Abstract

Crowdfunding platforms have become a valid alternative for raising funds for both entrepreneurial and humanitarian projects. The aim of our study is to investigate the factors influencing the likelihood of funding success across these two project types. Building on the charitable giving and entrepreneurial finance literature streams, we employ the lenses of signaling theory and behavioral decision making to hypothesize how the impact of certain factors varies contingent on the nature of the project, from a humanitarian plea to an entrepreneurial venture. We conduct our investigation on Kiva and find that gender bias and risk signals exhibit a stronger impact on the likelihood of funding success for entrepreneurial projects, whereas humanitarian projects are more affected by home bias. By reconciling prior inconsistencies in crowdfunding research and bringing forward new ideas, we aim to support the vigorous growth of an emergent phenomenon that is of growing social and economic importance.

Introduction

Crowdfunding is an emergent phenomenon that encompasses a variety of ways in which entrepreneurs and others in financial need can gain access to funding through online platforms by drawing on relatively small contributions from a relatively large number of individuals and circumventing standard financial intermediaries (Mollick, 2014; Larralde & Schwienbacher, 2012). Crowdfunding platforms were responsible for amassing US$34 billion in 2015, marking an exponential year-to-year growth, with the industry projected to reach an impressive US$1 trillion by 2025 (Massolution, 2015). There currently exist approximately 1,250 crowdfunding platforms worldwide, classified according to the compensation the crowd receives in exchange for their contribution, namely, warm glow feelings (donation), small gifts (reward), interest rate (lending), or share in the profits (equity; Kshetri, 2015). The phenomenon has also gained traction in the academic arena, with more than 140 papers published in top peer-reviewed management journals to date (e.g., Agrawal, Catalini, & Goldfarb, 2015; Belleflamme, Lambert, & Schwienbacher, 2014; Burtch, Ghose, & Wattal, 2014; Greenberg & Mollick, 2017; Saxton & Wang, 2014), most of which have focused on the determinants of funding success. However, despite the attention crowdfunding has received over the last few years, we still have much to understand about the phenomenon. This study focuses on the path to successful funding, and seeks to shine light on how this path might vary across heterogeneous types of projects. Our aim is to evaluate how the impact of certain success factors uncovered in prior literature may vary contingent on the nature of the project, from a humanitarian plea to an entrepreneurial venture.

We build on the published works of notable scholars who have extensively investigated the determinants of funding success across all platform types and have uncovered these determinants to be composed mainly of the characteristics of project design, including the risks entailed for lenders, the language used to describe the project and its economic versus social value, and the number of borrowers and competition among projects (e.g., Galak, Small, & Stephen, 2011; Meer, 2014; Stemler, 2013). In addition, the characteristics of the borrower have been shown to play a major role in funding success, such as gender, geography, network, and social capital (e.g., Burtch et al., 2014; Colombo, Franzoni, Rossi, & Lamastra, 2015; Greenberg & Mollick, 2017). For instance, with regard to gender, Marom, Robb, and Sade (2015) employ data from the popular rewards-based platform Kickstarter, and find that female entrepreneurs enjoy higher rates of success than do their male counterparts; in the context of lending, Ly and Mason (2012) corroborate that loans to women fund faster; and, in the context of donations, Greenberg and Mollick (2017) use social giving theory and conduct a laboratory experiment based on the premise that women are more likely to succeed at crowdfunding than men are. Building on such concrete findings from across platform types, we delve deeper into the determinants of funding success by investigating how the impact of gender and other key success factors varies contingent on the type of project. In contrast to prior studies conducted on platforms hosting homogeneous project types, we seek to investigate the effect of these success factors across heterogeneous types of projects that are found within the same platform. In particular, we are interested in comparing the results from projects of a humanitarian nature, such as rebuilding a house after a natural disaster, against projects with an entrepreneurial purpose, such as setting up a bakery. We use data from Kiva, a popular platform that hosts both entrepreneurial and humanitarian projects, and the homogeneous environment of the single platform helps our study design by eliminating any variance from platform design.

Based on a review of the charitable giving and entrepreneurial finance literatures, and by employing the lenses of signaling theory and behavioral decision making, we focus on three key determinants of success (gender, lender proximity, and perceived project risk) for which established theory provides fertile ground to hypothesize that the type of project moderates its impact on the likelihood of funding success. Our findings support the supposition that the nature of the project plays a major role for funding success, as risk, proximity and the borrower’s gender are shown to affect lenders’ funding propensity in very different ways contingent on the project being humanitarian or entrepreneurial. Through our study, we aim to advance the emerging crowdfunding literature, while also making a contribution to the nonprofit and entrepreneurial finance streams. We begin by briefly introducing our empirical setting, Kiva, and in the next sections, we proceed to develop four main hypotheses, which we test with econometric analysis; we close by discussing our results.

Kiva

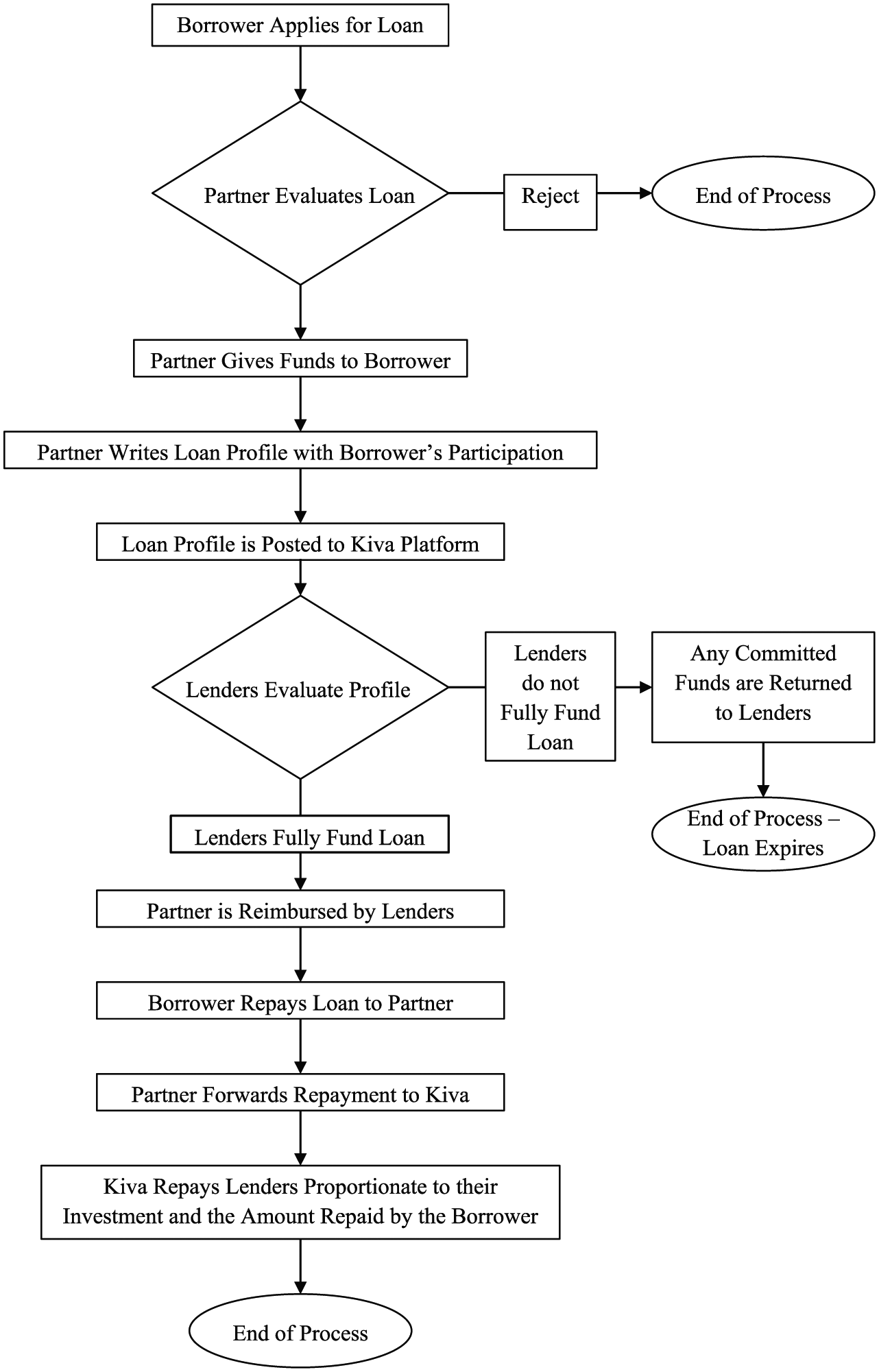

Kiva is a popular crowdfunding platform that acts as an online host for interest-free loan requests from individuals around the world. The process involves borrowers, lenders, Kiva, and their partners (Figure 1, adapted from Allison, McKenny, & Short, 2013). First, the borrower requests a loan from Kiva through one of their partners, usually a local microfinance institution that acts as an intermediary between borrowers and Kiva’s online platform. After some due diligence, the partner posts the borrower’s profile online, including information about the loan and risk characteristics. Lenders from around the world browse the different projects and decide which one to fund through a contribution of US$25 minimum. On receiving the funds, Kiva aggregates the capital and makes a transfer to the appropriate partner, who then passes on the money to the borrower. Although most partners charge borrowers an interest rate to support their ongoing operations, lenders receive zero interest on the loans.

The Kiva process.

Since its inception in 2005, Kiva has raised more than US$900 million, benefiting 2.3 million borrowers and capturing the attention of social media, financial institutions, nonprofit organizations, and scholars. Academic research sourcing Kiva data has produced an array of noteworthy results regarding the cues affecting crowdfunding success but has omitted to account for the nature of the project. In fact, due, perhaps, to this omission, the results have been mixed and, sometimes, even contradictory with regard to what drives funding success. In particular, some authors find that success is positively associated with ventures that signal an entrepreneurial orientation with dimensions of autonomy, competitive aggressiveness, and risk taking (Moss, Neubaum, & Meyskens, 2014), whereas others find that language conveying confidence, accomplishments, innovativeness, profitability, or risk taking is associated with slower funding, not faster (Allison, Davis, Short, & Webb, 2015; Allison et al., 2013). In the next section, we draw from the nonprofit and charitable giving literatures, as well as crowdfunding and entrepreneurial finance streams, to stipulate why the characteristics that drive funding success might vary between entrepreneurial and humanitarian projects. We frame these differences through the behavioral decision-making and signaling lenses, and we develop four main hypotheses.

Literature Review and Hypotheses Development

Why People Give

Past research on charitable behavior finds that the capacity and inclination of the individual to give are the two primary components of why people donate. Capacity generally refers to a person’s human and financial resources (Schlegelmilch, Diamantopoulos, & Love, 1997; Schlegelmilch, Love, & Diamantopoulos, 1997), and inclination addresses the social and psychological propensity that a person has toward giving (e.g., Bekkers, 2004; Schervish & Havens, 1997; Smith & McSweeney, 2007; Wang & Graddy, 2008). People’s giving behavior is also affected by demographic factors such as age, religious beliefs, gender, and ethnicity (e.g., Bennett, 2003; Mesch, Rooney, Steinberg, & Denton, 2006; Schervish & Havens, 1997; Shier & Handy, 2012). Another perspective on why people donate is that they expect to receive material or immaterial benefits in return for their donations, including the effect of warm glow, feelings of higher self-esteem, public recognition, or relief from guilt (Andreoni, 1989, 1990; Diamond & Kashyap, 1997; Mathur, 1996). In an overarching review of the literature on charitable giving, Bekkers and Wiepking (2011) address the question of why people donate and categorize the aforementioned factors into the eight most important mechanisms that drive charitable giving. These are the awareness of need, solicitation, costs and benefits, altruism, reputation, psychological benefits/warm glow effect, values, and efficacy. As the authors acknowledge, the Internet is a powerful tool for making people aware of those in need and for soliciting help.

In our study, Kiva activates most of these mechanisms that trigger charitable giving. The online platform connects lenders from all over the world to underprivileged borrowers, thus raising awareness of needs and soliciting action. Moreover, Kiva eliminates transaction costs by not charging fees and maintains an easy process for (re)investing that creates efficiency. Furthermore, reputation gains present as the social consequences of donations that Kiva lenders can enjoy by virtue of publicity and social networks. In addition, the joy of giving, also known as the warm glow effect, is often manifested in Kiva lenders’ testimonies as to why they participate in Kiva, alongside their belief that they are staying true to their values by contributing toward making the world a better place in an efficacious way. In fact, on taking a closer look at why people give through Kiva within this setting of charitable giving, we detect diversity in the motivations of Kiva lenders, in line with prior studies (e.g., Bajde, 2013; Galak et al., 2011). Lenders forego any interest payments, which raises the question of whether they are de facto donating or lending, or both (Galak et al., 2011). With its mission of connecting people through lending to alleviate poverty, Kiva attracts lenders who are motivated to help others in need. At the same time, however, Kiva positions itself beyond charity and embraces an entrepreneurial attitude, promoting an investor–entrepreneur rather than donor–recipient relationship (Bajde, 2013). We further analyze lender motivations by examining the reasons lenders give for participating in Kiva, in response to the statement “I loan because . . .” On conducting a content analysis of these responses, we are able to group them into the following three key themes:

Connection. Lenders stress the importance of feeling connected to a borrower in two ways. First, by providing a loan rather than a donation, lenders extend their relationship with the borrower beyond a one-off interaction to a relationship that lasts several months. Second, lenders go through a process of selecting a borrower by reading their story and seeing their photographs. This process creates a connection at a personal level that is very different from supporting an organization such as the Red Cross, where the individual receiving assistance remains unidentified.

Efficiency. Once the borrower repays the loan, the lender can use the same capital to lend to a different project by simply selecting another borrower. This uncomplicated method to continue helping highlights the efficiency of the process and casts a financial shade on the decision to lend, with lenders becoming concerned with getting their capital back and making another loan in the future. In fact, 81% of Kiva lenders are repeat lenders, averaging a respectable contribution amount of US$960 per lender.

Entrepreneurship. Many lenders feel that they are contributing toward promoting entrepreneurship in developing countries rather than merely providing economic aid. This consideration induces lenders to decide based on social and financial metrics, such as the reputation of the local partner and performance rates, to truly promote entrepreneurial activities in the region.

Following this analysis, and in line with prior studies, we propose that lending on Kiva fosters both prosocial and financial motivations on the part of lenders. Kiva lenders are not simply acting as donors, but they care about the loan being returned, because it is their way of remaining connected and efficient and of supporting entrepreneurial activity in developing countries. As a result, we expect lenders to be responsive to signals of quality, albeit to different extents depending on their inclination toward humanitarian or entrepreneurial projects.

Signals in Crowdfunding

Perhaps, the most notable characteristic of crowdfunding is the high degree of information asymmetry that exists in online transactions, because the information that borrowers have cannot be easily transferred to lenders. There exist practical difficulties such as restricted webpage space, as well as risks in publicly disclosing information about projects, that prohibit the crowd from accurately assessing the quality of a project. One way to amend this asymmetry is through the use of signals (Connelly, Certo, Ireland, & Reutzel, 2011; Spence, 1973). Signaling theory has been instrumental in combatting information asymmetry in investment decisions through borrowers credibly conveying information about their skill set and the riskiness of the project, and has proven a popular lens through which to examine investment decisions in crowdfunding (e.g., Ahlers, Cumming, Günther, & Schweizer, 2015; Lin, Prabhala, & Viswanathan, 2013; Moss et al., 2014). Notably, Lin et al. (2013) find support for the central premise of signaling theory that agents facing asymmetric information adapt by using signals to mitigate adverse selection in crowd lending, whereas Ahlers et al. (2015) study an Australian equity platform, and conclude that projects that present higher uncertainty (e.g., where financial projections are not available) have lower probability of funding success.

Signaling theory has also been employed within the empirical setting of Kiva. Allison et al. (2013) analyze the description written in Kiva’s borrower profiles, and conclude that lenders are drawn to narratives richer in language indicating blame and present concern, as projects with these features attract funding faster, whereas narratives with accomplishment rhetoric exhibit slower funding speed. Along the same lines, Allison et al. (2015) discover that profit and risk-taking language decrease the attractiveness of microloans, whereas human language increases it. Taken together, these findings suggest that Kiva lenders prefer projects with a charitable profile, projects that appeal to their prosocial motivations. However, Moss et al. (2014) find that ventures that signal an entrepreneurial orientation with dimensions of autonomy, competitive aggressiveness, and risk taking are more likely to get funded than are ventures that signal a virtuous orientation with dimensions of conscientiousness, courage, empathy, and warmth. This set of results suggests that Kiva lenders are drawn toward projects with an entrepreneurial or business orientation, seemingly contradicting the other studies. We propose that the misalignment in results might be due to the heterogeneity of the data set, because on Kiva, charitable projects coexist with entrepreneurial ideas. Consequently, the projects presented on Kiva attract lenders with varying motivations and cover all types of initiatives, from the needs of Nozimjon, a family man in Tajikistan requesting money to pay for his daughter’s medical treatment, to Maria Elena, a female entrepreneur in Bolivia seeking support to start a beauty salon. This reasoning leads to our first hypothesis:

Signaling Risk

Signaling theory has also been instrumental in assessing the risk of an investment. Both entrepreneurship and nonprofit literatures have explored the effectiveness of different risk signals on funding success. Entrepreneurship literature has underlined the influence of risk signals, such as the entrepreneur’s skill set and personal characteristics, prudent business planning and future performance indicators, as well as organizational and environmental influences (e.g., Ahlstrom & Bruton, 2006; Busenitz, Fiet, & Moesel, 2005; Coleman & Robb, 2009; Cumming & Johan, 2010; Hall & Hofer, 1993; MacMillan, Siegel, & Narasimha, 1986; Robb & Robinson, 2014). In crowdfunding in particular, several scholars have investigated the presence of market risks arising from information asymmetry, inherently risky businesses and novelty of regulations, calling for caution upon embarking on equity crowdfunding (e.g., Stemler, 2013). Along the same lines, some researchers have shown how risk proxies such as lower funding targets and shorter repayment durations can signal legitimacy by setting modest, achievable expectations (Frydrych, Bock, Kinder, & Koeck, 2014).

In the nonprofit arena, researchers have thoroughly investigated donations and the characteristics a nonprofit organization should possess to increase the number and volume of financing it may receive. These factors include the social issues addressed by the nonprofit organization, the sector it operates in, the efficiency of its operations, and CEO compensation (Balsam & Harris, 2014; Bowman, 2006). Moreover, these nonprofit scholars have also shown that philanthropists and charity donors are not as sensitive to risk as are venture capitalists, in that, they do not expect a monetary return but a social one (Yavas, Riecken, & Babakus, 1993). Hence, although venture capitalists spend time carefully evaluating the risks before deciding whether to invest in an idea, for charitable donors, the economic risk is not as important, because their main focus is on the social return the project can generate.

Because lending through Kiva presents a mix of charitable giving and financial decision making, we expect risk signals to have a different impact on humanitarian and entrepreneurial projects. Building on the existing literature, we posit that Kiva lenders contributing to humanitarian projects are generally less concerned with the risk associated with the loan than are lenders interested in entrepreneurial projects. Therefore, we propose that the risk of the loan has a negative effect on the probability of funding success for entrepreneurial projects and no effect for humanitarian projects. This reasoning gives rise to our second hypothesis:

Behavioral Biases in Crowdfunding

According to behavioral decision-making theory, in conjunction with rational thought processes, biases and behavioral tendencies are likely to influence the decisions of lenders. The complexity of selecting one project among many, in the presence of information and time constraints, can induce lenders to employ a heuristic to simplify decisions (Tversky & Kahneman, 1974). In doing so, a number of biases arise that may affect decisions, notably home bias and gender bias (e.g., Burtch et al., 2014; Galak et al., 2011; Lin et al., 2013). Over the last few years, academic scholars have explored the behavioral decision-making process of lenders in the context of crowdfunding, both theoretically and empirically, and have unveiled the presence of various biases in choosing which project to support. Specifically, evidence shows that lenders tend to favor borrowers who are more similar to themselves, often forgoing better alternatives that carry lower risk and higher return (Morse, 2015). In other words, lenders prefer to support others who belong to the in-group and are easier to evaluate. Such evidence comes in the form of geographical proximity between the lender and borrower (Burtch et al., 2014; Lin et al., 2013), gender (Galak et al., 2011), occupation (Galak et al., 2011), and culture (Burtch et al., 2014).

Importantly, geographical proximity between lenders and borrowers has been found to affect crowd behavior (e.g., Burtch et al., 2014; Galak et al., 2011; Lin & Viswanathan, 2016). Notably, Agrawal et al. (2015) determine that although the crowd is less affected by geographic proximity than that in traditional entrepreneurial financing, distance still plays a role in crowdfunding insofar as local investors invest early and are less responsive to decisions by other investors. Burtch et al. (2014) also find that lenders typically prefer borrowers who are socially proximate to themselves, in the sense that, they share a similar culture and are less geographically distant. Along the same lines, Lin and Viswanathan (2014) corroborate that lending-based crowdfunding platforms tend to indicate home bias, the tendency of lenders to prefer lending to projects located in the same geographical area, often forgoing better alternatives with lower risk and higher return. One explanation for this behavior is that the knowledge acquired through social proximity unearths soft information that mitigates the asymmetry of information reigning over investment decisions (Morse, 2015). Moreover, literature on charitable decision making suggests that, in general, donors are more prone to donate to victims with whom they can identify more closely (Galak et al., 2011) and with whom they have more similarities (Small & Loewenstein, 2003).

Building on these findings, we propose that Kiva lenders with charitable motivations are more inclined to lend to borrowers with whom they share more things in common, such as birthplace, culture, and customs. Thus, we expect the home bias effect to be present in the case of humanitarian projects and manifest in terms of a regional preference for North American borrowers. In our data set, Kiva lenders come from 234 countries across the world, but 90% of them come from only 10 countries, with North America leading with 65%. So, from the lenders’ point of view, the Kiva world is not truly global. By extension, as most of the Kiva lenders are from North America, we expect that, ceteris paribus, borrowers from North America enjoy a higher probability of funding success than do borrowers from the rest of the world. We also expect that lenders with an entrepreneurial orientation may be affected by home bias but to a lesser extent, as they tend to focus on less personal factors, such as profitability and risk, rather than social or geographic proximity. Consequently, we posit that personal information about the borrowers regarding their region of origin has a higher impact on the probability of funding for humanitarian projects than that for entrepreneurial projects (Hypothesis 3).

Moreover, the gender of the borrower was also shown to have an impact on lenders’ decision making in crowdfunding (e.g., Gorbatai & Nelson, 2015; Greenberg & Mollick, 2017; Marom et al., 2015). Marom et al. (2015) attest to female entrepreneurs enjoying higher rates of success than those of their male counterparts, Gorbatai and Nelson (2015) find that female linguistic patterns are preferred over male patterns, whereas Ly and Mason (2012) corroborate that loans to women fund faster. The directionality of the gender effect across crowdfunding studies is consistent and is in line with literature on social finance and microcredit, which has found that loans to impoverished borrowers tend to favor women over men, because female borrowers are considered more reliable (D’Espallier, Guérin, & Mersland, 2011). In addition, in the setting of donations, Greenberg and Mollick (2017) conduct a laboratory experiment based on the premise that women are more likely to succeed at crowdfunding than are men. The authors endeavor an explanation for the gender effect by introducing the concept of activist choice homophily. They believe that the basis of attraction between two individuals is not merely shared similarities but also perceptions of shared structural barriers and difficulties stemming from a common social identity based on group membership. As most humanitarian projects request money for medical treatments, study loans, or house renovations due to natural disasters, they convey an image of greater need than do entrepreneurial projects. Consequently, according to Greenberg and Mollick (2017), the activist choice homophily mechanism is more pronounced in humanitarian settings than that in entrepreneurial settings. Following this reasoning, we derive our fourth hypothesis:

Data and Method

Data

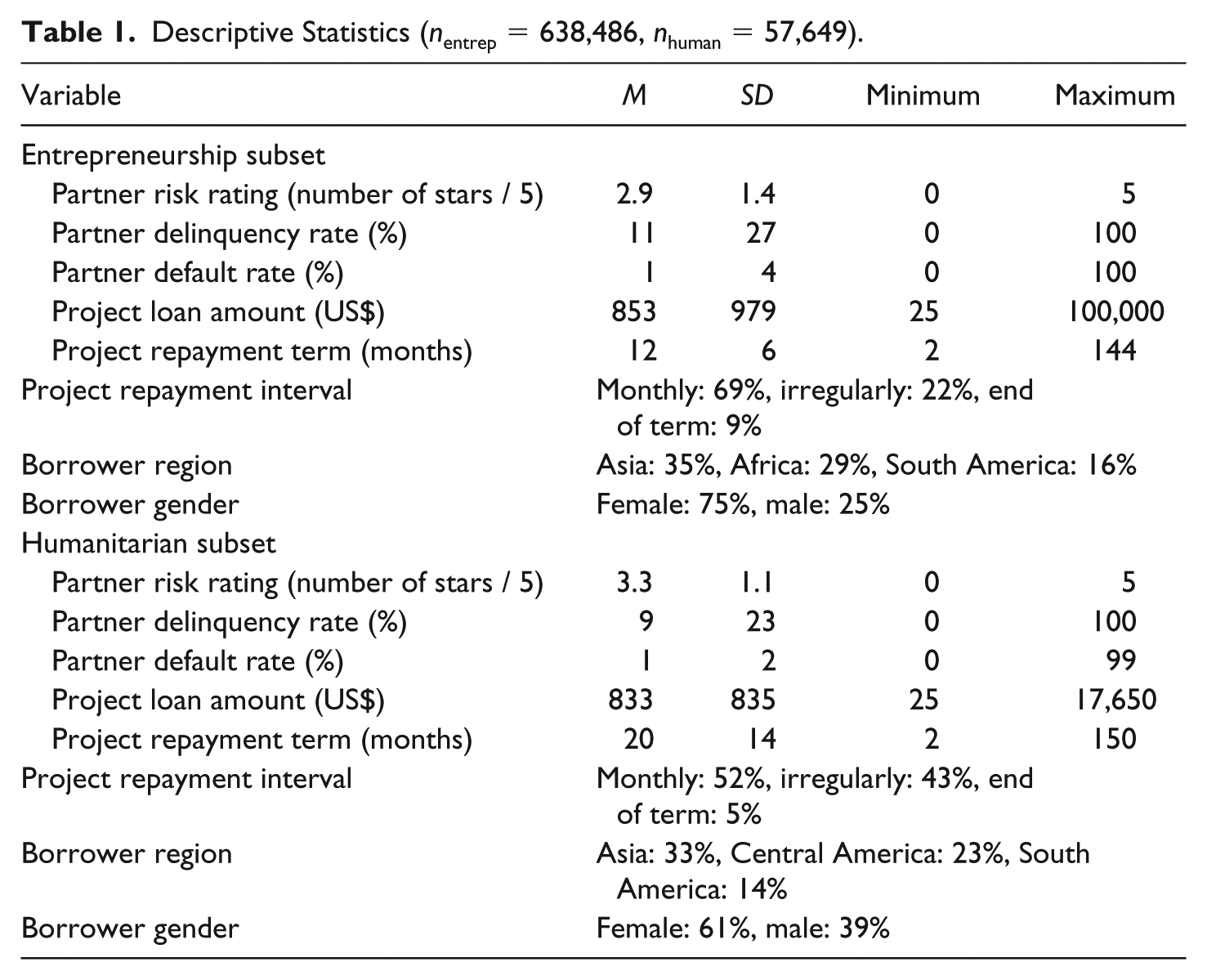

Kiva presents an ideal setting to test the differences between entrepreneurship and humanitarian projects because it is a venue for both types to coexist on a single platform, allowing for a homogeneous environment. We analyzed the entire population of 705,612 projects posted on Kiva from 2005 to 2015, thus avoiding sampling selection bias. After processing the data, we were left with 698,394 loan entries with full information. We classified projects into the two subsets of humanitarian and entrepreneurship based on content analysis of the text description, and we checked the robustness of our classification results using information provided by Kiva on the partners’ activities and areas of operation (Ly & Mason, 2012). For the classification, we distinguished between loans meant for a small business or revenue-generating project (such as Roldan’s, an entrepreneur from the Philippines, who needs to buy two numbering machines to expand his printing business) and loans intended for projects addressing a need of a humanitarian nature. Projects in the latter category include health (personal or family medical expenses), education (e.g., to cover education costs for oneself or school costs for a child), housing (e.g., to rebuild/renovate a home or add basic amenities), and personal use (e.g., wedding expenses). An example is Tuyen, a mother of three in Vietnam asking for money to construct a toilet inside her house. The majority of loans were labeled “Entrepreneurship” (638,486 loans, 91.4%), and the remaining 57,649 loans were labeled “Humanitarian.” We treated these two subsets as separate sets of information and conducted our analysis separately on each to facilitate direct comparison of the results.

The dependent variable is categorical and captures funding success. The variable denotes 1 for a project that was successful in attracting sufficient funding over a 30-day period on Kiva’s platform and 0 for unsuccessful. The entrepreneurship subset has a success rate of 97.2%, whereas for the humanitarian subset, this drops to 93%. Following our hypotheses, the explanatory variables capture certain characteristics of the project and the partner that proxy the degree of risk inherent in a particular loan and the characteristics of the borrower pertaining to region and gender. Descriptive statistics of the explanatory variables can be found in Table 1. Project characteristics that are related to risk as per prior literature are the loan amount, repayment term, and repayment interval (e.g., Frydrych et al., 2014). The higher the loan amount and the repayment term are, the higher the risk associated with the loan. The repayment interval can be monthly, at the end of term, or irregularly, and the degree of risk increases in this order. For the partner, the indicators of risk are the risk rating, delinquency rate, and default rate. The risk rating is a universal indicator for all partners computed based on due diligence and monitoring of the partner’s activities by Kiva. The higher the number of stars (0-5) the partner receives, the lower the risk. Furthermore, the average delinquency and default rates of the partner are inversely proportional to risk, with higher rates indicating a riskier investment. In the analysis that follows, we standardize the numerical independent variables to facilitate the interpretation of results, enabling us to discuss proportional changes when comparing findings between humanitarian and entrepreneurship projects.

Descriptive Statistics (nentrep = 638,486, nhuman = 57,649).

Finally, we include some control variables based on prior findings in the literature to account for several factors that may affect our results, such as the competition among loans, number of borrowers in a project, and sector of activity. Furthermore, we control for time effects across both months and years to remove seasonality and year heterogeneity from our causal model, as well as any learning effects on behalf of partners that may accrue from experience of working with Kiva. The inclusion of these controls as based on prior literature serves to reinforce the strength of our model in terms of causality but does not add to the theoretical discussion of our findings and, for this reason, we remove the controls from subsequent discussion.

Analysis

As our dependent variable is categorical, we employ pooled logistic regression and run our analysis over the two subsets of humanitarian and entrepreneurship. This representation allows us to comment on the directionality and magnitude of the coefficients of each subset separately, as well as to calculate the difference between them for comparison purposes. We report these differences in proportional terms (odds ratios). We also ran a single logistic regression over the entire data set, coding humanitarian as a categorical variable and including the interaction terms for all our explanatory variables pertaining to our hypotheses. The single logistic output allows us to test the significance of the difference between the humanitarian and the entrepreneurship subsets, as per Hypothesis 1.

Our results remain robust when compared with those of a multilevel model with partner fixed-effects specification, which we employ to test the presence of endogeneity issues arising from unobserved heterogeneity among Kiva partners. On comparison with the original logistic model, we find that the coefficients are very similar across the gender variable, risk characteristics, and control variables. The similarity of results between the two models is a good sign of the validity of our findings. However, the fixed-effects specification deprives our study of the ability to incorporate the region variables, because partners tend to be physically present in only one location, and consequently, region is one of the partner characteristics removed from the regression. Furthermore, the multilevel model also excludes risk variables that are common at the partner level, namely, the partner risk rating, delinquency rate, and default rate. Because the difference in coefficients is negligible (<0.00 in most cases), the results from this alternative model specification assuage our initial concerns for endogeneity arising from the unobserved heterogeneity of the partners. For parsimony reasons, we build our discussion of the findings on the pooled logistic regression (Table 1) that allows for the testing of all variables of interest pertaining to our hypotheses.

Results and Discussion

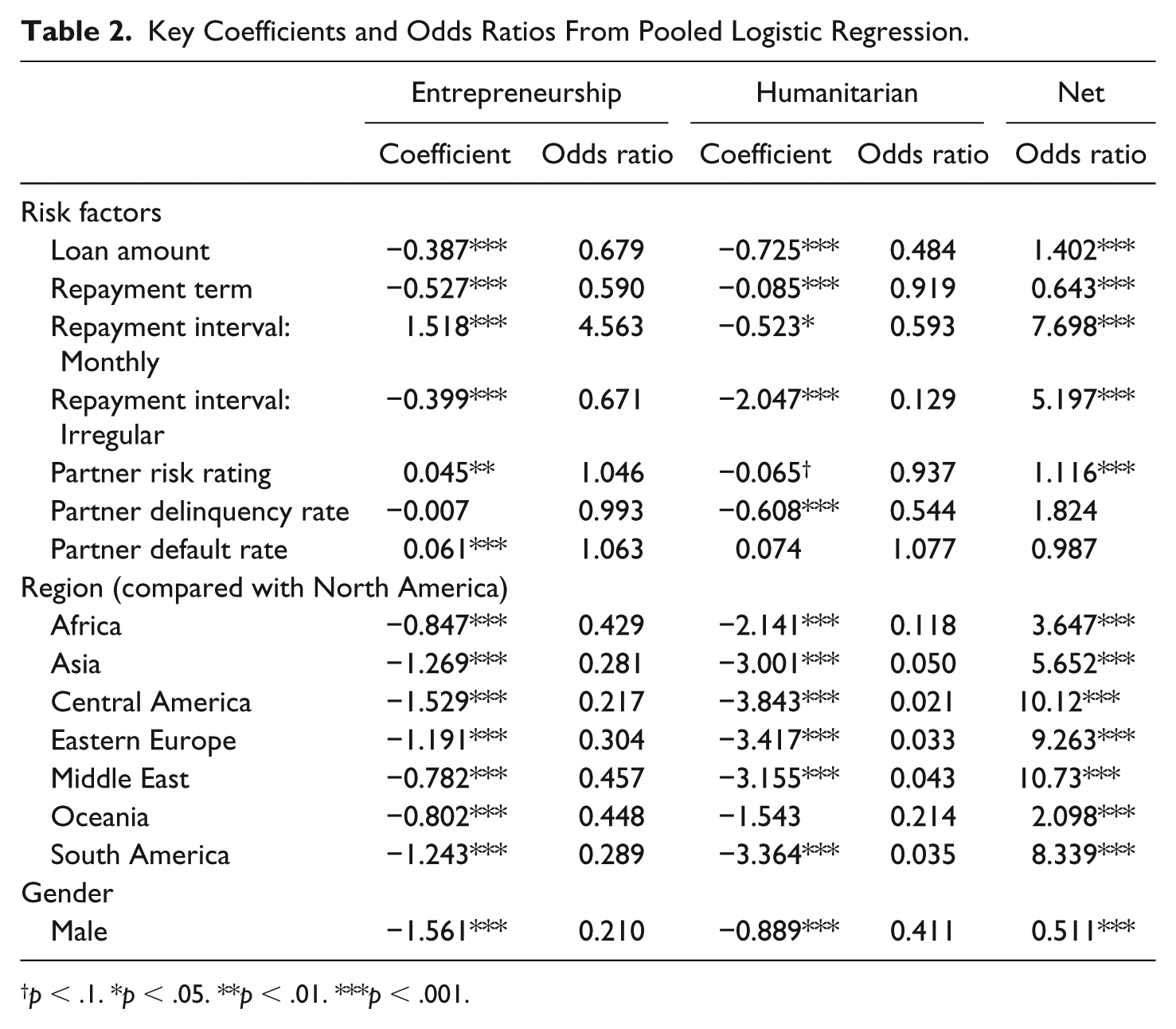

The key results are reported in Table 2, where the first column lists the names of the variables, the second column contains the values of the coefficients from the logistic output of entrepreneurship, and in the third column, we calculate their exponents (odds ratios). Similarly, the fourth and fifth columns contain the results from the humanitarian subset. Finally, the sixth column is calculated as the exponential of the difference in the coefficients between entrepreneurial and humanitarian projects, which gives the odds ratio of the difference across the two project types. An odds ratio higher than 1 indicates that entrepreneurial projects have a higher probability of success than do humanitarian projects, and the difference is given by the numbers in the decimal places, in percentage terms.

Key Coefficients and Odds Ratios From Pooled Logistic Regression.

p < .1. *p < .05. **p < .01. ***p < .001.

Success Signals in Crowdfunding Contingent Upon Project Type

Based on the variance of results in prior literature, we formed our first hypothesis regarding a probable differentiation between heterogeneous project types from the same platform. We argued in favor of the distinction that needs to be made when discussing the impact of a particular signal on crowdfunding success, pertaining to the inherent nature of the project, either humanitarian or entrepreneurship. The project type is an indirect measure of the motivations and proclivities of the lenders who choose to contribute to that project. Lenders who are drawn to humanitarian projects are more or less likely to consider certain signals compared with lenders drawn to entrepreneurial ventures. We find ample support for Hypothesis 1, in that, all the success factors we investigate (risk, lender proximity, and gender) mark a sizable and statistically significant difference between the two subsets, as depicted in the last column of Table 1. In terms of risk, most proxies exhibit a stronger impact on entrepreneurial projects. Regarding home bias, the difference between humanitarian and entrepreneurship is significant across all regions (with the exception of Oceania). For gender, projects led by male borrowers are 49% less likely to receive funding if they are of entrepreneurial rather than of humanitarian nature. Overall, these results justify our initial premise for pursuing this study and call for more research into the heterogeneity of projects found on crowdfunding platforms and, by extension, the heterogeneity of crowd motivations.

Risk Parameters Send Clear Signals for Entrepreneurial Projects, Mixed for Humanitarian Ones

With regard to risk, we hypothesized that risk signals have a negative effect on the probability of funding success for entrepreneurial projects and no effect for humanitarian ones. For entrepreneurial projects, our findings support this thinking, because (a) the higher the funding target, the lower the probability of funding by 32%; (b) the longer the repayment term, the lower the probability of funding by 41%; and (c) monthly repayment interval greatly increases probability of success compared with that of irregular or end-of-term repayment, a clear indication of risk aversion in the entrepreneurial context. In addition, (d) for this type of projects, the risk rating of the partner also has a significant impact, with projects belonging to a less risky partner being associated with a greater probability of funding. All variables, with the single exception of the delinquency rate, are significant.

For humanitarian projects, our findings are mixed. The partner risk rating and default rate lose in predictive significance as hypothesized, whereas the remaining variables challenge each other in the direction of influence. On one hand, looking at the repayment interval, where the benchmark is repayment at the end of term, we see how lenders to humanitarian projects prefer end-of-term repayments to both irregular and monthly repayments, which indicates their willingness to take on more risk vis-à-vis charitable ventures. The explanation behind this observation lies in lender motivations for giving the loan. In a hybrid environment such as Kiva, lenders to humanitarian projects are primarily driven by prosocial motivations and the intrinsic satisfaction of helping others (Bajde, 2013). As such, the lenders’ genuine interest in the successful completion of a project that can ameliorate the lives of less fortunate people predisposes them to greater flexibility in terms of repayment, thereby granting more time and autonomy to the borrower to recover the capital without compromising the project. This type of lender appears more prone to contribute where no savvy, profit-oriented investor would consider doing so. Very similar to nonprofit organizations in the global terrain, humanitarian lenders can be seen as trying to fill a gap in the financial system by helping out where traditional lenders consider it unfeasible. This observation hints at prosocial motivations dominating over risk preferences in humanitarian settings, an interesting interaction that merits further inquiry.

On the other hand, the results for the delinquency rate show that an increase in delinquent loans decreases the probability of funding for humanitarian projects by 46%. This risk parameter reflects the ability of the partner to gather repayments on time. In the absence of professional investors and established due diligence processes, crowd lenders largely rely on the judgment and ability of local partner staff who select the projects, provide local assistance, monitor progress, and collect repayments. Thus, a high delinquency rate reflects poorly on the ability of the partner to correctly assess project feasibility and borrower risk prior to promoting their projects. The delinquency rate acts as a capability signal to warn potential lenders about the efficiency of their contribution. In this case, the signal is transmitted by the intermediary of the crowdfunding process rather than by the project itself, which suggests that, given the option, the decision of association with a particular partner is a crucial signal from the borrower’s perspective.

Furthermore, some additional findings that arise are thought provoking. Regarding the size of the loan, this study finds that the higher the loan amount is, the lower the probability of success in both humanitarian and entrepreneurial projects, but the effect is stronger for humanitarian projects. Looking at the difference between the two subsets, when increasing the loan amount, entrepreneurial loans have a 40% greater chance of funding than do humanitarian loans, ceteris paribus. This result is an indication of risk aversion in both entrepreneurial and humanitarian contexts. One possible explanation is that the size of the loan sends distinct signals in each case. A larger capital contribution for a profit-making business may signal a serious commitment on the part of the entrepreneur to carry out his or her venture, whereas a large loan for rebuilding a house may signal extravagant spending that goes beyond covering basic needs and is more difficult to repay. Therefore, it is possible that the interpretation of the signal transmitted by the loan amount changes in conjunction with the type of project.

Home Bias, Gender Bias

Building on prior literature, we also posited that the borrower’s region of origin has a stronger impact on the probability of funding success for humanitarian than that for entrepreneurial projects. Our results strongly support Hypothesis 3. Because the similarity between lender and borrower is an important factor for predicting funding success, and because the majority of lenders come from North America, we expected the home bias effect to manifest as a strong preference for North American projects. Our model takes North America as a benchmark and finds that borrowers from all other regions have a much lower probability of success, for both humanitarian and entrepreneurship projects. For instance, an entrepreneurial project from Asia has a 72% lower chance of success than that of one from North America, and a humanitarian project from the same region has a 95% lower chance. Similarly, across all regions, the coefficients indicate a stronger impact of the region parameter for humanitarian projects than that for entrepreneurship, compared with North America, in line with our expectations.

Furthermore, with respect to the influence of gender on the probability of funding success, Hypothesis 4 is only partially true. We argued that projects led by women have a higher probability of funding than do projects led by men, and this is supported by the data. However, contrary to our hypothesis, the gender effect is stronger for entrepreneurial projects. Our results show that, compared with women, men have a 59% lower chance of funding with regard to humanitarian projects. However, the preference for women is even more pronounced for entrepreneurial ventures, where men have a 79% lower chance of success than do women. This result may seem counterintuitive according to prior entrepreneurial and nonprofit research. A possible explanation is that, due to the social nature of Kiva, even lenders interested in entrepreneurial ventures consciously prioritize women-led projects precisely to balance the male prevalence that usually occurs in the rest of the entrepreneurship world. This particularity of the data set may act as a limitation to the generalizability of our results on other crowdfunding platforms. Kiva lenders are not representative of the general population, as they have a social mind-set and may, therefore, appear biased in favor of disadvantaged populations such as female entrepreneurs. Nonetheless, our results may hold true in nonprofit settings, where people engaging in donation-based and lending-based crowdfunding already share part of this social mind-set; otherwise, they would have opted for more profitable investment options.

Conclusion and Future Research

Based on a review of the entrepreneurship and nonprofit literatures and employing the lenses of signaling theory and behavioral decision making, we hypothesized how certain success factors for crowdfunding projects have varying impacts depending on the nature of the project, from humanitarian to entrepreneurship. Even in the homogeneous environment of a single platform, heterogeneity in lender motivations persists and is reflected in the differentiating impacts that risk, lender proximity, and gender have on the different types of projects. This observation marks the key contribution of our research.

At the same time, our study is not without its limitations. Our model is built on cross-sectional data and this deprives us of the possibility to investigate fundraising success along the dimension of time. Here lies an opportunity for future researchers to study the crowd’s decision-making process, by following lenders over time to discern their longitudinal funding patterns. In addition, the use of more direct measures of lender motivations can add value to the field. Moreover, there is room for scholars to explore whether these behavioral tendencies persist in other crowdfunding models, such as rewards based and equity. Finally, we observe how some information displayed most prominently on the platform is likely to influence decisions to a much greater extent than will information that is harder to access. This observation reiterates the importance attached to the design of the online platform and makes platform design, or choice architecture (Thaler & Sunstein, 2008), a crucial feature for funding success awaiting further investigation.

Our study aims to add to the existing body of literature on crowdfunding and to help advance our understanding of the phenomenon by borrowing theoretical and empirical findings from the nonprofit and entrepreneurship research streams. As crowdfunding is an emergent phenomenon, with new online platforms and financing options appearing every day, developing a thorough understanding of what attracts lenders is important for both academics and practitioners. By reconciling prior contradictions in crowdfunding research and bringing forward new ideas and questions regarding behavioral aspects and biases, we wish to support the vigorous growth of this emerging phenomenon of growing economic and social importance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.