Abstract

This article addresses ongoing debates about whether the welfare state hinders or fosters self-employment. Starting a business can be an inherently risky undertaking and is thus not a feasible option for all people. Policies that have the potential to shoulder some of this risk can be particularly important for the decision to enter into self-employment. Taking individual differences in terms of risk tolerance into account, we focus on unemployment protection for the self-employed – a type of risk which is particularly difficult to privately insure oneself against – in order to investigate the ways in which policy can shape people’s perceptions of self-employment. We combine individual-level data from a 2009 Flash Eurobarometer survey with country-level data on unemployment policies in Europe in a multilevel design, finding that the presence of unemployment protection for the self-employed positively influences individual perceptions of the feasibility of self-employment. Risk-tolerant individuals, moreover, are found to be even more likely to assess self-employment as a feasible option in countries that offer unemployment protection to the self-employed.

Introduction

In the wake of the economic crisis, many governments sought to promote self-employment and business start-ups as a means of spurring job growth. For example, the European Commission’s (2010a) Europe 2020 strategy for ‘smart, sustainable and inclusive growth’ places particular emphasis on entrepreneurship and self-employment (see also Copeland and Daly, 2012). It must, however, be acknowledged that starting one’s own business is not feasible for everyone given the risky nature of many ventures. We therefore argue that welfare policies that in effect shoulder some of the risk of starting one’s own business should positively impact the extent to which people view this undertaking as feasible. While this is not a new argument – many before us have theorized and empirically investigated the influence of the welfare state on entrepreneurial activity (Stenkula, 2012) – we turn the focus to specific social policies that should have particular importance for the would-be self-employed – that is, unemployment insurance programmes for this group. Although there has been much scholarly debate over whether large welfare states in general hinder or foster entrepreneurship (Braunerhjelm and Henrekson, 2013; Henrekson, 2005), we argue that it is perhaps more meaningful to zoom in on the specific aspects of the social welfare system that may be particularly influential for individual perceptions of the feasibility of self-employment. After all, as public policies are meant to shape the behaviour of individuals, the existence of specific policy arrangements should be reflected in behavioural patterns (e.g. Dvouletý and Lukeš, 2016; Shafir, 2013).

Regardless of how and which welfare policies attempt to increase self-employment, it is clear that this employment option is not for everyone, for striking it out on one’s own is an inherently risky undertaking. Behavioural approaches acknowledge that public policies may not exert uniform effects across all groups of people (Chetty, 2015): For example, some people are simply more risk-tolerant than others and may therefore be more likely to see self-employment as more feasible compared to risk-averse individuals. We know from studies on the psychological roots of self-employment and entrepreneurship (Ahn, 2010; Cramer et al., 2002; Dvouletý and Lukeš, 2016; Kihlstrom and Laffont, 1979; Simoes et al., 2015; Skriabikova et al., 2014) that individuals differ with regard to their personalities and the ways in which they perceive and, consequently, react to contextual impulses (e.g. Stephan et al., 2015; Tonoyan et al., 2010) – such as social policies. We therefore argue that the impact of social policy is dependent on an individual’s level of risk tolerance. In more detail, we ask, ‘How do social policies impact individuals’ perceptions of the feasibility of self-employment?’ Moreover, does the willingness to take risks modify the relationship between policy and self-employment perceptions? By integrating two hitherto separate research strands, we advance an inter-disciplinary approach to deepen our understanding of the relationships between policies, personality and the perceived feasibility of self-employment. This comprehensive perspective can therefore shed light on the impact of (social) policies on individuals’ attitudes and behaviours concerning self-employment.

This article proceeds as follows: following a discussion of the individual determinants of self-employment activities and attitudes, we examine the ways in which social policy may impact the perceptions of the feasibility of self-employment. We derive hypotheses that account for differences in individual personality which we then test using individual-level data from a 2009 Eurobarometer Flash Survey combined with information about 27 European countries’ overall social expenditures and their social insurance for the self-employed. After presenting the results, we conclude with a discussion of the implications of our research and the ways forward.

Who are the self-employed?

There is a large literature examining the determinants of self-employment and entrepreneurship on both the macro and individual level (Bosma et al., 2005; Dvouletý and Lukeš, 2016; Freytag and Thurik, 2007; Koellinger and Minniti, 2009; Koellinger and Thurik, 2012; Lepoutre et al., 2013; Tonoyan et al., 2010). 1 The literature has identified numerous individual-level traits that have been linked to self-employment and entrepreneurship. Generally speaking, the better educated, males, higher earners, older persons, people who come from entrepreneurial families, risk-tolerant individuals and persons with high levels of social capital are more likely to engage in entrepreneurial activities (Román et al., 2013). While the bulk of the literature on individual determinants addresses entrepreneurship, there is a great deal of overlap with regard to self-employment, as shown by Simoes et al. (2015). We only refer to self-employment, as the survey data we work with explicitly ask respondents about their perceptions regarding self-employment.

The extant literature also offers some very intuitive answers to the question of who becomes self-employed: Both perceptions of desirability and feasibility weigh heavily in the individual decision to engage in self-employment. Ajzen’s (1988, 1991) theory of planned behaviour and Shapero and Sokol’s (1982) model of entrepreneurial events underscore the key role perceptions play for predicting future employment intentions and decisions. Perceived feasibility thereby constitutes the self-evaluation of one’s own competence and capacities necessary for achieving a task or behaviour, here, self-employment, referring to both the perception of individual skills and opportunity perceptions (Krueger and Dickson, 1994). The more one believes he or she has the competence to execute a target behaviour, the greater the likelihood that the person will carry out this action. In this regard, perceived feasibility constitutes a measure of behavioural control and is similar to Bandura’s (1986) self-efficacy concept. Prior studies demonstrated that those who see self-employment as something feasible will be more likely to partake in this type of economic activity than those who hold less optimistic views of this employment option (Ajzen, 1988; Arenius and Minniti, 2005; Bergmann, 2004a, 2004b; Koellinger et al., 2007; Lee et al., 2004; Segal et al., 2005; Shapero and Sokol, 1982; Sternberg et al., 2007).

How self-employment is perceived varies across countries: while Scandinavians tend towards more positive evaluations of the general feasibility of self-employment, people from both the Mediterranean and the Benelux countries perceive greater hurdles to self-employment. In other words, although people may perceive self-employment as a desirable option (Sternberg et al., 2007), they may nevertheless view it as a less feasible option due, for example, to a lack of finances, self-efficacy, administrative hurdles or a lack of information (European Commission, 2010b). Moreover, there is much less variation in terms of the perceived desirability of self-employment compared to the perceived feasibility (e.g. Guerrero et al., 2008). From this, it follows that the perceived feasibility is more useful for differentiating between groups of respondents who may eventually decide to start their own business. The perceived feasibility of self-employment is moreover where policy arrangements come into play: policies can influence how individuals perceive the risks and benefits associated with starting a business (Debus et al., 2017; Parker, 2004). Policies therefore delineate the opportunity structure within which individuals calculate the expected costs and benefits of an action, which eventually induces them to take action – or not.

In addition to the demographic characteristics and perceptions of the self-employed, we also know quite a bit about the attitudinal and personality attributes which may set them apart from non-self-employed individuals. The literature speaks of entrepreneurial mindsets (Haynie et al., 2010; Ireland et al., 2003), the entrepreneurial personality (Korunka et al., 2003; Vecchio, 2003) and specific sets of values (Licht, 2007) that have been shown to be related to an increased propensity to engage in entrepreneurial and/or self-employment activities, the desire or intention to do so, or to view self-employment in a generally positive light. There furthermore appears to be consensus in the literature that self-employment comprises a behavioural characteristic (Wennekers and Thurik, 1999). While entrepreneurial characteristics have been described and analysed using a variety of combinations of social–psychological concepts and adjectives, the concept of risk tolerance or low risk aversion appears to be common to a majority of approaches (Caliendo et al., 2009; Cramer et al., 2002; Ekelund et al., 2005; Kihlstrom and Laffont, 1979; Koudstaal et al., 2015; Skriabikova et al., 2014). Attitudes towards risk, as we argue below, seem to play a central role not only for the individual decision to engage in self-employment, but could also provide us with insights into how policies may impact people’s attitudes towards self-employment.

Social policies, risk and the feasibility of self-employment

Beyond the numerous ways in which individuals differ in terms of their personalities, socio-economic backgrounds and whether they see self-employment as something feasible, we also must acknowledge that the socio-political context in which a person lives plays a role in these employment decisions (e.g. Dvouletý and Lukeš, 2016; Stephan et al., 2015). In line with the findings that individual perceptions and decisions are context-dependent, we argue that policies represent contextual factors that can shape individuals’ perceptions (Almond and Verba, 1963; Books and Prysby, 1988; Debus et al., 2017). In a wider sense – and following the neo-institutionalist approach – policies can be considered as instances of institutions (Pierson, 2006) and have the potential to impact individual opinions and decisions. We thus argue that unemployment protection policies can ‘frame’ the way in which individuals perceive self-employment. Moreover, we have reasons to believe that different contexts can shape individuals’ risk perceptions as pertains to self-employment. Given the cross-national variation in self-employment rates, the question thus arises as to the influence public policies can have, not only on self-employment decisions, but also regarding how risky these decisions are perceived to be. In the following section, we review the literature linking the welfare state and self-employment and how risk comes into play.

The question of whether a generous, extensive system of social welfare ultimately fosters or suppresses self-employment activity has yet to be definitively answered. It has been conjectured that the welfare state, as a system designed to protect against a variety of different types of risks, can also protect against the risks associated with striking it out alone: ‘Protected by the welfare state, people engage in risky and profitable activities which they otherwise would not have dared to take’ (Sinn, 1994: 1). Due to its systems of social insurance, risk-taking is encouraged by the welfare state. Highly redistributive taxation and social insurance can thus enhance safety and stimulate risk-taking, much like private insurance can, as the state bears part of the risk in economic decisions (Sinn, 1996).

Bird (2001), drawing on Sinn’s (1996) models of risk-taking, finds empirical evidence for the claim that the welfare state encourages risk-taking: Redistribution functions as a form of income insurance that would reduce the potential losses of risky endeavours and investments. Similar conclusions have also been made by Cullen and Gordon (2007), who find that, contrary to conservative political rhetoric in the United States, higher taxes can actually encourage taking risks in terms of business decisions. Lower tax rates imply less risk-sharing with the government, thereby making self-employment risks less attractive to the risk-averse.

Numerous examples of self-employment-enhancing social policy hail from the United States. For example, Olds (2016) examines the food stamp programme during the early 2000s, finding that the expanded eligibility led to an increased likelihood that newly eligible households would own own their own business. Although most of the new entrepreneurs did not enrol in the programme, Olds argues that new business formation was made less risky by expanding the eligibility of food stamp programmes. In other words, knowing that the programme exists and could be used should the business fail appeared to boost self-employment.

A 2001 reform of French unemployment benefits had the unintended side effect of increased self-employment (Clasen and Clegg, 2003). Prior to 2001, starting a new business meant the unemployed would have to forfeit their unemployment benefits; the reform allowed people to continue receiving benefits under certain conditons and furthermore guaranteed that if the business failed, recipients would automatically become re-eligible. Firm creation rose 25 percent following this reform (Hombert et al., 2014). Such findings underscore the ways in which policy design, particularly in terms of eligibility, can potentially impact employment activities. While the examples mentioned are anecdotal, they nevertheless illustrate the ways in which welfare policies can make the option of self-employment more viable due to the ways in which they have been able to reduce some of the risks and uncertainties associated with starting one’s own business.

Despite the numerous studies which theoretically and/or empirically demonstrate a positive relationship between the welfare state and entrepreneurship, primarily due to the way in which social policies can serve to abate potentially risky activities, there is a further body of evidence showing that generous welfare state arrangements stifle self-employment (Robson, 2010; Torrini, 2005). For example, Robson (2010) hypothesizes that high unemployment replacement rates discourage the unemployed from entering into self-employment, as high levels of benefits encourage people to wait longer for job openings. This study illustrates a case in which necessity-based entrepreneurship may be suppressed when the necessity itself is addressed by generous unemployment programmes. Swedish entrepreneurship, for example, tends to be nearly entirely opportunity-based (Braunerhjelm and Henrekson, 2013). Even in Swedish regions with higher unemployment, necessity-based entrepreneurship is largely absent (Robson 2010). In other words, entering into self-employment from unemployment may yield a fall in one’s standard of living (Henrekson, 2005). Acemoglu and Shimer (2000) furthermore find the unemployed may search less intensely and thus spend more time unemployed when unemployment insurance is high; however, they arrive at the finding that moderate unemployment insurance can encourage people to pursue riskier options, such as self-employment, due to the balance of risk-sharing.

Henrekson (2005) argues that not only is necessity-based entrepreneurship crowded out by the Swedish welfare state, but the economic incentives for opportunity-based activities are suppressed as well. Examples include the high rates of taxation on entrepreneurial income, negative incentives for savings and individual wealth, high tax rates and the attractiveness of public employment in Sweden. Finally, Ilmakunnas and Kanniainen (2001), in their study of 19 Organisation for Economic Co-operation and Development (OECD) countries, find that welfare states create incentives that are detrimental to risk-taking with regard to starting a business. They find that large public sectors, such as those found in extensive welfare states, limit entrepreneurial opportunities. Moreover, they argue, contrary to Sinn (1994, 1996), that welfare states do not necessarily provide insurance against entrepreneurial risk in the same way they protect against labour risks.

Taking both lines of argument into account, we arrive at two competing assumptions regarding the impact of the welfare state on individual attitudes towards self-employment: that is, there are reasons to expect either a positive or a negative impact on the perceptions of self-employment as a feasible option.

Although there are many plausible arguments to be made for the welfare state as an obstacle to as well as a fosterer of self-employment, and empirical investigations seem to be continuously adding evidence to both sides of the debate, we would argue against an over-reliance on broad labels, such as universal, Nordic, continental or liberal, when examining and comparing cross-national self-employment, for doing so overlooks both the nuances in policy design and risks masking the cross-country differences in social programmes for the self-employed. Just as welfare states differ in terms of their policy spending foci – for example, high spending on the working-age population does not necessarily mean an equally high spending level on pensions or health care (Castles, 2008) – countries’ unemployment insurance programmes, for instance, can also vary across occupational groups. For example, a state with generous unemployment benefits may not extend the same level of generosity to self-employed persons. The design of unemployment protection for the self-employed varies widely; these different designs may in turn be a more meaningful source of variation in terms of the effects of the welfare state on self-employment. For example, it is conceivable that self-employment becomes much less risky and perhaps more feasible when self-employed individuals are able to enjoy more or less equal protection as their dependently employed counterparts. On the other hand, where unemployment protection is completely absent for the self-employed – that is, where neither compulsory nor voluntary programmes are available – self-employment may become a much riskier undertaking and thus may not be viewed as feasible. Moreover, if the only option for self-employed persons needing unemployment assistance are means-tested, highly conditional programmes, self-employment may also not seem such a worthwhile activity, for not only do such programmes tend to offer relatively low unemployment support, there is often a certain degree of stigma attached to being a recipient (Rothstein, 2001).

Welfare states of course do many other things beyond protecting against the risk of unemployment, and their functions have also evolved over time (e.g. Green-Pedersen and Haverland, 2002; Jensen, 2008, 2012; Jensen et al., 2014; Wolf et al., 2014). Countries do not, however, tend to have markedly different retirement and healthcare programmes for the self-employed versus dependently employed (e.g. Schoukens, 2002). While the self-employed are generally required to make social security contributions, they do not have employer contributions and, like many of their dependently employed counterparts, must rely on occupational and/or private schemes to save for old age beyond the basic statutory entitlements. Furthermore, unlike the risks associated with old age and health, it is much more difficult to privately insure oneself against the risk of unemployment (Moene and Wallerstein, 2001; Rehm, 2009). We therefore expect unemployment programmes for the self-employed to be particularly relevant for the perceptions of self-employment, that is, that the presence of such programmes will have a positive impact on individuals’ perceptions of the feasibility of self-employment.

The moderating role of risk aversion/risk-taking

Numerous studies have documented the pivotal role of attitudes towards risk, something which has not only been empirically well documented but is also a very intuitive answer to the question, ‘What kind of person becomes self-employed?’ The intuitive answer would tell us that since starting one’s own business is an activity that ultimately involves some degree of uncertainty, people who have greater risk tolerance may also be more likely to engage in entrepreneurial activities. This line of reasoning underscores the assumptions made by numerous classical economists (Knight, 2002; Say, 1971) and found a great deal of traction in occupational choice models (Blanchflower and Oswald, 1990; Kanbur, 1979; Kihlstrom and Laffont, 1979). These theoretical assumptions about the positive influence of risk-taking on self-employment decisions have also been documented empirically (Barbosa et al., 2007; Caliendo et al., 2009; Cramer et al., 2002; Ekelund et al., 2005; Stewart and Roth, 2001). Overall, the literature points to a positive influence of low risk aversion on entrepreneurial behaviours. Kan and Tsai (2006: 465), for example, find that status security offered by social policies decreases risk aversion, leading to a higher willingness to engage in the more risky occupation of self-employment.

The question, however, arises as to who is actually affected by these risk-reducing policies. Concerning the relationship between policies and risk aversion, we argue that the impact of social policies on the perceived feasibility of self-employment depends on an individual’s risk tolerance. In general, policies are thought to be designed so as to reach the broadest possible swathe of their target population (Howlett et al., 2015; Howlett and Mukherjee, 2014). We thus anticipate social insurance programmes aimed at the self-employed to contribute to feelings of security and reduce individual anxieties. These types of social policies therefore are designed to assuage the risks of striking it out alone. Social policies may, however, affect individuals’ perceptions in different ways and to varying degrees. For example, while an unemployment scheme may be universally designed, it could affect risk-tolerant and risk-averse individuals differently. We therefore examine whether social policies actually fulfil their risk-reducing purpose by altering risk-averse individuals’ probability of perceiving self-employment as feasible. If these policies truly lower general risks and anxieties, then the differences between risk-averse and risk-tolerant individuals should be smaller, and both should have similar perceptions of the feasibility of self-employment. We thus hypothesize the influence of social policies on the perception of the feasibility of self-employment to be the greatest for individuals with high risk aversion.

Data and methods

To test our hypotheses, we use data from the 2009 Flash Eurobarometer 283 (European Commission, 2010b). Our final sample comprises roughly 12,900 respondents of age 15–67 2 from 27 European countries. Our main variable of interest is the perceived feasibility of self-employment, which is captured by the following question: Would it be feasible for you to be self-employed within the next 5 years? The answer categories range from 0 = not feasible at all to 3 = very feasible (recoded so that higher values indicate higher feasibility). 3 As mentioned, feasibility concerns individuals’ perception about whether becoming self-employed in a given time period is a realistic option. Only those respondents who indicated that they were not currently self-employed were asked this question. The distribution of the dependent variable in the 27 countries is displayed in Figure 1. The graph shows that, on average, roughly 26 percent of respondents think that self-employment could be a feasible option. Second, there is notable variance across countries, with 6 percent of the variance in feasibility stemming from country differences.

Perceived feasibility of self-employment in 27 European countries.

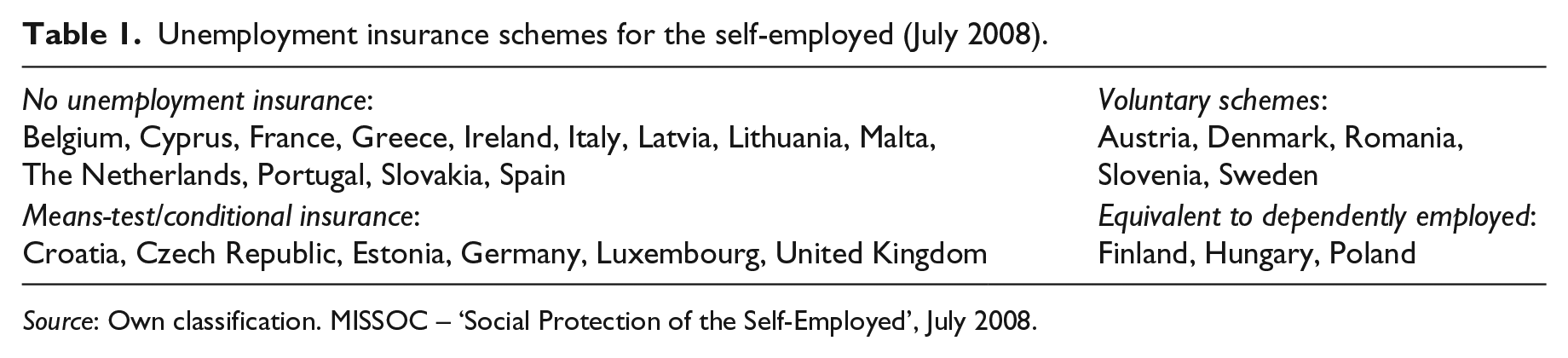

The main independent variables at the country-level variable are general social policies and unemployment insurance programmes for the self-employed. Social expenditures are measured as the total of all social expenditures as a percentage of the gross domestic product (GDP). For the latter independent variable, the data come from the Mutual Information System on Social Protection (MISSOC). MISSOC offers a unique data source on the ‘Social Protection of the Self-Employed’, which covers 32 countries and describes the basic principles as well as specificities of the social welfare system for self-employed persons. The information is updated twice yearly; we use information from July 2008. 4 All country reports include a description of unemployment protection. While the country reports differ in terms of how detailed the programme descriptions are, it is possible to ascertain whether (compulsory or voluntary) unemployment schemes for the self-employed exist and whether they are equivalent to the programmes for the dependently employed or whether there are stipulations concerning eligibility and/or conditionality. In assessing these programmatic data, the first step was to identify the countries in which an unemployment programme for the self-employed exists. We then identified those countries whose programmes were indicated to be identical to the programmes for the non-self-employed. For the remaining country programmes (countries with programmes for the self-employed that are not more or less equivalent to the unemployment insurance for the dependently employed), we made a final differentiation based on whether voluntary unemployment insurance exists (see also Clasen and Viebrock, 2008) or whether other, often means-tested and highly conditional, programmes were available. Table 1 provides an overview of the unemployment insurance programmes in the 27 countries.

Unemployment insurance schemes for the self-employed (July 2008).

Source: Own classification. MISSOC – ‘Social Protection of the Self-Employed’, July 2008.

In terms of the type of programmes that can reduce some of the risk of starting one’s own business, we can clearly say that we do not expect such a risk-reducing effect in the absence of unemployment insurance for the self-employed. The compulsory programmes that are equivalent to the unemployment insurance available for the dependently employed are, on the other hand, most likely to have a risk-diminishing effect. We would say the same of public voluntary schemes, albeit to a lesser degree. The means-tested and highly conditional unemployment programmes could have a risk-reducing component, but because they tend to be much less generous and may often be associated with social stigma, we would classify such programmes as having the potential to do slightly more in terms of risk reduction as compared to the complete absence of such a scheme, but less than voluntary and compulsory-equivalent schemes.

In our analyses, we test a dichotomous variable which groups the countries without any unemployment insurance for the self-employed together with the means-tested programmes and the voluntary and equivalent schemes together. This dichotomous variable captures the main divide in terms of potential risk reduction. 5

The moderator variable, risk aversion, addresses respondents’ agreement to the following statement: In general, I am willing to take risks. The answer categories range from 0 = strongly disagree to 3 = strongly agree (recoded so that higher values indicate stronger agreement). In addition to this moderator variable, further control variables are included on the individual level: gender, education, age and whether respondents live in an urban area. Prior research indicates that middle-aged men with higher levels of education living in metropolitan areas are most likely to be self-employed. In addition to these standard controls, we add a variable measuring the respondent’s general preference for self-employment to the models. 6 Finally, past research has demonstrated that a family history of self-employment is an important predictor of one’s own self-employment; we include an indicator capturing whether neither, either or both parent(s) are (or were) self-employed. A detailed list of all variables can be found in Appendix 1.

As we are dealing with a hierarchical data structure, we further add contextual-level controls; namely, the unemployment rate as well as the access to finance. 7 Both indicators are known to decisively influence the likelihood of becoming self-employed (on the influence of macro-level unemployment on self-employment, see Constant and Zimmermann, 2004; Fairlie, 2013; Rampini, 2004; on access to finance, see OECD, 2009; Sannajust, 2014). We implement multilevel models with cross-level interactions and varying slopes for risk-taking to test our three proposed hypotheses.

Results

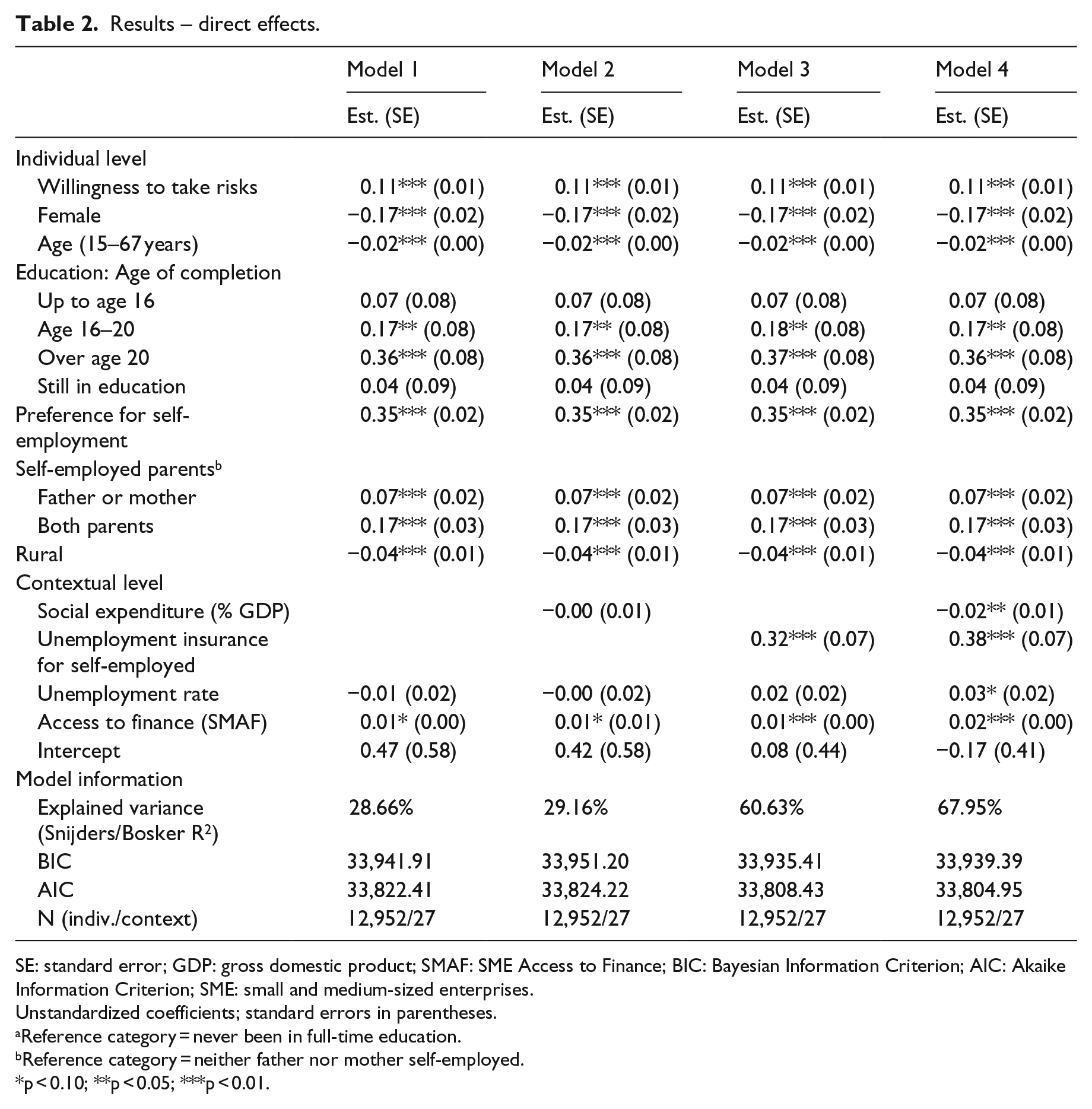

To address our research question on how social policies relate to the feasibility of self-employment and how this relationship is moderated by risk aversion, we run six models in a stepwise procedure: First, we inspect the relationship between different types of social policies, that is, overall spending and unemployment programmes and an individual’s tendency to view self-employment as feasible. In a second step, we implement a random slopesmultilevel model to test the interaction between the willingness to take risks and social policies on the perceived feasibility of self-employment. The results for these estimates are presented in Tables 2 and 3, respectively.

Results – direct effects.

SE: standard error; GDP: gross domestic product; SMAF: SME Access to Finance; BIC: Bayesian Information Criterion; AIC: Akaike Information Criterion; SME: small and medium-sized enterprises.

Unstandardized coefficients; standard errors in parentheses.

Reference category = never been in full-time education.

Reference category = neither father nor mother self-employed.

p < 0.10; **p < 0.05; ***p < 0.01.

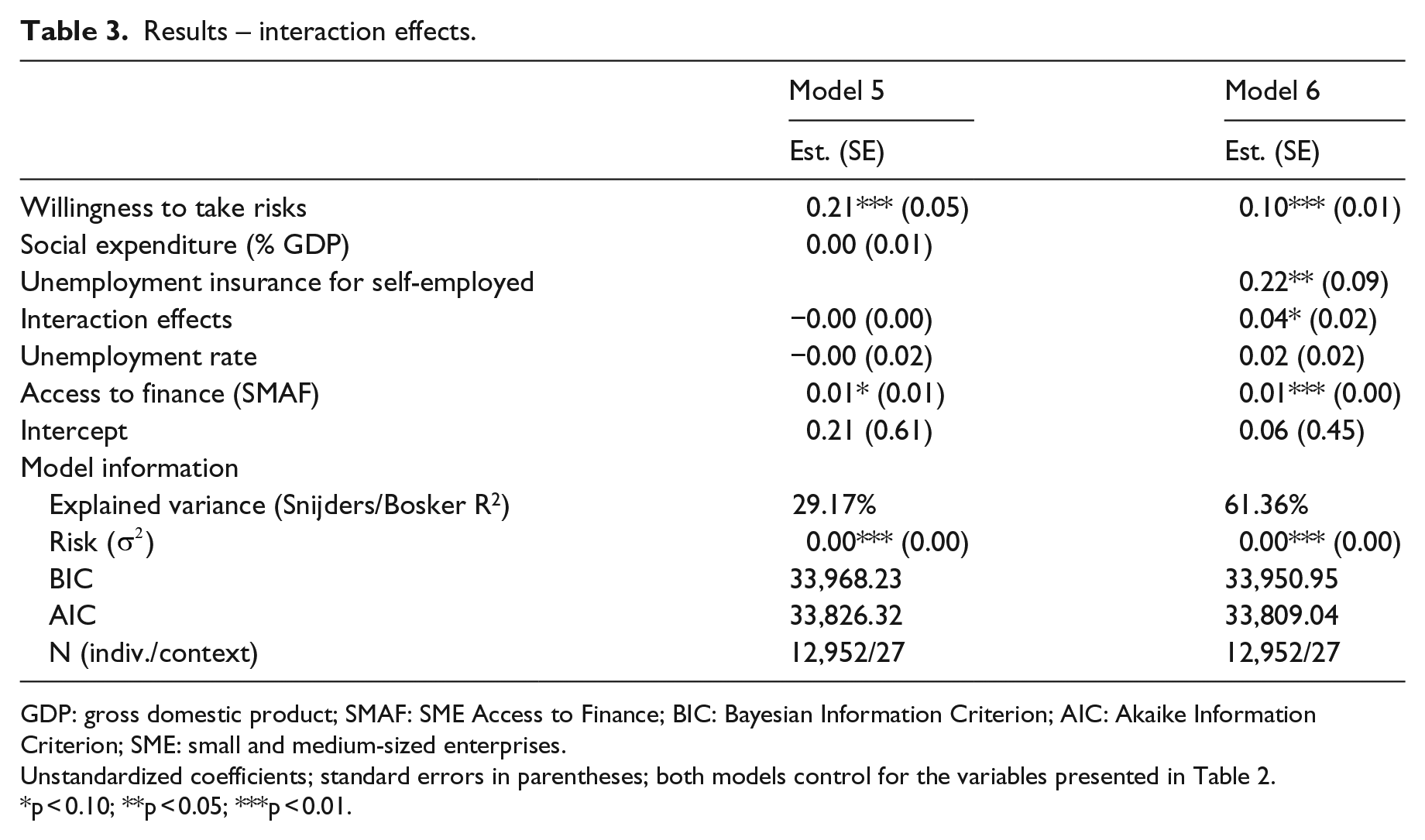

Results – interaction effects.

GDP: gross domestic product; SMAF: SME Access to Finance; BIC: Bayesian Information Criterion; AIC: Akaike Information Criterion; SME: small and medium-sized enterprises.

Unstandardized coefficients; standard errors in parentheses; both models control for the variables presented in Table 2.

p < 0.10; **p < 0.05; ***p < 0.01.

Before turning to our main results, we first estimate a model testing the basic explanations of the perceived feasibility of self-employment. In doing so, we can assess the added explanatory power of welfare policy arrangements to the following models. The results in our baseline model (Model 1) mirror previous findings: older, risk-tolerant, highly educated males from metropolitan areas see self-employment as a very feasible option. Moreover, a family history of self-employment as well as a general preference for self-employment over regular employment positively alters the perceived feasibility of self-employment. On the contextual level, we see that higher unemployment rates relate negatively to the feasibility of self-employment, whereas greater access to financing for starting one’s own business has a positive impact. Only access to finance significantly differs from zero.

Drawing on this baseline model, the following estimates in Models 2–4 add the welfare policy variables in a stepwise procedure: first, hypothesis 1 is tested in Model 2 by adding the overall social expenditures to the baseline estimates. Model 3 introduces the unemployment insurance indicator. Finally, Model 4 combines both social policy measures. Looking at the effect of social expenditure on the perceived feasibility of self-employment in Model 2, we see that while the effect is negative, it fails to reach statistical significance. In contrast, Model 3 reveals that unemployment insurance programmes have a strong positive and significant impact on feasibility perceptions. This supports our argument that risk-reducing welfare policy programmes are able to influence individuals’ perceptions of self-employment. Whereas the broader measurement of welfare policies does not seem to influence perceptions of feasibility, specific programmes for the self-employed do appear to have a decisive effect. This is supported by the greater proportion of the variance explained in Model 3: compared to the social expenditure model, Model 3 accounts for around 60 percent of the contextual variance in the feasibility of self-employment across the 27 countries. Compared to the baseline model, this is an increase of roughly 32 percent, whereas Model 2 – including the overall social expenditure measures – adds almost no additional explanatory power. Moreover, the model fit, measured by the Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC), indicates a better overall fit for Model 3 compared to Models 1 and 2.

To test whether these two social policy indicators are mutually dependent, we implement both measures simultaneously in Model 3. Turning to the results, we see quite similar patterns as before: the effect of the unemployment insurance programmes remains positive and significant – with a slightly stronger effect size. Compared to Model 2, we now observe a significant negative coefficient for the social expenditure measures, indicating that higher total expenditures correspond to decreasing levels of perceived feasibility of self-employment. Although these results underscore the idea that welfare policies specifically designed to reduce risk for the self-employed support the positive evaluation of self-employment, it may, however, be that the effect of both social policy indicators depends on an individual’s willingness to take risks. As discussed in the theoretical section, social insurance programmes seek to reduce risks for the entire target group of a policy, yet we know very little about how this risk-reducing mechanism is moderated by the actual level of risk aversion. Table 3 shows results testing this conditional relationship.

Model 5 presents the results for the interactive relationship between total social expenditures and an individual’s willingness to take risks. We see, however, that this interactive term is insignificant and thus indistinguishable from zero. The above observed negative effect of social expenditures on the perceived feasibility of self-employment seems to be independent of an individual’s tendency to take risks and thereby supports a more fine-grained approach to the effects of policies. Turning to the interaction coefficient (Model 6) testing the dependency between unemployment insurance programmes for the self-employed and the willingness to take risk, we observe a positive and significant coefficient. What does this imply, though? Simply put, the overall positive effect of these unemployment insurance programmes on the perceived feasibility of self-employment is greater for risk-tolerant individuals.

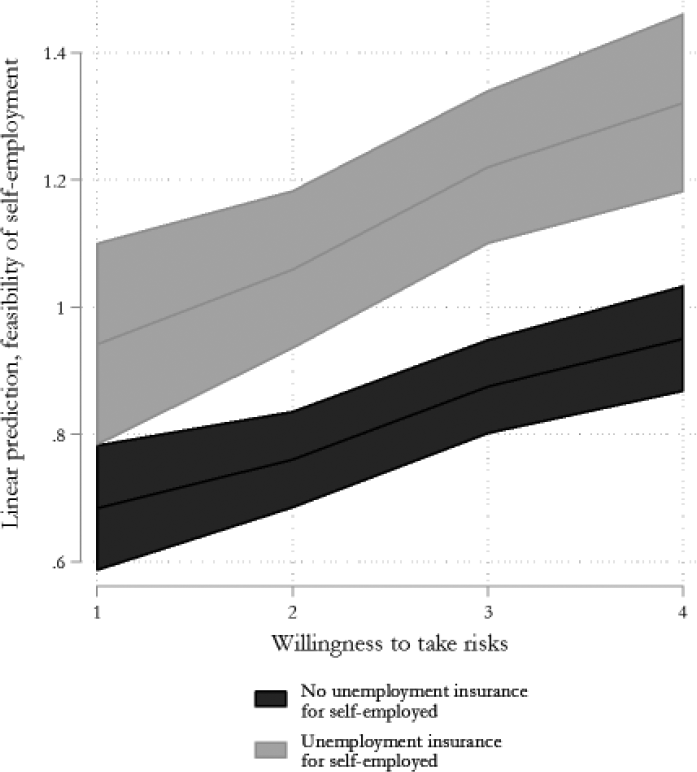

To obtain a clearer picture of this relationship, the results of Model 6 are shown in Figure 2. Here, we see how individuals’ perceptions of the feasibility of self-employment in countries with specific unemployment programmes for the self-employed (as depicted by the grey line) and in countries without (black line) change as the willingness to take risks increases. The grey shaded areas around each of the lines show the 95 percent confidence bands revealing the uncertainty of the estimated result. Figure 2 illustrates that more risk-tolerant individuals hold more positive views of self-employment, regardless of the social insurance programmes for the self-employed. This positive effect of risk-taking on self-employment feasibility is, however, amplified for individuals in countries with unemployment programmes for the self-employed. This effect is significantly different from the effect of risk-taking on perceptions for people in countries without such programmes, as indicated by the non-overlapping confidence bands for both estimated conditional effects. In other words, there is an empirically observable difference in individuals’ perceptions of self-employment as a feasible employment option in countries where unemployment insurance exist and countries where they do not. Where no insurance programme is present and a person is highly willing to risks, the average impact on the perceived feasibility of self-employment is 0.2. In comparison, the same net effect reaches roughly 0.4 if we encounter unemployment insurance programmes for the self-employed and high levels of risk-taking.

Effect of unemployment insurance programmes on the perceived feasibility of self-employment across different levels of risk-taking.

Focusing further on Figure 2, we find that the differences in the conditional effects are largest for highly risk-tolerant individuals; we see the lines continuing to diverge as risk-taking increases. Comparing this result to the assumption that policies are generally designed to affect a group of persons in a universal manner, we see here that the unemployment insurance programmes for the self-employed do not exert a uniform effect on all citizens in terms of how they perceive the feasibility of self-employment. The effect of unemployment insurance programmes on the perceived feasibility of self-employment decisively depends on a person’s willingness to take risks and is distinctively stronger for individual’s with a ‘riskier’ personality. Risk-averse individuals, who in general consider self-employment as less feasible, are, in turn, markedly less affected by these purportedly risk-reducing policies. This speaks against our hypothesis that risk-reducing policies should be of particular relevance for risk-averse persons.

Altogether, our results largely confirm our propositions: first, overall welfare expenditures have the tendency to reduce the perceived feasibility of self-employment, although this effect is weaker than the positive effect witnessed for the unemployment insurance programmes. Second, the existence of unemployment insurance programmes for the self-employed increases the evaluation of self-employment as feasible.

The robustness of our results needs to be examined given that we only have data for 27 countries at a single point in time. One way of testing the robustness of analyses with a rather small number of cases is to test for influential cases which could bias results and interpretations. We therefore estimated Cook’s D as well as dfBetas for our models (see Van der Meer et al., 2010). Belgium and the Netherlands could be identified as potential outliers based on their very low levels of perceived feasibility of self-employment in their respective populations (see Figure 1). We re-estimated our models excluding both cases and obtained similar or slightly better results than those presented above. Although we have a relatively small number of cases at the country level, our analyses show robust and substantive effects. We now know that there is at the very least a strong interactive relationship between the existence of unemployment insurance for the self-employed, an individual’s willingness to take risks and people’s perceptions of the feasibility of self-employment. This evidence allows suggesting that social policies are, first, capable of altering the feasibility of self-employment and, second, that this effect is strongest for risk-takers.

Conclusion

This study examined whether welfare programmes are capable of reducing the risks of self-employment and thereby altering individuals’ perceptions about the feasibility of this employment option. Compared to prior research, we added two innovations: first, we addressed the existing inconsistencies concerning the effect of social policies on the likelihood of starting a business by taking a deeper look at policies that specifically focus on reducing risks for self-employed persons, namely, unemployment insurance for the self-employed. Second, we assessed the assumption that public policies are designed to impact everyone equally, finding that this does not appear to be the case with unemployment programmes for the self-employed – a person’s willingness to take risk was revealed to be a decisive intervening factor.

Overall, this study advances our understanding of how the welfare state influences self-employment and entrepreneurship, arguing that the wide-angle lens often used to examine this question is perhaps less suitable for capturing the fine-grained policy differences that are particularly relevant to people in or considering self-employment. We zeroed in on unemployment programmes for the self-employed across 27 European countries, finding that the presence of these insurance schemes has a positive impact on people’s perceptions of self-employment as a feasible option. Although we expected these programmes to shoulder some of the risk of striking out alone, surprisingly, it was the risk-tolerant whose perceptions were found to be most impacted by the presence of unemployment programmes for the self-employed. While the risk-averse also tended to have more positive views of self-employment in countries with these programmes, the policies perhaps serve to amplify the attitudes and views of risk-takers who already have a higher propensity for self-employment. If it is a policy goal to promote self-employment and entrepreneurship, our results highlight that the mere presence of risk-reducing policies may not be sufficient to substantially impact the attitudes and behaviours of risk-averse individuals. It therefore remains a challenge to design public policies that can also impact those persons who would otherwise not consider starting their own business due in part to their personalities.

In addition to the findings and challenges outlined above, we conclude by outlining a few items for the future research agenda. Beyond people’s own individual tolerance for risk, people also differ in terms of their risk of future unemployment. For example, people in some industries face higher unemployment risks unemployment than others; these occupation-specific risks furthermore vary across countries (e.g. Rehm, 2009). While the data at hand did not allow us to test this further specification, future research should investigate how social policies can impact the perceptions of self-employment for persons in various industries. Second, despite the inroads made in this article towards a more nuanced understanding of the ways in which policies shape individuals’ perceptions of self-employment and how risk tolerance enters into this equation, we are dealing with a single year – namely, 2009. Many individuals were already experiencing the brunt of the economic crisis; others had yet to see the effects unfold. In other words, in order to more robustly test the claims and findings of this article, we need data beyond a single point in time. More specifically, we need to be able to evaluate whether we find shifts in how people perceive self-employment as the economic situation changes and whether social policies aimed at the self-employed moderate economic fluctuations and, finally, whether they do so for different groups. Such a perspective would also better connect our study with the emerging research agenda on behavioural changes brought about or moderated by public policies.

Footnotes

Appendix 1

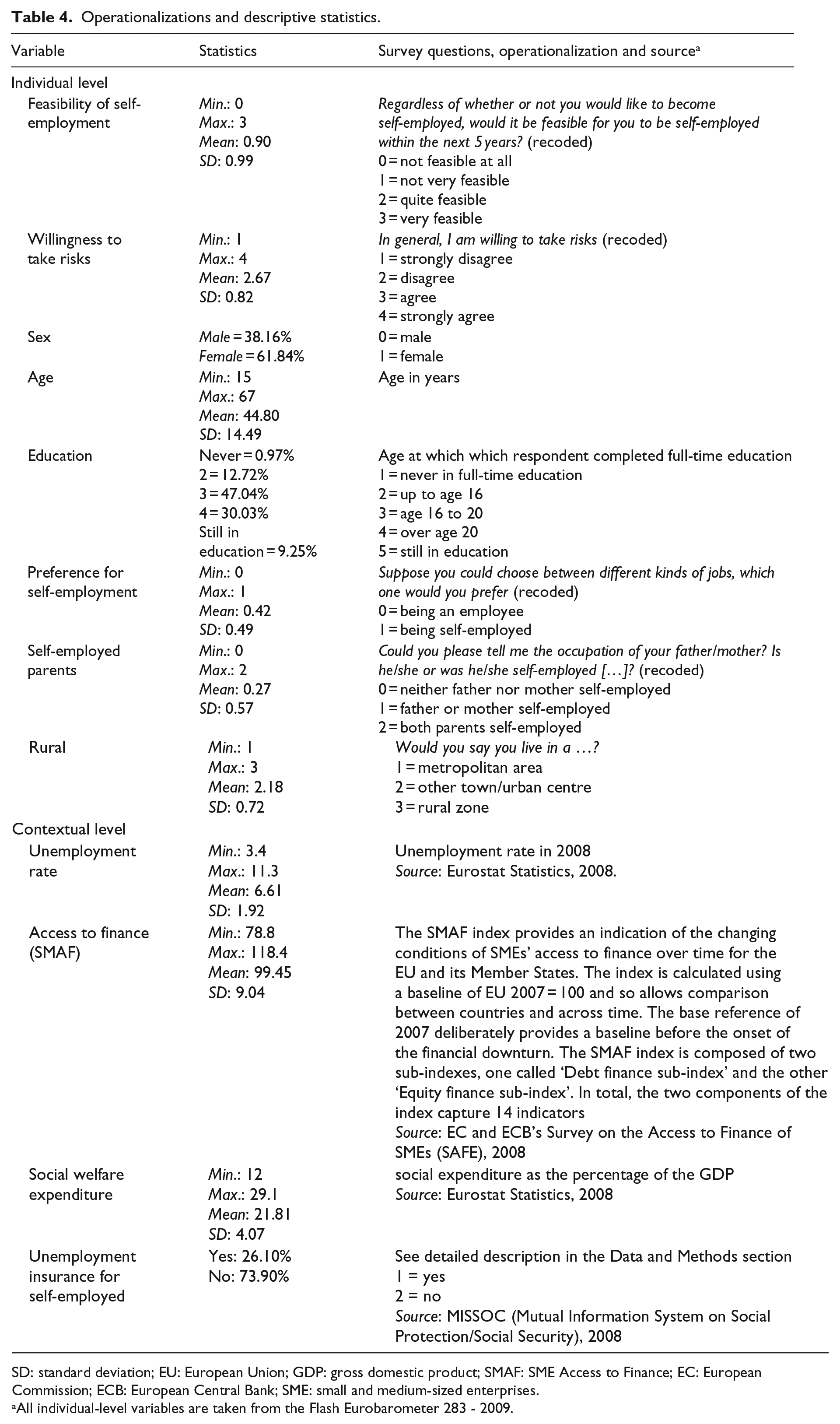

Operationalizations and descriptive statistics.

| Variable | Statistics | Survey questions, operationalization and source a |

|---|---|---|

| Individual level | ||

| Feasibility of self-employment | Min.: 0 Max.: 3 Mean: 0.90 SD: 0.99 |

Regardless of whether or not you would like to become self-employed, would it be feasible for you to be self-employed within the next 5 years? (recoded) 0 = not feasible at all 1 = not very feasible 2 = quite feasible 3 = very feasible |

| Willingness to take risks | Min.: 1 Max.: 4 Mean: 2.67 SD: 0.82 |

In general, I am willing to take risks (recoded) 1 = strongly disagree 2 = disagree 3 = agree 4 = strongly agree |

| Sex | Male = 38.16% Female = 61.84% |

0 = male 1 = female |

| Age | Min.: 15 Max.: 67 Mean: 44.80 SD: 14.49 |

Age in years |

| Education | Never = 0.97% 2 = 12.72% 3 = 47.04% 4 = 30.03% Still in education = 9.25% |

Age at which which respondent completed full-time education 1 = never in full-time education 2 = up to age 16 3 = age 16 to 20 4 = over age 20 5 = still in education |

| Preference for self-employment | Min.: 0 Max.: 1 Mean: 0.42 SD: 0.49 |

Suppose you could choose between different kinds of jobs, which one would you prefer (recoded) 0 = being an employee 1 = being self-employed |

| Self-employed parents | Min.: 0 Max.: 2 Mean: 0.27 SD: 0.57 |

Could you please tell me the occupation of your father/mother? Is he/she or was he/she self-employed […]? (recoded) 0 = neither father nor mother self-employed 1 = father or mother self-employed 2 = both parents self-employed |

| Rural | Min.: 1 Max.: 3 Mean: 2.18 SD: 0.72 |

Would you say you live in a …?

1 = metropolitan area 2 = other town/urban centre 3 = rural zone |

| Contextual level | ||

| Unemployment rate | Min.: 3.4 Max.: 11.3 Mean: 6.61 SD: 1.92 |

Unemployment rate in 2008 Source: Eurostat Statistics, 2008. |

| Access to finance (SMAF) | Min.: 78.8 Max.: 118.4 Mean: 99.45 SD: 9.04 |

The SMAF index provides an indication of the changing conditions of SMEs’ access to finance over time for the EU and its Member States. The index is calculated using a baseline of EU 2007 = 100 and so allows comparison between countries and across time. The base reference of 2007 deliberately provides a baseline before the onset of the financial downturn. The SMAF index is composed of two sub-indexes, one called ‘Debt finance sub-index’ and the other ‘Equity finance sub-index’. In total, the two components of the index capture 14 indicators Source: EC and ECB’s Survey on the Access to Finance of SMEs (SAFE), 2008 |

| Social welfare expenditure | Min.: 12 Max.: 29.1 Mean: 21.81 SD: 4.07 |

social expenditure as the percentage of the GDP Source: Eurostat Statistics, 2008 |

| Unemployment insurance for self-employed | Yes: 26.10% No: 73.90% |

See detailed description in the Data and Methods section 1 = yes 2 = no Source: MISSOC (Mutual Information System on Social Protection/Social Security), 2008 |

SD: standard deviation; EU: European Union; GDP: gross domestic product; SMAF: SME Access to Finance; EC: European Commission; ECB: European Central Bank; SME: small and medium-sized enterprises.

All individual-level variables are taken from the Flash Eurobarometer 283 - 2009.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is an outcome of the EU-funded collaborative research project CUPESSE (Cultural Pathways to Economic Self-Sufficiency and Entrepreneurship; Grant Agreement No. 613257; ![]() ).

).