Abstract

When faced with risky decisions, people typically choose to diversify their choices by allocating resources across a variety of options and thus avoid putting “all their eggs in one basket.” The current research revealed that this tendency is reversed when people face an important cue to mating-related risk: skew in the operational sex ratio, or the ratio of men to women in the local environment. Counter to the typical strategy of choice diversification, findings from four studies demonstrated that the presence of romantically unfavorable sex ratios (those featuring more same-sex than opposite-sex individuals) led heterosexual people to diversify financial resources less and instead concentrate investment in high-risk/high-return options when making lottery, stock-pool, retirement-account, and research-funding decisions. These studies shed light on a key process by which people manage risks to mating success implied by unfavorable interpersonal environments. These choice patterns have important implications for mating behavior as well as other everyday forms of decision making.

Making wise decisions for the future can be difficult. Consider that over half of U.S. households are not financially prepared to maintain their standard of living in retirement (Munnell, Hou, & Webb, 2014). Such obstacles ultimately stem from choices made when allocating resources to various areas of life: how much money to spend on luxuries versus necessities; how much time to devote to work, play, or relationships; and how much effort to expend on one task versus another.

When outcomes are uncertain—as they almost always are when making difficult decisions—people tend to spread their resources across multiple options (bet hedging). For example, financial advisers and retirement planners regularly preach the benefits of diversifying investments in order to hedge one’s bets against risk (Fidelity, 2015). Nevertheless, people (and other animals) remain sensitive to environmental fluctuations signaling the presence of opportunities and risks, and they alter their decision-making strategies in ways designed to exploit those opportunities and minimize those risks. In this research, we examined an environmental factor that is overlooked in classic decision-making theories but that plays an important role in guiding choices under uncertainty—the operational sex ratio (OSR), or the ratio of reproductively aged same-sex to opposite-sex people in the immediate environment. Does the choice to diversify or concentrate one’s resources depend on whether there are more men or more women in one’s current environment? Might particular sex ratios reverse the typical risk-management strategy of choice diversification?

Bet Hedging

Uncertain conditions are a fact of life. A formal approach to managing uncertainty through bet hedging was first developed by Bernoulli (1738/1954) and later influenced parallel approaches to allocation decisions within economics and evolutionary biology. In essence, because the fitness costs of negative events are typically greater than the fitness benefits of equivalent positive events, organisms can hedge against future adversity by trading off a concentration strategy (investing resources in a small set of high-yield options, which could result in loss of all resources) in favor of a diversification or variance-reduction strategy (distributing resources across many options, which reduces risk but also lowers potential yield; Philippi & Seger, 1989; Seger & Brockmann, 1987).

For example, diversification is useful in stock portfolios, because spreading funds across multiple companies and investment categories ensures against catastrophes brought about by the failure of any single company. Similarly, in birds, the “decision” to vary egg size and number across years and within clutches ensures against predation and ecological scarcity (Olofsson, Ripa, & Jonzén, 2009).

Whereas most examples of bet hedging in animals involve behaviors immediately related to survival or reproduction, humans hedge bets in a wide range of domains. The decision-making literature focuses largely on a particular type of bet hedging—choice diversification—which involves mitigating risk (i.e., payoff variance; Daly & Wilson, 2001) by allocating resources across a variety of options and thus following the adage to “not put all your eggs in one basket.” Choice diversification occurs because risk aversion leads individuals to spread investment across whichever options are currently available (Benartzi & Thaler, 2001; Rothschild & Stiglitz, 1971; Simonson, 1990). Under average conditions, people are generally risk averse (Kahneman & Lovallo, 1993), and thus choice diversification is widely considered the default behavior (Read & Loewenstein, 1995; Simonson, 1990). For example, people tend to allocate retirement savings and forms of distributive justice relatively equally across options and recipients (Fox, Ratner, & Lieb, 2005).

Given this default, why might people ever choose to avoid diversification and instead put their eggs in fewer baskets? Importantly, desired outcomes must be seen as achievable through diversification. Although reducing outcome variance may ensure against stochastic shocks, diversification that lowers the chance of success below threshold is ineffectual (e.g., if a large amount of resources is perceived as necessary for success, not acquiring this amount would be seen as a failure). In such situations, people may benefit instead from concentrating their investment into fewer options, even if this decision entails risk, in the hopes of passing the threshold for success. Consistent with this logic, previous studies have shown that people who are competitively more disadvantaged (e.g., participants told they are below average in intelligence) choose riskier gambles because they perceive that they are unlikely to succeed through safer, lower-risk means (Mishra, Barclay, & Lalumière, 2014).

Sex Ratios

In making decisions under uncertainty, people’s choices are shaped by fundamental goals designed to solve recurrent social challenges (Kenrick, Griskevicius, Neuberg, & Schaller, 2010). Although the human mind is adapted to face many such challenges, from an evolutionary perspective, mating-related problems and opportunities represent an especially critical domain (Maner & Ackerman, 2015), and one in which motivationally relevant cues can elicit broad changes in decision making (e.g., Li, Kenrick, Griskevicius, & Neuberg, 2012; Wilson & Daly, 2004).

One important environmental factor that affects variance in mating success is the OSR. The OSR dictates both the availability of potential mates and the degree of competition for those mates (Emlen & Oring, 1977; Weir, Grant, & Hutchings, 2011). Imbalances within the OSR can influence behaviors ranging from mating and parenting to aggression and other forms of decision making (Barber, 2001; Guttentag & Secord, 1983; Kruger & Schlemmer, 2009; Pollet & Nettle, 2008; Simão & Todd, 2003). For example, female-biased ratios are associated with decreases in marriage rates and paternal investment (Guttentag & Secord, 1983; South & Trent, 1988), whereas male-biased ratios are associated with increases in violence (Hudson & Den Boer, 2002).

Experimental manipulations of the local OSR demonstrate the plasticity of mating-relevant responses. Cuing the presence of more same-sex people, for example, increases the effort perceivers expend to view attractive opposite-sex faces (Hahn, Fisher, DeBruine, & Jones, 2014). Other studies manipulating perceived sex ratio show that OSR skew alters sociosexuality (Moss & Maner, 2016), preferences for facial symmetry (Watkins, Jones, Little, DeBruine, & Feinberg, 2012), and even the choices women make in family versus career planning (Durante, Griskevicius, Simpson, Cantu, & Tybur, 2012). Temporary changes in perceived OSR can also affect decisions less explicitly tied to mating outcomes. Griskevicius and colleagues (2012) examined spending versus saving decisions, finding that male-biased ratios motivate men to discount the future and spend more impulsively. Thus, both actual and perceived OSR skew affect a wide range of psychological outcomes, even ones not directly involving mating behaviors.

Effects of OSR depend on the direction of skew. In heterosexual populations, greater numbers of same-sex than of opposite-sex people create an unfavorable environment with respect to mating opportunities, placing a given individual at a competitive disadvantage. Conversely, greater numbers of opposite-sex than same-sex people create a favorable environment in which competition over mating opportunities is lessened. We suggest that people respond to unfavorable OSR skew by prioritizing strategies directly or indirectly associated with attracting potential mates. For example, consider a population in which there are five men for every three women. Each man must work harder to make himself stand out to potential partners. High-risk strategies may implicitly signal a person’s ambition and confidence, or they may facilitate acquisition of resources and status useful for courtship, thus helping lift individuals above the competition (Baker & Maner, 2008). One such strategy may involve a general decision-making approach in which people eschew choice diversification in favor of concentrating investment in fewer choice options.

A traditional view of bet hedging suggests that, when facing increased risk, people diversify choices to spread risk over multiple options (Benartzi & Thaler, 2001). As mentioned earlier, this appears to be the default behavior in simultaneous choice contexts and reflects people’s generally risk-averse approach to making decisions (Read & Loewenstein, 1995; Simonson, 1990). Yet situations in which one must compete vigorously for access to resources or mating opportunities elicit a general orientation toward risk seeking (Daly & Wilson, 2001). An unfavorable OSR implies increases in both intrasexual competition and the intersexual threshold for mating success. Consequently, people may perceive that risk taking is necessary (see Mishra et al., 2014). This suggests that, compared with people facing a favorable OSR, people facing an unfavorable OSR may be less likely to exhibit choice diversification and instead concentrate resources within fewer options. We evaluated this hypothesis in four studies.

The Current Research

To evaluate effects of OSRs, we conducted two studies using visual indicators of skew. In these studies, participants were asked to make decisions about lottery options (Study 1) or about personal retirement accounts and governmental financing of companies (Study 3). In two additional studies, we used news articles to manipulate OSR skew and measured investment decisions (Study 2) or decisions about governmental financing (Study 4). In Study 4, we also included a control condition to examine the relative importance of unfavorable versus favorable sex ratios, and we assessed potential psychological mechanisms. Prior psychological research on sex ratios has found mixed evidence for moderating effects of sex (Griskevicius et al., 2012; Hahn et al., 2014; Moss & Maner, 2016; Watkins et al., 2012), so we did not have strong predictions about sex differences.

Study 1

Method

Ninety-three participants 1 (40 female, 53 male; mean age = 32.0 years) from a mixed student and community sample were paid $4 to take part in a laboratory study. The study had a 2 (sex ratio: favorable, unfavorable) × 2 (participant sex: female, male) between-participants design. Participants were told they would complete a study on interpersonal memory. First, they were cued with visual indicators of either female-biased or male-biased sex ratios. They then made a choice between two lotteries, one featuring a single chance to win a high-return reward and the other featuring multiple chances to win a lower-return reward. Choice of the single-chance lottery represented the risky decision to concentrate investment in a single option, whereas the multiple-chances lottery represented the less risky decision to diversify.

To cue specific sex ratios, we first asked each participant to view a series of photo arrays featuring images of men and women who were ostensibly members of the local population. This sex-ratio manipulation consisted of a previously validated procedure that has been shown to effectively alter behaviors relevant to skewed sex ratio (Griskevicius et al., 2012). Three arrays were created, each with 18 head shots of men and women between the ages of 18 and 35 years obtained from public-domain Web sites. Participants were told that the photos came from three sources: a local dating Web site, a Web site of recent graduates of a local university living in the area, and a photographer who took pictures on the university campus.

Each participant saw all three arrays of faces. Within each sex-ratio condition, the three arrays contained 13, 12, and 14 faces, respectively, of the more prevalent sex. In the unfavorable-sex-ratio condition, each participant’s own sex was always more prevalent. In the favorable-sex-ratio condition, the other sex was always more prevalent. Participants initially saw all three arrays for 1 s each and then, consistent with the cover story on interpersonal memory, were asked to write how many men and women appeared in each array. Participants then viewed the same arrays again for 15 s each, ostensibly so they could check the accuracy of their initial perceptions. After this second viewing, participants again recorded the number of men and women, which served as a check of the sex-ratio manipulation (97% of participants were accurate in their count after the 15-s viewing period, and the other 3% were off only slightly).

As part of the cover story, participants were told they would next complete an imagination task in order to allow time to pass before a memory test (no test was actually given). They read the following instructions: Imagine you were at a convenience store and decided to play the instant-win lottery. These are the tickets you scratch off to reveal if you’ve won. Consider your choice as realistically as possible and choose whatever you would choose in real life. Note that there are no right or wrong answers, so just go with your gut for each question.

After reading these instructions, participants chose one of two options: one $10 lottery ticket for a $10,000 prize or ten $1 lottery tickets for a $1,000 prize each. Note that these two options have an approximately equal expected value assuming the same number of tickets is sold for each lottery (of course, participants may not have assumed that sales are equal). As the primary dependent measure, choice of the single $10 ticket would represent a decision to concentrate one’s eggs in one basket, whereas choice of the ten $1 tickets would represent a decision to diversify. Next, participants completed demographic measures, following which we conducted a suspicion check (no accurate suspicion was reported) and, finally, a debriefing.

Results

Experimental condition was coded to compare favorable sex ratios (men viewing female-prevalent ratios; women viewing male-prevalent ratios) with unfavorable sex ratios (men viewing male-prevalent ratios; women viewing female-prevalent ratios). 2 Additionally, participants who self-identified as bisexual or homosexual were removed from analyses because the study hypothesis made no predictions about those populations and because low numbers of these participants prevented sufficient independent analysis. 3

Lottery choices were analyzed using binary logistic regression with sex ratio, participant sex, and their interaction as predictors (Nagelkerke R2 = .156). Only a main effect of sex ratio emerged, b = 1.50, Wald χ2 = 4.851, p = .028, odds ratio = 4.46, 95% confidence interval (CI) = [1.18, 16.90]. 4 The odds of a person choosing the single $10 ticket option were 4.46 times greater following exposure to unfavorable sex ratios than to favorable sex ratios. Thus, seeing a greater scarcity of opposite-sex people led participants to choose the high-risk, high-reward option more often—putting one’s lottery eggs in one basket. Lottery choices were not predicted by participant sex, Wald χ2 = .208, p = .65, or by the interaction of sex ratio and participant sex, Wald χ2 = 1.219, p = .27.

Thus, Study 1 suggests that exposure to unfavorable sex ratios, compared with favorable sex ratios, leads individuals to choose riskier, less diversified options. This finding is consistent with the hypothesis that the competitive disadvantage implied by an unfavorable sex ratio motivates people to concentrate their choices into high-risk/high-reward decisions. However, Study 1 was limited by the fact that participants chose between only two options that varied not only in their level of diversification but also in the size of the reward associated with each choice. Consequently, increased choice of the single-ticket option may have reflected sensitivity to large rewards rather than aversion to diversification. We addressed this issue in the remaining studies.

Study 2

Method

One hundred and five participants (41 female, 64 male; mean age = 30.0 years) were recruited online from Amazon’s Mechanical Turk for a $0.45 payment. The study had a 2 (sex ratio: favorable, unfavorable) × 2 (participant sex: female, male) between-participants design. A cover story informed participants that the “People and Products” study evaluated a series of unrelated responses to social settings and decision-making contexts. To provide evidence of generalizability, we used a different manipulation of sex ratio from that in Study 1. Participants read a news article, purportedly from the Chicago Tribune, about current demographic trends indicating that the United States is becoming either more female biased or male biased. For example, participants in the female-biased condition read “Whether it’s in class, at work, out shopping or eating, people today should expect to see fewer men for every woman.” This article was adapted from one used in prior sex-ratio research (Griskevicius et al., 2012).

After reading this, participants completed an ostensibly unrelated task in which they imagined taking part in a stock-market investment pool (White, Li, Griskevicius, Neuberg, & Kenrick, 2013). In this pool, participants chose different stock packages in which to invest money. All packages included different numbers of companies but were framed as having a similar current overall value (although future performance was uncertain). Mitigating the limitations of Study 1, this design allowed a degree of flexibility in choice diversification and also held initial value constant so that sensitivity to apparent size of rewards was not an issue. Five sets of packages were displayed, with participants choosing one option from each set. For example, in one set, participants could choose to invest in 100 shares in eight different electronics companies, 200 shares in four electronics companies, 400 shares in two electronics companies, or 800 shares in a single electronics company. Choosing to invest heavily in a small number of companies reflected the relatively risky tendency to hinge one’s outcomes on the success of limited options, whereas the decision to invest in fewer shares of more companies represented the decision to diversify. Next, participants completed demographic measures (including familiarity with financial investing; 1 = not at all, 7 = extremely) and a suspicion check, and were then debriefed.

Results

Responses to the investment items were averaged across the five sets into an investment composite, with higher numbers representing a stronger decision to concentrate rather than diversify resources (Cronbach’s α = .89). A Sex Ratio × Participant Sex analysis of variance (ANOVA) on the investment composite revealed only a main effect of sex ratio, F(1, 101) = 5.21, p = .025, η p 2 = .05, 90% CI = [.003, .131]. Exposure to unfavorable sex ratios led participants to choose more shares in fewer companies (M = 2.28, SD = 0.72) than did exposure to favorable ratios (M = 1.99, SD = 0.66). That is, perceiving a scarcity of opposite-sex people produced less diversification in decision making. Neither participant sex, F = 0.002, p = .96, nor the interaction between sex ratio and participant sex were significant, F = 1.10, p = .30. Further, the effect of the sex-ratio manipulation remained significant when we controlled for self-reported financial-investment experience (mean investment experience = 3.73), F(1, 100) = 4.12, p = .045, η p 2 = .04, 90% CI = [.001, .118].

Consistent with the pattern found in Study 1, results showed that participants diversified less when confronted by cues signaling a competitive mating disadvantage. This occurred despite the fact that the initial value of concentrating one’s investment was identical to the value of diversifying that investment. Even when they possessed familiarity with the stock market, people faced with unfavorable sex ratios concentrated their investments in fewer options, which suggests that knowledge about the benefits of asset diversification did not insulate people from the effects of skewed sex ratios. Study 2 therefore provides clearer evidence of the impact of sex-ratio skew on diversification decisions. However, although the dependent measure used here did vary in the degree to which participants could diversify, it did not allow for completely free choice allocation. This issue was addressed in the next study by allowing participants to allocate resources freely across options in two types of investment tasks.

Study 3

Method

Seventy-eight participants (45 female, 33 male; mean age = 29.9 years) from a mixed student and community sample took part in a laboratory study for $8. The study had a 2 (sex ratio: favorable, unfavorable) × 2 (participant sex: female, male) between-participants design. The first part of the procedure mirrored that of Study 1. Participants were told they would complete a study on interpersonal memory and received the face-array priming task on individual computers (95% of participants accurately reported the sex ratio in each array after the 15-s viewing period).

Next, participants engaged in tasks that ostensibly allowed their memory to decay. These tasks introduced two new outcome measures that focused on the direct allocation of resources. The first measure mimicked realistic retirement-account investing by asking participants to imagine setting up a retirement account (e.g., 401k) from money withdrawn from their paychecks. As part of this process, they could choose to allocate their retirement funds among three investment-category options: stocks (described as higher risk but with the possibility of higher returns), bonds (described as lower risk than stocks but with lower returns as well), and cash (described as no risk but with little if any return, like a savings account). Participants could choose to allocate 0 to 100% of their funds to each option as long as the total summed to 100%. This procedure allowed participants to make allocations equally across categories (complete diversification), concentrate allocation within a single category (no diversification), or anywhere in between. All choices were made on the same screen.

Following this, participants completed one additional dependent measure involving investment decision making. They were told to imagine that the government was concerned that a new contagious disease would trigger a potentially deadly epidemic within the next 1 to 2 years. They then read the following scenario: Currently, 4 companies are working on a vaccine for this disease. However, they could all use additional funding to help their efforts. You are in charge of a government committee that wants to fund research to prevent this outbreak. On the next page, decide how you would like to distribute your funds among these companies. Remember, if a company receives more money they can work faster toward a cure; however, there is also no guarantee that each company will be successful.

The companies were labeled A, B, C, and D, but no other information about these companies was provided. As in the prior task, participants were able to choose to invest 0 to 100% of the funds in each company as long as the total summed to 100%. Because of the minimal information participants were given regarding each investment option, this task represents a relatively pure measure of diversification.

Finally, participants completed demographic measures (including a “yes/no” item assessing whether they currently had a retirement account) and a suspicion check, followed by a debriefing.

Results

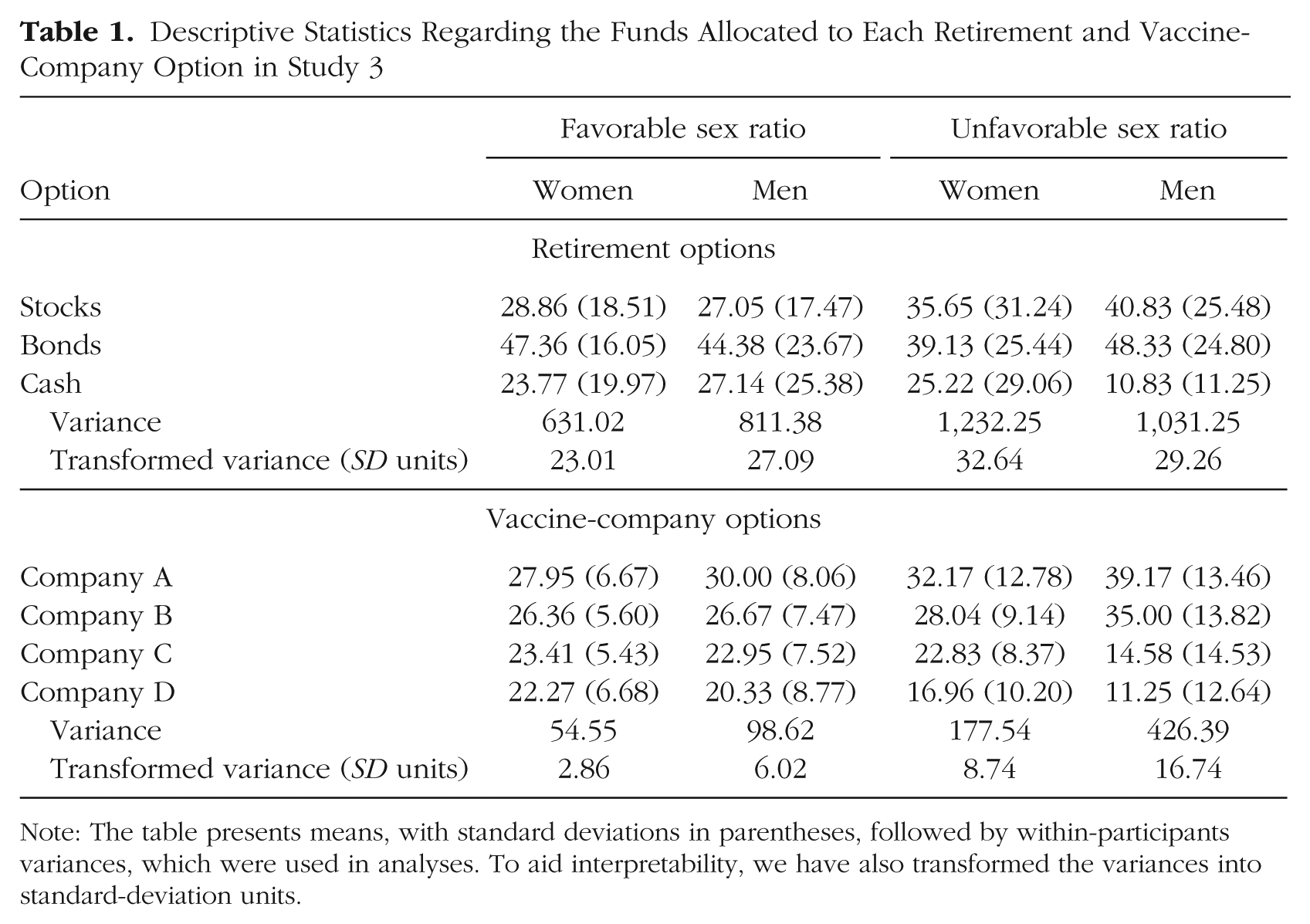

Because the goal of diversification is to increase the possibility of beneficial returns while also reducing variance across possible outcomes (Philippi & Seger, 1989), choice diversification does not merely involve choosing the lowest-risk option but instead focuses on spreading investments across multiple options. Therefore, instead of examining simple high- versus low-risk choices, we analyzed how sex-ratio skew influenced the variance in participants’ allocations within each measure. To do so, we calculated the within-participants variance of percentage invested in (a) the three retirement options and (b) the four vaccine-company options (untransformed descriptive data are presented in Table 1).

Descriptive Statistics Regarding the Funds Allocated to Each Retirement and Vaccine-Company Option in Study 3

Note: The table presents means, with standard deviations in parentheses, followed by within-participants variances, which were used in analyses. To aid interpretability, we have also transformed the variances into standard-deviation units.

These new variables represent the degree to which investment choices were concentrated in fewer options (higher variance scores) or spread across a greater number of options (lower variance scores). For example, spreading one’s investments equivalently across three retirement options (33.3% each) would result in a zero variance score, whereas concentrating most of one’s investment into a single option (e.g., 90% in one option, 5% in the other two options) would result in a much higher variance score. Because variance values are difficult to interpret intuitively, we also present the values for each test in standard-deviation units in Table 1.

A Sex Ratio × Participant Sex ANOVA on retirement-investment variance revealed only a main effect of sex ratio, F(1, 74) = 6.11, p = .016, η p 2 = .08, 90% CI = [.008, .184]. Exposure to unfavorable sex ratios led participants to invest more in fewer retirement-category options (mean variance = 1,163.33, SD = 897.25) than did exposure to favorable ratios (mean variance = 719.10, SD = 498.12). That is, seeing a scarcity of opposite-sex people produced less diversification in investment decisions. Neither participant sex, F = 0.004, p = .95, nor the interaction between sex ratio and participant sex were significant, F = 1.318, p = .26. Further, the effect of sex-ratio skew remained significant even when we controlled for whether a person possessed a current retirement account (20.5% had an account), F(1, 73) = 6.20, p = .015, η p 2 = .08, 90% CI = [.008, .188].

A Sex Ratio × Participant Sex ANOVA on vaccine-investment variance revealed a main effect of sex ratio, F(1, 74) = 14.93, p = .0002, η p 2 = .17, 90% CI = [.056, .290]. Exposure to unfavorable sex ratios led participants to invest more in fewer vaccine-company options (mean variance = 262.86, SD = 325.87) than did exposure to favorable ratios (mean variance = 76.07, SD = 187.64). In other words, seeing a scarcity of opposite-sex people produced less diversification in funding allocation, consistent with the finding for retirement investment. A main effect of participant sex also emerged, F(1, 74) = 6.31, p = .01, η p 2 = .08, 90% CI = [.009, .187], with men (mean variance = 217.81, SD = 317.25) diversifying less overall than women (mean variance = 117.41, SD = 231.10). A marginal Sex Ratio × Participant Sex interaction was also observed, F(1, 74) = 3.08, p = .08, η p 2 = .04, 90% CI = [.000, .133]. Pairwise comparisons indicated that the simple effect of unfavorable ratios was significant for men, F(1, 74) = 13.26, p = .001, η p 2 = .15, but only trending for women, F(1, 74) = 2.75, p = .10, η p 2 = .04.

When given complete flexibility to allocate resources in two realistic decision contexts, exposure to cues representing a competitive mating disadvantage led people to diversify less and instead to allocate a greater percentage of resources to fewer options. This occurred both when the options were explicitly connected to risk and return potential and when no information was provided about the choice options (the latter providing a relatively pure context to test choice diversification). Thus, unfavorable sex ratios triggered a general pattern of decision making that runs counter to the default tendency of choice diversification (Simonson, 1990).

Study 4

Method

To ensure a large sample with a relatively equal gender distribution, we recruited 150 participants from a student pool (44 female, 106 male) for course credit and 220 participants online from Mechanical Turk (124 female, 96 male) for a $0.45 payment. These two groups were combined (sample source did not moderate the reported effects), which yielded a final sample of 370 participants (168 female, 202 male; mean age = 29.8 years). We also extended the investigation by adding a no-sex-ratio control condition in Study 4. Thus, the study had a 3 (sex ratio: favorable, unfavorable, control) × 2 (participant sex: female, male) design. The procedure incorporated elements from prior studies. As in Study 2, participants read a news article that described demographic trends as becoming either more female biased or male biased. Participants in the control condition read an article detailing architectural changes in building construction as shifting from brick to stone veneer exteriors (using language that was closely matched to that used in the sex-ratio-skew conditions).

Participants then completed the (ostensibly unrelated) government-funded vaccine-research item from Study 3. As before, participants could choose to invest from 0 to 100% of the government funds in each of four companies, as long as the total percentage allocated across companies summed to 100. This task was chosen as the primary dependent measure because the minimal information given about each company makes the task a relatively pure measure of choice diversification.

Next, measures assessing the potential psychological mechanism underlying the predicted effects were given. These included a reward-responsiveness scale (e.g., “If I see a chance of something I want, I move on it right away”; Van den Berg, Franken, & Muris, 2010), two mating-impression-management items (e.g., “To what extent do you care about impressing potential romantic partners?”; Griskevicius et al., 2012), two intrasexual-competitiveness items (e.g., “To what extent do you feel competitive with people who are the same sex as you?”; Griskevicius et al., 2012), and two items assessing the perceived difficulty of mate attraction (e.g., level of agreement with “There will be a lot of competition to find someone desirable to date”; Durante et al., 2012). Full measures are reported in the Supplemental Material. Participants then completed demographic items and a suspicion check, followed by a debriefing.

Results

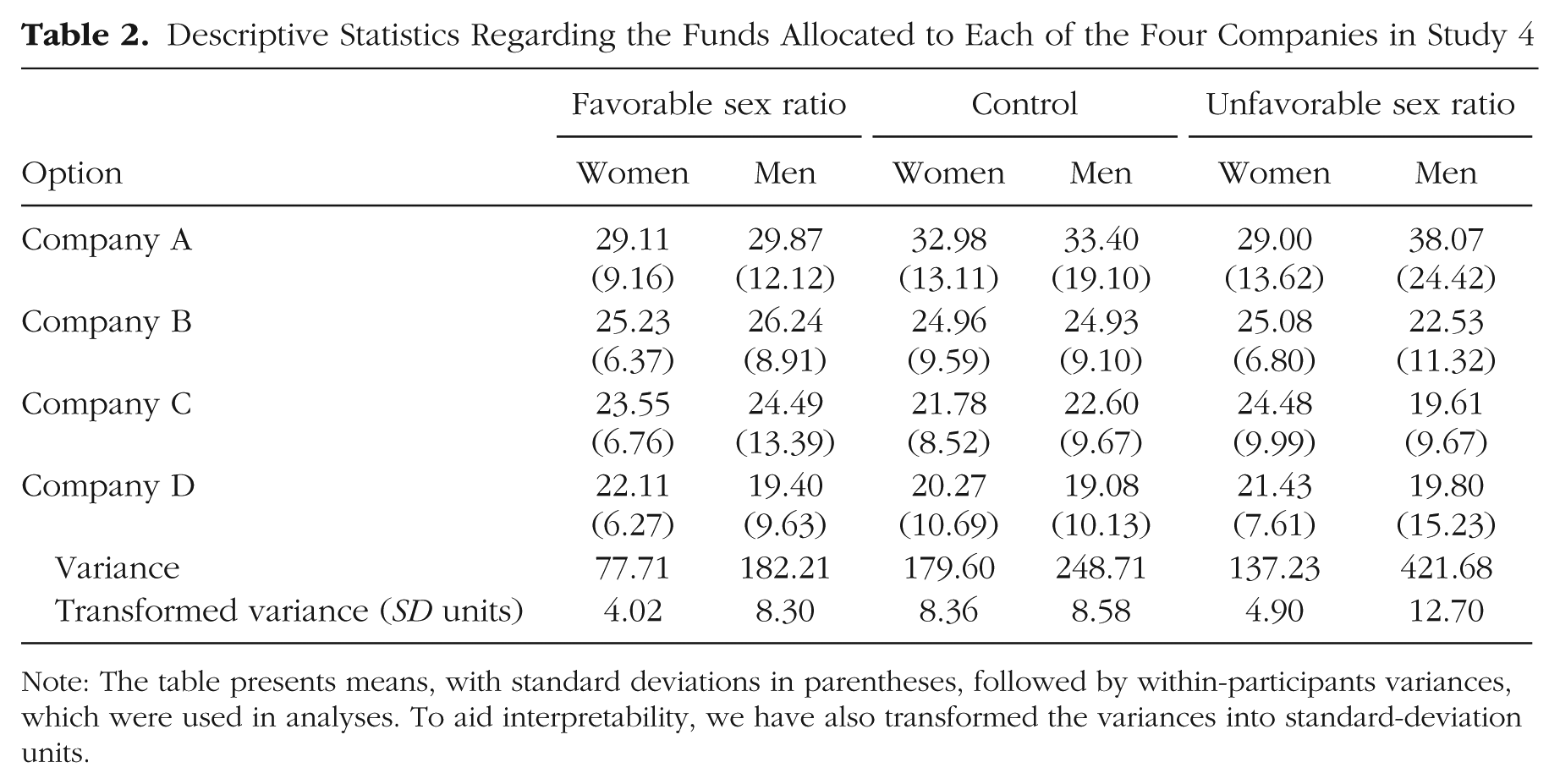

Three participants were removed for accurately guessing the hypothesis. As in Study 3, for our primary dependent measure, we calculated the within-participants variance of percentage invested in the four vaccine-company options (untransformed descriptive data are presented in Table 2). This variable represents the degree to which investment choices were concentrated in fewer options (higher variance scores) or spread across more options (lower variance scores).

Descriptive Statistics Regarding the Funds Allocated to Each of the Four Companies in Study 4

Note: The table presents means, with standard deviations in parentheses, followed by within-participants variances, which were used in analyses. To aid interpretability, we have also transformed the variances into standard-deviation units.

An omnibus 3 (sex ratio) × 2 (participant sex) ANOVA on vaccine-investment variance revealed a marginally significant main effect of sex ratio, F(2, 361) = 2.80, p = .06, η p 2 = .02, 90% CI = [.000, .030]. As expected, participants facing unfavorable ratios concentrated their investment in fewer options than did control participants, who in turn concentrated their investment more than did participants facing favorable ratios (see Fig. 1). Neither of these two specific comparisons reached significance (ps > .18). In addition, a main effect of participant sex emerged, F(1, 361) = 8.86, p < .01, η p 2 = .02, 90% CI = [.005, .056], with men diversifying less than women. The interaction of Sex Ratio × Participant Sex was not significant, F(2, 361) = 1.69, p = .19.

Results from Study 4: mean variance in investment allocations, separately for each of the three sex-ratio conditions. Higher numbers represent a greater concentration of investments into fewer options (i.e., less diversification). Error bars show ±1 SEM.

We next conducted an a priori test of the unfavorable- and favorable-sex-ratio conditions to determine whether we could replicate the effect found in Study 3. Using the standard t-test formula, but replacing the variance with the mean square error (Howell, 2013), we obtained a significant result, t(237) = 2.21, p = .014. These data replicated the effects found in Study 3 using a much larger sample. Finally, the overall pattern of means was confirmed by testing a linear contrast within the full model using weights of −1 (unfavorable), 0 (control), and 1 (favorable). This contrast was significant, p = .019.

We also assessed possible mediating effects. We created composites for each of the measures (reward responsiveness: α = .83; mating-impression management: r = .82; intrasexual competitiveness: r = .85; perceived mating difficulty: r = .61) and analyzed them in a 3 × 2 ANOVA. Main effects of sex ratio emerged for reward responsiveness, F(1, 361) = 3.59, p = .029, η p 2 = .02, 90% CI = [.000, .033], and mating-impression management, F(1, 361) = 5.89, p < .01, η p 2 = .03, 90% CI = [.002, .044], with unfavorable sex ratios leading to higher values on each measure. Perceiving that one was surrounded by more same-sex than opposite-sex individuals heightened positive reactions to reward signals and increased the drive to seek out and impress potential romantic partners. A main effect of participant sex also emerged on mating-impression management, F(1, 361) = 13.61, p < .001, η p 2 = .04, 90% CI = [.011, .073], with men showing higher scores on this measure than women. No interactions were significant.

Given the effects on reward responsiveness and mating-impression management, we evaluated whether these statistical measures mediated the effect of sex-ratio skew on funding variance. We entered sex ratio, participant sex, their interaction, and the two relevant mechanism composites into a simultaneous mediation analysis using the Hayes (2013) PROCESS procedure (Model 4, 10,000 bootstrap samples). Results indicated that only mating-impression management satisfied criteria for mediation (indirect effect = −13.92; 95% CI = [−37.23, −2.08]). These data are consistent with a model in which being in the majority sex (an unfavorable ratio) activated a desire to stand out as a potential romantic partner, which in turn led participants to concentrate their choices in investment decisions.

Internal Meta-Analysis

Each of these studies provides evidence that unfavorable (compared with favorable) sex ratios led to less choice diversification. To provide an overall measure of reliability and effect size, we conducted an internal meta-analysis. This approach is known to produce more meaningful estimates of the association between constructs than do single studies (Cumming, 2014).

Following the meta-analytic procedure recommended by Rosenthal and Rosnow (2007), we first examined the main effect of sex ratio. We converted the p values for each test of this main effect into z scores and weighted these by each study’s relevant degrees of freedom. The z-standardized significance levels (and df ) for each test were as follows—Study 1: z = 1.911 (df = 89); Study 2: z = 1.995 (df = 96); Study 3: zretirement = 2.144, zvaccine = 3.54 (df = 74); Study 4: z = 1.538 (df = 361). The overall main effect of sex ratio was significant (z = 3.36, p = .00039). The effect sizes for each test were as follows—Study 1: r = .3813; Study 2: r = .2174; Study 3: rretirement = .2709, rvaccine = .4026; Study 4: r = .0633. Weighting each test by its degrees of freedom, the overall effect size was r = .19. Thus, exposure to unfavorable sex ratios reliably reduced the propensity for choice diversification.

Although no effects of participant sex were observed in Studies 1 and 2, the funding-allocation task used in Studies 3 and 4 provided some potential evidence for sex differences. Consequently, and because the sex-ratio literature indicates mixed evidence for sex differences (Griskevicius et al., 2012; Hahn et al., 2014; Moss & Maner, 2016; Watkins et al., 2012), we evaluated whether participant sex reliably moderated the effect of skewed sex ratios across these studies. To do this, we submitted the Sex Ratio × Participant Sex interaction to the same meta-analytic procedure described above. The signs of the resulting z scores were assigned according to whether male or female participants produced the stronger sex-ratio effect within each interaction (negative for stronger female effects, positive for stronger male effects). The z-standardized significance levels (and df ) for each test were as follows—Study 1: z = 0.616 (df = 89); Study 2: z = −0.107 (df = 96); Study 3: zretirement = −0.659, zvaccine = 1.385 (df = 74); Study 4: z = 0.889 (df = 361). The overall interaction effect of Sex Ratio × Participant Sex (weighted by each test’s degrees of freedom) was not significant (z = 1.053, p = .146). Thus, no reliable evidence for a moderating effect of participant sex was observed in this investigation.

General Discussion

Although the default response to multiple decision options is typically to diversify one’s choices (Read & Loewenstein, 1995; Simonson, 1990), four studies showed that heterosexual people do just the opposite—put their eggs into fewer baskets—when the local environment contains higher numbers of same-sex than opposite-sex individuals. Although diversification has been shown to mitigate risk in animal outcomes (Olofsson et al., 2009), no research on human sex ratios has directly examined variance-management strategies, such as diversification. Here, we showed that people alter their choice strategy when faced with cues to competitive disadvantage, though the mating-relevant context of these cues promotes a risk-seeking rather than a risk-reduction strategy. Additionally, the pattern observed in Study 4 suggests that exposure to favorable sex ratios may also affect people’s choices (compared with control choices). This could reflect an expectation that some degree of intrasexual competition exists by default, and information that minimizes such competition encourages increased use of risk-averse diversification.

These effects occurred in domains that seemingly had little to do with mating, which suggests that the choice to concentrate investment reflected a general mind-set elicited by circumstances implying heightened intrasexual competition. We suspect that sex-ratio skew triggers a decision strategy that is applied in a range of possible situations (perhaps especially those in which concentrated choices help increase one’s romantic appeal). Overgeneralization of adaptive processes beyond their “proper domain” is not uncommon (Sperber & Hirschfeld, 2004) and may or may not be functional (Halberstadt, 2006; Zebrowitz & Montepare, 2006). The heightened levels of general reward responsiveness following exposure to unfavorable sex ratios are consistent with this possibility. Alternatively, it may be that eschewing diversification in favor of concentrating investment could help attract potential mates (by creating a positive reputation, increasing acquired resources, or simply reflecting a strong mate-pursuit motivation). This interpretation would be consistent with the mediating effect of mating-impression management observed in Study 4. Future research could profitably address whether effects of sex-ratio skew reflect overgeneralization effects or more strategic attempts at increasing desirability as a mate.

Beyond considerations of the mechanism underlying the effect of sex-ratio skew, this research has implications for understanding the motivational underpinnings of significant forms of decision making, such as financial planning, gambling, and product purchases. In fact, any domain in which people can spread or concentrate risk across multiple options may be susceptible to the competitive disadvantage signaled by OSR skew, including critical decisions about health care, business, or education opportunities. For instance, people often encounter a variety of recommendations for treating an illness (e.g., different medical procedures) across which they could choose to diversify or concentrate their efforts.

In sum, these findings contribute to a young but burgeoning literature suggesting that the OSR can influence a range of social processes. More broadly, this research illustrates how fundamental motivational systems designed to increase reproductive success are highly sensitive to social context. This approach integrates insights from ultimate (evolutionary) and proximate (decision-making) levels of analysis and, in doing so, provides evidence for a powerful process underlying diverse forms of decision making.

Footnotes

Acknowledgements

We thank Vladas Griskevicius for his assistance with study development and data interpretation, and Yuching Lin for her help in preparing manuscript materials.

Action Editor

Hal Arkes served as action editor for this article.

Declaration of Conflicting Interests

The authors declared that they had no conflicts of interest with respect to their authorship or the publication of this article.

Open Practices

All materials have been made publicly available via the Open Science Framework and can be accessed at https://osf.io/xgwhk. The complete Open Practices Disclosure for this article can be found at http://pss.sagepub.com/content/by/supplemental-data. This article has received the badge for Open Materials. More information about the Open Practices badges can be found at https://osf.io/tvyxz/wiki/1.%20View%20the%20Badges/ and ![]() .

.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.