Abstract

Charities in the United Kingdom have been the subject of intense media, political, and public scrutiny in recent times; however, our understanding of the nature, extent, and determinants of charity misconduct is weak. Drawing upon a novel administrative dataset of 25,611 charities for the period 2006-2014 in Scotland, we develop models to predict two dimensions of charity misconduct: regulatory investigation and subsequent action. There have been 2,109 regulatory investigations of 1,566 Scottish charities over the study period, of which 31% resulted in regulatory action being taken. Complaints from members of the public are most likely to trigger an investigation, whereas the most common concerns relate to general governance and misappropriation of assets. Our multivariate analysis reveals a disconnect between the types of charities that are suspected of misconduct and those that are subject to subsequent regulatory action.

Keywords

Introduction

Charities in the United Kingdom have been the subject of intense media, political, and public scrutiny in recent times (Public Administration and Constitutional Affairs Committee, 2016; Office of the Scottish Charity Regulator [OSCR], 2016). Public confidence and trust in the sector has been questioned in light of various “scandals” including unethical fundraising practices (resulting in the establishment of a new fundraising regulator for England and Wales in 2016), high levels of chief executive pay, politically motivated lobbying and advocacy work, and poor financial management. This last issue has gained traction among politicians and the media as a result of the demise of Kids Company, a prominent London-based charity that provided practical, emotional, and educational support to vulnerable children. It ceased operations in August 2015 amid accusations of, among other concerns, inadequate and improper financial conduct. Fraud in the U.K. charity sector is estimated to cost around £1.9 billion per year, with payroll and procurement fraud accounting for the vast majority of this figure (PKF Littlejohn, 2016). It was two cases of charity financial misconduct—at Moonbeams and Breast Cancer Research—that acted as the germinator for the establishment of a dedicated Scottish charity regulator (Lambert, 2011). Prior to OSCR, the Scottish charitable sector was very lightly regulated by the U.K. Inland Revenue, and there was significant support from the sector itself for clearer statutory regulation (Dunn, 2016). Cases and concerns such as these call into question the adequacy of charity monitoring and regulation, and their role in protecting and enhancing public confidence in the sector (Cordery, 2013; Krashinsky, 2003).

To date, there has been little academic research on the nature, extent, and determinants of regulatory investigations into alleged and actual charity misconduct; this is partly due to the difficulties in accessing and processing the administrative data necessary to study this outcome, as well as the relative infancy of charity regulatory regimes. Examining this topic allows researchers to “peer under the hood” of the sector, shining a light on aspects of charity behavior that are often overlooked. Research in this area has the potential to improve the evidence base on charity misconduct and accountability, improve regulatory practice through the targeting of resources at serious incidences of misbehavior, and dispel misperceptions around the conduct of these organizations (by providing context for media reports, for example). This article represents the first systematic U.K. study of charity misconduct. Although there is considerable variation in the level and type of monitoring, charity regulators internationally would benefit from a clearer understanding of the risks inherent in their sectors and the degree of action necessary to mitigate these issues. Using novel data supplied by the OSCR, our research describes the nature and extent of alleged and actual misconduct by Scottish charities, and asks what organizational and financial factors are associated with this outcome? We show that the factors which predict complaints about charities are not necessarily good predictors of the need for regulatory action. Our results support the move of charity regulators to a “risk-led” approach to regulation where a wide range of factors inform decisions about where limited resources should be focused in regulating the sector.

The article is structured as follows. First, we describe charity regulation in Scotland, and in particular, the misconduct monitoring program. This is followed by a review of the literatures on charity failure and fraud from where we derive suitable explanatory variables. We outline the data and methods before presenting our empirical results. The article concludes with a discussion of the theoretical and practical implications of the study.

Investigating Charity Misconduct

The Scottish Charity Register is maintained by the OSCR, which was established in 2003 as an Executive Agency and took up its full powers when the Charities and Trustee Investment (Scotland) Act 2005 came into force in April 2006. In Scotland, a charity is defined (under statute) as an organization that is listed on the Register after demonstrating that it passes the charity test: it must have only charitable purposes, the organization must or intend to provide some form of public benefit, it must not allow its assets to be used for noncharitable purposes, it cannot be governed or directed by government ministers, and it cannot be a political party (OSCR, n.d.). 1 One of OSCR’s main responsibilities is to identify and investigate apparent misconduct and protect charity assets. It operationalizes this duty by opening an investigation (what they term an inquiry) into the actions of a charity suspected of misconduct and other misdemeanors.

Investigations are mainly initiated as a result of a public complaint but they can also be opened by a referral from a department in OSCR or another regulator. For example, one of the founders of the charity The Kiltwalk reported the organization to OSCR (2015) on the grounds that he has concerns over the amount of funds raised by the organization that are spent on meeting the needs of beneficiaries. OSCR can only deal with concerns that relate to charity law—such as damage to charitable assets or beneficiaries, misconduct, or misrepresentation—although it can refer cases to other bodies such as when criminal activity is suspected. Upon receipt of a concern, the regulator will consider the following: whether it has a legal power to act; whether there is a risk to charitable assets, to beneficiaries, to the abuse of charitable status, and to the charity sector as a whole; whether the concern should be dealt with by another regulator or body; and the anticipated level of action required (OSCR, 2014). Finally, the outcome is recorded for each investigation. Outcomes are varied and often specific to each investigation but most can be related to three common categories: no action taken or necessary, advice given, and regulatory intervention.

Literature

The study of misconduct is part of the broader field of nonprofit failure and success. Mellahi and Wilkinson (2004) identified two leading schools of thought in the study of organizational success and failure: deterministic and voluntaristic. Population ecology theory is deterministic and focuses on organizational density, size, and age as affecting the life chances of organizations, as well as a suite of environmental factors (such as regulation and the state of the economy). All of these factors are considered outside the control of the organization. In contrast, the voluntaristic perspective sees “good strategic choices as the keys to organizational success. Particular emphasis is placed on organizational structure, the role and composition of the board, and how problems are perceived and solved” (Mellahi & Wilkinson, 2004, p. 268).

The study of charity misconduct has tended to focus on instances of occupational fraud, of which there are two major types: fraud conducted against the organization (e.g., misappropriation of cash by an employee) and fraud conducted by the organization such as the deliberate misreporting of financial performance (Greenlee, Fischer, Gordon, & Keating, 2007). Previous research has focused on the nature of fraud in the U.S. nonprofit sector, the organizations subject to fraud, and perpetrators of the said action (Archambeault, Webber, & Greenlee, 2015). Bradley (2015) conjectured that occupational fraud damages the organization subjected to it (through significant financial loss, reduced income from donations, and potential fines), intended beneficiaries (through the diversion of funds away from services), and the reputation of the nonprofits (loss of public confidence). It is posited that the nonprofit sector is particularly sensitive to the negative effects of fraud, especially asset misappropriation, as these organizations often lack sufficient controls for detecting and dealing with this issue (Archambeault et al., 2015). Douglas and Mills (2000) proposed five reasons why this might be the case: an atmosphere of trust surrounding the nonprofit, the difficulty in controlling certain revenue streams (e.g., cash donations), a lack of financial resources necessary to implement sufficient internal controls, a lack of business expertize in the organization, and the reliance on volunteer boards. Marks and Ugo (2012) corroborated these assertions and also theorized that the type of nonprofit is a relevant factor: For example, they argued that grant-making organizations might be more susceptible to financial fraud than commercial nonprofits due to the higher risk of misappropriation. Empirical research by Greenlee et al. (2007) and Holtfreter (2008) tentatively substantiated the conjectures of Douglas and Mills, finding some evidence of financial misconduct in the U.S. nonprofit sector. Krishnan, Yetman, and Yetman (2006) examined the financial statements of U.S. nonprofits and discovered that some of these organizations (38 of 101) reported an average of US$7 million less fundraising on their annual return than on their audited financial statements.

However, there are some significant limitations to previous studies. Research on nonprofit success and failure has mainly focused on the most economically important subsectors: In a review of the literature, Helmig, Ingerfurth, and Pinz (2014) found that the first four International Classification of Nonprofit Organizations (ICNPO) groups (Health, Culture and Recreation, Social Services, and Education and Research) accounted for the majority of studies in this field (102 of 147 reviewed articles). 2 With respect to misconduct, the scope of the topic has been narrowly defined, with an understandable yet limited focus on occupational fraud and its relation to financial losses. Many of these previous studies have been hampered by small sample sizes, necessitating exploratory work over descriptive and explanatory analyses (Archambeault et al., 2015). Consequently, much of this exploratory work has focused on nonprofit subsectors such as Human and Health Services (e.g., Gibelman & Gelman, 2001). Researchers have also struggled to acquire suitable data, with many studies relying on unrepresentative self-completion surveys conducted by third parties or analyses of print media reports of nonprofit fraud (see Fremont-Smith & Kosaras, 2003; Gibelman & Gelman, 2001; Greenlee et al., 2007). Finally, extant research is U.S. centric, with little academic focus on other geographies or charity sectors (Clifford & Mohan, 2016).

The availability of comprehensive regulatory data in other jurisdictions, such as Scotland, allows researchers to address important questions that are not currently possible with U.S. data. Contributing to the literature on charity misconduct, we address three research questions:

In answering these questions, we derive measures from studies of nonprofit success and failure that employed a population ecology perspective. The liability of newness hypothesis posits that recently founded organizations “are inexperienced, lack the resources to ensure resilience in times of crisis, and have not yet mustered sufficient external support” (Wollebaek, 2009, p. 269). Also, smaller charities are hypothesized as being more likely to fail, possibly due to difficulties in sourcing funding, volunteers, and staff (Barron, West, & Hannan, 1994; Bielefeld, 1994). The next section describes the operationalization of our variables in more detail.

Method

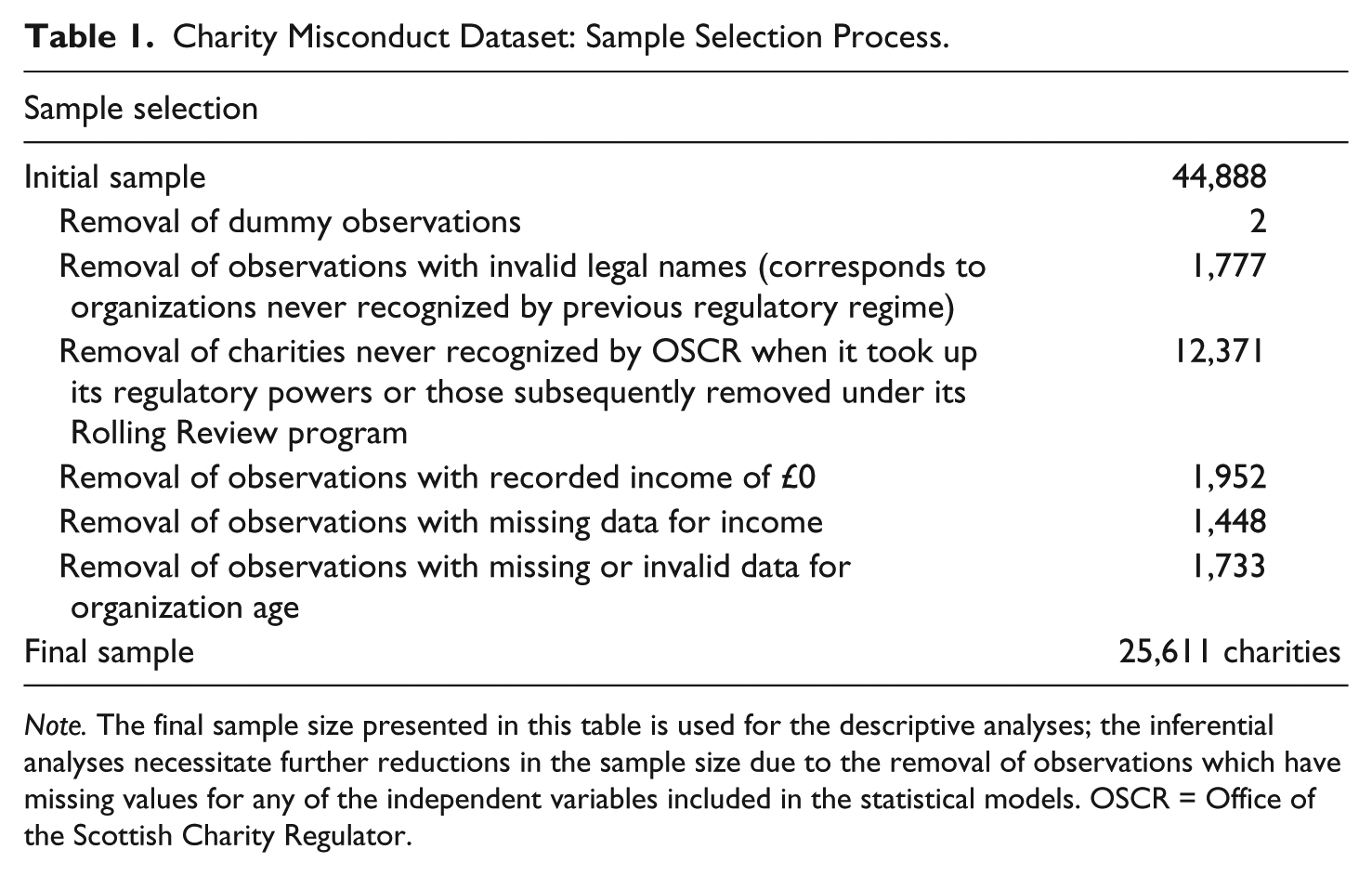

This study examines two dimensions of charity misconduct that deserve greater attention: regulatory investigation and subsequent action. Regulatory action can take the following two broad forms: the provision of advice (e.g., recommending a charity improves its financial controls to counteract the threat of fraud or misappropriation) and the use of OSCR’s formal regulatory powers (e.g., reporting the charity to prosecutors or suspending trustees). This study overcomes many of the limitations outlined previously by utilizing a novel administrative dataset, derived from OSCR, covering the complete population (current and historical) of registered Scottish charities. It is constructed from three sources: the Scottish Charity Register, which is the official, public record of all charities that have operated in Scotland; annual returns, which are used to populate many of the fields on the Register (e.g., annual gross income); and internal OSCR departmental data relating to misconduct investigations. Once linked using each observation’s Scottish Charity Number, this dataset contains 25,611 observations over the period 2006-2014. Table 1 summarizes the steps in the sample selection process.

Charity Misconduct Dataset: Sample Selection Process.

Note. The final sample size presented in this table is used for the descriptive analyses; the inferential analyses necessitate further reductions in the sample size due to the removal of observations which have missing values for any of the independent variables included in the statistical models. OSCR = Office of the Scottish Charity Regulator.

Dependent and Independent Variables

The outcome of being investigated by the regulator is measured using a dichotomous variable that has the value 1 if a charity has been investigated and 0 if not. The other two dependent variables are also dichotomous: Regulatory action takes the value 1 if a charity has had regulatory action taken against it and 0 if not, and intervention takes the value 1 if a charity is subject to regulatory intervention and 0 if not (i.e., it received advice instead). The dependent variables are modeled using binary logistic regression. Drawing on the reviewed literature, five independent and three control variables are operationalized in this study. For two, the literature suggests clear hypotheses for their effects. Size is a categorical measure of a charity’s most recent annual gross income; the literature supports a hypothesis that increasing size decreases the risk of failure. Age is the natural logarithm of the number of years an organization has existed; in line with previous studies, we posit a negative relationship between age and risk (Freeman, Caroll & Hannan, 1983; Hager, Galaskiewicz, Bielefeld, & Pins, 1996). In contrast, for three of our independent variables, the literature does not predict a clear direction of effect. Grant is a binary indicator of whether a charity only disburses grants to other organizations rather than carrying out charitable activities itself or a combination of functions; we hypothesize that grant-making organizations differ in their activities and behavior compared with other charities, and thus their risk exposure is distinct. Parent is a binary indicator of whether a charity has a parent organization (e.g., parish churches that are part of the Church of Scotland); greater oversight may reduce risk or it may increase the chance of reporting misconduct to the regulator. Complaint is a categorical variable that captures the actor that raised a concern with OSCR; we assume that some stakeholders will be better placed to identify misconduct than others.3,4 The three control variables are as follows: Field is a nominal categorical measure of a charity’s ICNPO category (see Mohan & Barnard, 2013, for how these categories were assigned), Geography is a nominal categorical measure of a charity’s geographical scope of operations, and Form is a nominal categorical measure of an organization’s constitutional form (e.g., limited company). Although these variables measure core characteristics of charities, the literature does not suggest a theoretical or empirical basis for the direction of association with the outcomes.

Results

The sample contains demographic, financial, and investigations data on 25,611 charities. Of these, 20,053 are listed as Active on the Scottish Charity Register, with 4,246 having been removed and the remainder either not subject to further monitoring by OSCR or are nonsubmitting charities (i.e., they have failed to submit their annual return on time or at all). The vast majority of organizations are defined as Standard charities (96%)—the remainder is Cross Border charities or Registered Social Landlords. The mean and median charity has £856,803 and £12,251 in annual gross income, respectively; the mean and median age in the sample is 24 years and 16 years. The three most common constitutional forms for Scottish charities are unincorporated associations (55%), companies (20%), and trusts (18%). Also, 18% of charities have a parent organization whereas 33% disburse grants to individuals and organizations. Finally, there is a wide distribution of ICNPO classifications in the sector though there are more populous categories such as social services (31%), religion (16%), culture and recreation (15%), and development and housing (11%).

Describing Investigations and Regulatory Action

There have been 2,109 regulatory investigations of 1,566 Scottish charities over the study period: This represents 6% of the total number of organizations active during this period. The number of investigations increased steadily during OSCR’s early years and then plateaued at around 400 per year until 2013/2014, when the figure has declined slightly. The majority of investigations (78%) concerned charities that were only investigated once in their history. A little more than 30% of investigations resulted in regulatory action being taken against a charity: 16% received advice and 13% experienced intervention by OSCR. There is no association between the number of times a charity has been investigated and whether regulatory action has been taken against it (Cramér’s V = .08, p < .001): Even in cases where an organization has been investigated 5, 6, or 7 times, regulatory action is uncommon. This peculiarity is perhaps accounted for both by the small number of charities that are investigated multiple times and the spurious or unfounded nature of the complaints made against these organizations.

For the 1,400 observations for which there are data, it is a member of the public that is most likely to contact OSCR with a concern about a charity (Table 2). Internal stakeholders of the charity account for 31% of all investigation initiators, though this disregards the strong possibility that many of those recorded as anonymous are involved in the running of the charity they have a concern about.

Actors That Trigger Regulatory Investigations.

Note. Percentages rounded to the nearest whole number.

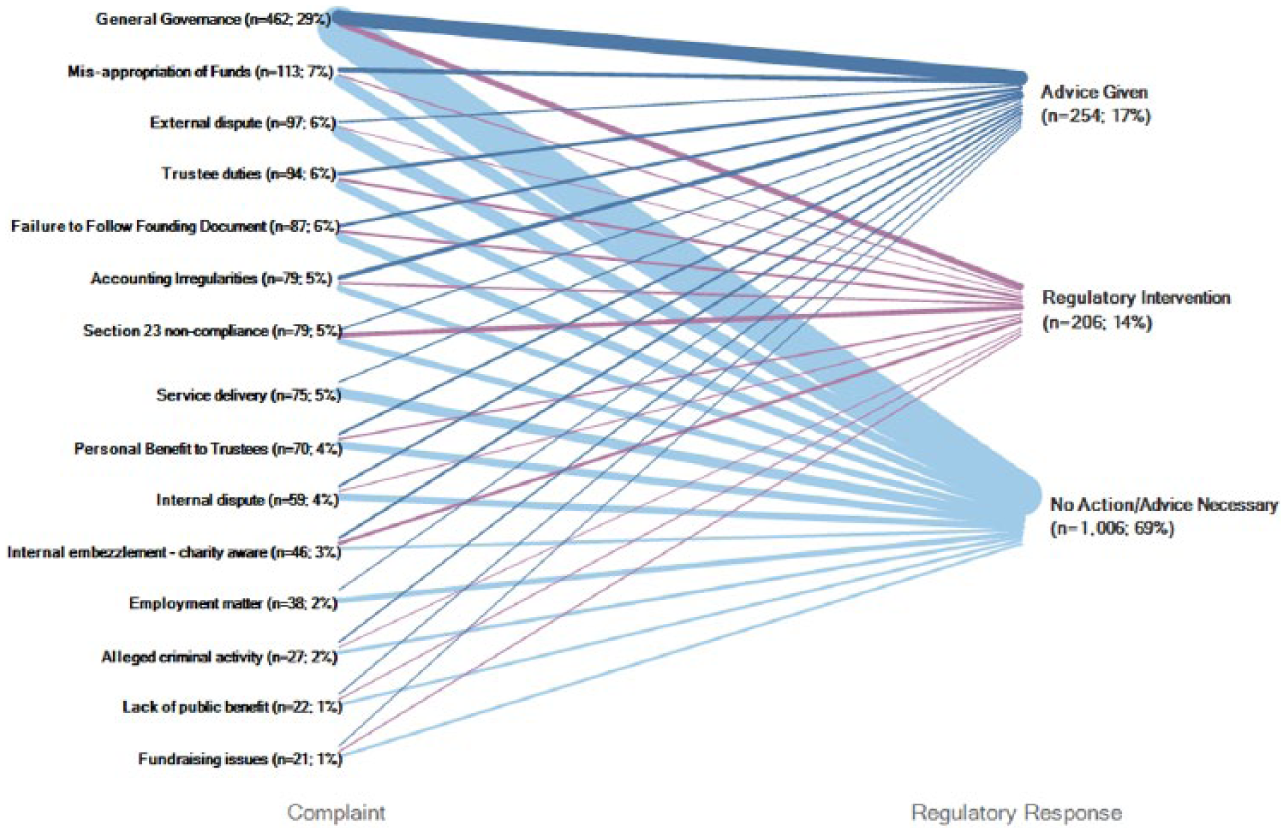

The concerns that prompt these actors to raise a complaint with OSCR are numerous and diverse. Figure 1 below visualizes the associations between the most common types of complaint and the response of the regulator. The overriding concern is general governance, as well as associated issues such as the duties of trustees and adherence to the founding document. Financial misconduct also ranks highly, particularly the misappropriation of funds and suspicion of financial irregularity. There is a moderate association between the actor making the complaint and the underlying concerns (Cramer’s V = .227, p < .001). Compared with average, trustees were less likely to report concerns about general governance, external disputes, and the misappropriation of funds, for example. We can see that most complaints do not result in any action, but General Governance, Trustee Duties, Section 23 noncompliance, and Embezzlement are most likely to lead to regulatory intervention. Concerns regarding the misappropriation of funds and accounting irregularities are most likely to result in the provision of advice by the regulator.

Association between type of complaint and regulator response.

Modeling the Risk of Investigation and Action

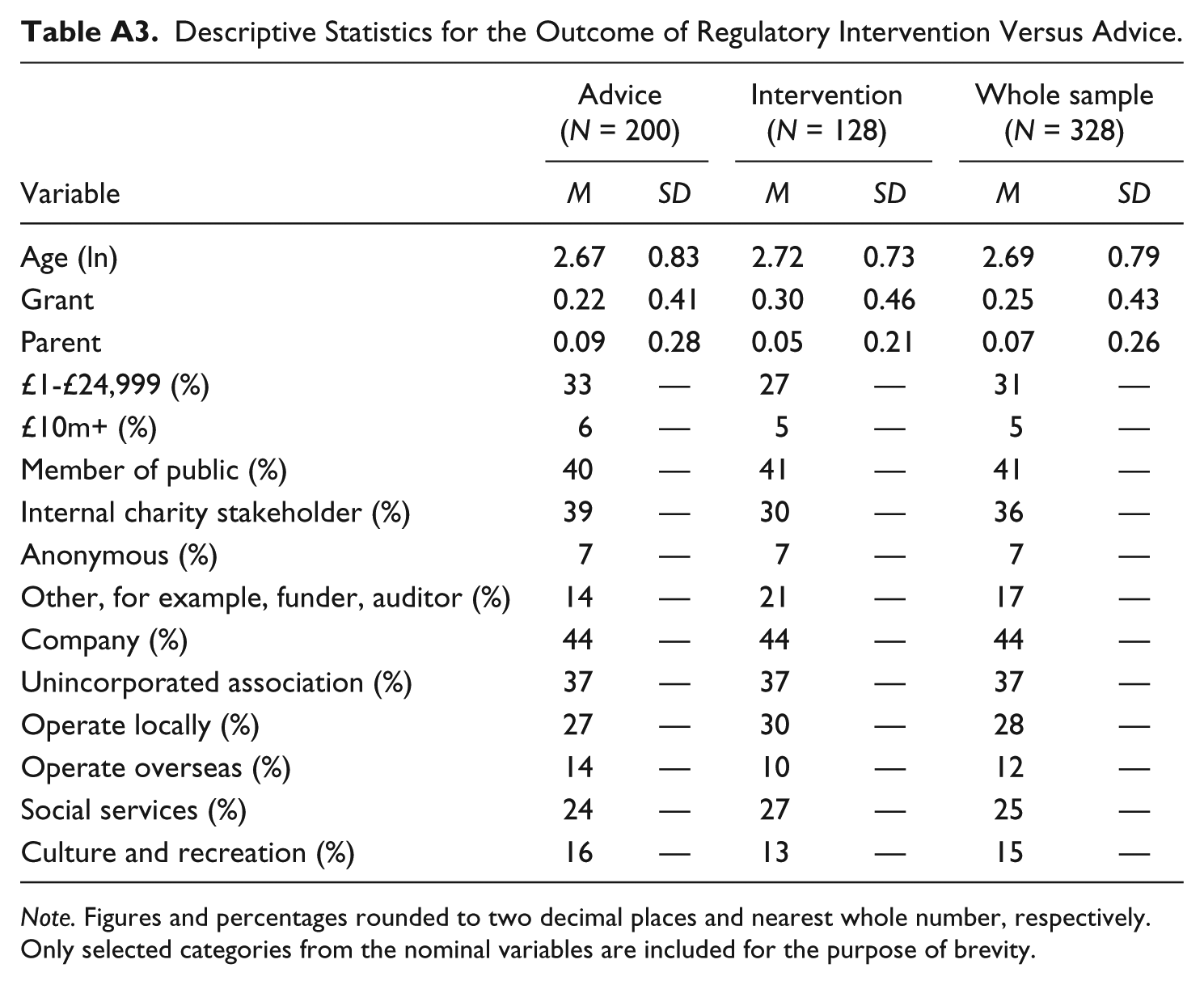

Before discussing the results of the multivariate analysis, Tables A1, A2, and A3 in the appendix contain descriptive statistics for the independent variables included in the statistical models. The typical investigated charity appears to be slightly younger, less likely to discharge grants, and has a parent organization, bigger, more likely to be a company, and considerably less likely to just operate at a local level. The typical charity subject to regulatory action appears to be slightly smaller and younger, less likely to have been subject to a complaint by a member of the public, and more likely to just operate at a local level. In contrast to those that received advice from the regulator, the typical charity that experienced intervention appears to be slightly older and smaller, more likely to have been subject to a complaint by an auditor, regulator, or funder, and less likely by an internal charity stakeholder. 5

We model the probability of investigation using binary logistic regression as a function of organization size, age, institutional form, field of operations, and geographical base. For the subsample of organizations that were investigated, we then model the probability of regulatory action, and its different forms, being taken based on the same characteristics plus the source of the complaint made. 6 In Table 3, we report the odds ratios (exponentiated coefficients) rather than the log odds as they approximate the relative risk of each outcome occurring. This is appropriate not only for ease of interpretation but also because the absolute chance of either outcome occurring is low (i.e., it is better to know which charities are more likely relative to their peers). The category with the most observations is chosen as the base category for each nominal independent variable.

Results of Logistic Regression on Dependent Variables.

Note. Figures rounded to two decimal places. Constant is omitted. Controls: Field, Form, and Geography. OR = odds ratio.

Models the probability of an organization being investigated.

Given an investigation, models the probability of the regulator taking any form of action.

Given regulatory action, models the probability of intervention, as opposed to advice.

p < .05. **p < .01. ***p < .001.

We first examine the effects of organization age and size on the outcomes. The coefficient for age varies across the three outcomes. A one-unit increase in the log of age results in a 5% decrease in the odds of being investigated or being subject to regulatory action; however, the odds of experiencing intervention compared with receiving advice are higher for older charities. There appears to be a clear income gradient present in the investigation model: As organization size increases so do the odds of being investigated compared with the reference category. A more nuanced examination of the effect of organization size is possible by comparing categories of this variable with each other and not just the base category (shown in Figure 2). Drawing on suggestions by Firth (2003), Firth and Menezes (2004), and Gayle and Lambert (2007), we employ quasi-variance statistics to ascertain whether categories of organization size were significantly different from each other. Unsurprisingly, the largest charities have significantly higher odds than their smaller counterparts; however, it appears that medium sized charities (those with income between £100,000 and £1 million) are not significantly different from each other and neither are organizations between £500,000 and £10 million.

Quasi-variance log odds of being investigated.

Although size is the strongest predictor of complaints, the effect of size on the likelihood of regulatory action occurring is reversed: Complaints about larger charities are less likely to lead to any sort of regulatory action. For being subject to regulatory intervention, the income gradient is less apparent, though there is some evidence that larger charities have higher odds than the smallest category.

The odds of experiencing each outcome are lower for charities that discharge grants (with the exception of intervention) or have a parent organization. With regard to the actor that initiates an investigation, it appears that stakeholders with a monitoring role (e.g., funders, auditors, or other regulators) are more likely than members of the public to report concerns that warrant some form of regulatory action; in contrast, internal charity stakeholders such as employees and volunteers have higher odds of identifying concerns that merit the provision of advice by OSCR and lower odds of triggering regulatory intervention in their charity. Although size predicts complaints, it is the source of the complaint that is a more reliable predictor of the need for regulators to take action.

Sensitivity Analyses

With regard to being investigated, we run separate regressions for charities registered in different eras (pre and post 2006) to control for the period at risk: That is, there may be an initial period where charities are not likely to be investigated as they have just been registered and not very identifiable or visible. The direction of the effect of our two main independent variables—age and size—is similar to the main regression: For both cohorts, younger, larger charities have statistically significantly higher odds of being investigated. We also explore the effect of different functional forms of organization size, leaving the other variables unchanged: A one-unit increase in the log of annual gross income results in a significant increase in the odds of being investigated and a decrease in the odds of being subject to regulatory action. Finally, an interaction term between size and age was included in the model-building process. The correlation between age and being investigated is stronger for larger charities, though the interaction overall was not statistically significant and thus was not included in the final models.

Discussion

This study has investigated the nature, extent, and risk factors of organizational misconduct in the Scottish charity sector. In an era of enhanced scrutiny of their activities and impact, we argue it is more important than ever to understand which charities trigger complaints about their conduct, the concerns and organizations that merit regulatory action, and what form this takes. This research contributes to the nascent charity misconduct literature, and the wider study of accountability in the sector, in a number of important ways. First, by describing the nature and extent of perceived and actual misconduct, we provide the first systematic, comprehensive description of this phenomenon, producing an evidence base of use to the field, policymakers, and practitioners. The distribution of risk and regulatory responses constitutes an informative account of misconduct in the charity sector, one that complements analyses based on alternative sources of data (e.g., Archambeault et al., 2015; Gibelman & Gelman, 2001). Second, we highlight factors associated with charity investigation and misconduct, showing the mismatch between those predicting complaints and those predicting regulatory action. This has considerable implications for charity regulators seeking to deploy their limited resources effectively and in a way that ultimately protects and enhances public confidence. As Fremont-Smith (2004) noted in her comprehensive account of charity governance, charity regulators (particularly in the United States) often lack the funds to carry out their enforcement activities properly and, thus, would benefit from analyses that help them target their resources more efficiently.

There is an element of predictability to the types of charities that are suspected of misconduct. The most prominent and consistent risk factor is the size of the organization: As size increases, the likelihood of being investigated increases sharply, even when controlling for other organizational characteristics. The largest charities are significantly more likely to be investigated compared with all other sizes. However, it is not yet clear that size is a causal or explanatory factor in being investigated; it more plausibly acts as a proxy for the “true” explanatory factor. This is supported by the disparity in the effect of organization size between the likelihood of being investigated and the likelihood of that investigation leading to regulatory action. Size is strongly predictive of complaints, but those complaints are no more likely to lead to regulatory action in large charities than small ones. The source of the complaint is a much stronger predictor of direct regulatory intervention than the organizational characteristics which predict the original complaint. The triggering of an investigation could be perhaps best understood as a function of two other concepts: visibility and high stakes. Larger charities are more likely on average to deliver services to a greater number of beneficiaries, operate across a greater number of geographies, interact with the public on a greater scale (e.g., through fundraising campaigns), and involve more staff and volunteers than smaller organizations (de Andrés-Alonso, Garcia-Rodriguez, & Romero-Merino, 2015; Luoma & Goodstein, 1999). As a result, they can be highly visible to many of the actors that initiate investigations. The degree to which actors perceive there is great deal at stake, in terms of the risk to charitable assets and beneficiaries, may also prompt complaints. Larger charities are often responsible for more valuable assets and services compared with their smaller counterparts, and this may spur an actor to report a complaint, with little regard to the substance of the concern. It is more difficult to theorize about the explanatory factors of actual misconduct occurring, mainly due to the absence of appropriate measures in the data. However, two plausible dimensions to the phenomenon on the organizational side are opportunity and controls. The degree to which charities feel that there is an opportunity to conduct itself in a way that is not compliant with public expectations and regulatory requirements may be a powerful predictor of misconduct. Finally, the strength of governance and financial controls may reveal which charities are hosts for employee, and by extension, organizational misconduct. These dimensions have received some attention in the nonprofit occupational fraud literature (e.g., Rothschild, 2013).

There are a number of limitations to this research that must be acknowledged. Organization size and age traditionally function as control variables in many studies and are good examples of the kinds of measures inherent in administrative data. These datasets tend to contain coarser or proxy measures of social science concepts compared with the richness of social surveys (Wallgren & Wallgren, 2007), and as such, there are characteristics which may be important in measuring risk that are not captured in the administrative data. Finally, the investigations data utilized in this study should not be considered as a complete record of dissatisfaction and misconduct in the sector. Many actors may be unwilling to raise their concerns with the regulator: For example, they may be unaware of to whom the complaint should be directed to or fearful of repercussions should they lodge their complaint (see Hogg, 2016). Rothschild’s (2013) study of misconduct reporting in the charity sector posited that whistle-blowers observe misconduct several times before reporting this behavior; the same study also found that whistle-blowers were subject to retaliation by the organization in a majority of cases. On the organizational side, some charities may be particularly adept at masking their misconduct from those able and willing to raise concerns. Therefore, the findings of this study should be considered in the context of other data sources covering this topic such as media investigations and parliamentary inquiries.

Despite these limitations, the results of this analysis have considerable practical applications for stakeholders in the sector, particularly regulators, and those with a monitoring function. Our findings support a risk-led approach to regulation, where a range of factors are used to make decisions about targeting regulatory action. OSCR aims to discharge its regulatory function in a progressive, proportionate, and preventive manner, and the efficient and effective targeting of its resources is critical in achieving this. Utilizing the predicted probabilities generated by the models to assign risk categories to charities and investigations could guide the allocation of scarce resources and achieve Cordery, Sim, and van Zijl’s (2015) call for a differentiated approach to charity regulation. Implementing such an approach requires regulators to be cognizant of the disconnect between complaints and misconduct. Our analysis shows that regulators face significant challenges in separating the “signal” (complaints about charities engaged in serious misconduct) from the “noise” (complaints outside the remit of the regulator, or not leading to regulatory action). Discontent at all levels can have an impact on trust in the sector (see Sargeant & Lee, 2002), and so the answer is not simply to try to reduce complaints. Rather, better guidance for charities on handling complaints within their own governance structures could reduce the number of unresolved issues that make it to the regulator. Just as important is increasing the “signal,” making sure that stakeholders with serious concerns about misconduct are able and willing to make complaints to the regulator. To this end, our analysis highlights the importance of good relations between regulators and stakeholders such as funders or auditors who tend to make complaints that do require regulatory action.

Conclusion

Reflecting on the discussion above, there are a number of fruitful avenues for research in this area. Regulatory data relating to investigations is generated on a continuous basis, providing the foundation for longitudinal analysis of complaints and misconduct; this type of data would be amenable to studying the duration to the first investigation and between subsequent occurrences for example. Furthermore, work could be done to understand the antecedents and outcomes resulting from investigations, particularly from the perspective of the charities and the actors that raise concerns. For example, Rothschild’s (2013) findings suggested that the frequency of observed misconduct, the democratic tendencies of management, and the alignment of values between the organization and whistle-blower should all be considered when seeking to understand the drivers of complaints about charity conduct. Although not incorporated into this study, it could be possible to access detailed qualitative data on the content of the advice provided by OSCR and any response to this contact by the charity. With regard to the posited explanatory factors (visibility and high stakes), additional data could be sought to test their effect; for example, annual U.K. charity brand surveys are available for purchase and OSCR possess detailed financial information for a subset of larger charities in Scotland. Finally, the dependent variables in this study could be utilized as explanatory factors in a wider study of charity accountability internationally. By combining investigations data with concerns raised by charities themselves (collected by OSCR since April 2016) and matters of material significance reported by independent examiners and auditors, there is the potential to conduct a multidimensional examination of misconduct and accountability in the sector.

By revealing the disconnect between the level of complaints and concerns that require regulatory action, we argue there is much work to do for practitioners in the sector with regard to charity reputation and stakeholder communication. Charity boards are ultimately responsible for the governance of their organization, and must ensure that adequate policies and procedures are in place. This includes reducing the risk of misconduct occurring, taking corrective action in response to guidance from the regulator, and developing the management and reporting functions required to deal with the consequences. Regulators and charity sector infrastructure bodies should consider developing guidance for charities of all sizes on how to cultivate and manage their reputations and communications with stakeholders. Recognition should also be given to the role that stakeholders such as funders and auditors must play in self-regulation of the sector, given their proximity to charities through their day-to-day activities. It is no longer sufficient (if indeed it ever was) to rely on charity status to convey trust and inspire confidence in the conduct of an organization.

Footnotes

Appendix

Descriptive Statistics for the Outcome of Regulatory Intervention Versus Advice.

| Variable | Advice (N = 200) |

Intervention (N = 128) |

Whole sample (N = 328) |

|||

|---|---|---|---|---|---|---|

| M | SD | M | SD | M | SD | |

| Age (ln) | 2.67 | 0.83 | 2.72 | 0.73 | 2.69 | 0.79 |

| Grant | 0.22 | 0.41 | 0.30 | 0.46 | 0.25 | 0.43 |

| Parent | 0.09 | 0.28 | 0.05 | 0.21 | 0.07 | 0.26 |

| £1-£24,999 (%) | 33 | — | 27 | — | 31 | — |

| £10m+ (%) | 6 | — | 5 | — | 5 | — |

| Member of public (%) | 40 | — | 41 | — | 41 | — |

| Internal charity stakeholder (%) | 39 | — | 30 | — | 36 | — |

| Anonymous (%) | 7 | — | 7 | — | 7 | — |

| Other, for example, funder, auditor (%) | 14 | — | 21 | — | 17 | — |

| Company (%) | 44 | — | 44 | — | 44 | — |

| Unincorporated association (%) | 37 | — | 37 | — | 37 | — |

| Operate locally (%) | 27 | — | 30 | — | 28 | — |

| Operate overseas (%) | 14 | — | 10 | — | 12 | — |

| Social services (%) | 24 | — | 27 | — | 25 | — |

| Culture and recreation (%) | 16 | — | 13 | — | 15 | — |

Note. Figures and percentages rounded to two decimal places and nearest whole number, respectively. Only selected categories from the nominal variables are included for the purpose of brevity.

Acknowledgements

The authors would like to thank the Economic and Social Research Council (ESRC) and the Office of the Scottish Charity Regulator (OSCR) for their generous financial support of the research through a collaborative PhD studentship. In particular, credit is due to Louise Meikleham and Judith Turbyne at OSCR for their substantial cooperation and feedback, and the anonymous reviewers for their insightful and constructive comments.

Authors’ Note

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.