Abstract

It is no secret that Iran has expressed interest in becoming a leading producer of LNG. Although currently not a producer at all, the country has made it repeatedly that transporting its gas reserves by sea is the best logical short-term goal vis-a-vis the many geopolitical, technical, and financial obstacles set against its international pipeline projects, which will take the best part of a decade to come to fruition, if at all. However, this by no means makes LNG a plan-B in the minds of policy-makers. LNG carries with it a unique set of advantages which make it a much-sought asset in oil diplomacy: Simply put, unlike with pipeline transit, suppliers can send their shipments wherever the price is right, making LNG supplies a “flexible pipeline” which will no doubt have an impact at the bargaining table. Indeed, it is not only investment and infrastructure which Iran needs to reclaim its position on the global market, but a comprehensive oil diplomacy to consolidate any headway made in the post-sanctions era.

Introduction

Recent years have seen an unpredictable expansion in global LNG trading, led by smaller producers like Qatar and countries like Malaysia, whose geographical position makes it difficult to think in terms of pipelines. Iran does not fit quite comfortably into either group. The market as certainly been crippled by the last decade of sanctions, yet it has the potential to outrank any OPEC nation in capacity. Its geographical position certainly provides few obstacles technically, yet politically, it finds itself in a region in turmoil, and most pipeline plans are forced to make giant detours in order to avoid chaos, war, and rival political influence. Both of these situations, among others make the prospect of LNG development and transport an exciting one for Iranian policy makers seeking to consolidate the progress made with the 5 + 1 agreement, which will see Iran re-enter the global energy market very soon. It is little surprise that the agreement equally buoyed its European delegates. The European market—the largest in the world—is desperate to secure any viable alternative to Gazprom, especially since the Ukrainian Crisis. For Iran, Europe would make the ideal market to begin trading with as soon as possible. This means plotting various oil and gas pipelines in the long term. In the short term, however, it means developing the necessary resources to deliver LNG supplies by boat.

This article attempts to explore the potential forks in the road Iran may encounter in this endeavor, while clarifying the greater context behind the country’s desire to overcome these obstacles.

Iran energy profile

Iran holds the world’s fourth-largest proven oil reserves, and according to BP’s last Statistical Review of World Energy, holds the world’s largest gas reserves at 33.6 trillion cm3. Despite these massive pools of potential resources, the sector has developed almost exclusively toward its domestic market. To demonstrate, in 2010, natural gas accounted for around 59% of Iran’s total domestic energy consumption, while oil consumption accounted for 39% of total energy use.

The energy sector in Iran: The fifth 5-year development plan

After the end of the Iran-Iraq War, Iran began to recover and redevelop her destroyed economy with the Five Year Development Plan, launched under the government of Hashemi Rafsanjani. The first Five Year Development Plan was implemented between 1989 and 1993. The major objectives of the Islamic Republic’s First Plan included:

Rapid movement toward a balanced and well-developed economy, Transfer of greater parts of the economy to the private sector, Protection of the lower-income brackets of the community, A shift from a centralized economy to a noncentralized (regional) economic structure.

While endeavoring to achieve these objectives, however, the government had to spend a good portion of the country’s financial resources to satisfy the basic needs of the people in the form of subsidies and other state aids. According to the statistics available, during the First Five Year Social and Economic Development Plan wrought the following changes:

Gross domestic product (GDP), on the basis of 1988 factor prices, increased by 7.3% Per capita GDP increased from 197,000 Rls at the start of the Plan to 240,000 Rls in 1993, And during the same period (of the plan): Fixed gross domestic investments increased by 13.3%, Private consumption increased by 7.7% per annum, Public consumption increased by 5.5% per annum, The ratio of fixed gross domestic investments to GDP which had been declining thus far, rose from 12.4% in 1988 to 16.3% in 1993.”

1

The Fifth Five Year Development Plan was implemented between 2011 and 2015. According to Article 125 of this plan, the Ministry of Petroleum was allowed to develop oil and gas fields with the aim of increasing 1,000,000 bpd oil production capacity and also to increase 2,500,000,000 cm3 natural gas capacity per day by developing current fields. Fields shared with the country’s neighbors were given specific priority. 2 According to the Fifth Five Year Development Plan, The National Iranian Gas Company (NIGC) has aimed to increase its export capacity to 328 million cm3 via both pipelines and LNG. Negotiations with consumer countries such as Kuwait, Bahrain, Jordan, India, and the European market continue regarding pipelines to export gas through Europe and Pakistan (the former, regarding the second phases of the Assaluyeh Field up to Bazargan on the Turkish border (1818 km long, 110 million cm3 daily), the later from Shehr to Pakistan (255 km long, 21.5 million cm3 daily)). 3

Iran energy policy post-sanctions era

Iran has declared its intentions to increase oil production and export capacity on countless occasions. The Ministry of Oil has recently presented a two-fold plan to achieve this; both short- and long-term. The short-term program first aims to mitigate the effects of sanctions and get the country’s industry and infrastructure back into shape, by using all means to:

Recover crude oil production capacity to that of 2005, Increase the export of crude oil capacity and other petrochemical products, Increase gas production in the South Pars field, Press forth with oil diplomacy, Eliminate barriers to the production and export of petrochemical products, Eliminate barriers to the production and export of LNG and condensates, and Optimize energy consumption.

These goals are to be achieved in order to give the Oil Ministry a springboard by which to attempt a more ambitious set of long-term objectives, which are namely to make the country:

The region’s top oil and gas producer. The second oil producing OPEC nation. The third biggest global gas producer. The foremost in terms of the value added in the production chain of oil and gas. A hydrocarbon corridor in the region, and center for trading oil and gas.

More bluntly then, the strategic objective of the Iranian oil and gas industry in the next two decades is to dramatically increase its share in the global energy market. This means maximizing the benefits of the international energy markets and increasing dependency on other countries, thus finding a strategic position for Iran in the global energy market. The maximization of oil income will require the adaption of coordinated measures, increasing export volume and stability, or increasing the price of oil.

The National Iranian Oil Company (NIOC) must become an international name, and its operations ought to expand beyond Iran’s geographical borders whilst at the same time maximizing its income domestically. It should invest and take part in global oil upstream projects and so obtain prosperity for the country and preserve and guarantee Iran’s interests; such as the stability of oil, natural gas, and LNG markets in the long term. 4

Iran’s natural gas plans

Export is still lower on Iran’s list of priorities than injection into the industry, stabilizing domestic consumption, and floating gas-based industries. Yet, joining the world gas market had previously been a much low priority, given economic considerations, and now that it finds its way onto the lips of more and more policy makers of late, has benefitted from the momentum gained thanks to the early successes of the country’s new international relations strategy. By launching the gas export plan, there have been attempts to create special zones for the development of gas-intensive industries, publicity of gas-based industries such as steel, cement, petrochemicals, etc., and the promotion of integrated gas projects and a diversification policy.

5

According to BMI’s Iran Oil & Gas Report, “large-scale exports from Iran will take at least five years to materialize (2016–2021). Such an increase depends on a significant ramping-up in production and the building-up the necessary export infrastructure.” The report also predicts that:

Gas trade with Iraq could begin in 2016 if the security the situation in sufficiently improved. Iran is expected to reduce imports from Turkmenistan due to greater domestic production.

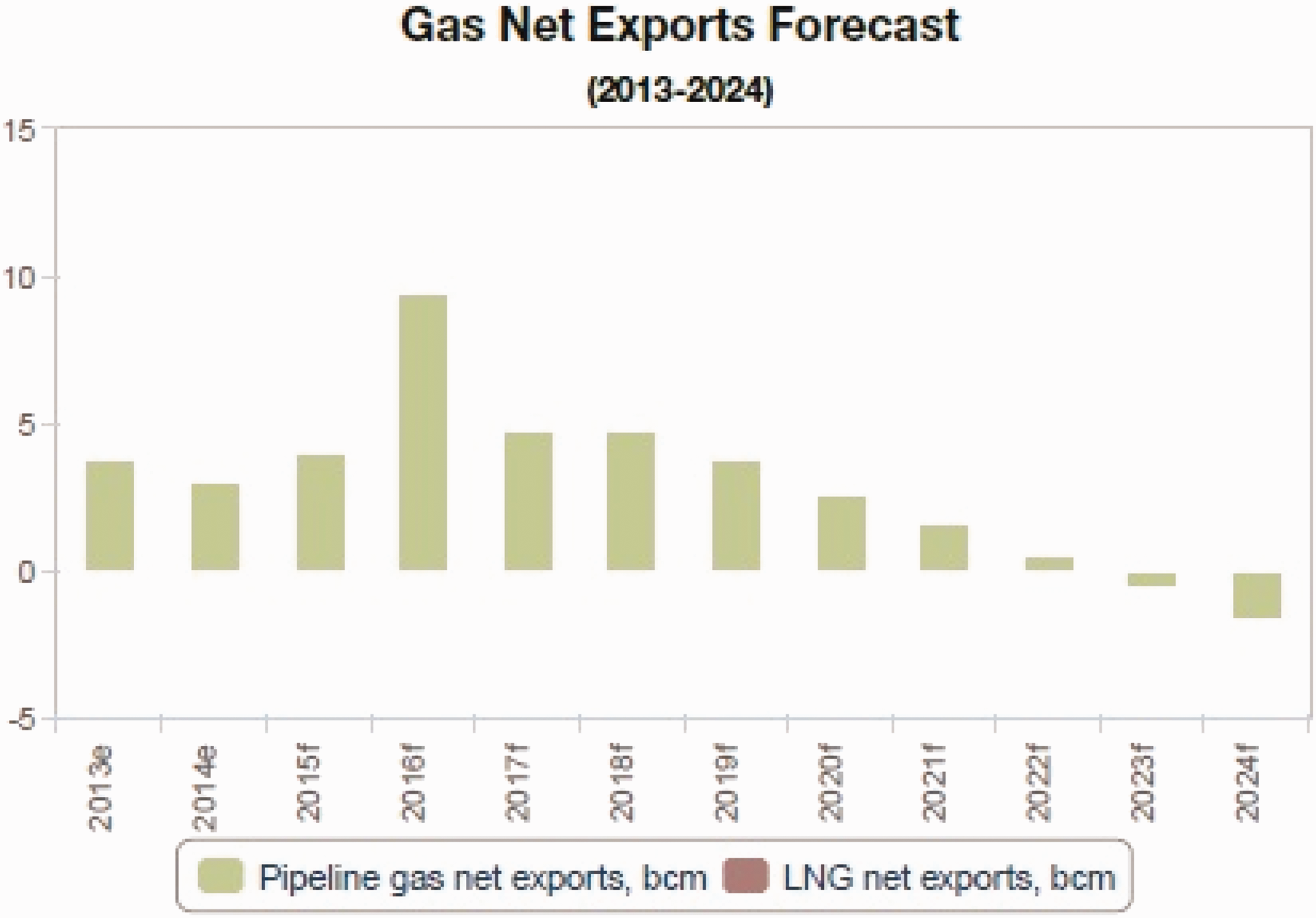

Iran trades small amounts of natural gas at the regional level by pipeline and is a small net exporter of natural gas to Turkey (about 3.0 billion cubic meters (bcm) in 2014). Iran imports gas from Turkmenistan and the majority of its exports go to Turkey. Iran notably relies on gas imports during the winter when residential demand peaks due to the cold weather.

Gas net exports forecast (2013–2024). e/f: BMI estimate/forecast. Source: BMI, EIA, IEA, OPEC. (Iran, Oil & Gas Report Includes BMI's Forecasts, Business Monitor International Ltd. March 2016.).

With the launching of the new South Pars phases (15, 16, 19,…); Iran will reduce its need for gas imports, enabling it to have greater export capacity. Iraq and Turkey to be the main benefactors to this, with Turkmenistan losing out greatly. 6

The Iran Oil & Gas Report looks at the country’s gas production, taking into account production levels after completion of the latest phases of the South Pars in late 2015 (phases 15 and 16), and later in 2016 (19). After the lifting of sanction, Iran will be able to access significant financial and technological support to speed up the development of the South Pars fields. However, it should be noted that Iran has a huge level of domestic consumption, especially for power plants designed for the generation of electricity. It is expected that a majority of the additional production over the coming years will be consumed domestically. Long-term, net export will also be highly dependent on the level of investments into the sector made post sanctions. 7 Iran sees LNG exports to the EU as an immediate priority, and thus, gaining investors is a key current objective. Even if this is the case, however, although exports to immediate neighbors such as Iraq, Pakistan and Oman will begin soon, BMI believes that due to problems in natural gas infrastructure, Iran will be unable to export gat to Europe before 2024. Nevertheless, LNG still remains the most viable and flexible option in order to significantly increase Iranian natural gas exports and there is a strong demand within Iran to move in this direction. Given the low price of gas production to boot, major LNG production will be greatly beneficial to Iran.

South pars field

The South Pars is the world’s largest gas field. Located in the Persian Gulf and shared by Iran and Qatar, the South Pars contains around 8% of the world’s proven gas reserves and more than 50% of Iran’s natural gas reserves. Development of the field has been divided into 29 phases, in order to secure the drilling, production, and transit of its 40 trillion cubic meters (tcm) of natural gas spread out over an area of 9700 square kilometers. This field contains 12 tcb of gas and 18 billion of Condensate. Iran is planning to have streamed all 23 phases of development by 2018. 8

Iran energy sector projects

Gas pipelines

Iran has extensive domestic natural gas and oil pipelines. This pipeline network involves 12 pipelines that are between 63 and 630 miles long. The pipeline which connects the Bandar Abbas refinery to the Esfahan refinery is the longest, with a capacity is 300 thousand bbl/d. The second longest pipeline connects the Ahvaz oil field to the Tehran refinery. This transports 300 bbl/d. 9 In addition; Iran owns some international pipelines which are used to transport oil and natural gas. Plans are underway for the building of further pipelines in the future, but the current number includes the following:

The Iran-Oman gas pipeline

Iran signed an agreement in March 2014 to export gas to Oman by 2017. According to this agreement, Iran is to export 10 million cubic meters per annum. Both sides are discussing the building of a 260 km underwater pipeline to carry Iranian gas across the Persian Gulf to the country. Oman’s gas reserves are roughly 900 bcm, while the country’s gas production is about 85 million cubic meters per day (mcm/d). 10

The Iran-Pakistan gas pipeline (IP pipeline)

Iran and Pakistan began work on the IP Pipeline in March 2013. The 2700-km pipeline transports gas from the Assalouyeh Energy Zone to Pakistan. Two thousand kilometers of it is run through Iran and 700 km through Pakistan. The revenue generated looks to be around $7.5 billion. According to the contract, it is scheduled to be constructed by December 2014. Iran is planning to export 1.5 mcm/d natural gas to the country. 11

Iran-Iraq pipeline

Iran signed agreement to export Iranian gas to Iraq. According this agreement, Iran is to export 40–65 mcm to Baghdad and Basra every day for 6 years. It is expected that Iranian gas will be ready for export to Iraq by end of 2017, with both countries having invested around $2.3 billion for construction pipeline. 12

Iran’s gas export to the Europe: When, how and how much?

By January 2016, two phases of South Pars field will come to stream and Iranian gas production capacity will be set to increase. The daily production guaranteed by the phases will mean 56.6 mcm of natural gas, 75,000 barrels of gas condensate and 400 tons of sulfur may be transported. 13 Iran increased natural gas production by 10%, to 202 billion cubic meters per annum (bcm/a) between March 2014 to March 2015, while the figure re-increased has by 5% during the current fiscal year. All of the increased output has been absorbed by domestic sectors, while the huge gas shortages in some sectors—such as electricity generation—and re-injection to oil fields continues. Iran is planning to increase gas production to about 400 bcm/a by 2019. 14 According Homayoun Falakshahi, Middle East Upstream Analyst at Wood Mackenzie, Iran’s “gas production is likely to significantly increase in the future, but most of the increase is sure to be absorbed by the re-injection needs in the country’s oldest oil fields. Gas production in 2014 (sales gas and gas available to re-injection, excludes flares and losses) was at 19.3 bcfd (or 546 mcm/d or about 200 bcm/a). We estimate this could grow to 25 bcfd (or 780 mcm/d or 258.4 bcm/a) by 2020 given new supply from South Pars.” 15

Iran LNG plan

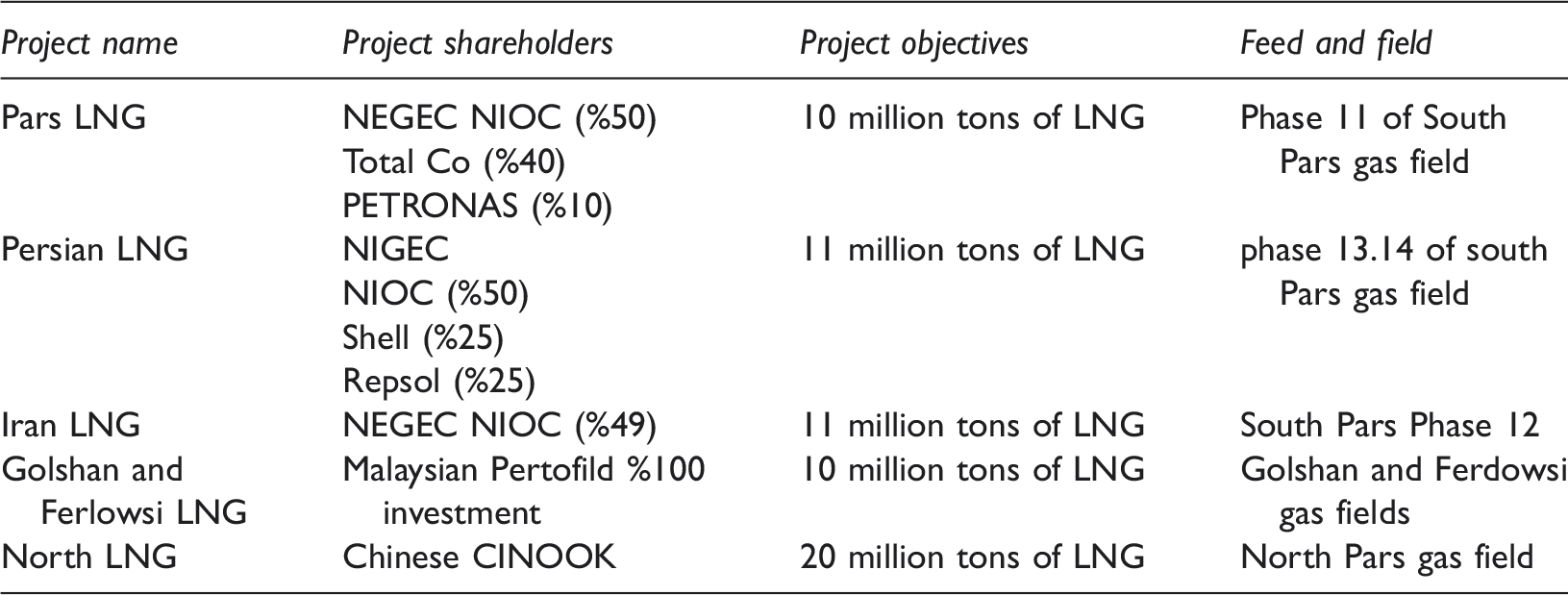

Iran LNG Projects.

Iran LNG projects

Iran plans to play a key role in the world energy market in coming years. 18 This is why the country has officially invited all foreign companies to invest in its energy sector, explaining that Arabian, Chinese, and European companies, too, should be keen to participate in Iranian LNG plans. Iran’s first priority is to complete its current LNG projects, reaching a production capacity of 10.5 million tons within 2 years. At present, Iran is not producing LNG, but to complete the next half of its development phase, it requires around $4.5 billion. If this is achieved, Iranian LNG will be set to go on stream by end of 2018. Other LNG projects will be a high priority beyond this, but the immediate problem will be surmounting the task of repairing the damage wrought to the country’s technological and infrastructural capabilities created by EU and US sanctions. 19

At the Munich Security Conference, Oil Minister Bizhan Zanganeh made plain Iran’s emphasis on LNG, which he termed a “flexible pipeline,” as a sort of cold shower for the European Commission. The “flexibility” amounts for the freedom of the seller to choose the destination of the LNG tankers if the “price is not right.” 20

Foreign companies, including Total, Petronas, Shell, and Repsol had been working on Iranian LNG projects before EU and US sanctions were imposed, so there has always been a realization—as the CEO of National Iranian Oil Company stated in October 2015—that LNG is both a more sensible choice for European consumers and much more economical than a pipeline. 21 Iran’s geographical position in the region, with huge offshore natural gas fields enables Iran to enter into the advantageous LNG markets of Asia and Europe. Iran aims to become a leading LNG exporter by the end of 2018 and negotiations with companies continue for participation in the completion of Iran’s first LNG facilities, set to increase capacity by 10.5 MT annually. Shell has officially stated that it is ready to complete Iran’s LNG projects. 22 Iran and Oman have signed an agreement which will see the former export gas to Oman to have it liquefied for export to international—and especially European—markets. 23

By December 2015, and after long negotiations, Iran and French companies had reached a final agreement on floating production of LNG from associated gas at an oilfield in the Persian Gulf. According to Rokenddin Javadi, the companies will form a consortium to build the Middle East’s first FLNG plant with a capacity to produce 1 million tons of liquefied natural gas a year, the plant’s feedstock will come from the gas currently being burnt at the Forouzan oilfield which Iran shares with Saudi Arabia. Iranian and French investors will be charged with acquiring LNG tankers for shipment and an FLNG vessel for turning natural gas to LNG. In any case, marketing and sales will be managed by NIOC. 24

Global LNG outlook

According to the Wood Mackenzie report, after 2015, construction of new LNG facilities around the world will decrease at present with 31 new LNG project under construction. Thus, LNG production capacity looks to decrease in the coming years. It is expected that a decrease in new LNG facilities construction will begin in North America and spread to other regions. A decrease in investment in North America will be begin by 2019, and develop further from then. Between 2019 and 2021, only 10–15 huge LNG projects are set to be constructed around world annually. Future natural gas markets also have an important effect on construction new LNG facilities around world. Decrease in demand for construction of new LNG facilities will thus result in an oversupply of LNG. Due to such conditions, international investors will logically put off investment in such projects. 25

By 2016, with aim of becoming world’s largest LNG exporter, the US will begin to stream its new LNG facilities; Cheniere’s Sabine Pass project includes six liquefaction trains, with production capacity about 4.5 MTPA. Australia is also planning to come to stream its new LNG project with Chevron’s Gorgon, the largest LNG project in the world, aiming to supply the whole of Western Australia. Australia is planning to become an LNG exporter by 2019 and play key role in the global market. Shell in Canada has also invested heavily in the B.C. LNG project. Similarly, Eni has declared its interest in African construction for Coral FLNG and Mozambique’s LNG facilities. 26 According to the International Energy Agency, there are six LNG projects in Australia, at a cost about $200 billion, which may struggle to break even due to falling oil prices, and has little prospect of having the third of its planning stages going ahead. As Fereidun Fesharaki, Singapore-based energy forecaster stated, the economics of the planned LNG projects in Australia are a “tragedy” because the over-optimistic expectations of Asian consumers mean they will continue to pay incredibly high prices. While the majority of Australian LNG will be supplied into Asia in accordance with long-term contracts, the deals are directly indexed against current oil prices, meaning a change in oil prices hit LNG prices 3–6 month later. 27

LNG pricing

The drop in oil prices has had a negative impact on LNG prices. By the end of 2015, JKM spot priced the LNG market to find East Asia was trading $7.28 per million btu (MMBtu) for December shipments, down nearly two-thirds from early 2014. It should be noted that the majority of LNG exporters have their cargoes signed up under long-term fixed-price contracts. But usually not all of a given supplier’s capacity secures buyers. It is expected that an additional 14–15 million tons may become surplus annually by 2016. Oversupply has decreased in demand too, with Japan and South Korea representing two major LNG importers in Asia who decreased their orders in November 2015. Japan’s net LNG imports dropped by 12.8% in November 2015, and South Korea’s level of imports have similarly fallen to their lowest levels in 6 years. 28 For 2016, some forecasts call for LNG prices of around $6 for MMBtu and falling to the $5 for the next 2 years. However, slowing increasing demand from consumer markets such as Asia, which accounts for two-thirds total global LNG demand, mean prices could easily dip and stay in the range of around $4 MMBtu range. This is a dismal projection for such huge cape intensive LNG projects as those in Australia, although US LNG project costs are expected to remain lower. However, even relatively low cost US-based LNG projects will enter a rough supply market until at least 2020. 29

Conclusion

The effects of long-term sanctions against the Iranian energy sector, problems in energy management, and a shortage in financial and technological resources are all factors delaying Iran’s ability to stream the majority of its oil, gas, and LNG projects. Due to sanctions against its energy sector, Iran’s neighbors such as Qatar, were able to exploit the country’s weakened position to secure their own place as the world’s foremost LNG exporter. Both countries share the South Pars field, and it is no coincidence that most of Qatar’s exports in LNG are sourced from this area. If Iran’s natural gas sector no longer suffers economic sanctions in the near future, the country will sooner or later be able to export natural gas to European and East Asian markets via massive pipeline projects.

Before sanctions were introduced, Iran had six LNG projects with a 75 million tons production capacity. Some European companies such as Shell, and companies from China and Malaysia, had signed agreement to complete Iran’s LNG projects, but all halted activities, bringing the projects to naught. Since the lifting of sanctions, Iran has expressed interest in completing its first LNG facilities, and needs $4 billion to complete its current stream marking 60% of its total plans. The country has invited all foreign companies to invest in its LNG projects. In the long term, the country is interested in exporting gas to Europe, but in the short term, exporting LNG to EU is its first priority. Iran is in negotiation with some EU countries such as Spain to discuss the terms of its future LNG exports. As Iran’s deputy of Oil minister made clear, British companies are already known to be taking an interest in some of the LNG proposals. 30

In the coming years, there will be extensive challenges facing the LNG market the world over. After prices plunged last year the LNG market all but collapsed, and so is going to have to modify itself for greater international competition aimed at increasing both demand and supply. After all LNG projects in the US and other regions come to stream, oversupply will be in favor of demand. In the meantime all suppliers will have to sell LNG at knock down prices. However, many of Iran’s LNG projects are small scale and aim to supply domestic demand. After completing its LNG projects the country may be faced with problems such as oversupply and low prices, and Iran will undoubtedly be up against great competition with other suppliers, but this may prove to be an advantage. It is expected that LNG prices may decrease to $4, with Iran having to produce LNG at low prices and sell with low prices to find stable market. For its part, the EU is evidently trying to reduce its dependency on Russian gas, and LNG will be the best alternative for achieving this. Iran also has the chance to complete its LNG project and sell to European consumers, but due to oversupply of LNG, Iran needs to use foreign policy and energy diplomacy wisely in order to find a stable demand market.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.