Abstract

This article examines the impact of the 2008–9 recession on training activity in the UK. In international terms, the UK is assumed to have a deregulated training market which is sensitive to changing economic conditions. However, national datasets and qualitative interviews suggest that, despite the severity of the recession, employers cut training expenditures by a small amount and the impact on training participation rates was minimal. Contrary to the starting assumption of a deregulated training market, the article shows that employers in the UK do not have a completely free hand and that a combination of market intervention and business requirements obliged most of them to sustain training despite the recession. These constraints included: compliance with legal requirements, meeting operational needs and satisfying customer demands. However, the recession prompted many employers to find ways of maintaining training coverage to meet these obligations, or as several respondents put it, ‘train smarter’.

Introduction

After almost 16 years of unbroken gross domestic product (GDP) growth, the UK economy entered its deepest post-war recession in the second quarter of 2008. Over the next 18 months GDP fell by 6.4 per cent. It is commonly assumed that training is among the first casualties in times of economic hardship. This view is repeated in both general and specialist commentaries (e.g. Charlton, 2008; Eyre, 2008; Kingston, 2009). Indeed, the UK Commission for Employment and Skills (UKCES) – together with the Confederation of British Industry (CBI), the Trades Union Congress (TUC) and some of the UK’s senior business leaders – published an open letter calling on employers not to cut training in the recession (UKCES, 2008). The assumption is that the UK’s market-based system of training gives little protection to training in times of recession, unlike in other parts of Europe, such as Germany, the Netherlands and France (Bellmann et al., 2011; Lloyd, 1999; Sprenger, 2011). In light of these concerns, this article examines how training activity – in terms of coverage, expenditure and characteristics – has fared in the face of the most severe economic downturn in recent history.

To address this question, the article draws on data from a range of sources. It analyses both employer and worker surveys and sets the results alongside qualitative interviews with 52 employers. The following section provides an overview of the theoretical arguments which link training to the economic cycle. It is shown that the theoretical basis for the presumed pro-cyclical character of training is contested, with some theoretical reasoning indicating a counter-cyclical pattern. The article then outlines the data sources used to shed empirical light on this debate. The two substantive sections of the article present, in turn, findings from the quantitative and qualitative analyses on which the research reported here is based. This evidence shows that, despite the severity of the recession, UK employers cut training expenditure only modestly and that training coverage held up. The article concludes by emphasizing the importance of institutional regulation of training markets and the centrality and integral nature of training to many forms of productive activity. These operate despite the comparatively deregulated nature of the UK’s training system and therefore serve to limit the pro-cyclical movement of training activity.

Theoretical expectations

While the impact of the recession on unemployment levels, vacancies, claimant counts and redundancies has been the subject of frequent analyses (e.g. ESRC, 2009; Gregg and Wadsworth, 2010; Jenkins and Leaker, 2010; ONS, 2009; UKCES, 2009), its effect on training has received relatively little serious analytical attention. By the same token, studies of training activity have rarely paid much attention to the effect of the economic cycle (see Keep and Mayhew, 2010). Nevertheless, there are theoretical reasons to expect that there is a connection, although the nature of the link is complex with the impacts pulling in different directions. Depending on the circumstances, training might be expected to increase, decrease or stay the same during an economic downturn.

Two main theoretical arguments suggest that training will fall during recessions. First, employers are likely to begin to lay off workers and/or cut recruitment. As a result, firms’ training requirements will be lowered (Majumdar, 2007). Second, cost pressures may heighten the need for short-term, quick-fix, financial solutions, resulting in cuts to ‘soft targets’ such as training budgets.

In a prolonged and deep recession, such as that of 2008–9, these pressures are likely to grow. As confidence dwindles, the incentive to ‘hoard’ and train existing workers is likely to diminish. The benefits of training become more doubtful and the costs can only be reduced so far (they still involve the wages of the trainees net of any severance costs). Costs may increasingly begin to outweigh benefits. Hence, training cuts are more likely the longer the recession. In a deep and prolonged downturn labour hoarding becomes less viable as employers’ expectations of future production are scaled back and the future costs of hiring ready-trained workers fall against the backdrop of higher unemployment (Brunello, 2009).

In contrast, training is more likely to be counter-cyclical when the recession is relatively shallow and short. Businesses experiencing a mild downturn may confidently expect to survive the downturn. Given the hiring and firing costs involved they may choose to ‘hoard’ labour, especially skilled and highly trained staff, in the expectation that workers will be needed as business picks up. This results in a period of slack, which reduces the opportunity costs (in terms of lost output) of providing productivity enhancing additional training to retained staff, who will be more productive when the economy recovers. It was on this basis that many of the wage and training subsidy schemes were introduced across Europe in 2008; the aim was to widen the practice of hoarding by cushioning businesses from the recession and encouraging them to increase training, thereby enhancing their preparedness for the recovery (Bosch, 2010).

However, the impact of the recession on training may also reflect long-term rates of profitability. In the early 1990s, even before the onset of recession, profits in the UK were falling as interest rates were hiked in order to choke off inflation. In contrast, profits were much higher immediately prior to the 2008–9 recession. Moreover, they have remained high throughout the recession as interest rates have been kept at historically low levels, spending levels have been maintained and the exchange rate allowed to fall (Gregg and Wadsworth, 2011). As a result, immediate pressures on employers to cut training were reduced, together with the requirement to lay off workers quickly (Bell and Blanchflower, 2011; Felstead, 2011).

Recessions may also increase employers’ incentives to train by intensifying competition in shrinking markets (Caballero and Hammour, 1994). If firms are obliged to compete on quality, enhanced training may be required. Moreover, if firms respond to slackness in one market by venturing into new products or processes, they are likely to need more training. The actions of employees themselves may also raise employers’ willingness to train. Quit rates fall in times of recession since alternative employment opportunities are scarce. Thus, for employers who train, some protection is offered against loss of investment through poaching. A counterpart of this argument concerns individuals who have not yet entered the full-time labour market. Deteriorating economic circumstances may encourage them to stay in education or vocational training, provided they can get the necessary funding (Dellas and Sakellaris, 2003).

Another theoretical possibility is that economic downturns may have little impact on patterns of training. Research on a previous recession in the UK suggested that some training is recession-proof, partly because a certain minimum level has to be carried out for businesses to operate (Felstead and Green, 1994, 1996). As well as the maintenance of essential production processes, these ‘training floors’ include requirements imposed by economy-wide, industry-specific and occupational labour market regulations, such as those covering health and safety at work, food standards and demonstrations of competence. These floors might also be expected to operate in subsequent recessions given that in some respects they have been strengthened. For example, although trade union density has continued to fall, unions now have more of a role in promoting workplace learning through government funding for the Union Learning Fund and the award of statutory rights for union learning representatives (Hoque and Bacon, 2008; Stuart et al., 2010; Wallis et al., 2005).

Whatever their effects on training investment levels, recessions also give employers the opportunity to reconsider the ways in which training is delivered. Employers might seek reductions in costs by renegotiating contracts with external providers or changing the form of training; for example, by taking training in-house, using experienced staff to train others, or increasing the use of e-learning. Although not new in themselves, increased emphasis on these methods may reflect pressure to make more effective use of resources as well as recognition that learning can occur in a variety of ways (IoD, 2009; Sfard, 1998). Thus, even if training expenditure falls, firms might retain the same level of training participation. More cost effective training, rather than less training, could be the outcome of recession.

Data sources and methods

Given this theoretical indeterminacy, empirical evidence is surprisingly limited. An investigation of a small sample of 20 employers and 11 providers in the south east of the UK reported that recession had had little effect on skills needs (Cox et al., 2009). Mason and Bishop (2010), on the other hand, found some evidence of reduced training coverage among 285 employers in five sectors and city-regions interviewed in 2008 and 2009. This article offers a more direct focus on the impact of the recession on training activity and its delivery in the UK.

To address this question, a range of datasets are used. Employer evidence comes from three sources. The first is the CBI Industrial Trends Surveys, a quarterly series begun in 1958. These ask member organizations about their training intentions and have done so in every quarter since October 1989. The second is the British Chambers of Commerce (BCC) Quarterly Economic Survey, which is also a membership survey. While its sample size is larger than the CBI’s (5000 versus 2000), it is a more recent survey with training data first collected in 1997. Thirdly, data are presented from the most recent National Employer Skills Survey (NESS) carried out in 2009 with over 79,000 employers taking part (Shury et al., 2010). They were asked to reflect on the effect of the recession on various aspects of training. They were asked whether the recession was positive (i.e. it had ‘increased’ the issue under discussion), negative (‘decreased’) or had made no difference (‘stayed the same’).

To complete the national picture, training data gathered by the Quarterly Labour Force Survey (QLFS) is examined. The QLFS is the main source of representative labour market information in the UK. Around 60,000 workers aged 16–65 are interviewed every quarter about a range of matters, including their experience of job-related training and education. They are asked whether they have had ‘any education or any training connected with your job, or a job that you might be able to do in the future’, first over a 13-week period and then over the four weeks prior to interview. For simplicity, in this article the four-week rate is used. The advantage of the QLFS indicators is that they provide a good guide to how work-related training and education activity have changed during the recession. To set that movement in context, however, it is important also to see how training activity fared in earlier years. For this, yearly averages based on quarterly survey data are calculated and then plotted over time.

At the end of the NESS 2009, respondents were asked whether they would be willing to take part in follow-up research – around two-thirds agreed to supply their names and contact details for this purpose. Accordingly, the article presents workplace-level evidence from 52 qualitative telephone interviews with a purposive sample of employers who took part in the NESS 2009. Those who, according to their responses to the NESS 2009, had been affected in different ways by the economic downturn were approached. They included 18 who had made cutbacks in training, 22 who had increased training and 12 who reported little change. They covered a spread of large and small establishments (36 had more than 100 employees, 16 had fewer) and industrial sectors (10 public sector, 20 manufacturing and 22 services). The sample also included employers with and without apprenticeship schemes. Telephone interviews, of approximately 30 minutes, were carried out between June and August 2010 and were fully transcribed. Most respondents were human resources (HR) or training managers; some were line managers. All were located in England, distributed across the major regions of the country. Interviews focused on obtaining employers’ narratives concerning training during and immediately following the recession.

Evidence from national datasets

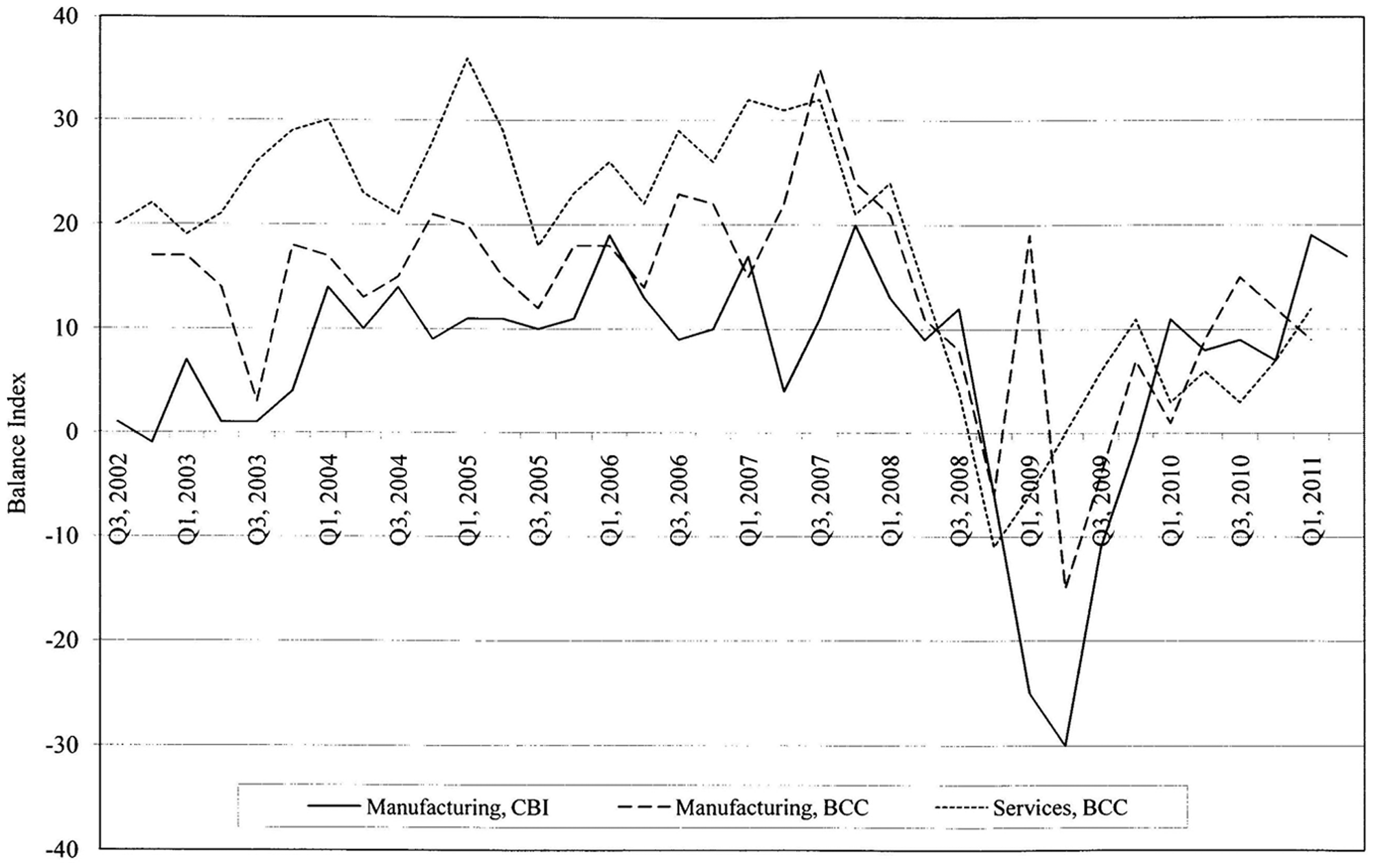

The analysis begins by examining some of the employer surveys which collect relevant training data over time. Figure 1 presents key findings for two long-running surveys of employer sentiments from 2002 to 2011. The CBI Industrial Trends Survey is forward-looking and covers CBI members in manufacturing industries. The respondents, who are generally chief executives or other senior managers, are asked, ‘Do you expect to authorize more or less expenditure in the next twelve months than you authorized over the past twelve months on training and retraining?’ The British Chambers of Commerce (BCC) Quarterly Economic Survey asks its members about changes to their training investment plans over the past three months. The BCC survey differentiates manufacturing and services, whereas the CBI survey focuses on manufacturing only. Both surveys publish a ‘balance’ index; that is, the difference between the percentage reporting an increase and the percentage reporting a decrease. Hence, they emphasize mood swings, since they do not reveal the proportions that remain stable. In addition, both series are based on the presumption that a training budget exists.

CBI and BCC Training ‘Balance’ Index, 2002–2011

Figure 1 shows the two series following a broadly similar path, with BCC employers, on the whole, a little more optimistic. BCC data also indicate that service employers are generally more upbeat than manufacturers. The negative influence of the 2008–9 recession on plans for training expenditure is unmistakeable. With one or two exceptions, the CBI and BCC results move in a similar direction, with optimism beginning to fall in the third quarter of 2008, becoming negative in the fourth quarter of 2008, remaining negative for the next two quarters, before returning to positive territory towards the end of 2009 and the beginning of 2010.

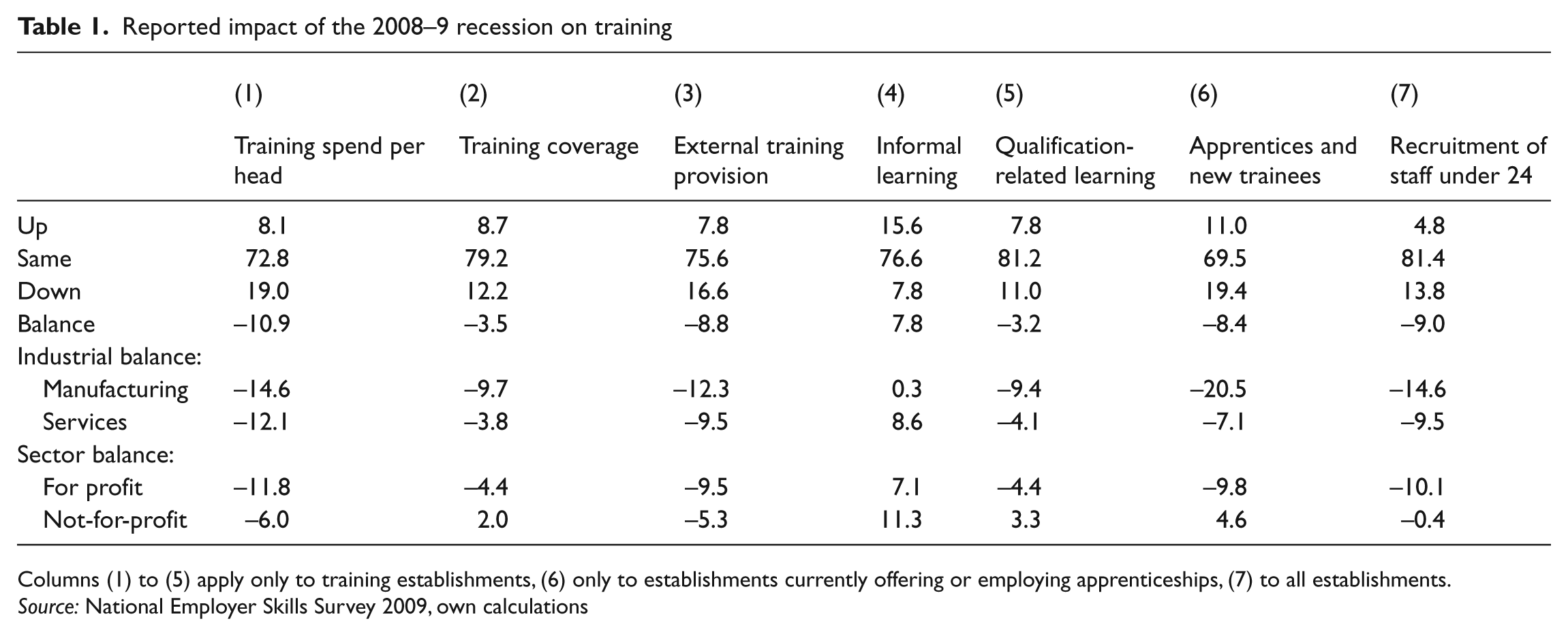

If employers’ expenditure plans were, indeed, negatively affected, what then were their subsequent actions? According to the National Employer Skills Survey (NESS) series, total training expenditure rose from £38.6b in 2007 to £39.2b in 2009, a real terms fall of 5 per cent (Shury et al., 2010: 172–3) – not such an alarming picture as suggested by employers’ earlier projections. The NESS 2009 also asked employers for their retrospective judgement of the impact of the recession on a range of aspects of training. Table 1 shows the proportions reporting an increase, decrease and no change for each aspect. In addition, it presents a ‘balance index’, defined by the difference between positive and negative responses.

Reported impact of the 2008–9 recession on training

Columns (1) to (5) apply only to training establishments, (6) only to establishments currently offering or employing apprenticeships, (7) to all establishments.

Source: National Employer Skills Survey 2009, own calculations

A large majority of employers reported that the recession had had no impact on spending per head, coverage, external provision, informal learning and qualification-related learning. A small minority in each case reported an increase under each of these headings. Nevertheless, a sizeable minority (19.0%) did report a reduction in training spending per head. A similar proportion (19.4%) said they had reduced recruitment of apprentices and new trainees. In all but one category, a negative balance index was recorded. Across all seven indicators the negative effects of the recession were felt most strongly among manufacturing establishments and those operating for profit (i.e. the private sector). Balance indices generated by the NESS 2009, then, echo those of the CBI and BCC data series. However, the CBI and BCC series do not reveal the proportions of unaffected employers. Caution should be exercised in interpreting the meaning of balance indices since they highlight overall shifts in sentiment without revealing the extent to which the bulk of sentiments remain unchanged.

One possible interpretation of these findings is that training expenditure in the UK is already low and therefore cannot be cut back. However, the results of internationally comparable surveys, such as the Continuing Vocational Training Survey, do not support this commonly held assumption. In fact, these results suggest that UK employers spend relatively more on training than countries such as Germany and Austria (Ok and Tergeist, 2003: Table 1).

Surveys of individuals’ training experiences cannot address expenditures, but can shed light on trends in the take-up of training. Do individuals report a similar picture to their employers? The Quarterly Labour Force Survey (QLFS) asks respondents whether they have had ‘any education or any training connected with your job, or a job that you might be able to do in the future’. Figure 2a presents the four-week training participation rate according to employment status. From the mid-1990s the training rate for those in employment rose steadily, peaking in 2001 and 2002 at around 15 per cent, then began to fall slowly. By the start of the 2008–9 recession, the participation rate had fallen close to where it had been in the mid-1990s, at around 13 per cent. The recession, therefore, is invisible in these data, with the slow downward participation trend continuing throughout the decade. A similar picture of rise and fall also characterizes the participation rate of those not in employment, although in this case the peak was reached in 2005.

Training rate by employment status

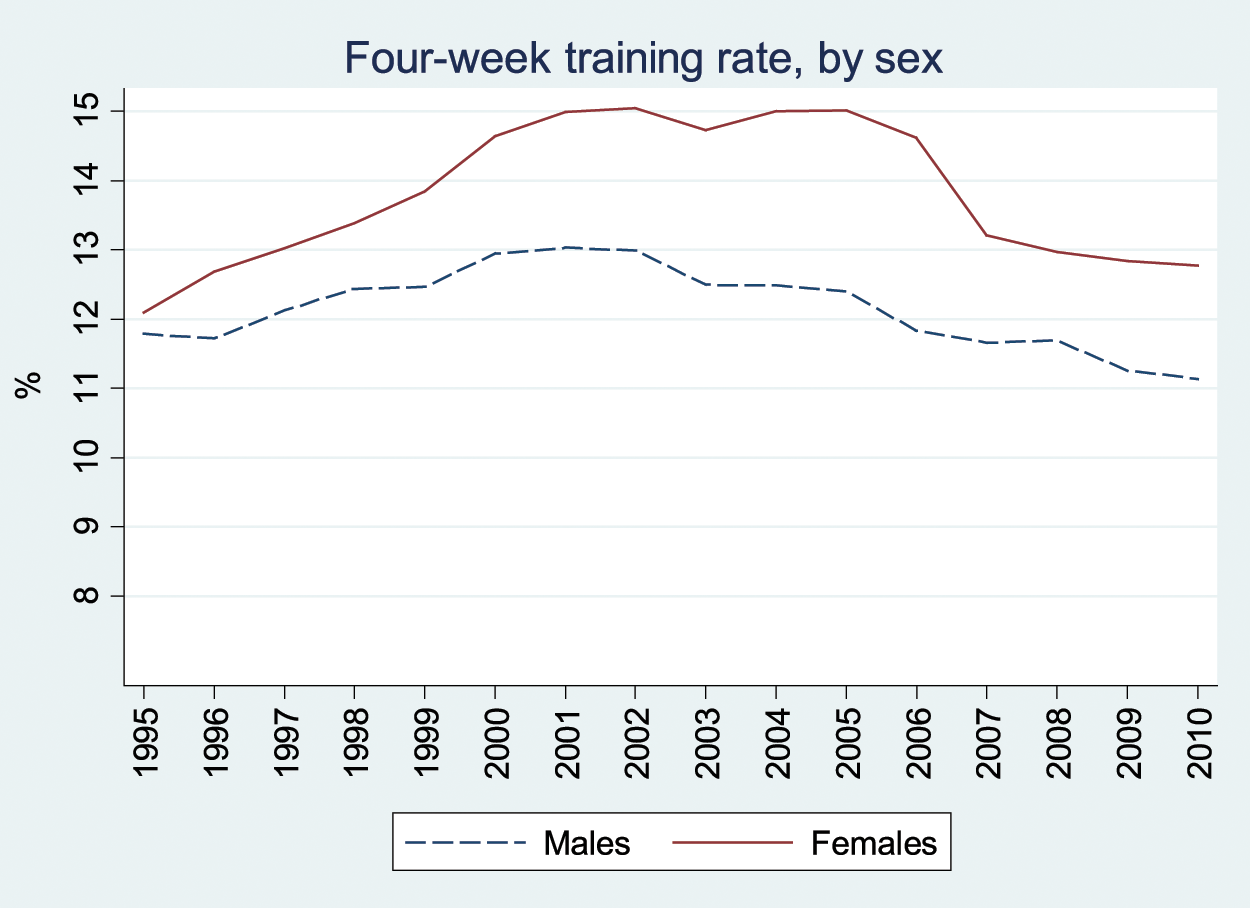

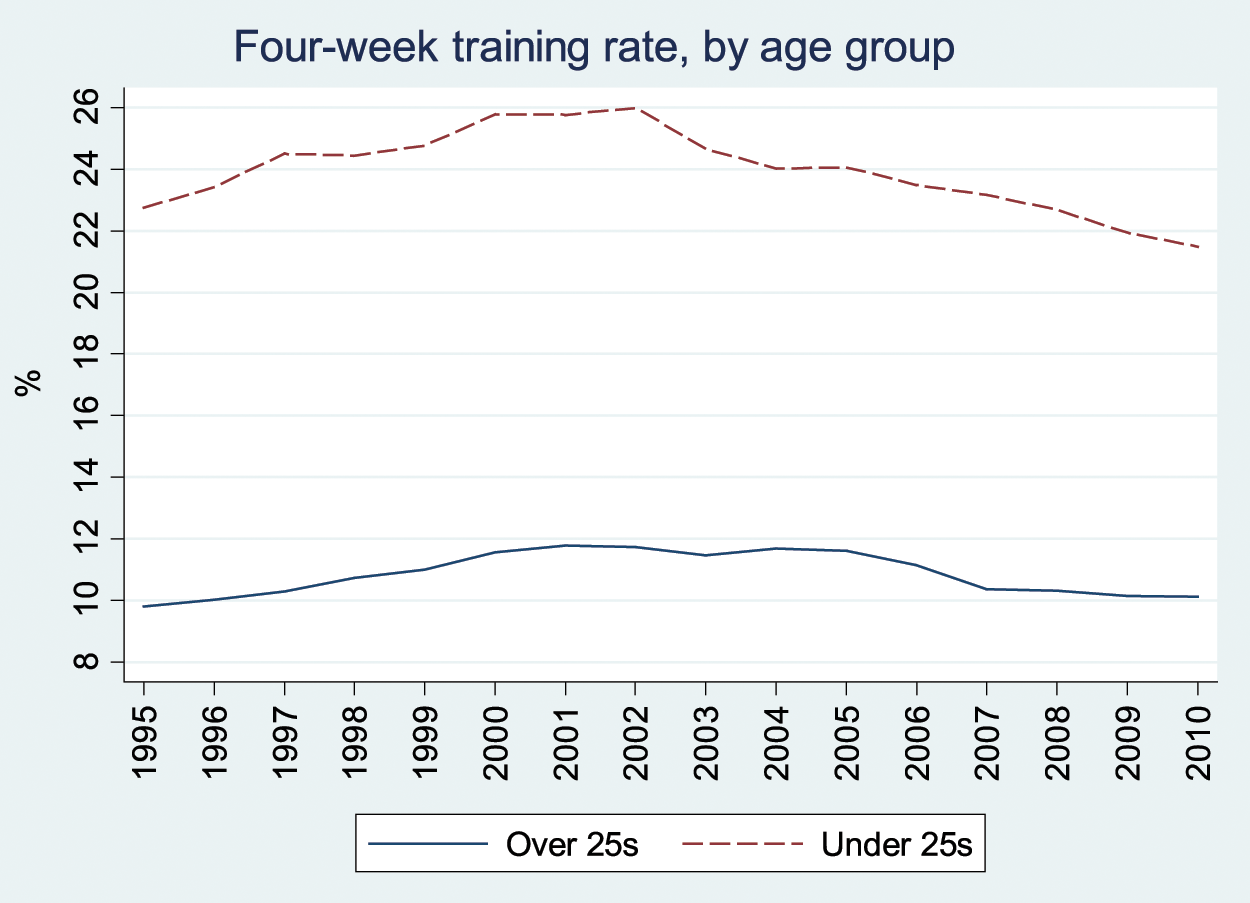

It may be anticipated that the impact of the recession on training affects some groups of workers more than others. Figure 2b shows the experiences of men and women: while men’s participation rate declined slowly and steadily from 2002 onwards, the decline for women began only in 2005, although the next two years saw a sharp drop. Again, however, there is no evidence of the recession. The patterns are also similar by age group with little noticeable recession-induced change in training rates among those under 25 compared to those over 25. The training participation rate of the young has declined since 2002 and continued to do so through the recession; the participation of those 25 and over declined since 2005 and hardly changed during the recession, remaining close to 10 per cent (see Figure 2c).

Training rate by sex

Training rate by age

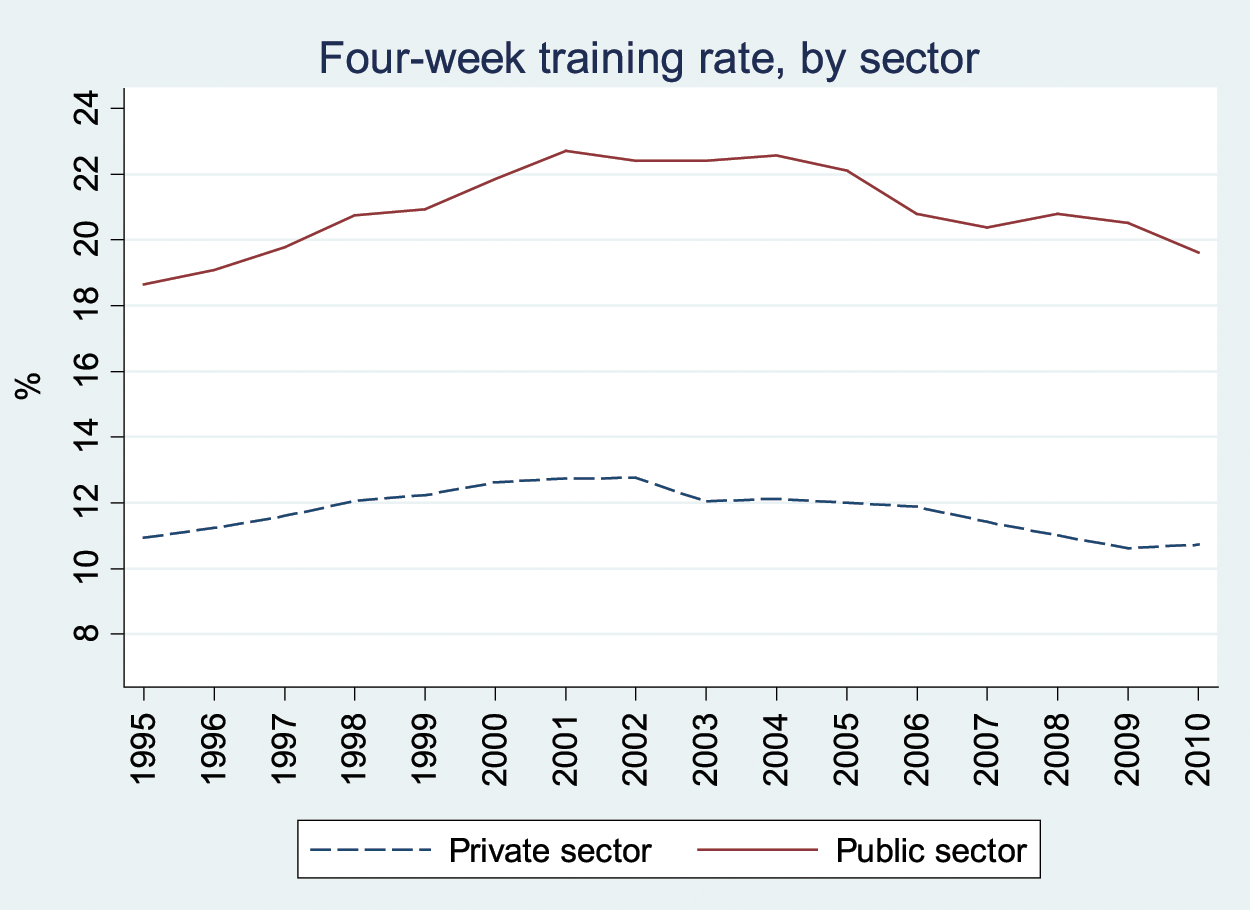

Training rate by sector

One area where the recession may have been having a somewhat greater, though as yet still small, impact is the public sector, where training participation rates have historically been considerably higher. While private sector rates barely moved in the recession, they fell in the public sector by nearly a percentage point (from 20.5% to 19.6%) between 2009 and 2010. This fall took place before public expenditure cuts really started.

A further piece of relevant evidence concerns the extent to which training takes workers away from their jobs (Mason and Bishop, 2010). Even though off-the-job training is not synonymous with external training, one might expect it to be more expensive than most in-house provision. Productivity is reduced while workers are away and the involvement of trainers, whether internal or external to the firm, involves cost. Off-the-job training is more commonly used for higher skilled workers. Figure 2e shows that the proportion of off-the-job training steadily declined from the mid-1990s, down from 73.0 per cent in 1995 to 61.1 per cent in 2010. The decline during the recession is largely a continuation of this trend.

Training that is off the job

The analysis suggests that the apparent differences between macro-level datasets can be reconciled through an examination of their provenance and the ways in which they are reported and used. Notwithstanding the experience of a significant minority of employers and the fears expressed in employer attitude surveys, on balance the data do not suggest that there has been a catastrophic overall decline in employers’ commitment to training. Furthermore, surveys of individual workers suggest that a slow decline in training activity has characterized most of the first decade of the 21st century and that this trend did not abate during the recession.

Qualitative evidence

National data-sets, then, suggest there has been some reduction in training expenditure in real terms but not much deviation in training coverage. In this section, the article examines employers’ lived experience of these changes, drawing on the findings of qualitative telephone interviews with NESS-participating employers.

The sample was designed specifically to highlight differences. Indeed, the interviews strikingly illustrate that the length and intensity of the 2008–9 recession was not uniform across the economy (cf. Artis and Sensier, 2010; Jenkins and Leaker, 2010). For some respondents – such as those in construction-related industries, heavy and light engineering and producers of luxury commodities and services – bad times had come early, hit hard and stayed long. Other parts of manufacturing, such as aspects of staple food processing, had been virtually unscathed. Financial and legal services had experienced some downturn but were weathering the storm and experiencing modest recovery in mid-2010. Experiences within the public sector were also mixed. Some public sector organizations had experienced long term retrenchment for several years prior to the economic crisis and a few had cut training in the recession. Most, however, suggested that 2008–9 had not been a time of exceptional difficulty. Rather, it was the spending reviews launched by the in-coming Coalition government that presented them with massive and immediate challenges to their expenditure plans. Both public and private sector organizations with long contracts had, thus far, avoided the worst effects of the downturn, although some were anticipating bleaker conditions in the future.

Many of the respondents echoed the view, discussed above, that training budgets are soft targets in times of economic hardship. Nevertheless, interviewees were virtually unanimous in saying that training should not be, and had not been, cut readily or willingly. In addition to awareness of their statutory obligations, they expressed a widespread belief in the strategic contribution of training to productivity.

Those organizations struggling for their very survival (about a tenth of the sample) had cut training to the bone, at least in the short term, and pushed it into the background. A number of heavy engineering plants were a case in point. At the other extreme, a similar proportion of the sample had significantly increased their spending on training during the recession. These included some organizations that had been untouched by the downturn but also some that increased training for reasons discussed below. Organizations between these two poles, a clear majority of the respondents, had modified their training regimes without entirely abandoning them. They typically reported some retrenchment in expenditure, often as part of general cost-cutting. The extent of cutbacks varied but generally the consequence was for some ‘nice to have’ programmes to be reduced or lost; for example, sponsored external courses for middle managers. However, respondents also expressed their commitment to the maintenance of training coverage, not only with respect to statutory minimum training and mandatory continuing professional development, but also for longer-term skills enhancement and succession planning. Even in organizations that had suffered redundancies and short-time working, some efforts had been made to protect and preserve training.

Interviews revealed a range of reasons for organizations, struggling with the impact of recession, to continue to train their workforces. Prominent among these were: external regulations, managerial imperatives and cost control strategies.

Training programmes required by statutory provisions, mandatory codes of conduct and legal regulations were indispensable to routine operations. Organizations differed in the extent to which they were subject to these pressures but most encountered ‘training floors’ of this kind (Felstead and Green, 1994). In some low-skill manufacturing enterprises they were largely confined to such basics as health and safety, fire drills and first aid. More frequently, they involved training in specific aspects of business operations, often with periodic updates, such as manual handling, food hygiene, fork lift driving, welding and so on. Some industry bodies and occupational associations had developed operating standards that created an on-going need for training. Staff engaged in aspects of construction, electrical installation and shop fitting required certificates before they could enter particular kinds of premises and sites. Among organizations providing professional, medical and technical services, training floors included more extensive and detailed provisions, monitored by regulatory bodies that prescribed requirements for routine practice and continuing professional development. Continuous change in codes and regulations applying to professionalized occupations generated further training needs.

Another source of external regulation, which sustained training regimes in some organizations, came from customers. Supermarkets, for example, required their suppliers and their suppliers’ suppliers to operate training regimes that went beyond minimum legal compliance. Those respondents who had increased training substantially during the recession included food manufacturers who had recently won large contracts with national retail outlets. The interviews suggest that where relations of production are dominated by end purchasers of goods and services, the trajectories of training regimes, in good times and bad, are shaped by training floors defined by horizontal as well as vertical constraints within the overall productive system (cf. Felstead et al., 2009).

In some organizations training had become deeply embedded in the legitimation of managerial controls and the maintenance of the wage-effort bargain. Those emphasizing employee participation, consensual decision-making and team working were prominent among these. So-called behavioural health and safety training represented one such approach. In these circumstances, it was difficult to cut back on training without unravelling managerial relations more generally. Training was said to prompt feelings of ‘ownership’, ‘responsibility’, ‘family’, ‘employee engagement’, ‘social skills’, ‘behaviours which we’re expecting people to display in the workplace’, ‘responsibility for developing themselves’, ‘attitudes rather than practices’ and ‘a counter angle to redundancies’. In addition to transmitting knowledge and skills, training was overtly directed towards generating motivation, inculcating discipline and fostering mutual surveillance in the workforce. It functioned as a channel of negotiation and communication, including with trade union representatives.

Respondents across the sample suggested that the quality of products and services was central to their market competitiveness, which in return reflected their investment in training. This edge became more, not less, significant when customers were hard to find during a recession. More specifically, however, for some of the organizations interviewed sustaining training coverage was a crucial aspect of their strategies for controlling costs of production through the management of the labour supply. Radical deviation from training programmes threatened market competitiveness and viability. Training enabled these organizations to acquire and retain labour more cheaply than their competitors, thereby keeping overall costs down. This was achieved by taking on talented but unqualified individuals and training them on the job. Where the credentials they obtained were specific to the organization, workers became locked into the company, at comparatively lower rates of pay, even after they had become skilled.

A widespread concern among respondents in manufacturing industry was that older workers taking retirement, or voluntary redundancy, were taking with them corporate memory, local technical knowledge and long-established skills. Although higher unemployment had made it easier for some to recruit in the short term, employers in engineering and related enterprises spoke of on-going skills shortages. Some had initiated apprenticeship schemes in response, although those in the south east of England were encountering difficulty in attracting suitable applicants. Some hard-pressed organizations in the sample had stopped taking apprentices but most were loath to let such schemes fall into disrepair, even if it meant taking on apprentices at the same time as, or shortly after, making redundancies. Those with their sights beyond immediate survival saw training as indispensable to pressing medium-term issues surrounding succession planning.

Some theorists argue that economic downturns are periods when firms are able to upgrade technology and that this, in turn, generates training needs. The qualitative interviews did not uncover much evidence of technological innovation, other than routine upgrading of IT. The interviews did, however, suggest that government funding for training had been of significance in maintaining coverage. Even organizations under severe economic pressure made use of these provisions.

The general pattern among the respondents, then, was – in line with the analysis of national datasets – for a retrenchment in training expenditure to be accompanied by a commitment, as far as possible, to maintaining training coverage. As a result, many were actively and consciously seeking more cost effective ways of delivering training. They expressed their thinking in phrases such as: ‘training smarter’; ‘doing more for less’; ‘a bigger bang for our buck’; ‘being creative with it’; ‘looking for a different way of doing training’; ‘spending more wisely’; ‘focus that pool of money’; ‘a cost effective way’; ‘getting it done in a different way’; ‘being pretty clever in looking at it’ and so on. Despite their heterogeneity, this approach had drawn the respondents towards a common package of measures. Notwithstanding differences of functions, processes and markets, a broadly similar shift of emphasis in training programmes was apparent across the sample. In most cases this entailed enhancing existing provisions and trends, rather than inventing from scratch. Moreover, the extent and form of this agenda reflected the circumstances of different industries, businesses and enterprises. Nevertheless, in organizations engaged in activities as varied as industrial manufacturing, light engineering, food processing, construction, retail, health care, education, professional services and public services, comparable approaches to maintaining training coverage were being adopted. These developments can be summarized as: focusing training on business needs; shifting from external to in-house provision; and increasing the use of on-line and e-learning.

A widespread response had been to adopt more systematic and parsimonious forms of administration of training resources, in order to focus training more tightly on proven business needs. Respondents spoke of: ‘insuring that we’re not wasting it’; ‘insuring that it’s absolutely focused’; ‘administered a bit better now’; ‘an awful lot more stringent’; ‘making better use of it’; and ‘we don’t waste money’. In some cases, this had enhanced the role of training managers and HR departments and/or senior corporate managers, in determining the distribution of dwindling training funds. Across the sample, respondents suggested that during the boom years, training had not always been allocated on the basis of rigorous cost-benefit analysis: ‘it was sometimes a bit hit and miss’, ‘it used to be very much ad hoc’, ‘just do things for the sake of it’. It was said that access to training had often previously been in the gift of local managers, particularly in organizations without dedicated training budgets, who did not necessarily have a strategic perspective on the organization’s overall needs. The quality and relevance of contents and delivery had not always been stringently evaluated. Repeatedly, respondents said that this was no longer the case.

Many organizations had not only become more systematic in allocating training but had also reshaped the mode of delivery. A common development had been, for economic reasons, a shift away from the use of external providers towards greater reliance on in-house trainers and, in some cases, in-house qualifications: ‘we started to concentrate more on in-house’; ‘there’s a lot that’s done in-house where we used to buy it in’; ‘we’re having to use what you’ve got’; ‘it’s effectively free, it’s common sense’; ‘we’ve spent more in-house’; ‘it’s all internal training we do at the moment’; ‘because it’s in-house it costs less’; ‘train a trainer people’; ‘we won’t be paying an external company’; ‘we produce the learning and it costs us less money’; ‘if people can do it in-house, by using internal skills, well that’s the way to go’. Commonly, this involved the incorporation of training responsibilities within the regular occupational roles of some managers and workers. A shift to in-house training could itself generate training needs, as regular staff adopted new tasks. However, increased in-house instruction and training of trainers was more suitable in some industries, and for some kinds of workers, than others. It was most easily achieved where training could be ‘Taylorized’. It was less applicable, though still deployed, where training focused on technical practices and professional skills. Obtaining assessed credentials also often continued to require recourse to external trainers.

Where in-house provision was not possible, the experience of the recession had made a number of respondents determined to reconfigure their relationships with external providers. They recognized their power within the productive system vis-a-vis all those who provided them with services, including external trainers. This was reflected in a robust willingness to renegotiate training prices and mode of delivery. Economies were made, and control over quality enhanced, by requiring external trainers to come on-site rather than sending employees away. Group and block bookings further reduced costs. Respondents in industrial manufacturing, food processing and legal, financial and professional services commented on these developments.

Some interviewees reported that the impact of the recession had accelerated the introduction of on-site e-learning programmes. Initial costs were a barrier for those in businesses and industries that had not previously invested in IT facilities. However, organizations that had developed suitable facilities in sufficient quantities perceived e-learning to be a cheap, standardized, cost-cutting and highly flexible mode of training. In some organizations, e-learning was associated with an expectation that at least part of the training would be done in employees’ own time and on employees’ own computers, thereby effectively shifting some of the costs onto workers themselves.

Conclusion

While existing literature provides some theoretical insights into the likely impact of recessions on training, the answers given are indeterminate and contingent on factors such as the severity and length of the recession, the financial health of companies both before and during an economic downturn, pressures to maintain training activity and the nature of the training provided. Depending on their specific circumstances, during an economic downturn firms may increase, decrease or stabilize their investment in training. This article has shown that for a variety of reasons, including government regulations and the centrality of training to productive activity, much training which goes on in the UK is a ‘must have’ item underpinned by a variety of ‘training floors’. However, the delivery of training is susceptible to change with the 2008–9 recession accelerating moves towards ‘smarter’ forms of training delivery.

The article has also shown that employers’ sentiments, especially when presented as balance indices, are sensitive to the economic cycle and can give an exaggerated impression of changes in perceptions, plans and behaviour, while disguising the fact that a majority of employers anticipate little or no change. Results from the National Employer Skills Survey 2009, for example, indicate that cuts in training expenditures were not as severe as feared. Although a minority of employers had cut expenditure and coverage as a result of the recession, most reported no significant change and some had even increased their commitment. Training expenditure in real terms fell by only 5 per cent between 2007 and 2009. Only a very small balance of companies indicated reductions in training coverage as a result of the recession, although some reported declining use of external providers. The limited impact on coverage is confirmed by the analysis of Quarterly Labour Force Surveys, which shows a slow decline in training from a peak in 2001–2, rather than a crash at the end of the decade.

The respondents’ narratives confirmed this account as well as providing a richer account of how and why this was achieved. Many employers had reduced their training expenditures, a few drastically, but most had found ways of maintaining training coverage. An overwhelming majority recognized that their enterprises were subject to a range of ‘training floors’; that is, forms of training which are indispensable. These included compliance with legal requirements, meeting operational needs, countering skills shortages, addressing market competition, fulfilling managerial commitments and satisfying customer demands. As a result, employers reported a widespread reluctance to dispense with training altogether and a determination to defend its ‘must have’ elements. Combined with some instances of increased coverage, it is possible to see how the recession is invisible in aggregate training statistics.

Employers achieved this outcome through a package of measures that a number of respondents referred to as ‘training smarter’. This involved: tightly focusing training on business needs; increasing in-house provision of training; drawing on members of the regular workforce to deliver training; renegotiating terms and relationships with external trainers; increasing the use of on-site group training; and, enhancing the role of e-learning. These measures are not new, but the interviews detected a shift towards greater use of this approach. This finding is consistent with the idea that sharp recessions are occasions for renegotiating traditional relationships, in this instance primarily with external training providers.

Although some disagreed, most of the respondents claimed that they would persist with their newly configured training regimes when the economy recovers. However, this is a matter for future research. Another crucial topic for investigation concerns the extent to which reductions in expenditure may have damaged the quality of training, despite the claims of respondents, and the extent to which the costs of training have been shifted onto employees. Moreover, the immediate effects of recession need to be set alongside the longer-term slow decline in training participation, whose consequences have yet to be evaluated in terms of its impact on the achievement of a competitively skilled workforce. Finally, by focusing on the immediate impact of the 2008–9 recession the longer-term effects have not been explored, such as the consequences for public sector workers who traditionally have greatest access to training but for whom the future looks uncertain given the announcement of savage public expenditure cuts.

Taken together, then, the evidence presented in this article suggests that a large part of training activity in the UK appears relatively immune to the effects of the economic cycle, although how training is delivered and by whom is much more susceptible to changes in the economic environment. Nevertheless, the conceptual starting point for many is that training in the UK is relatively deregulated and subject to market pressures. Accordingly, training activity would be expected to fall significantly in a recession, especially one as deep and as long as the 2008–9 downturn. However, the fact that this has not – so far at least – happened suggests that the characterization of the UK’s training market may need to be reassessed, especially if training remains relatively buoyant despite public expenditure cuts, a sluggish private sector recovery and a prolonged period of austerity in the years ahead.

Footnotes

Acknowledgements

This article is based on research findings emerging from an on-going LLAKES-affiliated research project entitled ‘Training in Recession: Historical, Comparative and Case Study Perspectives’. It is funded by the ESRC/UKCES Strategic Partnership (RES-594-28-0001-01). Material from the QLFS is Crown Copyright and has been made available by the Office for National Statistics (ONS) through The Data Archive and has been used by permission. The 2009 NESS was made available by the UKCES who also provided the contact details for the types of employers we wished to interview. The CBI data were kindly supplied on request. The following were instrumental in allowing us access to these datasets: Paul Casey, Susannah Constable, Ben Davies, Katie Gore, Nicola Grimwood, Christopher Taylor and Jonathan Wood. However, none of these individuals nor the organizations they represent are responsible for the analysis reported here.