Abstract

With a growing number of nations pursuing the Sustainable Development Goals and increasing their disclosure and reporting norms, Socially Responsible Investing (SRI) is an evolving strategy in developing countries whilst holding mainstream grounds in developed countries. The study examined the performance of SRI indices against their conventional and benchmark counterparts across select developing and developed countries during boom and recessionary periods over 14 years. Notably, the responsible indices in emerging countries are non-penalizing using the mean-variance and risk-adjusted return analysis. Similarly, SRI earned a premium in emerging countries to secure topmost ranks, using Fama’s decomposition model. The performance of SRI was significantly different in India, and abnormal returns were observed for select developing countries during the recessionary phase. Thus, SRI provides a safe haven to investors during adverse times and provides diversification benefits to responsible investors.

Introduction

Evaluating the performance of socially responsible investing (SRI) has been the subject of extant research, as more than $35.3 trillion are engaged in responsible assets worldwide (GSIA, 2018). The term could be defined as an approach to financial decision-making, which screens the investments for environmental, social, and governance (ESG) concerns. This manifold increase in SRI could be attributed to factors including climate change, inequality, terrorism, labour issues, and so on, influencing stakeholders to raise stakes in organizations fostering sustainable growth along with the pursuit of financial objectives (Zuckerman et al., 2016).

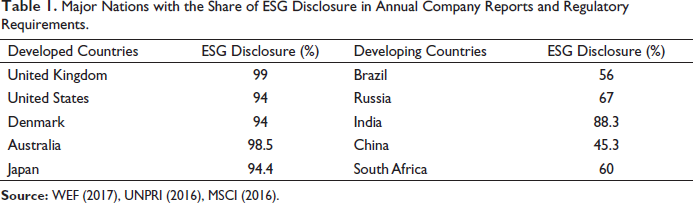

The concentration of global SRI assets remained in major developed countries due to regulatory interventions, healthy infrastructure, and mature financial markets (Vives & Wadhwa, 2012). The penetration of SRI in such developed countries is backed by regulatory norms on disclosure provisions and consistent corporate reporting (OECD, 2019). On the other hand, emerging-market investors remain sceptical due to factors such as insufficient data, an inconsistent ESG disclosure, 1 mechanism, 2 a naive investor base, an inadequate market infrastructure for supporting knowledge development, 3 or lack of experience, despite the huge potential for the advancement of SRI 4 (refer Table 1). Meanwhile, the modern portfolio theory (MPT) also assumes that the ultimate motive of a rational investor is to maximize their return. Thus, in this backdrop, the present article is an attempt to investigate whether the mainstreaming is driven by a superior performance of SRI in developed countries or simply due to greater disclosures reducing the information asymmetry, to identify whether the growth of SRI in developing countries crippling due to an underperformance of SRI in these countries and finally, the article seeks to answer if the SRI in developed countries outperform the SRI in developing economies.

Major Nations with the Share of ESG Disclosure in Annual Company Reports and Regulatory Requirements.

Notably, developed countries, with higher disclosures and reporting trends (as in Table 1), observe mainstreaming of the SRI phenomenon.

The study contributes to current literature in a significant manner. The focus of this article is on SRI performance evaluation as well as comparison in selecting developed and developing countries because a financial market phenomenon found in developed countries may have different implications and impact in developing countries. The study is unique to have been carried out using index database, isolating the impact of biases associated with funds (timing, operating cost, skill, and management) (Belghitar et al., 2014; Sauer, 1997; Schröder, 2007; Statman, 2000, 2006). Furthermore, the period between 2007 and 2022 highlights the inflection of SRI in select countries through economic conditions. To assess the performance of SRI indices, this article has engaged various traditional and risk-adjusted performance measures. Finally, the study presents a contrast of SRI performance with the conventional and broadmarket benchmarks in the select countries, which, to the authors’ best knowledge, have not been previously carried out.

For the analysis, the countries of the United States and United Kingdom are used as proxies of developed countries. The countries are economic superpowers having highly developed and penetrated financial markets SRI investing has evolved to be a mainstream investing strategy in these countries, supported by strong regulations, a mature investor base, and corporate volunteering. We study the economies of India and China, which are BRICS constituents and developing countries. The rest of the article proceeds as follows. In the subsequent section, we review the existing literature on both developed and developing markets. Section 3 discusses the data and methodology, whilst Section 4 discusses the empirical results. The last section discusses the findings, and the conclusion is summarized.

Literature Review

Socially responsible activities have their roots in society from age-old times (Renneboog et al., 2008) and have been practised by religious groups (Hussein & Omran, 2005). More recently, the religious screens became more holistic and expanded in the wake of social issues like apartheid, Chernobyl and Exxon disaster, the Vietnam War and the financial crisis (Gregory et al., 1997).

Globally, the SRI market has grown from a niche to a mainstream activity (Fowler & Hope, 2007). Extant literature exists studying the SRI in developed countries, comparing the performance of SRI against their conventional counterparts. The evaluation is carried out using various regression techniques and traditional and risk-adjusted return methods to test the under or outperformance of SRI instruments.

Hamilton et al. (1993) establishes the ‘no difference’ hypothesis, proposing that SRI neither underperforms nor outperforms the market counterparts. The majority of researchers found no significant difference in the performance of SRI (Bauer et al., 2004; Guerard, 1997; Luther & Matatko, 1994; Plantinga et al., 2008; Schröder, 2007; Von Wallis & Klein, 2015). This implies greater linkage of SRI to the conventional benchmarks movement through bull and bear (Shunsuke et al., 2012).

The second hypothesis by Hamilton et al. (1993) expects lower returns from SRI screening due to the reduction of diversification benefits (Markowitz, 1952). Adler and Kritzman (2008) and Belghitar et al. (2014) found evidence of SRI underperforming the conventional benchmarks due to a ‘cost of screening’ associated with SRI. As per the MPT (Markowitz, 1952), diversification reduces risk and maximizes long-term returns. SRI also imposes higher systematic and beta risk due to concentration of ESG in specific sectors only (Collison et al., 2008; Mill, 2006; Ortas et al., 2012; Ur Rehman et al., 2016). The higher risk can also be attributed to inconsistent ESG disclosures, inadequate regulations, especially in developing countries (Srinivasan, 2014; Tripathi & Bhandari, 2014; Ur Rehman et al., 2016). The concentration of SRI in certain sectors and industries or screening of other industries causes higher systematic risk and sensitivity (Collison et al., 2008; Mill, 2006; Ortas et al., 2012; Ur Rehman et al., 2016).

In line with the third hypothesis by Hamilton et al. (1993), extant literature also finds SRI outperforming the conventional investments (Collison et al., 2008; Curto & Vital, 2014; Hill et al., 2007; Hume & Larkin, 2008) due to mispricing of SRI securities (Barnett and Solomon, 2006; CapelleBlancard & Monjon, 2012; Hoepner & McMillan, 2009; Konar & Cohen, 2001; Kurtz 1997, 2005; Renneboog et al., 2008). However, because of screening out the ‘irresponsible firms’, SRI brings greater reliability to firms, ensuring ethical management practices and reducing externalities’ costs. Gregory et al. (1997), Guerard (1997), Goldryer and Diltz (1999), Mill (2006), and Schröder (2007) found that SRI acted as a financial safe haven during falling markets and even had higher cash flows into these funds, thus, supporting the ‘doing good whilst doing well’ hypothesis (Nofsinger & Varma, 2014; Parida & Wang, 2018; Paul, 2017).

A few studies studied SRI through the market-condition perspective, giving an insight into the conditional performance of the funds/indices. Previous studies have analyzed this question with different result. In contrast, Statman (2006), Hume and Larkin (2008), Managi et al. (2012), and Wei (2018) found SRI to be outperforming during the boom but underperforming the counterparts during falling markets. Furthermore, studies also found SRI rewarding investors with positive excess returns during the crisis period, encouraging higher money inflows towards relatively refuging funds (Nofsinger & Verma, 2012; Palma-Ruiz et al., 2020; Parida & Wang, 2018; Paul, 2018).

Few studies in the past have been carried out investigating the relationship between ESG disclosure and positive firm performance, stimulating the growth of SRI. Countries with regulatory ESG disclosure frameworks have better MSCI ESG Rating scores than those without, indicating better ESG risk management practices relative to risk exposure; the positive relationship between ESG disclosure and corporate ESG performance (UNPRI, 2016). Sehgal et al. (2022) found that sustainability disclosure positively affects the ROA/ROE in the long run. Roy (2019) cautioned investors to investigate whether the SRI indices really maintain ESG factors or not and do they disclose the impact on financial performances. According to Ahmad et al. (2021), results confirm that high ESG firms show high financial performance as compared to low ESG firms. Empirical investigation finds the firms listed in the ESG index to be having a higher firm value whilst exhibiting a positive correlation between firms’ higher rankings in the index and firm value (Aboud & Diab, 2018). Investigating the developing country of India, Sharma et al. (2019) found social disclosure to be having a significant positive impact on firms’ financial performance. Furthermore, the larger firms used this social performance as a competitive advantage.

ESG disclosures and SRI are indispensable to each other. Beck et al. (2018), Reverte (2012), and Bayoud et al. (2012) find that ESG reporting enhances firm value by decreasing information asymmetries between managers and investors regarding the environmental, social, and governance concerns. This further reduces the cost of equity attracting social investor. Sampong et al. (2018) found a positive and statistically significant relationship between social disclosure performance and firm value whilst Verbeeten et al. (2016) find that ESG disclosures are value-relevant for investor in Germany, seeking to invest consciously. Cahan et al. (2016) observe a positive relation between CSR disclosure and firm value measured by Tobin’s Q in 21 European countries. Thus, a positive relationship exists between ESG disclosures and responsible investor interest.

Cohen et al. (2011) find that investors value governance and CSR information and express their interest in investing in such corporations those disclose on these parameters, thus reiterating the focus of social responsibility investor on ESG disclosure. Hsu et al. (2019) finds that firms with adverse ESG performance observe lower disclosure quality, thus falling in consistency with preference of SRI investors towards ESG disclosures.

SRI in Emerging and Developed Economies

Different SRI markets give rise to heterogeneity of the results obtained (Sandberg et al., 2009). The geographical areas studied by various authors are diverse (Benijts, 2010), and difference in practice as well as performance of SRI was observed across different regions (López-Arceiz et al., 2018; Louche & Lydenberg, 2006). The financial performance of SRI varies with geography, time and screens used, across global continents (Arjaliès, 2010; Badía et al., 2020; Ortas et al., 2012).

Scant literature exists reflecting on SRI performance and its contrast in emerging and developed economies. The research in developing countries is hindered by lack of consistent data, naive investors, inadequate infrastructure, policy lags, and so on. Hill et al. (2007) carried out a cross-regional comparison of SRI performance, as they found SRI in American, European, and Asian markets beating the benchmark in the long run. It is observed that the high performance of the SRI in Asian economies is offset by higher volatility of returns, which draws from relatively mediocre market development, information asymmetry, and weak ESG frameworks in emerging markets (Hill et al., 2007; Tripathi & Kaur, 2020a, 2020b; Ur Rehman et al., 2016; Weber, 2014). In another cross-regional study evaluating 23 SRI mutual funds against benchmarks, the SRI was found to be a winning strategy across Europe, Australasia, and Asia Travers (1997).

Thus, a review of the performance of SRI implies inconclusive results. It also highlights a gap in SRI literature in emerging countries, where ESG disclosures and reporting are nascent (Williams, 2010).

Research Methodology

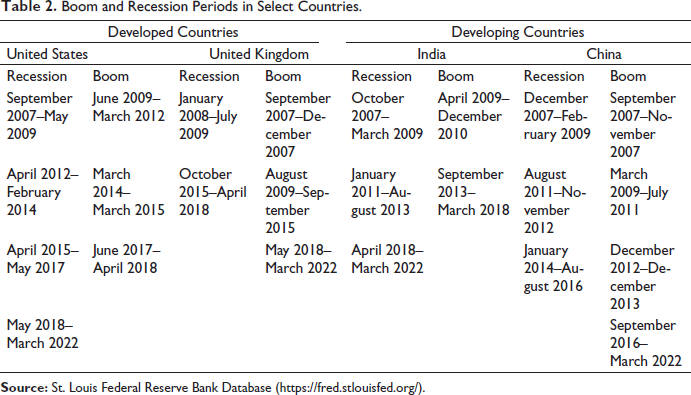

Through this study, the performance of SRI in select emerging and developed economies is carried out through period from 1 September 2007 to 31 March 2022. The data are taken from the inception of these indices. The study period is further segregated into boom and recession markets to study the impact of economic conditions on the performance of SRI in select countries. The economic conditions have been identified from the St. Louis Federal Reserve Bank Database (Table 2).

Boom and Recession Periods in Select Countries.

The closing monthly index values data were derived in dollar currency terms from

The data for SRI were taken from the MSCI ESG leaders’ index series, which were used as proxies for socially responsible investment indices for the study. The study uses the ESG leaders proxies for socially responsible investing indices due to the non-availability of sufficient historical index data under the SRI theme of investing for the select countries. The index undertakes best-in-class screening using the UN, ILO, UNGC codes and benchmarks. MSCI country index represents conventional investing style with constituent representation of about 85 per cent of the free float-adjusted market capitalization in respective countries. The broad market-specific MSCI Investable Market Indices proxies the benchmark index in our study, representing the investable universe.

For performance evaluation of select indices, we extract 91 days t-bills bond rate used for risk-free rate of return. We use descriptive statistics as well as traditional mean-variance techniques to find the characteristics of the dataset.

Performance Evaluation of Sustainable Indices Vis-à-vis Market Indices

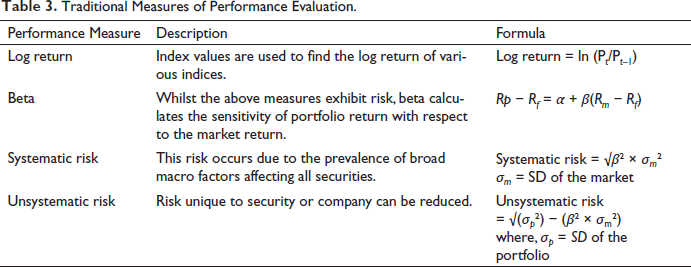

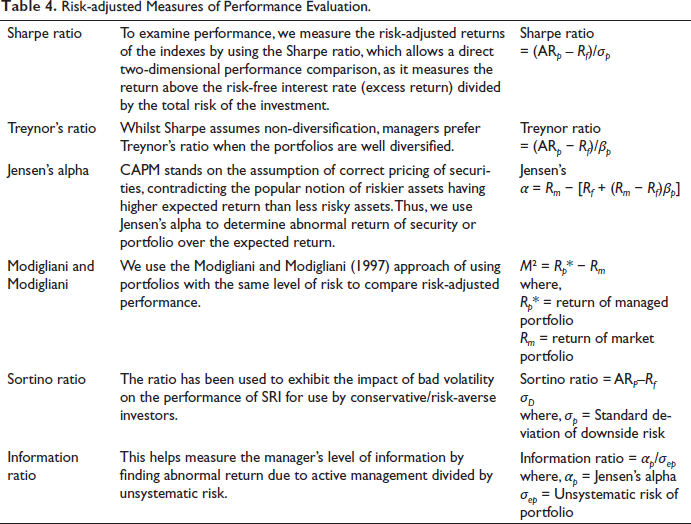

The series are evaluated using traditional and risk-adjusted measures of financial performance that are evaluated for all the indexes. The performance is measured using risk-adjusted evaluation measures, as the MPT assumes reduction of diversification benefits with the screening of investable universe. Hence, we follow these risk-adjusted evaluation technique used by Luther and Matako (1992), Belghitar et al. (2014), Statman (2006) and Consolandi et al. (2009), which helps measure performance, volatility, index alignment and quality and have been widely used in the extant literature (Hornuf Yüksel, 2022; Renneboog et al., 2008). As the literature finds inconclusive results of performance comparison between SRI and conventional counterparts, the authors further used Fama’s decomposition measure (Fama, 1972) to evaluate the portfolios ordinally and decompose the returns at different risk levels. CAPM-based market model regression helps analyze the impact of economic conditions on the excess returns (Tripathi & Bhandari, 2014; Tables 3 and 4).

Traditional Measures of Performance Evaluation.

Risk-adjusted Measures of Performance Evaluation.

Fama’s Decomposition Measure

The Fama’s performance measures evaluate the portfolios ordinally and decompose the returns at different risk levels. The risk premium can be divided into systematic and unsystematic risk whereas return from pure stock selectivity (R3) is the difference between the actual return and the sum of the other risk components.

…. Reward for systematic risk (R1) = βP (Rm − Rf)

Reward for unsystematic risk (R2) = [(σP / σm ) – βp ] × ( Rm – Rf)

Fama’s net selectivity (R3) = RP – [Rf + (σP / σm) × ( Rm – Rf)]

Total return on Portfolio = Rf + R1 + R2 + R3

Regression Analysis Using Dummy Variable

The use of single factor alpha is used to measure the sustainability risk, as the CAPM-based market model best estimates the vulnerability to market return of sustainability stocks. CAPM helps describe the relationship between systematic risk and expected return for assets. The model is as follows:

RP − Rf = α0 + α1D + β0(Rm − Rf) + β1D(Rm − Rf) α0 = Excess return for the recessionary period α0 + α1 = Excess return for Boom period β0 = Slope of Rp in recessionary period β0 + β1 = Slope of Rp in Boom period D = Dummy variable assuming value 0 for recession and 1 for the boom

Empirical Results and Discussion

Descriptive Statistics

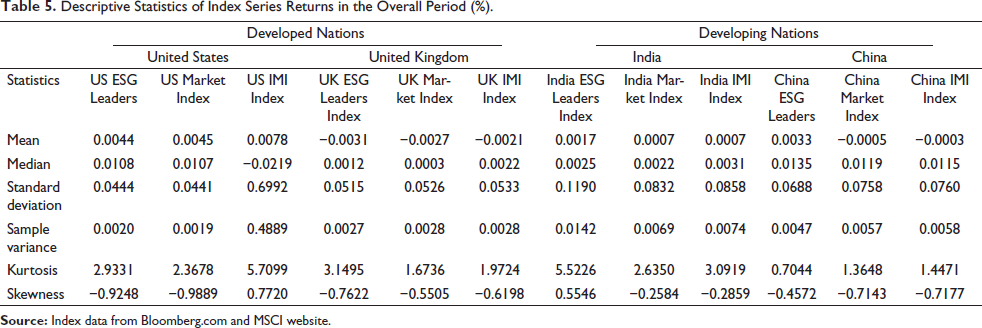

Exploring the descriptive statistics of the series, mean returns of SRI in the United States and the United Kingdom were found to be lesser than the conventional as well as market indices, implying SRI lagging in developed countries. SRI in the emerging countries, on the other hand, beat the conventional and market. We use higher moments of mean-variance analysis to examine the skewness in returns of the indices, where it was found that SRI was lowest in economies of the United States and the United Kingdom. Literature finds investors inclining towards greater skewness and lesser kurtosis (Belghitar et al., 2014), skewness for India’s ESG index is observed to beat the benchmarks by a significant margin. Kurtosis measure of tail distribution was observably high in the United Kingdom and India, whilst it remained low for countries of the United States and China (Table 5).

Descriptive Statistics of Index Series Returns in the Overall Period (%).

Performance Evaluation

Performance Evaluation During Boom

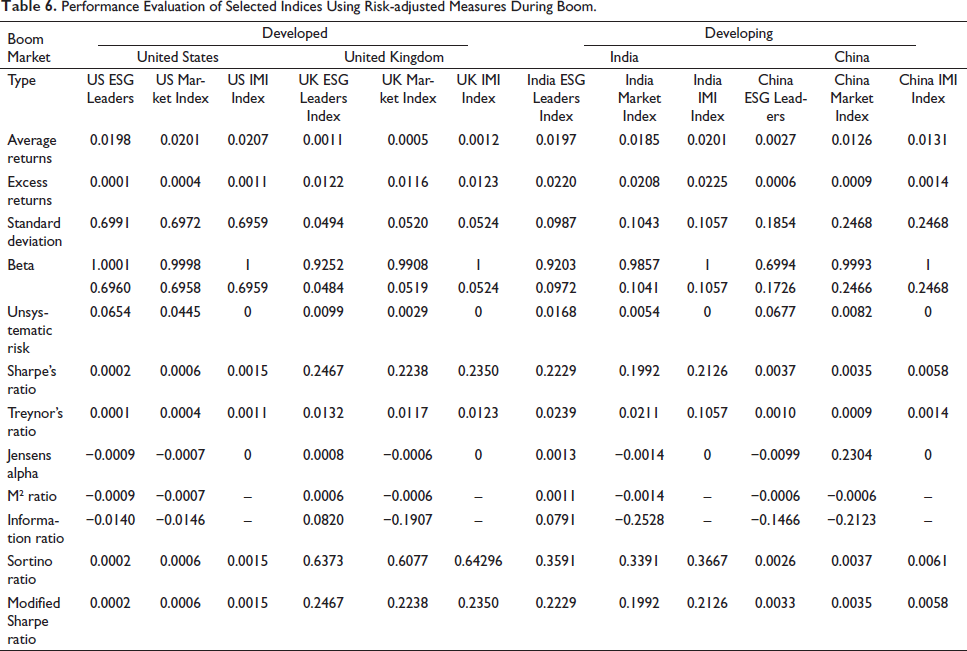

During the recorded period of boom (Table 6), the average and excess return measures indicate SRI index outperforming the conventional in the United Kingdom and India whilst underperforming both benchmark and conventional index in the economies of the United States and China. In contrast to the MPT, the risk remained lower for the screened indices than the unscreened counterparts. The SRI index of both the developing countries and the United Kingdom outperforms the conventional counterparts. The SRI in India, China and the United Kingdom exhibits rewarding results using the Sharpe ratio. The developed country of the United Kingdom shows similar performance, beating both the benchmark and the market index. The developing country of China has the least sensitivity to the market, measured using beta and systematic risk. In the boom period, excess returns were positive and highest for the SRI index in both India and the United Kingdom, whilst they remained negative for countries of the United States and China. Notably, the SRI investor is rewarded premium in developing countries of India and developed countries of the United Kingdom. The M² performance evaluation measure, too, generates positive rewards in these countries. A higher information and Sortino ratio of the SRI in the United Kingdom and India imply higher rewards for SRI.

Performance Evaluation of Selected Indices Using Risk-adjusted Measures During Boom.

Performance Evaluation During Recession

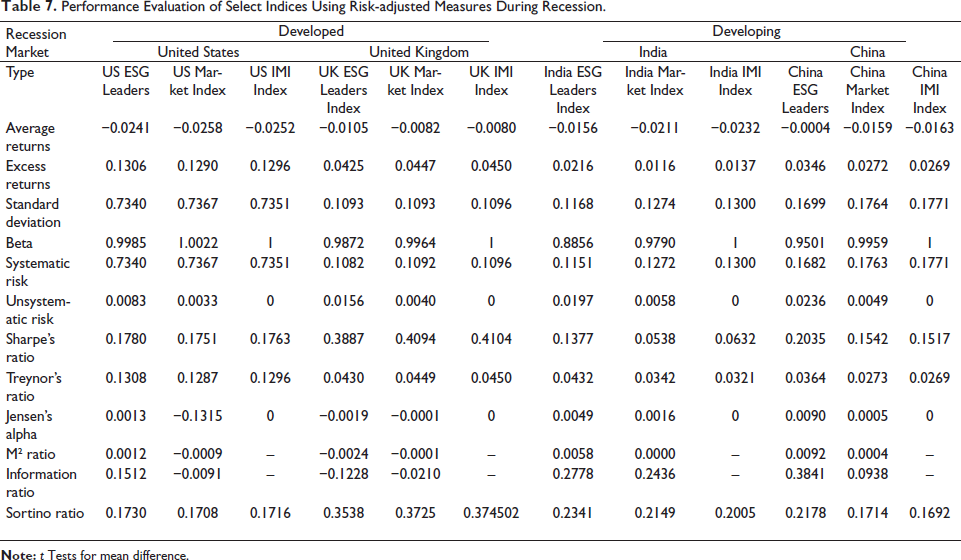

Through the recession, we use various traditional and risk-adjusted performance measures to examine the performance of SRI in select countries. A look (Table 7) at the returns reveals SR indices to be beating the counterparts in all the select countries. The superior performance of SR was not offset by high risk, and the standard deviation, beta, and systematic risk were lowest across the select countries. Lower beta implies less sensitivity of bearish market movement in SRI portfolio. A consistently high unsystematic risk suggests a greater need for diversification in SRI. The ESG index beat the counterparts when measured using Sharpe’s ratio, and Treynor’s ratio in all the select countries, except the United Kingdom. These risk-adjusted performance measures suggest positive reward to the responsible investor for every unit of risk undertaken.

Performance Evaluation of Select Indices Using Risk-adjusted Measures During Recession.

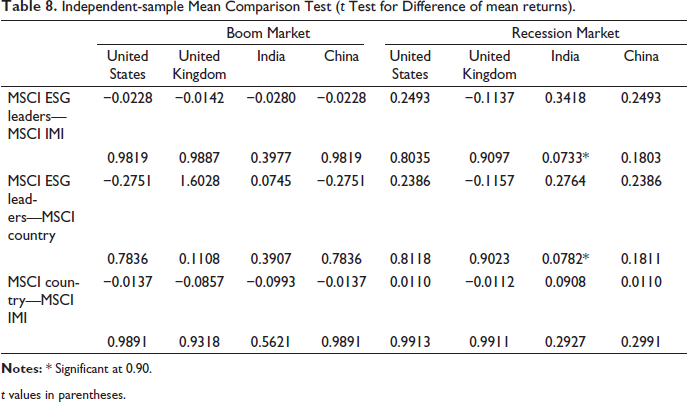

To test the significance of difference in mean of index returns across economic conditions, independent-sample t-tests were used (Table 8). During the economic condition of the boom, none of the countries witnessed significantly different mean returns from the general market or the broad market index. The SRI strategy failed to generate significant premiums during the expansionary periods but was not penalized as compared to the unscreened universe of stocks. Thus, the investors across developed and developing countries were equitably rewarded for pursuing their ethical and social investing orientations.

Independent-sample Mean Comparison Test (t Test for Difference of mean returns).

t values in parentheses.

We observe a significant difference between the mean returns of the India ESG index and its counterparts during the recession, implying a refuge to the SRI. There is no significant difference in the performance of SRI, the general and the benchmark index in the United States, the United Kingdom and China, resorting to sustainable investing strategy doesn’t penalize the investor in the selected countries.

Fama’s Decomposition Net Selectivity Measurement in Economic Condition

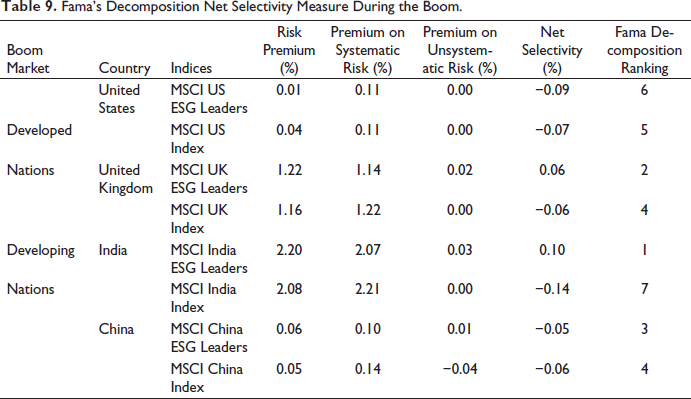

For the jubilant times of boom (Table 9), the SRI index in the developing country of India topped the Fama decomposition ranking by rewarding the conscious investor maximum in terms of positive net selectivity. SRI followed the superior rewards in developing countries in developed countries of the United Kingdom, which too managed positive net selectivity rewards. Notably, both the countries rewarded investors for the non-diversification of SRI portfolio. India notably earned maximum premiums for systematic risk for all select indices. For the developed country of the United States, SRI ranked lower than the counterparts in other nations, incurring a penalty for screening.

Fama’s Decomposition Net Selectivity Measure During the Boom.

Thus, as the market rode on highs of the expansionary phase, SRI investing was most rewarding in terms of stock selection in countries of India, the United Kingdom and China. Meanwhile, conventional stocks underperformed in the select countries so did SRI in the developed country of United States (Table 10).

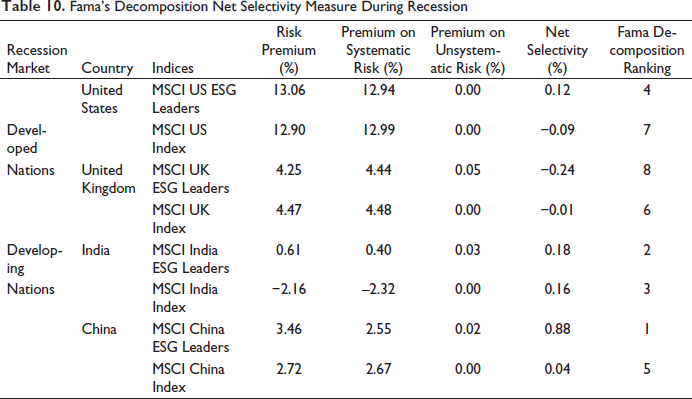

Fama’s Decomposition Net Selectivity Measure During Recession

SRI witnessed an outstanding reward during distressed market conditions, as the screened investments generated significantly higher net selection benefit for selection and commitment to socially inclined stocks than the conventional market. During the recessionary phase, the Chinese responsible investing developed the highest compensation for stock-picking risk, followed by ESG investing in India. Thus, SRI in both the developing countries has been most rewarding during market depressions, where the SRI investing ranks above conventional investing in terms of stock selection order. Notably, in the developing countries, the difference in compensation of the SRI index from the risk of stock selection is very pronounced, relative to the marginal compensations produced by the conventional index. Thus, markets brought rewards to screening investors for their stock-picking abilities and compensation for their socially conscious outlook. The ranking of SRI on stock selectivity measures highlights evidence of doing well whilst doing good during stressed times of the market.

Market Model on Select Indices in Developing and Developed Countries

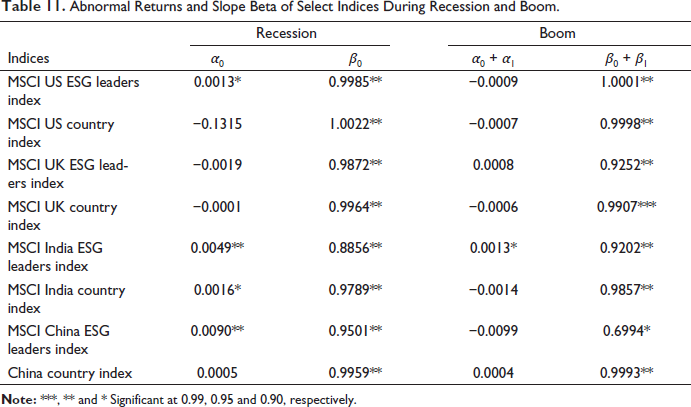

Table 11 shows the results of a dummy variable regression model to check the impact of business cycles (boom and recession) on the parameters of the market model.

Abnormal Returns and Slope Beta of Select Indices During Recession and Boom.

The alpha value of the socially responsible index in the developing country of India was positive and significant during the boom period. ESG index in India generated the highest excess return of 0.13 per cent per month. This highlights the prevalence of factors other than market risk premium inducing the portfolio return of SRI investor in India during the boom period. None of the portfolios is generating significant alpha value during the boom period (except India ESG Leaders Index) as security prices of stocks fell drastically in all countries other than the United Kingdom and India. As per MPT, the slope is significant for all the eight indices in select developed and developing countries; boom has a significant positive impact on the return of these portfolios. For the recessionary phase, SRI investors in the United States, India and China earn positive and significant excess returns. ESG China index is generating the highest excess return of 0.9 per cent per month.

During adversity, investors in emerging countries put more faith in socially responsible companies, and as a result, the impact of the recession is observed to be positive in the case of SRI indices. However, alpha values for the general stock indices in developed countries were negative and insignificant during the said period because the security prices of general companies had fallen severely; only India’s general stock index is generating significant alpha value during the recession period.

Conclusion

This study successfully investigated the performance of SRI and market counterparts for the time 2007–2022 using various traditional and risk-adjusted performances. The study analyses the performance in sub-periods of boom and recession in select countries of the United States, the United Kingdom, India and China.

Discussing the performance of SRI, the results of risk-adjusted performance measures contradict as observed by Statman (2006) and Hume and Larkin (2008) in the United States, indicating outperformance by SRI during the boom phase. The difference in observation may be caused by the difference in the management of funds, which were used in the literature. For the United Kingdom, our results are in line with Consolandi et al. (2009) and Charles et al. (2016) who observe a higher risk but no significant penalty for holding SRI portfolio across economic conditions. As found by Srinivasan (2014) and Tripathi and Kaur (2022), India managed to outperform its market counterparts using risk-adjusted performance measures. Whilst none of the select indices beat market counterparts in boom periods, we found that the performance of SRI India significantly outperforms the general and market index during the recessionary market.

The developing countries of India and China secured top position in Fama’s decomposition ranking method according to reward for net selectivity in both boom and recessionary periods. Regression using market-condition dummies reinstated the developing market rewards over developed economies, where the emerging economies of India and China earned significant positive excess returns. The abnormal returns may be assumed a result of mispricing, resulting from larger number of conventional investors resorting to SRI for seeking sustainable and stable earning opportunities during the recessionary times. In developing countries, this is especially relevant as not just the domestic, but the international investor seeks refuge in emerging-market opportunities and SRI implies to be a safe-haven investment to the responsible investor (Srinivasan, 2014; Tripathi & Bhandari, 2014; Tripathi & Kaur, 2022).

Therefore, from this study, we can conclude that even though SRI grows to be a mainstream investing style in developed countries, it does not outperform SRI in developing countries, where the phenomenon is still at a nascent stage. Given the disclosure trends, it can be said that SRI in developed countries is in fact driven by regulatory ESG disclosures and reporting, and not due to a superior performance of SRI in these economies over SRI in developing countries. Whilst international voluntary codes and regulatory norms support disclosure in developed countries, the adoption and implementation of international reporting standards are inadequate in developing countries crippling the growth of SRI in emerging economies.

The study has the following implications for Global Economies who are called out to unify in curating uniform ESG norms and guidelines, In a strive to attain global sustainable goals. Further, Global Corporations need to integrate and exchange their ESG business strategies, ethical competencies as well as sustainable practices. Their consistent disclosures and voluntary reporting by businesses in emerging nations will help the percolation of the sustainable strategy in the economy. In addition, Asset managers have a role in dispelling inhibitions about SRI and inducting interest of investors in ESG securities by integrating screening strategies in portfolio management subject to investor demand, risk appetite and global-investing trends. The study implies great relevance for active investors seeking benefits from globally diversified portfolios. They have a role in exercising their influence in making the corporations disclose material ESG concerns consistently, transparently and accurately.

The study is not free from certain limitations. Due to limited data for developing countries, the time before 2007 could not be considered. In addition, as the scope of this study is limited to the analysis of impact of Economic Conditions (boom and recession) on SRI, the bearish market condition, caused by stock movements during the COVID-19 period, could not be studied. In addition, qualitative parameters inquiring about the impact of socio-cultural factors on the penetration of SRI across different regions could not be studied due to the expanse scope of this study. Further, qualitative parameters inquiring the impact of socio-cultural factors on the penetration of SRI across different regions could not be studied due to the expanse scope of this study.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.