union sectors in Canada. A comparison with bank branches in Quebec and Atlantic Canada found that the number of bank branches was disproportionately greater in urban centers.

The data from the Canadian study can be interpreted in different ways. First, they may indicate that credit unions are more likely than banks to be located in small, rural communities that are in need of their services. In that regard, credit unions can be viewed as serving an important social mission. Second, the data could be viewed as indicating that credit unions are hesitant to enter into Canada’s markets in major urban centers or are doing so more slowly than banks, as might be suggested by market-failure theory (Ben-Ner, 1986; Hansmann, 1980; Weisbrod, 1974, 1977). Overall, market failure did not seem a compelling explanation because while credit unions had greater representation relative to the population and in relation to bank branches in rural areas and small towns, there was even greater evidence of credit unions consolidating rural and small town branches–in other words, doing what banks were engaged in, but at a slower pace. As mutual associations with a member-based board, credit unions may find it more challenging than banks to close branches in rural communities and small towns and to expand into more populated centers.

Put differently, the democratic structure of credit unions gives their clients a vote and voice in the decisions that are taken. Banks may survey their clients to determine what services are needed, but unlike credit unions, the clients of banks do not have the right to a voice and vote in decision-making, unless they are shareholders. The credit union board, which consists of elected representatives from the community that the credit union serves, would be expected to have an interest in retaining the credit union’s services in the local community and this may create a different dynamic than for bank branches, which are primarily beholden to their shareholders and in obtaining financial returns that enhance share value.

However, it is important to not overstate this point of difference between credit unions and bank branches; it is a difference in degree rather than an extreme categorical distinction. Even though credit unions are member-based, like many nonprofit mutual associations they tend to suffer from a weak self-perpetuating board and an inactive membership, and can be driven by management decisions (Chaddad & Cook, 2004; Cornforth, 2002; Spear, 2004; Wilcox, 2006). In the case of credit union performance, a primary concern for management is building deposits and financial returns; board members, while sharing those concerns, represent their members who want to retain high quality services in their local community. This point is borne out in a study of Irish credit unions (Byrne, McCarthy, Ward, & McMurtry, 2012). There may be a confluence on those objectives for many credit unions, but in the case of branches in very small communities, these objectives may conflict with each other.

Related to this point, the financial structure of credit unions, which relies upon earnings from transactions with members rather than equity investments by shareholders, may reduce the potential for access to sources of capital that could be used for greater expansion into urban markets. Put simply, in business terms, credit unions may pay a price for their financial structure and for being democratic associations.

Research Questions

The extent to which credit unions continue to maintain the same level of service in rural and small town America can be viewed as one measure of social mission. The United States population, like that of other developed economies, is heavily urban, and has become increasingly so over the past century. Currently, only 19.3% of U.S. residents are classified as rural, a decrease from 60.4% at the beginning of the 20th century (U.S. Census Bureau, 1995, 2012). For this study, we want to know whether credit union branches are responding to this changing demographic pattern, whether their representation in rural and urban communities differs from bank branches, and if so, why. We also want to know whether credit unions are serving lower income communities more than banks, as evidence of their social mission.

This study thus poses two questions:

Method

Three states were selected for study: Arizona, New Hampshire, and Wisconsin. They were chosen partly for practical reasons to make the work manageable and partly because of their distinct contexts. All three states have a strong credit union presence: In Arizona, state-incorporated credit unions claim a 50.8% market share of assets relative to other state financial institutions; the comparable figures for New Hampshire and Wisconsin are 35.3% and 19.7% (CUNA, 2012a). In addition, Arizona is the one of the most urbanized states in the United States; New Hampshire is relatively rural, and as mentioned, was the first state to have a credit union; and Wisconsin has a strong agricultural cooperative sector, and in many respects is similar to Western Canada. Of the three states, we expected that the Wisconsin data would conform most to the Canadian pattern.

There is one U.S. study (Deller & Sundaram-Stukel, 2012) whose findings relate closely to ours. Their research, for the entire United States, shows that credit unions operate in areas of low concentration of banks, in other words, they serve distinct geographic communities. A fundamental difference between their study and ours is that Deller and Sundaram-Stukel utilize the head office as their unit of analysis. Our research utilizes the branch, both for credit unions and for banks. We feel that the branch is the most appropriate unit for analysis, because as noted above, credit unions have consolidated into larger units over the years, but through branches they have continued to service many communities in which a head office is not located.

The first step of the study was to compile a database of credit unions and banks and their branches for each of the three states in the study. This information was obtained from the National Credit Union Administration (NCUA, 2012) 5300 Call Report Quarterly Data to December 31, 2011, Federal Deposit Insurance Corporation (FDIC, 2012) institution database, and the U.S. Census Bureau (2011).

Once this step was completed, we mapped the credit union branch locations by the population size of the community in which they were located, using a combination of information drawn from the U.S. Census and Google Maps. We classified community size as follows: less than 10,000; 10,000 to less than 100,000; 100,000 to less than 1,000,000; and 1,000,000 and above. We also classified the data by zip code and coded each zip code area according to its level of MHI as a percentage of county MHI.

Results

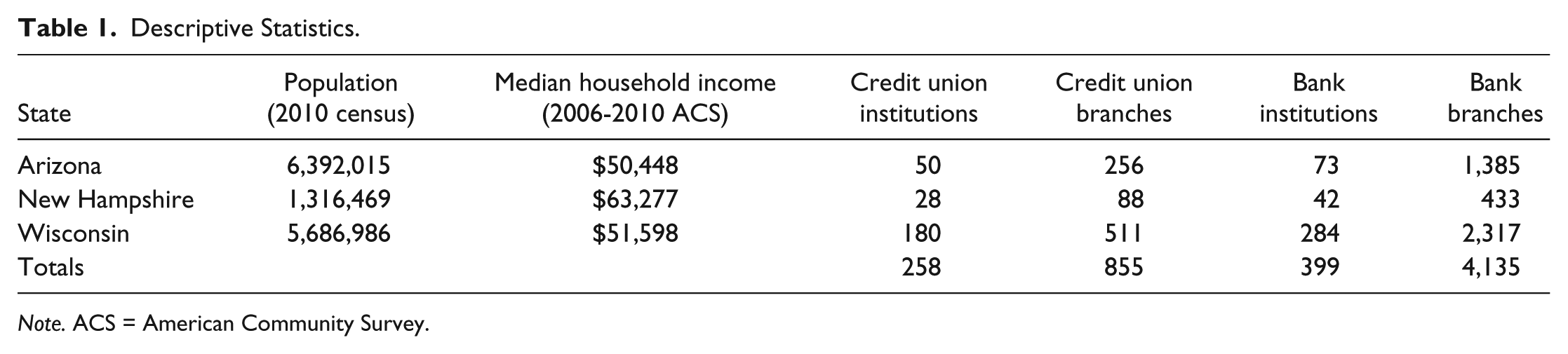

Table 1 provides basic descriptive data of the three states that were studied. Arizona has 50 credit unions and 256 branches, and its median income is $50,558. New Hampshire is a relatively small state, with a very high median income ($63,277), and with 28 credit unions and 88 branches. Wisconsin has a middle range median income ($51,598) with 258 credit unions and 855 branches. The MHI for the United States overall is $51,914 (U.S. Census Bureau American Community Survey, 2012).

Descriptive Statistics.

Note. ACS = American Community Survey.

Distribution of Branches by Community Size

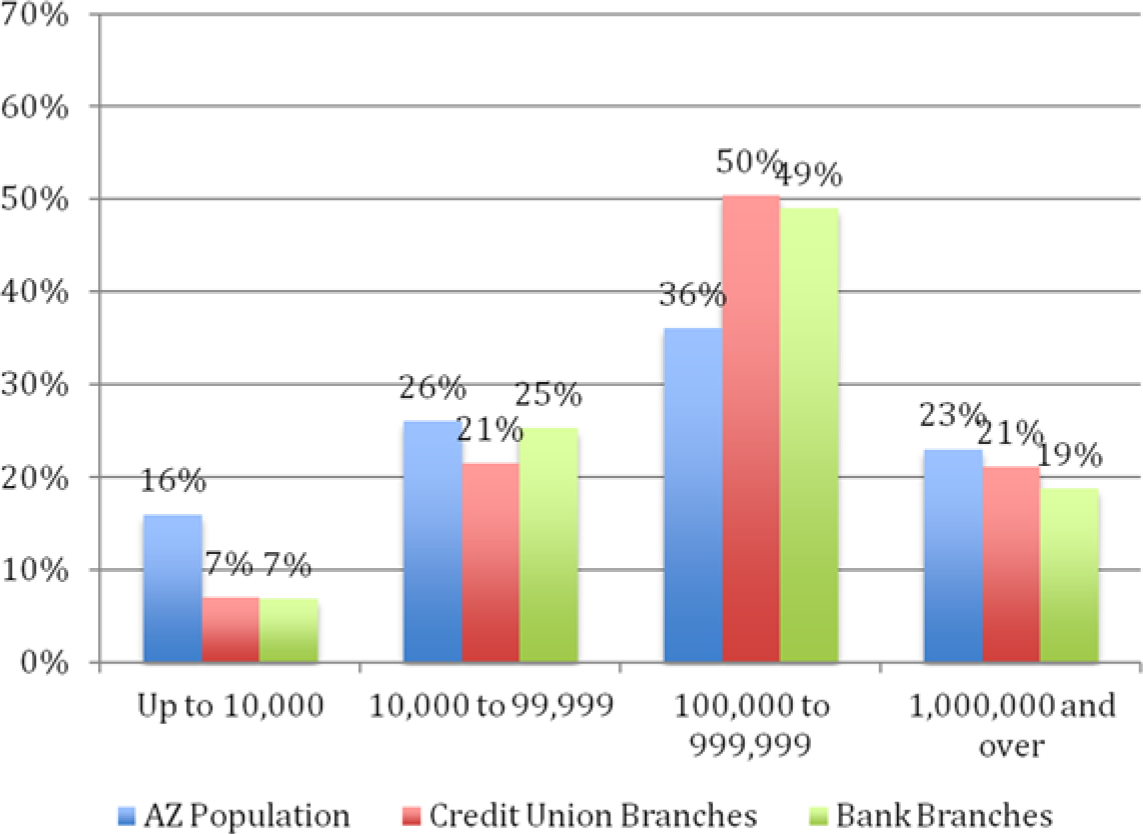

Figure 1 shows the data for Arizona. Credit unions and banks both have less representation in rural communities as compared with their population, and overall there is a similarity in the patterns. When tested statistically using a Pearson chi-square, there were no significant differences between credit union branches and bank branches in relation to the size of the community in which they were located.

Arizona credit unions and banks in relation to community size.

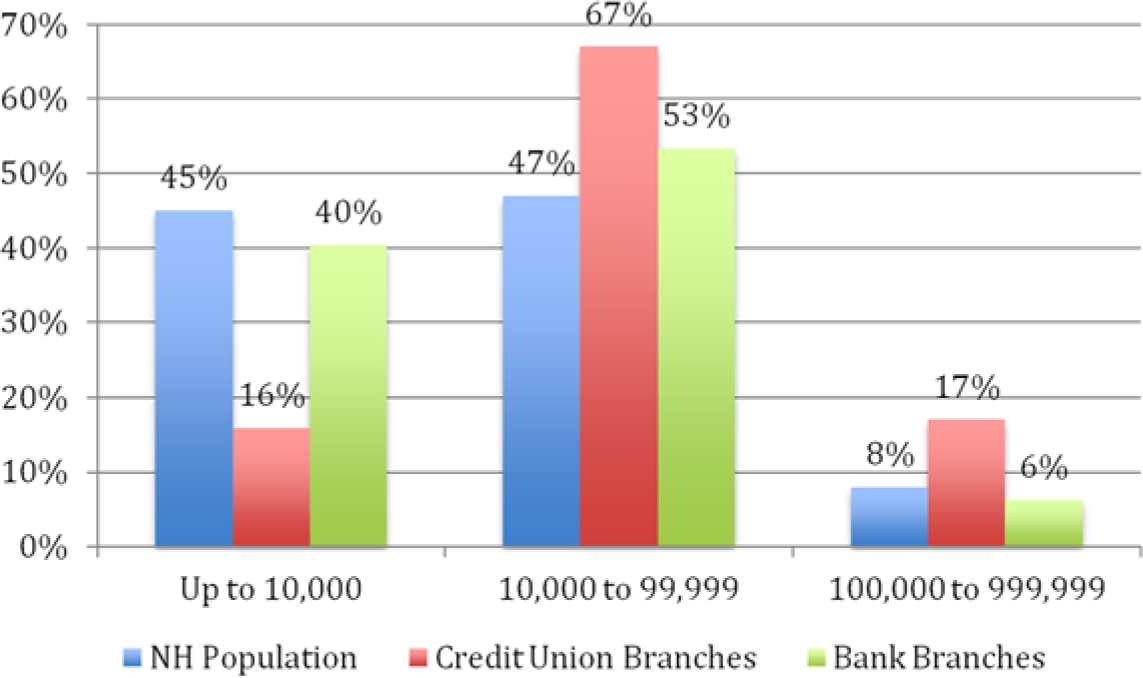

The data for New Hampshire are presented in Figure 2. There was a statistically significant difference in the distribution of credit union branches and bank branches (Pearson’s chi-square < .001). The data show that credit unions have less representation in smaller communities, which predominate in this state, and greater representation in Manchester, the one city with a population of at least 100,000. Interestingly, banks’ locations are more consistent with the population distribution in New Hampshire.

New Hampshire credit unions and banks in relation to community size.

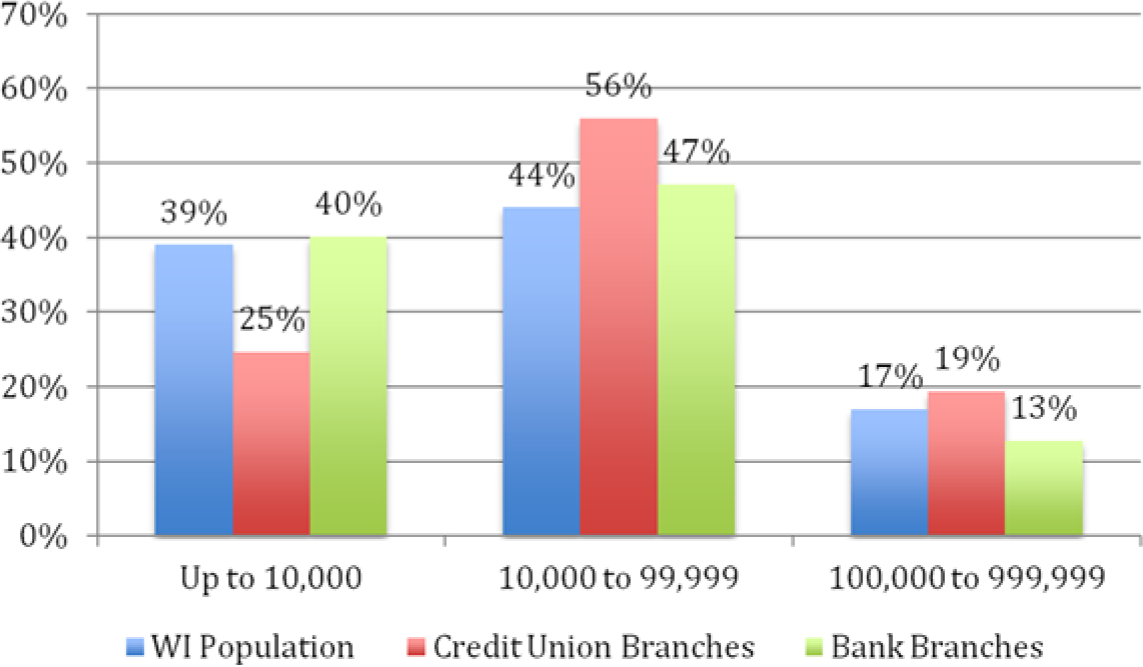

For Wisconsin, there was also a statistically significant difference in the distribution of credit union branches and bank branches (Pearson’s chi-square < .001). Credit union branches again have less representation in rural communities compared with both bank branches and population, and a greater representation in middle-sized communities (10,000 to less than 100,000) and larger communities (more than 100,000). Bank branches correspond to the population distribution of communities (Figure 3).

Wisconsin credit unions and banks in relation to community size.

We also looked at the number of zip code areas in the three states without any banks or credit unions, those with credit union branches only, those with bank branches only, and those with both credit union and bank branches. As can be seen in Table 2, there are very few zip codes with only credit union branches: 2 of 402 in Arizona, 2 of 246 in New Hampshire, and 11 of 771 in Wisconsin. Thus, from this analysis, credit unions are not serving areas not served by banks.

Distribution of Branches by Zip Code.

Distribution of Branches by MHI of Zip Code

To look at whether or not credit unions had greater representation in low-income areas than banks, we analyzed the branch data by zip code. The MHI of each zip code area was coded as a percentage of the county MHI, and then categorized as low, medium, or high. The low category included zip codes with a MHI up to 80% of the county MHI. The medium category included zip codes of 80% to less than 120% of the county MHI, and the high category included those zip codes with a MHI of 120% and higher of county MHI.

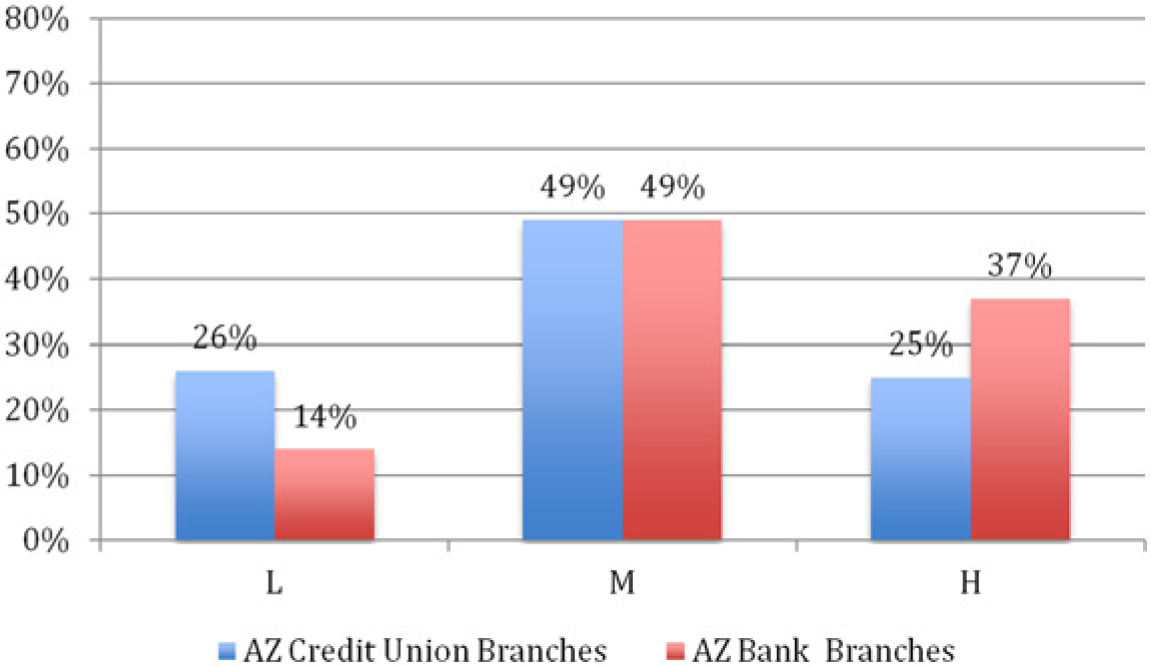

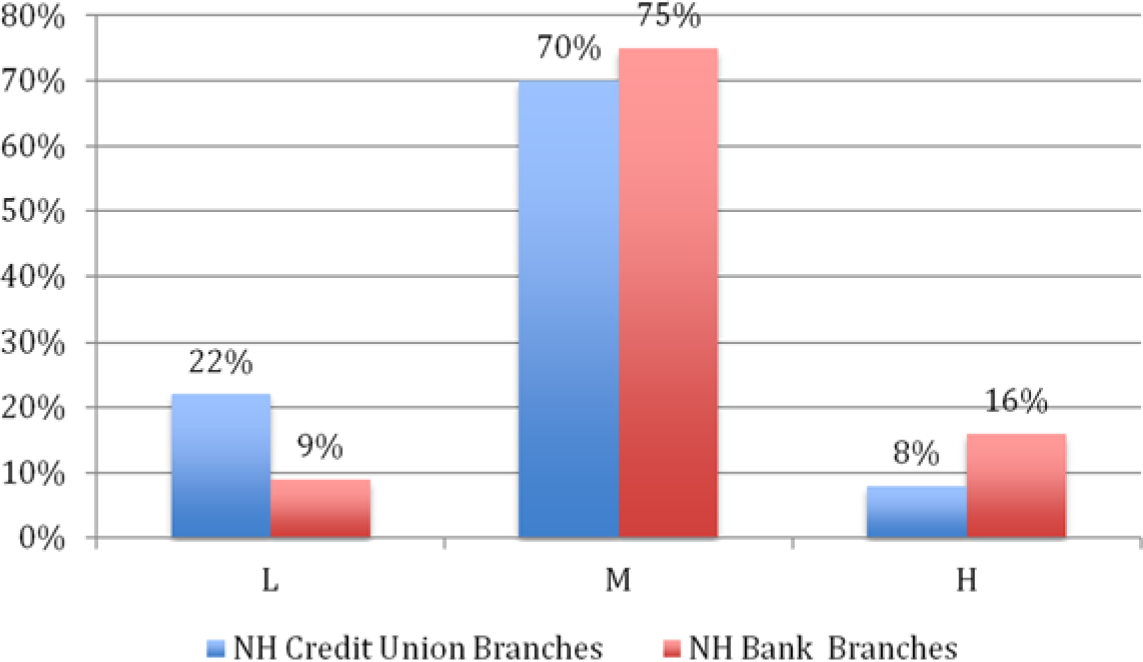

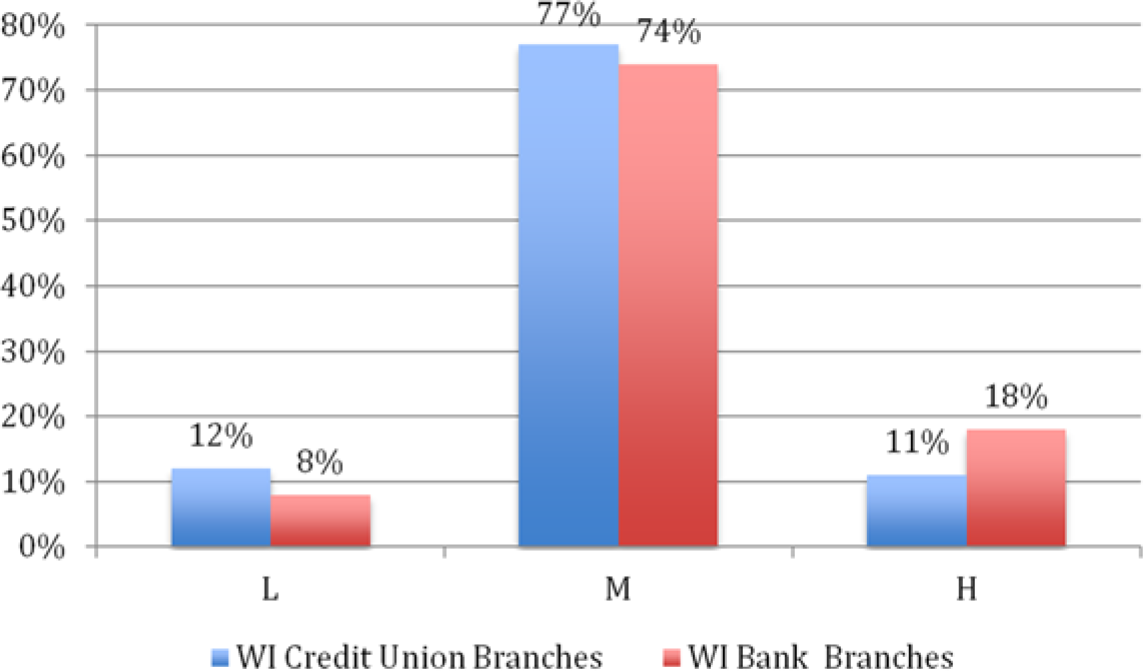

In all three states, as shown in Figures 4 to 6, credit union branches were significantly more likely to be located in low-income areas than bank branches, and bank branches were significantly more likely to locate in high-income areas than credit union branches (Pearson’s chi-square statistics for Arizona, New Hampshire, and Wisconsin, respectively, were p < .001, p < .01, and p < .001).

Arizona credit unions and banks in relation to zip code median household income as a percentage of county median household income.

New Hampshire credit unions and banks in relation to zip code median household income as a percentage of county median household income.

Wisconsin credit unions and banks in relation to zip code median household income as a percentage of county median household income.

Discussion

In the “Introduction” to this article, we asked two research questions:

The response to our first research question indicates that relative to banks, credit union branches are strongly represented in sizable urban communities. Part of the explanation for these data is that 80% of U.S. credit unions have an occupational bond of association (Deller & Sundaram-Stukel, 2012), often through manufacturing companies, which were more likely to be located in larger cities. This pattern differs from Canada where credit unions were pioneered primarily in rural and smaller communities, areas in which there were established farm-marketing and retail cooperatives. Of the three states that we studied, we expected that Wisconsin might be similar to the pattern in Canada and have a strong credit union presence in rural areas, as Wisconsin has a strong agricultural sector with many similarities to Saskatchewan and other Western provinces. However, there was no evidence to support that hypothesis, suggesting that the presence of a strong agricultural sector may not be a factor in whether credit unions are retained in rural communities.

Another way of looking at the urban/rural data is to determine whether credit unions serve geographic communities not serviced by banks. The data show that credit union branches are predominantly in the same geographic communities, broadly speaking, serviced by banks, and very few credit union branches are located elsewhere. This finding differs from that of Deller and Sundaram-Stukel (2012) who found that credit unions were spatially distinct from banks. However, that study used the head office as its unit of analysis; our study used the branch, which we would argue is the more appropriate unit of analysis. Another difference between the two studies is that Deller and Sundaram-Stukel used the entire United States, whereas our study used only three states. It is possible that if we used the entire United States our findings would differ, but we note that for the three states in our study there is no evidence of a distinct credit union spatial location.

Our second question asks, Do credit union branches have greater representation in low-income areas than banks? Our data show that there is strong evidence that credit unions serve low-income communities more so than banks. Even though a subset of banks are regulated to serve low-income areas through the federal Community Reinvestment Act of 1977, credit unions as a whole appear to be proportionately more represented in low-income communities than banks as a whole in the three states under study. This finding may appear inconsistent with the finding discussed above, which indicates that credit unions are not geographically distinct from banks in their location. However, the two findings are not at odds with each other. Put differently, our data suggest that credit unions and banks cluster in relation to population concentrations, but within that broad area, credit unions are more likely to situate themselves within lower incomes areas than bank branches. The difference between the two is one of degree.

These data are consistent with the intended public purpose of credit unions, outlined in the Federal Credit Union Act (FCUA) of 1934, intending federal credit unions “to make more available to people of small means credit for provident purposes through a national system of cooperative credit” (FCUA, 1934/2011, 3). This may be of contention, as some researchers have questioned whether credit unions have served this function in the United States (McKillop & Wilson, 2011; White, 2011). In raising this question, those researchers refer to the average income of credit union members. Our data refer to the average income of the community in which credit unions are located and show that credit unions do serve lower income communities. It is also possible that they serve the higher income members of those communities. This matter requires greater investigation. However, even if credit union members tend to be above-average income earners in lower income communities, it could be argued that there is a benefit to the overall community through the services offered by the credit union.

Interpreting the Data

a. Market Niche

The evidence that credit union branches are more likely to serve low-income communities than banks could be interpreted in different ways within the context of a capitalist market. These data, it could be argued, portray a form of niche market. It appears that credit unions in the United States are offering a similar mix of services as banks. In some areas, there are restrictions, or caps, to member business loans, which restrict product or service offerings. For example, the Federal Credit Union Act, applicable for federally insured credit unions, states that “no insured credit union may make any member business loan that would result in a total amount of such loans outstanding at that credit union at any one time equal to more than the lesser of— (1) 1.75 times the actual net worth of the credit union; or (2) 1.75 times the minimum net worth required under section 216(c)(1)(A) for a credit union to be well capitalized” (FCUA, 1934/2011, 12). Nevertheless, the types of products and services between credit unions and banks are similar. Thus, the market niche seems to be in relation to the customer base, rather than the types of products and services offered. Traditionally, the customer base or community served by a credit union was defined around an occupational bond of association, but to a greater extent credit unions have been allowed to define their bond around a geographic community, much like a bank.

One way that credit unions define their market niche is through branding themselves as distinct from other financial institutions, or what is often labeled as the “credit union difference” (Ketilson & Brown, 2011). This branding manifests itself in different ways including being a local financial institution that is owned in common by its members. Another distinct feature of credit union branding is their nonprofit and mutual or cooperative structure, meaning that the users of the service are members and that each member has one vote at the annual general meeting and in electing representatives to the board of directors. One consequence of a credit union’s cooperative structure is that the organization does not have access to “secondary capital” (i.e., capital not obtained from their member deposits and interest payments on loans). In general, external investors want voting rights associated with their shares and a portion of the profits commensurate with their investment. This poses a problem for credit unions, as they are based upon the principle that voting rights are accorded to membership, not capital, and utilizing their positive net income to enhance services and for rebates to members proportionate to their use of the service.

b. Market Accommodation

Credit unions not only have attempted to establish a market niche, but they have also accommodated themselves to the capitalist market to be competitive. They are part of a subclass of nonprofit organizations that operate in the market and compete with private-sector businesses (Quarter, Sousa, Richmond, & Carmichael, 2001). We refer to this group as social-economy businesses (Quarter, Mook, & Armstrong, 2009), and it includes some forms of cooperatives and social purpose businesses such as Benefit Corporations. Our research suggests that even though organizations of this sort have distinct features, they may accommodate themselves to the market and engage in whatever activities are feasible to ensure that they are financially viable. We label this phenomenon as Market Accommodation, one manifestation of which is the consolidation of credit unions from smaller to larger units and to situate themselves in relation to population size in communities. Not simply in the United States but also internationally, credit unions have been consolidated into larger units in part to be more competitive and address the cost of government regulations and in part to satisfy the demands for more products and services from their members (McKillop & Wilson, 2011). This structural change has strengthened them (Ward & McKillop, 2005), but it has also reduced the credit union difference. Another manifestation of market accommodation is breaking down the limits associated with a narrow bond of association and effectively lobbying the U.S. Congress to modify the legislation to serve a broader market.

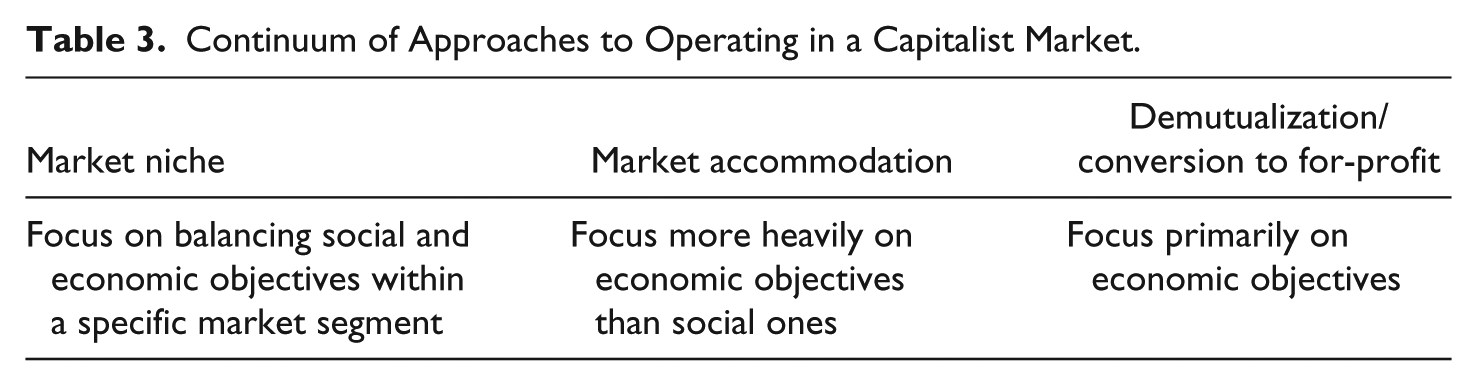

If market niche and market accommodation are set on a continuum, then demutualization (conversion into a bank) could be viewed as the next step (Table 3). This phenomenon–conversion into a bank–involved only 27 U.S. credit unions in a study by Wilcox (2006), but nevertheless it is noteworthy. Unlike market accommodation, where the organization retains its credit union structure, demutualization results in the termination of the credit union and its conversion into a different organizational structure. For the credit union and other forms of mutual associations, decisions to merge or to demutualize are submitted to a vote of the membership, one member/one vote. The membership may be uninvolved and often professional management has a major influence on these decisions.

Continuum of Approaches to Operating in a Capitalist Market.

For our study, the behavior of credit unions may best be explained by a combination of Market Niche and Market Accommodation. These approaches pertain not only to credit unions but also to all forms of social-economy businesses, that is, nonprofits, cooperatives, and social enterprises attempting to navigate the business market while sustaining social objectives that differ from the norms of conventional business corporations.

Unlike nonprofits in general, social-economy businesses operate in the market, competing with private-sector firms. They require managers who know how businesses operate, and they have to engage in the practices of businesses in general, while integrating the organization’s social goals. Trying to understand the circumstances under which social-economy businesses are able to successfully manage the tension between their social and economic bottom lines and under which they conform to conventional business practices is a worthwhile research endeavor.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Social Sciences and Humanities Research Council of Canada [grant number 833-2009-1000].