Abstract

Our analysis of 2707 news stories explores the framing of flooding in Britain over the past quarter century and the displacement of a once dominant understanding of flooding as an agricultural problem of land drainage by the contemporary concern for its urban impacts, particularly to homes and property. We document dramatic changes in the volume and variety of reporting about flooding since 2000 as the risks of flooding have become more salient, the informal ‘Gentlemen’s Agreement’ between government and private insurers has broken down, and flood management subjected to greater public scrutiny. While the historic reliance on private insurance remains largely unchallenged, we show that other aspects of flood hazard management are now topics of active political debate to which the looming threat of climate change adds both urgency and exculpatory excuses for poor performance. We conclude by reflecting on the significance of the case for grand theories of neoliberalisation and governmentality.

1. Introduction

The news media play a crucial role in the apprehension of environmental risks and in framing whether and how they become social problems of wider public concern. While there is now a well developed literature on media constructions of climate change (e.g. Boykoff, 2011; Carvalho and Burgess, 2005; Dirikx and Gelders, 2010; Olausson, 2010), there has been little systematic research into media coverage of flooding and other extreme weather events through which the impacts of climate change will actually be experienced. A number of studies have explored media representations of Hurricane Katrina (e.g. Izard and Perkins, 2010) and the dynamics of media coverage and disaster aid (e.g. Benthall, 2008; Okere, 2004), but this work tends to focus on discrete events and on the framing of disaster victims rather than the risks they face.

Looking specifically at flooding, Wilkins (2000) found that coverage of the 1993 Mississippi and 1997 Red River flood disasters in the US tended to focus on the event and its impacts, rather than on the underlying vulnerabilities to them or potential mitigation measures. In the UK, Gavin et al. (2011) also found coverage in national newspapers to be thin in quantity, episodic in character, and narrowly focused on newsworthy flood events, with only occasional efforts to contextualise flooding, connect its incidence to climate change, or attribute responsibility for failures to manage it. But taking a longer historical perspective, Hall (2011) and Pantti and Wahl-Jorgensen (2011) both found that blame has become a more prominent feature of disaster coverage in Britain over time, a finding consistent with Rojecki’s (2009) comparison of coverage of the Great Mississippi floods of 1927 with Hurricane Katrina of 2005, in which an optimistic frame about the need for national solidarity, governmental intervention, and technological control over nature gave way to a fatalistic one about the power of nature, futility of any collective response, and a moralising focus on individual victims, who were understood as responsible for, even deserving, their miserable fates.

Such media framings shape the politics and management of risk in several ways. First, news reporting plays an important role in agenda-setting and thus in driving policy development (McCombs, 2005). Second, the media constitute a crucial component of the wider public sphere in which such matters are decided in liberal democracies. News reporting serves as a medium for scientific experts, interest groups, and policymakers to communicate with the public and with each other about risk and as an arena for publicising the resulting deliberations and ensuring they are open and democratically accountable (Nelkin, 1995). Moreover, changes in the logics of government now make these communicative functions as crucial to the actual management of risk as to its democratic warrant. With power in advanced liberal democracies increasingly operating through logics of individual choice and self-regulation (Rose, 1999), risk communication helps inculcate new norms of subjectivity, prudential conduct and individualised responsibility. An extensive body of work on the social amplification of risk has explored how the quantity and character of news coverage can amplify or dampen public perceptions of risk (e.g. Kasperson et al., 1988), while critical media studies scholars have highlighted the role of issue sponsors in promoting particular media ‘packages’ designed to influence public opinion and promote particular forms of conduct and action (e.g. Gamson and Modigliani, 1989).

In the specific case of flood hazards, the traditional reliance on engineering flood defences is now giving way to new approaches that frame flooding as a risk to be accepted and managed (Butler and Pidgeon, 2011; Johnson and Priest, 2008; Porter and Demeritt, 2012). As the government’s flooding strategy for England explains, “for the system to work effectively, the public needs to understand and act on the advice and information given” (DEFRA, 2004: para 13.1). In this context, media coverage of flooding can be understood not just as an instrument for influencing public opinion but also as a rough indicator of it, insofar as commercial pressures ensure that media coverage tends to reflect, albeit in complex ways, the underlying mood of the mass market readerships to which it is appealing (Allan et al., 2000; Gamson and Modigliani, 1989; Gunther, 1998).

Accordingly this paper explores how flooding has been framed in UK broadsheets over the period of this policy shift from flood defence to flood risk management. After discussing our methodology, we begin by quantifying the broad patterns of coverage over time, before exploring in more detail how flooding has shifted from an agricultural problem to an urban one managed through private insurance but subject to increasing political controversy and public debate. We conclude by reflecting on the significance of this case for grand theories of neoliberalisation and governmentality.

2. Methodology

Our analysis focused on the national broadsheet newspapers: the Times, Financial Times, Telegraph, Guardian and Independent, plus their sister Sunday papers. Though their circulation is not as high as the tabloids’, British broadsheets enjoy greater agenda-setting influence over both policy and other media, which often run with stories first broached in the broadsheets (Carvalho and Burgess, 2005).

We selected flooding stories for analysis from the Nexis database, whose digitally searchable holdings of the Financial Times, Guardian and Times stretch back to 1985, with the Independent joining on 1 September 1988 and the Telegraph on 1 October 2000. After trialling various Boolean terms for the relevance and comprehensiveness of searches in 2007, when widespread flooding in England generated extensive news coverage, we settled on “flood!” AND “rain” OR “risk” within the same paragraph. Applying these terms over the period 1985 to 2010 generated 7074 articles from which we then removed all duplicates, news stories focused on flooding in other countries, and those in which flooding in the UK was discussed only in passing. This left a final set of 2707 stories for analysis in which the incidence, risk or management of flooding was a major feature of the story.

Each story was then individually reviewed and assigned a primary content code as well as additional secondary ones to reflect its content with greater granularity. The primary coding scheme is summarised in Table 1. As with the protocol for the search terms, our content codes were developed iteratively by working through several subsamples selected from across the time series of stories. The robustness of content coding performed by the first author was then tested by comparison against a sample of stories re-coded by the second author.

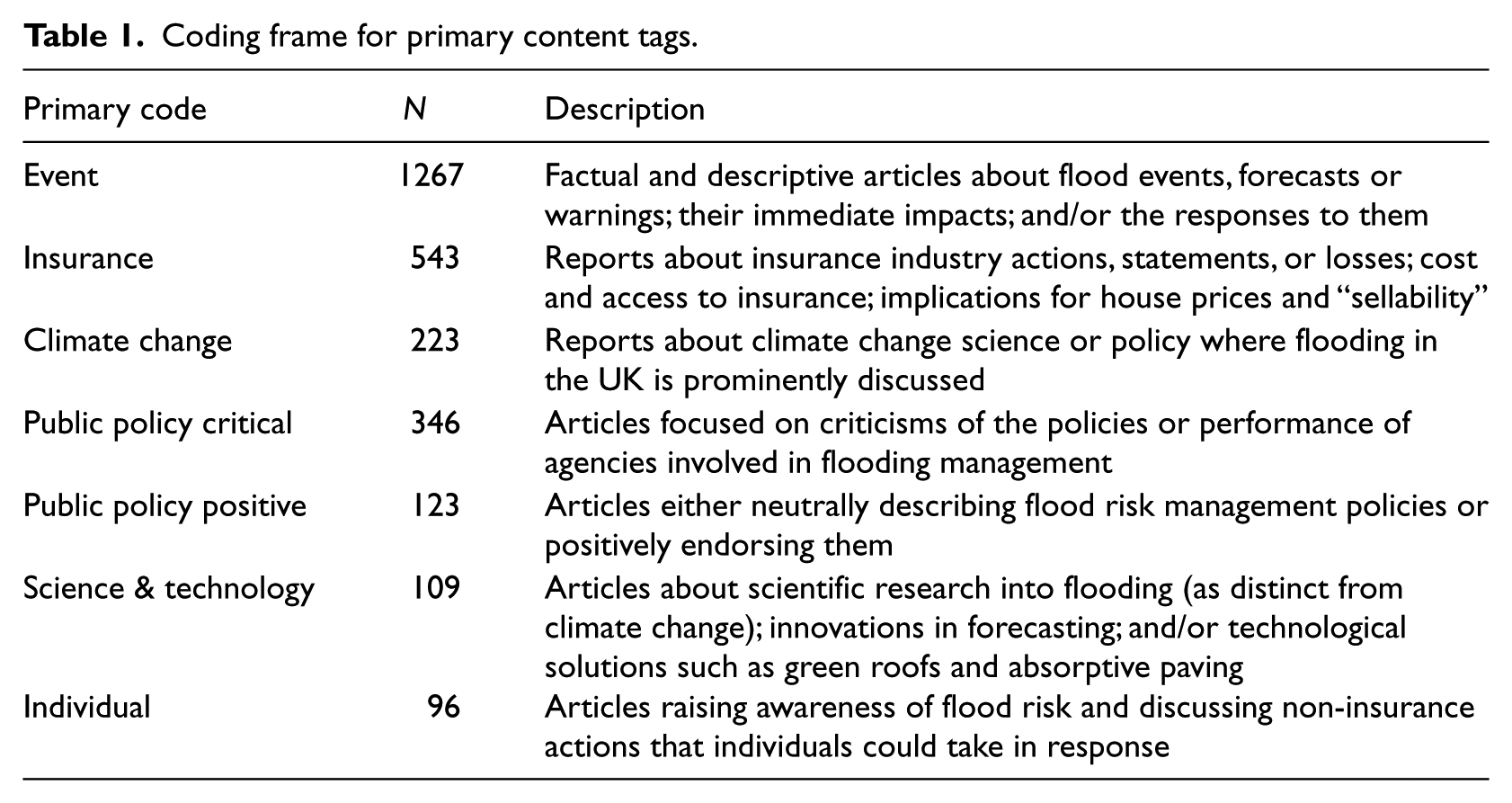

Coding frame for primary content tags.

While the frequency of different codes provides a broad indication of their relative salience, qualitative analysis is required to explore their framing and its relationship to underlying discourses of power (Fairclough, 1992). ‘Frames’ and ‘framing’ are central concepts to such discourse analysis, even if, like the idea of discourse itself (Lees, 2004), they have lost some sharpness through sometimes careless use. For Miller (2000: 211) frames are the “perceptual lenses, worldviews or underlying assumptions that guide communal interpretation and definition of particular issues”. Taken as a noun, the concept of a ‘frame’ directs critical attention to the substrate of prior norms and commitments through which perception is filtered and sense-making organised. By contrast, as a verb the concept of ‘framing’ points to the processes structuring individual texts both thematically and strategically, such as the selection of sources, use of imagery, and arrangement of the story (i.e. on the front page, in the headline, or buried in the final paragraph) so as to enable “the public to rapidly determine why an issue is important, who is responsible, and what might be the consequences” (Dirikx and Gelders, 2010: 732, emphasis in original). In the analysis that follows we attend to both the wider frames through which flooding is apprehended and the framing practices through which they are reinforced and naturalised in the press.

3. Patterns of flooding coverage

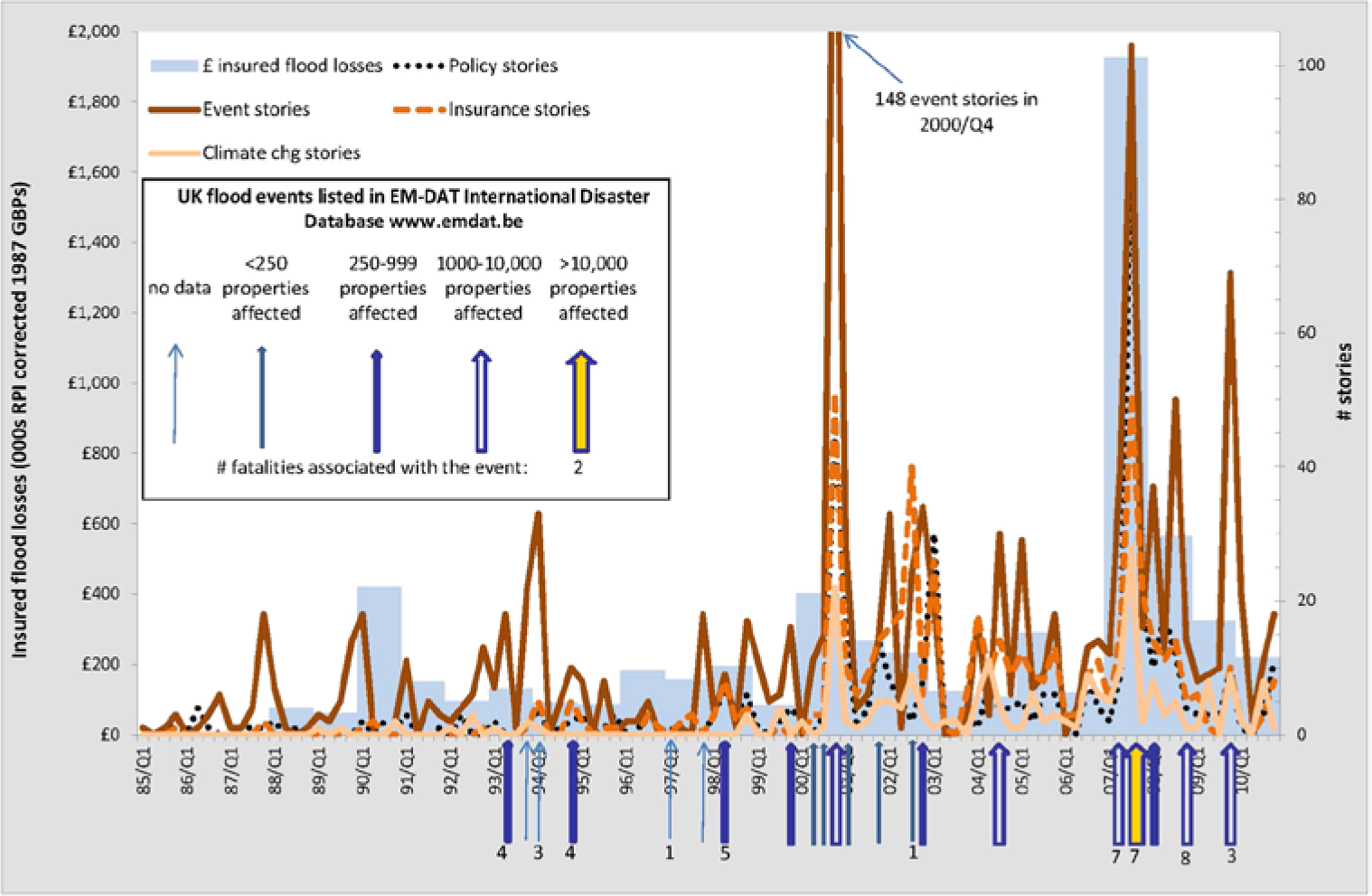

The last twenty-five years have witnessed dramatic changes in broadsheet reporting about flooding in Britain. The coloured lines in Figure 1 show the number of flooding news story codes appearing in each quarter since 1985. During the 1980s and 1990s there were comparatively few stories about flooding, and most of these were factual news items describing discrete flood events. Since 2000, however, there have been substantial increases both in the total number of stories and in the proportion of them concerned with aspects of flooding other than its mere incidence.

Flood events and the changing pattern of flood-related news stories in British broadsheets, 1985–2010. Note that the black dotted line for ‘policy stories’ is a combination of two separate primary content codes for ‘public policy critical’ and ‘public policy positive’. To improve clarity the secondary y-axis for number of stories has been truncated at 105, reducing the height of the spike in ‘Event’ coverage in 2000/Q4, which totalled 148. The insured losses data shown by the grey bar chart, which were originally given by the ABI (2012) as nominal figures, have been adjusted to a base rate of 1987 RPI-corrected Great British Pounds (GBP) to enable interannual comparison. The figures for 1988–97, when the ABI did not distinguish flood losses from the larger category of weather-related losses, are estimated at 17% of annual weather losses, which was the ratio of flood losses to weather losses in the period 1998–2011 when disaggregated data are available. This estimated figure will tend to underestimate total flood losses resulting from large events and to over-estimate them from smaller events.

The grey bar chart and coloured arrows below the x-axis in Figure 1 show various indicators of the frequency and scale of flood events in the UK from the Association of British Insurers (ABI, 2012) and the EM-DAT database of international disasters. While there is some suggestion here that the recent shifts in the volume and pattern of news coverage may be responding to increases in the frequency and severity of flooding, the time series of flood events is both patchy, with recent events better captured than those in the 1980s and 1990s, 1 and noisy. Several recent studies have found no statistically significant evidence for long-term increases in flood frequency in Britain (Hannaford and Marsh, 2008; Robson, 2002), and both the news coverage itself and the record of insured flood losses from the Association of British Insurers (ABI, 2012) highlight flood events in 1987, 1990, 1993, and 1994 every bit as devastating, whether measured in terms of lives lost or Retail Price Index corrected flood damage costs, as the more recent and better documented floods of the 2000s.

Arguably what has changed over the last 15 years or so is not the frequency of flooding so much as the responses to it from the press and wider public at large. The recent shifts in the volume and in particular the variety of flooding coverage are much more dramatic than those in the flooding record itself, while the timing of surges in coverage has become increasingly de-coupled from that of actual flood events. The data in Figure 1 thus suggest important shifts both in the saliency of flooding as a news item and in the ways it is framed as a problem in the press and by implication in the wider public sphere as well, insofar as news coverage both reflects and shapes public perceptions of risk (Kasperson et al., 1988; Gamson and Modigliani, 1989).

These changes cannot be attributed to sampling biases or the late addition of the Telegraph to the Nexis database on 1 October 2000, just days before the devastating floods of autumn 2000. As Table 2 shows, this watershed event triggered major increases in the volume and variety of flooding coverage in all the other broadsheets. Were the digitally searchable run of the Telegraph extended farther back in time, there is every reason to expect it would show the same basic patterns as its competitors.

Primary content tags by broadsheet.

Despite recent increases in other kinds of stories, the bulk (47%) of broadsheet coverage is still devoted to descriptive news reports about flood events. The incidence of flooding is both immediately palpable and dramatically out of the ordinary, unlike climate change, which has often depended upon other events, such as meetings of the IPCC or the international Conference of the Parties to the UN Framework Convention, to lend it news value (Anderson, 2009). Flooding, by contrast, is a newsworthy event in and of itself, conforming to journalistic norms of immediacy and factualness while also satisfying the ‘if it bleeds, it leads’ imperative for attention-grabbing drama (Hannigan, 1995). As a result there was little evidence for partisan bias among British broadsheets in the volume of attention they pay to flooding (Gavin et al., 2011), as there is for climate change (Carvalho and Burgess, 2005). When it floods, it is news, and journalists in all the major broadsheets report on it. Often written with local bylines by journalists reporting from flood afflicted areas, the stories we have coded as ‘events’ typically enumerate where and when flooding is occurring, describe the emergency response, and detail the resulting damage done. The tone of such reporting is factual, and its aim is simply to chronicle events without structuring them into an overarching narrative from which some moral judgement can be made (cf. Cronon, 1992). Through this narrow focus on flood events, “the audience is entertained by the hazard without being informed about it” (Allen et al., 2000: 8).

There are three reasons to see the recent increases in the volume of broadsheet coverage devoted to flooding as evidence of deeper shifts in the saliency and framing of flooding as an issue. First, individual flood events now attract a comparatively greater volume of news reporting than in previous years. For example, the Easter 1998 floods led to 5 fatalities and damaged 1900 properties across the Midlands with an estimated insured loss of £500–700 million (Environment Agency, n.d.), but attracted just 7 ‘events’ stories. After just two days, all was forgotten, at least in the national press. By contrast, a much smaller and more localised flash flood event in Cornwall in November 2010, causing no fatalities and a mere £6 million in damages to 250 properties (Environment Agency, n.d.), generated 15 news stories about an event that in terms of its spatial extent, hydrological magnitude, and economic cost was comparatively minor. Nevertheless the flood prompted a visit from the Prime Minister (Guardian, 19 November 2010), desperate to draw a line under a series of critical stories blaming budget cuts for the damages and the disappointing performance of the Environment Agency and Met Office (e.g. Times, 13 November 2010; Guardian, 21 November 2010).

Second, discourse analysis shows that the way events are covered has also changed. Whereas reporting about flood events in the 1980s and 1990s was largely factual and descriptive, more recent news coverage has tended to adopt more of a ‘human-interest angle’, with journalists directly quoting victims and using more emotive language and headlines to dramatise the event. Compare, for example, “Floods halt traffic” (Financial Times, 21 May 1986) and “Wales hit by flooding” (Guardian, 31 December 1986) with “Death and destruction on England’s wettest day” (Telegraph, 21 November 2009) or “Carlisle Cut Off as Gales Wreak Havoc” (Guardian, 9 January 2005). Zemp (2010: 55) noted a similar “trend toward the tabloidization of disaster coverage” in Switzerland, with broadsheets and tabloids alike making increasing use of human interest stories, attention-grabbing photos and graphics, and dramatic headlines in their coverage of floods in 1999, 2000 and 2005 as against events she analysed in previous decades.

Third, the once near exclusive focus on covering discrete flood events of the 1980s and 1990s has broadened so that there is now a much wider variety of newspaper articles about flooding. For example, 71 (78%) of the 91 flooding stories in the 1980s were immediate news reports describing flood events and their impacts. By contrast, in 2007 out of 469 stories, 123 (26%) dealt with the potential policy measures for managing flood risk, more than in the entire decade previously. These stories have broadened the focus beyond recounting the sudden incidence and impact of flooding to encompass discussion about its wider causes, longer term impacts, and the responsibilities for dealing with them. As a result newspapers now give more sustained attention to the risks from flooding in the period between major events, so that 2006, a year without any major flooding in the UK, saw 98 news stories about flooding, more than in any single year in the 1980s and 1990s. This thematic broadening of flooding coverage and temporal extension of the issue-attention cycle both point to important underlying shifts in the way that flooding is framed in British broadsheets.

4. Urbanising flood hazards

The last twenty-five years have seen important shifts in where the problem of flooding was framed as occurring and thus in what kind of a problem it was imagined to be. A number of the very earliest stories in our sample capture traces of an older frame about flooding as an agricultural problem of flooded fields and inadequate land drainage (Johnson et al., 2005; Scrase and Sheate, 2005). Thus a 2 February 1988 story in the Times, headlined “Heavy storms deepen farmers’ gloom”, led by noting that “millions of acres of farmland are under water” before describing the efforts of farmers to cope with flooded crops, delays to spring planting, and added winter feed costs from livestock unable to graze waterlogged pastures. Often written by dedicated Agriculture or farming correspondents, such as those employed by the Times and Telegraph, stories with this agricultural frame were relatively common in the early years of our study period, appearing, as a secondary code, in 16% of flooding stories in the 1980s.

But this agricultural frame soon fades out, along with the dedicated Agriculture correspondent in the Times, who last appears in our data set in 1989. Barely 1% of the 2202 flooding stories published after 2000 make any reference to farming. A dozen or so stories during the 2000 and 2007 floods in England noted the impacts on agriculture (e.g. “Farmers warn of ruined crops and food shortages”, Independent, 3 November 2000; “Floods drive up broccoli, carrot and potato prices”, Times, 4 July 2007), but they were matched by an alternative frame that now blamed farmers for the flooding (e.g. “Intensive farming blamed for swollen rivers”, Guardian, 9 November 2000; “Flooding is blamed on sheep and cows”, Telegraph, 2 April 2003; “Intensive agriculture lets rainwater drain too soon”, Times, 12 September 2007). Farming, once the primary victim of flood hazards, has become a villain in newspaper coverage, when it is even noticed at all.

This transition reflects deeper shifts in the British economy and society. While agriculture may still dominate the land, occupying 77% of land cover in the UK, it contributes less than 0.5% of GDP (Angus et al., 2009). Things were very different in the immediate post-war period. Food supplies in Britain were rationed, and with imports limited by balance of payment problems, increasing domestic food production was a national priority. In this context the devastating floods of 1947 and 1953 were understood as devastating as much for their impacts on the harvest as for the hundreds of lives lost in the immediate disasters (Hall, 2011). To increase domestic food production, the Ministry of Agriculture provided generous subsidies for land drainage and flood prevention schemes to open up low-lying flood plains to agriculture. By the 1980s, however, the problem was no longer food shortages, but overproduction, and the focus for river engineering works shifted from land drainage to flood defence (Scrase and Sheate, 2005).

In an urban society, the impacts of flooding on cities and towns are the most meaningful, and so they are what the newspapers headline. Thus the front page of the Independent (13 October 2000) declared, “Rising floods force hundreds to abandon their homes”, while inside the fold it and many other papers that day recounted the remarkable story of Vernon Bishop who was swept out of his high street jewellery shop in Uckfield, East Sussex, by rising flood waters and miraculously rescued some three quarters of a mile downstream by a Coast Guard helicopter. Beyond such immediate human drama, coverage of flood events often focused on damage to homes and property, making flooding an economic as much as an environmental problem. After severe flooding swept over Yorkshire and Humberside in June 2007, the Financial Times (27 June 2007) described how “businesses and households face long disruption”. In-depth feature articles focused on individual victims were a common device for personalising the impacts of flooding, such as the Independent (21 November 2009) headline lamenting, “Flood Chaos: ‘For some people, everything has gone’”. While this particular piece was framed around the emotional costs of the Cumbrian floods of 2009, it was more common to focus on economic ones. Of the 76 news stories about those floods, 17 mentioned economic costs, and 6 were centrally focused on the issue. Flooding, in short, is an issue with a strong place on the ‘money beat’ of British broadsheets. At times this economic frame entirely eclipsed the wider human costs of flooding. For instance, readers of a Times (26 October 1998) story, headlined “Britain faces a repair bill of £400m”, would have had to read quite carefully to note that at least 11 lives had also been lost in the downpours over the previous weekend.

5. A problem for private insurance

This focus on economic damage to homes and property both reflects and reinforces a longstanding approach in Britain to flooding. Unlike those in most European Union member states, governments in Great Britain are not involved in directly compensating flood disaster victims (Botzen and van den Bergh, 2008). 2 Instead, damage costs have been transferred to the private sector through commercial insurance. Under the so-called ‘Gentlemen’s Agreement’, first hammered out between the insurance industry and the government in 1961, insurers would provide affordable flooding coverage by making it a standard part of buildings and contents policies on the understanding that government, in turn, would fund flood defences so as to reduce the risk to acceptable levels (Huber, 2004). Reiterating a longstanding government commitment to such insurance-based solutions, Elliot Morley, the then Junior Minister responsible for flood defences, was quoted in the Times (5 January 2003) explaining “there would be no government help or compensation for households hit by flooding … [as ] [w]e are leaving it to the operation of the free market”. With damage costs underwritten by private insurance, the environmental risk of being flooded has been transformed into the financial risk of premiums and excess charges rising or of being unable to afford insurance and the securities it affords (Priest et al., 2005).

From the very beginning of our data set, flood events were often followed by insurance stories detailing their implications for industry profits, the price and accessibility of insurance cover, or the logistics of making insurance claims. After the great storms of 1987, for example, the weekly ‘Family Money’ column of the Times ran a series of stories advising readers on dealing with loss adjusters and shopping around for the best rates, while the ‘Weekend Money’ section of the Guardian (24 October 1987) ran similar advice. Their placement within the newspaper served to reinforce the wider framing of flood costs as an issue of consumer rights vis-à-vis private insurers. The Guardian (17 August 1996), for example, advised flood victims: If your insurance company does insist you wait for a few months before it is prepared to assess the full cost of the damage, it may be prepared to make an interim payment to see you through … Even if you are not ready to make a claim immediately, let your insurance company know you plan to do so and set about listing the damage as soon as possible.

The volume and frequency of such insurance-related stories increased substantially after the autumn 2000 floods. Whereas the first 15 years of our study, from 1985–2000/Q3, saw 56 insurance stories, comprising just over 10% of the total for that period, the 10-year period from 2000/Q4 onwards had 487 insurance stories, comprising 23% of the total over that period. As Deputy Prime Minister John Prescott told Parliament, the 2000 floods were a “wake-up call for everyone” (Times, 1 November 2000). Following fast on the heels of nearly £1 billion in insured losses from flooding in 1998, the scale of the autumn 2000 floods increased the public saliency of insurance as the primary mechanism for financing a further £1.2 billion in insured losses (ABI, 2012), while also prompting the industry to challenge the terms of the Gentlemen’s Agreement under which it was underwriting those risks. Such changes had been mooted before. A slow trickle of stories through the 1990s warned that “climate change may force up the costs of insurance” (Guardian, 5 February 1990), lead to more sharply differentiated and “higher insurance premiums for homes at risk from flooding” (Times, 8 January 1994), or even result in insurance against “flood damage… be[ing] withdrawn” (Financial Times, 4 November 1994).

After the ‘catalytic’ floods of autumn 2000 (Johnson et al., 2005), the insurance industry became more insistent about the need for the government to uphold its end of the Gentlemen’s Agreement. The Financial Times (19 February 2001) reported: Leading insurers have told the government that it has two years to offer properties across Britain better protection against flooding. If not, they warned ministers, the industry might be unable to continue providing cover for nearly all households and businesses.

There was extensive coverage of the negotiations leading up to the Association of British Insurers (ABI) finally updating the Gentlemen’s Agreement with a more formal Statement of Principles in September 2002. On the condition that government flood defence expenditures met certain specified levels and that other steps were taken to reduce exposure, insurers pledged to continue offering flood coverage to existing customers for a further 3 years where the risk of flooding was, or soon would be due to planned flood defences, no greater than 1.3% annual probability, but with premiums and other terms reflecting that risk. The Statement of Principles was renewed in 2005 and then revised again after the 2007 floods, this time with the proviso that it would “not apply to any new property built after 1 January 2009” (ABI, 2008).

Throughout these negotiations, a steady stream of stories warned of the disastrous consequences for consumers if insurers and the government could not reach agreement. Many of these were initiated by industry press releases designed to put pressure on the government to tighten planning regulations and increase flood defence spending (e.g. Guardian, 16 February 2002). While coverage of these debates observed journalistic norms of balance (cf. Boykoff, 2011), with competing claims carefully attributed to industry or government claims-makers rather than being reported simply as fact, the need for more government action was widely acknowledged, and the broad outlines of the industry case were explicitly endorsed in editorials (e.g. Times, 5 November 2000; Financial Times, 8 November 2000; Guardian, 4 January 2003; Independent, 22 September 2002) and sometimes tacitly too in the framing of news coverage. For instance, after describing the ongoing row between the ABI and government about whether the additional £150 million committed to flood defence in the July 2002 Comprehensive Spending Review was sufficient, a story in the Telegraph (3 August 2002) concluded by quoting a Cambridge resident, Colin Walsh, as saying “Rather than leaving it to insurers after the event, the Government needs to take more responsibility for managing floods.”

Although insurers were sometimes criticised for raising premiums needlessly (e.g. Financial Times, 8 September 2001) or for dragging their feet in paying out on claims (e.g. Independent, 11 July 2007), the basic idea that flood damage costs should be funded through commercial insurance was never really questioned. Reacting to the social inequalities crystallised by the 2007 floods, for instance, Guardian (3 July 2007) columnist, Polly Toynbee, took aim not at insurance, but at the regional inequalities in flood defence spending that left Hull vulnerable but London “the only really well-defended part of Britain, where the Thames barrier is built to withstand everything below a once in 2000-year freak flood”. Though she noted the difficulties facing the uninsured, there was no suggestion here, or anywhere else in our data set of British broadsheet coverage, that the government should assume the responsibility for directly compensating flood victims, as in other European countries. Sometimes the prevailing private insurance-based model of disaster finance was explicitly endorsed, such as the comment piece in the Independent (6 January 2003) headlined, “If you want to live near a river, then pay the price”, or this editorial in the Times (28 July 2007): It is vital that the Government and insurers understand and meet their responsibilities. Ministers have pledged money to improve flood defences but now they must deliver … Meanwhile, insurers must realise that it’s their job to pool risks so that all members of society can reasonably afford cover if they want it.

But more typically it was simply taken for granted that “if your home is prone to flooding, you’ll need more than a pair of wellies: watertight cover is a must” (Telegraph, 25 June 2005).

6. Property and the individualisation of flood risk

As with private insurance, there was a consistent expectation that individuals are responsible for managing their own risk. For instance one Financial Times (3 July 2007) commentator editorialised: Insurers had been warning that, unless the government spent more on defences, home owners in high-risk areas could find it harder to get cover. Would that be such a bad thing? People should certainly take flood risk more seriously when buying properties. They are foolish to place faith in the authorities to prevent homes being built in the wrong places or to protect them afterwards.

Often located in the property or personal finance sections, a steady drumbeat of stories described the actions people should take to reduce the risks posed by flooding. While the focus in the 1980s and 1990s was exclusively on how to get the best deal from private insurers, after 2000 the breadth of advice widened to encompass advice about preparedness and clean-up, such as moving furniture and valuables upstairs away from rising flood waters (Telegraph, 14 October 2006) or disinfecting toys and other personal effects contaminated by sewage-laced flood waters (Times, 15 October 2000).

In the context of a much wider frame about Britain as a nation of enterprising homeowners, flood risk was often seen through the optic of property values and “sinking house prices” (Times, 7 November 2000). For example, new Environment Agency flood maps were greeted with headlines that “crudely drawn maps could hit house values” unfairly (Times, 30 March 2002). Others, however, counselled their use was essential since “with flooding an ever-increasing risk, it is down to the househunter to be aware of the danger signs before buying a property” (Telegraph, 5 November 2000). With property prices booming in Blair’s Britain, homes were no longer just places to live, but financial assets whose value was supposed to appreciate to fund another step up the property ladder. Flooding threatened that vision of property as a goldmine and nest egg all rolled into one, and newspapers, often in dedicated property pages, fed that frame with warnings that “just living in the vicinity of a recent flood may be enough to send house prices plummeting even if there is very little chance that your property would be affected” (Telegraph, 28 October 2001). Those who stayed on “face spiralling costs for home insurance as excesses for flood cover rise to levels that are making their properties virtually impossible to sell” (Guardian, 8 November 2009).

This idea of property somehow rendered “unsellable” or “unsaleable” first emerged during the autumn 2000 floods in the Guardian on 5 November 2000 in two separate stories, the first warning that “Homes in flood-prone areas may be blighted” and the second, in the Cash section, predicting “Floods set to sink price of houses: Potential buyers could be scared off by a history of inundation”. Usage of these terms took off rapidly thereafter, and they appeared in a further 55 separate stories in our data set, including one accompanied by a wry cartoon that reinforced the wider frame of risk individualisation with its picture of a couple struggling, on their own, to defend their family home and property against rising waters (Figure 2).

Cartoon by Howard McWilliam, which appeared in the Telegraph 30 November 2009 to illustrate a story by Alison Steed, “Floods: 500,000 homes could become unsellable”. Reproduced with permission of the artist, www.mcbill.plus.com

Even as they acknowledged the precarity of those living in flood prone areas, newspapers offered consumer advice about how to cope. “Floods can flush out cowboys, so beware builders touting door-to-door, and never pay cash in advance”, warned the Telegraph (15 February 2009). Consumers were strongly encouraged to shop around. By switching their insurance provider, “homeowners in areas at risk of flooding could slash their insurance premiums by 40% and save hundreds of pounds”, counselled Sunday Times (29 September 2002) Money editor Kathryn Cooper. This optimism remained undimmed, even as revisions to the Statement of Principles allowed insurers to ramp up premiums and refuse cover to those at greatest risk. For these people newspapers recommended installing flood gates, airbrick covers, and other property-level flood protections to “minimise the damage to your home” (Guardian, 8 February 2009). Such do-it-yourself protections, the Telegraph (25 June 2005) noted approvingly, would “also improve [homeowners’] prospects for insurance”. The installation of property-level flood protection has been heavily promoted by both government and insurers, but buy-in from householders has been slow, as much because of the tacit model of risk responsibility that it involves as the actual expense (Harries, 2012).

7. Climate change, policy, and the blame game

Alongside the continued emphasis on insurance and other individualising approaches to managing flood risk, government policy has also received more, and increasingly critical, press attention. In February 1990, for example, severe flooding right across Britain, on a scale judged by the Institute of Hydrology to “have no modern precedent” (Marsh and Bryant, 1991: 26), generated just 22 news stories, only two of which addressed policy. Focused on flood defence, both features were sympathetic and excused the National Rivers Agency from any blame for the flooding which was “in effect, beyond man’s control” (Independent, 10 February 1990). Similarly the initial coverage of the Easter 1998 floods treated it as a “freak weather” event (Guardian, 18 April 1998) and provided no background news analysis of the underlying factors, such as climate change, crumbling defences, or lax planning laws, which several stories earlier that year had highlighted as increasing vulnerability to flooding. It was only later, with publication of the government’s Independent Review (Bye and Horner, 1998), that press attention shifted to how “the flooding was made worse by the lack of action by the [Environment] Agency in repairing flood defences, maintaining water courses and providing warning” (Guardian, 2 October 1998). While the Financial Times (2 October 1998) headlined with calls from Labour backbenchers for the resignation of the Agency’s chairman, other papers gave a sympathetic airing to “Agency demands [for] cash for flood defences” (Independent, 3 June 1998) and to the conclusion of Peter Bye that “blame had to be shared by local authorities which had allowed development on flood plains, against clear advice from the agency and its predecessor bodies” (Independent, 3 June 1998).

Coverage of subsequent flood events was accompanied by much more sustained and critical discussion of flood defence policy, planning controls, land use practices, and the wider need to address climate change. Indeed, in 2007/Q3, there was almost as much reporting about flooding policy and the responsibilities for it as there was about the event itself. No longer just an environmental issue, flooding has become a political one. This politicisation was driven, in part, by the insurance industry and its ‘sponsorship’ (cf. Gamson and Modigliani, 1989) of criticism in the media of government policy. For instance in 2002, several papers reported a campaign initiated by Norwich Union, then the market leader in home insurance, “urging anyone at risk to contact their local authority and MP to urge them to improve the management of flood risks” (Telegraph, 23 February 2002). As well as being generated by special interests, criticism of government policy also was amplified by partisan politics. The rising saliency of flood risk provided a convenient stick for the opposition to bash the government, and coverage of their criticisms generated additional coverage of flooding policy, as did the Pitt Review into the 2007 floods and the resulting Flood and Water Management Act (2010).

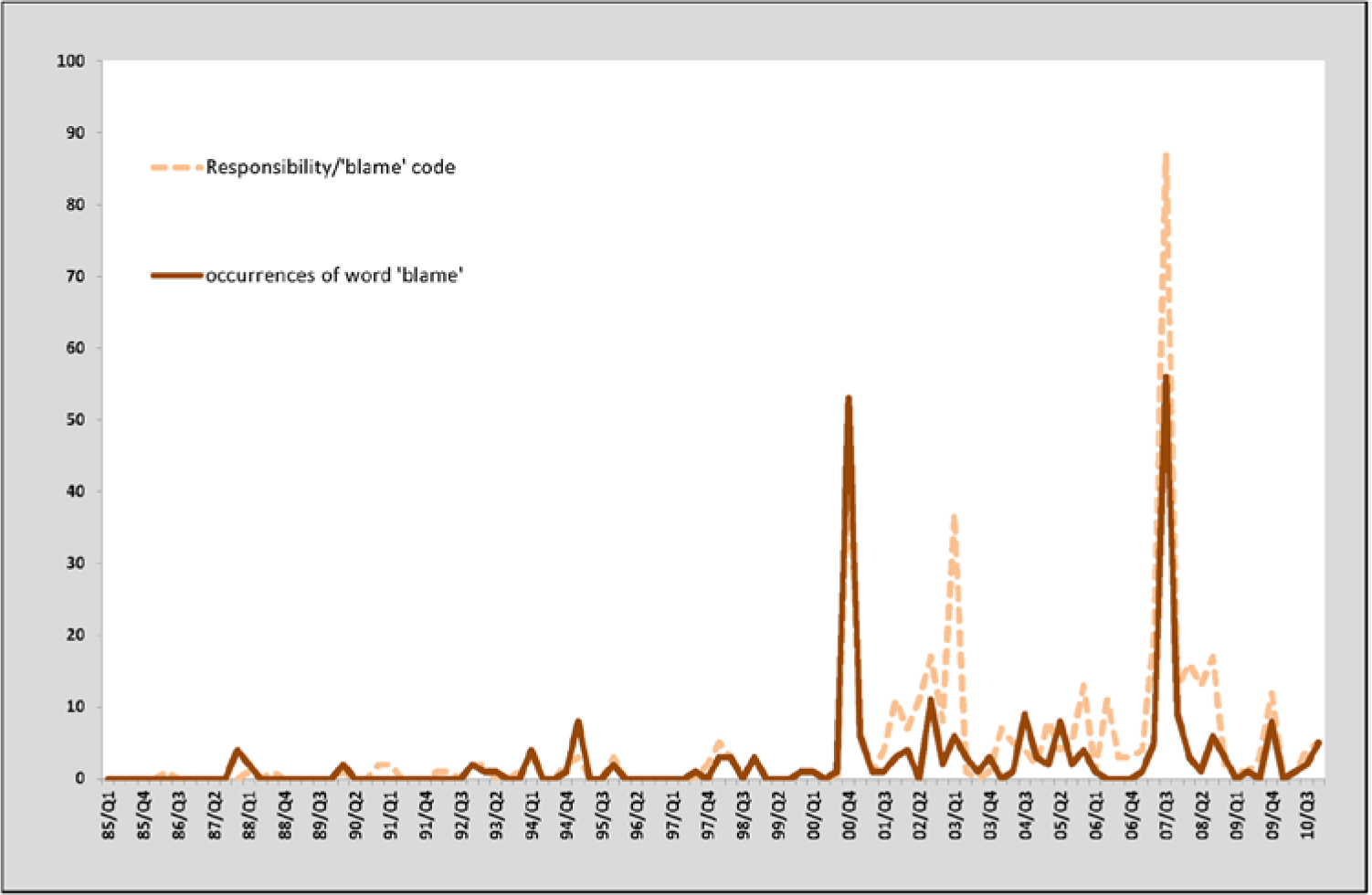

The increasing focus of media coverage on policy and governance has helped transform flooding from an uncontrollable act of God to be endured into a foreseeable risk that must be managed through appropriate precautionary action. In turn, discharging that responsibility creates the additional institutional risk of liability and blame in the event of failure (Rothstein et al., 2006). The word ‘blame’ appears quite sparingly in news coverage in the 1980s and 1990s when it was almost exclusively applied to hydrometeorological phenomena, such as when “the Meteorological Office blamed an usually strong jet stream” (Times, 12 January 1993) or when the “NRA [National Rivers Authority] experts blamed a rapid thaw of snow in the Pennines” (Independent, 2 February 1995), as the immediate cause of flooding. After 2000, however, its frequency increased substantially and was more typically applied to groups or institutions as the proximate cause of flooding problems for which they were being held liable (Figure 3). Thus the Guardian (21 December 2000) reported on a cross-party Parliamentary Select Committee Report claiming that “The floods which ravaged Britain this autumn could partly be blamed on the Ministry of Agriculture … because of its failure to impose rules on farmers to prevent flooding”, and Leeds residents flooded for the second time in less than a year “blamed the council and Yorkshire Water for failing to unblock local drains” (Times, 5 May 2005), while at the height of the 2007 floods newspaper editorialists variously blamed the Environment Agency (Telegraph, 30 July 2007), the planning system (Times, 23 July 2007; Guardian, 24 July 2007), the government in general (Telegraph, 22 July 2007), its lack of investment in flood defences (Guardian, 24 July 2007) and failure “to push through a global treaty” on climate change (Independent, 23 July 2007).

The number of stories assigned the secondary content code ‘responsibility/blame’ (dotted line) and the total number of times the word ‘blame’ occurs in news stories by quarter, 1985–2010.

In the face of such criticisms, organisations sometimes indulged in ‘blame games’ of their own (Hood, 2012), which they played out through the press. The Environment Agency, for example, has consistently blamed its own difficulties managing flood risk on local planning authority failures to control development (Porter and Demeritt, 2012), while insurers responded to the consumer backlash against rising premiums and the withdrawal of cover by blaming government policy, climate change, or sometimes both at the same time (e.g. Financial Times, 10 September 2007).

The threat of climate change adds urgency to these debates, and its importance is acknowledged by a growing volume of coverage (see Figure 1). While science reports were often cautious, correctly noting that “opinion is divided on how much of the problem can be blamed on climate change” (Guardian, 16 September 2000), politicians and editorialists were quick to make the link between flood events and climate change. At the height of the 2000 floods, for instance, Prime Minister Tony Blair was quoted telling flood victims, “We have to put in the right protection for people against the possibility of floods and work to deal with the issue of climate change” (Independent, 3 November 2000). A decade later Climate Change Secretary Chris Huhne urged the UN Climate Conference to action by invoking the £4.5 billion in flood damages suffered in Britain, earning himself a rebuke from the Telegraph (10 December 2010) for misrepresenting the science.

The uncertainties of attribution are not the only reason to be sceptical about the hopes of Gavin et al. (2011) that linking flooding to climate change necessarily offers an effective way to motivate action. Sometimes it can imply that the only way to solve flooding is by preventing climate change. Thus a story about future flooding and other climate change impacts in Britain quoted the Environment Secretary “urging people and businesses to redouble efforts to reduce carbon emissions” rather than identifying any immediate actions that might be taken to adapt to them (Times, 18 June 2009). In the context of flood risk management, invoking climate change can also help provide officials with a convenient rationale for failures and for the limits of government protections. In the face of criticisms about failures to prevent flooding, Elliot Morley, MP, the minister responsible for flood defence, responded that with climate change, “We can’t guarantee that floods won’t happen. There are some areas that you just can’t economically or technically defend, and sometimes there are extremes of weather that it is very difficult to predict” (Times, 28 October 2001). Similarly, after Environment Agency Chief Executive Barbara Young was given a “roasting” by the Commons Public Accounts Committee, she rejected calls to resign or repay bonuses given to her and other senior managers, saying, “It was not the Environment Agency that flooded the country. It was the weather” and that the flooding was “so great” that nothing “could have stopped houses being flooded” anyway (Independent, 2 July 2007).

8. Conclusion

In this paper we have documented substantial shifts in broadsheet reporting about flooding in Britain over the last twenty-five years. Once an agricultural problem of land drainage, flooding is now understood primarily as a threat to homes and personal property, and this urban-economic focus dominates recent coverage of its incidence and the risks that entails. Moreover individual flood events now attract greater volumes of coverage than a generation ago. The focus of reporting has also broadened to encompass discussion of its wider causes, longer term impacts, and the responsibilities for dealing with them, so there is now sustained discussion of flooding and the risks it poses in the period between major events.

These shifts in media coverage both reflect and amplify deeper shifts in public perceptions of flooding as a problem and in the politics of its management. In Britain flood damage costs are financed through private insurance, and this framing remains largely unquestioned, despite increasing controversy over its costs and the terms under which insurance cover is made available to consumers. For many scholars, this reliance on commercially purchased private insurance against life’s perils is the hallmark of fundamental shifts in the norms and logic of government. Invoking the ideas of Michel Foucault, governmentality theorists see individualised, insurance-based approaches to flood risk management as part of a wider shift within advanced liberal democracies towards securing life through logics of individual choice and prudential conduct rather than through protections directly provided by a providential state (e.g. Butler and Pidgeon, 2011). By contrast, critics of neoliberalisation associate private insurance with a roll-back of welfare state protections in the face of relentless budget cutting, the privatisation and marketisation of public services, and a more general ascendance of market forces over the state and civil society (e.g. Haughton et al., 2010). Some support for such grand theories can be found within the tendency, particularly marked in the money and property sections of the broadsheets, to discuss flooding through the optic of house prices and thus to frame the environmental risk of being flooded as a financial risk for consumers to manage by shopping around for the best insurance deal, taking care before buying property liable to flooding and, if necessary, installing property-level flood protections to minimise the frequency and severity of flood damages.

In other ways, however, the case of flooding does not fit these grand narratives very well. British reliance on private insurance for financing disaster costs dates from the early 1960s, the very apogee of the welfare state, and so cannot be read as symptomatic of its eclipse before the forces of neoliberalisation. Far from reflecting rampant state roll-back and the hegemony of technocratic risk management through market-based logics of individual choice and self-regulation, as the neoliberalisation and governmentality theses posit, the increasing newsworthiness of insurance is a function of the increasing politicisation of flood management and in particular of demands by insurers for more government action to mitigate flooding risks. The intensification of this lobbying campaign is directly recorded in media reporting through the 1990s of the industry “warning” the government (Guardian, 23 June 1990) about the need to hold up its end of the Gentlemen’s Agreement, before stepping up its pressure after 2000 by “giv[ing] the Government two years in which to provide adequate flood defences before they start excluding areas of high risk from insurance cover” (The Times, 4 July 2001). Close analysis of media coverage also reveals the role of industry ‘sponsorship’ (cf. Gamson and Modigliani, 1989), through press releases, research and conferences, in amplifying political controversy about the adequacy of planning controls and state funding for flood defence and with it public perceptions of risk.

Partly as a result flooding and its management are now subjects of open political debate in ways that they were not previously. In this context the looming threat of climate change both underscores the urgency of improving the governance of flooding while simultaneously offering exculpatory excuses for failures to prevent its incidence. As part of its “making space for water” strategy, the government is committed to moving towards a “risk-based” approach in which individuals and the private sector take on more responsibility for managing their own exposure rather than looking to the state for protection from flooding (DEFRA, 2004), but this framing is not uncontested. Indeed, analysis of media coverage shows quite clearly that political debate over flooding policy has intensified in recent years, as has scrutiny of those agencies, public and private alike, responsible for managing it. There is simply no empirical evidence for sweeping claims about a new “post-political” age of “post-democratic governing … in which ideological or dissensual contestation and struggles are replaced by techno-managerial planning, expert management and administration” (Swyngedouw, 2010: 225). Instead, the increased public saliency of flooding, combined with its framing as a risk that can be anticipated and thus must be managed, has put the spotlight on the performance of state agencies in discharging those responsibilities and on the attribution of blame when things go wrong. As a result the increased reliance on non-departmental public bodies, like the Environment Agency, to deliver government policy at arm’s length from ministers and the political process has, somewhat paradoxically, been accompanied by much greater public scrutiny of agency performance and partisan political debate about flood risk management policy in Britain more generally (Krieger, 2011).

Footnotes

Acknowledgements

The text has benefitted from comments on an earlier draft provided by Lukasz Erecinski, Sandra Junier, Phil Hendy, James Porter, Henry Rothstein, David Self, Sam Tang, and by two anonymous referees.