Abstract

In the current era of digital business ecosystem, firms have been looking for fresh perspectives to frame its business strategies and create value for customers. Competitive advantage can be generated only when the value created by a firm for its customers exceeds the cost of creating such value. Creating value for customers in health insurance has been a strategic priority for insurance firms. Indian health insurance firms are competing in the area of launching new products which are technology driven and are striving to provide more value to the society through their services. This study explored the value creation process in the health insurance industry. Using case study research with health insurance industry as unit of analysis, this study explored the interactions between stakeholders within the boundaries of the health insurance ecosystem. The role of the stakeholders was explicated using the value net framework which categorised them into customers, competitors/substitutes and suppliers. A value creation framework based on stakeholder collaboration was proposed for the health insurance industry which would further enhance the competitive advantage of health insurance firms in India.

Introduction

The structure of an industry influences its levels of competition and profitability (Elango & Sambharya, 2004; Nayak et al., 2022). The ability of firms to capture value from its resources determines the probability of attainment of competitive advantage (Kaleka & Morgan, 2017). Firm managers must focus on understanding the environmental threats, internal strengths and reduce internal weaknesses to be able to gain competitive advantage (Barney, 1991). Explicating the nuances of the interactions between different players in an industry requires a comprehensive analysis of the industry (Horváth & Szabó, 2019). A good industry analysis should focus on the profitability aspect of the industry over the last 3–5 years and understand the root causes influencing the profitability (Porter, 2008).

Value creation has been pursued by firms as a strategy to attain competitive advantage (Zondag et al., 2017). Increasing customer demands have forced firms to explore avenues of co-operation and networking rather than adopting adversarial market positions (Kähkönen, 2012). Harnessing the combined competencies existing across different players in an industry has proved to stimulate creation of enhanced customer value and generate competitive advantage for firms simultaneously (Watson et al., 2018). In this study, using the value net framework, the creation of value for customers has been illustrated using the case of the health insurance industry in India (Daidj & Egert, 2018). A value net framework for health insurance has been proposed to understand how different players compete, cooperate and collaborate to co-create customer value (Daidj & Egert, 2018).

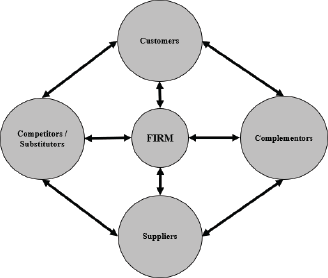

The Value Net Framework

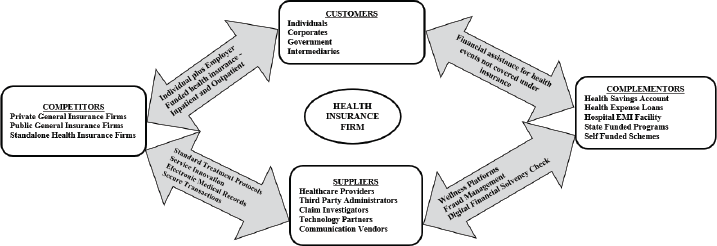

The creation of value through collaboration between stakeholders in an industry forms the foundation of the value net framework (Bovet & Martha, 2000). Value net comprises of all firms in an industry along with suppliers, customers, complementors, competitors, regulators and industry organisations (Zondag et al., 2017). This framework (Figure 1) entails that firms and stakeholders in an industry collaborate to increase the value proposition for products and services which would not be individually possible for any firm (Nalebuff & Brandenburger, 1997).

The essence of the value net framework relied in the nature of cooperation and sharing of core competencies to serve the common customer for the industry and parallelly fulfilling the business objectives of individual firms (Ritter et al., 2004). Knowledge management capability as an inalienable characteristic of health insurance firms has been found to be crucial in delivering value to customers (Gibbert et al., 2002). The interactions between the constituents of a value network created a conduit for knowledge sharing and information exchange thus making it suitable for analysing the health insurance industry (Bovet & Martha, 2000). The success of customer relationship management has been critically dependent upon knowledge management practices and both share common objectives of delivering more value to customers (Gebert et al., 2003).

Context of the Study

In India, the health insurance sector has seen significant growth in the last 5 years with the private standalone health insurance companies which are driving the larger part of the growth in this sector (Insurance Regulatory and Development Authority of India [IRDAI], 2019). The liberalisation of the market in the year 2001 untapped potential which attracted multiple foreign players to invest in the attractive health insurance market in India (Teli, 2014). Health insurance market has grown in size, but profitability has been a concern over the last few years (Joy, 2018). The presence of a large untapped population and developing healthcare infrastructure along with the incentives to do business in India is providing Indian companies access to foreign capital and expertise in the health insurance space (Kapur & Ramamurti, 2001).

Historically, health insurance business was conducted by general insurance firms in India and was also termed as non-life insurance (Joo, 2013). Insurance density is measured as ratio of premium collection (in USD) to total population while insurance penetration is measured as ratio of premium (in USD) to the Gross Domestic Product—GDP (in USD) (Vimala & Alamelu, 2018). Since the year 2001, when the insurance sector was opened up in India to the private sector, the insurance density for the non-life sector increased from USD 2.40 in the year 2001 to USD 19 in the year 2018. During the same period, non-life insurance penetration increased from 0.56% to 0.97% (IRDAI, 2019).

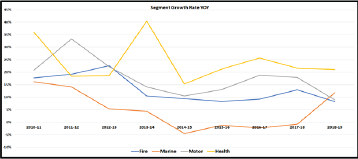

The growth rate of insurance has been linked to the economic progress of a country (Akinlo & Apanisile, 2014). With an increase in the penetration of insurance, the risk-taking ability of society was enhanced thus spurring increased economic activity (Brainard & Schwartz, 2008). In India, the health insurance segment has been the fastest growing among all the general insurance lines of business maintaining an average growth rate of 24.3% over the last 9 years. Figure 2 depicts the growth rate of the different lines of general insurance business from 2010–2011 to 2018–2019.

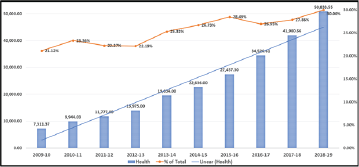

Along with the increase in the premium for the health insurance segment, the share of health insurance as a percentage of the total general insurance business increased from 21.12% in 2010–2011 to 30% in 2018–2019. Figure 3 indicates the trend of growth rate and share of health insurance out of total general insurance premium from 2009–2010 to 2018–2019.

In the current era of digital business ecosystem, firms have been looking for fresh perspectives to frame its business strategies and create value for customers (Subramaniam et al., 2019). Creating value for customers in health insurance has been a strategic priority for insurers (Choudhry et al., 2010). Interestingly, value creation has also been a considered as a source of competitive advantage (Onetti & Zucchella, 2014). Unlike insurance of products, property or vehicles, health insurance is used during critical health emergencies and hence has drawn greater attention compared to other types of insurance.

Research Objectives and Methodology

The objective of this study was to understand how stakeholders in an industry collaborate to create value for the customer. In the context of the health insurance industry, this study specifically examined the role of healthcare providers, intermediaries and other non-insurance entities in the insurance ecosystem in creating value for insured individuals. Stakeholder engagement in co-creation of value for customers is a useful process to enhance corporate performance (Loureiro et al., 2020). There has been an increased interest in understanding how collaboration between firms, support service providers and customers contributes to value creation which benefits all stakeholders (Breidbach & Maglio, 2016). Few studies have explored the organisational capabilities required to create customer value (Zhang et al., 2015). Following the guidelines on case study objectives of ‘what, why and how’ questions proposed by Eisenhardt (1989), the objectives of this study were formulated as.

To understand the structure of the health insurance industry in India To understand the role and interaction of stakeholders in the industry To develop a stakeholder engagement framework for creating value for customers

This study draws from the case study research design using industry as the unit of analysis (Yin, 2017). Due to the lack of studies in value creation in the health insurance industry, the in-depth case study approach was considered as appropriate for this study (Yin, 2017). The research framework involved a detailed analysis of the industry including the business trends, competitive strategies of firms and their interactions with the support service providers.

Case study method has been found to be useful in analysing an industry structure using the value net framework (Kähkönen, 2012; Zondag et al., 2017). Since exploring the processes of value creation was the objective of this study, the value net framework was considered as appropriate to conduct a comprehensive industry analysis. This method also aided in exploring the interfaces between firms, industry stakeholders and customers in a real-life context—health insurance industry (Eisenhardt, 1989).

Analysis of the Health Insurance Industry in India

The health insurance industry in India, as the unit of analysis for this case study, was examined using the value net framework. Secondary financial data for the case was compiled up to financial year 2018–2019 as audited figures have been released by the regulator up to this period in its latest annual report. All the financial figures reported in this study are based on the statistics presented in the Insurance Regulatory and Development Authority of India (IRDAI) Annual Report 2018–2019. The constituents of the value net framework for the health insurance industry are described in the following sections.

Customers

The buyers of private health insurance mainly comprise of the retail population who buy health insurance for themselves and their families (Jefferies, 2020; Nayak et al., 2018). Corporates and other mass employers buy health insurance for employees and their families, although the mechanism varies across industry (Sanghvi, 2020). The state and central government provide health insurance for the social sector (Saxena, 2018). Individual agents, corporate agents, brokers and web aggregators facilitate the purchase of insurance for their clients who prefer to buy policies through an intermediary than an insurance firm directly (Krishnamurthy et al., 2005).

Individuals purchasing health insurance have a significant choice among the 32 insurance firms selling health insurance in the market (IRDAI, 2019). The information on the products, price and benefits are readily available for comparison on the web portals of the insurance firms or third-party portals providing comparisons of products and services (Kalyani, 2020). Health insurance products have a portability feature which allows the insured member to change the insurance firm every year without any loss of benefits or continuity in the coverage (Nirmal, 2018). This poses a major challenge for health insurance firms as retention of customers is a key measure of success of the health insurance portfolio (Verhoef & Lemon, 2013). Acquisition cost for a new customer is always higher although it is also critical to add new customers while maintaining a good retention of the existing portfolio (Ansari & Riasi, 2016). A high retention of customers without adding new ones increases the risk of claims with the increasing age of the existing portfolio (Fang et al., 2016).

Individual Health Insurance

For health insurance, all products are filed with the insurance regulator and the price structure is approved along with any incentives or discounts which are to be offered to customers (IRDAI, 2020). Although this acts as a safeguard for individual customers who could have advance information of the cost of health insurance, but at the same time, it does not allow any additional negotiating power outside what was already defined in the product (IRDAI, 2020). The retail health portfolio for the public-sector insurers is much higher compared to the private sector (IRDAI, 2019) indicating that individuals tend to trust the public-sector enterprises to invest their money than the private sector (Srinivasan, 2019). The fear of stability of the private sector firms also acts as a driver to individuals preferring the public sector considering the government as a custodian of public sector firms (Livemint, 2018). Health insurance is still considered as a tax saving instrument (Motiani, 2018) rather than a protection against unforeseen risk resulting in individuals opting for low coverages and products which do not suit their requirements (Pettigrew & Mathauer, 2016). However, the scenario is gradually changing with private sector services improving and standalone health insurance firms witnessing a faster growth of their retail business (Asthana, 2018).

Group Health Insurance

Group health insurance is the largest portfolio of the health insurance business comprising of corporates, government enterprises and the government (Balachandar, 2019). Firms which buy health insurance for its employees and dependents have a high bargaining power due to the large number of employees and other businesses which they could give to the insurance firm (Subramanian, 2013). Any large firm having considerable assets could offer its fire, engineering, property and other asset related insurance to an insurer and negotiate low-cost health insurance for its employees (Nair, 2013). Although, there has been an attempt by the regulator to influence insurers to treat the health insurance portfolio as a standalone business, group health insurance is still not viable for most insurers due to such cross-subsidisation strategies (ZeeBiz WebTeam, 2018). Insurers who do not adopt such strategies tend to lose group insurance business as it is possible for a corporate to move its business from one insurer to another every year at a lower price (Shetty, 2014). Large corporates are also able to negotiate wellness benefits and additional value-added services for its employees (Rathor, 2020). Group health policies thus have different models with varying family composition, restrictions on accessibility to hospitals and limits for treatment and premiums to be paid by the firm or the employee (Sanghvi, 2020). However, low pricing in group health insurance finally leads to service issues when insurance firms attempt to hedge the risk by implementing strict claim assessment guidelines (Kulkarni, 2019).

Government Tenders for Health Insurance

Governments or government enterprises purchasing health insurance choose the tender mode thus driving down the premiums to lower levels and sometimes below the actual risk premium (Saxena, 2018). New insurance firms which are eager to build a topline, quote aggressively for such tenders and gradually make the mass insurance portfolio unviable (Sakle & Tainwala, 2015). The governments are making this portfolio further aggressive by introducing processes of reverse bidding where the top three or five bidders are required to bid again for the lowest price (Madia, 2018). The regulator and the industry body of insurers are making efforts to drive consensus among insurers to participate in such tenders with sound actuarial pricing and without resorting to unviable strategies only to gain market share (Mehta, 2018).

Insurance Intermediaries

Agents and web aggregators constitute another major portion of buyers of health insurance (National Insurance Academy, 2020; PwC, 2019). There is still a large proportion of the population which prefers to buy insurance through an agent (Vellakkal, 2009). This probably stems from a fear of technicalities of insurance or the complications of service delivery at the time of a claim (Thanawala, 2016). Insurance business through agents is driven by commission amounts which are capped by the regulator (Bhaskaran, 2011; Saraswathy, 2016b). Agents can negotiate better service terms for their clients and incentives for themselves as premium negotiation is not possible due to the products being approved by the regulator (Halan, 2017). Brokers who mainly participate in group health business have a high bargaining power due to the nature of the group business (Karaca‐Mandic et al., 2018). Almost 65% of the group health business is channelled through brokers (Saraswathy, 2018). Although the broker industry is partially regulated, the government has notified a 100% foreign direct investment in the broker firms which is expected to result in stronger regulations to monitor their business (Shah et al., 2020). There is a strong need for self-regulation in the broker industry to improve the group health insurance portfolio for the benefit of all stakeholders (Jenkins & Misra, 2018; Roy, 2018).

Suppliers

Suppliers for the health insurance industry comprise of healthcare providers (hospitals, diagnostic centres and doctors), Third Party Administrators (TPAs), claim investigators, technology partners and communication vendors (couriers, post and e-mail/short messaging service—SMS vendors).

Healthcare Providers

Healthcare providers being the delivery point of health insurance services act as the source where customers redeem their health insurance benefit (Trish & Herring, 2015). The quality, price and nature of the service provided by the hospitals determines the future decision of the beneficiary with regard to the health insurance product (Kolstad & Chernew, 2009). The hospital industry had inadequate regulations in certain states leading to absence of any protocols or guidelines which were standardised or could serve as a benchmark (Sengupta, 2018). The government tried to bring in a semblance of discipline through the Clinical Establishments (Registration and Regulation) Act, 2010, however, the same has not been fully effective in curbing the existing malpractices in the healthcare delivery industry (Tirth et al., 2013). There are inadequate standards for infrastructure of hospitals or pricing of services (Dutta, 2018). Even where it exists, there are glaring differences when compared across different states or regions (Bhuyan, 2018). The recent standardisation of prices of stents and implants by the government has faced resistance from the hospital industry but was welcomed by patients (Rajagopal, 2018). The hospital industry lacks transparency in terms of pricing of services (Devadasan, 2017). The mechanism of pharmaceutical companies incentivising doctors to prescribe specific medicines or modes of treatment has led to supplier induced demand as patients are not fully qualified to understand how much and what treatment they require (Raghavan, 2017; Singh, 2017). Hospitals could bargain for prices with the insurance company based on the demand for their services by patients (Trish & Herring, 2015). The reverse is possible if the insurer is able to provide a high volume of business to the hospital but in such circumstances, the negotiating power of the insurer is limited due to the strong cartelisation in the hospital industry (Lakdawalla & Yin, 2010; Mazumdar, 2015). Moreover, hospitals are reluctant to share any evidence on the outcome of the surgeries or the infection rates, mortality rates or success rates of the consultants (Adhikari et al., 2015; Bhat & Rajagopal, 2005). In light of this, there is no standard method by which insurers or even patients could evaluate hospital services objectively (Garg et al., 2019). In the current scenario in India, customers trust the doctor or the hospital due to word of mouth and traditional societal norms which help the healthcare providers to influence the insurer through the choice of the customer (Berger, 2014). Insurers have implemented various mechanisms like standardised pricing, medical audits and insisting on accreditation as a regulatory provision which has put some pressure on the hospital industry to standardise its processes (Chitra, 2016c).

Third Party Administrators

Third Party Administrators (TPAs) are a critical entity among the suppliers as these players manage the services that insurers provide to their customers (Bhat & Babu, 2004). This includes assistance for member enrolment, cashless services, claim reimbursement and customer service (Bhat & Babu, 2004). These are regulated by IRDAI and have strict norms for licensing and operations (IRDAI, 2019). Insurance firms outsource its services to the TPAs depending on the strength of the TPA in servicing in specific geographical areas (Sane & Singh, 2012). The service quality of TPAs varies and depends on diverse factors such as the volume of business that the insurer provided, and the service fee paid by the insurer (Bhat et al., 2005). Retail customers have the choice of selecting a TPA which the insurer has to provide; also, corporate customers choose TPAs based on the service quality and recommendations of the broker or insurer (Grönroos & Gummerus, 2014; Sanghvi, 2019). The bargaining power of TPAs is high where these TPAs have good working relationship with the corporate clients or brokers directly and hence could demand a premium for its services (Bhat et al., 2005). The services of the TPAs has not been up to the mark across the industry as they do not own the customer and hence there is no direct incentive for exemplary service (Dilawari & Koley, 2016). The insurer may decide to change the TPA due to cost or service factors and hence the TPAs also attempt to minimise its cost of servicing (Bhat & Babu, 2004). This has resulted in many insurers doing away with TPAs and managing the services internally through its own teams (Chitra, 2016b). This provided insurers with an opportunity to customise service offerings and increase customer retention (Nair, 2011). TPAs too are now improving its services and managing costs effectively to offer insurers an alternative to in-house management (Singh et al., 2019). Some TPAs have set up parallel companies to provide value added services like wellness services, health check-up and concierge services to help customers and manage costs more effectively (Sanghvi, 2019).

Claim Investigators

Claim investigators in health insurance are now an important constituent owing to the increasing number of frauds and moral hazards (Akhter, 2018; Saraswathy, 2016a). The investigators could be individuals or agencies having professionals who have an expertise in this area (Rawte & Anuradha, 2015). Insurance companies engage investigators depending on the expertise for investigating claims where there is a suspicion of cost inflation, misrepresentation of facts, forgery of documents or high amounts involved (National Health Authority, 2019). There is no regulation for investigators in the health insurance space and hence insurers depend upon the past success rates of investigators or the profile of the vendor employees (ENS Economic Bureau, 2019). There is a lack of good investigators and hence insurers employ doctors or paramedic professionals for such work (National Health Authority, 2019). The individuals and agencies do not have a very high negotiating power unless they have established themselves with a good track record.

Technology Partners

Technology partners are currently in high demand in the health insurance sector (Gupta & Tripathi, 2016). The health insurers have realised the importance of integrating digital platforms in its operational processes to remain competitive in the market (Cappiello, 2018; Sivanandh & Balasubramanian, 2016). In contrast to the health insurance industry, the healthcare delivery market has adopted innovations in technology at a rapid pace to improve health outcomes (Albahri et al., 2018). Customer expectations are driving insurers to transform its processes to paperless mode and provide faster customer services (Saleem, 2017). Sensing this need, many entrepreneurial firms have come up in this space and are offering solutions to the insurers (Krishnan, 2020). The absence of a standard and structured software which can address all the needs of a health insurance portfolio has made this area more competitive (Kumar, 2019). However, very few players have been able to establish themselves as trusted partners and deliver an end-to-end solution for the industry (Verma, 2020). Large technology vendors demand a high price for any development work but lack the domain knowledge for health insurance (Agarwal, 2020). At the same time, insurers have the intellectual knowledge base required to develop a standard software but lack the technology expertise to execute the project (Sangani, 2019). Hence, most projects are managed on a partnership basis with an agreement of staggered payments on successful implementation of modules (PwC, 2019). Vendors who provide server space on the cloud, hardware providers and service support partners also form an important part of the technology support required by health insurers and could demand a price for their service with proven credentials in the market (Deshpande, 2019). The technology requirements for health insurers will only grow in the future and technology companies could command a price if they are able to demonstrate the ability to deliver superior quality products (Gramling, 2014).

Communication Vendors

Lastly, communication vendors serve as a medium of dialogue between insurers and its customers (Arnold, 2020). The turnaround time for various services like policy and claim related communication through letters, e-mails, messaging services and social media updates define the service standards for the insurer (Asghari & Babu, 2017). Customers form an opinion about the insurer based on how fast they responded to their needs (Meyer & Schwager, 2007). Courier companies which commit service timelines demand a price for its service and insurers utilising their services do create a positive impression in the minds of customers (PwC, 2019). The negotiating power of the vendor depends upon the geographical spread (in case of couriers) and technology superiority for electronic services (Bharucha, 2017). Insurers do not hesitate to engage the best communication vendors as it impacts the customer acquisition and retention strategies and improves the net promoter score (NPS) for their services (Branding, 2017; Sachdev, 2020).

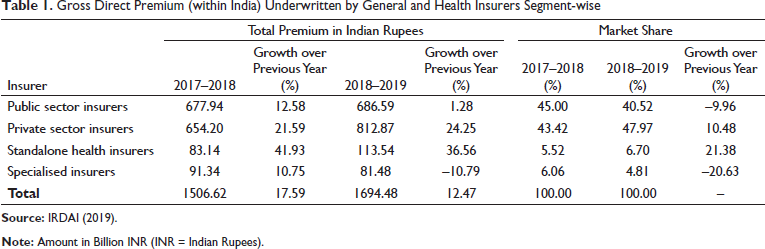

Competitors

In the year 2020, there were 34 insurance organisations licensed by the Insurance Regulatory and Development Authority of India (IRDAI) to conduct general insurance business in India (IRDAI, 2019). Among these firms, four public sector insurers had a market share of 40.52%, while 21 private sector firms had a market share of 47.97% in the year 2018–2019. There were seven standalone health insurance firms which had license to conduct only health insurance business and occupied a market share of 6.70% in 2018–2019. There were two specialised insurers which did not conduct health insurance business and held about 4.81% of the market share in the year 2018–2019. Table 1 presents the market share of the insurers in financial year 2018–2019 and increase in market share over the previous financial year.

Gross Direct Premium (within India) Underwritten by General and Health Insurers Segment-wise

The total direct premium for the general insurance industry in India was ₹1694.48 billion for the year 2018–2019. The growth for the public-sector insurers for 2018–2019 was 1.28%. The private general insurers registered a growth rate of 24.25% in 2018–2019. The standalone health insurance firms grew by 36.56% in 2018–2019. The premium for the health insurance business was ₹508.34 billion in 2018–2019.

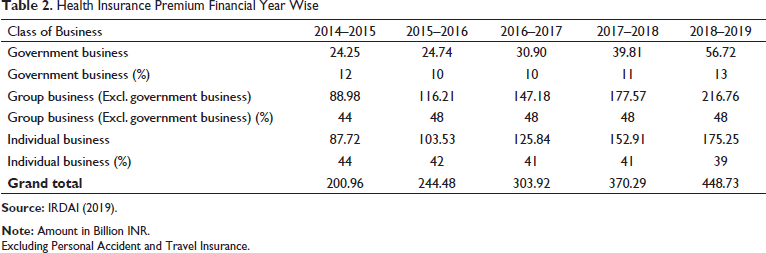

The growth in the premium has been led by the group health business followed by the individual health business. Government Health Insurance schemes have not registered a sustained growth trend, and this could be linked to the issues of management and administration of the schemes at the local level (Palepu, 2018). Also, the government programs in some states have been running through trust models at the state level which reduced the scope of participation of insurance companies in these mass schemes (Raghavan & Sinha, 2018). The focus on retail business is embedded in the growth strategy of all insurance companies which recognised that profitable growth is possible in this segment (Singhal et al., 2016). However, the temptation of adding to topline growth through group health business has been affecting the industry in maintaining a healthy portfolio (Murali, 2013). Table 2 provides the health business done by insurance companies in the group, individual and government segments over the last 5 financial years.

Health Insurance Premium Financial Year Wise

Excluding Personal Accident and Travel Insurance.

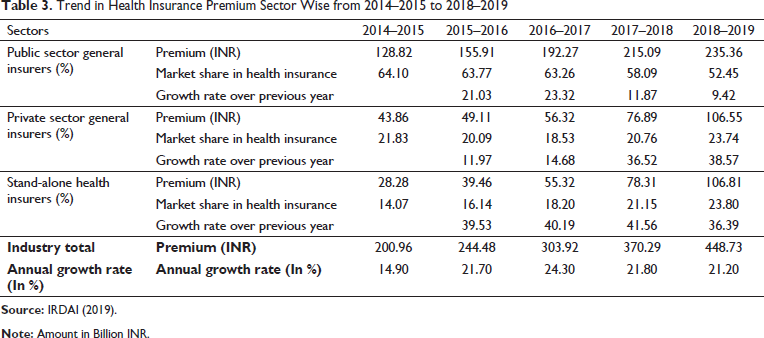

The growth in health insurance premium has been significant for the standalone health insurance companies which were formed with the purpose of conducting only health insurance business in the country. During the period 2014–2015 to 2018–2019, while the private sector companies grew at an average rate of 25.44% increasing its market share from 21.83% to 23.74%, the public sector grew at an average rate of 16.41% with its market share decreasing from 64.10% to 52.45%. During this period, the standalone health insurance firms displayed a strong average growth rate of 39.42% and increased its market share from 14.07% to 23.80%. The health insurance industry grew at 20.78% during this period. The standalone health insurance firms thus grew at a higher rate than the average growth rate of the industry. The decrease in the market share of the public sector firms was thus transferred to a little extent to the private sector firms and to a greater extent to the standalone health insurance firms. Table 3 presents the trend in health insurance premium over the last 5 years for different insurer segments.

Trend in Health Insurance Premium Sector Wise from 2014–2015 to 2018–2019

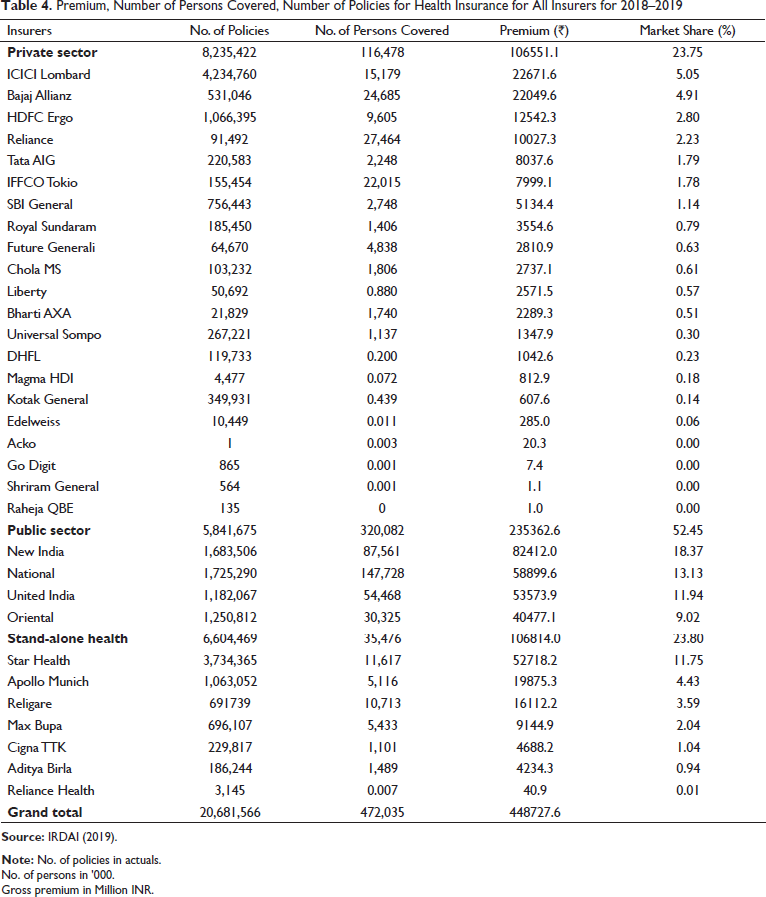

Table 4 provides the premium, number of persons covered and number of policies for health insurance across all insurers for the year 2018–2019. The top 10 firms among 21 firms in the private sector commanded a market share of 21.70%. Compared to that, the top four standalone health insurance firms out of the total seven firms commanded a market share of 21.81%.

Premium, Number of Persons Covered, Number of Policies for Health Insurance for All Insurers for 2018–2019

No. of persons in ’000.

Gross premium in Million INR.

Profitability of insurance firms is determined by the combined ratio which is a sum of claim ratio, administrative expenses and business acquisition costs (Chen & Wong, 2004). Claim ratio denotes the proportion of claims paid to premium collected for a segment (Joo, 2013). A review of the claim ratio for health insurance for the year 2018–2019 indicated that while the public sector had a claim ratio of 105%, the private sector was better at 84%. In contrast, the standalone health insurers had a healthy claim ratio of 63% which reflected their focus and strategy to do business profitably (Akhter, 2018). Considering that the acquisition cost for health insurance business is considerably high, along with the administrative costs, the overall combined ratio for the insurance firms was a cause of concern which needs to be addressed for long term sustainability of the business (Murali, 2013). Table 5 presents the trend of claim ratios for the health insurance portfolio for different insurer segments. The claim ratio for the industry has fluctuated over the last 5 years due to the high claim ratio for public sector insurers.

Trend of Claim Ratio for Health Insurance Sector Wise from 2014–2015 to 2018–2019

Table 6 provides the claim ratios for health insurance for different class of businesses done by general insurers. The high claim ratios are driven by the government and group health business.

Trend of Claim Ratio for Health Insurance Business Class Wise from 2014–2015 to 2018–2019

The standalone health insurance firms have differentiated themselves from the other private and public-sector insurers conducting health insurance business by launching innovative products in the market (Kulkarni, 2018). These products incorporated flexible benefit plans, specific disease plans, adoption of Internet of Things (IoT) and wearable technologies and simplified operational processes (Nayak et al., 2019b; Ramamoorthy & Kumar, 2018). Newer entrants also made the product wordings simpler by removing the technical jargon and involving customers in the insurance value chain (Singh, 2020). Standalone health insurance players also promoted its products in the market to a greater extent than the private or public-sector insurers (Shruthi, 2017). Since the advertisements are regulated by IRDAI and the number of complaints related to mis-selling are quite high (Roy, 2017), one could note that not much activity was reflected in the print or digital media space for health insurance promotion (Noronha, 2013). The awareness of health insurance is still at a level lower than expected (Singh & Shukla, 2017). The regulator is involved in awareness activities to sensitise customers on the frauds involved in health insurance sales (Dhawan, 2017), but no focused attempts have been made to increase penetration of health insurance (Chakrabarti & Shankar, 2015).

Health insurance business is currently conducted by general insurance companies and standalone health insurance companies (IRDAI, 2019). The market share of the general insurers declined when the regulator allowed pure health insurance companies to operate with new licensing requirements (Chitra, 2016a). Some general insurers like Shriram General Insurance and Magma HDI General Insurance have not been active in doing health insurance business (IRDAI, 2019). The encouraging performance of specialised health insurance companies has attracted some general insurers to consider buying stakes in the standalone health insurance firms to create a larger health insurance portfolio (Chakrabarty, 2020). Further, there has been a long-standing demand from potential investors to relax the norms for setting up health insurance business with a lower capital requirement of ₹500 million compared to the existing ₹1 billion (Business Standard, 2013). With such a relaxation, many foreign players having large health insurance operations in other mature markets would enter India with more innovative products (Badala & Jain, 2020). New insurers like Digit Insurance and Acko General Insurance are emphasising on business models which would be completely technology driven for sales and servicing and might eliminate or reduce the dependence on the traditional agency model followed by general insurers (Manikandan & Shrivastava, 2020). This might greatly reduce operational costs and give them adequate margins to experiment with new products and services (Liu et al., 2018). Large hospital chains like Manipal Hospitals (stakeholder in Manipal Cigna Health Insurance) and Max Hospitals (stakeholder in Max Bupa Health Insurance) have invested in the health insurance business and have the added advantage of offering services to insurance customers at their own hospitals (Mor, 2015). This also provides these firms with an opportunity to offer lower cost of treatment for its customers and also extend various preventive services to reduce claim frequency and severity (Thomas, 2011). Health insurers need to constantly innovate on products and services to ensure that they are able to counter the competition offered by new entrants (Cappiello, 2020).

Complementors

Health insurance companies provide assistance to customers by offering cashless services at the time of hospitalisation or reimbursing their expenses later when the customers made a claim with submission of original documents (Ranjan et al., 2018). New business models like health savings accounts based on this concept have been formed where assistance could be provided to needy individuals when they are in need (Steinorth, 2011). Such models have been successful in mature insurance markets like the United States and were expected to be a strong substitute for health insurance (Freudenheim, 2007). Financing companies like Bajaj Finserv and Tata Finance offer loans to customers at zero interest rates which could be repaid in monthly equated instalments (Business Wire India, 2018). This presents an attractive option to individuals who do not wish to pay premiums for health insurance for a considerable period of time and were not getting anything in return unless there was a health episode in the family (Montazerhodjat et al., 2016). They find the option of availing a loan only when required for health expenses as a safer choice than buying insurance (Thanawala, 2017). Hospitals also recognised the need for patients paying medical bills in equal monthly instalments to make specialised treatment affordable for everyone (HT Brand, 2020). This also attracted patients to a hospital which offered such a facility as it alleviated the need to arrange for immediate cash by the patient (Mitra, 2016). With the government sponsored health scheme offered under the Ayushman Bharat scheme, a significant proportion of the population would come under the ambit of a health plan (Lahariya, 2018). However, major Indian states are choosing to implement the scheme through a trust model without involving insurance companies (Sharma, 2019). Enrolment of a larger part of the population under social health insurance schemes funded by the government could reduce the market available for private health insurance (Maurya & Mintrom, 2020). Moreover, many large corporations having a significant health expenditure prefer to have a captive health plan where they manage the health risk of their employees internally (Gonzalez, 2018). Entities like Indian Railways, central Public-Sector Units (PSUs), the armed forces, the Central Government Healthcare Scheme (CGHS) and self-funded schemes by corporates (FE Bureau, 2018) might decrease the potential untapped market available to health insurance firms.

Value Net Framework for Health Insurance

The factors that emerged as key for the health insurance industry in India were the business environment in which the health insurance firms were operating—competitive environment, technological environment and regulatory environment juxtaposed with the factors operating at a firm level—product innovation, management of knowledge resources, culture of the firm, customer service quality delivered by the firm and the strategic intent of the firm embodying the technology policy, strategic orientation and first mover advantage gained by the firm. Firms have increasingly realised that they operated in a marketplace which coexisted within a social milieu (Brennan & Merkl-Davies, 2018; Nayak et al., 2019c). Establishing an emotive relationship between customers and the firm, which circumvents commercial interests, and creating value led to strategic advantage for the firm (Butz & Goodstein, 1996).

The framework as depicted in Figure 4 emerged from the analysis of the health insurance industry which represented the process of value creation through engagement of all stakeholders. The framework harmonised the role of different stakeholders in the industry to protect the health of individuals and also improve their quality of life. While the competitors implemented their business strategies to increase market share through innovative insurance products at different price points, the suppliers were required to implement standard treatment protocols with standard pricing to ensure sustainability of the insurance products. With the increased awareness and use of digital applications, automating and securing transactions between suppliers and insurers would enhance the value of insurance products for customers (Nayak & Bhattacharyya, 2019). Complementors played a major role in supporting individuals who were not a part of the insurance net due to issues related to accessibility or affordability. Availability of funds at a short notice with easy repayment norms could provide a lifeline to such individuals and also assist insured individuals to tide over health episodes not covered by insurance. This framework addressed the research objectives by explicating the role of stakeholders in the health insurance industry and outlined the process of collaboration among them. The outcome of the study would facilitate in presenting an enhanced value proposition to the customer.

Conclusion

In this case study, a value creation framework based on stakeholder collaboration was proposed for the Indian health insurance industry to enhance the comprehension regarding attainment of competitive advantage. The framework developed in this study would help health insurance managers in channelising firm resources for better value creation. The current health insurance market is turbulent in terms of fast changing strategies, unclear guidelines on public and private sector responsibilities, incomplete liberalisation of the market, wary foreign investors and shifting customer loyalties. Health insurance firm managers also face challenges from non-insurance-based substitutes which allowed access to finance and treatment options to individuals without having to pay regular premiums for a health insurance plan. Health insurers are required to manage its business more actively due to the decreasing profitability and increasing competition from newer entrants in the private sector. Voluntary private insurance which is often portrayed as a solution to counter health risks is plagued by adverse selection, moral hazard and cost escalation. Apart from burgeoning administrative expenses of the insurance companies, the utilisation of third-party administrators (TPA) had also become a liability for insurance companies (Selvaraj & Karan, 2009). Internal firm factors like the structure of the market and the business environment determine the sustainability of health insurance (Austin & Hungerfold, 2009; Thomas, 2017). It is essential to gain deeper insights into these factors to enable the health insurance firms to achieve stability and provide customers with a better experience in health insurance services. Present day insurance market has great potential compared to the scenario that existed before a decade. The scenario has changed today with more informed customers who used digital and social media to compare and understand insurance benefits before making a purchase (Nayak et al., 2019a). The outcome of this study is expected to help in developing a framework for health insurance firms to become more stable and contribute to societal benefits.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.