Abstract

Environmental Kuznets curve literature mostly uses a single indicator as a measure for environmental degradation. However, each single variable captures only a part of the environmental problem, and a reduction in any single measure does not indicate that the environmental problem is diminishing in general. Our study is the first one which investigates the validity of the environmental Kuznets curve hypothesis for the Mexico, Indonesia, Nigeria, and Turkey (MINT) countries by employing the ecological footprint as the measure of environmental degradation. Autoregressive distributed lag results indicate that the environmental Kuznets curve hypothesis is valid for each of the MINT countries for the period of 1971–2013. The long-run coefficients of our augmented environmental Kuznets curve model show that fossil fuel energy consumption, exports, urbanization, and financial development are the most common causes of anthropogenic pressure on the environment. The effects of exports and imports are negative and positive on environmental degradation, respectively. The long-run coefficients of urbanization, financial development, and renewable energy consumption differ at certain levels for the sampled countries. The results of the analysis point to a number of different policy proposals for each country.

Introduction

The world is faced with the challenge of confronting the two pertinent issues of economic development and environmental preservation. The issue of environmental preservation has, however, become one of the greatest interest given its unique attention as a serious contemporary issue of both developed and developing countries because of the accumulation of greenhouse gases (GHGs) in the atmosphere which leads to an increase in mean global temperatures.

Rapid industrial growth over the recent centuries has heightened demand for energy resources, making it increasingly difficult to trade-off between economic development and environmental impacts because this demand is met mostly from energy production from non-renewable fuels that cause GHG emissions. Despite the genuine concerns about the resultant effects of increased GHG emissions, they are grudgingly seen as a necessary cost of rapid economic development. It is therefore crucial to understand the inter-temporal links in the environment-income nexus if GHG emissions are to be reduced.

The environment-income nexus, commonly referred to as the environmental Kuznets curve (EKC) hypothesis, was proposed by Grossman and Krueger 1 and Selden and Song 2 . It is represented by a quadratic function and has an inverted U-shaped curve.3–7 The EKC hypothesis is based on the notion that environmental quality deteriorates with the increase in gas emissions during the initial stages of social economic development; however, there exists a certain threshold above which an economy ought to grow and environmental quality increases, forming an inverted U-shaped curve. Many studies have been carried out to test the EKC hypothesis for different countries and country groups. Some scholarly works that verify the existence of the EKC hypothesis include Apergis and Ozturk, 8 Balaguer and Cantavella, 9 Bilgili et al., 10 Charfeddine and Mrabet, 11 Heidari et al., 12 Kasman and Duman, 13 Li et al., 14 Mrabet and Alsamara 15 , Pablo-Romero et al., 16 and Wang et al. 17

One profound shortcoming of most studies examining the relationships among economic growth, energy consumption, and the environment is the use of carbon dioxide (CO2) emissions as an indicator of environmental impacts. 18 However, according to studies, such as that of Al-Mulali, Saboori & Ozturk, 19 CO2 emissions constitute only a small part of the total environmental damage caused by higher levels of energy consumption. On the other hand, the ecological footprint (EF) indicates anthropogenic pressure on the environment.20–29

Since 2001, the world’s attention has been drawn to Brazil, Russia, India, and China––known as the BRIC countries––as a potentially powerful growing bloc of the global economy. Moreover, Jim O’Neil of Goldman Sachs identified another emerging economic bloc, which he referred to as the MINT, meaning Mexico, Indonesia, Nigeria, and Turkey (see http://www.bbc.com/news/magazine-25548060, accessed 24 September 2017). These countries have shown tremendous economic progress displaying very similar economic features, such as large and growing populations, which provide them with unique potential prospects, and they have been greatly acknowledged as emerging economic giants that play significant roles in global economics.30–34

According to Jim O’Neill, MINT countries are now poised to be the world’s largest economies in the next three decades given their unique advantages. Gold Sachs predicts a steady growth trend through 2020 for these countries, while US investments forecast an annual growth of 5% in each of the MINT countries. Based on these prospects, MINT countries will likely individually yield from about 1% to 2% of the world economy over the next decades. Statistics from 2016 show that MINT countries had a population of 654.1 million (Indonesia 261.1 million, Nigeria 186.0 million, Mexico 127.5 million, and Turkey 79.5 million) with a tendency of steady, rapid growth, and a similar positive trend is expected over the future horizons (see https://data.worldbank.org/indicator/SP.POP.TOTL, accessed 24 September 2017). According to scholars such as Ghosh, 35 Jumbe, 36 Mehrara, 37 Nnaji et al., 38 Nnaji et al., 39 and Shiu and Lam, 40 empirical studies have established strong positive energy-economic growth/activity relationships, echoing the need for vibrant energy in speedy developments of the MINT. It is the economic agenda of the MINT countries to transform themselves into fully industrialized economies as soon as possible, and to achieve this, efficient energy consumption is needed as inefficient energy systems lead to wastage, such as the rapid reduction of energy resources, environmental degradation, and increased cost of energy products and services. 41

This study, therefore, aims to analyze the relationships among the EF, gross domestic product (GDP), fuel, renewable resources, trade, urbanization, and financial development in the EKC framework for the MINT countries by applying autoregressive distributed lag (ARDL) methods. According to authors’ best knowledge, this study investigates the augmented EKC hypothesis with fossil fuel, renewable energy consumption, trade, urbanization, and financial development for the case of MINT countries separately by adopting EF as an indicator of environmental degradation for the first time in energy economics literature. To this aim, we adopt time series analysis for each country to provide robust estimation results and separate policy implications for MINT countries.

This paper consists of five sections with a literature review, an overview of data and methodology, empirical results, conclusion, and policy implications, respectively.

Literature review

Following the pioneering article of Kraft and Kraft, 42 the economic growth-energy nexus has been extensively studied by many researchers. Many of these studies found a causal relationship between economic growth and energy consumption. 43 The required energy for economic growth has been mostly satisfied with fossil fuels which are detrimental to the environment. The trade-off between economic growth and environmental quality presents a bitter choice between the two; thus, the relationship between the sustainable use of natural resources and sustainable economic growth has become a vital subject among researchers. 44 Growth-environment nexus literature has been developed on several strands, and one of the most important is the EKC hypothesis. The EKC hypothesis reinterpreted the idea of Kuznets 45 which claims that there is an inverted U-shaped relationship between economic growth and income inequality and applied it to the growth-environmental degradation issue. Grossman and Krueger 1 investigated the relationship between income and environmental degradation and found a similar inverted U-shaped relationship. Basically, this hypothesis asserts that, although there will be environmental degradation during the first phase of economic growth, after a certain threshold is reached, degradation will decrease. This optimistic idea gained great attention from various scholars, and many early studies found support for this hypothesis.2,46–48 However, later studies provided mixed results which triggered the criticism that EKC hypothesis testing very sensitive to econometric methodologies, 49 choice of country and region, 50 time span, and data availability.6,51,52 Also, the results are quite sensitive to model building, that is, the determination of dependent variables and independent variables. 53

EKC studies use an environmental quality indicator as a dependent variable. Most of the previous studies used a single variable as a proxy of environmental degradation.54–57 The most widely used single indicator for environmental pollution is CO2 emission. 58 As an alternative to CO2 emission, a wide variety of single measure indicators have been used to represent environmental damage, such as nitrogen dioxide (NO2),59,60 sulfur dioxide (SO2),61–63 industrial waste, 64 water pollution, 65 threatened species, 66 and deforestation. 67 There are also studies that use several single variables to enhance the context of the research. 53 However, there are several problems regarding the use of these variables. First, they only represent a portion of the problem, which is criticized as the major weakness of most of the EKC studies. 68 Also, as a result of technological progress, some specific pollution indicators might decline. But, this does not mean that overall pollution is declining. There might be a shift from one pollutant type to another. 69 Another point is that, even though the EKC hypothesis might be valid for a specific emission, the more important consideration is whether or not there is deterioration in resource stocks. 70 Thus, the use of a composite indicator might reduce the aforementioned problems.

There have been many efforts made to measure the environmental damage created by human actions. In fact, several environmental performance indexes that capsulize various environmental indicators have been proposed. 71 The EF shows the human demand for natural resources, and it is one of the most comprehensive indicators of natural resource consumption currently available, 72 a comprehensive indicator of anthropogenic pressure on regenerative biological capacity,73,74 and one of the most widely recognized measures of environmental sustainability. 75

The EF has been used by many EKC analysts as a dependent variable.11,15,76–82 However, studies that use the EF to investigate the EKC hypothesis have provided mixed results. York et al. 27 conducted a study of 139 countries by using the EF as a dependent variable and found that the EKC is generally only relevant in developed countries. Bagliani et al. 78 investigated the EKC hypothesis for 141 countries, and they could not find any support for the hypothesis. Indeed, the results showed that the EF increases when income per capita gets higher. The findings of Caviglia-Harris et al. 83 also support those of Bagliani et al. 78 and confirm that the EKC hypothesis did not hold for their sample. Boutaud et al. 79 found partial empirical evidence for the validity of the EKC for their sample of 128 countries. Al-Mulali et al. 84 found strong evidence for the validity of the EKC hypothesis for the upper-middle- and high-income countries, which is compatible with the theoretical expectations. Ozturk et al. 80 also provided similar findings. Charfeddine and Mrabet 11 tested the EKC hypothesis for 15 Middle East and North Africa (MENA) countries for the period of 1975–2007 and found support for oil-exporting countries and for most of the entire sample. However, for the non-oil exporting countries, the EKC was not validated. Acar and Aşıcı 76 found weak support for the EKC. Their results indicated a relationship only between income per capita and the EF of production. Mrabet and Alsamara 15 used two different environmental indicators, EF and CO2, for comparison purposes, to investigate the EKC hypothesis for the case of Qatar. Their results validated the EKC hypothesis for the EF indicator. Wang et al. 82 used the spatial econometrics approach and could not find support for the inverted U-shaped relationship between the EF and economic growth. Saboori et al. 81 found evidence for the EKC hypothesis for 6 organization of petroleum exporting countries (Algeria, Iraq, Venezuela, Nigeria, Qatar, and Kuwait) out of 10 for 1977–2008 by comparing short- and long-run income elasticities.

The core of the EKC model includes an environmental degradation indicator as a dependent variable and GDP and GDP square as independent variables. 81 However, there are also other determinants for this relationship.86 The omission of relevant control variables has been criticized by researchers because it causes omitted variable bias. Energy use is one of the most employed variables as a result of its powerful link with GDP growth.8,86 Because of its vital importance, several forms of energy consumption are explored in the energy-growth-environment literature.87,88 Theoretically, we expect that different energy types might have different effects on environmental degradation. So, it is preferable to use renewable energy as a separate variable rather than using an aggregate energy figure. 89 Also, the trade–environment relationship has been extensively elaborated in the literature90–92 and has become one of the most important control variables in the EKC literature. 93 The relationship between trade and the EF is explained by Andersson and Lindroth 94 in detail. They suggest that trade causes increases in income and consumption in the host country. Therefore, higher consumption leads increases in EFs of the countries. Following the study of Liddle, 95 we include international trade as a control variable by splitting it as exports and imports to check whether they have opposite-signed coefficients or not in our model. Financial development is also an important determinant of environmental studies, and there is an abundance of findings which claim that financial development might contribute to environmental protection.96–98 It is suggested that financial development in a country attracts foreign direct investments and increases trading activities. Therefore, it stimulates economic growth and energy consumption. This leads increases in environmental degradation. On the other hand, financial development may decrease environmental degradation with higher investments in environmental friendly projects. In their recent study, Ali, Abdullaha, and Azam 93 incorporated financial development and trade openness variables in their EKC model and concluded that EKC holds for the case of Malaysia. Moreover, urbanization has gained importance in environmental studies. Urban lifestyle might have important implications for the EF as well. Urbanization has been investigated in many EKC studies, most of which report significant coefficients for the variable.80,84,99–104

Data and methodology

The variables used in this study are the EF (gha per person) (ECO), GDP per capita (constant $2010) (GDP), renewable energy consumption (percentage of total) (REN), fossil fuel energy consumption (percentage of total) (FUEL), exports of goods and services (percentage of GDP) (EXP), imports of goods and services (percentage of GDP) (IMP), urban population (percentage of total) (URBAN), and domestic credits provided by the financial sector (percentage of GDP) (FD). Time series data were used from the period of 1971–2013. GDP, fossil fuel energy consumption, exports, imports, urban population, and domestic credits were collected from the World Bank Development 105 Indicators; EF data were collected from the Global Footprint Network Database; 106 and renewable energy consumption was collected from the OECD Database. 107

Unit root tests

Augmented Dickey and Fuller (ADF) and Philips–Perron (PP) unit root tests were adopted in order to investigate the integration levels of the conducted variables.108,109 The ADF test eliminated the possibility of rejecting a true null hypothesis of non-stationarity. The PP test was used as an alternative technique to the ADF test. The PP test computed a residual variance that was robust to autocorrelation by adopting non-parametric statistics for residuals. 109

The bounds test for level relationship

The bounds test through the ARDL approach for level relationship was developed by Pesaran et al.,

110

and it can be applied whether the independent variables are integrated of order one, I(1), order zero, I(0), or mutually co-integrated. One of the biggest advantages of the ARDL approach is that it estimates the error correction model (ECM) by choosing the optimal lag lengths for regressors separately, and it eliminates bias estimations in ECMs. The bounds test through the ARDL approach suggested the estimation of the following ECM:

After revealing the long-run equilibrium relationship among variables in Equation 1, short-run and long-run coefficients were estimated by adopting the ECM. The speed of adjustment of the short-run values of the regressors to the long-run equilibrium level of the dependent variable was also estimated by the following ECM model:

Causality test

This study employs the Granger causality test through the ECM in order to estimate the directions of possible long-run equilibrium relationships among the variables.

The Granger causality test suggested the estimation of the following ECM:

Empirical results

ADF and PP tests were applied in order to investigate the integration orders of the variables in the conducted models. a All variables for Turkey and Mexico were not stationary at their level forms, and they became stationary when their first differences were taken, meaning that they were all integrated of the same order, I(1). On the other hand, fuel energy consumption and trade openness for the case of Indonesia and financial development and fuel energy consumption for Nigeria were stationary at their level forms, meaning that they were integrated of order zero. In summary, ADF and PP unit root test results provided a mixed order of integration of the variables for Indonesia and Nigeria, while variables for Turkey and Mexico had the same order of integration.

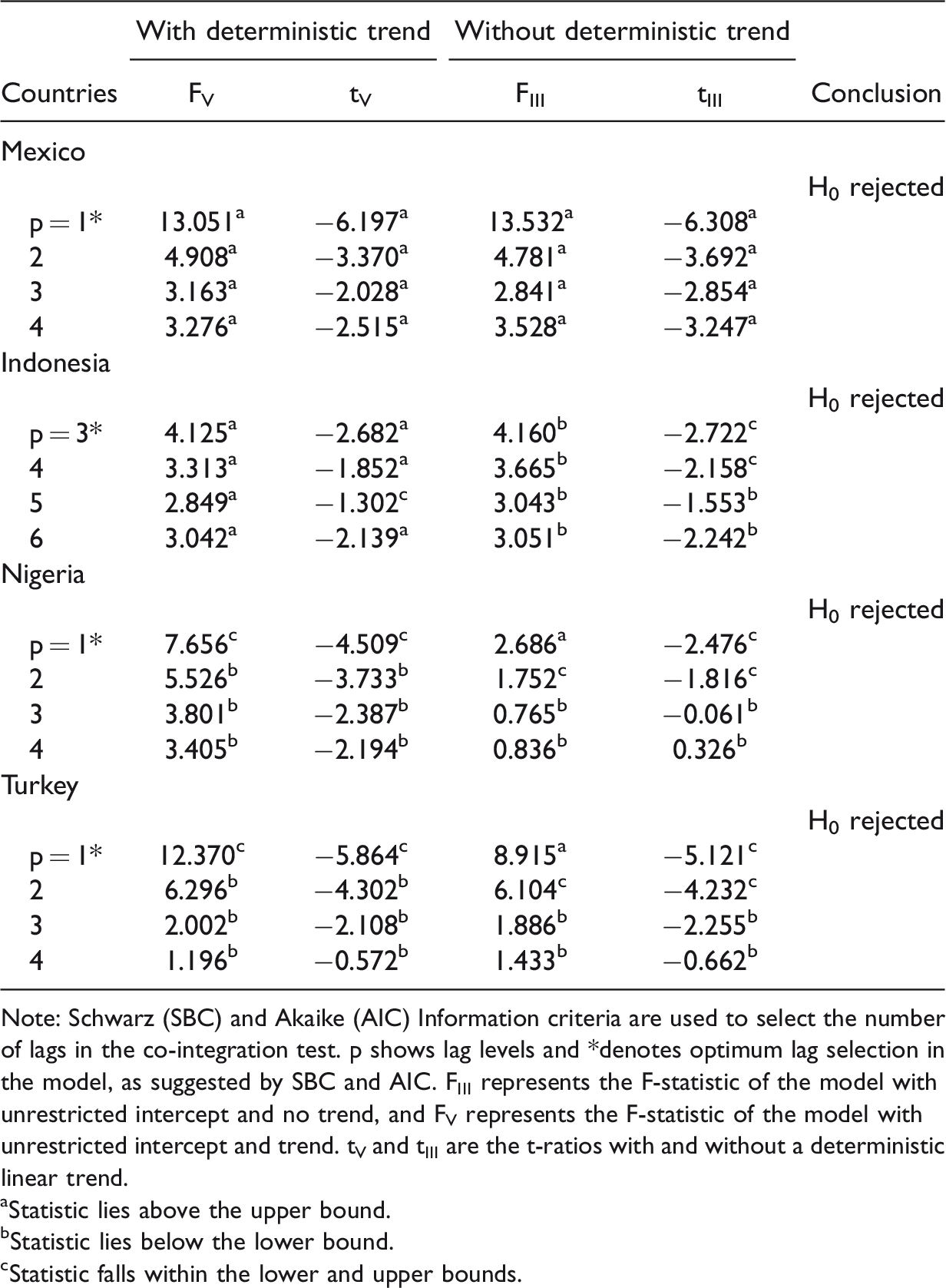

The level of relationships among environmental degradation, real income, squared real income, fuel energy consumption, renewable energy consumption, exports, imports, urbanization, and financial development were revealed by the bounds test under the ARDL approach for MINT countries individually. Table 1 indicates the results of the bounds test for the level of relationship. F-statistics for scenarios 3 and 5 of Pesaran et al. 110 were compared with the critical values of Narayan 111 for small samples, and t-statistics were compared with the critical values of Pesaran et al. 110 in order to reject the null hypothesis of there being no level relationships among variables.

Bounds test results for level relationship.

Note: Schwarz (SBC) and Akaike (AIC) Information criteria are used to select the number of lags in the co-integration test. p shows lag levels and *denotes optimum lag selection in the model, as suggested by SBC and AIC. FIII represents the F-statistic of the model with unrestricted intercept and no trend, and FV represents the F-statistic of the model with unrestricted intercept and trend. tV and tIII are the t-ratios with and without a deterministic linear trend.

Statistic lies above the upper bound.

Statistic lies below the lower bound.

Statistic falls within the lower and upper bounds.

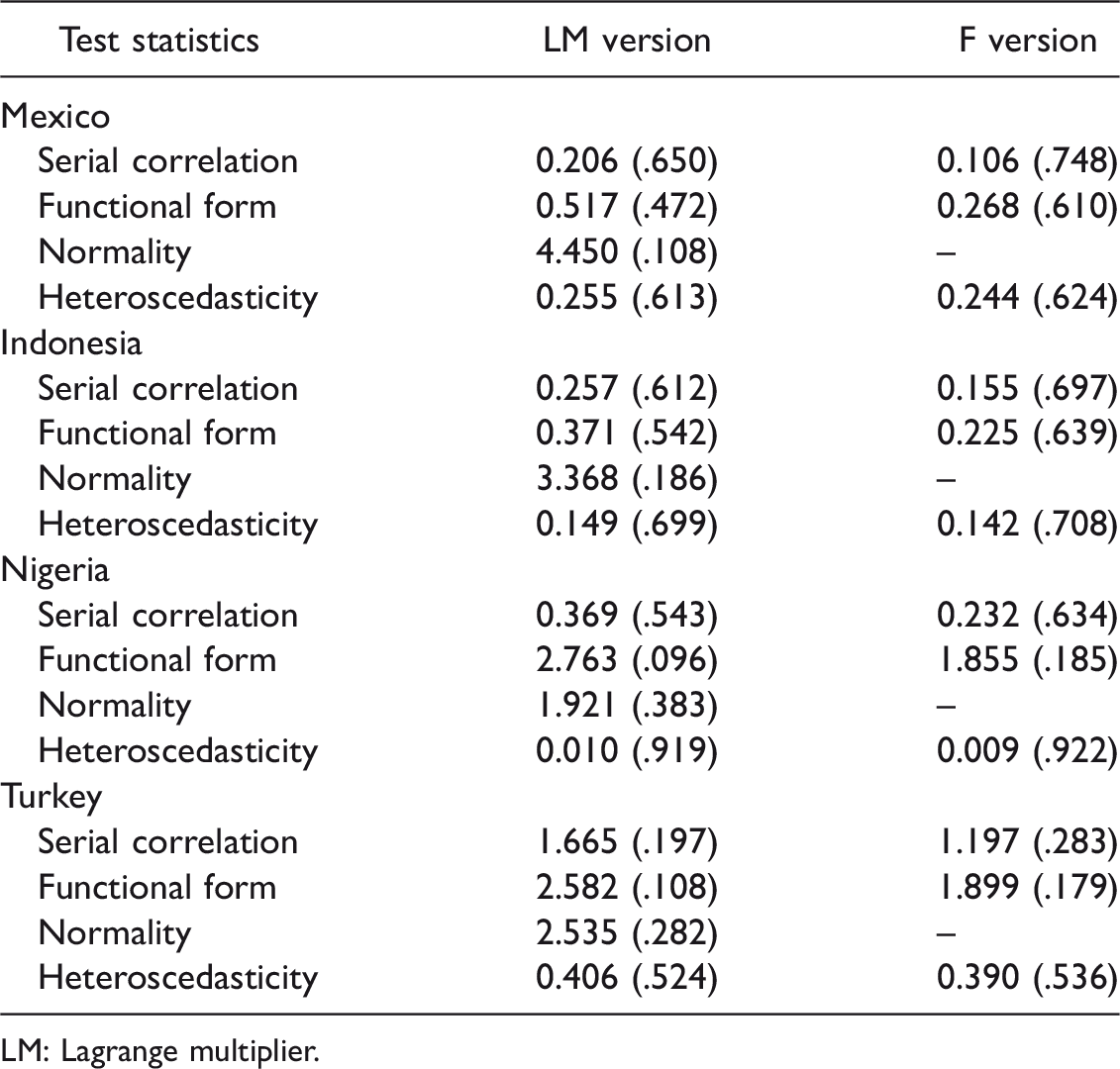

After revealing the level relationship between variables in the conducted models, the robustness of the ARDL models was investigated. Existence of serial correlation, functional form, normality, and heteroscedasticity were investigated by calculating Lagrange multiplier (LM) and F-statistics for the ARDL models. Diagnostic test results in Table 2 suggest that the ARDL models for the MINT countries have no diagnostic problems as probability values of both LM and F-statistics are insignificant at a 5% level of alpha.

Diagnostic test results.

LM: Lagrange multiplier.

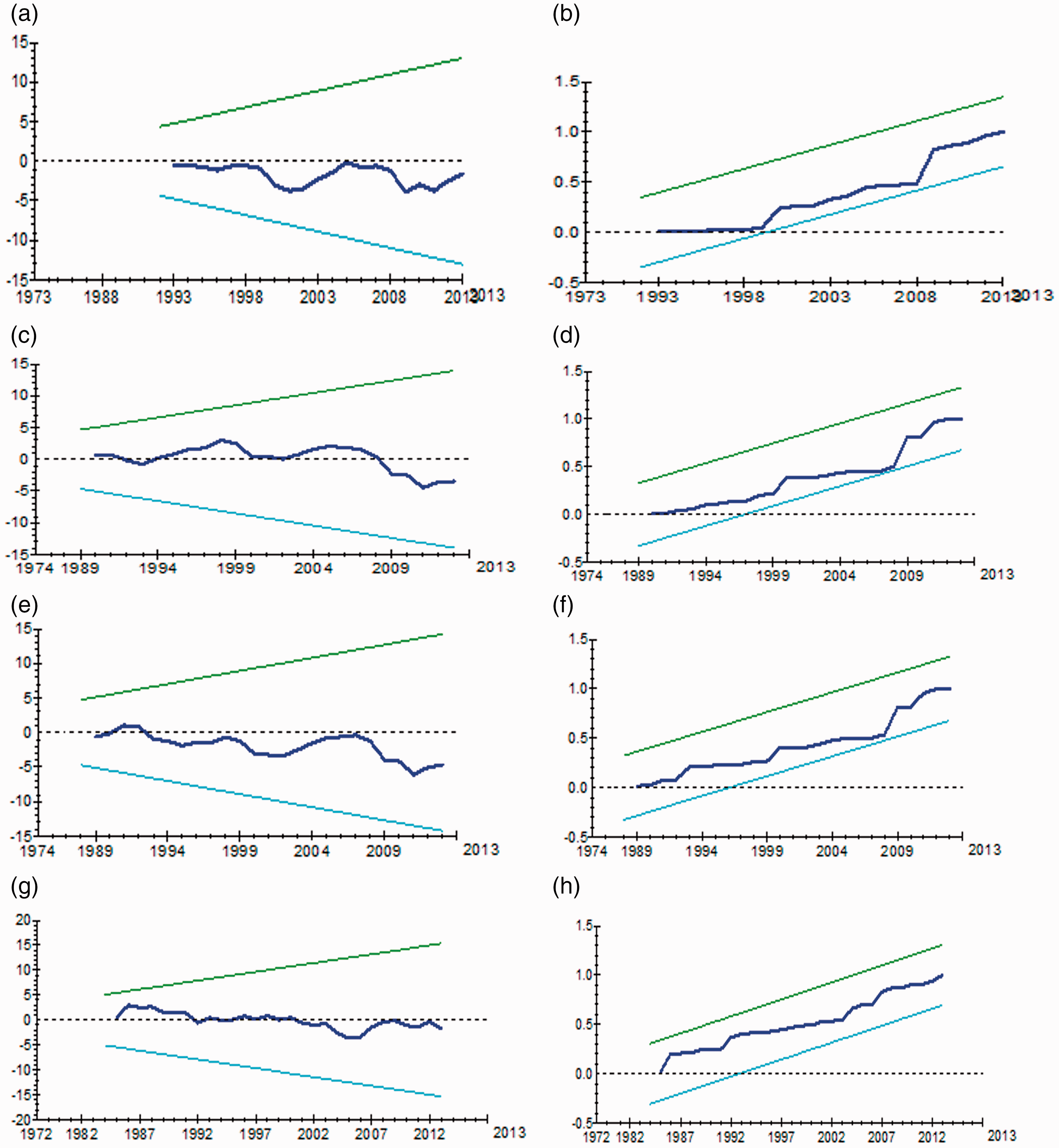

The stability of the ARDL models was investigated using the CUSUM and CUSUMSQ methods. Figure 1 indicates the CUSUM and CUSUMSQ graphs for Mexico, Indonesia, Nigeria, and Turkey, respectively. According to these methods, the conducted ARDL models were stable in both the long and the short run.

Stability test results. (a) CUSUM for Mexico, (b) CUSUMSQ for Mexico, (c) CUSUM for Indonesia, (d) CUSUMSQ for Indonesia, (e) CUSUM for Nigeria, (f) CUSUMSQ for Nigeria, (g) CUSUM for Turkey, and (h) CUSUMSQ for Turkey. The straight lines represent critical bounds at 5% significance level. CUSUM: cumulative sum; CUSUMSQ: cumulative sum of squares.

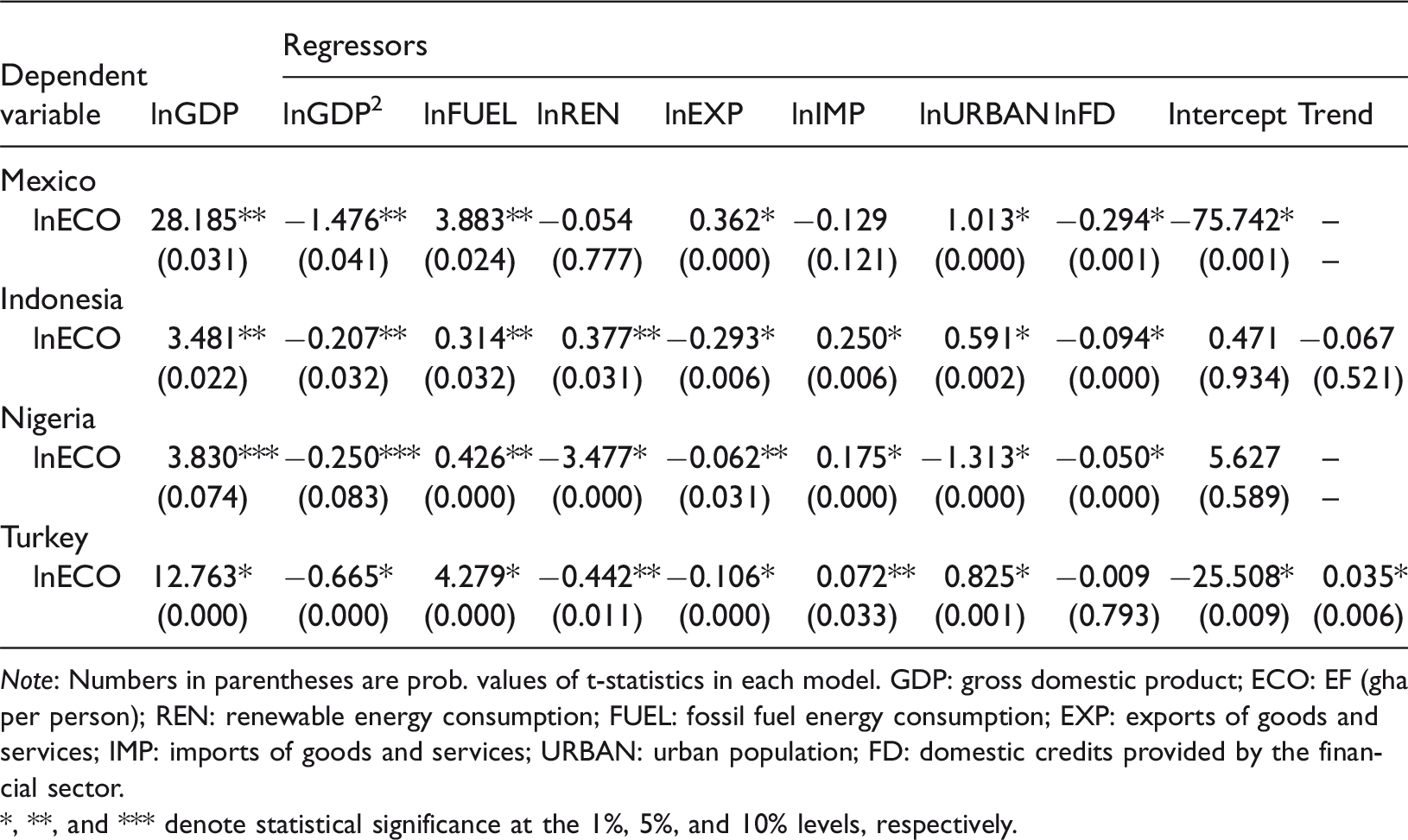

The level coefficients were estimated by applying separate long-run ARDL models for each country individually. Table 3 summarizes the results of the long-run ARDL estimations. The existence of the EKC hypothesis can be tested by comparing the long-run coefficients of the GDP and squared GDP. If the coefficient of the GDP is statistically significant and positive while the squared GDP is statistically significant and negative, the EKC hypothesis holds for the host country. When we compared the estimated long-run coefficients of the GDP and the squared GDP for Mexico, Indonesia, Nigeria, and Turkey, respectively, the estimated coefficients of the GDP were statistically significant and positive while the estimated coefficients of the squared GDPs were negative. Our findings suggest the existence of the EKC hypothesis for the cases of MINT countries. Turning points of per capita GDPs for Mexico, Indonesia, Nigeria, and Turkey are calculated as US$14,013, US$4483, US$2079, and US$14,705, respectively. These findings indicate that turning points of Mexico, Indonesia, and Turkey are not within the range of sample per capita GDP, meaning that they have not reached their turning points yet. On the other hand, turning point of Nigeria is within the sample per capita GDP. Our empirical findings show that in term of implied turning point there is no uniformity among the countries under investigation.

Level coefficients in the long-run model through the autoregressive distributed lag approach.

Note: Numbers in parentheses are prob. values of t-statistics in each model. GDP: gross domestic product; ECO: EF (gha per person); REN: renewable energy consumption; FUEL: fossil fuel energy consumption; EXP: exports of goods and services; IMP: imports of goods and services; URBAN: urban population; FD: domestic credits provided by the financial sector.

*, **, and *** denote statistical significance at the 1%, 5%, and 10% levels, respectively.

The findings of the ARDL estimations suggest that, in the long run, fossil fuel energy consumption, exports, urbanization, and financial development are the common significant determinants of the EF, which is used as a proxy for environmental degradation for the cases of the MINT countries. Renewable energy consumption is statistically significant and has an elastic, negative impact on the EF for the cases of Mexico, Nigeria, and Turkey. This finding suggests that increasing the usage of renewable energy reduces the environmental degradation, and this contradicts the findings of Apergis et al. 115 and Bölük and Mert. 87 In the literature, exports and imports are well-known determinants of environmental degradation. Our findings indicate that imports contribute to environmental degradation in Indonesia, Nigeria, and Turkey, while exports reduce the environmental degradation, meaning that imports increase the domestic consumption and contribute to EF of the host countries. Our results are consistent with Liddle 95 and Hasanov, Liddle, and Mikayilov. 116 Moreover, urbanization in Indonesia, Turkey, and Mexico have a statistically significant and positive impact on the EF in the long run. On the other hand, there is a significant long-run negative relationship between urbanization and EF in Nigeria. The estimated negative impact of urbanization in the case of Mexico supports the findings of Ozturk et al. 80 Finally, financial development has statistically significant and negative impact on EF for the case of Mexico, Indonesia, and Nigeria, meaning that these countries are successful in allocating their financial resources to improve environmental quality in the long run.

The speed of adjustments and short-run coefficients were estimated by adopting the ECM through the ARDL approach. Table 4 indicates the results of the ECMs through the ARDL approach for the cases of MINT countries. The ECM models suggest that the EFs of the MINT countries converge to their long-run equilibrium levels by 162.4%, 93.7%, 68.4%, and 99.9% speed of adjustments every year by the contributions of the short-run values of the GDP, GDP squared, fuel, renewable energy consumption, exports, imports, urbanization, and financial development, respectively. In addition, there are statistically significant short-run impacts of regressors on the EF at different lag levels for the cases of the MINT countries.

Conditional error correction model through the autoregressive distributed lag approach.

Note: GDP: gross domestic product; ECO: EF (gha per person); REN: renewable energy consumption; FUEL: fossil fuel energy consumption; EXP: exports of goods and services; IMP: imports of goods and services; URBAN: urban population; FD: domestic credits provided by the financial sector.

*p-lag structures in the model.

The directions of the long-run relationships among variables were revealed by adopting Granger causality test through the vector error correction model. Results of the Granger causality test are summarized in Appendix 1. Panels (a), (b), (c), and (d) indicate results of the causality test for the cases of Mexico, Indonesia, Nigeria, and Turkey, respectively. There are unidirectional causal relationships running from the GDP, squared GDP, renewable energy consumption, fuel energy consumption, exports, imports, urbanization, and financial development to the EF. Unidirectional causal relationships suggest that, when there is a change in real income, squared real income, renewable energy and fossil fuel energy consumption, exports, imports, urbanization, and financial development, respectively, there is a change in the EF of MINT countries. Moreover, as it can be seen in panel (b), there are unidirectional causal relationships running from the GDP, squared GDP, renewable energy consumption, fuel energy consumption, exports, imports, financial development, and the EF to urbanization for the case of Indonesia. Causal relationships which are running from energy consumption variables to urbanization are in line with Liddle and Lung. 117

Conclusion

Our study investigated the validity of the EKC hypothesis for each of the MINT countries. In contrast to the majority of empirical studies that use a single variable as a measure for the environmental pollution to test the EKC hypothesis, we used a more inclusive measure, namely, the EF as a proxy for the pressure on the environment. We used a time series approach to estimate the country-based coefficients which enabled us to identify the most suitable policy implications for each country in our sample. The long-run equilibrium relationships among the EF, fossil fuel energy, renewable energy consumption, exports, imports, financial development, and urbanization were revealed by adopting the bounds testing approach for the cases of the MINT countries. The ARDL model estimations confirmed the validity of the EKC hypothesis for each of the four countries under investigation. Another common finding for each of these countries is the significant effects of exports, urbanization, and fossil fuel consumption on the environmental degradation index. This finding signifies the importance of energy efficiency in emerging countries. In order to increase their energy efficiency, emerging countries should take some actions to achieve the usage of clean energy in their industries. Creating financial incentives, such as tax credits, subsidies, and grants, and setting national regulations can lead to increases in the adoption of clean technology and, in turn, efficient usage of energy by polluting industries. They can also provide an award mechanism to encourage polluting industries to adopt clean energy.

Our results show that the effects of renewable energy, international trade, urbanization, and financial development differ among these countries. Financial development has statistically significant and negative impacts for Mexico, Indonesia, and Nigeria, which means that financial systems of the host countries are successful to direct the financial resources to environmental friendly sectors. Financial resources can be used to increase the level of public awareness and to encourage polluting industries to adopt clean energy and new pollution mitigating technologies by providing subsidies and soft loans. Also, financial resources can be used to encourage polluting industries for investing in environmental friendly projects to reduce environmental degradation. The inverse relationship between urbanization and environmental pressure that was observed in Nigeria shows that the urban planning strategies of these countries can overcome the negative effects of urbanization on the use of environment. The long-run coefficient of renewable energy consumption for the cases of Nigeria and Turkey suggests a negative relationship between renewable energy and environmental pollution. This finding indicates that increasing the level of renewable energy consumption for these countries is a possible solution for environmental pollution. The policy makers of Mexico and Indonesia should invest more in research and development (R&D) activities in order to achieve the efficient usage of renewable energy and promote the adoption of clean technology in the production phase of renewable energy. Another remarkable result, in terms of policy implementation, is the effects of exports and imports on environmental pollution. Exports contribute to the environmental quality in Indonesia, Nigeria, and Turkey, while imports increase the level of environmental degradation. Policy makers of these three countries should be aware of the positive impacts of imports and take precautions against the negative impact of imports on environmental quality.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.