Abstract

The growing use of donor-advised funds (DAFs) is changing the way many donors give to charity. Despite the increasing influence and importance of DAFs in the nonprofit sector, very little is known about how people actually use them. We conducted 48 in-depth interviews with DAF users, collecting rich qualitative data about why and how donors use DAFs. We use these data to sketch a DAF giving process with four phases and multiple decision points. We highlight some of the common donor strategies that are used with DAFs. Overall, we present evidence of abundant diversity in individual adaptation for giving through DAFs.

Introduction

Emerging forms of philanthropy can reveal important insights into why and how individuals voluntarily donate—a behavior that, in 2019, realized almost $450 billion in donations to charitable organizations in the United States (Giving USA Foundation, 2020). Researchers have studied recent forms of emerging philanthropy such as the growth of giving circles (Eikenberry, 2006), simultaneous solicitations such as GivingTuesday (Vance-McMullen, 2019), and the use of social enterprise within nonprofits (Fitzgerald & Shepherd, 2018). Daniels and Lindsay (2016) argued that donor-advised funds (DAFs), perhaps more than any other concurrent trend, are “reshaping the landscape of American philanthropy” (p. 1). DAFs function as charitable giving accounts that are managed by 501(c)(3) “sponsor” organizations. Donors make tax-deductible contributions into DAF accounts and later “advise” sponsors on where and how much to grant to another 501(c)(3) organization. In 2019, DAFs received over 12% of all household charitable contributions and managed over $142 billion in tax-exempt assets (National Philanthropic Trust, 2021a). Both of these figures have increased every year since 2006, when Congress first started tracking DAF metrics through the Form 990. Despite the conspicuous growth of DAFs observable from organizational data, little is known about how individual donors use DAFs.

Studying the use of DAFs can be challenging because individual (account or donor) data are difficult to collect. On the Form 990, DAF sponsors report aggregated totals for contributions, grants, number of accounts, and assets. While these data facilitate analyses of organizational performance metrics over time (see Heist & Vance-McMullen, 2019), they do not help answer questions about how or why individuals use DAFs. Many DAF sponsors also provide annual reports with valuable insights about their clients’ charitable activities (see Fidelity Charitable, 2016, for example). Although helpful, these reports focus on the donors of a single DAF sponsor rather than a broader array of DAF users. When quantitative data are scarce, many scholars have turned to qualitative methods to research emerging topics in philanthropy (Child et al., 2015; Dale, 2018; Eikenberry, 2006; Fitzgerald & Shepherd, 2018). We, likewise, use a qualitative approach to study this increasingly popular form of philanthropy.

Practitioner literature indicates common reasons for using DAFs, including tax benefits and convenience (Rooney, 2017). While motives and mechanisms for using DAFs are undoubtedly connected (e.g., donating appreciated securities through DAFs), our goal is to more deeply understand how individuals use DAFs. What are the various decisions that donors make when using a DAF, and how are those decisions connected? Does the separation of the tax deduction from grantmaking influence the way donors give through DAFs? What is the timing of DAF grantmaking after contributions are made? Through qualitative analysis, this article serves as an initial exploration to answering these questions. Findings, furthermore, provide a conceptual framework for future work on understanding DAF giving.

Background and Literature Review

Historical Context

DAFs are the fastest growing form of philanthropy in the United States. From 2015 to 2019, the number of DAF accounts has more than tripled—from 272,781 to 873,228 (National Philanthropic Trust, 2021a). But where did they come from, and why are they so popular now? Early forms of DAFs appeared among community foundations (CFs) in the early 20th century. Berman (2015) explained that DAFs emerged during a period when early income tax laws incentivized more private involvement in the public sector. Later, the Tax Reform Act of 1969 enforced greater control over philanthropists, specifically private foundations, by demanding more accountability and transparency. In response to this shift in tax policy, CFs began to promote DAFs as a way for philanthropists to circumvent the strict regulations on private foundations (Berman, 2015). Then in the 1990s, Fidelity Investments and other commercial investment firms opened their own charitable subsidiaries to offer DAFs to their clients, which led to an expansion in the use of DAF accounts. Religious organizations and other charities likewise began to sponsor DAFs to cater to their constituents. The most growth in the last 2 years can be attributed to companies that facilitate charitable giving in the workplace by establishing DAF accounts for employees to direct a portion of each paycheck to charity (Ebeling, 2018). DAFs are now sponsored by a variety of organizations, including CFs, national sponsors, and single-issue charities, each catering to a unique—but potentially overlapping (i.e., some DAF users have multiple accounts)—subset of donors.

Evidence about the efficacy of DAFs in facilitating charitable giving is mixed, largely due to limited data. Critics are concerned that donors may stockpile tax-deducted charitable dollars in DAFs with no promise of the funds being used for charitable purposes (Andreoni, 2017; Callahan, 2017; Colinvaux, 2017, 2018; Gelles, 2018; Hussey, 2010; Madoff, 2014, 2016a, 2016b; Sherlock & Gravelle, 2012). National Philanthropic Trust (2021a), on the contrary, reported that the aggregate payout rate among DAFs has remained between 15% and 25% for the past 10 years, depending on how it is calculated (see also Andreoni & Madoff, 2020). Moreover, the aggregated payout rates include DAF-to-DAF transfers, which Giving USA Foundation (2020) reported to be 4.4% of all grants. Heist and Vance-McMullen (2019) found evidence that DAFs may be used as pass-through vehicles, where money is moved in and out within the same year. However, the extent to which individual donors stockpile money or use DAFs as pass-through vehicles is unknown. In contrast to data available on the Form 990, which do not detail individual DAF activity, the interviews from this study provide a more nuanced understanding of the ways individual donors, rather than sponsor organizations, use DAFs.

DAF Giving Process and Timing

Donating to charity is a complex decision-making process that involves social, psychological, economic, and religious considerations among others. Sargeant (1999) developed a process model of individual giving behavior to diagram the various inputs, determinants, psychological processes, and decisions, as well as charitable outputs, involved in giving. Inputs included fundraising appeals, brand recognition, knowledge, and the mode of ask. Determinants of giving included extrinsic factors such as age, gender, social class, and income, as well as intrinsic determinants such as a sense of social justice, empathy, fear, and sympathy (Sargeant, 1999). Sargeant’s model provides a framework for understanding the relationships of various determinants within the process of charitable decision-making. It does not, however, provide a framework for the transactional process of transferring resources from donor to charity. Hibbert and Horne (1996) suggested that “if research into donor behavior is to progress, it needs to look beyond ‘why’ people donate to consider the reality of ‘how’ they donate” (p. 4). As DAFs are an intermediary philanthropic vehicle, they affect the transactional process—or the “how”—of giving. Similar to Sargeant’s (1999) giving process model, we track the multiple inputs involved in using a DAF; however, in contrast to Sargeant (1999), we also track the flow of resources from donor to recipient organization through DAFs.

DAFs change the flow of money from donor to nonprofit, disrupt traditional fundraising relationships (Rooney, 2017), and desynchronize previously synchronous elements of charitable giving decisions. Heist and Vance-McMullen (2019) provided a model in which donors first contribute cash or assets into a DAF and receive a tax deduction upfront; second, the donated assets are managed and invested by the sponsor organization; and third, donors advise the sponsor to grant out of the DAF account to another charity. While this model acknowledges there are multiple phases in the DAF giving process, it does not identify the multiple decision points within the phases or the iterative nature of some phases of DAF giving.

Conceptualizing multiple decision points within phases is important because the phases of the DAF giving process bifurcate decisions that happen simultaneously under traditional giving models. In other words, the decisions of whether or not to give and what or how much to give may be separated from the decisions of where to give and when to give (Rooney, 2017). This separation necessitates a new framework with which to apply previously identified determinants and elements associated with charitable giving. Take, for example, the price of giving, which is known to directly affect charitable giving behavior (Heist & Cnaan, 2018; Vesterlund, 2016). Andreoni (2017) explained how DAFs effectively lower the after-tax price of giving by facilitating the donation of noncash assets (often highly appreciated). This tax-effect can help explain contributions into DAFs, but it cannot explain grants out of DAFs. Instead, DAF grantmaking requires another set of social, psychological, and economic factors for explanation. Furthermore, consider how benefits of giving, such as warm glow, may be experienced at multiple phases of the DAF giving process. Andreoni and Serra-Garcia (2016) found experimental evidence that donors experienced some aspects of warm glow by committing to give a week before the transaction was made. This suggests that it is possible that donors experience warm glow during the initial phase of setting up a DAF and may also experience warm glow during future phases of DAF giving. Owing to the unique nature of DAF giving, further exploration is merited to clearly articulate the various stages and decision-making processes involved with giving through DAFs.

A conceptual model with multiple decision points provides a framework to analyze other social, economic, and psychological phenomena associated with charitable giving. Research in neuroscience has identified cognitive processes associated with empathy, value estimation, rewards, and social cognition occurring in different parts of the brain during charitable giving decision-making (Harbaugh et al., 2007; Hare et al., 2010). Judgment and decision-making scholars have identified numerous psychologic phenomena such as the identifiable victim effect (Jenni & Loewenstein, 1997), the friends of victims effect (Small & Simonsohn, 2008), or overhead aversion (Gneezy et al., 2014). Bekkers and Wiepking (2011) categorized eight social and psychological mechanisms driving charitable giving and philanthropy, including awareness of need, cost, and benefits analysis, and social and psychological motives. The model developed in this article allows such phenomena to be understood within the unique context of DAF giving.

Related to the economic incentive to reduce the price of giving, industry reports, financial periodicals, and practitioner publications commonly identify DAFs as a way to optimize tax savings. As has already been mentioned, DAFs facilitate the donation of noncash assets and provide an immediate income tax deduction without a requirement for immediate distribution. Some people donate into DAFs in years of income volatility or liquidity events to maximize a charitable deduction and “smooth” charitable giving through periods of income fluctuation (Andreoni, 2017). Another tax-saving strategy is the concept of pre-paying or “bunching,” in which people contribute several years of donations into a DAF in one year to maximize tax deductions (Andreoni, 2017). Some evidence of this strategy was manifested when DAF assets spiked at the end of 2017 because the standard deduction nearly doubled from the Tax Cuts and Jobs Act (McCambridge & Rooney, 2018). Interviews from this study allow us to explore the extent to which DAF donors pursue tax-saving strategies.

Madoff (2016a) questioned the legitimacy of allowing this timing difference between the tax deductibility of a contribution into a DAF and the ultimate grant made to another 501(c)(3) and challenged the overall benefit of this timing separation to the nonprofit sector. Others have contended that this flexibility in timing could be beneficial. Harris and Hemel (2019) explained how the separation fits well with the life cycle of most donors, positing that DAF donors can make contributions when they are busiest in their careers and their earnings are highest and then grant money when they have more time and energy to direct the funds. This article does not directly address public policy debate around the timing of the deduction, but findings from this article help elaborate upon the nuances of individual circumstance related to issues of timing and philanthropy.

Timing is a critical element of donors’ philanthropic strategies. Frumkin (2006) explained: “The timing of giving is inextricably connected to the value proposition, the vehicle through which giving will take place, the style of the donor, and the theory of change that is pursued” (p. 293). Andreoni (2017) calculated the average “shelf-life” of DAF resources to be 3 to 4 years at the organizational level. At the individual level, we can expect considerable variation in the timing of money moving in and out of DAFs. Many CFs use an “endowed DAF” model, where the DAF account is treated like an endowment, the principal assets are preserved, and the grantmaking is made consistent with a minimum payout rate (typically 5%; North Carolina Community Foundation, n.d.). The endowed model helps CFs to ensure sustainable long-term funding for community-based philanthropy. Notwithstanding, several industry reports (from both CFs and commercial national sponsors) have indicated that DAF donors have accelerated their DAF grantmaking in 2020 to respond to the COVID-19 pandemic (National Philanthropic Trust, 2021b; Parks, 2020; Theis, 2020). Such potential variation in timing strategies indicates the flexible nature of DAFs in facilitating emergent strategic approaches to giving.

Methods

Qualitative methods are particularly useful to examine under-researched areas (Creswell, 2013), areas where theory is undeveloped or underdeveloped (Ravitch & Carl, 2016), and areas where complex processes occur (Marshall & Rossman, 1995). There is precedent for the use of qualitative methods specifically in areas of philanthropic research (Dale, 2018; Trobe, 2013). Considering the lack of extant research on DAFs, this study employed a pooled case comparison approach. Unlike secondary analysis, which uses existing data originally collected for another purpose, or meta-analysis, which synthesizes findings across multiple studies, pooled case comparisons combine raw data from two or more independent studies (Heaton, 2011). As West and Oldfather (1995) write, “a unique and essential quality of pooled case comparison is that raw data from separate studies are not simply compared but are pooled for new analysis” (p. 457).

The Two Studies

The data used for this pooled case comparison came from two studies. Methodologically, the studies were quite similar; see Table 1 for an overview of each study. In terms of sampling, both studies used a purposeful selection approach to sampling, which emphasizes identifying participants who can both “provide information that is particularly relevant to [our] questions and goals” and with whom productive relationships can be formed (Maxwell, 2013, p. 97). This approach was selected, in part, because participants were likely to have sensitivity around discussing financial matters, and because there is no existing registry or list from which to draw interviewees. Sampling for Study 1 stemmed from two sources: (a) the authors’ personal connections with existing DAF users (n = 8) and (b) referrals from managers of DAF sponsors (n = 7). These initial 15 interviews then yielded 10 additional referrals for a total of 25 interviews. Sampling for Study 2 stemmed from a university research center with a focus on philanthropy (n = 15), the researchers’ personal networks (n = 5), and snowball sampling (n = 3). In both cases, researchers continued recruiting and interviewing individuals until the researchers agreed that data saturation in the form of “informational redundancy” had occurred, and interviewees shared similar comments or sentiments (Sandelowski, 2008).

Comparison of Two Studies.

In terms of data collection, both studies used semistructured interviews to collect data and had independently developed protocols with similar aims and questions. Both included open- and closed-ended questions covering a variety of subjects: (a) motivation for using DAFs (e.g., perceived or realized benefits, prior knowledge of DAFs); (b) DAF management (e.g., initial set up, mechanisms for contributing, and involved parties); and (c) DAF giving behavior (e.g., timing and grantee selection). The 25 interviews for Study 1 took place between June 2018 and March 2020. All but four of these interviews were conducted over the phone, and the interviews lasted between 16 minutes and 65 minutes, averaging 36 minutes in length. Study 2’s 23 interviews took place between March 2020 and August 2020; these interviews were conducted primarily over Zoom. Table 2 includes descriptive information of the full sample.

Description of Interviewees.

All interviews were audio-recorded and then professionally transcribed. To protect participant anonymity, pseudonyms were assigned. Each participant was treated in accordance with the ethical guidelines set by the Institutional Review Board of the studies’ respective universities.

Analytic Approach

The codebook was developed through both deductive and inductive processes. Prior to coding, all coders familiarized themselves with the data by reading completed transcripts, after which they generated a list of preliminary inductive (i.e., generated direction from participant statements) codes and definitions. Preliminary deductive codes were generated from scholars who have identified conspicuous elements of DAF activity and reasons for using them (Andreoni, 2017; Heist & Vance-McMullen, 2019; Rooney, 2017). Using this initial codebook as a foundation, coders independently coded the same three transcripts, both applying previously identified codes and developing new ones. The team then collectively revisited the codebook, collapsing duplicative codes, creating new codes, and clarifying code descriptions. This multistep process was an initial step toward establishing interrater reliability (IRR), with the goal of reliably eliminating inconsistencies between coders (Ravitch & Carl, 2016). Once the codebook was sufficiently developed and clarified, the coders tested IRR on a previously uncoded transcript, refining and retesting until reaching a kappa score greater than 0.8.

Following protocols developed by both West and Oldfather (1995) and Yin (2014), data from each study were analyzed separately (using qualitative software Dedoose, version 8.3.20) and then collapsed and compared. Some sections of text were overcoded, where multiple codes are applied to a single passage, while others were not relevant to the research focus and thus received no code assignments. Each transcript was coded by at least two coders.

Results and Discussion

The presentation of results follows a conceptual model of the DAF giving process, which organizes a multitude of decision points into a four-phase logic model. This model provides a frame of reference to discuss distinct behaviors related to DAF giving. Throughout our results, we discuss variations in individual applications, some common strategies across donors, and possible implications of our findings.

DAF Giving Process

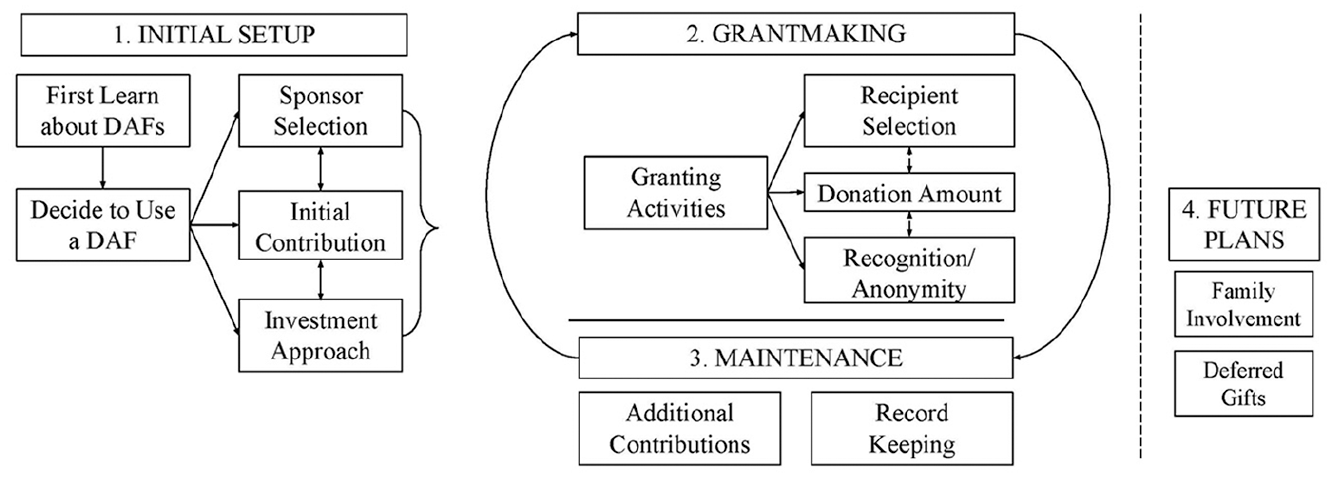

We identified four phases of the DAF giving process: (a) initial setup, (b) grantmaking, (c) maintenance, and (d) future plans. Figure 1 represents a diagram of the DAF giving process, and the arrows attempt to show the interconnectedness of the decisions involved. The phases follow a logical order, but we found considerable variation in the timing of donor engagement within each phase. The initial setup phase happens in a relatively short and finite period. The grantmaking and maintenance phases comprise a cyclical and iterative process that happens within a year, over multiple years, or even over a lifetime. Donors considered previous contributions when making grants and conversely considered their grantmaking decisions when making additional contributions. Some donor strategies related to both phases are also presented. The future plans phase is presented last but lacks any definite chronological relation to the other phases. Some donors had future plans before initiating a DAF, and some had not yet considered future plans for their DAF after years of use.

DAF Giving Process.

Phase 1: Initial setup

The initial setup phase included learning about a DAF, choosing a sponsor, making an initial contribution, and selecting an investment approach. Although many of these decisions could be modified later, donors generally stuck with their original choices, making initial setup important for future DAF activity. Those who had made changes had often been using DAFs for many years (i.e., decades) and several had multiple DAFs. Donors mainly learned about DAFs at their place of work, from their involvement with philanthropic institutions, or family and friends. Contrary to popular critique that financial service firms are pushing their DAF products on their clients (Gelles, 2018; Hobson, 2020), professional advisors were less frequently cited as points of DAF introduction, which is in line with existing research (Bank of America, 2018). However, referrals from advisors were more common among participants who were contributing larger sums of money. When choosing a DAF sponsor, participants often had prior experience or familiarity with the institution. For example, CF donors typically had some direct involvement with the CF prior to opening a DAF there. Similarly, national sponsor DAF donors cited the convenience of combining charitable giving services with the other financial services of the parent company. As Peyton shared, “I had my brokerage account with [Parent Company], and it was the logical convenient choice.”

When making initial contributions into the DAF, we found different rationales for timing, donation amount, and asset types depending on circumstances. Several donors made an initial contribution based on a liquidity event (like Yael, who sold her winery) or another form of income volatility (like Bill, who had a retirement bonus). Donating nonpublicly traded assets (like the winery) are especially attractive to DAF donors, because DAFs are public charities, which allow for more favorable (i.e., less restrictive) tax deductibility limits than private foundations. A few participants specifically deployed a “bunching” technique by initiating their DAF with enough resources to supply funds for several years of their normal charitable giving, in a way that would allow them to itemize their DAF contribution as an income tax deduction. Most participants used some form of appreciated assets (generally securities) to initially fund their DAF. Some participants used cash to fund the DAF, which mainly reflected the lack of appreciated securities in the participant’s wealth portfolio. For some, tax savings were not the primary motivator for cash contributions, like Priscilla who contributed to her DAF from a payroll deduction, or Gordon who used the proceeds from surrendering his cash value life-insurance policy to set up his DAF at the CF where he served on the board. In other cases, high income provided the tax motivation for donating cash to the DAF.

Some participants contributed resources from another DAF or private foundation. A couple of interviewees had a DAF initiated for them with funds from family member’s DAFs as a way to pass on family philanthropy. Some donors in our sample used funds from one DAF account to establish an account at another DAF sponsor organization either to support a specific cause or community represented by the organization or for more convenience. Two participants used distributions from a private foundation to fund a DAF, each for different reasons. One interviewee was exploring the option of closing down the private foundation and using the DAF vehicle as an alternative vehicle. The other used the DAF “like an overflow acount” for the minimum 5% payout requirement, for two reasons: “I just don’t have enough charities that I want to support that year or. . . I’ve made a pledge, but it’s not going to be within that calendar year.” Both DAF-to-DAF transfers and private foundation transfers, as ways to fund DAFs, are controversial for reasons that will be discussed later.

Once a DAF is funded, the donor generally has the option to select an investment strategy for the DAF funds. National sponsors seemed to have more variety in investment options; however, a few donors seeking social impact investments chose DAF sponsors specializing in this area. Regardless of options, most participants mentioned little interest in either investment strategies or performance, other than a few participants who specifically noted an interest in seeing their account grow. Only a few could share details about how money in the DAF was invested or the returns on those investments. One possible reason for this lack of interest was the short time horizon expected for the money in the DAF. Priscilla explained, “I didn’t actually do it as a growth vehicle at all. I just did it as a holding tank for the money that I wanted to contribute.” Some participants, who voluntarily shared their professional experience with finance or accounting, were more involved in the investment approach. Overall, however, few participants reported making changes to their investment strategy after the initial setup.

The vast majority of participants directly or indirectly discussed the tax-saving benefits of donating to a DAF. This motivation was typically coupled with contributing appreciated assets into the DAF, in line with tax-saving strategies explained by Andreoni (2017). Participants often recognized the tax benefit of giving during years with high income or capital gains. Walter put the tax benefit most succinctly when he commented that DAFs allow donors to “get the charitable deduction in the year they want to receive it.” Isaac explained it in more detail: You have an asset where you have a very low cost basis and a huge tax liability. By giving it to your donor-advised fund, you discharge that entire tax liability. That’s really a very efficient way of giving. It’s the most efficient way of giving, but it requires you to have an asset that’s appreciated.

Other participants were more vague about the role taxes played in their charitable decisions, describing DAFs as “a tax convenient way” to give or saying that it allows them to give “tax efficiently.” Participants had varying degrees of awareness of the specifics of the tax benefits. Carissa told us “my friend explained the benefit in tax write-off options of a DAF. Now I know I didn’t understand correctly but still, I thought it was a benefit.” Almost all respondents had some level of awareness of the tax implication of donating to a DAF.

The second-most prominent reason why participants described using DAFs was for the convenience and ease of use. For example, participants referred to DAFs as “a low-cost, low hassle, win-win type of thing,” and, “once it’s gone through the process, it’s set up and it’s so easy.” Participants commented particularly on how “really easy” or “very easy” it was to transfer appreciated assets, especially when they had an investment account at the same parent company as a national sponsor. Adam spoke of how his sponsor made it easy to identify stock “with the largest unrecognized gains” and that a big advantage is the “real time access to this where I can time [contributions] much more precisely,” referring to the ability to time—during the day—the donation of a security to the DAF.

Phase 2: Grantmaking

The grantmaking phase includes donors’ decisions about how much, when, and to whom to make grants. Analyzing donor responses about grantmaking, we found a wide range of causes, key considerations, and some complications. Our findings suggest DAFs facilitate extant philanthropic behaviors and preferences. Participants in this study gave before using a DAF, gave in addition to using a DAF, and would have given even without a DAF. They issued grants to a wide variety of nonprofits, representing a host of charitable causes, including to “a local school for girls” or “environmental causes” or for “tithing.” However, we did find that the type of sponsor organization mattered. Those giving through a CF exhibited more geographic (local) preferences, and those giving through single-issue charities exhibited more cause-related (specifically religious) preferences. When asked whether or not donors sought or received grantmaking recommendations from the sponsor organization, only a few donors with CF and faith-based DAFs had engaged with their sponsor in a way that affected their grantmaking. Most participants expressed that they did not want that kind of engagement with the sponsor. Even rarer was incidence of DAF sponsors blocking a grant request from a donor—only two interviewees had this experience. From our sample, we found donors bring their own philanthropic agendas while using a DAF as a philanthropic tool.

DAF grantmaking can involve several strategic considerations. Of top concern to nonprofit leaders is the issue of anonymity. Most of our participants chose not to give anonymously most of the time. Viviana shared, “Typically, we do attach our name, though I think we have given anonymously.” For the few who had chosen anonymity on specific occasions, we found a few different rationales. Anonymity allowed them to avoid recognition, to avoid receiving subsequent solicitations, or to avoid social stigmas. For example, Wendy explained: So we don’t usually give anonymously through that fund. But when we give our bigger gifts, we try to give anonymously. It’s hard, I think once your name gets out there having given a certain amount, the number of people that start calling you is really overwhelming.

In contrast, both Janet and Una gave anonymously to their children’s schools to protect their children from bias or stigma. One participant in particular gave anonymously most of the time to avoid unwanted solicitation. Moreover, some participants simply did not want to be recognized as a matter of personal preference.

The added layer of separation between donors and charities created by DAFs can precipitate challenges. For example, some DAFs offer partial anonymity, listing only the fund name (which may or may not include a family name), but not the name of the donor, making it difficult for charities to acknowledge and steward the donor. On the other side, several participants expressed a lack of responsiveness from recipient charities, and on occasion, they had to make extra effort to request confirmation of receipt and acknowledgment for a gift. For example, Yvonne shared, “I gave a $25,000 donation in January out of the donor-advised fund. I had documentation in my [DAF] account that it was transferred to [Charity], and that it was received. I never got a thank you note.” Giving through DAFs can make it difficult for charities to recognize donors, and this lack of responsiveness disrupts the appreciation donors often seek.

Conversely, donors also said that “[the DAF] has made it a lot easier to make a grant,” especially to small charities and for small amounts. For example, Henry spoke of the ease to donate appreciated assets to a DAF to a small charity: A lot of the charities that I deal with are very small, and so it’s a big undertaking for them [to handle appreciated securities]. . . [The DAF] was just a convenient way to handle transactions with charities, and it had the added advantage of making it easy to use appreciated securities.

For ease in grantmaking, Bill explained that he could use the online DAF platform to grant to any charity he could think of, “I was overwhelmed by finding no problem finding any charity imaginable.” The convenience factor, however, varied by sponsor. For example, a couple of our interviewees who used multiple DAFs appreciated the ease of the national sponsors’ websites but were frustrated by the length of time it took for smaller sponsors to make grants.

Finally, DAFs created an opportunity to connect with new organizations. As Victor shared, “We’re giving more, and it gives us more opportunities to say, ‘Well, here’s a request for some money. Let’s evaluate it and say yes or no.’ Before it was almost always a no.” This is particularly important during natural disasters and crises like the COVID-19 pandemic, in which we have seen reported increases in DAF grantmaking. Several Study 2 participants mentioned COVID response giving (as they were interviewed during the pandemic), like Denise who said, “Whereas in my own personal giving, it’s a little bit more loosey-goosey and COVID-19 hit, so I’m going to give to this service organization . . .” This individual flexibility to respond to changes in the giving environment is facilitated by the flexibility of using the DAF vehicle as an intermediary.

To summarize, the consistent theme across our interviews was that DAFs provided a high level of flexibility to the grantmaking phase, allowing donors to pursue individual philanthropic strategies customized to their own unique preferences and life circumstances. The grantmaking phase often followed an iterative, cyclical pattern with the maintenance phase. Donors make grants out of the DAF, then contribute more resources into the DAF to plan for subsequent donations.

Phase 3: Maintenance

The maintenance phase focuses on the near-term efforts involved with maintaining the DAF, including reviewing records of contributions and grants, and making decisions about additional contributions. During the maintenance phase, participants periodically checked their DAF balance and, if needed, added more to the account. When asked the approximate balance of their account, most participants could readily answer, but answers were often contextual, indicating that the balance changed depending on where donors were in the grantmaking/maintenance cycle. DAF balances fluctuate depending on grantmaking, additional contributions, and investment returns. Phrases such as “we just added some more” or “we are about to spend it down” gave some indication of where participants were in the DAF giving cycle. Participants also used their DAF to conveniently keep track of their giving, which helped for both the grantmaking process and for tax-filing. Donors only have to report contributions into the DAF on their tax returns and do not have to report the (often more numerous) grants made from the DAF. Explained Sergio, “It’s just such an easy way of doing it, maintaining it, and managing it. Record keeping is just so easy.” Record a keeping was one of the DAF features closely associated with perceptions of convenience and was frequently mentioned as reason why people like to use DAFs. Record keeping also allows donors to easily repeat previous donations and look at historical giving to make more strategic decisions about giving in the future.

As mentioned above, the Grantmaking and Maintenance phases represent a cyclical and iterative process. Throughout the interviews, participants explained their personal strategies that governed their approach to these phases. Presented here are several of the more common strategies, but this synopsis is by no means exhaustive of all strategies donors may take with DAFs.

Most donors had some sort of annual reckoning with their DAF use, and a common strategy was to contribute money into a DAF in anticipation of what would be granted the following year. When asked if she keeps a lump sum in her DAF, Una, who gives about $350,000 to nonprofits every year, responded, “No, we’ve been spending it down every year.” Similarly, Quinton reported having a current balance of $4,000 (at the time of the interview) but that he normally contributes and then grants out about $75,000 per year. This annual budgeting strategy did not seem to be limited by gift amount. Kayla explained, “We give away $5 million a year. So we put the $5 million in, we spend it down, we put the $5 million in, we spend it down.” This annual strategy has a high “flow rate” of money through the DAF, and a payout rate that would be difficult to calculate (see Heist & Vance-McMullen, 2019).

A few interviewees had used the “bunching” technique, explained above, so that DAF contributions could be itemized in 1 year, and grants could be made in subsequent years. Yael explained, We don’t have a donor-advised fund where the money just sits there; it pretty much gets spent within a year or two of putting it in there . . . We put a bunch of money in the donor-advised fund, so we could mete it out over years, but we’re just finishing that chunk of money.

In fact, all of the participants who used this strategy had short-term time horizons (2–3 years) on their DAF grantmaking/maintenance cycle.

For some interviewees, additional contributions had more to do with the timing of investments. When an appreciated asset was prime for donating, or when experiencing a liquidity event, some participants would contribute into the DAF for future grantmaking. Norm explained, I put in a little over a million dollars or something like that in stock, highly appreciated stock, so [a] liquidity event. It’s been there, and every year my wife and I will distribute $50[,000] to $100,000, sometimes more, out of that DAF. Occasionally, we put more money into it.

Notice a roughly 10 to 20 year horizon for granting out this charitable money, with intention to add more as time progresses. Jocelyn had a bit shorter time horizon, but with the same rationale: I’m roughly spending it down, but . . . when eight years, five years from now and markets are up again. and I want to take some off the table instead of selling and paying capital gains tax, I’ll move it into the DAF knowing that I want to give money away anyway. So yeah, part of it’s a market related question.

Time horizons for grantmaking on the contributed assets also varied considerably.

A few of the participants had long-term strategies for their DAF grantmaking/maintenance cycle. One approach was to use the DAF like an endowment, similar to a private foundation, where a percentage of the assets would be granted. David explained: I set myself up a budget of 5% a year. So, the fund has over 2 million dollars in it right now, so 5% a year is over a hundred thousand dollars. I try to just make that as my annual budget, because I want the fund to stay stable and even grow, if possible, which it has been doing.

Although the strategy has a long-term trajectory, it still involved short-term cycles of grantmaking and maintenance. Grantmaking in this model seemed to be more structured, and yet involved annual granting decisions similar to other DAF giving strategies. Maintenance in this model focused on reviewing market returns and records of previous grantmaking.

Phase 4: Future plans

The future plans phase included long-term plans beyond the immediate grantmaking/maintenance cycle that may include family involvement or end-of-life plans. Only Study 1 participants were asked about future plans. Among the responses, there was substantial ambiguity around future plans for their DAFs. Most of the participants were more focused on the immediate grantmaking/maintenance cycle. Some participants, however, did have plans for how their DAF use may change. Rita had an end-of-life plan with a partial remainder beneficiary and with her spouse named as successor: Then, on my death, a couple percent of the DAF will go to my alma mater . . . and the rest would just go to my spouse to grant out. I think that in the future, we will set up further successors that will probably include members of the next generation.

Rita, however, was one of very few participants who articulated clear postmortem plans for their DAF.

More of the discussion on future plans revolved around family member involvement. Janet explained her family members “can make grant recommendations. So, we ask them to do some research and to tell us who they recommend and why. And then we can all learn about it.” Zoe and her spouse revealed to their children their intention that the DAF be “passed on” in hopes “it will grow and [their children] can make grants from it.” One of the interviews included Laurie and her adult son, Michael, who were using the DAF vehicle as a tool to encourage next-generation participation in family philanthropy. Michael explained, “I feel like I inherited the practice of philanthropy, just with being given an allowance growing up, but part of that being moved to [a DAF], that my parents had set up when I was a kid.” Nevertheless, next-generation involvement cut across the various giving strategies. Adam who took an annual approach to DAF giving, Bill who had an 8- to 10-year plan for giving away a retirement bonus, and David who used it as an endowment, all had children and grandchildren involved in their DAF plans. Such overlaying and intersecting strategic considerations underscores the vast heterogeneity of individual adaptation made possible through the DAF giving process.

Limitations

As with any study, there are limitations to this research. Importantly, generalizability is not a goal of qualitative research (Ravitch & Carl, 2016); findings from our relatively small sample of 48 households should not be interpreted to represent those of all DAF users. Although we successfully recruited a diverse sample in terms of gender, DAF sponsor type, and giving amounts, our sampling approach yielded participants who were relatively homogeneous in other areas (e.g., most of our interviewees were middle aged or older, as can be expected of those who have accumulated surplus wealth), and we did not access the growing segment of workplace DAF users who are younger and lower income (Ebeling, 2018). Furthermore, we observed that our participants tended to be highly conversant in financial or philanthropic matters. We are unsure, however, if this is a result of a selection bias or if this is representative of DAF users broadly. Not all interviewees provided (or were asked to provide) DAF balances and annual contributions; future research could focus more specifically on how these values fluctuate or remain consistent over time. Finally, while we were able to achieve data saturation and identify common themes across research participants, we should also note that this does not imply perfect consistency in all themes across all participants. We have captured those areas that have achieved broad agreement and included discrepancies or dissenting opinions in our analysis. Conclusions drawn from this study should be evaluated within both the robust landscape of charitable giving literature as well as the burgeoning research on DAF usage.

Conclusions

This article provides a conceptual framework for analyzing the various decisions involved in DAF giving, as well as insights on DAF donor strategies and variation of uses. This framework and our initial insights on individual DAF uses will need to be tested and refined. The data from this study took years to compile as a result of the efforts of multiple researchers and institutions. The interview data represent an initial foray into the study of individual DAF donor behavior.

Our study confirms long-held assumptions that taxes are a strong motivator for using a DAF. We found plenty of evidence that our participants considered the tax advantages when deciding to use a DAF in the initial stage, and from time to time when making additional contributions. We did not, however, get the sense that minimizing tax liabilities was the singular motivation for using a DAF and that convenience and flexibility also motivated DAF giving. Unlike tax savings, which can be isolated to specific points of DAF giving, decisions involving convenience and flexibility seemed to pervade all phases of the process and were manifest in various ways among participants. The distinction between the tax-saving features of DAFs and other philanthropy facilitating features must be made to truly appreciate donor perspectives of giving through a DAF.

From our observations, DAFs enable donors to handle the tax implications of philanthropy up front and then allow time for the more altruistic motives or strategic considerations of giving to take precedence. Several interviewees expressed how the DAF allowed them to focus more meaningfully on their charitable giving. Jocelyn put it this way: Once I gave the money away, it made me get really serious about it . . . It wasn’t one of those things, ‘oh I’ll get around to it.’ I’ve got to figure this out, this is serious. So having the vehicle pushed me to be more strategic.

To what extent DAF donors are more strategic, or take more time, with their philanthropy is an area for future study.

The conceptual model of the DAF process presented in this article separates and organizes the multiple decisions made throughout DAF giving. Olivia succinctly concluded, “The main reason we’ve [used a DAF] is to separate the funding from the giving.” The DAF Giving Model should encourage researchers and practitioners alike to conceptualize DAF giving as a complex set of interconnected decisions that follows a logical, partly cyclical and iterative, and personally strategic process. The mere phrase of “giving through a DAF” assumes a simple intermediate transaction, yet we have found that the flexibility of DAFs allows donors to “give through a DAF” over a period of months, years, and even lifetimes. This desynchronization of the timing of giving behavior complicates both the study and management of DAFs. We have begun to identify some of the strategic approaches that donors may take when using a DAF. These variations in patterns are another area for more research and for nonprofit managers trying to understand donor behavior. Knowing that donors may use a DAF on an annual basis, contribute a large sum into a DAF from a liquidity event, or use the DAF like an endowment allows researchers and nonprofit leaders to explore these patterns in greater detail. It is important to note that donors may use more than one strategy concurrently and, when circumstances change, may shift their strategic approach.

We do not offer normative opinions about what time frames for contributing to and granting from a DAF are better or worse. We do, however, assert that the various donor strategies may be used to inform policy-making. For example, early in the COVID-19 crisis in 2020, many called for all DAF donors to empty their accounts (Cantor, 2020), and some sponsors implemented challenges to their clients to give in response to the pandemic (The NonProfit Times, 2020). Considering some of the strategies evidenced in the interviews, those who gave annually through a DAF would not be in the best position to make an emergency gift to COVID-19 response effort as they likely already had plans for where they were going to give that year (and how much) and would have to divert giving away from other causes. Moreover, should donors with this strategy have chosen to increase their giving in response to the pandemic, it may have been less convenient or tax-efficient for them to do so at that time through a DAF. With large losses in the stock market early in the pandemic, and the expanded charitable deductions that were part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act, DAF users would likely give directly to a response-related organization from a checking account instead of using appreciated assets. In contrast, those who had deposited larger sums for multiyear giving would be best situated to make COVID-19-related gifts from their DAFs because they have more resources than their immediate giving demands and more flexibility in their plans for their DAF. For those with long-term plans, it is unclear whether they would maintain their predetermined strategy or switch strategies to grant out of their reserves. Some sponsor organizations may even have policies around maintaining a balance within the DAF. More research is needed to explore how DAF donors respond during shocks to the giving environment.

In sum, DAFs facilitate hundreds of thousands of Americans giving to charity, and they have become an important philanthropic vehicle in Canada, Australia, the United Kingdom, and elsewhere. Our research suggests that donors follow a DAF giving process in which they make multiple interconnected decisions over time. The flexibility of DAFs allows remarkable individual adaptation. The giving process, which separates various elements of philanthropic decision-making, requires more thoughtful approaches to how donors, nonprofit leaders, policymakers, and researchers understand DAFs and their users.

Footnotes

Acknowledgements

The authors would like to thank the participants in this study for their willingness to discuss their philanthropic giving and those who were willing to make referals for this study. They acknowledge the Research on Religion and Urban Civil Society (PRRUCS) at the University of Pennsylvania for their partial support of the study. We are also grateful to the anonymous reviewers for their generous and helpful feedback.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received partial financial support from the Research on Religion and Urban Civil Society (PRRUCS) at the University of Pennsylvania for the research and authorship, of this article.