Abstract

India’s healthcare system is witnessing increased medical inflation, which is outpacing per capita Gross Domestic Product growth. With increased lifestyle diseases and, most recently, a pandemic caused by COVID-19, the cost of financing healthcare has become a huge issue, especially when government spending on healthcare is so low. In light of this, this article emphasises the significance of privately purchased, that is voluntary health insurance in addition to the government-sponsored health insurance programme for the vast uninsured population. Starting with the history of health insurance in India, this article examines premium growth, underwriting profit, investment income, net profit, incurred claims ratio and other metrics. Following that, the difficulties in the health insurance industry and their breadth are examined through a review of literature and recent newspaper reporting. The key issues resulting in negative underwriting experience are the inefficient risk pooling and unregulated private health care costs. A risk-sharing mechanism with an indemnification model must be implemented for better cost management to eliminate value fragmentation. Finally, ideas are given for resolving the challenges and increasing the market share of the health insurance company, with a focus on long-term business models such as managed care.

Keywords

Introduction and History of Health Insurance

Insurance has a long history in India. It is mentioned in Manu’s (Manusmriti), Yagnavalkya’s (Dharmasastra) and Kautilya’s writings (Arthasastra). The writings speak of pooling resources that could be redistributed in the event of emergencies like fire, flood, epidemics and famine. If we look at the history and development of health insurance in India, we can see that the first Insurance Act was passed in 1912, during the pre-independence period.

In 1947, the Bhore Committee recommended for the improvement of healthcare services in India.

In 1948, through The Employees’ State Insurance Act, the Central Govt. introduced ESIS (Employees’ State Insurance Scheme) for the blue-collar workers employed in the private sector.

In 1954, Central Govt. Health Scheme (CGHS) was introduced for Central Govt. employees and their dependents.

Finally, in 1986, Mediclaim introduced and Govt. insurance companies started selling policies. Health insurance was disability insurance, which has evolved as a type of health insurance. Liberalisation in 1999 and the Establishment of IRDAI (Insurance Regulatory and Development Authority of India) as a statutory body in April 2000, through Malhotra Committee recommendations, marked a new era in the insurance business in India. Post-liberalisation, this sector opened up for private and foreign players. Foreign companies were permitted to own up to 26% of the business.

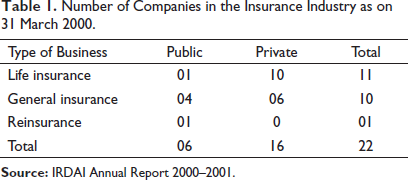

As per the IRDAI Annual Report of 2000–2001, just after the liberalisation of Indian insurance markets, the value of business both life and non-life was estimated at $8 billion a year. Insurance penetration (premiums as % of Gross Domestic Product [GDP]) for life business was 1.39 and for non-life business, it was estimated only 0.54 taking the overall penetration to 1.93% of GDP. Insurance Density was valued at $8.5 where life business contributes $6.1 and the contribution of non-life insurance business in this was $2.4. Insurance Density is the amount of premium per capita in a particular year. The number of companies doing business with life insurance was 11 and in the general insurance sector, it was 10 (see Table 1).

Number of Companies in the Insurance Industry as on 31 March 2000.

The Evolution of Health Insurance Business in India

Among the general insurance business, the fire and motor segment was significant. Health insurance or Mediclaim products were sold by life insurance companies and general insurance companies as riders attached to the policies. The Insurance Act of 1938 and IRDAI Act, 1999 prescribed encouragement towards the establishment of the standalone health insurance company but no one came up with such applications. In 1986, the four public sector General Insurance companies introduced Mediclaim policies, and in 2002–2003 audited business reports showed 1000 Cr. of health insurance business portfolio. Other than Mediclaim for the general public, other types of health policies like Jan Arogya for economically weaker sections, Community based health insurance group schemes for BPL (below poverty line) category were also sold by those companies.

Present Scenario: Health Insurance Sector

The present scenario is far improved, health insurance segment has undergone many changes since then. In the insurance sector, the government has approved 49% FDI, up from 26% previously. As a result, international players and more private companies entered the health insurance market. The Number of Network hospitals increased and the Third-Party Administrators (TPAs) were linked with insurance companies for efficient and quick settlement of claims. The health insurance sector now comprises of 28 companies including four public sector general insurance companies, private sector general insurers and five standalone health insurance companies. As on 31 March 2020, there were 24 TPAs registered by IRDAI. As per the IRDAI Annual Report of 2019–2020; 70% of total claims were settled through TPA out of total claims of Rs. 1.67 Cr.

Life Insurance Versus Non-life/Health Insurance Sector

Globally the share of non-life and life business in 2019 was 53.66% and 46.34%, respectively. In India, the life insurance business always has the major percentage of premium income in 2019 the share of non-life business in premium income was 25.06% and the rest of 74.94% was contributed by life insurance. The Life Insurance segment did more business than the health segment. Life insurance policies are more successful due to their benefits as a saving instrument and a tax shelter. Health insurance, on the other hand, is indemnity-dominated. In 2019–2020 56,865.13 Cr. health insurance premiums have been underwritten.

Publicly Funded Health Insurance Schemes

Apart from health insurance policies sold by companies, there are a number of government-sponsored health insurance schemes in place. The following is a list of central government-sponsored health schemes:

In 2008, the Rashtriya Swasthya Bima Yojana (RSBY) was launched.

In 2018, the Ayushman Bharat-National Health Protection Mission (AB-NHPM) was launched. These health insurance plans are primarily targeted at the poor and vulnerable in both rural and urban areas.

Janani Shishu Suraksha Karyakaram in 2011 was launched to benefit more than 12 million pregnant women who access Govt. facilities for their delivery which provides absolutely free and no-expense delivery suppled with cash assistance.

Different state governments also launched their own sponsored health insurance schemes.

Community-based Health Insurance

Apart from government-sponsored health insurance, community-based health insurance provided by NGOs with the assistance of banks and other financial institutions falls under the category of micro health insurance and is targeted particularly for the vulnerable population who cannot afford voluntary health insurance plans at more expensive premiums. Around 2% of the population is covered by CBHI (Bhat et al., 2018).

Group Health Insurance

Some institutions as an employer provide group health care plans for their employees and their families, with or without/partial employee contributions. General insurance companies and standalone companies also sell group health plans to the public. Premiums under group health plans are less compared to individual health policy premiums.

Share of Health Insurance Business

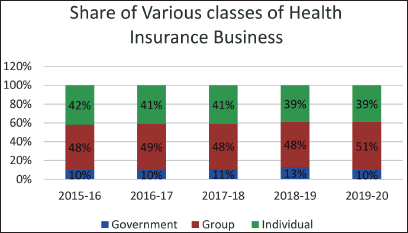

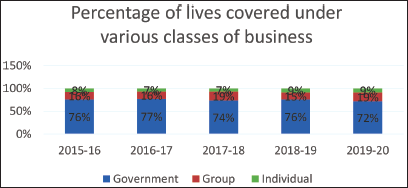

Health insurance business can be classified through three forms—Government, group, and individual health insurance business. Figure 1 shows that in 2019–2020, Individual health business, which is voluntary health plans, account for 39% of total premium income, while group health plans account for 51% and government schemes account for just 10%. Group business has grown over the last five years, according to a five-year trend. Figure 2 shows the percentage of live each class of business covered for the last five financial years. Individual businesses covered just 9% of lives, while group businesses covered 19% and government schemes covered 72% (highest).

Financial Parameters of Health Insurance Business

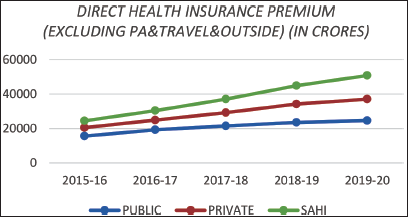

Health Insurance Premium

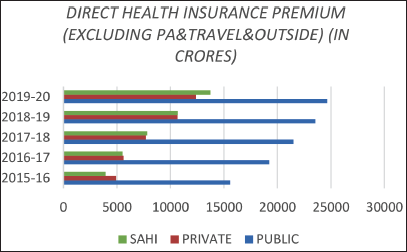

The growth of the health insurance business has been analysed in terms of ‘Premium.’ It is found that in the last five years it grows 57.98% in the public sector, 152.30% in private sector and in standalone insurance companies at 248%. It can be presented graphically (see Figures 3 and 4).

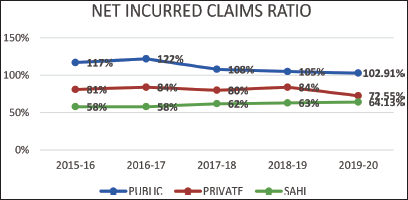

Net Incurred Claims Ratio

Net Incurred Claims Ratio of health insurance companies can be defined as the ratio of net claims paid in a particular financial year out of net premium collected in the same year. If the claims ratio is less than 100% it means collected premium contributed towards profit after settlement of claims. It measures the efficiency of the health insurance business. As per IRDAI Annual Report 2019–2020 an amount of Rs. 40,026 Cr. has been paid towards claims by General and Health Insurers. The average amount of claim paid per person was Rs.23,866. The trends in claims ratio of the public sector health insurers of the last five years are decreasing even if it is showing greater than 100%. In this case, Standalone Health Insurers (SAHI) and private health insurers shows efficient figures as compared to this. It can be shown graphically (see Figure 5).

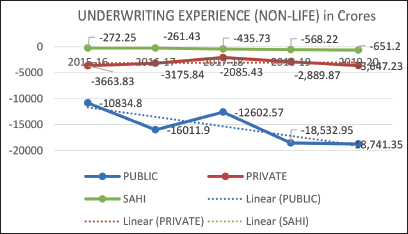

Underwriting Income

Underwriting experience of health insurance companies shows the profit or loss earned after meeting commission and operating expenses and claims settlement from the net earned premium.

Underwriting Profit/Loss = Premium Earned (Net) − (Claim Incurred (Net) + Commission and Operating Expenses related to Insurance Business + Premium Deficiency)

Underwriting is the main business of health insurance and the business of standalone health insurance companies and other non-life general insurers in India is showing a continuous trend of loss, which can be shown graphically (see Figure 6):

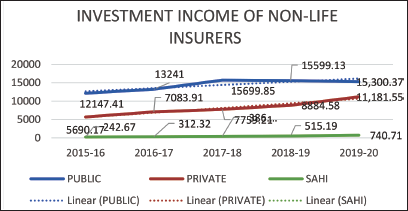

Investment Income

Underwriting and investment income are the two main sources of income for the health insurance industry. Income generated through investment in various financial assets and markets adds the most to net profit and hence compensates underwriting losses. The graph depicts the investment income of non-life insurance companies (public and private) and standalone health insurance companies from 2015–2016 to 2019–2020. (Figure 7).

For, non-life business in both the private and private sector investment income has shown upward trend. SAHI also reported continuous increases in investment income over the five years.

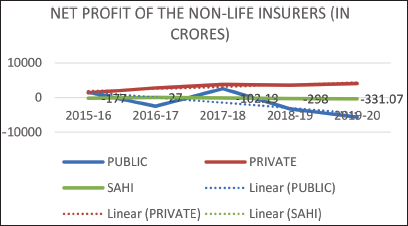

Net Profits

Continuous losses question the survival of the companies basically the stand-alone companies as general insurance companies have businesses other than health to cover the losses. This needs to be addressed. Net profit is calculated adding other incomes, that is investment income with underwriting income and then deducting of tax. The graphical representation is as follows:

The trend of private non-life insurance companies shows a positive trend whereas public non-life insurers show a downward trend of net profit. SAHIs show a net profit of 27 Cr in 2016–2017 and in the rest of the years recorded losses. In 2019–2020 reported a loss of Rs. 331.07 Cr (Figure 8).

Issues in Voluntary Health Insurance Business

The analysis of the financial parameters of health insurance businesses shows that the private health insurance market is quickly expanding. In terms of profitability and underwriting results, the last five years have seen negative underwriting profits, indicating a major structural issue in the Private Voluntary Health Insurance Business. The current indemnity-based health insurance paradigm, according to Thomas and Sakthi Vel (2011), is not sustainable and leads to a regressive loss-making cycle. Many factors contribute to this, including onerous regulations, a lack of standards, high claim payments and expensive administrative costs. Therefore, this article aims to address the issues underlying this business supported with the review of previous literature and published secondary data. The key issues identified are as follows:

Inefficient Risk-pooling and Problem of Adverse Selection

The availability of a large risk pool, in which a large number of healthy low-risk members finance the health care expenditures of a smaller number of high-risk members, is an essential pre-requisite for a successful health insurance scheme (Thomas & Sakthi Vel, 2011). According to a recent study on the health insurance industry, even significant increases in net premium and Compound Annual Growth Rate resulted in underwriting loss. The increase in claims, commissions and management costs has outpaced the increase of premiums received (Dutta, 2020). The availability of a large risk pool, in which a large number of healthy low-risk members finance the health care expenditures of a smaller number of high-risk members, is an essential pre-requisite for a successful health insurance scheme. Cases of adverse selection are causing the high claims. Since buying a health policy is not mandatory all persons are not contributing to the pooling thus only the poor of health end up buying insurance (Thomas & Sakthi Vel, 2011). Only a certain portion of the Indian population is covered by health insurance out of this individual health insurance covers only 9% of lives and 19% by group health insurance policies (2019–2020). Sengupta and Rooj (2019) reported adverse selection in voluntary health insurance, implying that the health market is distorted by higher insurance enrolment of high-risk persons compared to low-risk individuals, potentially exacerbating the disparities in insurance access and enrolment. Low health insurance coverage combined with significant inequality may result in significant out-of-pocket (O-O-P) health spending, making healthcare pricey and inaccessible to a substantial portion of the population.

Not Inclusive Due to Pricing

Private health insurance focuses on the middle-class population of the country (APL category). The growing middle-class population helps this industry to expand. The cost of such a policy is currently ranges from Rs. 3,500–7,000, to cover a minimum sum insured of 3 lakhs. They charge more if the person is of higher age and can exceed Rs. 15,000 each year (Source: Arogya Sanjeevani Policy, ET Money rates, 30 May 2021). This pricing approach may exclude a large proportion of the population from subscribing, necessitating the customisation of products that are affordable to India’s people (Thomas & Sakthi Vel, 2011). Furthermore, according to Sengupta and Rooj (2019), private health insurance is often expensive and non-inclusive, making it unavailable to the bulk of the population.

The Unregulated Private Health Care Costs

In the absence of adequate public spending on health and government infrastructure, the ‘urban-centric curative private health sector’ arose, servicing around 80% of health requirements (Jilani et al., 2009 as cited by Borooah, 2020). According to a report by the High-Level Expert Group (2011) of the Planning Commission of India, cost escalation is the result of a lack of regulatory framework and varying quality in the services provided by this sector (as cited by Borooah, 2020). The private healthcare industry, which has become a lucrative financial opportunity, comprises a wide variety of practitioners and facilities. The impoverished cannot afford to go to elite hospitals. Small private clinics and nursing homes are accessible to middle-class families, but the expenses are prohibitive (Borooah, 2020). A large number of outpatient payments are done in the private sector, but this sector is highly fragmented and various types of providers (variability in service costs). Some are informal providers and less than qualified (Montagu et al., 2016 as cited by Bhat et al., 2018). ‘Hospitals in collusion with Pharma Firms are Burning a Hole in Your Pocket’—(Patel, 2017 as cited in Hati et al., 2019). Doctors, bureaucrats and politicians are also part of it (The All-India Drug Action Network). In the same article, it was said that drug price restriction could be the single most important measure for reducing healthcare spending in both outpatient and inpatient settings. This excessive costing has a direct impact on claims expenses of health insurance companies.

Scope of Voluntary Health Insurance Business

Inadequate Health Expenditure by Government and High Out-of-pocket Payments for Healthcare

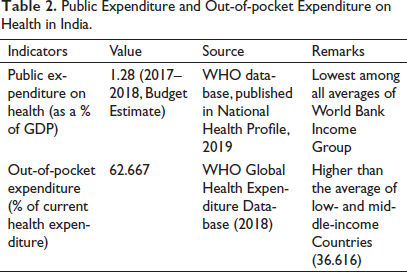

Public expenditure on health in India is very low in proportion to GDP leading to high O-O-P private expenditure (Table 2).

Public Expenditure and Out-of-pocket Expenditure on Health in India.

Despite the fact that government health care providers provide services at a cheap or no cost, individuals always prefer private health care unless it is extremely difficult. They sell assets, including inherited property, and borrow money to fund medical expenditures (Borooah, 2020). Nearly 75% of healthcare spending originates from household budgets, and catastrophic healthcare costs are a major source of poverty (Kasthuri, 2018). The expansion of private-sector healthcare providers eased the door for health insurance companies. Infrastructure, qualified medical personnel, doctors and first-rate facilities and services are all available. Medical tourism has also opened up opportunities for health insurers to sell overseas health insurance, as patients from all across the country boost health insurers’ market share. Even the Government (Central as well as state) now became the purchaser of private health services through various health insurance schemes. It empanelled with various private hospitals and bound to reimburse the amount on behalf of members of the health insurance schemes.

Government Sponsored Schemes Cannot Provide Coverage to All

Various health insurance programs are run by the central government to provide health coverage to people living BPL and other vulnerable groups including unorganised workers in our country. The AB-Pradhan Mantri Jan Arogya Yojana (PMJAY) was launched in 2018 to replace the RSBY, a previously publicly funded health insurance scheme (RSBY). In PMJAY coverage amount increased to Rs. 5,00,000 annually for each of the target families from the earlier yearly coverage of Rs. 30,000. This step has been acclaimed as a big step towards the achievement of Universal Health Coverage. A recent study based on Chhattisgarh by Garg et al. (2020) revealed that merely increasing the coverage level did not reduce O-O-P spending or catastrophic health expenditure (CHE) as well as utilisation of hospital care. Previous literature also reported unsatisfactory outcomes of such schemes. ‘Less than a third of the 6,000 households’ examined in Maharashtra were aware of the RSBY (Ghosh, 2014), (also mentioned by Borooah, 2020). Private hospitals on the scheme’s panel either refused to accept the cards or tried to evade them through other tactics, citing ‘bureaucratic delays in payment’. Private hospitals first consented to join in the hopes of increasing market share, but are now gradually withdrawing, as seen by the fact that the number of impanelled hospitals has decreased from 7,865 in 2009–2010 to 4,926 in 2016–2017 (Borooah, 2020). Moreover, benefits under these schemes were claimed to be cashless basically up to the coverage amount including pre-and post-operative care, diagnostics, drugs and transportation but hospitals overcharged and some cases found the problem of ‘double billing’ basically illegal copayments for either drug, diagnostic tests and others (Garg et al., 2020).

Even if we set aside government initiatives and wait for their appropriate implementation, as well as increased public investment in health, the problem of inadequate financial security for the health of our country’s residents does not go away.

Government-sponsored health insurance schemes targeted a certain segment of the population based on their income and wealth position, such as BPL card holders and workers in the unorganised sector. However, the AYUSH-PMJAY aimed to have covered the lives of 500 million approximately 40% of India’s population covering more of the poor people including BPL. Bhat et al. (2018) mentioned as ‘targeting the people’ is one of the most difficult aspects of successfully establishing large-scale health insurance systems given the limitations of targeting observed previously.

Uninsured Population Requires Attention

The estimated 500 million population which is approximately 40% of the whole population are said to be protected through central government-sponsored health schemes. There are fully state-sponsored schemes like one in Chhattisgarh where non-poor families are also covered against hospital care up to Rs. 50,000 annually (Garg et al., 2020). In West Bengal, one scheme named ‘Swasthya Sathi’ was operational from 2016 and targeted to cover lives of diverse low-earning workers as well as state government contractual employees and civic volunteers until in 2021 it is announced that all families irrespective of income status (except those having any other state-sponsored health protection or allowance) will get protection up to Rs. 5,00,000 annually. The success of such a program is yet to be known. It may seem impractical to provide coverage to such a large population without charging a premium at this time of escalating medical healthcare costs, which is why empanelled private hospitals refuse to accept such health cards.

Now, 99.74 million persons (as per IRDAI report 2019–2020) were covered under Private health insurance including group health business either by employers or purchased from other financial institutions. This figure excludes personal and travel insurance as well as health policies sold by life insurance companies.

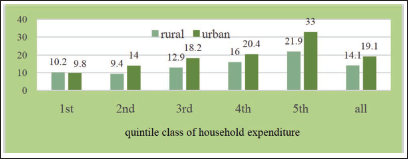

Even if we exclude CGHS and employer-provided schemes, Government Supported Health Insurance, State level schemes, CBHI an estimated 548.43 million people (taken from Bhat et al., 2018) are without any financial protection, and we will find that in proportion to lower wealth quintiles, higher quintiles have more coverage both in rural and urban areas, according to the NSSO’s 75th Round report on health (see Figure 9). Pandey et al. (2018) mentioned in the article the proportion of households experiencing CHE increased more in the poorest than in the richest quintal (as cited by Hati et al., 2019). This opens the door for the private voluntary health insurance market to cover a larger portion of the population by safeguarding lives.

Development of Strategies for Expansion of Business

Building Awareness Along with Product Innovation

India is traditionally a saving-led economy so always they find an investment component in their policy. Even though the mechanisms of health insurance and life insurance are vastly different, most consumers are unaware of this. Money-back policies, as well as profit-sharing, equity-linked and mutual fund investments, are the most popular (Krishnamurthy et al., 2005; Thomas & Sakthi Vel, 2011). Many people believe that if hospitalisation does not occur, such insurance is pointless and a waste of money when they could save the money in other ways while also receiving a return on their investment. People view of it as an investment, but if they grasp the risks and uncertainty of the future and take this into account, it will be more sellable. IRDAI, agents and executives can come forward to educate and inform the public about the mechanism and benefits available to them. In addition, more benefits such as wellness advice (dietary and exercise), OPD care, will be added to existing features such as ‘bonus in sum insured for claim free year’, and ‘top-up facility’, ‘free medical checkups’. Products are to be customised keeping in mind the uninsured population of various age and income groups. Recently, from 1 April 2020, IRDAI has launched ‘Arogya Sanjeevani’ which is a basic and standard health insurance policy for providing in-patient medical coverage including COVID treatment from 1 to 5 lakh. Particularly to give coverage for COVID patients, ‘Corona Kavach’ and ‘Corona Rakshak’ launched last year. Again, for the critical disease coverage like cancer, cardiac ailments, renal failure and liver transplants ‘critical illness cover is available’. One article published on the Money control website by Kulkarni (2021) emphasised the importance of having such a policy where the cost of such treatments is high as well as there is expensive post-hospitalisation care. This policy will help in case treatment leads to job loss or loss of income for a long period. Hence, awareness and proper guidance to customers with benefit both parties.

Inclusion of Out-patient Coverage

Inpatient hospitalisation is covered by health insurance policies or government-sponsored health insurance programs. According to Bhat et al. (2018), growing O-O-P health expenditures are generated by outpatient care spending, as evidenced by NSSO data. In addition, almost 75% of outpatient care is provided in a private setting, as patients prefer. Furthermore, some households may seek (or refuse) care to avoid financial hardship. This may be level playing field for private health insurance business. Currently, several general insurance companies offer outpatient coverage (for an additional price) that covers benefits such as medical practitioner and specialist fees, routine check-ups and vaccines. The task of such OPD claim management may be complex for the insures as it is a frequent event and no standardisation is there in medicine prices. This may be the problem that prevents insurers to regularise OPD cover (Gambhir et al., 2019). Despite this issue, if insurers can sell more OPD policies, it will benefit people with chronic diseases such as diabetes, sinusitis, arthritis and other conditions that necessitate frequent doctor visits on the one hand, and insurance companies will earn more premiums on the other. Most importantly, it will bring insurers into the ‘Curative’ segment. According to Thomas and Sakthi Vel (2011), insurers can gain greater knowledge and flexibility into managing care by increasing such benefits, and hence preventative care can reduce needless hospitalisation.

Partnership with Community-based Health Insurance Organisations

Purohit (2020) proposed Community Based Health Financing, which allows resources to be pooled to cover the uncertain risk of medical bills in exchange for regular premium payments. As per the CSO data NGOs engaged in health insurance are only 0.144%. This distribution suggests a possible scope for the private health insurance business. Notable schemes like ACCORD, SEBA and SEWA have a partnership through GIC with Mediclaim. Therefore, this mechanism along with the expertise of health insurance companies can expand the business along with overall coverage to poor, remote and various target group populations in the urban and rural areas of the country.

Introduction of Risk-sharing Mechanism Along with Indemnity

The indemnity health insurance model is simple to implement, and India is now doing so. However, there is an issue when there is no standard referral mechanism in place that can provide a first-level prospective utilisation evaluation to prevent overuse of medical resources. As previously noted, hospitals are accused of using a system of ‘double billing’, or charging insured patients more for the same treatments as uninsured patients. The indemnity aspect of the contract has led to cost inflation rather than cost reduction (Thomas & Sakthi Vel, 2011). Hospitals salivate at the thought of treating patients who are covered by comprehensive insurance. It’s impossible to avoid milking them. The US which is said to be pioneer in health insurance tried managed healthcare models, where hospitals ‘step into the shoes of insurers’ by dispensing with their services, instead taking role of a ‘meddlesome middleman’ (Murlidharan, 2021). Also, advocated by Thomas and Sakthi Vel (2011). To decrease misuse of in-patient facilities, contract negotiations with healthcare providers are essential, as is strict monitoring of the healthcare delivery mechanism and financial incentives on the part of policyholders.

Elimination of Value Fragmentation

‘In India, health insurers are the most affected entity because of the misalignment in cost-management objectives between the insurers and hospitals (who drive up the cost by supplying medical services in excess’—(Thomas & Sakthi Vel, 2011, p. 409).

Fragmentation cannot be effectively addressed only by controlling medical demand. It is necessary to create an integrated system that connects primary health care (preventative), doctors, insurers, hospitals and patients. At the moment, India lacks well-organised health records, making it difficult for insurers to assess risks. As you progress along the preventive path, your risk decreases since insurers will have a better understanding of your health profile. To address this issue Prime Minister announced on the occasion of 74th Independence Day (15 August 2021) to issue Health ID cards (Sarkari Yojana, 2022) to the residents to our country under ‘one nation one health card scheme’. All the tests and treatments done by a resident will have to be recorded in that database. The integrated system will prevent unnecessary paperwork and improve underwriting efficiency reducing operating expenses. Claim Settlement procedure will be easy and hassle-free leading to efficient service delivery to customers.

Summary and Conclusion

In India, Private Voluntary Health Insurance has come a long way since liberalisation, with rising medical demand, good Private Sector Healthcare infrastructure and a recognition of the necessity for health insurance to cover unforeseeable medical catastrophes. Premium income is increasing, yet there are several challenges with this business that have been identified in this study. To make the health insurance business sustainable, an integrated effort by insurers, IRDAI, doctors, Health Care Providers and government engagement is essential. In the non-life market, the Insurance Density Ratio, or average premium paid per person in India, is quite low. Insurance agents play a crucial role in making health insurance more inclusive. They must raise awareness and assist potential clients in enrolling in health insurance packages. Selling higher-sum-assured insurance is not a solution for meeting bottom-line criteria; instead, effective risk diversification is necessary. Most notably, the cost structure of health care for pharmaceuticals, diagnostics and surgical procedures must be regulated, which is a pressing requirement it is necessary to have an efficient service delivery system and an easy-to-use claim settlement process. Many people bought health insurance policies in the last year 2020 between April and September due to the COVID-19 outbreak. Despite rising premiums and enrollment, health insurers are finding it difficult to resolve claims originating from the second wave of the COVID outbreak in India, which has increased hospitalisation. The cause for this is due to the exorbitant fees imposed by private hospitals and the indiscriminate use of medical resources. In the indemnity model, a Managed Care Mechanism where Insurance Companies and Health Care Providers collaborate and share risks might be created. In general, a holistic approach is required to make the health insurance business a profitable one.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.