Abstract

Drawing from the awareness–motivation–capability (AMC) perspective, this article develops a theoretical model, linking the relationship between the entrepreneur and investors to the entrepreneur’s exit path from her venture. It is argued that the relationship between the entrepreneur and the investors can be construed as being co-opetitive in nature, that is, simultaneously involving collaboration to grow the venture and competition to obtain a larger equity stake in the venture and broader decision-making rights. The article contributes to the entrepreneurship literature by developing a co-opetition view of the entrepreneur–investor relationship, theoretically modelling different exit pathways, and linking them to success versus failure perceptions of the entrepreneur’s exit from her venture.

Entrepreneurial exit is ‘the process by which the founders of privately held firms leave the firm they helped to create; thereby removing themselves, in varying degree, from the primary ownership and decision-making structure of the firm’ (DeTienne, 2010, p. 203). When, how and why founder-managers 1 leave their ventures have lasting implications for their post-exit well-being and subsequent entrepreneurial actions, the survival and growth of the ventures they leave behind and the economy in aggregate (Brockner, Higgins, & Low, 2004; Collewaert, 2012; DeTienne, 2010; Ucbasaran, Westhead, Wright, & Flores, 2010; Wright, Robbie, & Ennew, 1997). Exit is a distinct domain of the entrepreneurial process (DeTienne & Chirico, 2013), receiving increasing scholarly interest (Wennberg & DeTienne, 2014). The literature has considered the characteristics of the entrepreneur (Boeker & Karichalil, 2002; DeTienne & Cardon, 2012; Ucbasaran, Lockett, Wright, & Westhead, 2003) and firm performance context (Wennberg, Wiklund, DeTienne, & Cardon, 2010) as key determinants of an exit event, largely overlooking the drivers of different exit pathways (DeTienne, McKelvie, & Chandler, 2015).

Despite growing scholarly interest, two central and interrelated conceptual gaps remain in the entrepreneurial exit literature. First, a more refined view of the entrepreneur’s exit is needed to decouple it from firm exit and conceptualise it as an outcome that is not invariably negative. Even though the entrepreneur’s exit (from her venture) and the firm’s exit (withdrawal from a product market, technology or country, or ultimate dissolution of the firm) are conceptually distinct and do not necessarily happen at the same time; they have often been examined as a singular exit event that is predominantly equated to failure (Sarkar, Echambadi, Agarwal, & Sen, 2006; Strotmann, 2007; Van Praag, 2003). Entrepreneurs can exit from their ventures due to personal circumstances such as divorce or retirement (Wennberg et al., 2010), succession in a family business (DeTienne, 2010) or opting in to paid employment (Van Praag, 2003). They can also leave their firms by cashing out, referred to as a harvest sale (Wennberg et al., 2010), and subsequently start a new venture or take over an existing one to pursue better business opportunities (Shane, 2000), also referred to as entrepreneurial recycling (Mason & Harrison, 2006). Such exits imply neither the founder’s exit from self-employment nor closure of the venture. Accordingly, ‘entrepreneurship research needs to move beyond the over-simplified notion of equating exit with failure if further progress is to be achieved’ (Wennberg & DeTienne, 2014, p. 10).

A second gap is that the literature has overlooked the subtleties that the entrepreneur’s disengagement process leading to an eventual exit entails, particularly as it pertains to perceptions of success versus failure of the exit event. An entrepreneur can leave her venture voluntarily or involuntarily, and the exit can be viewed as a positive or negative outcome (Collewaert, 2012), implying different combinations of exit pathways and corresponding success versus failure framings. While being ousted from a rapidly growing start-up is widely considered to be a negative outcome for a founder, harvest sale of a profitable business or planned succession in a family firm is typically viewed as a positive outcome (Wennberg, Wiklund, Hellerstedt, & Nordqvist, 2011). Positive versus negative framing of an exit matters because it impacts the growth of the venture that is left behind—particularly when the founder-CEO takes her social network away (Bamford, Bruton, & Hinson, 2006)—as well as the founder’s self-efficacy and her subsequent entrepreneurial endeavours (Hessels, Grilo, Thurik, & van der Zwan, 2011; Jenkins, Wiklund, & Brundin, 2014; Shepherd, 2003; Ucbasaran, Shepherd, Lockett, & Lyon, 2013).

These gaps collectively highlight a need to look into and contextualise the exit process that precedes the exit event, to understand how an entrepreneur leaves her venture, and how her exit is construed as a positive versus negative outcome. With few notable exceptions (e.g., DeTienne et al., 2015; Wennberg et al., 2010), entrepreneurs’ exit from their ventures has predominantly been conceptualised and studied as an event because the exit of the founder-CEO is a critical juncture for the venture (Wasserman, 2003) and, in part, due to the event-based terminology adopted in foundational papers such as departure (Bates, 2005) and exit (DeTienne, 2010). Thus, refined process models of exit that consider different facets and drivers of entrepreneurs’ disengagement from their ventures are needed to describe, explain and predict different exit pathways (DeTienne et al., 2015; Leroy, Manigart, Meuleman, & Collewaert, 2015; Moroz & Hindle, 2012).

This article aims to begin filling these gaps. To that end, it develops a conceptual model of an entrepreneur’s disengagement and exit from her venture by considering the characteristics, attitudes and discretionary power of the entrepreneur and investors (e.g., angel investors and venture capital firms), with regard to the entrepreneur’s exit. The relationship between the entrepreneur and investors is key to understand such outcomes as innovation and venture growth (Timmons & Bygrave, 1986; Timmons & Sapienza, 1992), entrepreneurs’ as well as angel investors’ exit intentions (Collewaert, 2012), and founder/CEO dismissal and succession (Bruton, Fried, & Hisrich, 1997; Wasserman, 2003, 2006). Different theoretical approaches have long been used in the literature to model the entrepreneur–investor relationship, ranging from agency theory and stewardship theory, to prisoner’s dilemma (Arthurs & Busenitz, 2003; Cable & Shane, 1997; Landström, 1992; Schulze, Lubatkin, Dino, & Buchholtz, 2001; Shepherd & Zacharakis, 2001; Tosi, Brownlee, Silva, & Katz, 2003; Van Osnabrugge, 2000; Zacharakis, Erikson, & George, 2010). However, a theoretical view that models the implications of both the cooperative nature of the entrepreneur–investor relationship and the inherent tension between them, regarding their respective equity stakes and control rights, has not yet emerged.

Drawing from the core premises of the Awareness–Motivation–Capability (AMC) perspective, this article theorises that an entrepreneurial motivation (the entrepreneur’s core motivation), exit intention (whether the entrepreneur has explicit exit plans vs. reactively exits from her venture) and discretion (the extent to which the entrepreneur controls her exit path) will determine the disengagement path to an eventual exit event. The article then links different exit pathways to perceptions of success of the entrepreneur’s exit via testable propositions, also considering the conditioning role of firm performance context in entrepreneurial ventures. As such, the article makes two key contributions to the rapidly growing entrepreneurial exit literature. First, it conceptually decouples entrepreneur’s exit from firm exit and contextualises it as a positive or negative outcome, conditioned by the disengagement pathway that leads to the exit event, thereby refining and enriching the construct. Second, it offers novel insights based on simultaneous consideration of the attitudes and decision-making powers of the entrepreneur and investors, relative to one another, regarding the entrepreneur’s exit. In doing so, the article contributes to the development of a refined and richer view of the disengagement process leading to an exit event and advances the exit literature beyond an event-based paradigm.

In the remainder of the article, first an overview of various conceptualisations of exit in the literature is provided. Then, the core arguments of the AMC perspective are revisited and a Motivation–Intention–Discretion (MID) model of the entrepreneurial disengagement process embedded in the co-opetitive relationship between the entrepreneur and investors is developed, along with testable propositions. The article concludes with a discussion of the implications of the proposed model for future research as well as its boundary conditions and limitations.

Theoretical Background

Conceptualisations of Exit in the Entrepreneurship Literature

Exit is conceptualised and studied commonly at two levels of analysis in literature: (a) at the individual level, marking the time at which the founder-manager leaves her venture and (b) at the firm level, denoting the venture’s ceasing to exist as a going concern (Dehlen, Zellweger, Kammerlander, & Halter, 2014; Leroy, Manigart, Meuleman, & Collewaert, 2015). This article is broadly concerned with the former. Both of these conceptualisations signify a transition point in time between two distinctive states: the entrepreneur’s being engaged with her venture versus having departed and the firm’s continuing to operate as a going concern versus having being discontinued.

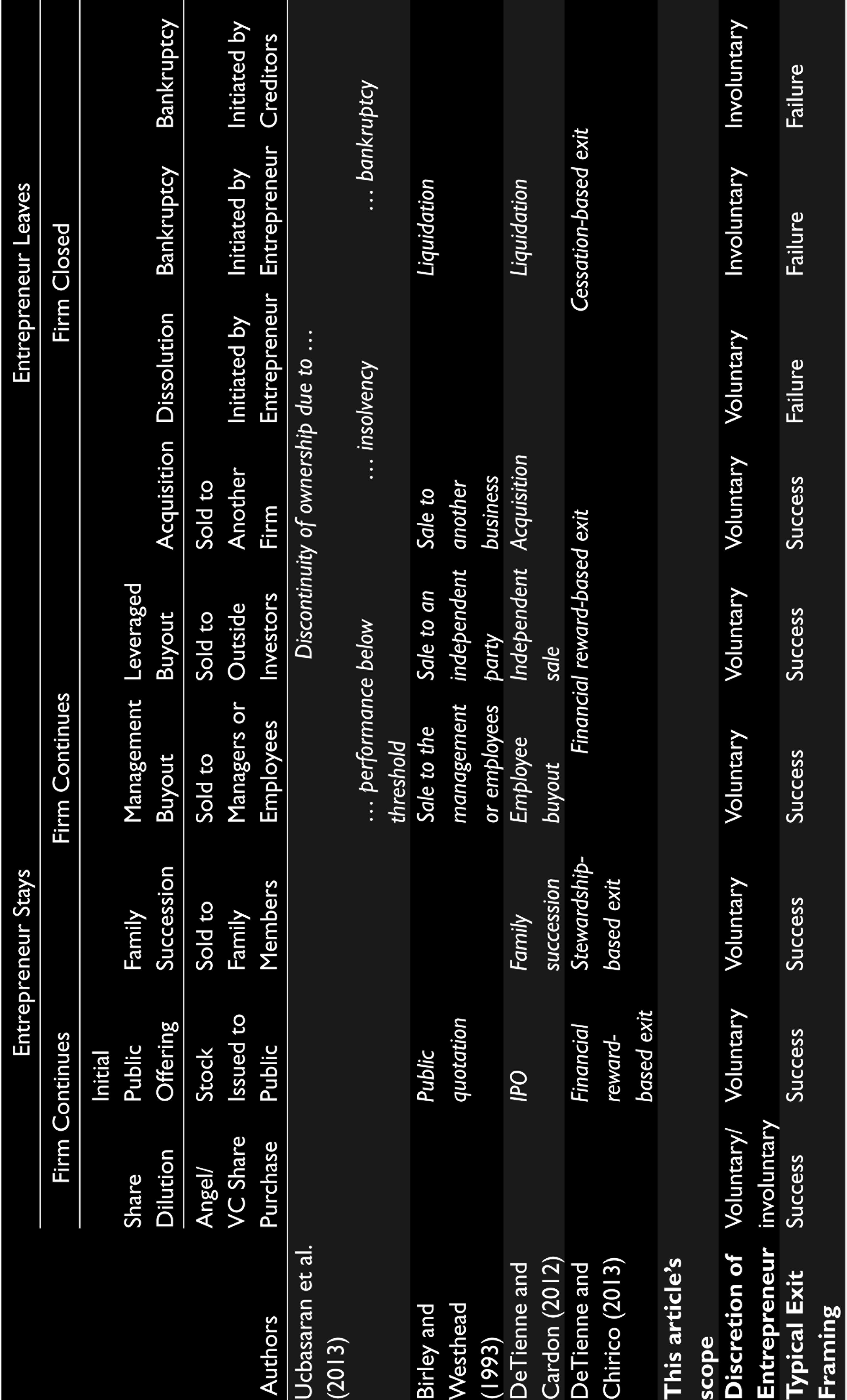

Even though some researchers have used the term exit to refer to a firm’s abandoning a market or industry (Bowman & Singh, 1993; O’Brien & Folta, 2009), economics and strategy scholars generally conceptualise exit as the closure of the firm as a going concern and study why and how new ventures cease to exist as privately held businesses through such means as acquisition/buyout, voluntary dissolution or bankruptcy (Hessels et al., 2011; Parker, 2000; Strotmann, 2007). This research stream is primarily concerned with determinants of firm closure (Doi, 1999; Fortune & Mitchell, 2012; Headd, 2003; Strotmann, 2007) and its impact on entrepreneurial activity on a regional or national scale (Mason & Harrison, 2006). Definitions of firm exit in this stream of research range in scope from broad (e.g., discontinuity of ownership) to specific (e.g., bankruptcy initiated by creditors) (Ucbasaran et al., 2013). For example, Gimeno, Folta, Cooper, and Woo (1997) do not differentiate between the reasons for and conditions surrounding the discontinuance event and use the term organisational discontinuance to denote the firm’s ceasing to exist either through being sold or otherwise discontinued. Among the few that differentiate between the reasons for exit are Balcaen and colleagues (2012), who examine a sample of firm exits in Belgium and find that about two in five exits are court induced (typically through bankruptcy proceedings), another two in five are due to voluntary dissolution and about one in five are acquisitions, including mergers and splits. They show that acquisition, voluntary liquidation and bankruptcy constitute fundamentally distinct exit routes for distressed firms and suggest that perceptions of firm failure (i.e., the severity of the failure) differ based on the exit pathway. With few exceptions like Headd (2003), who distinguishes between closure as an event and failure as a perception or attribution, firm-level conceptualisations of exit predominantly imply the firm’s and the entrepreneur’s failure as she goes out of business with her venture (Coad, 2014; Strotmann, 2007).

An entrepreneur’s exit from her firm can, but does not necessarily have to, overlap with the firm’s closure or dissolution (Cardon, Stevens, & Potter, 2011). An entrepreneur’s leaving her firm is primarily a personal decision with a significant impact on the entrepreneur’s emotions, well-being, and welfare, as well as her future entrepreneurial undertakings. The micro view of exit thus focuses on individual-level determinants and outcomes of the entrepreneur’s decision to exit her venture and, at times, also leaving self-employment (Brigham, De Castro, & Shepherd, 2007; Khan, Tang, & Joshi, 2014; Lin, Picot, & Compton, 2000; Stam, Thurik, & Van der Zwan, 2010). Major research themes in this stream deal with causal attributions of failure, learning from failure and coping mechanisms that entrepreneurs use to overcome the negative emotions like grief associated with exit (Cardon et al., 2011; Cope, 2011; Jenkins et al., 2014; Shepherd, 2003; Singh, Corner, & Pavlovich, 2007; Shepherd & Hayni, 2011; Ucbasaran et al., 2013; Ucbasaran et al., 2010).

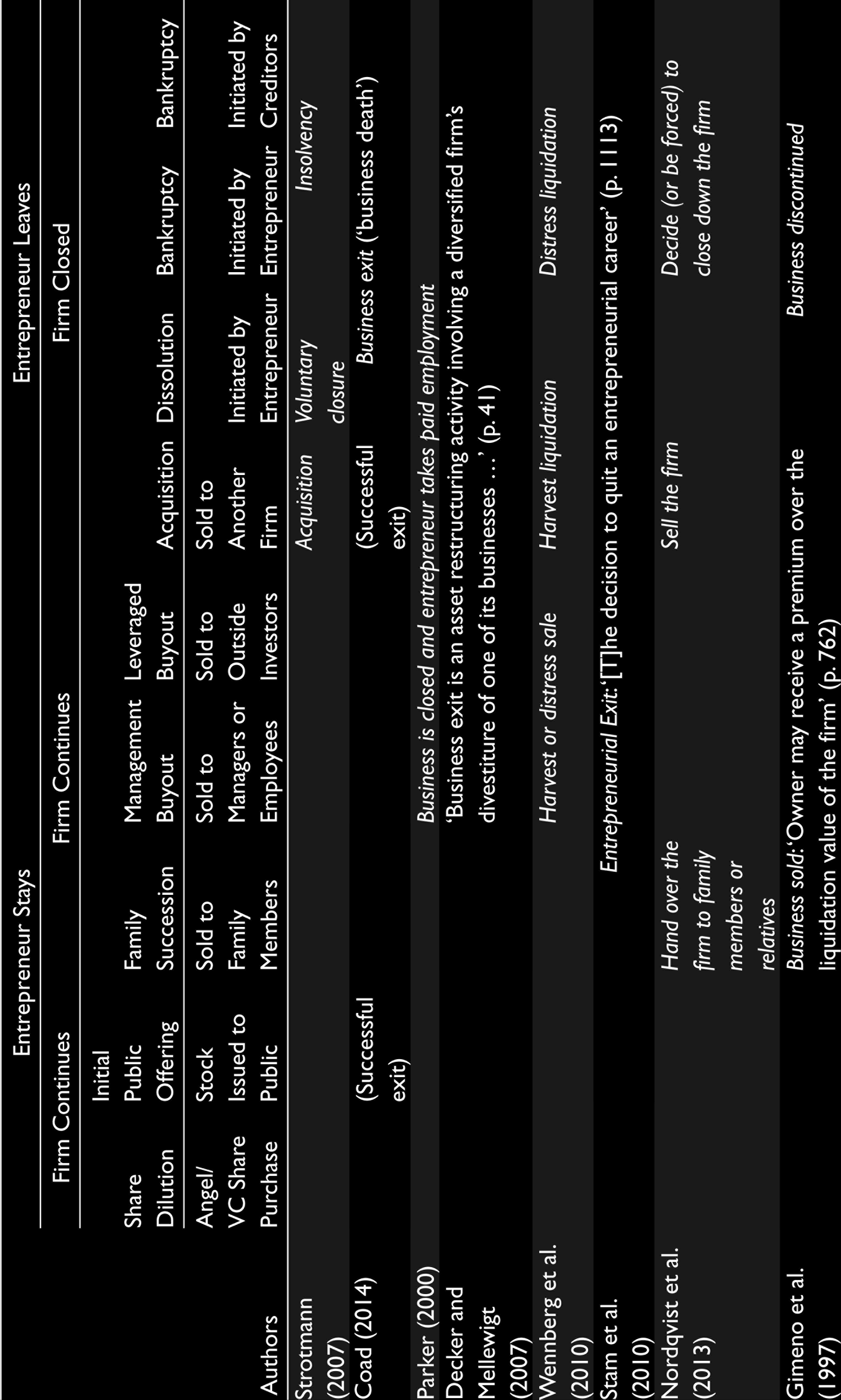

Research that has examined the subtleties of exit strategies has identified different routes for entrepreneur’s exit such as family internal succession, initial public offering (IPO), acquisition by third parties (which can be employees, outside investors, or an acquiring firm such as a supplier or a competitor), or liquidation (Dehlen, Zellweger, Kammerlander, & Halter, 2014; DeTienne & Cardon, 2012). DeTienne and colleagues (2015) synthesise these exit pathways in a typology of three higher-order exit strategies such as financial harvest, stewardship and voluntary cessation. Although these individual exit routes are conditioned to a certain extent by firm exits, or closures, researchers assert that entrepreneurs may exit their firms for reasons other than business failure, including business success (e.g., Ucbasaran et al., 2013). Our current understanding of entrepreneurs’ exit from their ventures thus includes voluntary exits of entrepreneurs through such means as a harvest sale (entrepreneur leaves, firm continues under new ownership) and harvest liquidation (entrepreneur leaves, firm is liquidated), both of which can happen in profitable firms (Wennberg et al., 2010), as well as unprofitable ones. To provide a more encompassing view of the diversity of exit conceptualisations, Table 1 summarises major studies examining exit at individual and firm levels of analysis and the few studies differentiating between positive and negative outcomes.

Conceptual Scoping of the Exit Construct in Literature

The preceding literature review and summary table suggest that most studies on exit have focused on the discontinuation of the firm through such means as acquisition or bankruptcy (voluntary or induced), which often, but not always happens concurrently with the exit of the entrepreneur. Even though this is not the only way entrepreneurs leave their ventures, this convenient overlap appears to have led to a methodological as well as conceptual agglomeration in this research stream (DeTienne et al., 2015; Wennberg & DeTienne, 2014). Detailed data on an entrepreneur’s exit—distinct from firm closure—are scarce. Contrastingly, abundant archival data on firm closures appear to have had a strong influence on how exit has been operationalised and studied empirically in literature. The few empirical studies that used primary data were not able to dissect the nature of divergent exit pathways either. Using Global Entrepreneurship Monitor (GEM), for example, researchers used only one dichotomous (yes/no) survey question to capture an entrepreneur’s exit experience in the preceding 12 months if the entrepreneur had sold, shut down, discontinued or quit their business (Autio, Pathak, & Wennberg, 2010). One study which used primary data to dissect the reasons for exit (Justo, DeTienne, & Sieger, 2015) found that about 5 in 10 Spanish women entrepreneurs who were sampled exited their ventures due to business failure, 3 in 10 exited due to personal reasons such as retirement, and 2 in 10 chose to exit to pursue better opportunities.

Another critical yet under-examined aspect of the exit process is the relationship between entrepreneurs and investors. The influence of investors on managerial discretion and various strategic outcomes has been well documented in the literature (Dalton, Daily, Certo, & Roengpitya, 2003; Elango, Fried, Hisrich, & Polonchek, 1995; Fried, Bruton, & Hisrich, 1998). For example, board and voting rights can provide investors with the right to dismiss the top management team (Parhankangas & Landström, 2006) or a veto right to replace the CEO (Cumming, 2008), which can strongly influence exit pathways of entrepreneurs. The nature of the entrepreneur–investor relationships, and how it can change over time, has also been elaborated in different literatures (Bruton, Chahine, & Filatotchev, 2009; Cable & Shane, 1997). More recently, the conflict between entrepreneurs and investors has been examined in the context of trust and cooperation between the entrepreneur and investors (Bammens & Collewaert, 2014; Zacharakis et al., 2010), as well as with regard to the entrepreneurs’ and investors’ intentions to exit from the venture (Collewaert, 2012). However, implications of the relationship between the entrepreneurs and investors have not been considered in modelling the entrepreneur’s exit pathway.

The Awareness–Motivation–Capability Perspective

Building on the arguments of organisational change, learning and decisionmaking literatures, the Awareness–Motivation–Capability (AMC) perspective (Chen, 1996; Miller & Chen, 1994) is formulated as a determinant of competitive tension, defined as ‘the strain between a focal firm and a given rival that is likely to result in the firm taking action against the rival’ (Chen, Su, & Tsai, 2007, p. 102). The AMC framework helps clarify when, why and how firms respond to competitive attacks from their rivals. According to this framework, the competitive actions that a focal firm might take are determined by three factors: (a) whether the firm is aware of the competitive attacks directed towards itself; (b) whether the firm is motivated to respond and ‘defend its turf’; and (c) whether the firm commands the necessary resources and capabilities to respond. If the focal firm is not aware of the rival’s actions, or does not identify a certain action as a competitive attack, a competitive response is unlikely. Even if the action is detected and identified as a competitive attack, the focal firm may still not be motivated to respond, for example, when the market space at stake is not of strategic importance to the focal firm and can thus be abandoned to the rival. If the focal firm detects the attack and is motivated to respond, the likelihood and effectiveness of a response are determined by the extent to which the focal firm possesses the requisite capabilities.

The AMC perspective is a surprisingly suitable theoretical lens to examine entrepreneurs’ exit from their ventures. The core premise of the AMC framework is that a focal firm needs to possess an awareness of the interactions between two parties and the implications of their actions, a motivation to respond and the capability of doing so. In a new venture, investors are akin to large block holding activist investors in public firms who act as principals and need to monitor their agents (managers/entrepreneurs) to protect themselves against opportunistic behaviour (Arthurs & Busenitz, 2003; Jensen & Meckling, 1976). Not surprisingly, it is often the investors who are responsible for the replacement of the CEO (Bruton et al., 1997; Gorman & Sahlman, 1989). On the other hand, the founder-manager adopts a dual principal/agent role in which she is not only responsible to herself as a principal (owner), but also to the investors as their agent (manager) who runs the venture on a daily basis. Thus, the entrepreneur and investor cooperate to create value (i.e., to successfully grow the firm) while they also compete for power for broader control rights and obtain a larger equity stake in the firm.

In this respect, this relationship between the entrepreneur and the investors is akin to co-opetition, which is referred to as an ongoing process of actions and reactions between two opposing parties, whereby a focal firm or business unit can achieve success by engaging in competitive action with another one while also partnering with the same party to overcome technological and market challenges (Gnyawali & Park, 2009). Simultaneous competition and cooperation can take place between competing firms in the market (Gnyawali, He, & Madhavan, 2006) or within firms, for example, across organisational units with different goals and priorities (Tsai, 2002). In the context of an entrepreneur’s disengagement and eventual exit from her venture, the focal party is the entrepreneur and the second party is the investors of the venture. Even though the two parties’ interests are in alignment, particularly during the early stages of the venture, the strategic direction that the founder/manager and the investors prefer might differ as the venture grows, causing tension between them (Collewaert, 2012) and possibly causing drastic change in the leadership (Wong, 2017; Gelles, de la Merced, Eavis, & Sorkin, 2019).

Entrepreneurs start their journeys with various motives such as pursuing independence, self-realisation, achieving personal financial success or creating innovation (Carter, Gartner, Shaver, & Gatewood, 2003; Douglas & Shepherd, 2002; Hessels, Van Gelderen, & Thurik, 2008). The entrepreneurial intentions literature broadly categorises entrepreneurs based on their cognitive styles (Brigham et al., 2007), growth aspirations (Carland, Hoy, Boulton, & Carland, 1984; Gundry & Welsch, 2001; Dutta & Thornhill, 2008; Douglas, 2013) or planning formality (Lyles, Baird, Burdeane Orris, & Kuratko, 1993; Berry, 1998; Brinckmann, Grichnik, & Kapsa, 2010). Some entrepreneurs prioritise rapid growth of the venture and plan formally to grow and/or expand the business, while also utilising broader types of funding (Gundry & Welsch, 2001). Others might prioritise their lifestyle as an autonomous business owner and prefer not to be beholden to the whims of outside investors.

Various terms have been used in the literature to differentiate growth-oriented and lifestyle-oriented entrepreneurs who often have divergent goals. Carland and colleagues (1984) refer to the former (i.e., outcome- or growth-oriented founders) as ‘entrepreneurs’ and the latter (i.e., process- or lifestyle-oriented founders) as ‘small business owners’. Dutta and Thornhill (2008) use the term ‘analytic’ to denote the former and ‘holistic’ for the latter. Douglas (2013) categorises the former as entrepreneurs with growth-intentions versus the latter as entrepreneurs with independence-intentions. Even though the specific nomenclature may differ, there appears to be a consensus in literature in broadly classifying entrepreneurs who are performance oriented (i.e., those who intend to grow their venture and seek financial gain) versus those who are lifestyle oriented (i.e., those who view the venture as a means to achieve autonomy and self-actualisation).

It is thus plausible that entrepreneurs exhibit a similar variance in the reasons for and the possible ways in which they would prefer to exit their ventures, particularly given their differing performance versus lifestyle motivations. Some entrepreneurs may exit from their ventures through deliberately planned exit pathways, as opposed to doing so haphazardly and in a reactionary manner. Further, regardless of their intent, they may be capable of controlling their exit versus reacting to circumstances such as being ousted by shareholders or through involuntary bankruptcy proceedings. The extension of the AMC framework to the entrepreneurial exit domain serves as a useful theoretical lens that can clarify the factors and conditions that shape an entrepreneur’s exit from her venture as positive or negative. Below, a graphical representation of the proposed conceptual model is provided, and an MID model of exit is developed by drawing arguments from the three core elements of the AMC perspective.

A Motivation–Intent–Discretion Model of Exit

Entrepreneurs’ motivation in embarking upon their entrepreneurial journey conditions their view of and openness to an eventual exit event as a positive or negative outcome. Prior entrepreneurial experience of entrepreneurs is shown to impact their ex-ante preference for exit events such that entrepreneurs with more experience prefer an exit through IPO or acquisition, rather than through independent sale or liquidation (DeTienne & Cardon, 2012). This is, in part, due to their focus on the growth and performance of the venture, as they have ‘a desire to make money and build their own financial wealth’ (Fauchart & Gruber, 2011, p. 941) through the success of the venture. Thus, entrepreneurs with performance motivation can view certain exit pathways that entail large financial payouts as positive and desirable outcomes (DeTienne et al., 2013). On the other hand, lifestyle entrepreneurs, who are more invested in their ventures emotionally, might not be as open to the idea of exiting their ventures by choice. Lifestyle entrepreneurs, who start an entrepreneurial career primarily due to the associated lifestyle implications like identification with a specific profession, market, technology or autonomy, are more attached to their ventures. As such, these entrepreneurs engage with their ventures with relatively weaker importance placed on performance, growth and financial return than profit-motivated entrepreneurs (Zellweger & Astrachan, 2008). In this respect, the entrepreneurial motivation of the entrepreneur serves as a conditioning factor as to whether the entrepreneur might view exiting the venture, in advance, as a possibly positive and desirable outcome, instead of framing any kind of exit as a failure to be avoided. Thus:

The AMC perspective posits that the actor is the focal element in competitive dynamics literature as the originator of actions (Smith, Ferrier, & Ndofor, 2006). The secondary factor, following the arguments of the AMC perspective, is intentions of the entrepreneur, which refers to the exit intentions regarding a particular, that is, foreseeable and/or imminent exit prospect. This is different from being open to the generic idea of exit as a possibly non-negative outcome, in that exit intention is focused on the prospect of a specific exit event. As such, it is not dispositional, but attitudinal. Entrepreneurs can entirely disengage from their ventures, which is defined as ‘seizure of all activities geared toward the goal of firm creation’ (Khan et al., 2014, p. 39) even during nascent stages, that is, before the venture is formally launched. An entrepreneur can be open to the idea of exit as a non-negative outcome in general, but she can still have a negative view of the prospect of a specific exit prospect. In this regard, entrepreneurial motivation can be considered as a long-term (e.g., strategic or trait-like) characteristic of the entrepreneur, whereas exit intention refers to a short-term (e.g., tactical or state-like) characteristic.

Entrepreneurs can have positive or negative attitudes towards an exit prospect for various reasons. For example, an entrepreneur may have a higher valuation of her venture than what is offered by a potential buyer; she may view specific stipulations regarding voting rights to be unfavourable with respect to her pay-off; or she might be simply expecting a substantial increase in firm performance or growth prospects in the near future, which can boost the valuation in a subsequent exit opportunity. Even under a positive performance framing, the prospect of an imminent milestone in the growth trajectory of the venture, for example, a new equity funding round or an imminent IPO, might cue the entrepreneur not to desire to leave her venture just yet, even though she might have an exit plan.

In the case of a lifestyle entrepreneur, awareness of exit as a potentially positive outcome is expected to be low, and thus, her attitude towards a specific exit prospect is expected to be negative under normal circumstances. Two exceptions to normal circumstances are: (a) a life event such as ailment, old age (retirement) or family contingencies such as a loss in the family or relocation and (b) when the business is on the brink of bankruptcy and waiting a little longer can decrease the salvage value of the business—both of which can force the entrepreneur to exit the business prematurely. Neither of these cases is desirable for the entrepreneur; however, the prospect of a timely exit that can prevent further losses and salvaging more from the business (in terms of financial and physical assets, business connections, reputation) might be deemed to be a compulsory course of action. In other words, the prospect of an imminent exit can be preferred when compared to a worse outcome in the near future, thus conditioning the entrepreneur’s attitude to her exit ‘at this time’ to be positive. Stated formally:

The last component of the MID model is the discretion of the entrepreneur, which refers to the extent to which the entrepreneur can determine the exit pathway. Entrepreneurs typically decide how to run their businesses themselves. However, angel investors and venture capital firms influence executive decision-making significantly. The business experience and connections of seasoned investors serve as additional value-added inputs that they bring to the venture they invest in. However, investors’ role as important shareholders can also create additional tension with respect to strategic decision-making in the firm. As external investors get more involved in decision-making for the firm over time, the entrepreneur’s freedom in decision-making becomes more limited. In addition, the entrepreneur and the investors may have different goals regarding the future of the venture. Most angel investors and venture capital firms are primarily for-profit investors, who expect large investment return multipliers in exchange for the high risk that they have taken by investing in an unlisted entrepreneurial venture with minimal to no collateral (Mason & Harrison, 1996). While they may share this trait with some entrepreneurs, not all entrepreneurs are entirely performance motivated. Further, entrepreneurial motivation and aspirations can also change during the lifetime of the venture. A performance motivated entrepreneur can eventually develop new aspirations, and the primary motivation for her engagement with her venture may change (e.g., towards more positive social or environmental impact, a focus on sustainability, fair trade practices, or giving back to their community). When investors disagree with the entrepreneur regarding the future strategic direction to be taken, tensions can mount to such an extent that the entrepreneur can be forced to leave, or being ousted from her venture. Given that executives are less likely to be ousted from their firms when they retain a greater share of ownership (Boeker & Karichalil, 2002; Fredrickson et al., 1988), whether the entrepreneur can be forced to exit is determined by the relative power of the entrepreneur and the investors. This, in turn, is primarily determined by the evolving shareholding and/or decision-making rights that investors accumulate over time, in relation to the entrepreneur’s voting rights as the entrepreneur’s equity is typically diluted in successive fundraising rounds. Thus:

Perceptions of Success Versus Failure

The conditions under which the entrepreneur exits, based on the MID model proposed above, would impact perceptions of success of the entrepreneur’s exit. Combining the arguments above, the entrepreneur’s motivation in becoming an entrepreneur, her attitude towards a certain exit prospect, and whether she chose or was forced to exit the venture collectively determine the exit pathway and subsequent success perceptions of the exit event. Ideally, a performance-motivated entrepreneur would take advantage of favourable circumstances to exit through a harvest exit by determining when and how she would exit the venture. This can happen through closure of the firm, for example, through acquisition by another firm to eliminate competition or redeploy the assets of the closed venture. It can also happen when the firm continues its existence but the entrepreneur cashes out, thereby achieving her financial return goal with a success framing. Even if the entrepreneur did not have a profit-motive, such a harvest sale of the business can still be considered a success, as it can provide new resources and an opportunity for a fresh start. Thus, entrepreneur’s intention to exit and discretion can shape the success framing of the exit event.

Another factor that conditions the exit pathway of an entrepreneur is firm performance. As stated in a review, ‘A variety of factors, such as human capital, prior entrepreneurship experience, and the overarching objectives of a firm combined with general environmental conditions (munificence, volatility, etc.) influence perceptions of firm performance and future potential, as well as the decision to continue, discontinue, or sell the firm’ (Shepherd, Williams, & Patzelt, 2015, p. 27). Firm growth and performance context can determine if and when an entrepreneur might desire to exit her venture, and if so along which dimensions—ownership and/or management. New ventures that grow slower than expectations are considered to exhibit low performance, which can be attributed to financial constraints (Pissarides, 1999) or a lack of requisite skill set to manage the firm (Boeker & Karichalil, 2002). If low performance is attributed to financial constraints, the firm (and thus the entrepreneur) might seek external funding that would likely decrease the equity stake of the entrepreneur through dilution, while the entrepreneur would continue to manage the venture, manifesting in a diminishment of her equity stake but not managerial decision-making. If, however, low performance is attributed to a lack of managerial capabilities, investors would try to oust the entrepreneur from the venture or at least replace her with a ‘better’ manager while the entrepreneur keeps her equity stake in the firm.

On the other hand, high growth, which is typically associated with high performance for new ventures might also call for a founder’s replacement with professional managers having a different set of skills that might be more geared towards maintaining the momentum of the firm (Wasserman, 2003). In this case, the founder’s replacement with professional managers happens with a positive performance framing and in anticipation of improvements associated with the growth of the venture. This, in turn, might lead to a founder’s exit from managerial decision-making role but would likely reinforce her motivation to maintain an equity stake in the venture to capitalise on the future success of the firm (Bussenitz, 2019).

In sum, entrepreneurs can exit their ventures in low- and high-performance contexts along ownership and/or management dimensions, under different success (positive) versus failure (negative) connotations. A high-performing (rapidly growing) venture creates conditions for both the entrepreneur and the investors to continue their collaborative stances to accelerate the growth of the business, whereas a low-performing (slowly growing or declining) venture might entice the investors to seek to improve the management of the firm through voluntary or forced founder replacement. Thus, all else being equal, exiting a high-performing firm would likely be perceived as a failure for the entrepreneur. In contrast, an entrepreneur’s exiting a low-performing firm (e.g., before the firm goes bankrupt) should be perceived as a success, since losses would be curbed and the entrepreneur would be able to recover sooner. Stated formally:

Discussion

Most new ventures fail within the first few years of their inception and most of the survivors fail to live up to the expectations of their founders (Cassar, 2014). Founders of firms that are liquidated for any reason, by definition, have exited their venture. However, not all exits of entrepreneurs can be seen as failures. Many founders leave their successful ventures for good reasons such as emergence of better opportunities, desire to harvest their investment or life events such as retirement (DeTienne, 2010). Thus, exit is not always forced upon, but sometimes deliberately chosen by the entrepreneur (Gimeno et al., 1997). Entrepreneur’s exit thus needs to be distinguished from the firm’s closure to refine our understanding of the drivers and outcomes of the entrepreneurs’ parting ways with their ventures. The complex and dynamic nature of the entrepreneur–investor relationship creates an entanglement of the ownership and management dimensions of the entrepreneur’s engagement with her firm. Ownership and management, the two defining but separate dimensions of a founder-manager’s engagement with her firm, have received scant attention with respect to their simultaneous but distinct relevance to the entrepreneur’s disengagement from her venture (Robbie & Wright, 1995). In this context, several research questions are of interest not only for scholars, but also for practitioners (i.e., entrepreneurs) with regard to their ability to exit and their view of the success of an exit event (Wennberg & DeTienne, 2014).

Implications for Research

Different exit paths have important implications for research on entrepreneurial phenomena at various levels of analysis. For example, DeTienne and Chirico (2013) proposed that higher socio-emotional wealth and lower performance thresholds might lead families to exit from their businesses via stewardship-based, as opposed to cessation-based, exit paths. The choice of exit paths and the conditioning factors that might change the framework around exit decisions and pathways can have implications for valuation of firms as well as impacting the subsequent ownership structure and the strategic direction that might be chosen for the firm after the exit of the founding individual or family. Mueller, Volery, and Von Siemens (2012) find that entrepreneurs’ locus of attention, as measured by the amount of time they spend on various functions, shifts from the environment to the interior of their ventures as their ventures grow. In particular, entrepreneurs spend significantly more time on environmental scanning during the start-up phase, but their attention during the subsequent growth stage is directed inward, that is, more towards developing their organisation and business. These findings suggest that novice entrepreneurs might have different attitudes towards exit in comparison to serial or portfolio entrepreneurs. As such, the nature of the exit process as well as the timing of an eventual exit event can provide important signals to investors, employees and other stakeholders regarding the characteristics of the entrepreneur and the firm. For example, a serial entrepreneur who starts a new venture with the explicit goal of exiting from the new venture within a short time frame, for example, contingent upon meeting some growth and/or performance milestones/metrics to obtain a high acquisition or IPO premium, might attract certain kinds of employees and investors that might be different than those who would be attracted by a novice entrepreneur who commits to growing the firm with a longer strategic and temporal horizon as well as personal commitment to stay for longer.

In line with some scholars’ assertions that a planned exit strategy facilitates the process of a successful exit (Headd, 2003), entrepreneurs are increasingly planning their exit strategies at the onset of their ventures. However, our understanding of whether, and if so, how having an exit plan leads to a successful exit is limited. There are several interesting research questions in this vein. For example, do these entrepreneurs plan their exit as specific pathways or do they simply expect to have exited their venture by a specific future date or upon arriving at a milestone in the life of the venture? What are the individual-, firm-, and industry-level factors that impact an entrepreneur’s exit pathway choice? For example: Is exit planning affected by the entrepreneurial motivation (e.g., lifestyle vs. profit) and/or industry characteristics such as complexity, dynamism and munificence—particularly with respect to existence of a vibrant equity market, as well as frequent IPO events? The drivers, conditioning factors and outcomes of exit planning, for the entrepreneur and the venture, offer a promising avenue for future research.

Future research can address a number of other interesting research questions regarding exit and its implications for the entrepreneur and the firm, for example, whether, and if so, under what circumstances the entrepreneur’s exit changes the nature of the new venture qualitatively into an established or ‘mature’ firm. Stated differently, what makes a firm new and when is a venture considered to be established? Given that founders’ identity is shown to influence the subsequent organisational behaviour and performance of new ventures, going beyond the initial stages of the venture (Haveman & Khaire, 2004), it would be interesting to examine whether the founding entrepreneur’s passion helps or hinders the transformation of the venture into a mature organisation with its own personality. The successful (e.g., planned and desired) exit of the entrepreneur after the initial growth of a start-up can be a turning point in the life cycle of the firm, signifying a rite of passage into maturity as an organisation. Accordingly, how an exit event is perceived by the third parties in the broader marketplace, vis-à-vis the entrepreneur’s discretion or choice versus being coerced to exit, becomes more important. Conversely, a prolonged detachment process that does not result in the entrepreneur’s completely leaving the new venture, at least in the equity dimension, can be a signal to the market that a rapidly growing high-tech business, for example, has still not fully achieved its value potential in the capital markets.

Different types of entrepreneurs might respond to an unsuccessful exit differently. For example, serial and portfolio entrepreneurs might respond to their exit differently than novice entrepreneurs because the former two groups have multiple reference points in their respective past and (con)current entrepreneurial experiences (Westhead, Ucbasaran, & Wright, 2005). Novice entrepreneurs, however, might hold on to their ailing ventures longer than is rational, leading to larger economic and cognitive losses. Future research can examine the types of entrepreneurial motivation (e.g., performance- vs. lifestyle-oriented) to provide insights regarding when and under what circumstances perceptions of the entrepreneur differ from those of other stakeholders such as investors and the market at large.

Another avenue that future research can examine is the implications of entrepreneurial exit from the perspective of different constituents. Open source development and crowdsourcing, for example, are two prominent mechanisms in which large numbers of dispersed stakeholders contribute to the development and launch of new products and/or ventures. Examining the involvement and voice of such broad constituencies in making decisions regarding the future of a new venture might lead to interesting findings. For example, the recent acquisition of Oculus, a virtual reality systems company, by Facebook led to an outcry by numerous crowdfunding backers who backed the company financially via Kickstarter in the early stages of the lifecycle of the firm as well as a broader group of enthusiasts who had been following the venture’s development from the nascent stage. 2 These constituents did not appreciate Facebook’s acquisition of Oculus despite Facebook’s assertion that Oculus would be run as an autonomous entity within the expanding Facebook ecosystem of firms, platforms and products. While this can be termed as a successful partial exit for Oculus’ founding team along the equity dimension (they retained their managerial roles), early crowdfunding backers considered this as a negative outcome for the firm. Although non-equity crowdfunding backers have no legal say in the strategic direction that the firm will take, they constitute a critical early adopter community and they have been involved with the venture, both financially and technically, from its very inception. Alienating such a key stakeholder group might be costly for such firms that aim to capitalise on the idiosyncratic relationship with their respective customer bases. Thus, the determinants of entrepreneurs’ exit choices offer fertile ground to test the applicability of various theories on perception, attachment, ownership and control regarding firm-user relationships.

Limitations

One important limitation of the proposed model is that it considers the exit of individual entrepreneurs from their firms. Upper echelons view has examined top management team characteristics (Hambrick, 2007; Hambrick & Mason, 1984) and entrepreneurship scholars have examined the impact of Top Management Team (TMT) characteristics on entrepreneurial founder team member entry and exit (Guenther, Oertel, & Walgenbach, 2016; Ucbasaran et al., 2003). In firms that have founding teams, conflict or cohesion among the founding team members (Ensley, Pearson, & Amason, 2002) can lead to different levels of disengagement of the founding team members from their venture. Disengagement and eventual exit of individual TMT members can have different effects on perceptions of success of the firm after some, but not all, founding TMT members exit. Thus, a key limitation of the proposed model is that it applies to founders-managers, not founding teams, receiving investment from outside investors.

Another limitation is that the investors are assumed to have the same preferences for the entrepreneur to leave the firm or stay. Thus, the model does not consider what happens when investors differ, among them, in their preference regarding the entrepreneur’s exit. Investors with different goals and investment horizons might vary in their preferences for various strategic outcomes, the entrepreneur’s exit being an important one. However, the implications of this kind of conflict are beyond the scope of this article and can be examined in future research.

Conclusion

In closing, this article echoes Wennberg and DeTienne’s call: ‘[E]ntrepreneurship research needs to move beyond the over-simplified notion of equating exit with failure if further progress is to be achieved.’ (Wennberg and DeTienne, 2014, p. 10). Attitudes towards and planning for exit impact future decisions and behaviours of entrepreneurs, thus providing critical information pertaining to the entrepreneurial process and new venture growth trajectories (DeTienne et al., 2015). Several scholars stated that a refined understanding of the entrepreneurial process requires a better understanding of the predisposition and cognition of the individual entrepreneur (Brigham et al., 2007). Thus, refined process models of entrepreneurs’ journeys through their ventures need to be developed, as well as the journeys of the ventures themselves, starting with opportunity recognition during the nascent stages of the venture to the entrepreneur’s exit. It is hoped that this article would contribute to the development of a more refined and richer view of entrepreneurs’ exit from their ventures.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.