Abstract

The prevailing neoclassical economic view in tax-behavior research is that trust is good, but control is better. The advice for combating tax evasion is to deter illegal behavior with rigid audits and harsh fines. But control and punishment may have unintended side effects; therefore, psychological variables (e.g., attitudes toward taxation, social norms, and perceived fairness) are receiving increased attention. The slippery-slope framework integrates both economic and psychological perspectives on tax compliance. It assumes that taxpayers abide by the law either because they fear detection and fines (enforced compliance) or because they feel an obligation to honestly contribute their share (voluntary cooperation). Whereas enforced compliance depends on the power of authorities, voluntary cooperation originates from taxpayers’ trust in the authorities. A growing body of empirical research supports this framework’s assumptions. The psychological approach to tax behavior has led to a change in tax authorities’ practices for regulating citizen behavior. Under the labels of “enhanced relationships,” “horizontal monitoring,” and “fair-play initiatives,” several European countries are advancing cooperative strategies with taxpayers.

Citizens’ tax compliance is of utmost importance for a state to provide public goods and redistribute wealth. Nevertheless, citizens are suspected of being reluctant to pay their share, under the assumption that, rather than voluntarily contributing to the commons, they are motivated to maximize their own profit and to keep their gross income while remaining eager to benefit from public goods. What strategies should tax administrators apply to regulate taxpayers’ behaviors effectively?

The regulation of tax behavior is the focus of an enduring field of research in economics and an emerging topic in many other social sciences. Although research on tax compliance and tax evasion has long been dominated by economists, in recent years, sociologists, political scientists, legal scholars, philosophers, anthropologists, and psychologists in particular have contributed substantial knowledge to this field. Accordingly, the number of interdisciplinary publications relating to psychological determinants of tax compliance is continually increasing (Kirchler, 2007).

The Neoclassical Economic Approach

Although the relevance of psychological determinants of tax compliance, such as attitudes toward the tax system, was the focus of early economic research (e.g., Schmölders, 1960; Veit, 1927), the current prevailing view is that trust is good, but control is better. The scientific advice for combating tax evasion is to impose audits and fines serious enough to incentivize rational, utility-optimizing citizens to honestly contribute their share. Based on the economics-of-crime paradigm (Becker, 1968), the standard model for income-tax compliance (Allingham & Sandmo, 1972) defines tax compliance as a decision under uncertainty. Taxpayers face the option of either abiding by the law and paying taxes honestly or cheating and taking the risk of being caught and fined. It is assumed that the probability of audits, penalty rates, individual income levels, and the tax rate determine citizens’ decisions to comply or not to comply. According to the neoclassical economic approach, taxpayers are driven by profit-maximizing motives, rationally comparing possible options and choosing the option that promises the highest expected profit. Given the relatively low probability of audits and the mild fines for detected tax evasion in most countries, the model leads to the conclusion that tax evasion must be rampant. However, this is not the case: Compliance is surprisingly high (Alm, McClelland, & Schulze, 1992).

Reviews of empirical studies on the impact of the parameters in the Allingham–Sandmo model reveal inconsistent findings (Andreoni, Erard, & Feinstein, 1998; Fischer, Wartick, & Mark, 1992; Kirchler, Muehlbacher, Kastlunger, & Wahl, 2010). The impact of audit probability on behavior appears to be much weaker than expected; the intended effect of penalties is highly ambiguous, and the relevance of income level and tax rates is controversial and disputed among scholars in the field. Rather than objective audit probability, subjective probabilities may determine compliance behavior. Tax evaders who admitted to cheating on taxes in a survey perceived the chances of being caught to be significantly lower than did honest taxpayers (Mason & Calvin, 1978). Nevertheless, the correlation between compliance and perceived risk of being audited also seems to be weak (Elffers, Weigel, & Hessing, 1987). In a nutshell, the neoclassical economic approach poorly explains and scantly predicts tax compliance.

Psychological Determinants of Tax Compliance

Apart from the weak empirical support for the impact of audits and fines, a more general criticism of neoclassical economic reasoning has been put forward—namely, that regulation based solely on incentivizing behavior might crowd out the intrinsic motivation for cooperation (Frey, 1997). Punishing illegal behavior may have undesired side effects (e.g., reactance), and even rewarding compliant behavior might be counterproductive in the long run. Consequently, a thorough psychological analysis of tax behavior is needed. Subjective knowledge of tax laws, attitudes toward the political system in general and taxation in particular, personal and social norms, and the perceived fairness of the distribution of the tax burden and the procedures applied by tax authorities were identified as dominant drivers of tax compliance.

Generally, compliant taxpayers have more positive attitudes toward taxation; in other words, this group holds values and personal norms according to which cooperation is more desirable than competition or egoistic profit optimization, and perceives strong social norms to adhere to the law (Kirchler, 2007). Social norms regarding tax compliance among a reference group shape taxpayers’ behaviors significantly. Compliant taxpayers differ from tax evaders in their perceived social acceptance of tax evasion and beliefs about the tax behaviors of others. According to Wenzel (2004), social norms elicit concurring behavior. However, if identification with a relevant reference group is strong, the prevailing social norms will determine behavior.

Fairness considerations imply comparisons of contributions and benefits, as well as comparisons of how one feels one is treated relative to others. Distributive fairness (relative tax burden and benefits from public goods), procedural fairness, and retributive fairness were confirmed to be strongly related to compliance (see Kirchler, 2007). However, as in the case of social norms, fairness considerations are not always relevant to compliance. For instance, trust in authorities was found to be a boundary condition for the impact of procedural fairness. If taxpayers distrust their authorities, the applied procedures are evaluated with extra suspicion. On the other hand, if authorities are considered trustworthy, taxpayers seem to perceive their activities through rose-colored glasses (van Dijke & Verboon, 2010).

Empirical evidence leaves no doubt about the paramount importance of psychological variables in tax compliance; however, audits and fines should not be neglected. Under certain circumstances, economic determinants, such as audits and fines, may be more important than psychological determinants, or vice versa (Kirchler, 2007).

The Slippery-Slope Framework of Tax Compliance

The slippery-slope framework of tax compliance (Kirchler, Hoelzl, & Wahl, 2008) integrates results from research on the economic and psychological determinants of tax compliance. Tax compliance is assumed to be determined by the power of authorities and taxpayers’ trust in those authorities. These two dimensions, and their interaction, determine whether citizens comply through enforcement or voluntarily. The power dimension represents citizens’ perceptions of the authority’s potential to detect and punish tax evasion. Power is assumed to be high if audits are frequent and effective and fines are perceived as severe. Trust in authorities originates from citizens’ belief in tax authorities’ benevolence, service orientation, and professional engagement for the commons, and is assumed to be affected mainly by psychological variables, such as knowledge and attitudes, personal and social norms, and perceived fairness.

The slippery-slope framework proposes that tax compliance can be achieved by taking actions to increase power and build trust. Power and trust-building measures are assumed to stimulate different motivations for paying taxes. Power measures based on control and punishment result in enforced compliance, whereas trust-building measures should lead to voluntary cooperation. Although enforced and voluntary cooperation may yield similar amounts of taxes paid, their differentiation is of strong practical relevance. First, ensuring enforced compliance, compared with voluntary cooperation, requires costly measures of audits. Second, enforced and voluntary cooperation necessitate different regulation strategies (i.e., responsive regulation; Braithwaite, 2009). However, power and trust are also assumed to affect each other. This is the case when high-trusting citizens become whistle-blowers and thereby help to increase authorities’ power, or when excessive power measures, such as harsh audits and fines, are perceived as signals of mistrust.

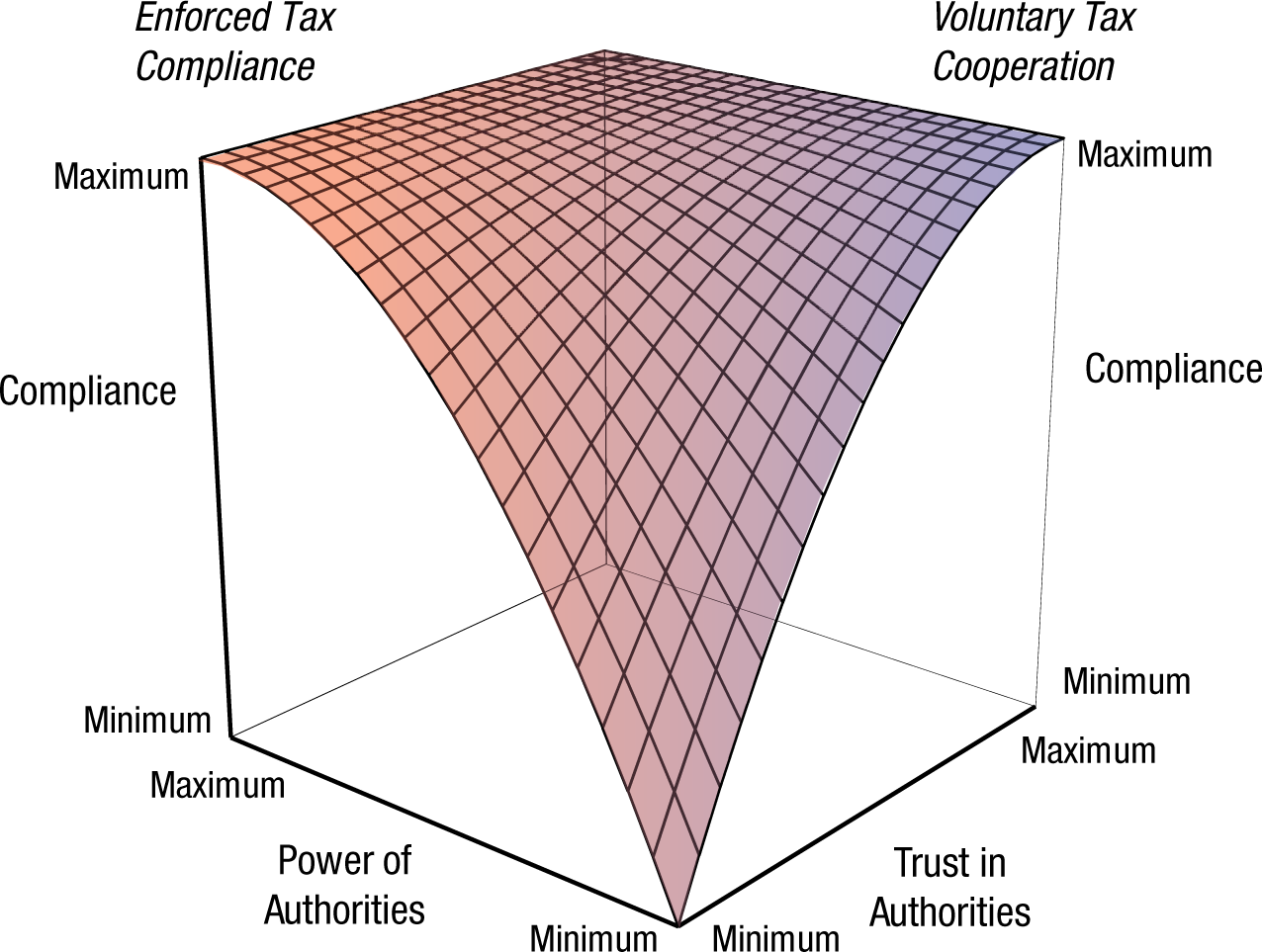

The proposed relations of perceived power, trust, and enforced and voluntary compliance are depicted in Figure 1. Under conditions of low power and low trust, it is likely that citizens seek to maximize their individual outcomes by evading taxes, such that overall compliance is at a minimum. In that case, higher compliance can be achieved either by strengthening power or gaining trust. The term “slippery slope” refers to the reciprocal influences of power and trust. A decrease in one dimension may evoke a decrease in the other and thus result in a strong decline in tax compliance.

Graph illustrating the slippery-slope framework of tax compliance, in which outcomes (enforced compliance vs. voluntary cooperation) are a function of taxpayer compliance and the power of tax authorities. Adapted from “Enforced Versus Voluntary Compliance: The ‘Slippery Slope’ Framework,” by E. Kirchler, E. Hoelzl, and I. Wahl, 2008, Journal of Economic Psychology, 29, p. 212. Copyright 2008 by Elsevier. Adapted with permission.

Furthermore, power of and trust in authorities are indicators of the interactive climate that prevails between taxpayers and authorities. A synergistic climate is characterized by high mutual trust between taxpayers and authorities. Taxpayers are willing to comply, and tax administration provides customer-oriented services. Accordingly, Feld and Frey (2007) explain the high tax morale in Switzerland as resulting from the efficient cooperation between citizens and authorities. In an antagonistic climate, mutual trust is low, and authorities need to adopt costly measures to monitor citizens and catch the profit-maximizing “robbers.”

Empirical Evidence for the Slippery-Slope Framework

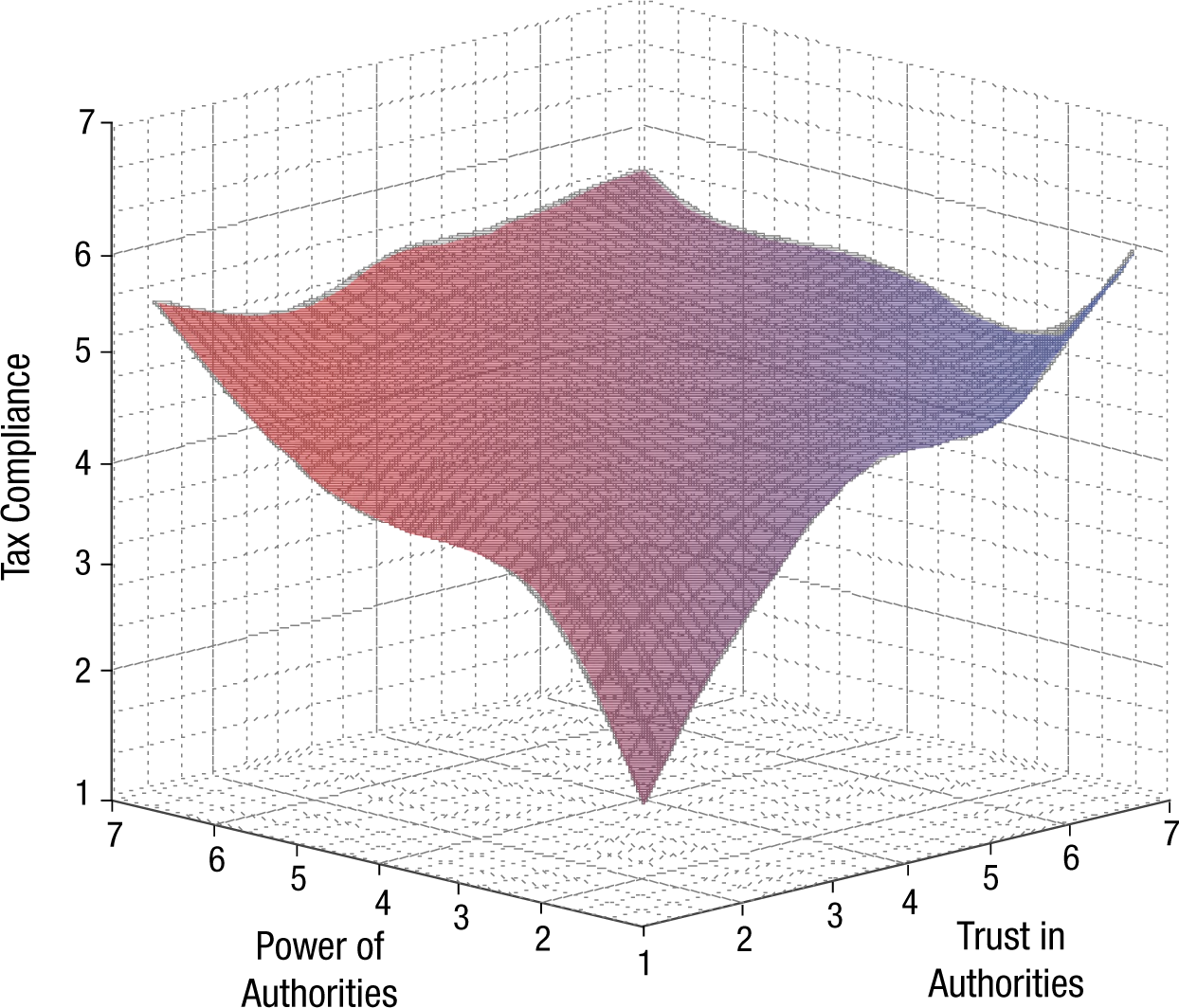

The assumptions of the slippery-slope framework have been the subject of extensive empirical study. A survey of a representative sample of self-employed taxpayers in Austria confirmed the hypothesized effects of perceived power on enforced compliance and of trust on voluntary tax cooperation. Figure 2 shows the relationship among power, trust, and tax compliance. Strong compliance was related to high power and high trust, whereas, in the case of low power and low trust, compliance slid “down the slippery slope,” to the lowest value (Muehlbacher & Kirchler, 2010).

Graph showing tax compliance as a function of power of and trust in tax authorities, based on data from a sample of self-employed taxpayers. Adapted from “Tax Compliance by Trust and Power of Authorities,” by S. Muehlbacher and E. Kirchler, 2010, International Economic Journal, 24, p. 609. Copyright 2010 by Taylor & Francis. Adapted with permission.

Similar findings were obtained in a survey of representative samples of taxpayers from Austria, the United Kingdom, and the Czech Republic (Muehlbacher, Kirchler, & Schwarzenberger, 2011). Beyond the strong impact of power and trust on tax compliance, perceived trust in authorities was identified as a highly significant predictor of voluntary cooperation (β = 0.29), whereas the effect of power on voluntary cooperation was close to zero (β = 0.06). Enforced compliance, by contrast, was strongly related to the power attributed to authorities (β = 0.31), but was not related to trust (β = −0.19). Interestingly, voluntary cooperation was generally higher among older people and taxpayers with higher levels of education, whereas enforced compliance was stronger among less educated taxpayers.

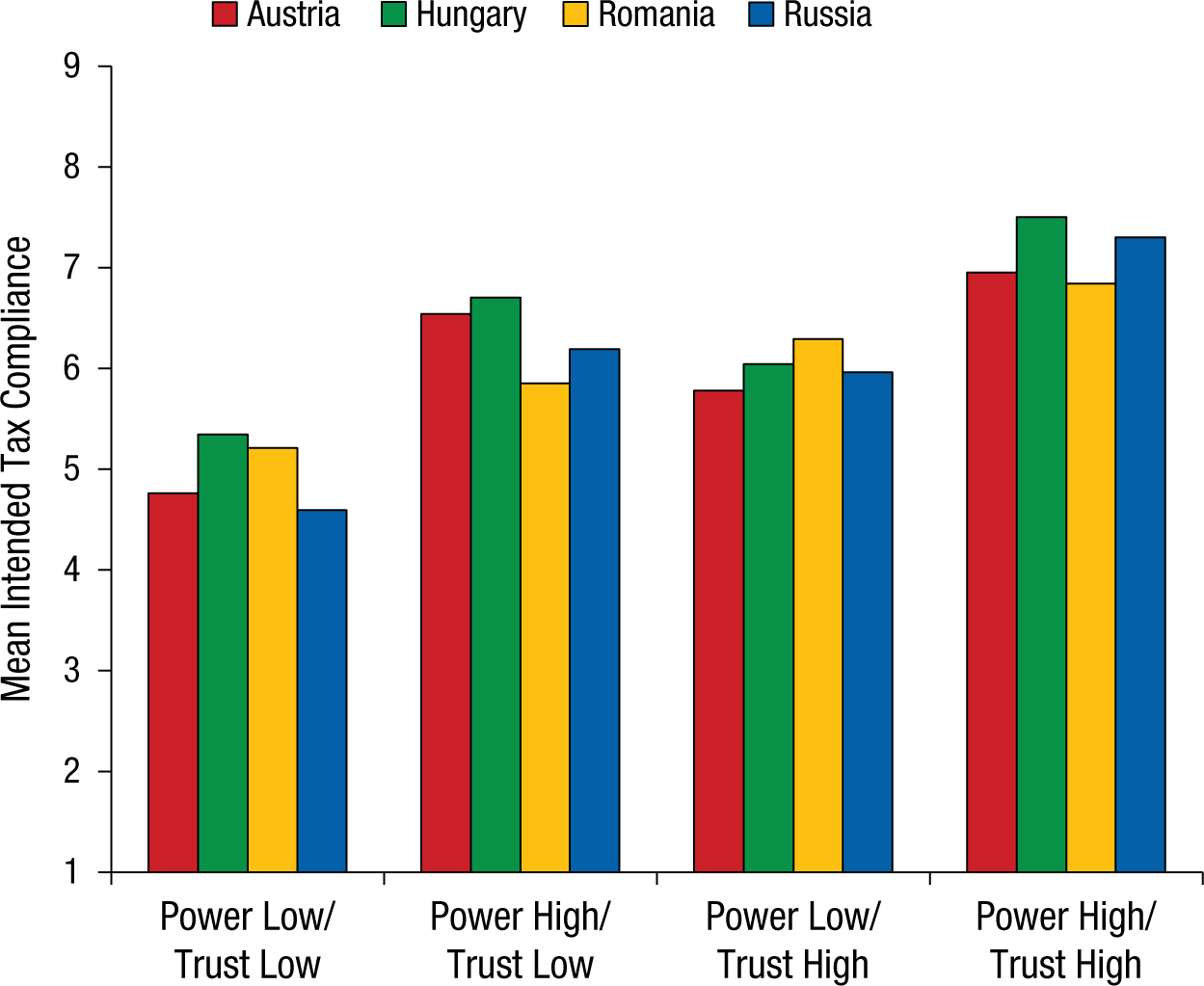

An experiment was conducted to manipulate the power of authorities and taxpayers’ trust in authorities, using scenario techniques, and to assess intentions to declare taxes honestly in four European countries: Austria, Hungary, Romania, and Russia (Kogler et al., 2013). The aim was to test the impact of power and trust on compliance in countries with different institutional, political, and societal characteristics. In a 2 × 2 design, scenarios described tax authorities as either trustworthy or untrustworthy and as either powerful or powerless. Data from this study, graphed in Figure 3, showed that intentions to declare taxes honestly were highest in all countries if the authorities were described as powerful and trustworthy; conversely, evasion was high if both power and trust were at a minimum. In addition, perceptions of high power boosted enforced compliance, whereas high trust was related to strong voluntary cooperation. As in many studies on tax evasion, women were found to be more honest than men.

Graph showing mean intended tax compliance as a function of power of and trust in tax authorities, based on data from a cross-cultural experiment. Data shown were drawn from Kogler et al. (2013; Table 2).

Further confirmation was obtained in an online experiment using a sample of self-employed taxpayers and in a paid laboratory experiment using a student sample. In the latter, tax-compliance behavior had real monetary consequences, such that participants left the laboratory with more or less money depending on their decisions during the experiment. As predicted, the amount of taxes paid was highest if authorities were described as powerful and trustworthy (Wahl, Kastlunger, & Kirchler, 2010).

A recent study with a sample of self-employed Italian taxpayers (Kastlunger, Lozza, Kirchler, & Schabmann, 2013) distinguished two forms of power: legitimate power, which is perceived as a tool to protect cooperative citizens from free riders, and coercive power, which is perceived as oppressive in the absence of trust. Coercive power was negatively related to trust in authorities, whereas legitimate power was positively related to such trust. Thus, the framework’s assumption that trust and power interact with each other was confirmed.

Conclusion

The slippery-slope framework integrates puzzling empirical findings from economic and psychological studies on tax behavior. The framework was formulated to integrate economic and psychological perspectives and proposes that both the power of authorities and taxpayers’ trust in authorities are important determinants of compliance. Empirical studies on the impact of power and trust on intended and observed compliance in the laboratory have supported this assumption. Tax authorities should promote cooperation, rather than relying exclusively on the deterrent effects of audits and fines (Alm et al., 2012).

The psychological approach to explaining tax behavior has contributed to a change in tax authorities’ views on regulating citizens’ behaviors and has affected governmental supervisory practice. That power and trust are essential for good tax governance is being seriously considered by authorities in various countries (Organisation for Economic Co-operation and Development, 2013). For instance, to improve interactions with their clientele, tax administrators in the Netherlands and Austria have started pilot projects for young entrepreneurs. Duties and service facilities are explained to these inexperienced taxpayers, and cooperation—rather than control—is fostered right from the start of a business. In the “fair-play” initiative, Austrian tax authorities emphasize differences between taxpayers in their willingness to pay and the importance of reacting with adequate regulation strategies ranging from deterrence to support (Müller, 2012). In 2005, the Dutch Tax and Customs Administration introduced a pioneering supervisory approach, “horizontal monitoring,” as an alternative to the traditional “vertical monitoring.” This approach is based on the firm conviction that a positive relationship, based on mutual trust, between taxpayers, tax practitioners, and tax authorities reduces unnecessary supervisory costs and burdens, complex discussions about tax designs on the edge of legality, and aggressive tax planning with retrospective adjustments (Committee Horizontal Monitoring Tax and Customs Administration, 2012).

In summary, paradigms in the scientific discussion on tax behavior and regulatory practice seem to have changed recently, in line with the propositions of the slippery-slope framework. By emphasizing the importance of trust as a precondition for voluntary cooperation, the theory has contributed to knowledge about the behavior of compliance-minded taxpayers. Regulation takes place on a slippery slope, and authorities are required to find the right balance between offering supportive services and ruling with an iron fist.

Footnotes

Declaration of Conflicting Interests

The authors declared that they had no conflicts of interest with respect to their authorship or the publication of this article.