Abstract

This article explores the politics of expertise in financialized real estate markets. It questions: What expertise is valued in decision-making? How does the type of knowledge demanded by market actors reflect a prioritization of particular forms of expertise and their corresponding experts? In turn, what does this mean for how problems, in this case the question of sustainable property, are understood and navigated in real estate markets? To explore these questions, I interrogate the motivations behind sourcing experts and data in Zurich’s property market. Drawing from interviews with investors and consultants in sustainable real estate, I explore how financial sector sustainability agendas become usable in urban contexts. Building on ideas from the politics of expertise and knowledge coalitions, I show how sustainability is translated into financial(ized) processes: increasing demand for finance-aligned data and consultancies. This reconfigures urban expertise and renders sustainability a financial issue with an urban materiality, rather than an urban issue with financial roots.

Introduction

In mid-2024, I found myself standing in a Google-inspired office that houses a sustainability consultancy in the cool part of Zurich, a few kilometres but seemingly very far from the glass facades and heavy wood of the investment firm I visited the day before. Over the course of our hour-long conversation, the sustainability consultant I was interviewing explained the value of their work – and its evolution. It started as a university spin-out – a story told to build legitimacy – and rode the wave of the 90s and early 00s tech boom. The company evolved, responding to growing demand for understanding sustainability in an urban context. What was once a digital platform became a client-facing advisory firm for investors looking to improve sustainability credentials while investing in property. My interviewee explained that the change had been an organic evolution, including rapid growth driven by demand for the measurement, assessment and follow-on advice to improve sustainability agendas in the real estate industry. The company is now one of the biggest advisory firms for real estate funds, including assessments of current environmental, social and governance (ESG) performances; sustainability strategy development; and data for international benchmarking processes. This conversation was the starting point for exploring ideas around the politics of expertise: What types of expertise are now valued in decision-making? What type of knowledge is (now) needed for city development (see also Raco and Savini, 2019)?

This article’s primary contribution is therefore a reconciliation of the urban politics of expertise, with ideas on urban financialization and sustainability agendas. I am concerned with how the financialization of property markets – as an ongoing and dynamic, sometimes contested, process – is enabled by particular types of knowledge and expertise. I am interested in how new forms of knowledge create spaces of investability – or make certain spaces more investable. In focusing on knowledge production and use, I am concerned with the people and the data that drive this process, and I question what the motivation for sourcing these experts and data is. The way a problem is framed, especially when a ready-made solution is assumed, reshapes the kind of expertise considered necessary to address it. Urban development and sustainability are inherently political, involving complex challenges like reducing buildings’ carbon footprints and managing climate risks. When financial systems define and validate sustainability issues in economic terms, the kind of knowledge valued in the built environment shifts. This makes financial experts appear best equipped to solve such problems, especially in contexts like Switzerland, where markets are highly financialized.

Noting the well-established literature on knowledge in urban and regional policy making, including with regards to specific urban futures and the role of finance (see Ward, 2018), in this article, I focus on cross-sector learnings. Inspired by research that takes seriously the complexities of the private sector and the need to unpack the black box of what is happening in urban development (Raco et al., 2019), to more precisely and successfully influence the outcomes, I focus purely on private actors. I draw on interviews with investors and consultants specializing in sustainable urbanism, as an entry point for understanding how sustainability agendas from the financial sector have been enmeshed and rendered usable in an urban context.

Drawing on ideas around the politics of expertise (Robin, 2022; Robin and Acuto, 2022), research on knowledge coalitions (Taşan-Kok, 2024) and real estate market dynamism (Adams and Tiesdell, 2012), this article answers the question of how financialization evolves in the face of sustainability agendas. Specifically, I answer: How do urban real estate investors learn about, design and implement ESG strategies? What data do they need? What is the role of consultants in this process? I argue that consultants are hired to bring expertise and knowledge that enables the transference of ESG-informed financial logics into an urban context. Consultants provide a reputational dimension: they allow in-house teams to externally validate hypotheses and approaches. My analysis shows that while the role of consultancies at the point of market development for ESG and sustainability concerns is apparent, the future is less clear, with a growth in in-house experts and an emerging but as yet uncertain move away from this initial transfer and performance of expertise.

An evolving urban politics of expertise and the role of finance

This article takes as a starting point that urban development and management are increasingly financialized, understood as having more deeply embedded financial actors and their logics in the everyday processes (Pike and Pollard, 2010). Financialization is rooted in a growing societal role for finance, understood as a spatially and temporally articulated system of human–environment relationships, where people generate value systems through money (Wójcik, 2025; Wójcik et al., 2024). Finance is made most visible in relationally constituted global financial networks (GFN), which are defined by a multiplicity of industries, and are constituted through the connections of place, people and policy that make up international financial centres and their networks (Pažitka et al., 2021). This cross-sectoral understanding calls to attention dominant industries, including real estate, but also the supporting plethora of actors that enable finance as an object and financialization as a process. Recognizing this relationality requires engaging with how different types of firms and knowledge co-constitute changing markets within GFN.

Part of this is acknowledging and exploring how investment decision-making is never made in a void; it reflects the particularities of the situation, and the decision-making tools and knowledge at the disposal of the actors and organizations making the decisions (Shimbo and Sanfelici, 2023). In urban real estate markets, actors create and work with knowledge coalitions, using market intelligence to navigate market and regulatory dynamics (Taşan-Kok, 2024). As Harris (2023) explains, ‘experts and expertise have always been a central, if largely assumed and underacknowledged, component to any modern, technological society’ (p. 62). The politics of what knowledge is valued is contested (Harris, 2023; Trundle and Organo, 2022). The contestations and politics of what sort of knowledge is valued plays out across urban development and governance processes (Perry, 2023). The transformation of urban experts under the dominant systems of urban growth, including but not limited to a more financialized system of property ownership, requires sustained engagement with what this means for the type of expertise or experts needed.

Critical urban scholarship, including planning research, needs to continue to explore the political economy of urban expertise, to examine how particular tools or devices used to navigate the politics of expert interactions, create and reinforce inequality (Robin and Acuto, 2022). In a more financialized model of urban development and ownership (i.e. not just the means of producing urban spaces but in their ongoing management and eventual potential destruction), private expertise is a driving force (Nethercote, 2022). This mode of development requires investors to learn new ways of operating, including the development of new techniques of valuation (Crosby and Henneberry, 2016), which therefore created a new politics of urban expertise (Robin, 2022), where shifting knowledge practices demand new types of information, devices and mechanisms (Colenutt, 2022; Rydin, 2016).

Attending to the contingent nature of knowledge production and how mechanisms allow certain experts to assert their dominance, Nethercote (2022) shows the assemblage of a market for so-called build-to-rent rental housing in Australia. Their analysis, building on the long history of market-making analysis following Callon (2007), shows how consultants and experts are brought into the process to make legible, and ultimately investable, new forms of real estate (Nethercote, 2022; see also David and Halbert, 2014). Many of these consultants might be broadly categorized as international property consultants, who work to translate sites and projects into assets for investors (see, for example, Crosby and Henneberry, 2016; Searle, 2014), often requiring intermediary organizations to help navigate different systems of knowledge or ways of valuing sites (Halbert and Rouanet, 2014). Rather than merely translating knowledge into a ‘valuation’ practice to be replicated across contexts and asset classes, consultants therefore navigate the realities of site-specificities (Shimbo and Sanfelici, 2023). As financial systems evolve, what remains an interesting question is both how financial logics remain – or are contested – in urban decision-making process as new agendas, such as sustainability, come to bear (Attuyer et al., 2012; Hall and Foxon, 2014; Theurillat and Crevoisier, 2013). In this article, I build on Attuyer et al. (2012) who show how large investors respond to regulatory demands around sustainability. Rather than focus compliance and how this must be reconciled with existing business and investment processes, I examine responses to emerging agendas and social pressures which are often reinforced through private regulations rather than state-driven agendas. I examine how particular types of knowledge or information are demanded and the way in which this is deployed as a form of expert-making practice (Kuus, 2011).

This matters because the consequences of urban financialization are stark. Urban financialization, particularly the financialization of housing (Aalbers et al., 2020; Taylor and Aalbers, 2024), has rendered property ‘just another asset class’, rather than recognizing its other values, including the social value of a home or the impact on tenants (Aalbers, 2019; Fields and Uffer, 2016; Waldron, 2024; White, 2023; Wijburg et al., 2018). Research has shown how financial motivations increase evictions, decrease property maintenance, undermine the creation of ‘homes’ and embroil the ‘unwilling subjects’ of financialization into the processes (Fields, 2017).

At the same time, in many property markets globally, new types of firms or models for providing housing have appeared, as investors seek new opportunities for investment (August, 2020; Beswick et al., 2016; Gotham, 2012; Nethercote, 2020), often at the edge of traditional forms of real estate investment (Horton, 2021; White and Madden, 2024). Investors have to make sense of the market, to better understand how real estate fits within their portfolio of other assets: What role does it play in providing stability? How is it part of a diversification strategy? How can different properties complement one another? How should decisions be made about what to invest in, how long to maintain ownership and how to exit a property? This requires navigating entrenched understandings about how housing should work – the ideologies at play (White and Madden, 2024) – and finding a way to articulate an alternative vision, leveraging pervasive narratives about crisis, under-supply or sustainability to justify shifts in property norms (Brill and Durrant, 2021; Nethercote, 2022).

While more property is becoming, to borrow from industry language, ‘asset worthy’, such that there was an over 20% growth in assets under management between 2022 and 2023, translating property into a standardized asset class is not frictionless (Guironnet et al., 2016; Shimbo and Sanfelici, 2023). While there remain certain ‘rules of the game’ or local norms (Ballard and Harrison, 2020; McAllister et al., 2016; Rogers and Koh, 2017), particularly for navigating planning systems, emerging knowledge(s) and practices need to be better understood (Raco and Savini, 2019). With a growing (direct) role for investors in shaping urban outcomes, that is, in deciding what to fund, what to buy and what to sell (or renovate or destroy), the types of knowledge which informs investment decision-making has become more prominent. This is accentuated by both the diversity of investors (Özogul and Taşan-Kok, 2020) and the related range of motivations, regulations and interactions (Stirling et al., 2023; Taşan-Kok et al., 2021). As others have noted, despite pushback against the idea that institutional property ownership (particularly in rental housing markets in Europe) is less prominent than it was predicted to be, it remains important for urban scholarship to understand the strategies that are developed and employed by market actors (Oxenaar et al., 2024).

Within the wider conceptual discussions around financialization and financial geographies, my interest in this article is with sustainability dimensions of financial transactions, and how these are applied in an urban context. The integration of sustainability agendas in urban development has a long history. Research has shown how sustainability ideas have been included in urban decision-making to various degrees and often in contested ways, for example, how the pragmatist approach of planners cannot overcome the ideological framings around sustainability such that it gets watered down in its application (Metzger et al., 2021). This article draws on research showing how sustainability objectives and approaches have been subsumed by financial imperatives and processes. Sustainability issues are now increasingly captured within ESG assessments and strategies, and are therefore increasingly the concern of investors and fund managers, rather than those ‘closer’ to the real estate such as developers or contractors. As such, in this article, I focus on the financial sustainability logics and practices, revealing how the assumption of sustainability under the umbrella of investment decision-making actions necessitates certain people, practices and knowledge.

Case and methods

The research for this article was conducted in Zurich, Switzerland. Zurich is an established node in GFN, understood in this article as the structures and agencies of financial centres, offshore jurisdictions, financial and business services, and governments (Coe et al., 2014). Zurich connects core people, places and institutions within the wider network of international finance. There is long history of classifying cities based on an assumed economic hierarchy or prominence in particular sectors (cf. Sassen, 2001; Wójcik et al., 2019), with more recent focuses on financial activity showing that Zurich is the eighth biggest banking centre globally (Wójcik et al., 2019). In addition, while London remains the largest banking sector, 20% of the biggest banks operating in London are headquartered in Zurich. Analytically, Zurich therefore represents an important location from which to better understand emerging financial logics. With the particular focus on real estate, Swiss cities are additionally important because of their long-standing institutional property ownership. Large financial actors such as UBS’ real estate funds have substantial portfolios across the city. Moreover, Zurich, as with Switzerland as a whole, is a country of tenants and relatively high-quality housing and as such has long been attractive for institutional investment (Theurillat and Crevoisier, 2013).

Data to investigate the research questions were collected from the following sources:

Attending corporate events, both online and in person. During the events, I actively participated, including raising questions directly to asset managers and investors about their concern and engagement with sustainability issues. The events included:

Roundtables with Swiss asset managers who focus on real estate acquisition and management. These events were typically small and closed, with around 20 invitees included from leading firms in the city. The format was largely discussion based with a few ‘interventions’ or ‘provocations’ which illustrated the position of core organizations.

Annual report launches. These events were open events to all and were typically online. The events were largely a presentation of results and expectations in the future with a short Q&A and the end.

ESG strategy and update launches which were similar formats to annual report launches.

ESG and sustainability-specific events, for example, the launch of a new framework for measuring carbon emissions in buildings by advocacy organization. These were a mix of smaller and intimate roundtables discussing how to improve the framework and larger meetings.

Interviews with 20 experts working in urban investment between 2023 and 2024. These interviews complement previous interviews with investors from other cities, as well as direct experience working in climate and sustainability strategy development prior to academia. Interviews included in the data set for this article were:

ESG and sustainability consultants (n = 4);

Planning consultants who attended ESG and sustainability events (n = 6);

Investors, broadly defined but including representatives from asset management companies, real estate investment funds and pension funds (n = 5);

Data providers and research consultants, including global leaders in corporate real estate research and local consultants (n = 5).

The interviews typically lasted between 1 and 2 hours and included interactive dimensions such as working through financial models together or discussing possibilities around strategy-making processes.

Discourse analysis of corporate reports collected from corporate websites, published between 2019 and 2025. The analysis focused on key terms identified during preliminary meetings with investors and financial experts (not included in the interviews). These were complemented by themes identified in the literature. Documents were coded for ecological concern, social concern, claims of responsibility, identified market concerns, identified solutions. Documents were collected in the following forms:

Annual reports from the largest institutional investors in the city;

Sustainability strategies from the largest institutional investors in the city;

Annual reports, sustainability reporting, ESG and sustainability strategies and quarterly updates from interviewee’s companies;

General strategies including board documentation where possible for ESG consultants.

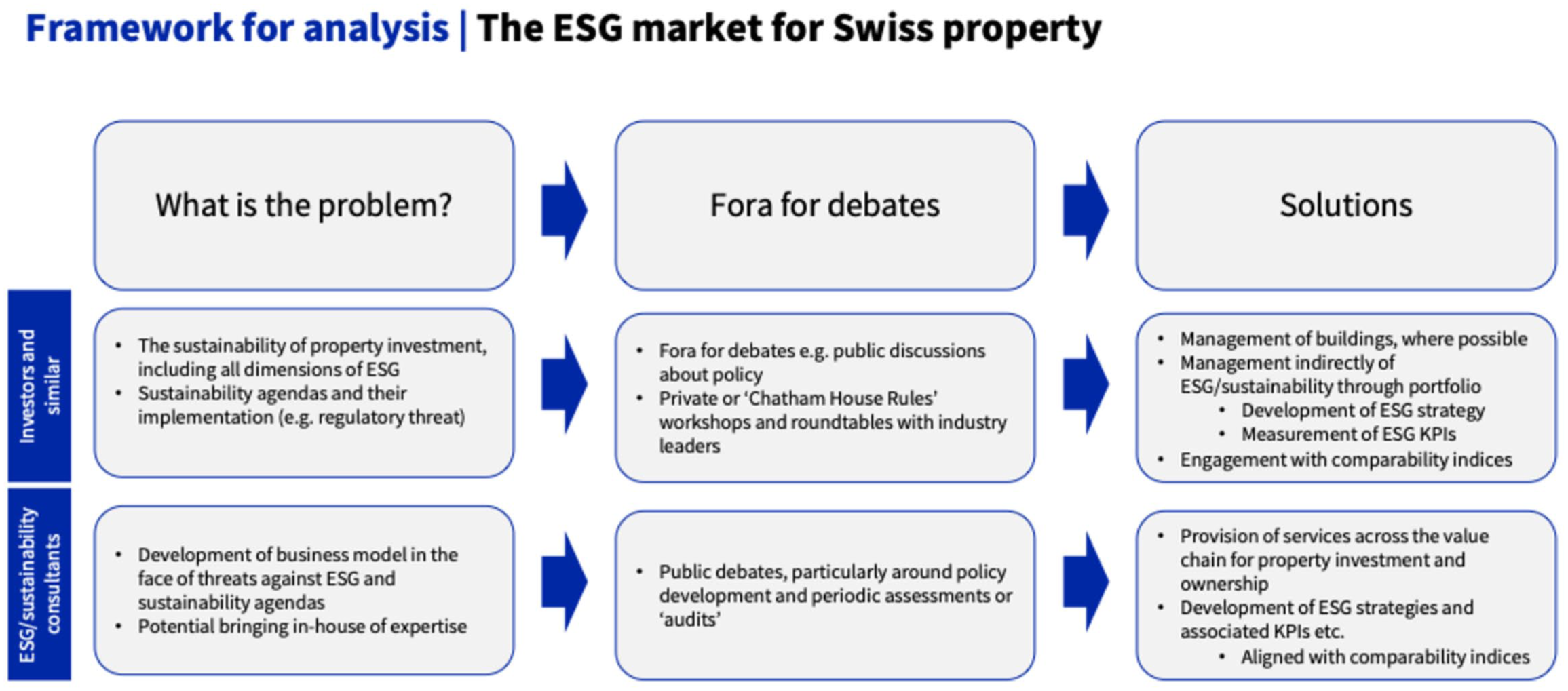

These data were then applied to the following framework (Figure 1). This framework brings together the different actors interviewed and engaged in ESG practices in Swiss property investment, to reveal both the tensions (i.e. the different ways they understand the problem, engage in the solution and think through their role in long-term market provision) and their alignment. In particular, it helped provide a second level of analysis of the data of emerging findings.

Framework for analysis.

To understand how consultants do this and to engage in their role at the intersection of ESG and financialization, this research follows the tools and practices approach to financialization (Chiapello, 2020).

Consultants: providing knowledge, expertise and validation

Consultants have become a staple in urban decision-making, most notably planning consultants who help negotiate directly with authorities, leveraging past experiences, tacit knowledge and personal networks to advance project decisions on behalf of developers (see, for example, Robin, 2022). Consultancy work more generally has become a standard feature of the corporate world, with the industry valued at over 900B USD in 2021. Consultants are understood to bring value to a project in their roles as advisors and legitimators, while allowing firms to outsource some of the trickier politics of corporate decision-making (Mazzucato and Collington, 2024). At the start of this research, it seemed that an easy answer to whether to use ESG consultants, yes: hire consultants for ESG and sustainability work. Mirroring Mazzucato and Collington (2024), consultants were seen to provide two core competencies for developers and investors alike: first, expertise and knowledge on sustainability, including data; and second, a sense of legitimacy and external validation of ideas. However, as the project and interviews evolved, it became clear that investors, particularly those with long histories in other asset classes, felt in-house experts were increasingly important. What is important to reflect on is that for these actors, working in rapidly evolving markets, direct operationalizations of their approaches are difficult; instead, I focus here on the relational processes and forms of expertise that operate through interpretation and framing rather than visible spatial outcomes.

All investors and consultants interviewed saw the core aim of hiring consultants as bringing new forms of knowledge and expertise into the decision-making, with a view that this external expertise would provide a more informed long-term financially sound approach. The changing role of consultants is illustrated in Figure 2.

Illustration of consultant–investor interaction.

Consultancies perform their value by articulating their advisory role as that of an ‘expert’. They typically hire graduates from top-tier universities and then institutionalize particular norms and ways of working that develop a culture of shared knowledge and recognition that their external perspective is both more precise and more strategic because of their exposure to multiple projects and industries over the course of their careers. 1 In the context of ESG and sustainability consultants in Zurich’s property investment, the knowledge can be broadly broken into two categories: sustainability-focused knowledge, for which technical experts were hired; and financial knowledge or ways of working, which speaks to the ongoing process of financialization.

To understand ESG and sustainability, financial investors are heavily influenced by and reliant on consultants. This was particularly true in the early stages of market development, where ESG or sustainability teams within funds or asset management companies investing in real estate were small and did not have the capacity or sometimes skill set to assess, strategise and articulate responses to sustainability ideas. Across the corporate reports analysed, 6 categories of consulting services were identified, as shown in Figure 3.

Tables of consulting services.

Through these services, external experts shape norms and practices (see Knight and Dixon, 2011). As one consultant explained what they are required to do for property owners and investors: Our clients are basically from the banking and insurance sector – also pension funds, and the public cities and cantons. Mainly it is institutional investors or institutional portfolio, for example UBS [. . .] What we do for them: we are trying to support them along the whole journey – how to improve your portfolio in a more sustainable way [. . .] it always starts with the beginning – having a strategy and defining KPIs. (ESG Consultant #1, 2024)

What is notable in how the consultant articulates their value: the firm is specifically concerned with ESG and sustainability in real estate, yet the level they operate at is the portfolio. Departing from the way environmental standards and practices were used to introduce strategy at a building level (Attuyer et al., 2012), these consultants working as more broadly defined ‘sustainability’ or ‘ESG strategy’ consultants specializing in articulating how material changes in business practice translate into investability and financial gains for funds. Examples of how this specifically translated into firm practices include a new reliance on consultants to conduct an ‘ESG audit’, with a view to identifying areas for action. Various sustainability-related actors, artefacts and types of knowledge are mobilized, at different points in the urban development (and investment) and management process, without ascribing a hierarchy where one type of knowledge or one way of abstracting the urban is considered the most viable (Robin, 2022), pointing to an ongoing evolution between what is active and what is latent in decision-making processes (Robin, 2022).

This embedding of financial ways of seeing urban investment, that is, in operating at the portfolio rather than building level, echoes wider patterns seen in this analysis financial logics and practices make their way into urban processes. One interviewee, a CEO trained in Finance who has recently moved into the real estate sector, explained that the origin of their business was trying to address the gap between the financial market and the real estate market. As they saw it, real estate markets lack the knowledge to make informed ESG and sustainability-driven decisions. Working with a wider team of experts, they provide modelled answers to questions around carbon footprints for buildings, as well as risk exposure to extreme events. They saw the role of their firm as being a bridge between the financial world and the real estate sector – helping the latter to ‘catch up’ (ESG consultant #1, 2025; supported further by an interview with ESG advisor). In this way, it is clear that their consultancy work and the provision of particular knowledge positioned them as central experts in defining and ultimately solving problems of sustainability. This is echoed in sustainability reports and online courses offered by consultancies in Zurich who note that Sustainability has long been a key issue in the real estate industry. However, while ecological and social aspects are often in the spotlight, the economic component is frequently underestimated – even though it is crucial for the future viability of investments. (Wüest Partner, 2025)

As is evident in the quote above, there is a recognition that sustainability expertise must sit alongside traditional economic or financial expertise – such narratives work to frame ESG as intimately related to profitability and defines the ‘problem’ investors need to fix as one which is both a question of sustainability (broadly-defined) and profitability.

Core in this problem-definition practice is ensuring the knowledge brought to discussions is understood as important by investors, and that it directly changes how funds act, that is, that it was considered meaningful and actionable by other interviewees. When discussing this form of expertise with investors, it emerged that fund managers see sustainability-specific knowledge as important, particularly when coupled with an awareness of the financial risks and an ability to articulate ideas to more finance-focused people. As one fund manager reflected ‘the balance between technical and being able to speak to the c-suite (the executive level management)’ (Fund manager #2, 2024). In this way, even the more narrowly defined sustainability experience and knowledge was orientated towards investment and financial language and know-how.

These uses of consultants can be understood as an evolution of green market-making activities shown through a reconciliation of ideas from financialization and the politics of sustainable urban development literature. The calculative practices and strategies that shape how investors make decisions about sites and projects (see, for example, Crosby and Henneberry, 2016; Guironnet and Halbert, 2018; van Loon and Aalbers, 2017) must consider how green regulations of standards are translated into market practices over the last decade (Attuyer et al., 2012). In this case, by focusing on the specific use of ESG and sustainability consultants, it becomes evident that financial actors do not only mediate this through established teams and internal processes but also utilize experts, to various degrees, to help inform that decision-making process. Moreover, rather than these experts focusing on translating a site or building to make it investable and/or to translate particular building standards into a financial language (Guironnet and Halbert, 2018), they instead focus on translating investments into green investments – often with little material impact on projects or sites themselves. To do this work of translating and integrating ESG agendas, consultants respond to data demands around ESG and sustainability.

ESG data and knowledge demands: aligning financialized understandings

In helping investors navigate ESG and sustainability demands, consultants must provide data, in a manner that reflects the financialized logics outlined above. This is particularly evident in the emphasis on quantitative modelling which strongly contrasts with more traditional qualitative methods of knowing the city (Raco and Savini, 2019). In its crudest sense, the focus on quantitative data can mean that a buyer purchases a multi-family block without viewing the property, because property statistics alone are sufficient for decision-making. In its more complicated form, it has driven demand for more and better-quality data, a form of capital increasingly driving the contemporary political economies (Sadowski, 2019). In recent years, this has been furthered by technological changes that have shifted expectations for what data can be harvested, cleaned and modelled with. In a financial context, and increasingly in a real estate context, this has shifted market expectation to be that decisions should be more data-driven, with published data behind decisions, and less reliance on the ‘hunch and intuition’ which was historically seen as very important in real estate markets, as one interviewee explained: to be able to push the real estate department to publish as much as their peers, as other asset classes. For now they are behind. (Data specialist #1 2024).

In an interview with one data provider firm who provide data for ESG-based decision-making, the CEO expressed a desire to become ‘the Bloomberg terminal of real estate’, likening their data provision services to the famous data available on traditional asset classes that is well-used by financial actors. As Taşan-Kok (2024) has shown in knowledge networks in Amsterdam, the most visible part of market intelligence channels and networks is the data providers. Building on this, the example here shows how particular types of data present certain types of knowledge as more (or less) valuable. My interviewee went on to explain: ‘before the terminal it was the wolf of wall street, after Bloomberg, the data was available and the finance jobs were more mathematical and quantitative and we are expecting the real estate to change, with data and with us’ (Consultant #2, 2025). The language used here and the comparisons invoked demonstrate how the real estate data firm is aligning their services that frame a financial solution as superior. This data – or market intelligence – may not directly influence what investors do in the immediate term (see also Taşan-Kok, 2024), but it becomes a core means by which investors understand the market and changes how they engage with decision-making.

The second way data emerges is in how the financial sector requires investors to communicate their success relative to others. Data is an important component of all the comparability indices, including in the ESG market. Funds’ growing role in urban development, including in long-term ownership of property, comes with an associated marketing of their abilities and attractiveness to would-be investors. With increased consumer demand for sustainable investments, funds have responded. This in turn has driven comparability indices in real estate. As one fund manager explained, The funniest things some time, if I go speak to an investor he tells me ‘for me building certification, the data, is not that important but the [comparability index] is important – to know you have 5 stars is important’. Yeah but you know to have the five stars I need the data. (Fund manager, #2, 2024)

The data demand here is clearly driven by investor requirements to show sustainability performance and therefore attract further capital to this specific fund. These data are very broad, the most common comparability index is GRESB

2

which uses over 500 indices to compare funds. The nature of such broad comparability processes is that data is a mix of proxy data based on modelled estimates of carbon footprints per square metre; survey data where possible (particularly of tenants); internal assessment data, that is, internal assessment of the social performance of the fund manager as measured by social policies at a firm level; and a quantified assessment of governance processes at a firm level, that is, the translation of board oversight into calculable figures. As one consultant explained how his work relates to GRESB, The external pressure [for ESG consultancies] comes from two sides: it is legal from government and also from investors who are more and more trying to only invest in ESG funds. So GRESB is then the answer to everything. You have your annual report and you report on your annual numbers and you have a thing like GRESB where you get the star rating. (ESG Consultant #1, 2025)

Justifying consultancies: bringing a sense of legitimacy and validation

To advance both their agenda and their role in the ecosystem of urban knowledge and politics, consultants must continually work to be seen as experts (see Keidar, 2023; Mazzucato and Collington, 2024; Vogelpohl, 2019). In the ESG market for Swiss property, this was done in two ways, driven by two factors: first, building on the long-standing corporate belief that consultants can provide the ‘hard’ answers or solutions which might challenge dominant corporate narratives; second, the need to comply with international standards and perceptions that external auditing is more reliable.

Interviewees reflected that external experts were a way of generating momentum internally, without one employee needing to push for a sustainability agenda individually. This was particularly supported by investors and comments by asset managers at roundtables who saw themselves as the one pushing sustainability agendas from within their firm.

We are discussing the possibility of bringing in new ways of financing that would require changes to the building materials in order to justify new types of capital – [representative of investment fund] reflected that this is not supported in a company wide way, but that he will continue to engage in conversation with colleagues about how the evidence presented at today’s event will fit within their sustainability agenda. (Field notes, Real estate roundtable, 2025, name redacted by author)

Consultants have a long history of being used to make hard or more politically challenging decisions in corporate settings. For sustainability, interviewees were most concerned with ensuring broad organizational support for ESG-focused changes, particularly if they do not directly align with commercial agendas, but that having an external expert articulate the value of improving ESG ratings legitimized an agenda that had some support internally, and helped elevate it.

At the same time, one fund manager interviewed also explained that external validation of their ESG audit and or strategy was important for communicating with stakeholders, including regulatory bodies (public and private). Moreover, there was self-awareness that the advice needed to be considered substantial enough to overcome accusations of greenwashing, as a leading real estate advisory firm in Zurich explain, their services include the provision ‘indicators and ratings derived efficiently and automatically [..] the risk of greenwashing is also mitigated’ (Wüest Partner, 2024, emphasis added).

External validation and the role of consultancies in urban development have always been important, as third-party actors such as planning consultants act as important intermediaries in planning processes, both with regulatory bodies and with the wider public (Stapper et al., 2020). One interviewee reflected that ‘of course investors need external audits to show they are reliable’ (Corporate research consultant #1, 2024). Again, consultants provide a legitimacy-making role which validates assessments, strategies and communications beyond the firm.

The future of ESG consultancy work

What is important to note is that the market for consultancy work is not stable (The Financial Times, 2023), and there is a subtle but clear challenge to the dominant view that external experts are needed. This can be seen in two main ways: first, that the market remains fractured and uneven in the type of support offered, as well as the type of firm providing it; second, that there is a notable (but small) shift to in-house experts.

Throughout the research, interviewees reflected how expensive this form of expertise is: ‘We work with consulting firms for sustainability, but you don’t want to know how much it costs.’ (Portfolio manager #1, 2024)

As part of managing this cost, investors seek out specific niche consultants, not relying too heavily on the larger consultancies. Investors and developers included in this research used a range of consultancies; this reveals the non-consolidated nature of this market, while the market for ESG assessments has grown substantially, there is not one firm who are considered ‘the’ best consultants as exists in traditional strategies or consultancy projects (e.g. McKinsey, BCG and Bain for strategy; or Savills, CBRE, JLL and Knight Frank for consultancy on London property).

The second way the market was shown to be unstable was a recognition of bringing experts in-house and the growth of sustainability-focused teams. As one fund manager reflected, at their real estate fund, there was massive growth within the firm, despite continued resistance to a stronger ESG agenda, where they had moved from a single person to ‘now have 4 or 5 people working only on ESG’ (Fund manager #2, 2024). In discussions with one of the largest private banks in Switzerland, the ESG team was keen to explain that they hired in-house experts. Fieldnotes from this conversation highlight that the bank was concerned that demand for ESG information would be sustained and become part of ‘business as usual’ and therefore bringing the expertise in-house was a better long-term business decision (fieldnotes, 2024). This reflects an emerging recognition that consultancies are expensive and do not always deliver a product that is reliably replicable by the firm in future years for ongoing assessments. The lack of clarity about whether the current ESG metrics will become part of normal business, and debates about the potential growth of regulatory requirements versus pushback against ESG more broadly in society creates uncertainty, especially for consultancies who therefore have to continually articulate their value. As one leading consultant explained, At the moment there is no external pressure for our clients to report these numbers. As long as they don’t have enough pressure there’s not going to be any budget for it. (ESG Consultant #1, 2024)

As is evident in the quote above, consultancies see the potential introduction of regulations as important in sustaining their business. As such and to negotiate the potential impact, many of the leading firms actively engage in the policy development process. This is well-established in Switzerland, where leading consultancies in real estate, including those that provide ESG and sustainability services, have long been part of the broader political process. However, in addition to the well-established roles of bigger consultancies, other firms noted their continued engagement, promoting it as part of their legitimation actions: As a sustainability-focused consultancy, Intep continuously observes regulatory and political developments and actively helps shape them [..] By taking an active role in drafting legislation and regulations, we respond flexibly to current and future requirements. In doing so, we open up new markets and give our clients an advantage, preparing them for complex frameworks. (Intep, 2024)

Across interviews, there was less concern with conflict between the different parties involved in decision-making, and rather a concern with what wider policy and regulatory contexts might do. Regardless of whether it was an in-house expert or a consultant, there was alignment across organisations and interviewees that ESG and sustainability measures are required and that relatedly expertise to navigate them is needed.

Discussion: rendering sustainability a financial issue

The way in which particular knowledge(s) and data are utilized in urban decision-making, specifically what knowledge is needed and who positions themselves as experts, has consequences beyond the shift in type of knowledge found in urban discussions: it redefines the parameters of decision-making. The integration of ESG and sustainability agendas into real estate funds’ decision-making practices has helped shift sustainability from being an urban or societal question, to a financial question. This is not because the types of data demanded and utilized are not concerned with environmental elements (or social and governance), but rather that the process of quantifying it for the sake of comparability renders it overly simplified and focused on its capacity to undermine the financial stability of the fund’s performance, rather than the fund’s engagement with the data. The way actors focus on ESG’s usefulness for comparability indices reveals an internal rearticulation of the value of the knowledge, away from its original form and towards an index which is primarily assessing risk and profitability.

This adds to the vast literature on how the way in which a problem is understood and then articulated within policy contexts, comes to shape which types of expertise are then used to ‘solve’ problems (Ferguson, 1990; Hughes-McLure and Mawdsley, 2022; Li, 2007). Much has been written on how problem-definition practices have ultimately re-shaped various societal challenges into a financial framing within critical scholarship (Hughes-McLure and Mawdsley, 2022). It is also important to consider the re-articulation of urban problems to align with financial solutions, as has been shown in this analysis. In looking at the intersection of urban expertise, financialization and the politics of sustainable development, the findings presented above illustrate how ESG consultants operate as key intermediaries in the financialization of urban real estate. The instrument-based approach to financialization (cf. Chiapello, 2020), which required paying attention to the practices and tools that support and facilitate financial actors’ involvement in a range of different situations, revealed the strategies, practices and legitimating actions of consultants. In this context, consultants and the instruments they introduce, including ESG audits, sustainability metrics, data standardization frameworks and comparability indices, function as the tools through which financial logics are embedded into urban decision-making. Their work translates abstract sustainability goals into calculable, investable forms, aligning environmental and social considerations with financial rationalities. Thus, the proliferation of ESG consultancy practices not only evidences the growing institutionalization of sustainability but also reveals how financialization operates through specific expert practices and the instruments that make such expertise actionable and legitimate in the market.

The way in which the problem is framed, with an ‘in the bag solution’ to hand (Hughes-McLure and Mawdsley, 2022), also redefines the politics of expertise required to navigate – and even to challenge the situation. The politics of urban development, and the role of sustainability agendas, is a deeply political issue: how to tackle the existing large carbon footprint of buildings, how to minimize the emissions of future buildings and how to manage exposure to climate risk are deeply important for understanding the built environment’s relationship with wider climate change issues. When financialized systems enable a transfer of knowledge and the validation of financial understandings of a problem – in this case sustainability – the type of knowledge required by other actors in the built environment must correspondingly change. For those working to reshape how Swiss property and its market actors navigate the dual challenges of housing scarcity and affordability with ecological controversies, the defining of the problem as one that can be measured and addressed through financial mechanisms creates a politics of expertise where financial experts are best placed to solve it.

Conclusion

In this article, I use the issue of sustainability to critically reflect on the way in which new(er) forms of knowledge and expertise are translated into urban questions. This research shows that both consultants and data pressures are increasingly re-defining the problem of sustainability as one which can have a financial ‘fix’ or solution. In doing so, this work adds to the existing body of literature on how problem-definition work heavily influences the types of solution which can then be put to work (Li, 2007). Putting the idea of problem-definition into conversation with wider research on the urban politics of expertise (Robin and Acuto, 2022) reveals how the redefinition of sustainability – though undoubtedly contested and still defined in a traditional sense by other actors within real estate and urban decision-making circles – creates a cycle where financial knowledge becomes prioritized.

Future research is needed to understand the ways in which this type of knowledge is made legible. I take inspiration from Leins’ (2020) ethnography of investment actors in Switzerland and how they dealt with the ‘arrival’ of ESG as an expectation. What remains less understood in an urban context, but which was not the focus of this article, is how these new issues which ‘arrive’ in financial circles and come to re-shape the financial sector are then contested as they radiate to different sectors in a (at least partly) financialized world. As Robin and Acuto (2022) note in their introduction to a special issue on the urban politics of expertise, to understand the politics of expertise and how it is changing also requires thinking about how alternative modes or models of expertise can be developed and harnessed: what radical forms of knowledge are put to work as the politics of what is valued is redefined in urban decision-making, as is the case for sustainability? And importantly, what is our role as academics? We need to continue the agenda of unpacking the complexity of the private sector, seeking to understand the variegated ways in which different forms of capital or investment find their space within the wider web of financial logics unfolding property markets (Taşan-Kok, 2024) – and ensure that the types of knowledge(s) we are building can provide that critical understandings to challenge new forms of expertise.

Footnotes

Acknowledgements

I would like to thank the SURB group at GIUZ, University of Zurich for their inputs at our fantastic retreat and our ‘thinking coffees’, including the advice on responding to reviewers, and the Responsible City team across Switzerland. In particular to Hanna Hilbrandt for her always well-considered comments on an earlier draft and Michelle Schaffer for their essential background research throughout this project. I look forward to many projects together. I would also like to acknowledge Sarah Hughes-McLure’s ongoing brainstorming on ESG and all things urban with me.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship and/or publication of this article: The funding for this project was provided by the Swiss National Science Foundation grant no. 219821.

Ethical approval and informed consent

Ethical approval was approved by the Department for Philosophy, University of Zurich (2024). Informed consent was collected from interview participants.

Data availability

Data for this project are not publicly available.