Abstract

More than half of Chinese high-technology firms are led by top executives (chairman and CEO) with R&D background. This study investigates whether and how top executives’ R&D background affects corporate innovation outcomes using a sample of listed firms in the high-technology industries in China. We find that the R&D background of top executives is positively related to innovation outcomes. We also find evidence on the mediating effect of R&D expenditure and moderating effect of corporate risk-taking on the above relationship. Our baseline results are robust to tests that address concerns caused by potential unobservable characteristics, reverse causality and other issues. Findings of our study have important implications for firms that aim to enhance their innovation outcomes and countries regarding their research policymaking and R&D management.

Introduction

A CEO’s research orientation is a good indicator of a company’s motivation to innovate and ultimately affects innovation outcomes. Research-centric CEOs create the organisational conditions to foster innovation like supporting research-oriented managers to innovate, increase their managerial discretion and allocate more resources to R&D. This, in turn, helps innovation thrive.

—Forbes, 19 November 2019 (Amyx, 2019)

Extant literature has studied the effect on firms’ innovation outcomes of various CEO characteristics, such as military experience (Benmelech & Frydman, 2015), pilot CEOs (Sunder et al., 2017), inventor CEOs (Islam & Zein, 2020) and technical backgrounds (Barker & Mueller, 2002; Daellenbach et al., 1999). However, one important area that has received little attention is top executives’ R&D background. 1 This lack is surprising given that top executives’ R&D background enables firms to make effective innovation strategy choices in the first place (Ahuja & Lampert, 2001; Omar et al., 2017). It is also a good indicator of a company’s critical organisational conditions in which innovation capabilities reside (Amyx, 2019; Talke et al., 2010; van de Wal et al., 2020). This article aims to investigate whether and how CEO’s R&D background affects corporate innovation outcomes using a sample of high-technology firms in China.

The first reason of focusing on high-technology firms is that innovation activities are crucial for survival in high-technology industries. Competition in these industries is knowledge-based and our study of top executives’ background, experience and knowledge on R&D, therefore, provides a good understanding of one of the major sources of competition (Yun et al., 2016). Second, compared with other industries where the R&D function is often outsourced (Chesbrough, 2003; Chesbrough & Crowther, 2006), high-technology industries have seen the majority of R&D activities being internally conducted, which provides a context where the mediating effect of R&D investments on the relationship between top executives’ R&D background and innovation outcomes can be investigated. Third, although firms in high-technology industries tend to involve in more innovation activities than those in other industries, not all high-technology firms are equally innovative. It is therefore important to understand factors that are supportive of corporate innovation within this population of firms (Hayton, 2005).

The rationale of using China as a laboratory to investigate the effect of CEO with R&D background on corporate innovation is twofold. First, China, which has been well-known as the world’s manufacturing centre, also emerges as a global innovation leader. 2 For example, according to the data from the World Intellectual Property Organisation (WIPO)’s Patent Cooperation Treaty (PCT) System, China filed 58,990 applications in 2019, which surpassed the United States (57,840 applications in 2019) as the biggest filer of international patents—a position previously held by the United States each year since the PCT began operations in 1978. 3 Moreover, the PCT applicant list in China largely comprises organisations from the corporate sector and the PCT top ten applicants are all companies. 4 Second, as opposed to many other countries, including the United States where CEOs of big pharmaceutical giants, for example, are more likely to have a background as company lawyers, salespeople or finance managers, than one in pharmaceutical or medicine R&D (Felix & Bistrova, 2015), more than half of our sample high-technology companies in China are led by top executives (CEO and/or Chairman) with R&D background. This provides a sound context where the effect of CEO with R&D background on corporate innovation is investigated.

Using a sample of listed firms in the high-technology industries in China over the period from 2012 to 2017, 5 we investigate whether and how top executives’ R&D background affects corporate innovation outcomes. We find that the R&D background of top executives is positively related to innovation outcomes. We also find evidence on the mediating effect of R&D expenditure and moderating effect of corporate risk-taking on the above relationship.

The positive correlation between top executives’ R&D background and innovation outcomes, however, needs to be interpreted with caution. The observed positive correlation could be caused by unobservable variables that may also explain innovation outcomes. One way to address such a concern is to analyse variations among firms led by top executives with R&D background only. If top executives’ R&D background does indeed drive the above positive correlation, then this effect should be stronger for top executives with longer R&D experience. Our results show that the longer the R&D experience of top executives is, the better the innovation outcomes. Our observed positive correlation could also be caused by potential reverse causality in that firms pursuing innovation strategies and outcomes may be more likely to select top executives with R&D background (Chaganti & Sambharya, 1987; Datta & Guthrie, 1994; Thomas et al., 1991). To address this concern, we employ the propensity score matching (PSM) method, which shows that our baseline results are robust.

The contribution of this study to the literature is threefold. First, this article answers the call for studies on mechanisms behind China’s innovation achievements at the firm-level (Wang et al., 2014; Xiong & Xia, 2020). Second, this article builds upon the earlier studies that investigate the effect on firms’ innovation outcomes of various CEO characteristics. Our article is complementary to those studies by examining the impact of top executives’ R&D background, which is an important but yet underexplored characteristic of top executives. Two studies closest to our study are the Islam and Zein (2020) study examining the impact of ‘inventor CEOs’ on corporate innovation and van de Wal et al. (2020) study looking into the impact of CEO research orientation on firm innovation outcomes. Islam and Zein (2020) find a causal relationship that ‘inventor CEOs’ contribute to higher quality corporate innovation. Given that inventor CEOs may not be prevalent everywhere, our study complements the Islam and Zein (2020) study by examining the impact on corporate innovation of R&D background of top executives, which is a broader and more prevalent phenomenon and of which the findings are more generalisable. van de Wal et al. (2020), which uses 109 CEOs from 87 U.S.-based pharmaceutical firms over the period 2001–2013 as a sample, find that research-oriented CEOs increase their firms’ innovation outcomes. Our study complements the van de Wal et al. (2020) study by focusing on all high-technology industries. Third, this study not only reveals the association between top executives’ R&D background and corporate innovation outcomes, but also further attempts to explore the underlying mechanisms and moderating factors, which contributes to a comprehensive understanding on the relationship between top executives’ R&D background and innovation outcomes.

The remainder of this article is organised as follows: The second section presents the literature review and hypothesis development. Research design and empirical results are discussed in the third and fourth sections, respectively. The fifth section concludes the article and makes some discussions.

Literature Review and Hypothesis Development

Literature Review

A growing body of literature has related various CEO characteristics to innovation or R&D spending, but considerably limited attention has been put on CEO R&D background, which is an important aspect of a CEO’s personal characteristics that may influence corporate innovation strategies and performance (Islam & Zein, 2020).

Some earlier studies that close to our study have connected R&D background of top management team (TMT) to innovation strategies, but these studies have focused on the other way around, that is, the impact of innovation strategies on TMTs’ R&D background. For example, Datta and Guthrie (1994) study CEO successions and find that firms with higher R&D spending are more likely to appoint new CEOs who have technical backgrounds.

Some other studies have examined the impact of the technical or other backgrounds of the TMT or CEO on innovation commitment. For example, Daellenbach et al. (1999) find that the proportion of a firm’s top managers with working experience in technical areas (namely, engineering, production or operations or R&D) are positively related to the firm’s commitment to innovation. Barker and Mueller (2002) find that firms where CEOs have significant working experience in marketing, engineering or R&D tend to have greater R&D spending. While these two studies attempt to explore the impact of TMT technical backgrounds and provide a theoretical base for our study, they have focused on the impact of broad TMT backgrounds that cover engineering, production, operations, marketing or R&D and failed to lay a solid theoretical foundation and explore the mechanisms underpinning the impact of each background. Another limitation of the above studies is that they only focus on the impact of the technical or other backgrounds of the TMT or CEO on R&D spending, which makes them unable to reveal the impact of TMT backgrounds on innovation outcomes.

Two studies closest to our study are the Islam and Zein (2020) study and van de Wal et al. (2020) study. Islam and Zein (2020) examine the impact of ‘inventor CEOs’ on corporate innovation and find that ‘inventor CEOs’ contribute to higher quality corporate innovation. van de Wal et al. (2020) use a sample of 109 CEOs from 87 U.S.-based pharmaceutical firms over the period 2001–2013 as a sample to investigate the impact of CEO research orientation on firm innovation outcomes. This study shows that research-oriented CEOs increase their firms’ innovation outcomes.

R&D background of top executives are considered important for corporate innovation because it represents top executives’ superior ability to assess, select and conduct innovative investment projects based on their R&D experience (Islam & Zein, 2020). It also indicates a company’s critical organisational conditions in which innovation capabilities reside (Amyx, 2019; Talke et al., 2010; van de Wal et al., 2020). However, the relationship between R&D background of top executives and corporate innovation is not yet obvious. Despite their R&D experience, top executives may be incapable of commercialising or marketing their firms’ technologies (Islam & Zein, 2020), or lack other functional or operational capabilities. Thus, whether and how a R&D background enhances a top executive’s ability to successfully spark firm-wide innovation remain open empirical questions. This article aims to answer these questions using a sample of high-technology firms in China.

Hypothesis Development

Top Executives’ R&D Background and Corporate Innovation Outcomes

We posit that R&D background as an individual characteristic of top executives can be associated with innovation outcomes for the following reasons.

First, from the perspective of managerial attitudes and beliefs, R&D background, particularly long-term R&D experience, enable top executives to develop their attitudes and beliefs on the importance of innovation. Such beliefs are important as they help give higher priority to innovation and create an innovative organisational culture. Second, from the perspective of managing innovation activities, top executives with R&D background create the organisational conditions and culture to foster innovation such as changing the compensation schemes of R&D executives and increasing their managerial discretion (Lerner & Wulf, 2007), attracting talents through labour market sorting (Van den Steen, 2005), prompting tolerance for failure (Tian & Wang, 2014) and allocating more resources to R&D (Amyx, 2019). This, in turn, increases innovation outcomes. Last but not least, as innovation activities are usually full of complexity and uncertainty and consume a large amount of resources, top executives’ R&D background enable them to accumulate innovation-related reputational, social and relational capitals, which play significant roles in corporate innovation activities.

Therefore, it is expected that R&D background of top executives has a significant influence on corporate innovation outcomes. Hence, we posit the following:

Hypothesis 1: R&D background of top executives has a positive effect on innovation outcomes.

Mediating Effect of R&D Expenditure

First of all, it is argued that top executives with R&D background are motivated to allocate funds to the R&D function. Accordingly, devoting funding to R&D can benefit their self-interests because it can be used to support compensation, reputation, career development and so on (Dalziel et al., 2011). From the perspective of managerial attitudes and beliefs, top executives with R&D background tend to value the contribution of R&D investment as a precursor of innovation, and in turn are willing to invest on R&D activities. From the perspective of functional expertise, top executives with R&D background can be said to be experts in product and/or process R&D (Finkelstein, 1992). Such knowledge and expertise allow them to provide advice or make decisions on R&D projects. Therefore, top executives with R&D background will be more capable than other top executives of making R&D investment decisions.

Top executives’ R&D background also sends out powerful messages to finance providers about their understanding, expertise and emphasis on R&D projects, which are characterised with high degree of uncertainty (Hall & Lerner, 2010; Useem, 1979). These messages are important because they help reduce the information asymmetry between funds users and providers, which makes it relatively easy for firms to obtain external finance for their R&D projects. The role of top executives’ R&D background is expected to be particularly important in high-technology firms because of their typically sophisticated and untransparent natures in business as compared with other firms.

Collectively, these arguments suggest that top executives’ R&D background will enhance R&D investments. We therefore propose the following hypothesis:

Hypothesis 2a: R&D background of top executives has a positive effect on R&D expenditure.

R&D has been the determinant of innovation that has received the most attention from researchers because R&D investment is one of the most important mechanisms in determining innovation (Baldwin & Hanel, 2003; Becheikh et al., 2006). R&D investments are important to innovation because they are vital to create the new knowledge required to develop innovations. This is particularly true for innovations of a high degree of novelty, which consumes heaps of resources and requires high level of R&D investments (Amara et al., 2008; Caloghirou et al., 2004; Romijn & Albaladejo, 2002).

Given the vital role of R&D investments in innovation, one can expect that R&D background of top executives help them effectively set up R&D investment strategies and allocate resources for R&D investments, which, in turn, strengthen innovation outcomes. These arguments suggest that R&D investments intervene in the relationship between top executives’ R&D background and innovation outcomes by playing a mediating role. Therefore, we posit the following:

Hypothesis 2b: R&D expenditure plays a mediating role in the relationship between top executives’ R&D background and innovation outcome.

Moderating Effect of Risk-Taking

Existing literature on innovation has identified a couple of contingency factors that can influence the relationship between R&D and innovation (Damanpour, 1996). Among the possible factors, top executives’ attitude towards risk plays an important role in their R&D investment decision making because R&D investments are featured with long payback period and high risk (Tan, 2001).

Top executives with R&D background present path dependence on R&D investments when dealing with risks. More specifically, their R&D experience would enable them to believe the importance of R&D investments in dealing with risks on one hand. On the other hand, based on the upper echelons theory and resources-based view, top executives’ human, social and relational capitals would make them capable of doing so. This is particularly important when firms are facing financial constraints because top executives with R&D background may prioritise R&D investments in the event of financial constraints.

From the perspective of managerial reputation and career concern, when a firm faces risks, it will attract attention, monitoring or even criticisms from shareholders and other stakeholders. In this case, top executives with R&D background are able to capitalise their expertise and experience in selecting R&D projects and managing R&D activities to engage in R&D initiatives, which is a means of boosting stakeholder confidence in the firm and improving their personal reputation. This is particularly true for high-technology firms. Top executives with R&D background as insiders can also use their information advantage to increase their negotiation power with shareholders and find excuses for declining performance, which help them reduce the possibility of dismissal and career concerns.

To sum up, these arguments suggest that top executives with R&D background tend to increase R&D expenditure when the level of corporate risk-taking is high. Hence, we propose the following hypothesis:

Hypothesis 3a: Corporate risk-taking positively moderates the relationship between top executives’ R&D background and R&D expenditure, that is, top executives with R&D background tend to increase R&D expenditure when the level of corporate risk-taking is high.

On one hand, corporate risk-taking represents executives’ willingness to take risks in the pursuit of profitable opportunities (Faccio et al., 2011). More specifically, top executives with R&D background tend to have a strong belief on the importance of innovation. Because of this belief, top executives would support innovation activities through maintaining or even increasing R&D investments in the event of volatility in performance and high uncertainty (Yun, 2016). Also because of this belief, top executives with R&D background tend to promote an organisational culture that encourages innovation and tolerates failure, which benefits innovation efficiency and outcome (Sunder et al., 2017; Tian & Wang, 2014).

On the other hand, R&D background would enable top executives to know well about innovation practices, improve innovation strategies, facilitate cooperation among various departments and teams to support the conduct of R&D projects, and integrate various technologies and knowledge resources (Galasso & Simcoe, 2011). More importantly, top executives with R&D background are deemed to provide continuous funds especially at the critical stages to bypass the difficult periods, which greatly helps improve innovation outcomes. The above arguments are particularly true for high-technology firms because of severe competition they face.

Collectively, these arguments indicate that corporate risk-taking is expected to intervene in the relationship between top executives’ R&D background, R&D investments and innovation outcome by exerting a moderating effect. Thus, we posit that:

Hypothesis 3b: Corporate risk-taking positively moderates the mediating role of R&D expenditure in the relationship between top executives’ R&D background and innovation outcomes, that is, the effect of top executives’ R&D background on innovation outcomes through R&D expenditure is more profound when risk-taking is high than that when risk-taking is low.

To illustrate our hypotheses, we develop a conceptual framework (Figure 1).

Research Design

Data and Sample

Our sample consists of A-share companies in the high-technology industries listed on the Main Board and Growth Enterprise Market over the period 2012–2017. High-technology industries are determined according to the High-tech Classification of Manufacturing Industries (2017) and High-tech Classification of Service Industries (2018) issued by the National Bureau of Statistics of China. We exclude firms marked with ST and *ST, and observations with a ratio of debt-to-total assets being bigger than 1. 6 All continuous variables are winsorised at the 1st and 99th percentiles. We also eliminate firms that never disclose R&D and patent information during our sample period. Applying the abovementioned filters yields our final unbalanced panel dataset consisting of 798 firms and 3,535 firm-year observations. Data on characteristics of corporate top executives are obtained from Wind Information Co., Ltd (henceforth WIND) and the China Stock Market & Accounting Research (CSMAR) Database, which are leading financial data and solutions providers in China. 7 Annual reports and companies’ websites are used to source some missing information from the abovementioned databases. Data on innovation outcomes are from CSMAR. Data on innovation outcomes missed in CSMAR for some companies are further obtained from other sources, including Patent Database Service Platform of China Intellectual Property Right Net (for patents registered in China), European Patent Office (EPO, for patents registered in Europe) and United States Patent and Trademark Office (USPTO, for patents registered in the US), where possible. 8

Variables

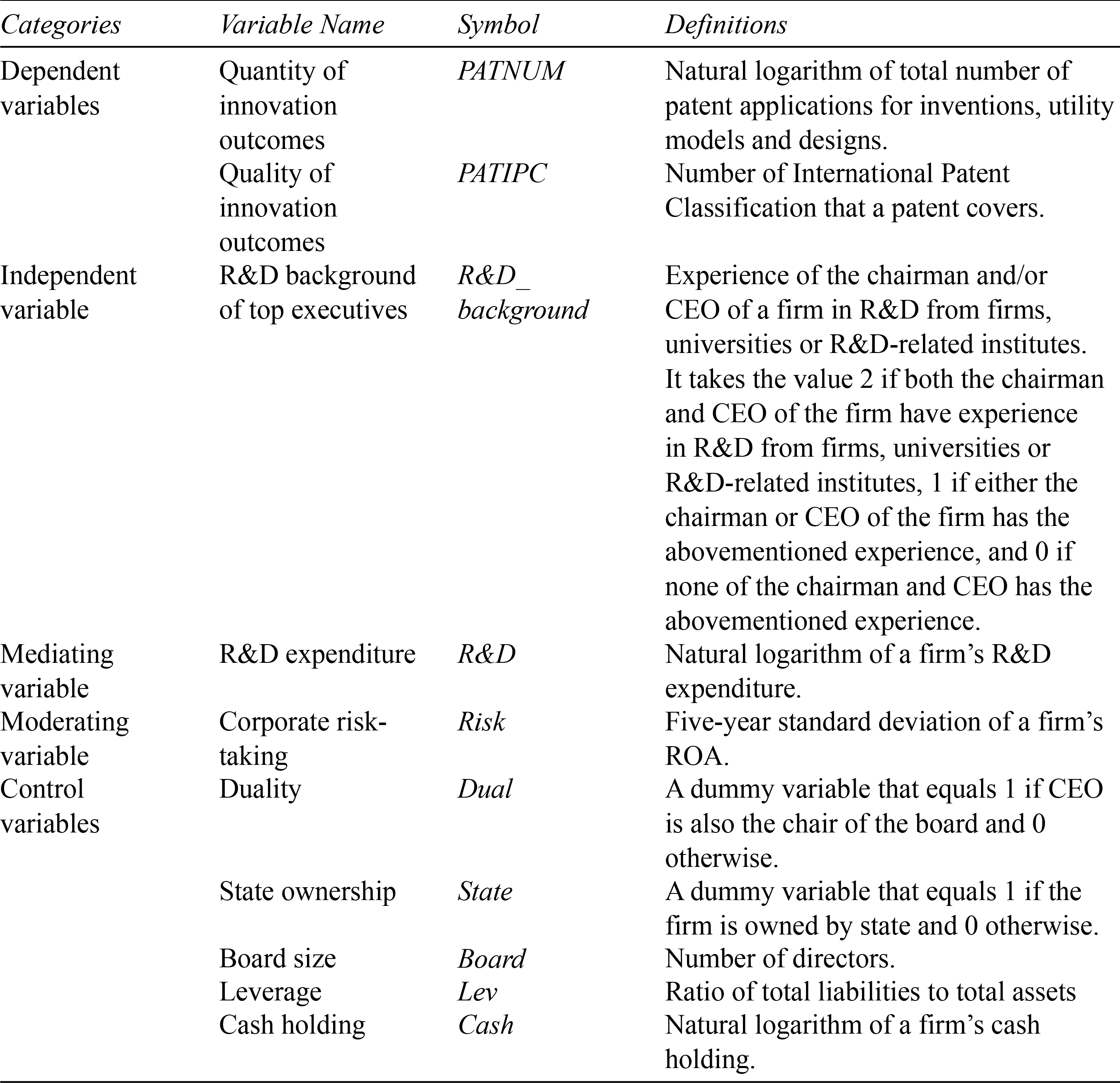

The dependent variable is measured by both the quantity and quality of innovation outcomes. Following Dosi et al. (2006) and Tan et al. (2014), among others, we use the number of patent applications to proxy for the quantity of innovation outcomes. One reason of using the number of patent applications rather than the number of granted patents is that patent grants are prone to bureaucratism (Tan et al., 2014). Following Fabry et al. (2006) and Hao et al. (2018) and given the availability of the patent data in China, we choose to use the number of International Patent Classification (IPC) that a patent covers to proxy for the quality of innovation outcomes. 9 Because a high number of IPC of a patent indicates that the innovation output tends to be more fundamental and generalisable, the higher the number of IPC, the higher the quality of innovation outcomes.

Following Daellenbach et al. (1999), among others, the independent variable in this study, that is, R&D background (R&D_background), is constructed based on the background of corporate top executives. Specifically, we manually check the resume of the top executives of a firm and assign to the variable the value 2 if both the chairman and CEO of the firm have experience in R&D from firms, universities or R&D-related institutes, 1 if either the chairman or CEO of the firm has the abovementioned experience, and 0 if none of the chairman and CEO has the abovementioned experience. For example, Mr Daokui Qu, who is the current CEO of Siasun Robot & Automation Co., Ltd. (stock code: 300024.SZ), first worked on robots in the State Key Laboratory of Robotics after he graduated from Shenyang Institute of Automation Chinese Academy of Sciences in 1986.

The mediator variable in this study is R&D expenditure (R&D). Following existing literature, R&D is measured as the natural logarithm of a firm’s R&D expenditure. As existing literature also uses R&D intensity, calculated as R&D expenditure divided by sales revenue, to proxy for R&D expenditure, we use R&D intensity as an alternative measure for R&D expenditure in a robustness test.

The moderator variable in this study is corporate risk-taking (Risk). Following Boubakri et al. (2013) and Faccio et al. (2011), Risk is measured as the five-year standard deviation of a firm’s return on assets (ROA). The underlying idea is that corporate high-risk decision making is full of uncertainty, which causes volatility in financial performance.

Following existing literature, this article includes a set of control variables, such as duality (Dual), state ownership (State), board size (Board), Leverage (Lev) and cash holdings (Cash). Detailed definitions of variables can be seen in Table 1.

Model Specifications

To test the effect of the R&D background of top executives on innovation outcomes, we specify the following panel data regression model:

where innovation_outcomes is measured by PATNUM and PATIPC and R&D background of top executives is represented by R&D background Given the potential endogeneity issue and the possibly lagged effect of R&D background on innovation_outcomes the main independent variable takes the lagged value.

Definitions of Main Variables

To test the mediating effect of R&D expenditure in the relationship between R&D background and innovation outcomes, we specify the following panel data regression model:

where R&D represents R&D expenditure.

To test the moderating effect of risk-taking on the relationship between top executives’ R&D background and R&D expenditure and further on the mediating role of R&D expenditure in the relationship between R&D background and innovation outcomes, we specify the following panel data regression model:

where Risk represents corporate risk-taking.

Note that the above models have passed the heteroscedasticity test. We further conduct the PSM test as part of the robustness tests to address the potential endogeneity concern. Firm and year fixed effects (FE) are also included.

Results

Descriptive Statistics

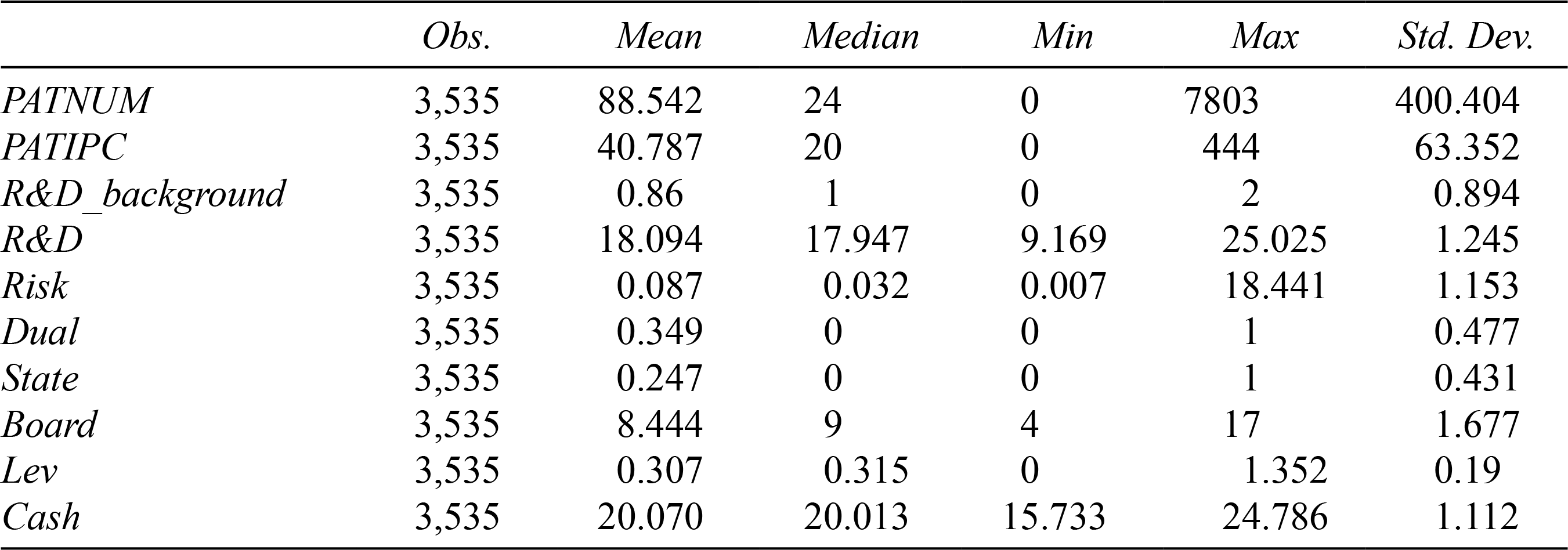

Table 2 presents the descriptive statistics of the main variables. The standard deviation of PATNUM is 400.404, indicating a high variation of the number of patent applications among the sample firms. This is not surprising because the number of patent applications of some firms, such as BOE Technology Group Co., Ltd. and TCL Technology Group Co., Ltd., can reach around 7,000 per year, whereas that of some firms is minimal. A similar pattern is found in PATIPC. R&D_background is 0.86 on average, indicating that top executives, including chairman and CEO, of a large proportion of our sample firms have R&D background. 10 This statistic highlights the importance of investigating the impact of R&D background on innovation outcomes in China. R&D, on average, is 18.094. This indicates that the average R&D expenditure of our sample firms is 72,131,399.01 RMB. Risk, which is measured as the five-year standard deviation of a firm’s ROA, is 0.087 on average.

Descriptive Statistics of Variables

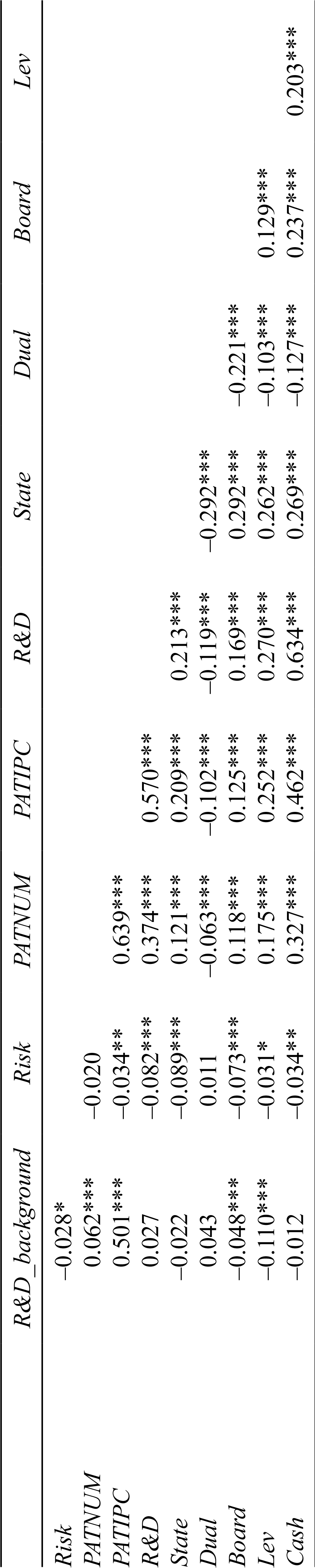

Table 3 presents the correlation coefficient between the key variables, which shows positive correlations between R&D background and innovation outcomes. This result provides preliminary evidence consistent with our hypothesis 1. We also conduct the correlation analysis between independent variable and control variables, which shows that the correlation coefficients and VIF are relatively small. This indicates that the multicollinearity problem is not a big concern.

Regression Results

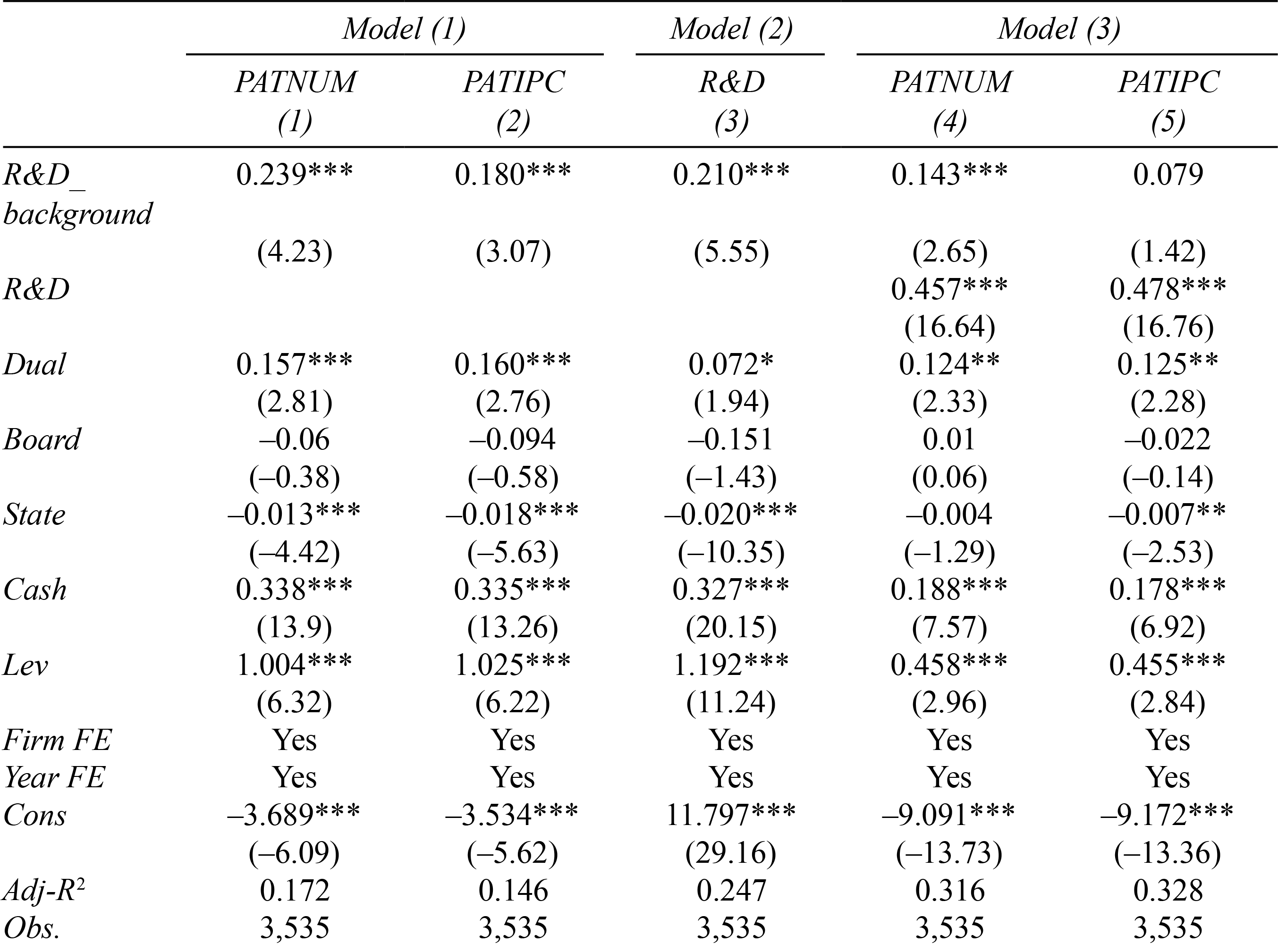

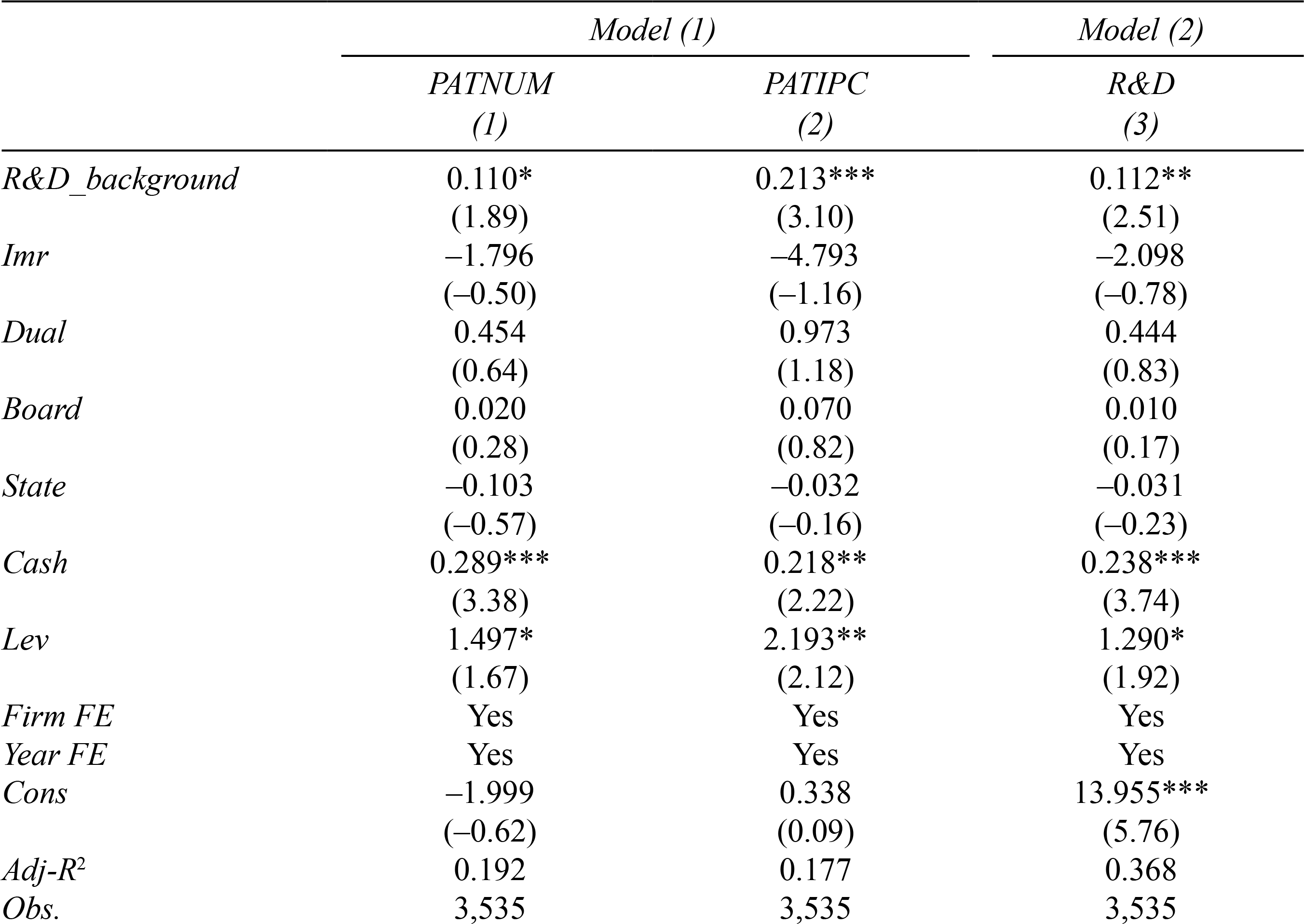

The FE panel regression is applied to Model (1) based on Hausman test. As shown in Columns (1) and (2) of Table 4, top executives’ R&D background has a significantly positive effect on both the quantity (PATNUM) and quality (PATIPC) of innovation outcomes. This result suggests that R&D background of top executives in a firm helps the firm increase its innovation outcomes. Therefore, Hypothesis 1 is supported.

Correlation Analysis

Column (3) of Table 4 reports a significantly positive effect of top executives’ R&D background on R&D expenditure, indicating that R&D background of top executives in a firm helps the firm increase its R&D expenditure. Hypothesis 2a is thus supported. Note that it is not surprising for high-technology firms to maintain their core competencies through consistently high R&D expenditure. However, by only selecting high-technology firms as a sample, our results show that top executives’ R&D background still exerts a positive effect on R&D expenditure among high-technology firms.

Model (3) incorporates both top executives’ R&D background and R&D expenditure to examine the mediating effect of R&D expenditure in the relationship between R&D background and innovation outcomes. Column (4) of Table 4 shows that the estimated coefficient of R&D_background is statistically significant, indicating that R&D expenditure plays a partial mediation role in the relationship between R&D background and the quantity of innovation outcomes. Column (5) of Table 4, however, presents a statistically insignificant estimated coefficient of R&D_background, indicating that R&D expenditure plays a full mediation role in the relationship between R&D background and the quality of innovation outcomes. The results support Hypothesis 2b, which suggests that R&D expenditure is one of the channels through which top executives’ R&D background affects innovation outcomes.

Effect of Top Executives’ R&D Background on Innovation Outcomes and the Mediating Effect of R&D Expenditure

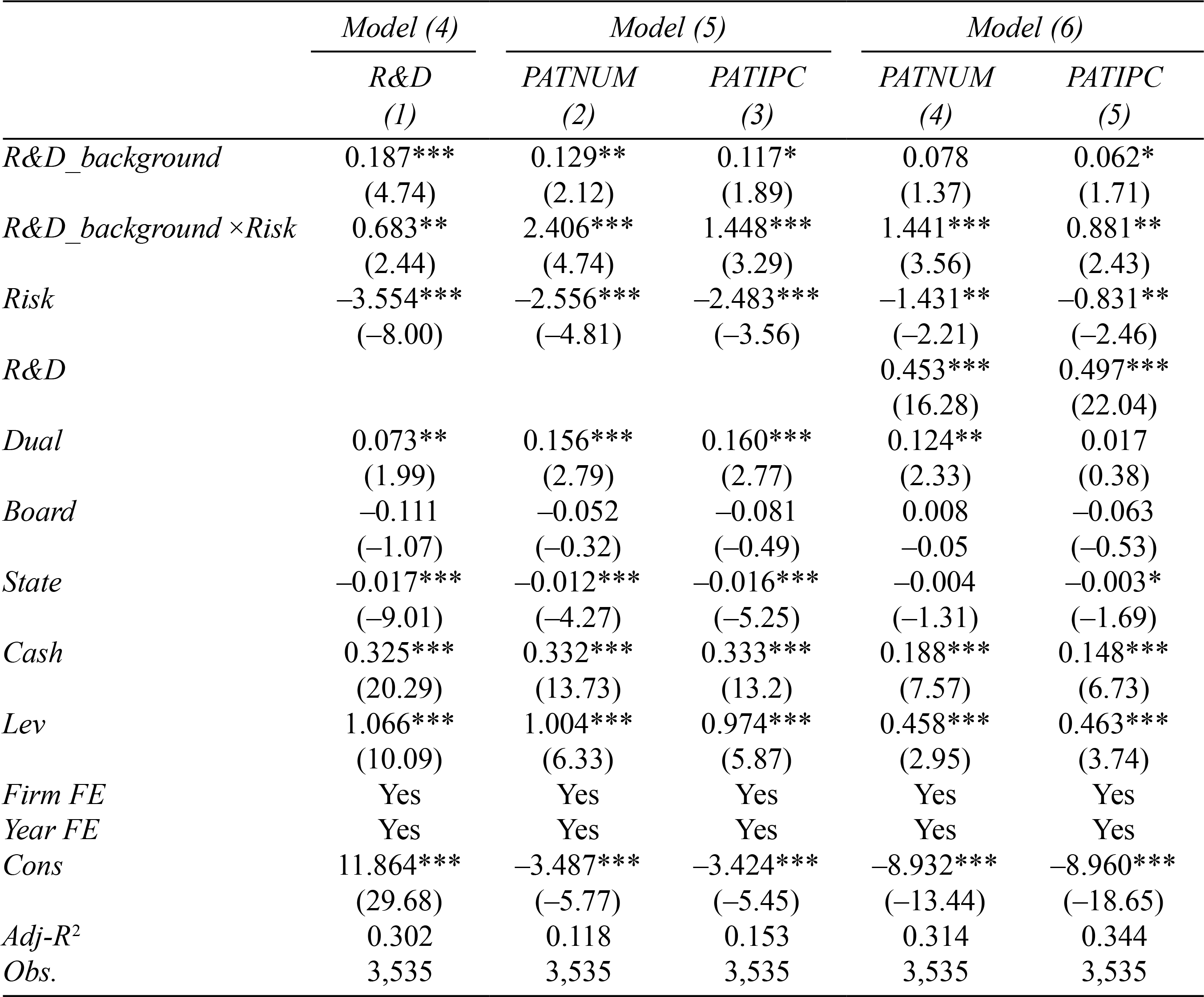

Table 5 reports the results on the moderating effect of risk-taking on the relationship between top executives’ R&D background and R&D expenditure and further on the mediating role of R&D expenditure in the relationship between R&D background and innovation outcomes. Column (1) of Table 5 shows that a firm’s risk-taking can have a diminishing effect on its R&D expenditure, but firms that have top executives with R&D background have promised higher R&D expenditure than those that do not have R&D-background top executives. This result suggests that top executives with R&D background exhibit risk preference attitude and tend to increase R&D expenditure to proactively deal with risk. Therefore, Hypothesis 3a is supported.

Moderated Mediating Effect of Risk-Taking

A similar result is shown in Columns (2) and (3) as that in Column (1), that is, although a firm’s risk-taking can have a diminishing effect on its innovation outcomes, firms that have top executives with R&D background have achieved better innovation outcomes than those that do not have R&D background top executives. The above result can be seen from the positive coefficient of the interaction term between R&D_background and Risk in Columns (2) and (3). Furthermore, the estimated coefficient of R&D expenditure (R&D) in Column (4) and (5) is positive. According to Wen and Ye (2014) and Wen et al. (2006), the above results all together indicate that the effect of top executives’ R&D background on innovation outcomes through R&D expenditure is more profound when risk-taking is high than that when risk-taking is low. In other words, the role of top executives’ R&D background of a firm is further important when the firm’s risk-taking is high in that R&D background of top executives help the firm achieve further innovation outcomes through increasing R&D expenditure. Therefore, a positive moderation effect of corporate risk-taking on the mediating role of R&D expenditure in the relationship between top executives’ R&D background and innovation outcomes, that is, a moderated mediating effect, is observed. Hypothesis 3b gets supported.

Robustness Tests

Endogeneity Caused by Unobservable Variables

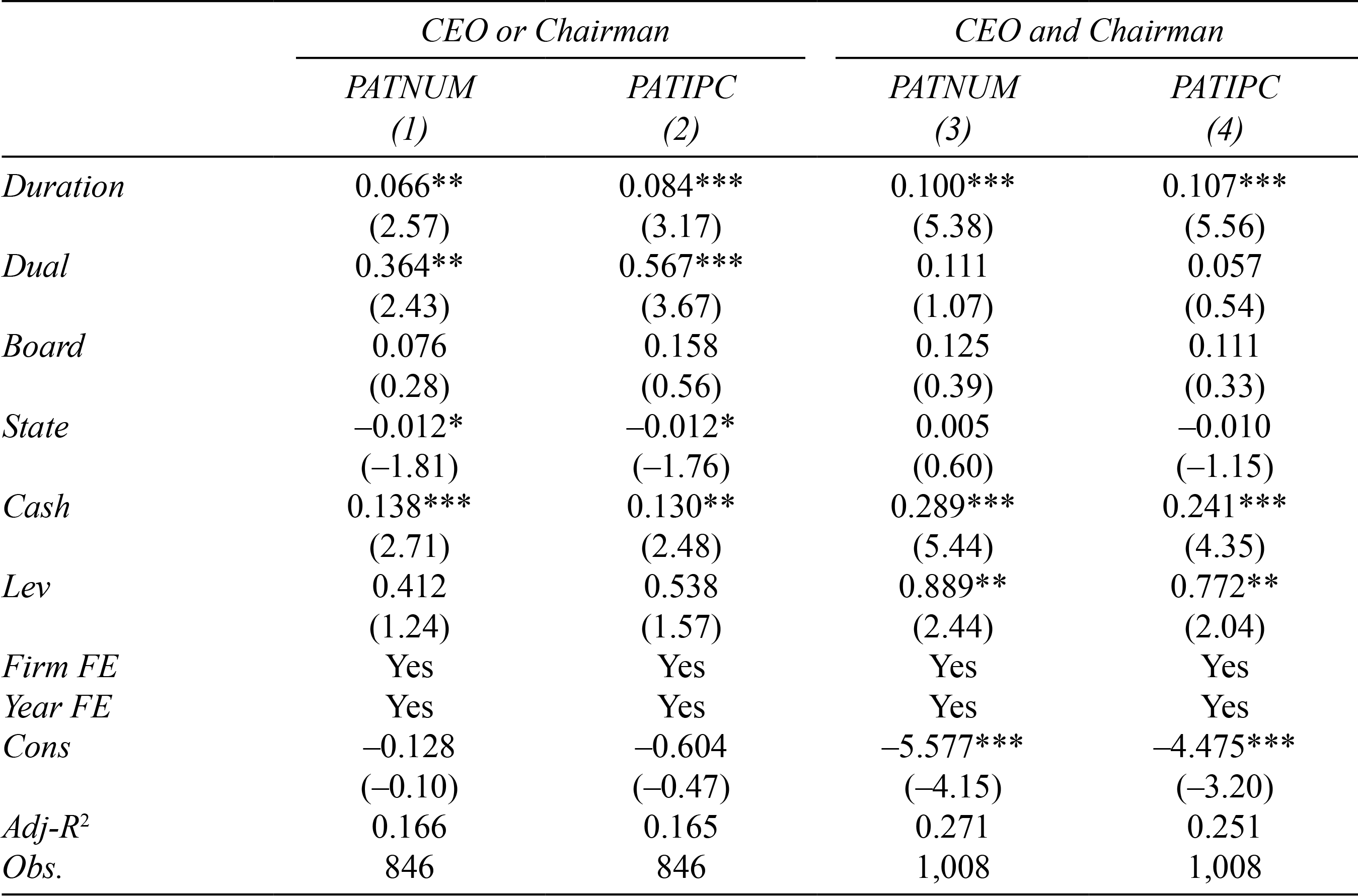

The positive correlation between top executives’ R&D background and innovation outcomes observed in our baseline results could be caused by unobservable variables that may also explain innovation outcomes. To address such as concern, we attempt to analyse variations among firms led by top executives with R&D background only. The underlying rationale is that if top executives’ R&D background does drive the above positive correlation, then this effect should be stronger for top executives with longer R&D experience. Hence, we use the duration of the R&D-related experience of top executives (Duration) as an alternative measure. Duration is measured as the natural logarithm of a top executive’ duration of R&D-related experience from the first year of their first R&D-related experience to the sample year. Columns (1) and (2) of Table 6 present the results, which show that the coefficients of Duration are positive and statistically significant at the 1 per cent level. This result indicates that the longer the R&D experience of the top executive (CEO or chairman) is, the better the innovation outcomes. We further explore whether the above impact is profound if both the CEO and chairman of a firm have R&D-related experience. In such cases, Duration of the firm is calculated as the average of the duration of CEO and chairman. Columns (3) and (4) of Table 6 show that the coefficients of Duration are not only positive and statistically significant but also bigger in magnitude than those in Columns (1) and (2). This result suggests that both CEO and chairman having R&D-related experience does strengthen the impact of such an experience on innovation outcomes.

Alternative Measure of R&D Background of Top Executives

Result of the PSM Test

Endogeneity Caused by Reverse Causality and/or Self-Selection

Given that the relationship between top executives’ R&D background and innovation outcomes may be endogenous in that innovation outcomes may cause firms to select top executives with R&D background (Chaganti & Sambharya, 1987; Datta & Guthrie, 1994; Thomas et al., 1991), we employ the PSM method to tackle the potential endogeneity issue. The results presented in Table 7 show that regardless of whichever matching tactic is used top executives’ R&D background significantly improves corporate R&D spending and innovation outcomes. Hence, our baseline results in Tables 4 and 5 are qualitatively unchanged.

We also employ the two-stage least squares (2SLS) approach to further address the potential endogeneity concern. More specifically, we use the industry mean of R&D intensity in the previous year as an instrumental variable to estimate the 2SLS model. F value in the first stage of the regression is above 10, indicating no evidence that our instrumental variable is weak. The second stage of the regression is presented in Table 8, which shows that our baseline results hold.

This study may be subject to endogeneity concern caused by selection bias in that our sample may have not been selected randomly (Antonakis et al., 2010). To address such a potential concern, we employ the Heckman two-stage model. To illustrate, we introduce the industry mean of R&D expenditure in the previous year at the first stage of the regression. The inverse Mills ratio (Imr) generated from the first stage is not significantly associated with innovation outputs and R&D expenditure in the second stage (see details in Table 9). The overall results show that our baseline results remain constant after addressing endogeneity.

Other Robustness Tests 11

We also do some other robustness tests to further ensure the robustness of our results. Specifically, we use an alternative measure of R&D expenditure, that is, the ratio of R&D expenditure to sales revenue. We also use the natural logarithm of the number of patent applications for inventions only as an alternative measure of the quantity of innovation outcomes. The results of these robustness tests show that our baseline results largely remain constant.

Result of the 2SLS Regression (the Second Stage)

Conclusions and Discussions

Given the important but yet underexplored role of R&D background of top executives played in corporate R&D and innovation practices, this study uses a sample of listed firms in the high-technology industries in China over the period of 2012–2017 to investigate the impact of top executives’ R&D background on corporate innovation outcomes and further examine the mediating effect of R&D spending and moderating effect of risk-taking on the above relationship. We find that R&D background of top executives is positively associated with innovation outcomes. We also find that top executives’ R&D background affects innovation outcomes via R&D expenditure, which plays a mediating role in the R&D background-innovation relationship. Moreover, we find that the effect of top executives’ R&D background on innovation outcomes through R&D expenditure is further profound when risk-taking is high, that is, the moderating effect of corporate risk-taking.

Result of the Heckman Two-Stage Model Test (the Second Stage)

Our findings support the positive role played by top executives’ R&D background in enhancing corporate innovation outcomes. This may help explain the thrive of the high-technology industries in China and the increasingly strong position of China as an emerging global innovation leader. Moreover, our study reveals that the positive contribution abovementioned is achieved through the willingness and capacity of top executives with R&D background to ensure R&D spending especially when corporate risk-taking is high. Findings of our study have important implications for firms that aim to enhance their innovation outcomes. First, high-technology firms need to optimise their structure of top executives to allow for the increase of the voice and power of top executives with R&D background when setting up and implementing their innovation strategies. Second, firms need to develop the organisational culture to promote tolerance for failure and proactively respond to risks. Our findings also have implications for countries, especially developing countries, regarding their research policymaking and R&D management (Hwang et al., 2017). To illustrate, on a macro level, the government in developing countries may make policies to create an environment where innovation activities are encouraged and supported. On a micro level, firms may introduce incentives to attract executives with R&D background and tolerate failure.

Although we examine the consequences of top executives’ R&D background, we do not study the antecedents of top executives’ R&D background, that is, why and how technocrats become top management, which calls for future research. The extremely small size of the sample where non-R&D-background top executives become R&D-background top executives during our sample period does not allow us to conduct a difference-in-difference (DID) test as an alternative way to address the potential endogeneity concern. Future research may consider doing such a test when sufficient data are available. Moreover, although our primary focus is R&D investments as the mediating factor and corporate risk-taking as the moderating factor, which are arguably the most important factors that affect innovation particularly for high-technology firms, we do recognise the possibility of other channels and moderators, such as emotional support, organisational culture, top executive networks and so on. Future research may continue to explore the impact of these possible factors on innovation when data are available.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

This project supported by the National Natural Science Foundation of China (71702006, 71802010), High-level Teachers in Beijing Municipal Universities in the Period of 13th Five-year Plan (CIT&TCD201904035, CIT&TCD201904031)