Abstract

India has set itself a long-term goal of providing universal health coverage for all its citizens and over the past few decades, significant progress has been achieved by the government, towards meeting this goal. But, due to funding inadequacy, public health infrastructure continues to suffer from perennial shortages, impacting the rural and indigent population segments the most. As a consequence of these shortages, nearly 70% of health spending is borne by households, out-of-pocket sources, and delivered by private health care facilities. This scenario usually leaves the families impoverished and in debt, as private sector medical costs are mostly unaffordable. Universal health coverage in India is, hence, severely constrained by resource shortages and affordability. Health insurance, which has made a presence in India over the past decade, can deliver a solution to the above challenges. While, government health insurance schemes have demonstrated varying degrees of success, funding shortfalls have constrained their expansion plans. Private health insurance, on the other hand, can recalibrate their approach and play a significant role in spreading universal health coverage. By developing a strategy of addressing primary care needs and intelligently coexisting with public health insurance, private health insurance can provide an immense boost to universal coverage, by providing affordable health care access for all Indian citizens.

Introduction

The goal of universal health coverage, as defined by the United Nations, is to ensure that all people obtain the health services they need without suffering financial hardship when paying for them. This requires a strong, efficient, well-run health system; a system for financing health services; access to essential medicines and technologies; and a sufficient capacity of well-trained, motivated health workers. 1

Several countries have pledged to deliver the above mandate to their populations through either government action or private partnerships. While several countries have improved their health indicators, each country has faced challenges either in infrastructure and resources or in the case of developed nations, cost escalations and excluded indigent segments.

India, with around 20% of world's population, has also ambitiously set itself universal health care goals and health is increasingly becoming a major area of government focus. While government is investing in expanding the public health infrastructure, traditionally India has had a rich legacy of private health care services. Even with both government and private infrastructure, access to quality healthcare is still a distant dream for vast segments of the population. While health care infrastructure shortfalls are acknowledged, affordability for medical care needs is another big hurdle for the population.

Health insurance, both government sponsored and private, is a recent initiative in India and can play an important role in addressing affordability and consequently access to health care. In this paper, the author argues for a wider role for health insurance and makes suggestions for increased role of private health insurance, given the critical limitations on government funding. Private health insurance, with suitable changes in their business and market strategies, can play a crucial enabler role in the goal of achieving universal health care for India's teeming population.

India's health care landscape

Historically, the health policies in India were integrated with the Government's national five year development plans. During the initial decades of independence, the focus was on basic health aspects such as water supply and sanitation, control of malaria, rural health units, services for mothers and children, health education and training, self-sufficiency in drugs and population control.

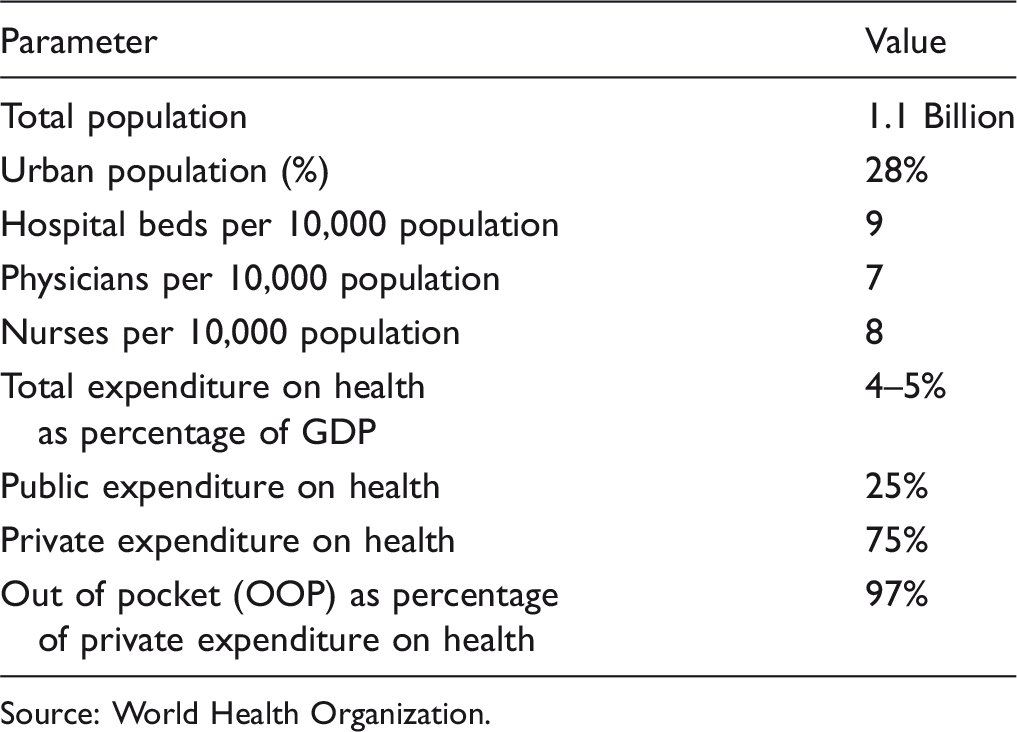

A few key macro health indicators for India.

Source: World Health Organization.

The existing National Health Policy, which has set the vision for health care delivery, envisages a three-tier structure comprising the primary, secondary, and tertiary health care facilities to bring health care services within the reach of the people. The primary tier is designed to have three types of health care institutions, namely, a sub-centre (SC) for a population of 3000 to 5000, a primary health centre (PHC) for 20,000 to 30,000 people, and a Community Health Centre (CHC) as referral centre for every four PHCs, covering a population of 80,000 to 120,000. An SC is the first peripheral contact point with the rural community and it is staffed by one female auxiliary nurse and midwife and one male health worker and one lady health visitor for six such SCs. The PHC is the first contact point between a village community and the medical officer and it is staffed by a medical officer and 14 other staff. It acts as a referral unit for six SCs and has four to six beds for patients. It performs curative, preventive, and family welfare services. The CHC is the third level of rural health care and addresses a population of 120,000. It is supposed to be staffed by four medical specialists (surgeon, physician, gynaecologist, and paediatrician) and supported by 21 paramedical and other staff. It has 30 indoor beds with one operation theatre, X-ray and labour room and laboratory facilities and serves as a referral centre for four PHCs. 5

Next to the primary tier, there are the district and sub-district hospitals which function as the secondary tier for the rural health care, and as the primary tier for the urban population. The third tier (tertiary care) is provided by specialty health institutions in urban areas which are well equipped with sophisticated diagnostic and investigative facilities.

Even as this infrastructure has provided significant improvement in health indicators, it is still underfunded with significant shortfall in both infrastructure availability and staffing (at district hospitals).6,7 This shortfall is further compounded by the wide disease spectrum and burden in India. India has a high incidence of infectious and communicable diseases (such as malaria, tuberculosis, leprosy, diarrheal diseases, HIV) and non-communicable diseases (such as cancer, diabetes, heart and kidney diseases, accidents and injuries). While in earlier periods, communicable diseases accounted for most of the morbidity in the population, currently non-communicable diseases have also evolved into major public health problems and accounted for 60% of all deaths. 8 Chronic diseases and injuries continue to be the leading causes of death and disability in India and are projected to show pronounced increases in their contribution to the burden of disease during the next 25 years. Most chronic diseases are equally prevalent in poor and rural populations and often occur together. Although a wide range of cost-effective primary and secondary prevention strategies are available, their coverage is generally low, especially in poor and rural populations. Much of the care for chronic diseases and injuries is provided in the private sector and can be very expensive. Apart from these shortfalls, the audit of these programmes has thrown up significant drawbacks that have adversely affected the functioning of the public health system. 9 These weaknesses in India's public health care delivery systems have resulted in poor reach of quality health services and inadequate financial risk protection against health care costs. The common citizen in India receives low value for money in terms of the quantity and quality of health care services in the public sector and as a result, most Indians access private health care that is expensive. This has generated an overwhelming demand for private sector health care services. An estimated 54% of the medical institutions, 75% of the hospitals, 51% of the hospital beds, 75% of the dispensaries, and 80% of all qualified doctors are in the private sector, and given the demand, there is a continued growing interest for private groups to enter the Indian health care market and set up provider chains. 10

The most significant impact of this skewed demand for private health services (in conjunction with the inadequate spend in public health services) is reflected in the nature of funding on health care. As shown in Figure 1, most of the health care funding comes from household OOP sources.

11

Source of healthcare funding in India.

While limitations in the system force the citizenry to towards private health care, affordability is a major impediment in India's universal health care roadmap. Given that India's monthly per capita income 12 is less than US$136, OOP medical costs are simply unaffordable for a majority of India's population. These expenditures are hence, typically financed by borrowing and the financial impact of medical treatment for diseases on individual households is severe, with either families resorting to asset mortgages and children having to discontinue schooling and take up employment to provide an additional source of income.

In summation, India's health care follows a dichotomous model that delivers high-quality health care for the high-income urbanised population, whereas for the rural and less affluent sections, which constitute almost 75% of India's total population, health care services remain out of reach and remain a significant hurdle to the goal of delivering universal health care.

Given this underfunded health landscape, health insurance can play a key role in meeting the funding shortfalls and ensuring equitable access to quality health care for a wide segment of the population. This paper analyses the issues facing health insurance in India and offers suggestions to help it play a role in fulfilling the universal health care goals of the country.

Health insurance in India

As discussed above, despite health being a key government ministry, majority of India's health infrastructure is in the private sector and more than 70% of health care expenses are met by consumers and not the government. Given that medical costs are unaffordable for a majority of India's population, having a wide spread health insurance net is critical in ensuring equitable health care for all.

India began its health insurance journey almost 70 years back with employer health insurance programmes such as the Employees' State Insurance (ESI) and Central Government Health Scheme (CGHS).13,14 Subsequently, retail commercial health insurance was introduced in India by the government-owned general insurers as a standardised annual indemnity product in mid 1980s, with a view to providing alternate financing options to members and helping them access better quality health care. Currently, with the increased liberalisation of the insurance industry, many private players have entered the health insurance market resulting in increased awareness and growth of health insurance,

15

as shown in Figure 2.

Health insurance premium in India (US$ Millions).

Even as health insurance shows a steep growth, the majority of the health insurance members in India are still covered under employer programmes or welfare schemes. Employers in both the public and private sector offer employer-based health insurance schemes for reimbursement of employee's health expenditure. To address health coverage for the common citizen, the Rashtriya Swasthya Bima Yojana (RSBY or the National Health Insurance Scheme) was launched in 2008, as a central government initiative. RSBY provides health cover to below the poverty line (BPL) households, with beneficiaries entitled to secondary level inpatient care up to an annual sum of US$440 for a range of diseases; even pre-existing conditions of up to five members in a family are covered. Additionally, to address rural and below poverty population, the government provide social health coverage through the NRHM and at the state level through health insurance schemes. While NRHM attempts to ensure universal coverage through government funding from tax sources, the RSBY and the state health insurance schemes provide health coverage through insurance mechanisms. In addition to the above programmes, several NGOs also provide community insurance schemes to help the underserved and remote population. 16

Currently, only 32% (or 380 million) of the total population of India is covered under the various health insurance schemes, with the majority covered under either government or employer programmes, with commercial private health insurance having around 6% penetration of the country's population as shown in Figure 3.

Population covered under health insurance plans (in %).

Review of health insurance schemes in India

Currently, there are three central government health insurance schemes, several state government and rapidly growing private insurance markets. Of the government schemes, the CGHS covers largely the civil servants, ESI addresses the organised/formal sector employees, and RSBY (and the state government schemes) facilitates health care services to rural and/poor population. While CGHS and ESI are governed by employment, the RSBY and other state government health plans are run by the ministry of health. Overall, RSBY uptake has not been very high and the enrolment of BPL families is lower than expected and has not succeeded in providing financial protection to the poor. 17 Moreover, enhancing covered medical expenses has not helped address universal coverage. RSBY continues to be essentially a catastrophic health insurance scheme that promises access largely to specialist medical care at the secondary and tertiary levels. 18

The performance of private health insurance is definitely more positive having achieved a penetration of 6% of the population. But despite the increased penetration, the private health insurance industry in India is characterised by lack of innovation and significant operating overheads, and the sector has not evolved significantly enough so as to play a major role in the country's universal health policy. Moreover, despite showing good growth in premium income, the industry has only recently turned profitable, after several years of operating at over 100% incurred claims ratios.

Role of health insurance in delivering universal health care

While it is recognised that universal health care in India has a significant ‘last mile’ problem due to public infrastructure and resource shortfalls, health insurers can step up and address key gaps in financing health services and improve access to essential medicines and services.

A look at a few other countries and their strategy of leveraging health insurance to deliver universal health coverage has lessons for India as well. In Russia, one meaningful tool to establish universal health care is the government's guaranteed health package, which is covered by the mandatory medical scheme. The scheme specifies free-of-charge services to include consultation with a GP or specialist and two or three diagnostic procedures. 19 Thailand's public health insurance scheme provides treatments within a defined benefit package to registered members for a co-payment of US$0.80 per chargeable episode. This schemes were able to rapidly address close to 96% of the population, ensuring universal health care for the country's population. 20 In China, a system of three health insurance schemes (New Rural Cooperative Medical Scheme, Urban Resident Basic Medical Insurance, and Urban Employee Basic Medical Insurance) have covered 95% of the nation's residents by the end of 2011. 21 In Mexico, the health insurance system comprises three subsystems which are the social security system, social protection system, and the private system. The social security schemes offer different services, including health insurance and pensions, for salaried workers in the formal sector of the economy and insure about 48 million people. The publicly subsidised system, social protection system, offers health insurance to all Mexicans not covered by any of the social security schemes and insures around 58 million people. Together these two systems address 93% of the population. 22

In India as well, the government is considering a massive expansion of the RSBY scheme and plans to use the RSBY as a blueprint for universal insurance rather than starting a new coverage programme from scratch. With this expansion, the government proposes to cover not just the health needs of rural and below poverty workers, but also other indigent population segments. Towards this aim, as a first step, the RSBY operations have been transferred from the Ministry of Labour to the Ministry of Health. 23 And in the most recent budget, the government has announced the launch of a new health protection scheme to provide quality medicines at affordable prices. 24 Along with the expansion of the coverage, the government is actively pushing public–private partnership (PPP) models in the design and delivery of the RSBY programme. Under this approach, RSBY scheme has actively enabled a successful PPP model, by which although the premium burden of the policies is borne by the government, the actual insurance mechanism is offered by commercial insurers through competitive bidding. Similarly, both public and private healthcare institutions are eligible for empanelment under the scheme. 25 This PPP-based initiative towards expansion of health coverage provides indemnity-like coverage delivered by private participation, but without burdening the consumer with unaffordable premium.

While these government initiatives will take time to fully fructify, private health insurers also need to learn from these global examples. The private health insurers in India have to think beyond immediate short-term objectives and apply their skills and expertise in addressing ground level improvements. In this context, it is worthwhile to recollect Professors Prahalad and Hart's seminal report titled ‘The Fortune at the Bottom of the Pyramid’, on how firms can operate profitable businesses by addressing requirements of the low income population. 26 Their report has highlighted, with examples, how global firms have reworked their business models and captured significant market share from the world's traditionally poor population segments. The advantage that global firms have in terms of resources and knowledge can be coupled with reworked cost and distribution and alliances models so as to meet the market expectations of a low income population. Some of the widely acknowledged successes from India are from the consumer sector where today one can purchase a bottle of soda for US$0.10, a shampoo sachet for US$0.03 or stay in a business hotel at US$15 per night. 27 Health insurers need to exploit this paradigm and actively explore how to expand the market at the lower end. Currently, all private health insurers are targeting the middle class segment of the population, with indemnity products designed with typical annual premiums of around US$100 per member, with annual maximum cover of US$10,000. When compared to a mature health insurance market (such as US), the premium rates in India do not align with the overall health economics of the country. For example, the average premium in India is twice the per capita spend on health care, whereas in US the premium is half of the per capita health care spend. This kind of pricing has made health insurance unaffordable for the majority of the population and has resulted in products having a limited market acceptance and there is an urgent need for a more realistic pricing of the product, in alignment with the acceptable price points. 28 Continuing in this bottom-of-the-pyramid philosophy, there is an urgent need to formulate micro health insurance policies and schemes that are affordable to the majority of the population. With a suitable benefit plan design, it is possible, as shown in various pilot studies,29,30 to operate a commercially viable micro health plan, which can help in expanding universal care. One of the examples cited in several studies is the Yeshasvini health care programme in the Indian state of Karnataka. This is a cooperative venture between the public, private and cooperative sectors to insure the rural poor against surgical procedures. It focuses on surgical procedures the cost of which could be catastrophic for the poor households and provides a maximum indemnity coverage per person per year of approximately US$3,000. 31 Currently, Yeshasvini has grown to be one of the largest government-supported, self-funded micro health insurance schemes in India with over 3.5 million members, who make an annual contribution of US$3.50 per year. 32 While, this programme has its set of innate challenges, it has established the premise that a low premium subsidised health insurance model can vastly expand universal health coverage.

In line with the micro-insurance, health insurers need to widen their benefits. Currently health products cover only inpatient treatment. This benefit coverage has encouraged over-utilisation of tertiary care and pushes up the premium cost. Health insurers have to offer benefits that are relevant to the health burden in India. For example, benefits have to cover outpatient, drugs and preventive care programmes for both communicable and non-communicable diseases. This approach will significantly address the goal of universal health care by allowing members to address day-to-day health needs, such as a visit to the GP, an antibiotic regimen or a vaccination.

Another opportunity for health insurers is to address the plan design and introduce plans that are India specific. Indian health insurers continue to design and sell only indemnity plans and have not innovated with new models. Health insurers need to move away from the simple indemnity model and introduce products that promote risk sharing between all stakeholders. Given that consumers in India tend to pay a higher OOP component, insurers have to focus on products that include elements of member liability such as copays, coinsurance and deductibles. This approach will lower the premium cost and make the insurance products acceptable across a wide section of population, including the rural segment.

A combination of the above techniques will lower premiums and address the primary health needs of majority of the population. Several studies have confirmed the price elasticity of health insurance demand33,34 and hence lowering of premium will significantly expand coverage.35,36 By applying the metrics from these empirical studies, it is estimated that health insurance penetration in India can increase by almost 50%, if annual premiums are brought down to US$20.

Revisiting the Yeshavini cooperative health programme, the empirical data show that member contribution of US$3.50 and an equivalent government contribution have enabled rolling out a successful health insurance scheme for an annual contribution of less than US$10 per member. 37 For a private plan, this implies that even by including administrative and management overheads and a profit margin, it is possible to deliver a health insurance plan with a US$20 annual premium. Health insurers need to analyse the low premium models more critically and help expand the market coverage.

Given the Indian health scenario, health insurers can begin offering these low premium starter plans that address vaccinations and treatment for communicable diseases, preventive care interventions, GP visits and out-patient treatments, common drugs and even disinfection and sanitation needs. Such a health plan will address the major existing gaps in primary care and the government plans can kick-in to address tertiary and catastrophic expenditure needs. Apart from the wider social objective, by preventing sickness and ensuring patients stay healthy, health insurers can effectively manage their financial risk because wellness measures are significantly less expensive to the health insurer in terms of claims outflow.

Summary and conclusions

Given India's poor health indicators with wide incidences of infectious, non-communicable, chronic and lifestyle illnesses, Indian health insurers have a large social responsibility in meeting the huge funding gap in India's health care economy.

Health insurers have to innovate and provide products that have realistic and affordable premiums with basic benefits that provide interventions and incentives that address the root causes of sickness such as preventive measures, sanitation, hygiene, and wellness care.

As the industry introduces these new products, adequate care has to be taken to avoid the pitfalls associated with excessive profit maximisation and has to ensure that benefits are equitably distributed across all participants in the health ecosystem.

As the insurers move to a central structural role in uplifting India's health profile, the greatest beneficiary will be the population of the country. This approach will expand universal health coverage manifold by increasing health insurance penetration and providing health care access for major segments of the under-served population. The covered citizen will now have the confidence of being a card-carrying member of an insurance plan, which offers genuine empowerment to address his health care needs, including timely care from the private sector providers. This eco-system, once established, will be the key achievement of health insurers in helping the nation meets its universal health coverage goals.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.