Abstract

We analyse the effect of innovation on technical progress in Spanish manufacturing firms by identifying and explaining how the following innovation factors affect technical progress: research and development (R&D) activities and expenditures, patents, innovations in products and in processes, internal organisation of innovation, outsourcing R&D activities, public R&D funding, external relationships of innovation and different ways of external collaboration for innovation. We focus on how firm behaviour and structure drive these innovation factors. Our results are based on multiple regression analyses using firm-level data from 2010. We show that innovations in product, processes and R&D activities (especially external R&D activities) are more likely to improve the productivity of Spanish manufacturing firms. In addition, the activities related to the internal organisation or the external collaboration for innovation generates a higher productivity level. This positive effect is bigger when a firm collaborates with universities and/or technology centres and employs recent college graduates, especially those with degrees in science, engineering or technology.

Introduction

The article is structured as follows: first, we analyse productivity factors and propose a hypothesis for each one; second, we explain the model, data and methodology; third, we analyse and discuss the results; finally, we conclude.

Innovation Factors Determining the Productivity

Previous literature studies innovation’s effect in firms on their productivity. Some papers study only one innovation factor; for example, Beneito (2001), Doraszelski and Jaumandreu (2007), Fluviá (1990), Grandón and Rodríguez Romero (1991) and López Pueyo and Sanaú Villarroya (1998) use a production function to analyse how R&D capital affects production. Beneito (2001) considers the use of advanced technologies, Doraszelski and Jaumandreu (2007) the R&D process, Fluviá (1990) the R&D investment, Grandón and Rodríguez Romero (1991) the technology imports and López Pueyo and Sanaú Villarroya (1998) the public funding for R&D.

Other papers study the simultaneous effects of various factors on productivity, as we do in this work. Crèpon, Duguet and Mairesse (1998), for instance, analyse the number of patents and R&D expenditures; Gu and Tang (2003) analyse R&D investment, patents, machinery investment and internal organisation; Rosell-Martínez and Sánchez-Sellero (2012) study the effects of foreign direct investment (FDI) and R&D expenditures; and Sánchez-Sellero, Rosell-Martínez and García-Vazquez (2014) analyse how innovation drives Spanish manufacturing companies’ ability to absorb spillovers from foreign direct investment. They find the following results: Crèpon et al. (1998) maintain that firm productivity correlates positively with a higher number of patents and R&D expenditures. Gu and Tang (2003) hold that there is a strong and positive relationship between innovation and productivity using their mentioned measures of innovation. Rosell-Martínez and Sánchez-Sellero (2012) conclude that capital-intensive and R&D-intensive sectors offer the most convenient conditions for innovation to generate technical progress. Sánchez-Sellero et al. (2014) find that R&D activities boost the generation of new knowledge and absorptive capacity from FDI.

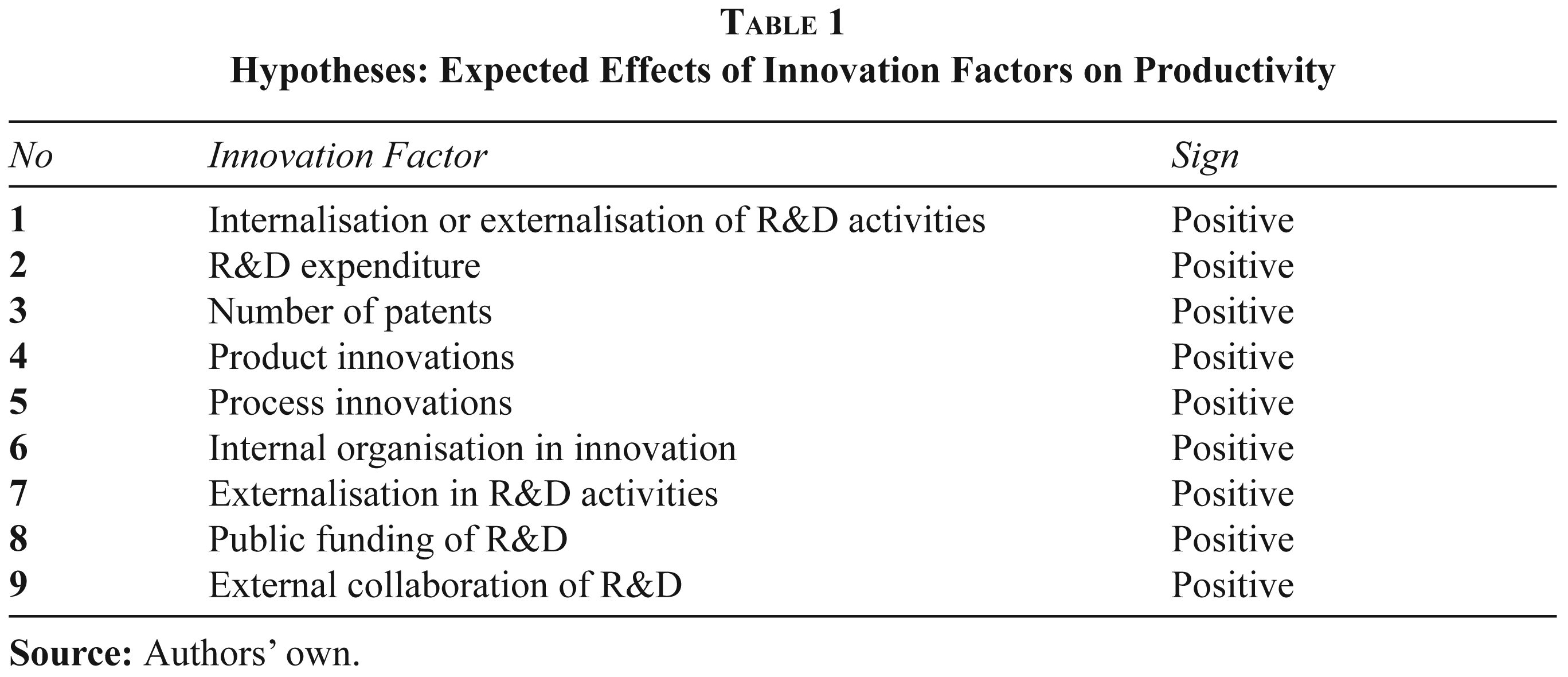

We conduct a more ambitious and complete analysis of the innovation determinants of productivity by updating and extending the innovation determinants of productivity to R&D activities and expenditures, patents, innovations in products and in processes, internal organisation of innovation, outsourcing R&D activities, public R&D funding and external relationships of innovation. We carry out these analyses at the firm level. We propose and test the hypothesis on the light of the literature as given in Table 1.

Hypotheses: Expected Effects of Innovation Factors on Productivity

R&D Activities

Many studies prove that R&D activities affect productivity improvement. Griliches (1979), for example, proposes a model of R&D capital stock to analyse how R&D investment affects innovations and increases productivity. Also, Griffith, Redding and Van Reenen (2004) show how R&D activities affect productivity growth in a group of industries in twelve OECD countries. The studies show that R&D directly stimulates productivity growth through innovation and indirectly stimulates it through the transfer of technology.

Other empirical studies apply this production function and add R&D activities (Czarnitzki and O’Byrnes, 2007) to the list of factors that increase productivity, employment, and competition in an economy. In fact, Barge-Gil and López (2011) show that R&D is a primary source of innovation and one of the determinants of firm productivity growth.

R&D Expenditures

The Spanish Sustainability Observatory (2011) studies R&D investment in relation to GDP. Its 2011 study finds that a country’s R&D expenditures determine whether productivity will increase and whether the economy will experience a long period of economic growth. According to the study, Spanish R&D expenditures are insufficient in the current economic crisis.

Nevertheless, Griliches and Mairesse (1984) conclude that R&D investments for 133 American firms between 1966 and 1977 have a strong relation with productivity. Other authors, such as, Maté García and Rodríguez Fernández (2002) and Gu and Tang (2003), also relate productivity growth to R&D expenditure.

Maté García and Rodríguez Fernández (2002) apply a theoretical model to relate productivity growth to R&D expenditures in Spanish firms (they use the ESEE database of business strategies for 1993–1999). They conclude that firm R&D investment has a significant positive effect on productivity growth. They also find relatively weak R&D investment in Spanish firms, which could involve a reduction in competitiveness relative to other European countries that do a great deal of R&D investment.

Patents

If innovation is the primary source of productivity growth, then the number of patents should reflect innovation and thus productivity growth. The number of patents may influence productivity. Crèpon et al. (1998), for example, incorporate the number of patents as an additional variable in the production function and finds that is has a positive effect on productivity. The relation between new patents and GDP growth can be an inverted U shape, implying that putting stronger protections on intellectual property can hinder economic growth. This suggests that there is an optimum level of protection to maximise economic growth.

On the other hand, how R&D affects patents depends on the quality of the patents and how well existing patents affect productivity. The earlier the firm begins the innovation process, the more patents it will get, and the more it will be able to absorb new ideas that have big results. The main advantage of patents is the generalised diffusion of the innovation in the patent description, which will help other firms to benefit from this innovation and to increase the collateral effect on productivity of other firms and on the general economy (Blazsek and Escribano, 2010).

Product Innovation

Product innovation is important in productivity analysis. Huergo and Moreno (2004) show that technology leading to process innovation and/or product innovation has the biggest effect on the growth in global productivity.

The study of Spanish manufacturing firms in Calvo González (2000) and Vega-Jurado (2008) show that the 30 per cent of firms’ sales is due to the introduction of new products that are the results of firm innovations. The majority of product innovations are entirely new products in the market. These studies find that Spanish manufacturing firms tend to innovate more in product than in process.

The creation of new products arises from new needs among consumers. In that sense, R&D affects productivity through its application of new knowledge generated by new products and new process (Czarnitzki and O’Byrnes, 2007).

Process Innovation

Previous literature finds a relation between process innovation and productivity growth. Smolny (1998) proposes that process innovations reduce production costs by optimising capital allocation and/or job productivity. The model of active learning proposes that creating and applying process innovations generate positive effects on R&D activities and on productivity (Pakes and Ericson, 1998).

More recent studies confirm this tendency for process innovations to improve productivity (Rochina-Barrachina et al., 2008). They also find that the amount of productivity growth depends on firm size, and that small firms increase their productivity when they implement new processes, especially if they do so right away. On the contrary, big firms which wait for as long as two years to implement new processes still show productivity growth.

Also, process innovation is a result of the no-productivity standstill (Huergo et al., 2004). Young firms tend to show major productivity gains, which over time tend to converge into average growth rates. This suggests that process innovations affect productivity growth in every part of the firm life cycle.

Internal Organisation of Innovation

Internal organisation of innovation is a tool that firms use to reach innovation objectives. They can be technology or R&D managers or committees (Colombo and Rabbiosi, 2014), plans for innovation activities, calculations to measure the results of innovation or evaluations of alternative technologies (Loof and Johansson, 2014). We identify which firms conduct these activities and how they affect productivity.

One factor that can better stimulate innovation is organisation culture— particularly an organisation’s ability to get employees to accept innovation as an essential value (Hartmann, 2006). An innovative firm also needs organised systems, as well as experienced and qualified technical employees to improve its productivity (Baldwin and Johnson, 1996). Milgrom and Roberts (1995) present a global model of the firm in which decisions about job duties, personnel management, outsourcing and technology choices are complementary. In other words, they find that an effective production system is really a group of complementary elements. If the firm gets an effective production system and recruits easily experienced and skilled people, then the organisation has more tools to innovate and to improve the productivity.

Skilled employees, solid organisation and efficient use of new machinery reduce the time to spread and adopt technology (Camacho López and Moreno Galbis, 2006). The studies of organisational changes that promote the adoption of communication and information technology are also recent. Askenazy and Gianella (2001) and Bresnahan, Brynjolfsson and Hitt (2002), for example, empirically show the importance of adopting technology to improve productivity. For this purpose, Bresnahan et al. (2002) investigate the effect on productivity of the combination of three related innovations: information technology, complementary workplace reorganisation and new products and services.

Externally Conducted R&D Activities

Lockshin et al. (2007) obtain econometric evidence at a micro level that productivity improves for firms that combine external and internal R&D. Also, they find that external R&D has positive effects when internal R&D expenditure level is sufficient. Similarly, Vargas et al. (2007) find that capital investments in internal and external technology improve productivity, though this strategy depends on the type of investment. Firms that have little to invest in technology get better results if they use external resources. On the contrary, firms that have a lot to invest in technology get better results if they develop internal activities.

Other studies do not find that external R&D activities are effective innovation strategies. Vega-Jurado et al. (2008), for example, find that R&D externalisation has no significant effect on innovation in Spanish manufacturing firms, because those firms fail to assimilate and integrate external R&D. On the contrary, the study finds, internal R&D activities (such as, machinery and equipment purchases) are important determinants of innovation.

Zahra and Nielsen (2002) find that the main deficiency of external R&D is that firms buy technologies that are also available to competitors. Thus, this kind of external R&D offers no sustainable competitive advantages. Also, the external assets do not always fit with the assets and processes of the firm, requiring firms to spend more in training. We study the effect of outsourcing R&D activities on productivity.

Public Funding for R&D

Huergo and Moreno (2004) find that public funding is an effective tool to stimulate R&D investment. We find that public and private R&D funding are not substitutes; rather, they are complementary activities. A small proportion of small manufacturing firms that receive public funding in Spain (Cotec, 2000) demonstrate that the current system does not provide enough incentive to firms—it should be accessible to smaller firms.

Despite strong theoretical arguments that generalised awarding of R&D funding helps, the evidence of its effects on firms is relatively modest. Jaumandreu (2004) analyses whether subsidies stimulate R&D expenditures, in the sense that research projects only occur when subsidised, and if public funding displaces private funding. We find that subsidies are potentially effective in encouraging firms to carry out R&D activities. In particular, big firms require more subsidies than small firms. Jaumandreu (2009) concludes that subsidies do play a role, although modest, in encouraging R&D investments. The weak effects seem to be the result of the conservative application of public R&D funds, and they suggest that there is room to improve the funding and efficiency of its application.

External Collaboration for Innovation

External collaboration for innovation involves actively participating in innovation projects with other organisations, such as, other firms, clients, suppliers, universities, technology centres, etc. This kind of collaboration allows firms to develop or access knowledge and techniques that they cannot develop or access alone. Mutual learning can also create synergies (Tanaka et al., 2005).

However, innovation still depends on internal factors and the interactive process that nurtures relationships with external agents. To stimulate innovation, firms can get information from clients, suppliers, universities, research institutes, public authorities, consultants, the press, conferences, etc. (Hagedoorn, 2002; Santamaria, Nieto and Barge-Gil, 2009), which means that a firm’s ability to obtain, develop, and use resources and capacities depends on its ability to absorb external knowledge through external collaboration (Teece et al., 1997).

Vega-Jurado et al. (2009) show that firms are not self-sufficient when it comes to technology and that they therefore must collaborate with other firms and institutions. R&D activities promote this and accelerate the efficiency of new-product and new-process development. In turn, purchasing external knowledge creates the ideas and resources that fuel successful innovation.

Collaborations and informal contacts also play an important and decisive role in transmitting information and creating knowledge, in addition to increasing productivity (Trigo, 2011). Geographical proximity is a relevant factor in how companies collaborate.

Data, Model and Methodology

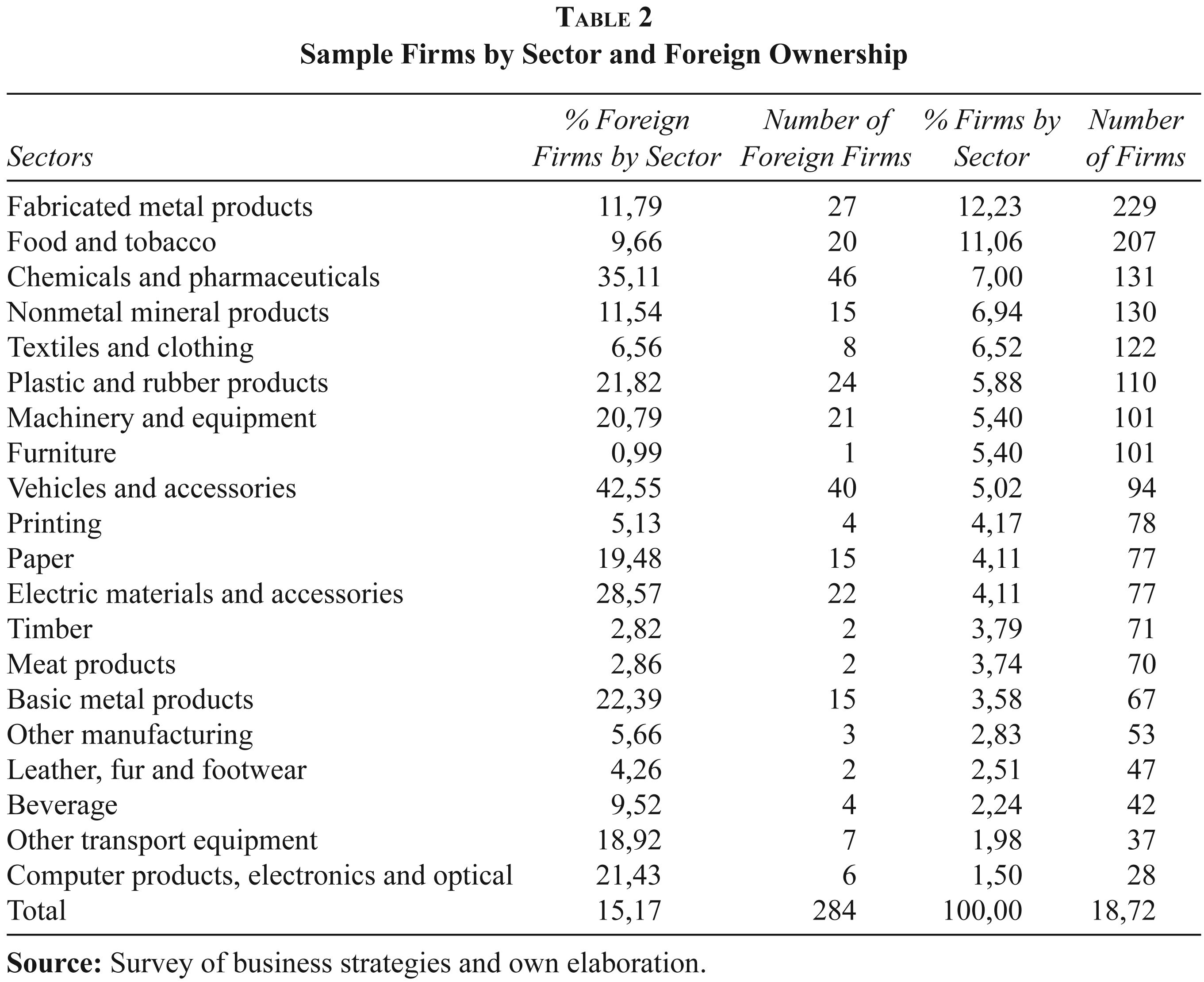

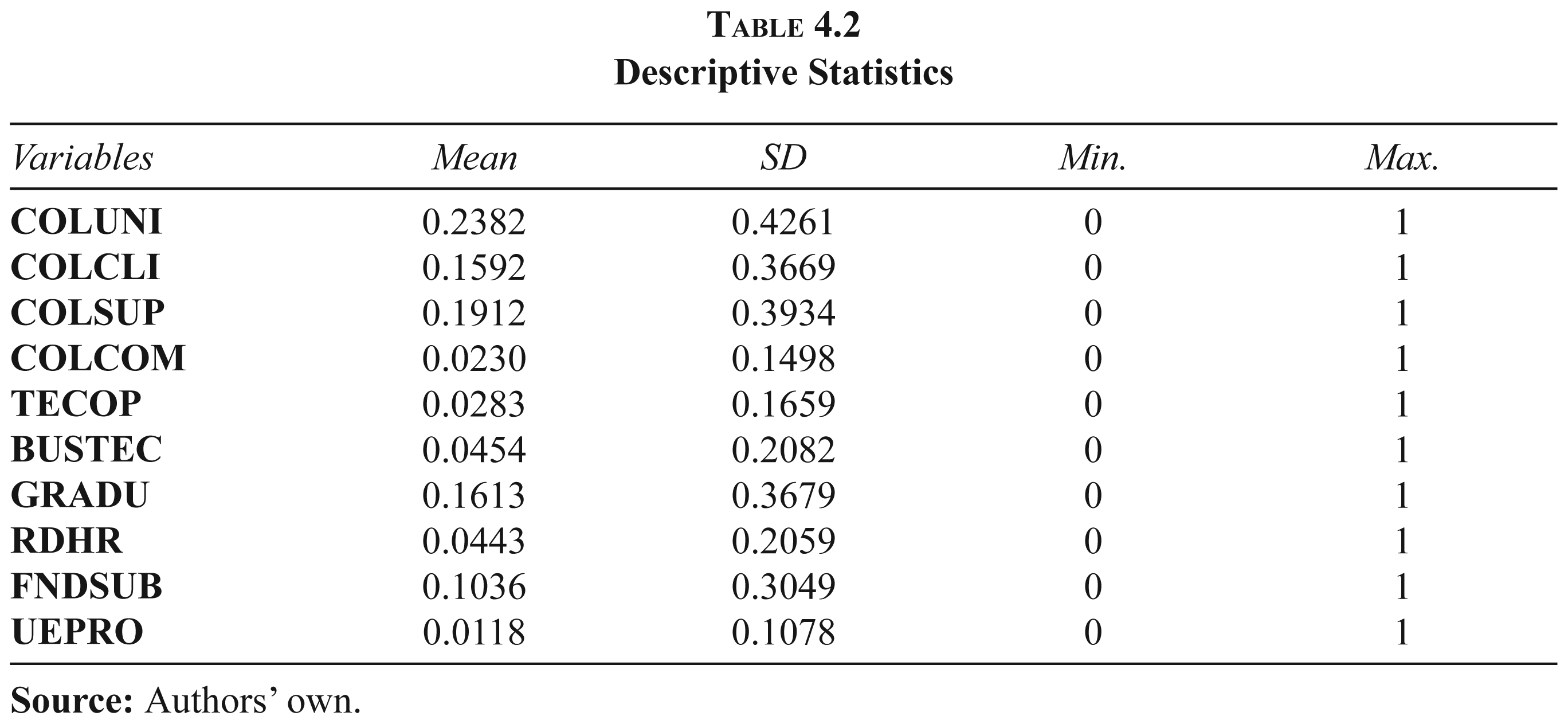

We analyse homogenous, company-level information from a voluntary annual survey of firms, with a high participation rate (around 91 per cent). The population of reference is composed of firms with ten or more employees within the manufacturing industry. Our data is from 2010 for 1,872 firms in twenty manufacturing sectors, among them the 15,17 per cent are foreign firms, 1 as we can see in Table 2. The information is from the Spanish Finance Minister’s survey of business strategies (Spanish Finance Minister, 2010). 2 The sample-selection criterion is the stratified random sampling by sector and size from a representative sample population.

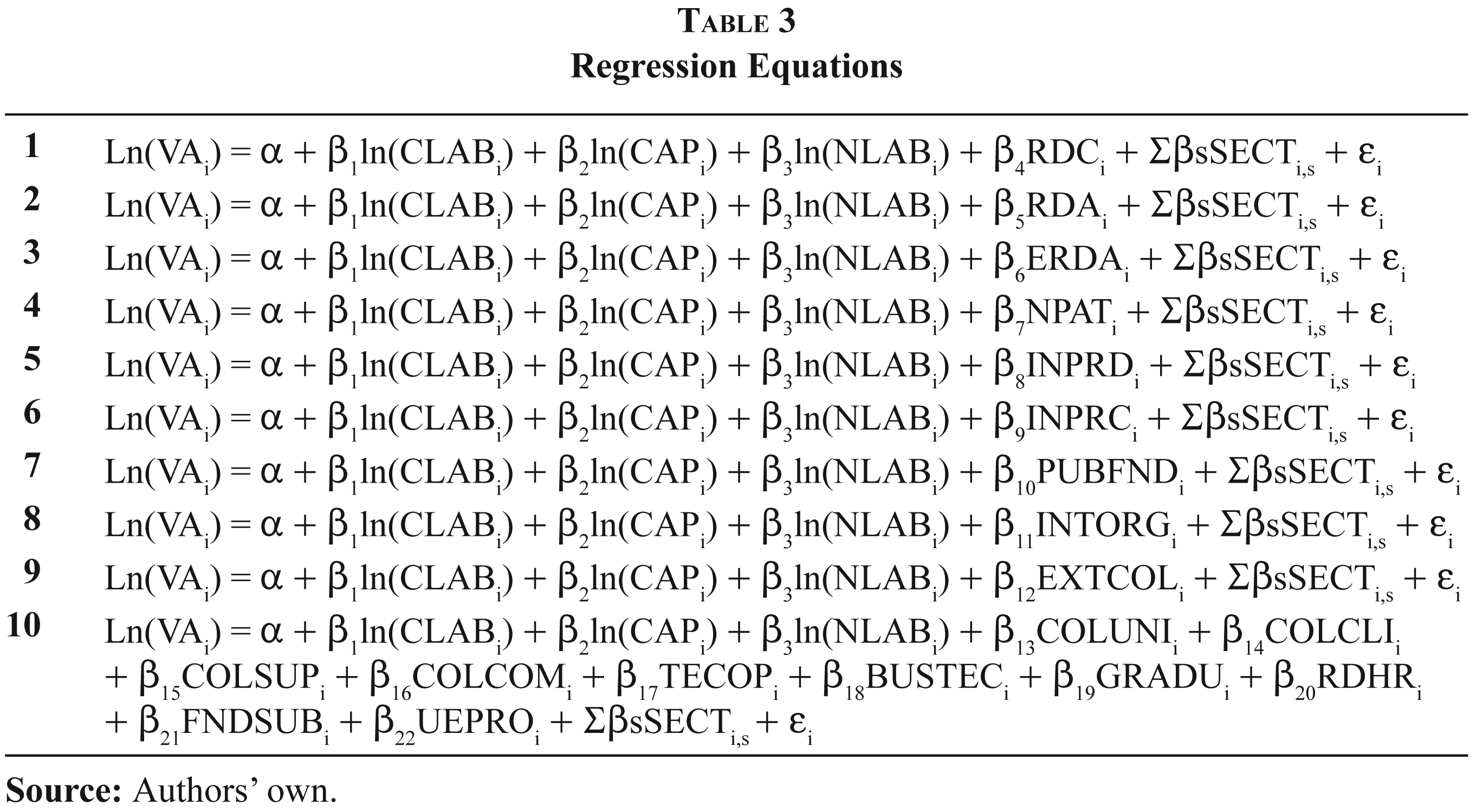

We consider one variable for each one of the aforementioned nine innovation factors and ten variables for different ways of external collaboration for innovation. In this way, we introduce alternatively each innovation factor in the traditional production function. In addition we propose the tenth production model which considers the effect of the different ways of external collaboration for innovation. We take in consideration several models to avoid the collinearity between variables. In the following, the models are production functions that explain how innovation factors affect added value (output).

Sample Firms by Sector and Foreign Ownership

Regression Equations

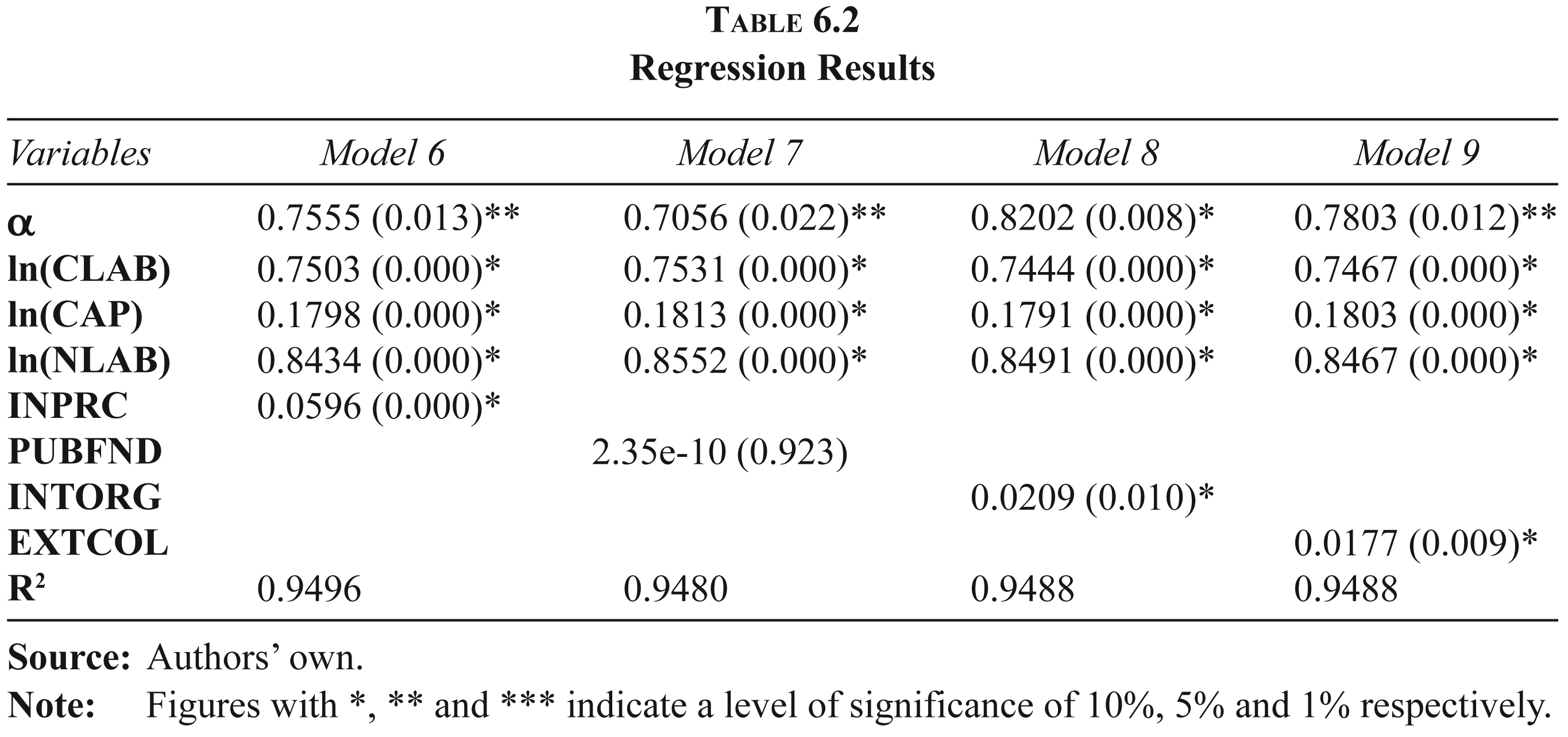

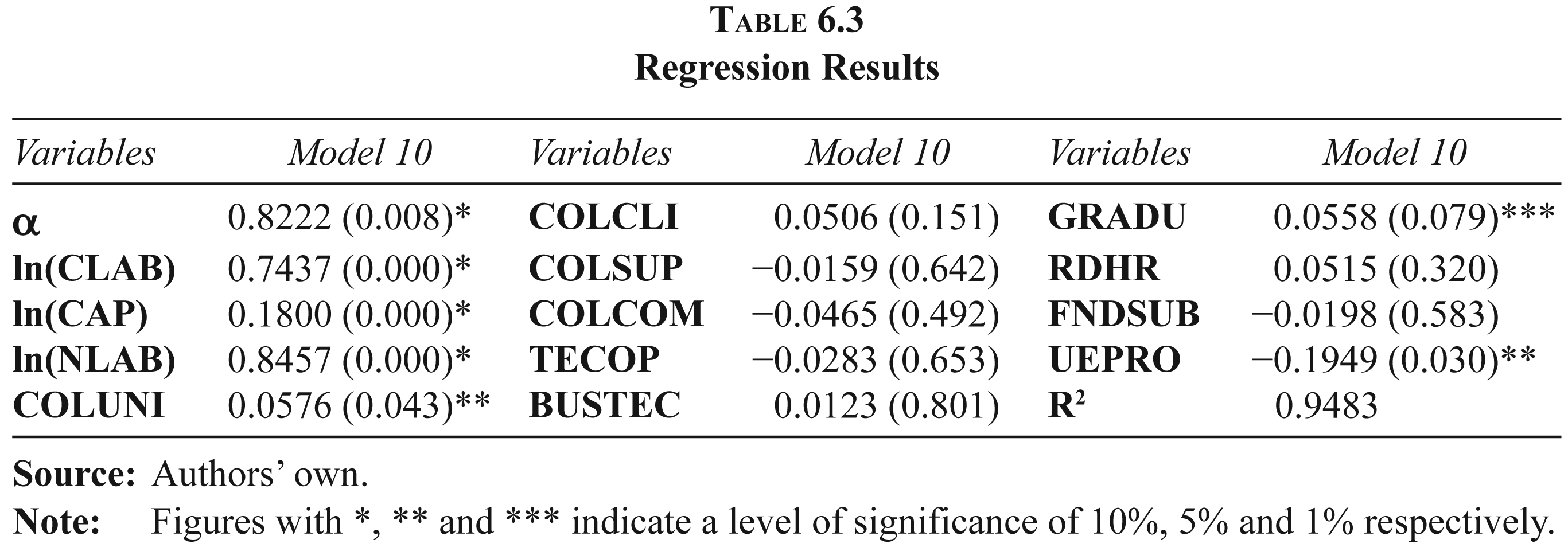

where α is the natural logarithm of technological level. VA is output measured as value added. Value added is the sum of sales, variation in stocks for sale, other current management income and variation in stocks bought, less purchases and external services. CLAB is the cost of the input labour per employee and it enables us to analyse the substitution effect between capital and labour. CAP servicing of capital input, which equals tangible fixed assets. NLAB is the servicing of labour input, expressed as number of workers employed. SECTi,s equals 1 if firm i belongs to sector s. In any other case, it equals zero. The coefficientβ Model 1. RDC is R&D costs divided by the stock of capital. Model 2. RDA (internal and external R&D activities) equals 1 if the company conducts R&D activities internally or externally, 2 if the company conducts R&D activities both internally and externally, and zero otherwise. Model 3. ERDA (externally conducted R&D activities) equals 1 if R&D activities are carried out externally; otherwise, it equals zero. Model 4. NPAT is the number of patents. Model 5. INPRD (product innovations) equals 1, 2, 3 or 4 to indicate how many of the following product innovations a firm achieves: (a) incorporation of new materials, (b) incorporation of new components or intermediate products, (c) incorporation of new designs and presentation and (d) incorporation of new functions. If the company makes no innovations, the variable equals zero. Model 6. INPRC (process innovations) equals 1, 2 or 3 to indicate how many of the following process innovations a firm achieves: (a) introduction of new machinery, (b) introduction of new software or (c) new methods of organising production. If none happen, the variable equals zero. Model 7. PUBFND is the amount of public R&D funding divided by total R&D costs. Model 8. INTORG (internal organisation of innovation) equals 1, 2, 3 or 4 to indicate how many of the following mechanisms a firm puts in place: (a) a technology or R&D manager or committee, (b) a plan for innovation activities, (c) calculations to measure the results of innovation or (d) evaluations of alternative technologies. If none of these are present, the variable equals zero. Model 9. We include in this model only EXTCOL as an innovation variable. EXTCOL (external collaboration for innovation) equals 1, 2, 3, 4, 5, 6, 7, 8, 9 or 10 to indicate how many of the following activities the business conducts: collaborating with universities and/or technology centres (COLUNI), collaborating with clients on technology (COLCLI), collaborating with suppliers on technology (COLSUP), collaborating with competitors on technology (COLCOM), having technological cooperation agreements (TECOP) (joint ventures), owning shares of businesses developing technological innovations (BUSTEC), employing recent college graduates (GRADU), especially those with degrees in science, engineering or technology, recruiting personnel with R&D experience in a business context (RDHR), funding innovation with subsidies (FNDSUB) or participating in research programmes of the European Union (UEPRO). If the business conducts none of these activities, the variable equals zero. Model 10. We propose in this model the aforementioned ten variables related with external collaboration for innovation that we mentioned in EXTCOL. These variables are COLUNI, COLCLI, COLSUP, COLCOM, TECOP, BUSTEC, GRADU, RDHR, FNDSUB and UEPRO.

As we have already commented, previous papers studied partially these factors. This is the first article that provides an overview of all these factors to explain innovation in firms.

Results and Discussion

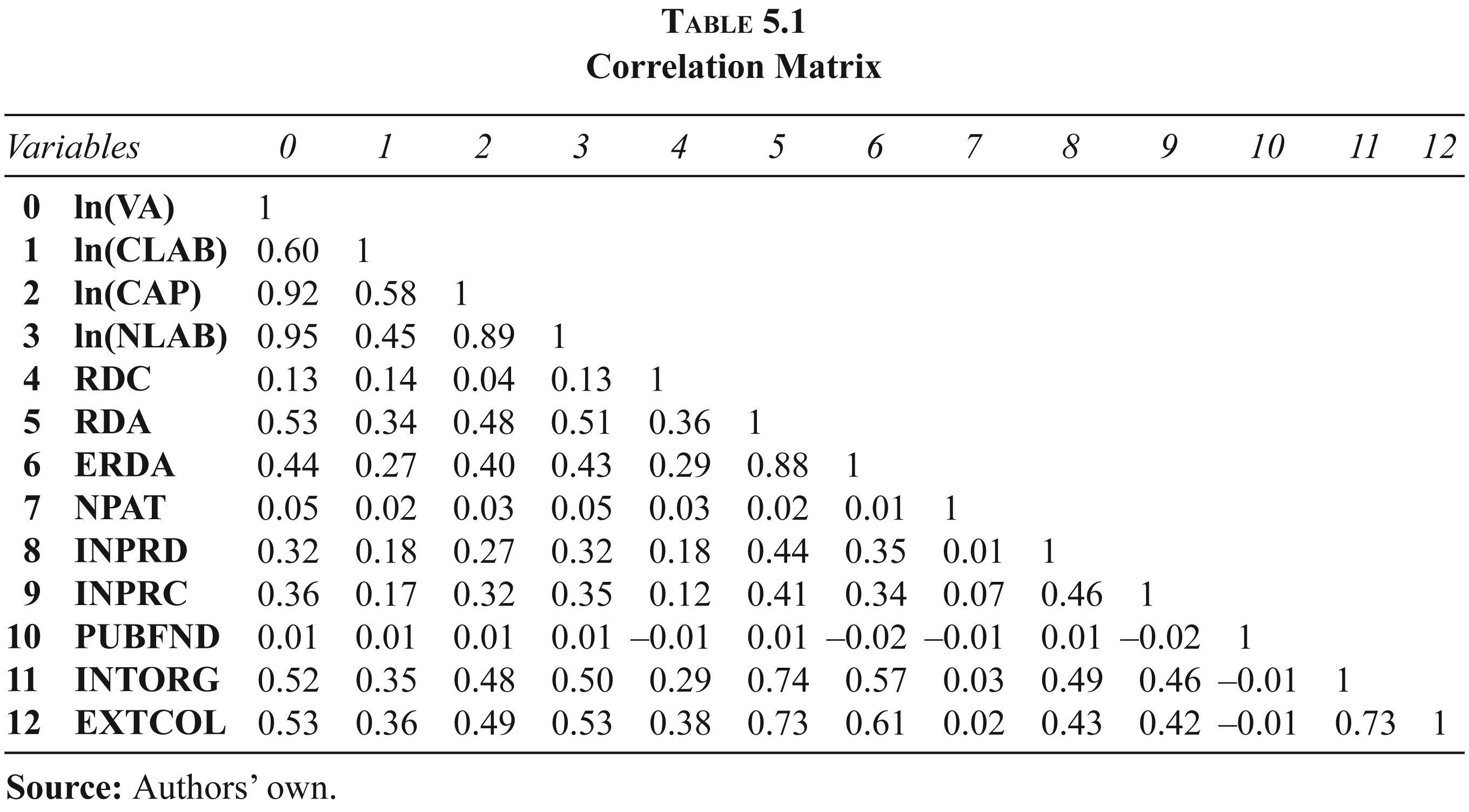

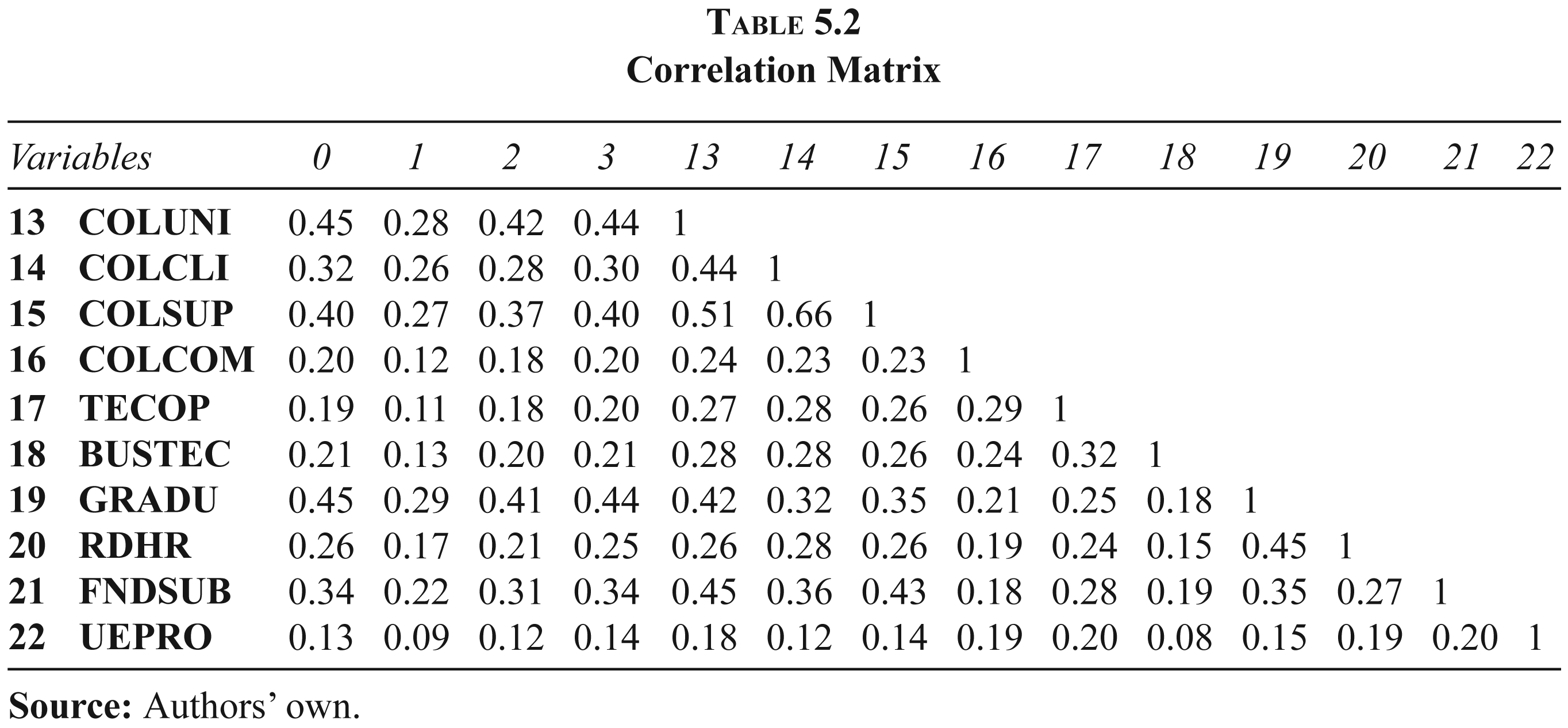

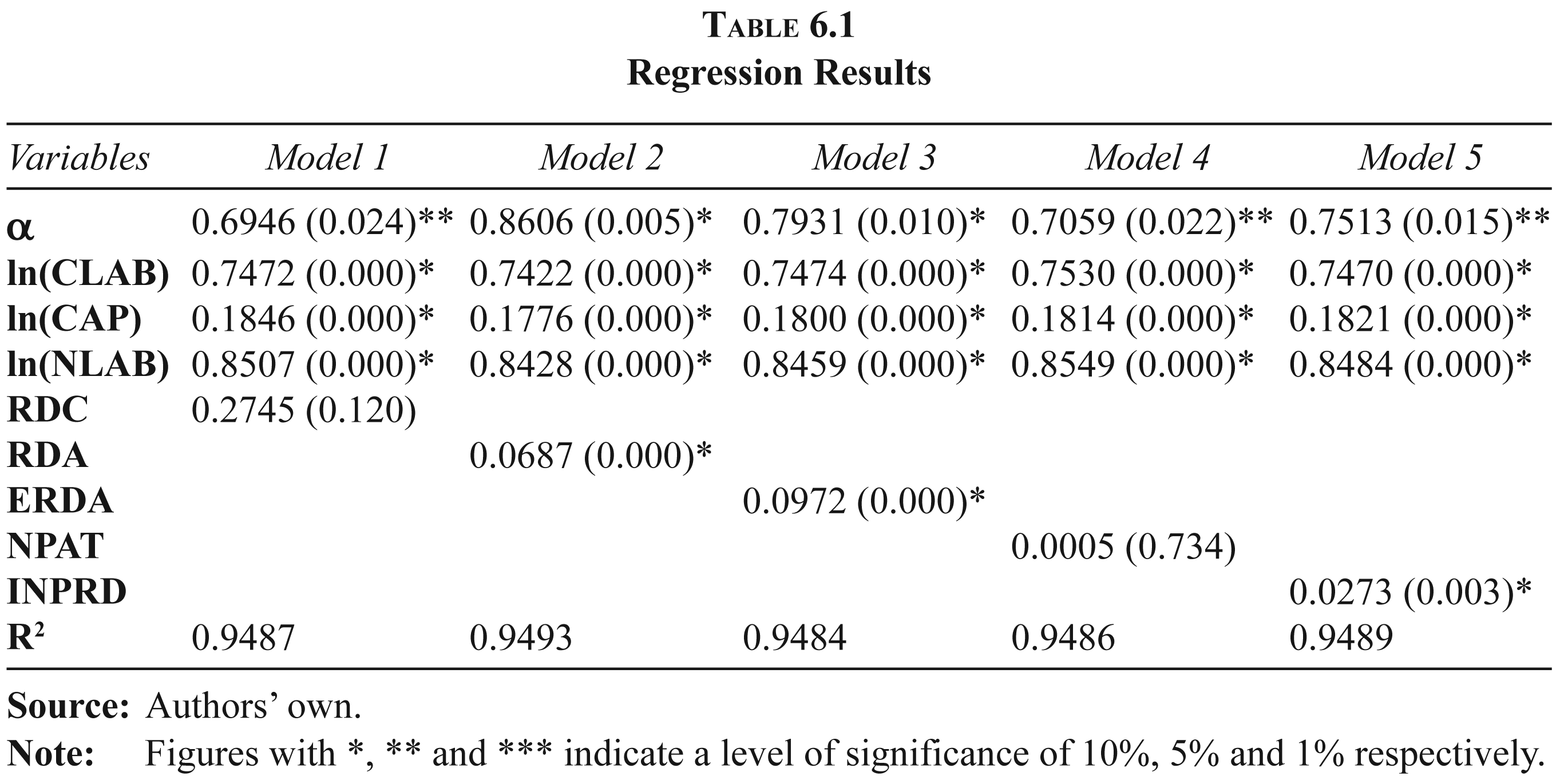

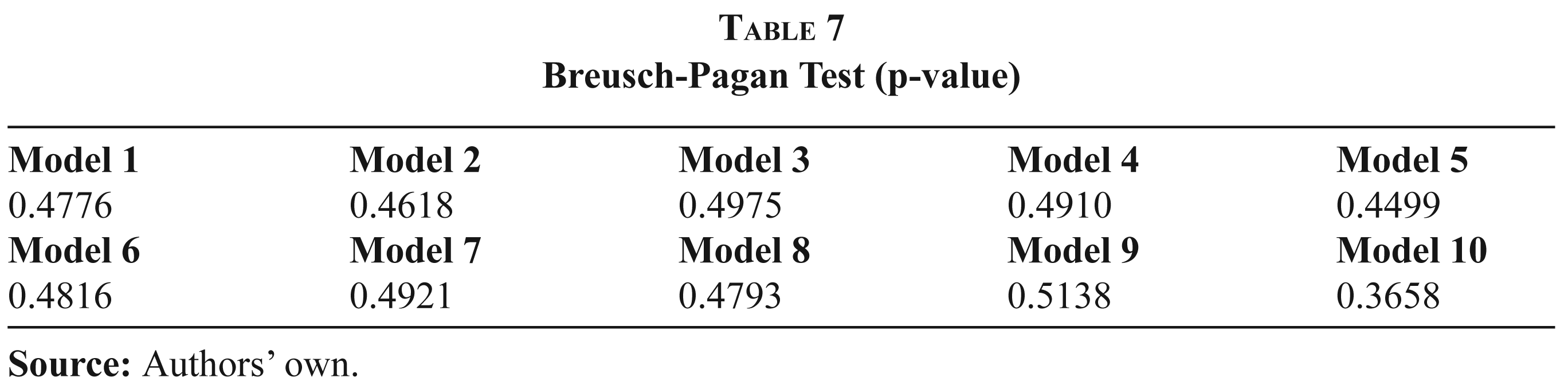

We obtain all the estimations with Stata 9.0 (see Tables 4.1, 4.2, 5.1, 5.2, 6.1, 6.2, 6.3 and 7), as well as the descriptive statistics (mean, standard deviation, minimum and maximum), a correlation matrix for the independent and dependent variables of expression (1) to interpret the regression results and the p-value of Breusch-Pagan Test. The correlation coefficient (R2) of all the models are 0.95—very close to one—so the goodness of fit is very high. We apply the Breusch-Pagan test to check for heteroskedasticity. This test shows that the null hypothesis of homo-skedasticity can be accepted in each one of the regression equations. Because of this reason, we apply ordinary least squares (OLS) estimation.

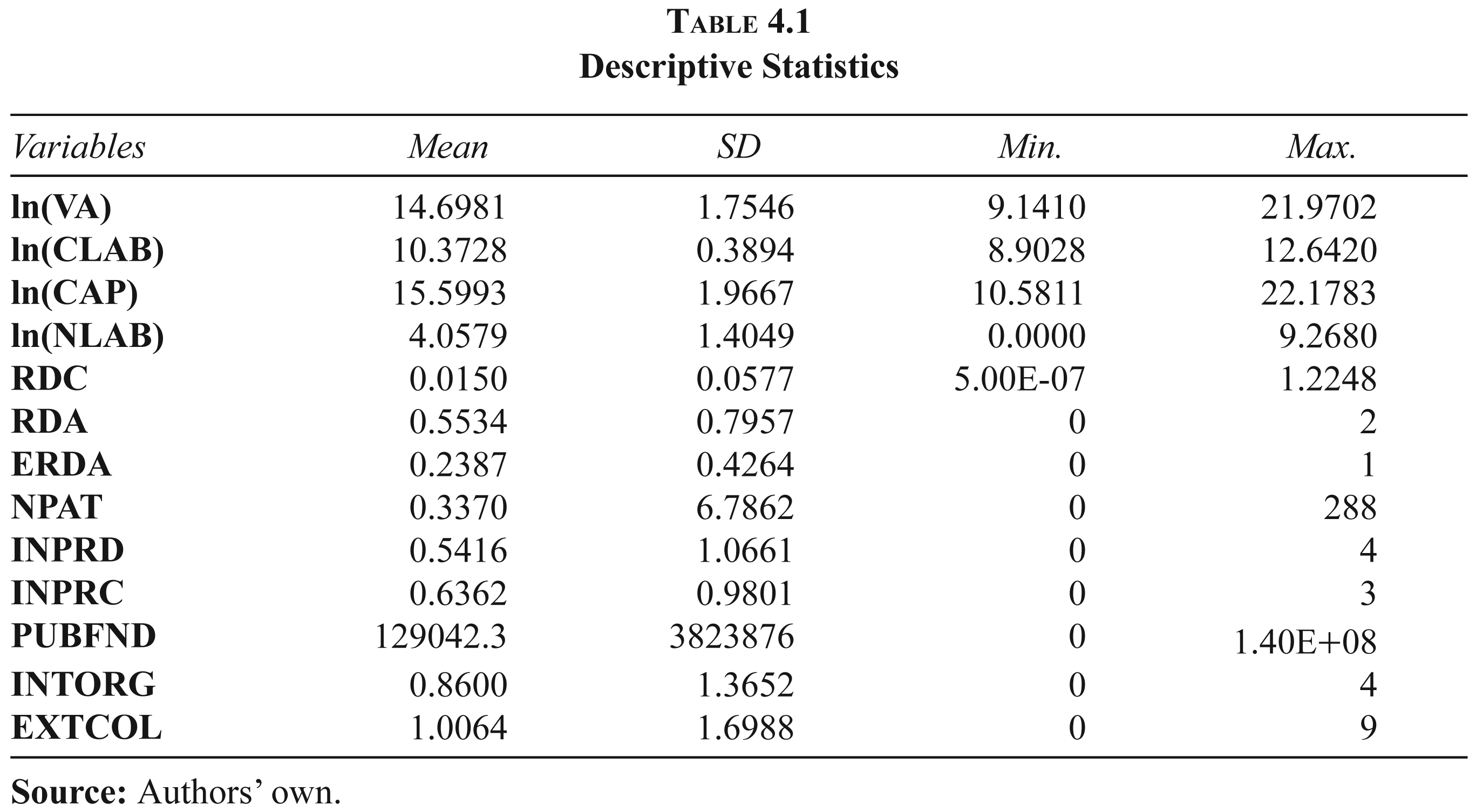

Descriptive Statistics

Descriptive Statistics

Correlation Matrix

Correlation Matrix

Regression Results

Regression Results

Regression Results

Breusch-Pagan Test (p-value)

The elasticity of the output of labour and capital is consistent with the hypothesis of constant returns to scale. The estimation gives a coefficient for capital of 0.18 and a coefficient of 0.85 for labour (number of workers), together amounting to roughly 1.03. This is not statistically equal to 1, suggesting slightly increasing returns to scale.

R&D activities and the externalisation of R&D activities have a positive relation with productivity, confirming Hypothesis 1 and 7. The estimation gives a higher coefficient for externalisation of R&D activities than a coefficient for R&D activities. These two estimation results suggest that external R&D activities immediately give higher improvements on productivity than internal R&D activities. This is due to the external R&D activities have had more time to be proven and they have been successful previously in other firm. This finding supports other evidence in the literature.

Nevertheless, R&D expenditures have no effect on productivity, so it is not possible to confirm Hypothesis 2. In the production function, we include R&D costs divided by the stock of capital (RDC) in a redundant manner in the estimation of output. This expenditure is included in input capital, estimated as a stock (a proxy for the input capital). Because the coefficient for this variable can be zero, this capital’s output is as elastic as the rest of the assets. The explanation likely lies in the way the survey measures R&D expenditures (it counts them when they are included as fixed assets). This accounting method occurs only if the innovation has been real, effective and valuable. We interpret that to mean that the correct development of R&D improves productivity more than the amount of R&D expenditures does.

Because the number of patents (NPAT) can equal zero, there is no proof to confirm Hypothesis 3. Despite this, NPAT is in the model because patent ownership implies that firms are exploiting this advantage, that it is difficult for others to appropriate it, that its privacy is enhanced, and that there is no interest in using third-party innovations or improvements.

Public R&D funding has no significant effect on productivity; therefore, we cannot confirm Hypothesis 8. The reason is that some of these firms carry out R&D only for getting public financial support.

Product and process innovations are positive at the 1 per cent significance level, confirming hypotheses 4 and 5. This implies that product and process innovations improve the generation of technology knowledge and productivity.

There is proof to confirm Hypothesis 6, because the positive relationship between internal organisation and productivity is significant. So, if a firm carries out a higher number of activities related to the internal organisation of innovation, then it reaches a higher productivity.

External collaboration for innovation has positive and significant effects on productivity; therefore, we confirm Hypothesis 9. This result is mainly due to the collaborating with universities and/or technology centres and to the employing of recent college graduates, especially those with degrees in science, engineering or technology. On the other hand, if a firm participates in research programmes of the European Union then it affects negatively on productivity.

Concluding Remarks

This study supports previous findings that innovation is a source of productivity. We analyse data from 2010 for 1,872 firms in 20 industries via a function– production model. The models include the following innovation factors on productivity in Spanish manufacturing firms: R&D activities, R&D expenditures, patents, product innovations, process innovations, internal organisation of innovation, externalisation of R&D activities, public funding for R&D and external collaboration for innovation, relationships of innovation and different ways of external collaboration for innovation.

Our findings show that R&D activities improve the productivity of Spanish manufacturing firms. External R&D activities have a bigger effect than internal R&D activities. This result explains firm decisions to externalise R&D for innovations that have had more time to be proven and they have been successful previously in other firm.

In addition, product and process innovation give firms better tools to carry out activities. We confirm that innovation in product and production process improves the application and production of required knowledge that improves productivity.

If a firm carries out a higher number of activities related to the internal organisation or the external collaboration for innovation, then it reaches a higher productivity. This positive effect is bigger when a firm collaborates with universities and/or technology centres and employs recent college graduates, especially those with degrees in science, engineering or technology.

Our findings create future research opportunities, such as the study of vertical relations between firms (such as with suppliers and clients).

Footnotes

Acknowledgements

This study was supported by the Spanish Ministry of Economy and Competitiveness and FEDER (project ECO2012-36290-C03-01) and the Regional Government of Aragón and FSE (project S125). We acknowledge the suggestions of the anonymous referees, editor and César Sánchez-Sellero.