Abstract

Loss aversion is a central element of prospect theory, the dominant theory of decision making under uncertainty for the past four decades, and refers to the overweighting of potential losses relative to equivalent gains, a critical determinant of risky decision making. Recent advances in affective and decision neuroscience have shed new light on the psychological and neurobiological mechanisms underlying loss aversion. Here, integrating disparate literatures from the level of neurotransmitters to subjective reports of emotion, we propose a novel neural and computational framework that links norepinephrine to loss aversion and identifies a distinct role for dopamine in risk taking for rewards. We also propose that loss aversion specifically relates to anticipated emotions and aspects of the immediate experience of realized gains and losses but not their long-term emotional consequences, highlighting an underappreciated temporal structure. Finally, we discuss challenges to loss aversion and the relevance of loss aversion to understanding psychiatric disorders. Refining models of loss aversion will have broad consequences for the science of decision making and for how we understand individual variation in economic preferences and psychological well-being across both healthy and psychiatric populations.

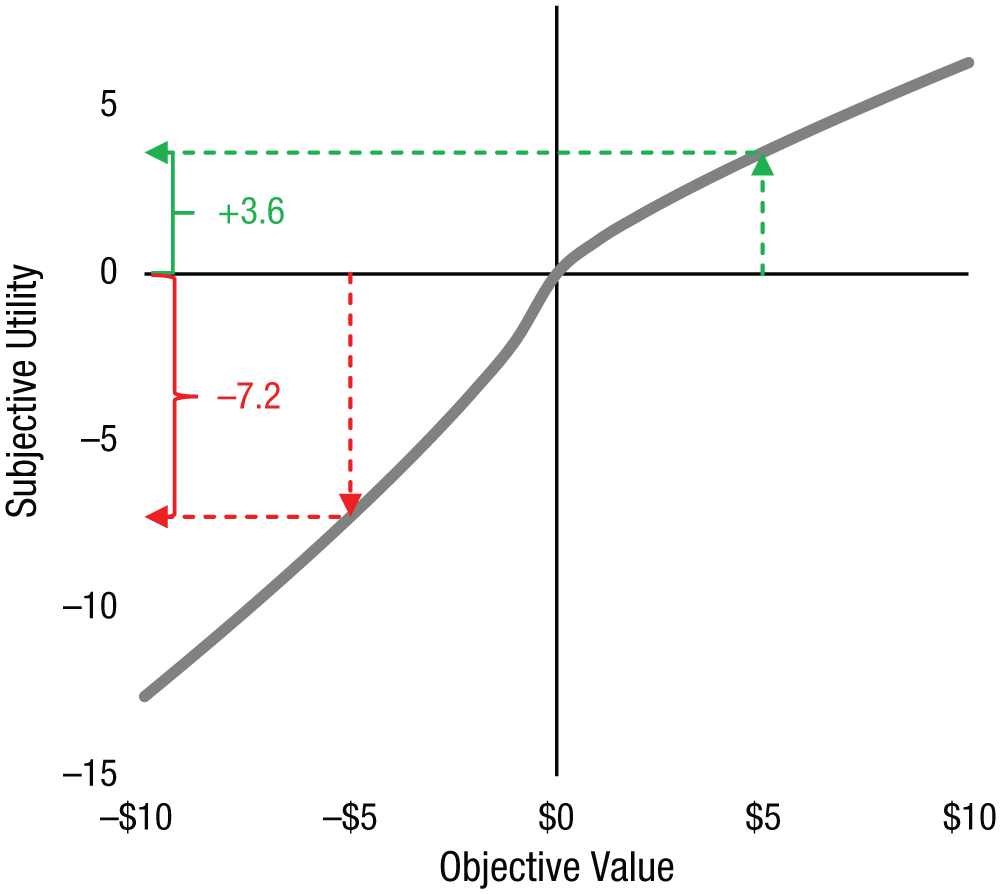

For centuries, psychologists and economists have studied how we make decisions in the face of uncertainty. One particular framework, prospect theory, has dominated research on risky decision making since its introduction almost four decades ago (Kahneman & Tversky, 1979). Arguably the single most influential aspect of prospect theory is the idea that when making choices, people overweight losses relative to equivalently sized gains, a phenomenon called loss aversion, introduced with the memorable phrase “losses loom larger than gains” (Kahneman & Tversky, 1979, p. 279). Loss aversion was computationally formalized as a multiplicative weight on losses relative to gains, represented by the parameter λ (Tversky & Kahneman, 1991; see Fig. 1), and was separate from risk aversion (arising from curvature in the utility function), represented by the parameter ρ: If x ≥ 0, then u(x) = xρ. If x < 0, then u(x) = −λ × (–x)ρ.

An example prospect-theory utility function (gray line) with a loss-aversion coefficient λ of 2 and risk-aversion parameter ρ of 0.8 capturing the relationship between subjective and objective values. The loss-aversion coefficient of 2 here means that losses carry exactly twice the weight of equally sized gains in determining decisions. The green and red lines in the figure show how the objective (and equally sized) values of +$5 and –$5 get translated into very different subjective values; the utility of a loss of $5 is −7.2 (red line), twice the magnitude of the utility of an equally sized gain, +3.6 (green line). While the steepness of the slope in the loss domain versus the gain domain reflects a typical degree of loss aversion, curvature in the utility function captures common features of economic choice, including risk aversion in gains and risk seeking in losses. This curvature means that $5 is worth more than a lottery with equal probabilities of receiving $10 or $0, even though the average return of the lottery and the sure $5 are the same.

Loss aversion has been argued to be present in both risky settings (Gächter, Johnson, & Herrmann, 2007; Kahneman & Tversky, 1979) and riskless settings (Gächter et al., 2007; Tversky & Kahneman, 1991). It is not normatively good or bad per se—for example, in a survival context, loss aversion may prevent starvation or death, but in an investment context, loss aversion can reduce earnings. In keeping with commonly accepted shorthand, hereafter we use the phrase loss-averse behavior to indicate decisions that are consistent with loss aversion as specified within prospect theory.

Who Is Loss Averse, and For What?

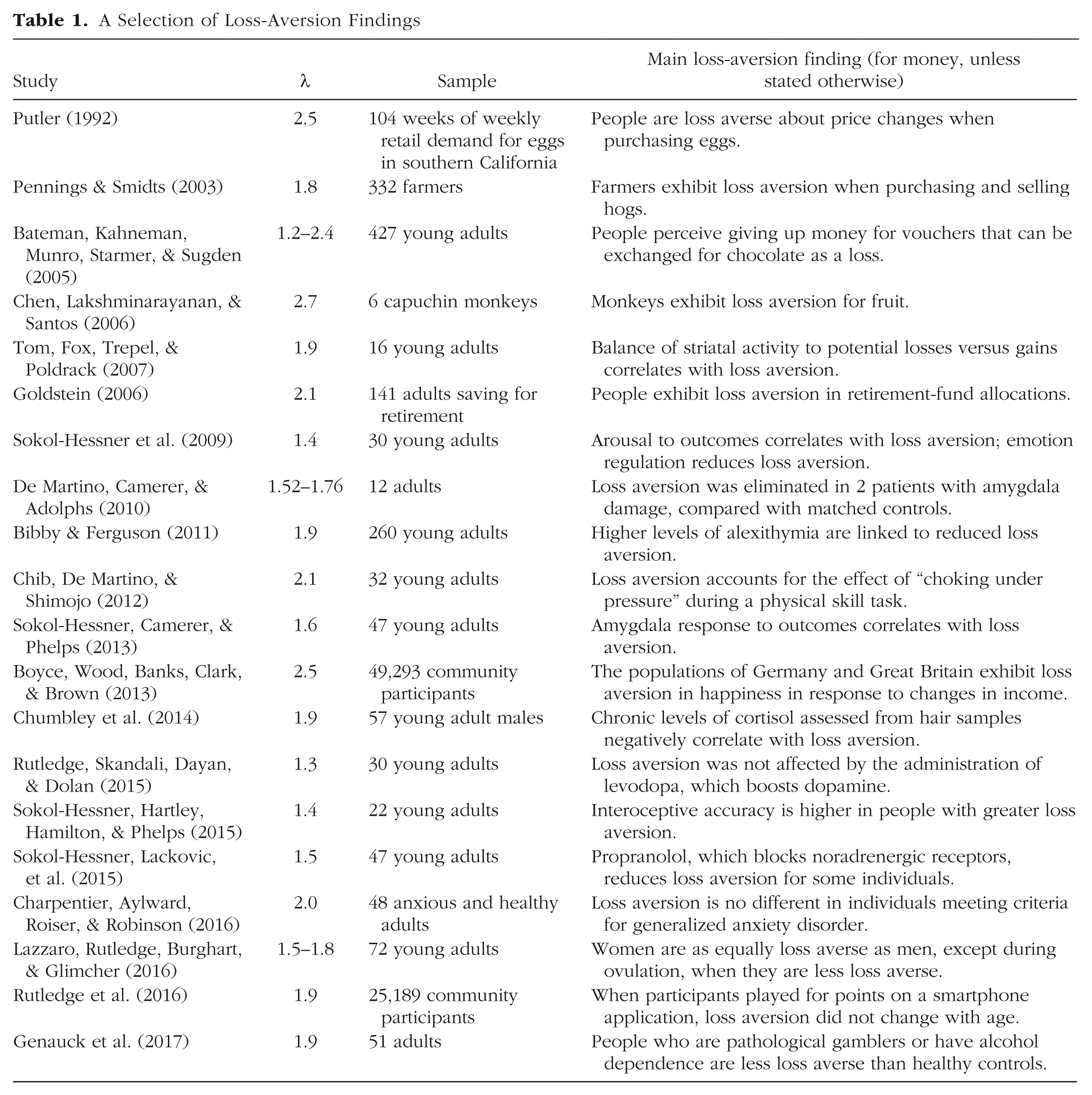

Research on loss aversion has become considerably more common in recent years, establishing that loss-averse behavior is nearly ubiquitous, appearing across different groups of people, types of choices, and even species. For example, professional traders (Haigh & List, 2005), taxi drivers (Camerer, Babcock, Loewenstein, & Thaler, 1997), young and elderly people (Rutledge et al., 2016), and capuchin monkeys (Chen, Lakshminarayanan, & Santos, 2006) exhibit loss-averse behavior (see Table 1). People are loss averse for money (e.g., Rutledge, Skandali, Dayan, & Dolan, 2015; Sokol-Hessner et al., 2009), goods (Bateman, Kahneman, Munro, Starmer, & Sugden, 2005), and labor decisions (Camerer et al., 1997). Loss aversion is generally higher for larger stakes in singular (not repeated) choices, is reduced but not eliminated by experience (Camerer et al., 1997; Haigh & List, 2005), and can vary with context such that in some environments (such as casinos), individuals may have lower average levels of loss aversion than in other environments.

A Selection of Loss-Aversion Findings

Often overlooked is the fact that loss aversion varies considerably across individuals but is stable over time within individuals (Brown et al., 2014; Rutledge et al., 2015), making it a reliable measure of individual differences in risky decision making. Such variability also means that while the population may, on average, be loss averse (λ > 1), a given individual may be gain–loss neutral (λ = 1), or even gain-seeking (λ < 1). Importantly, recent studies have also begun to establish the affective and neural processes underlying loss aversion, with critical implications for understanding how and when it is observed, why healthy populations have so much variability, and how it is affected by psychiatric disorders.

Loss Aversion and Affect

The ubiquity of loss-averse behavior and the aforementioned variability in loss aversion simultaneously raise the question, “What is the source of loss aversion?” One compelling response comes from affective science, which suggests that loss aversion has its roots (in both its ubiquity and its variance) in asymmetric emotional responses to either potential or actual losses and gains. Psychophysiological research has shown that arousal responses to loss and gain outcomes are correlated with the estimated degree of individual loss aversion, and emotion-regulation strategies reduced loss aversion and physiological responses to loss outcomes (Sokol-Hessner et al., 2009). Further links to emotion have been established by studies reporting that people with high interoceptive ability have increased loss aversion (Sokol-Hessner, Hartley, Hamilton, & Phelps, 2015), while people with alexithymia, a disorder of affect perception, have reduced loss aversion (Bibby & Ferguson, 2011). Hormones, associated with more gradual changes in emotion, have also been linked to loss aversion in that both ovulation in females (Lazzaro, Rutledge, Burghart, & Glimcher, 2016) and elevated levels of the stress hormone cortisol have been linked to reduced loss aversion (Chumbley et al., 2014; but see Sokol-Hessner, Raio, Gottesman, Lackovic, & Phelps, 2016).

Equally important to consider, however, are the aspects of affective experience to which loss aversion does not appear to be related. Individuals with generalized anxiety disorder do not have increased loss aversion (although they do have increased risk aversion, a dissociation identified through the use of computational modeling; Charpentier, Aylward, Roiser, & Robinson, 2016). Happiness after gain and loss outcomes is not related to loss aversion as expressed at the time of decision (Kermer, Driver-Linn, Wilson, & Gilbert, 2006; Rutledge, Skandali, Dayan, & Dolan, 2014), although people do expect loss outcomes to have a greater emotional impact than equivalent gains (Kermer et al., 2006). Moment-to-moment happiness instead depends on the cumulative impact of recent outcomes relative to expectations about those outcomes (e.g., prediction errors), with no differential emphasis on losses compared with gains on average (Rutledge et al., 2014). Together, these findings suggest that asymmetric affective processing of gains and losses may be most strongly present during the anticipation of possible gains and losses and the immediate experience of gain and loss outcomes, with both types of emotional experience being associated with loss-averse choices.

However, asymmetric gain/loss processing does not extend even a few seconds after outcomes occur to longer-lasting emotional states such as happiness. But one study found that year-on-year losses in income decreased subjective well-being more than year-on-year gains in income increased subjective well-being (Boyce, Wood, Banks, Clark, & Brown, 2013). One possibility is that income losses disproportionately influence subjective well-being not because of the experience of the loss itself but because of an increase in the number of negative events resulting from decreased income (e.g., difficulty paying for normal daily expenses that were previously affordable). In other words, if the experience of a loss is brief and does not have significant lasting consequences (perhaps because of its small size), then its impact may be rapidly diluted by time, but if a loss leads to an increased frequency of subsequent negative events (as could happen with a significant decrease in income), then its affective impact may also persist and lead to the observed asymmetric gain/loss response pattern similar to that expressed during decisions and consistent with loss aversion. If such asymmetric outcome processing is, in fact, at the root of the effect of income changes on happiness, then the magnitude of that effect for a given person should correlate with that person’s loss aversion as measured from his or her decisions.

These recent findings suggest that loss aversion and subsequent gain/loss processing have an underappreciated temporal structure that is critical to determining when one would expect to observe loss-averse behavior and disproportionate affective consequences for losses. Decisions between options with potential gains and losses reflect how an individual would emotionally experience those gains and losses, but given even small amounts of time or intervening events, affective responses rapidly equilibrate and diverge from decisions.

The Neural and Psychological Basis of Loss Aversion

Understanding why and how loss aversion and asymmetric gain/loss processing occur requires neuroscience. In turn, a greater understanding of the underlying neural mechanisms promises to aid the development of more accurate models of human behavior. Behavioral scientists who take the time to learn about the brain may benefit from understanding the physiological constraints that it places on behavior. Research on the neuroscientific basis of loss aversion has identified several critical neural components, suggesting a model of loss aversion in the human brain and providing links to the neuroscience of affect. While cortical structures, including the ventromedial prefrontal cortex and posterior cingulate cortex, have been implicated in representing the overall subjective value of stimuli (Clithero & Rangel, 2014), two subcortical targets have emerged as the most consistently related to loss aversion. Neuroimaging studies have consistently identified two regions whose activity at the time of decisions and the receipt of outcomes correlates with loss aversion: the striatum (Canessa et al., 2017; Canessa et al., 2013; Chib, De Martino, Shimojo, & O’Doherty, 2012; Sokol-Hessner, Camerer, & Phelps, 2013; Tom, Fox, Trepel, & Poldrack, 2007) and the amygdala (Canessa et al., 2013; Charpentier, De Martino, Sim, Sharot, & Roiser, 2016; Sokol-Hessner et al., 2013). Studies of patients have provided corroborating evidence that damage to the amygdala eliminates loss aversion (De Martino, Camerer, & Adolphs, 2010).

One of the major neuromodulatory inputs to the striatum is dopamine, which has long been linked to risk-taking behavior but not to loss aversion itself. Dopaminergic inputs to the striatum are known to represent the subjective value of rewarding options (Lak, Stauffer, & Schultz, 2014), but it is not known whether these subjective values reflect potential losses. One study administering a chemical precursor to dopamine, levodopa, during a risky decision-making task revealed that while levodopa increased both reward seeking (i.e., gambling in trials with potential gains but not losses) and happiness after small rewards, levodopa did not affect loss aversion (Rutledge et al., 2015). Computational models identified this increase in reward seeking as changes in a value-independent Pavlovian “approach” parameter. Another study in which participants chose between safe and risky options that featured only potential gains also revealed an overall increase in risk taking for rewards after levodopa administration (Rigoli et al., 2016). Dopamine has been linked to happiness resulting from rewards, and a link between happiness and recent “good” news is consistent with extensive literature on dopaminergic systems representing deviations from expectations (e.g., prediction errors; Rutledge et al., 2014). Healthy aging, during which there is a substantial decline in the dopamine system, is also associated with a marked reduction in reward seeking but no change in loss aversion (Rutledge et al., 2016). These findings suggest that dopamine’s role in risk taking may be most directly related to reward seeking and not loss aversion per se.

In contrast, converging evidence has been found for a possible neurohormonal mechanism underlying the amygdala’s role in loss aversion. Studies on rodents have found that the amygdala influences striatally mediated actions to avoid aversive stimuli via a noradrenergic pathway (McGaugh, 2002). Loss aversion might rely on a similar amygdala–striatal noradrenergic circuit in humans. Supporting this hypothesis, positron-emission tomography assays of noradrenergic activity have found that individuals with lower noradrenergic transporter density (presumably leading to greater noradrenergic transmission) are more loss averse (Takahashi et al., 2013) and that the noradrenergic receptor antagonist propranolol selectively reduces loss aversion but leaves risk attitudes unaffected (Sokol-Hessner, Lackovic, et al., 2015), in contrast to the effects of the dopamine precursor levodopa. Finally, in contrast to the parallel decline of the dopamine system and reward seeking over the life span, discussed above, the noradrenergic system is more stable over the life span (Moll et al., 2000), potentially explaining why loss aversion does not change substantially with age.

Together, these findings suggest a novel model for the neural mechanisms underlying loss aversion (see Fig. 2), in which the striatum receives dopaminergic inputs that reflect the subjective value of potential rewards and the amygdala modulates the striatum via a noradrenergic pathway sensitive to potential losses. This model of loss aversion is consistent with proposals that an amygdala–striatal modulatory circuit dependent on noradrenergic signaling contributes to a variety of flexible behaviors (LeDoux & Gorman, 2001; Phelps, Lempert, & Sokol-Hessner, 2014). On the basis of this model, we predict that while manipulations of the dopaminergic system will modulate risky decision making in contexts with potential gains but not losses, these manipulations will have little effect in the presence of potential losses because of modulation of the striatum by amygdala inputs. In contrast, boosting noradrenergic activity will increase the tendency to avoid losses in decisions that feature both potential gains and potential losses.

Psychological and neural model of loss aversion. In this model, reward and loss information, which have separate neural substrates, converge on the striatum to affect choices. VTA = ventral tegmental area.

Challenges to Loss Aversion

Loss aversion has been subject to challenges in recent years because of research that emphasizes context dependence. These studies have revealed consistent shifts in decision making as a function of recent history (Jeuchems, Balaguer, Ruz, & Summerfield, 2017; Post, van den Assem, Baltussen, & Thaler, 2008; Rigoli et al., 2016) or current context (Louie, Khaw, & Glimcher, 2013; Yamada, Louie, Tymula, & Glimcher, 2018) explained by biologically plausible normalization models that consider values relative to their context. Given our growing understanding of the importance of context in decision making, it is unsurprising that loss aversion varies across environments (Ert & Erev, 2013; Mukherjee, Sahay, Pammi, & Srinivasan, 2017; Tversky & Kahneman, 1981), although there is yet no model that explicitly integrates contextually sensitive normalization computations with the gain/loss asymmetries that explain loss aversion.

However, even in a context in which loss aversion is not present at the group level, we would still expect individuals to exhibit degrees of loss aversion that are meaningfully above and below the group average. These stable individual differences should persist across different contexts because of consistency in the underlying affective and neural processes. We contend that recent studies challenging the extent of loss aversion present in different environments do not invalidate its usefulness. Our framework highlights the value of using computational models to capture stable individual differences, regardless of group-level averages, in predicting the choices people make and in relating these differences to well-being.

Conclusion

Prospect theory has dominated the field of decision making for nearly four decades precisely because of its explanatory power. Though prospect theory consists of multiple components (including probability weighting, a reference point, and risk attitudes), loss aversion is arguably the most famous aspect of the theory and a central reason for its continued remarkable dominance and its wide range of influences on science, business, medicine, and policy.

The sources of individual variability in loss aversion remain under investigation. The question of who is loss averse and by how much has critical implications, especially in psychiatric contexts. Although anxiety disorder affects risk but not loss aversion (Charpentier, Aylward, et al., 2016), one possible theory of depression is that negative events are overweighted relative to positive events during decision making, leading an individual to perceive all possible actions as typically leading to poor outcomes. Another clinical context in which loss aversion may have particular importance could be hoarding, in which individuals are unable to dispose of goods, a behavior that could be explained by an excessive degree of loss aversion. When considering the possible roles of loss aversion in psychiatric disorders, the specific stimuli (e.g., monetary vs. social outcomes) may be important, as gain–loss asymmetries may have unique characteristics in different domains, and these asymmetries may also vary with context. More broadly, the pervasive nature of loss aversion, combined with its variability, suggests that loss aversion may be of wide and profound relevance in understanding the choices that people make.

The psychological and neurobiological framework that we propose for understanding loss aversion reflects a number of recent advances in computational and affective neuroscience. Our model makes novel predictions for the emotional consequences of loss aversion and the situations in which neuromodulatory manipulations will affect choices. We predict that the asymmetric affective consequences of loss aversion will rapidly diminish with time and that manipulations of the dopaminergic system will alter risk seeking but not loss aversion, in contrast to manipulations of the noradrenergic system, which will alter loss aversion. However, many unanswered questions remain. In this light, continued refinement of psychological and neural models of loss aversion and decision making will have broad benefits for the science of decision making and society more generally, not only because of continuing economic relevance but also because of the importance of loss aversion for well-being in healthy and psychiatric populations.

Recommended Reading

Ert, E., & Erev, I. (2013). (See References). Six experiments highlighting specific situations that increase or decrease loss-averse behavior, with the authors ultimately questioning the validity of the concept of loss aversion in the face of manipulations that easily alter its extent.

Phelps, E. A., Lempert, K. M., & Sokol-Hessner, P. (2014). (See References). A thorough review detailing the neuroscientific bases of various interactions between emotion and decision making relevant to the study of loss aversion.

Rutledge, R. B., Skandali, N., Dayan, P., & Dolan, R. J. (2015). (See References). Explains the effect of pharmacologically boosting dopamine on decision making under uncertainty as increasing reward seeking without affecting loss aversion.

Sokol-Hessner, P., Hsu, M., Curley, N. G., Delgado, M. R., Camerer, C. F., & Phelps, E. A. (2009). (See References). Links loss aversion to physiological arousal responses to gain and loss outcomes, and shows that emotionregulation strategies can reduce both loss aversion and arousal responses to loss outcomes.

Footnotes

Action Editor

Randall W. Engle served as action editor for this article.

Declaration of Conflicting Interests

The author(s) declared that there were no conflicts of interest with respect to the authorship or the publication of this article.

Funding

R. B. Rutledge is supported by an Medical Research Council Career Development Award (MR/N02401X/1) and by the Max Planck Society. The Wellcome Centre for Human Neuroimaging is supported by core funding from the Wellcome Trust (091593/Z/10/Z).