Abstract

This study examines the linkages between foreign equity flows and stock market returns of Bursa Malaysia. Specifically this article intends to investigate whether past stock returns influence foreign equity flows or vice versa in a short-term time horizon. To explore the linkages between these two variables, this study employs bivariate vector autoregressive (VAR) model. In addition, to determine the causal relation between stock returns and foreign equity flows, this study utilizes VAR Granger causality test. The findings of this study provide evidence that foreign institutional investors are momentum traders, while foreign retail investors are contrarian traders with regard to the return of Malaysian equity market. Another main finding is that domestic equity returns have an effect on fund flows of foreign retail investors and vice versa; meanwhile, there is a positive causal relation between domestic equity returns and foreign institutional fund flows.

Keywords

Introduction

The relation between foreign equity flows and stock market returns has received wider attention in the finance literature. Two main areas are being studied: first, whether foreign investors are ‘return chaser’, meaning that foreign equity flows are being influenced by equity return and second, whether foreign equity flows affect returns of the local bourse. Basically, there are two main findings on the linkages between foreign equity flows and stock market return. The first group of findings show that foreign equity flows and equity returns are positively correlated (Adaoglu & Katircioglu, 2013; Bohn & Tesar, 1996; Brennan & Cao, 1997; Chandra, 2012; French, 2011; French & Li, 2012; French & Naka, 2013; Froot, O’Connell & Seasholes, 2001; Grinblatt & Keloharju, 2000; Jinjarak, Wongswan & Zheng, 2011; Lin, 2006; Lin & Swanson, 2004; Phansatan et al., 2012; Samarakoon, 2009). These findings suggest that foreign equity investors demonstrate positive feedback or momentum trading behaviour in buy and sell trades, respectively. In this scenario, foreign investors purchase more than what they sell of the local stocks when the stock market shows an upward trend and they purchase past winning stocks and sell past losers.

The second group of findings show that foreign equity flows have an impact on the equity return of the local bourse (Chandra, 2012; Dahlquist & Robertsson, 2004; French & Li, 2012; Froot & Ramadorai, 2008, Froot et al., 2001; Ülkü & İkizlerli, 2012). All of these findings can be linked to price pressure hypothesis (Scholes, 1972), which states that prices will depart momentarily from their information-efficient values due to uninformed shifts in demand surplus so that compensation can be furnished to those that provide liquidity.

Basically, there are two main groups of investors in the stock market, namely, the retail (local and foreign) and institutional (local and foreign) investors. However, the focus of this study is only on foreign investors both retail and institutional. The sample selection is motivated by past findings which show the existence of linkages between foreign equity flows and local stock market returns. For instance, the findings of Froot et al. (2001) demonstrate that international investors pursue momentum trading strategies for their equity investment, particularly in an emerging market. Momentum trading, also known as positive feedback trading, exists when net fund flow is positively and significantly associated to lagged local market returns and past fund flows. Alternatively, contrarian trading or negative feedback trading occurs when there is a negative and significant relationship between foreign fund flows and past market returns of local stock market.

The remainder of this article is organized in the following manner. The second section reviews past literature on the topic under study. The third section provides the objectives and rationale of this study. The fourth section discusses the data and methodology employed in this study. The fifth section presents the analysis of the results and lastly, The sixth section provides the conclusions of this study.

Review of Literature

Foreign equity flows are considered as an important element for the development and stability of a financial market particularly in emerging countries, including Malaysia. Knowledge on how the international investors behave in relation to local stock market performance can help the authority of the local countries to improve several aspects of its stock market, such as, liquidity. Among the area of studies that have been carried out with regard to foreign investors is the association between their trading activities and domestic market return. This area will be explored further in this study using data of Malaysian stock market. The findings of this study will contribute to the body of literature especially in the area of behavioural finance as well as enrich the knowledge with respect to the linkages between foreign equity flows and equity return of local stock market.

Prior literature documents voluminous studies on the linkages between international flows of equity capital and stock market return of the local countries. Basically, there are two main findings on this topic. First, foreign equity flows are found to be influenced by stock return of the local countries and second, foreign equity flows are found to have an impact on stock market return. These two main findings show evidence of bidirectional relationships between foreign equity flows and stock return.

The findings of previous studies that show the direction of causality runs from stock return to foreign equity flows involving emerging markets include Bekaert, Harvey & Lumsdaine, 2002; Bohn & Tesar, 1996; Brennan & Cao, 1997; French & Li, 2012; French & Vishwakarma, 2013; Ülkü & İkizlerli, 2012; Samarakoon, 2009. In the study of Bekaert et al. (2002), they provide proof that positive returns’ shocks have an impact on the short-term international equity flows into emerging markets. They relate their findings to momentum effect of equity trading.

Froot et al. (2001) provide an ample study on daily foreign portfolio flows into and out of 44 countries for a 4-year period from the year 1994 to 1998. The results of their study reveal several evidences regarding the relationships between international equity flows and equity returns. Among the evidences is that past returns have an impact on equity flows which is consistent with positive feedback trading by foreign investors. Jinjarak et al. (2011) also obtain similar findings as those by Froot et al. (2001). Based on a sample comprising 67 countries, they find that past equity returns have valuable information in predicting future equity flows.

Brennan and Cao (1997) examine the correlation between foreign purchases of equities and local index return in 16 emerging markets. Their findings support the positive association between foreign purchases of equity by US investors and domestic market returns. The phenomenon persists even though the lagged domestic market returns are substituted with the contemporaneous returns.

Samarakoon (2009) explores the interaction between foreign equity flows and stock market returns using daily trade data of Colombo Stock Exchange (CSE) which is categorized according to investor classes. The findings of the study reveal that equity trades either buy or sell by local and foreign investors, both individual and institutional, are significantly and positively associated with past returns. This signifies that all classes of investors demonstrate positive feedback trading strategies in equity buying and contrarian trading strategies in equity selling.

A study by French and Vishwakarma (2013) on the dynamic linkages between foreign equity flows and equity return of Philippines Stock Exchange also provides similar findings as those by Bekaert et al. (2002) and Brennan and Cao (1997). Another study by Chandra (2012) also supports the findings that stock market returns influence the trading behaviour of foreign equity investors. Parallel results also are observed in a study by French and Li (2012) and Lin (2006) involving Brazilian stock market and Taiwan’s stock market, respectively.

Several studies examine the relationships between stock returns and foreign equity flow using data of Istanbul Stock Exchange (ISE). Among others is a study by Adaoglu and Katircioglu (2013) which reveals that monthly stock return has an influence on monthly net foreign equity flows for the pre-EU accession negotiation period (European Union accession negotiation of Turkey). A similar study also has been carried out by Ülkü and İkizlerli (2012) which shows that there is an existence of negative feedback trading behaviour of foreign investors with respect to past domestic returns in ISE. Nevertheless, the circumstances only occur in upward trend markets, particularly under macroeconomic instability.

Lin and Swanson (2004) examine the association between equity market returns and foreign equity flows for the eight largest emerging Asian stock markets. Their findings reveal that there is minimal proof of feedback trading. The equity flows are significantly positively influenced by past stock returns and the relationships are only observed in Malaysia and the Philippines stock markets. A later study by French (2011) on Johannesburg Stock Exchange (JSE) reveals that international equity investors investing in South Africa are due to high returns on JSE.

Even though most of the studies reveal that there are positive relationships between stock returns and foreign equity flows, French and Naka (2013), however, find opposite results. Their study signifies that there is trivial response to return surplus of positive shocks to US equity inflows to China and India. The inflows of US investors into Chinese and Indian markets are based on the fundamental values and unique characteristics of China and India, respectively.

Another category of findings on the relation between equity returns and foreign equity flows is that the latter has an impact on local stock returns. Among these is Lin and Swanson’s (2008) study which investigates international equity flows of US residents to several emerging stock markets in Latin America and Asia as well as to numerous developed markets in Europe, Canada and Japan. One of the findings is that information contribution argument is stronger than the feedback trading argument. In other words, the influences of equity flows on returns are stronger than the impact of past return on flows. Past literature on this subject matter includes Bekaert et al. (2002), Dahlquist and Robertsson (2004), French and Li (2012), Froot and Ramadorai (2008), Froot et al. (2001) and Ülkü and İkizlerli (2012). The findings of Chandra (2012) also are consistent with the findings of other researchers. However, the linkages are only in the very short term.

In summary, past literatures show that there are linkages between equity returns and foreign equity flows in both directions. However, studies on a similar topic are still scarce involving Malaysian equity market. Therefore, this study seeks to examine the linkages between equity return of local country market and international equity flows. In order to investigate the relationships among these two main endogenous variables, this study employs the vector autoregressive (VAR) model. This study attempts to fill a gap in the knowledge by exploring the causality using more recent data.

Objectives and Rationale of Study

The objective of this study is to investigate the daily dynamic relation between trading behaviour of foreign equity investors and stock market returns of Bursa Malaysia. Specifically, this study intends to provide answers to two main research questions. First, whether past stock market returns affect foreign equity flows and second, whether past foreign equity flows affect stock market returns. Besides that, this article intends to examine the direction of causality (either unidirectional or bidirectional) between stock market returns and fund flows of foreign equity investors.

In the context of Malaysian stock market, not many studies have been carried out on the behaviour of equity flows of foreign investors. This may be due to the restriction on the availability of data relating to investors’ trading activities on Bursa Malaysia. Therefore, the findings of this study will contribute to the body of literature on the topic of behavioural finance particularly involving emerging economies. By analyzing the relation between foreign equity flows and return of the local stock market, the findings would be able to assist other investors, especially local traders, either retail or institutional, in their trading strategies on Bursa Malaysia.

In addition, foreign funds can give benefits to the local country in terms of liquidity and cost of capital. In this respect, the liquidity and cost of capital of the local country would increase and decrease, respectively. Syamala, Chauhan and Wadhwa (2014) also assert that the involvement of foreign institutional investors in the domestic equity market helps to lower down the information asymmetry and consequently enhance the liquidity level of local equity market. Hence, the policymakers in Malaysia would be benefited from this study by being able to know the behaviour of foreign investors, both institutional and retail, in terms of equity purchases in order to attract them to invest in Malaysian equity market. Moreover, selling transactions of foreign equity investors can affect the stability of local stock markets. Thus, not only the purchasing activities but also the selling activities of equities need to be understood by Malaysian policymakers.

Data and Methodology

The main data of this study is the net flows (NF) of foreign funds both institutional and retail into Malaysian equity market which are obtained from Bursa Malaysia. The NF is in the form of number of shares traded and the value of trades (in Ringgit Malaysia). The NF is represented by equation (1) as proposed by Hong and Lee (2011) and Phansatan et al. (2012).

where NF Jt is the net flows of foreign equity on day t by group J (institutional and retail investors), BUY Ji,t is cumulative buy on day t by investors J in the form of either the number of shares traded or value of trades and SELL Ji,t is cumulative sell on day t by investors J in the form of either the number of shares traded or value of trades. Another main variable employed in this study is the stock market return. The stock market return is calculated as shown in equation (2).

where KLCIR is return of FTSE Bursa Malaysia Kuala Lumpur Composite Index (FBMKLCI), IND t is index closing value on day t and INDt−1 is index closing value on day t − 1.

The index closing value is obtained from Bursa Malaysia. The data on trading behaviour is only made available starting October 2009; hence, the sample period for this study covers from October 2009 to February 2013. Throughout this article, the following abbreviations are used which are KLCIR, FINF, FRNF and TFNF. Specifically, the meaning of each abbreviation is as presented in Table 1.

Abbreviations of Variables

Past literatures provide evidences that there are linkages between foreign equity flows and domestic market returns (Adaoglu & Katircioglu, 2013; Bekaert et al., 2002; Bohn & Tesar, 996; Brennan & Cao, 1997; Chandra, 2012; Dahlquist & Robertsson, 2004; French, 2011; French & Li, 2012; French & Vishwakarma, 2013; Froot & Ramadorai, 2008; Froot et al., 2001; Grinblatt & Keloharju, 2000; Jinjarak et al., 2011; Lin, 2006; Lin & Swanson, 2004; Phansatan et al., 2012; Samarakoon, 2009; Ülkü & İkizlerli, 2012). Hasbrouck (1991) recommends that the joint interaction between foreign equity flows and equity returns should be modelled as VAR system. Thus, this study employs a bivariate VAR model to explore the trading behaviour of foreign equity investors as well as the relations between their trades and domestic stock returns. In the VAR system, both foreign equity flows and domestic index returns are treated as endogenous variables. The VAR model has been used as the methodology by other researchers in previous studies, such as, the study by Samarakoon (2009). The advantage of using VAR model is that it has a characteristic that enables each variable in the system to be treated symmetrically. In addition, the variables in the system are permitted to influence each other; therefore, this allows feedback to be incorporated in the analysis (Enders, 2004).

As mentioned in the above paragraph, the VAR model will be utilized to relate foreign equity flows to past returns as well as returns to past foreign equity flows. With regard to the relations between foreign equity flows and past returns, if equity index returns positively and significantly influenced net foreign equity flows, this signifies that foreign equity investors follow a momentum or positive feedback trading strategy. This is because the investors purchase more than what they sell when the domestic equity market has already been in upward trend. On the other hand, the investors follow a contrarian trading strategy if the equity index returns negatively and significantly influences net foreign equity flows. In this situation, the investors tend to trade in the opposite direction to past domestic equity returns. With respect to the relations between returns and past foreign equity flows, a positive price momentum is observed if prices keep rising and falling following equity purchases and sales, respectively. On the contrary, a negative price momentum is observed when the reverse situation occurs (Samarakoon, 2009).

In this study, we extend the VAR approach by utilizing the Granger causality test in order to examine the causal direction between foreign equity flows and local country equity returns. In order to run VAR model, all the time series data used in this study need to be stationary and the optimal lag length needs to be determined. Therefore, this study carried out a unit root test to determine the non-stationarity of the variables as proposed by Dickey and Fuller (1979, 1981). The determination of the appropriate number of lags is based on the Akaike information criterion (AIC).

Analysis of Results

Descriptive Statistics and Correlation Coefficients

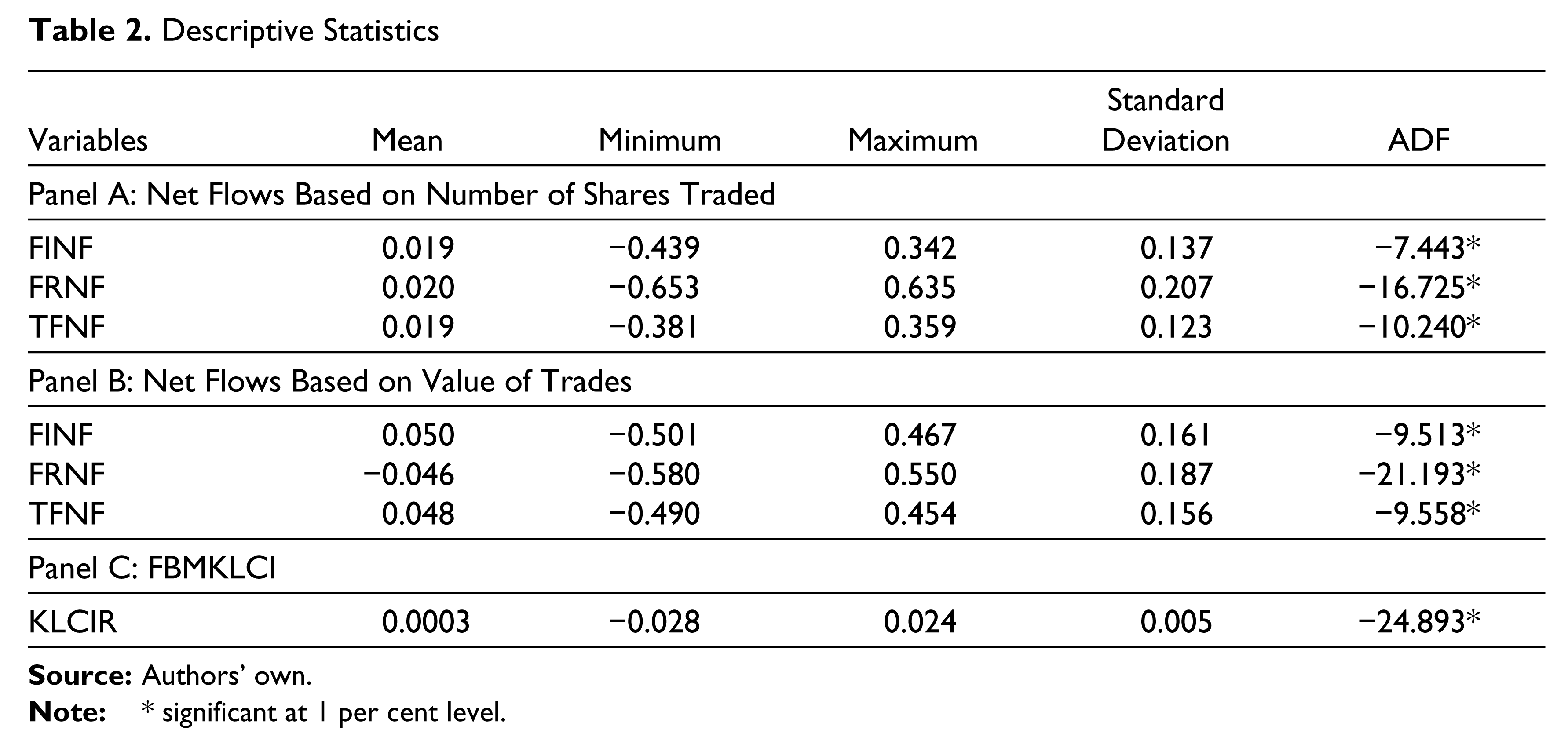

The summary statistics of all variables utilized in this study, namely, domestic equity returns (KLCIR), foreign institutional net fund flows (FINF), foreign retail net fund flows (FRNF) and total foreign equity net fund flows (TFNF) into local market for a period from October 2009 to February 2013 are reported in Table 2. Panel A describes the statistics for NF of foreign funds based on number of shares traded, while Panel B describes the NF of foreign funds based on value of trades. Mean, minimum, maximum, standard deviation and augmented Dickey–Fuller (ADF) test statistics together with their respective critical values are reported for all data series. The mean values for FINF, FRNF and TFNF of Panel A and FINF and TFNF of Panel B are positive meaning that on average foreign investors buy more than sell for the sample period used in this study. The figures of ADF test statistics in Table 2 also show that there is no unit root for the data series under study. All the time series of FINF, FRNF and TFNF (both based on number of shares traded and value of trades) are stationary at level while the time series of KLCIR are stationary at first difference. The stationarity of the data enables this study to proceed with bivariate VAR and VAR Granger Causality test to determine the causal relation between returns of local equity and fund flows of foreign equity.

Descriptive Statistics

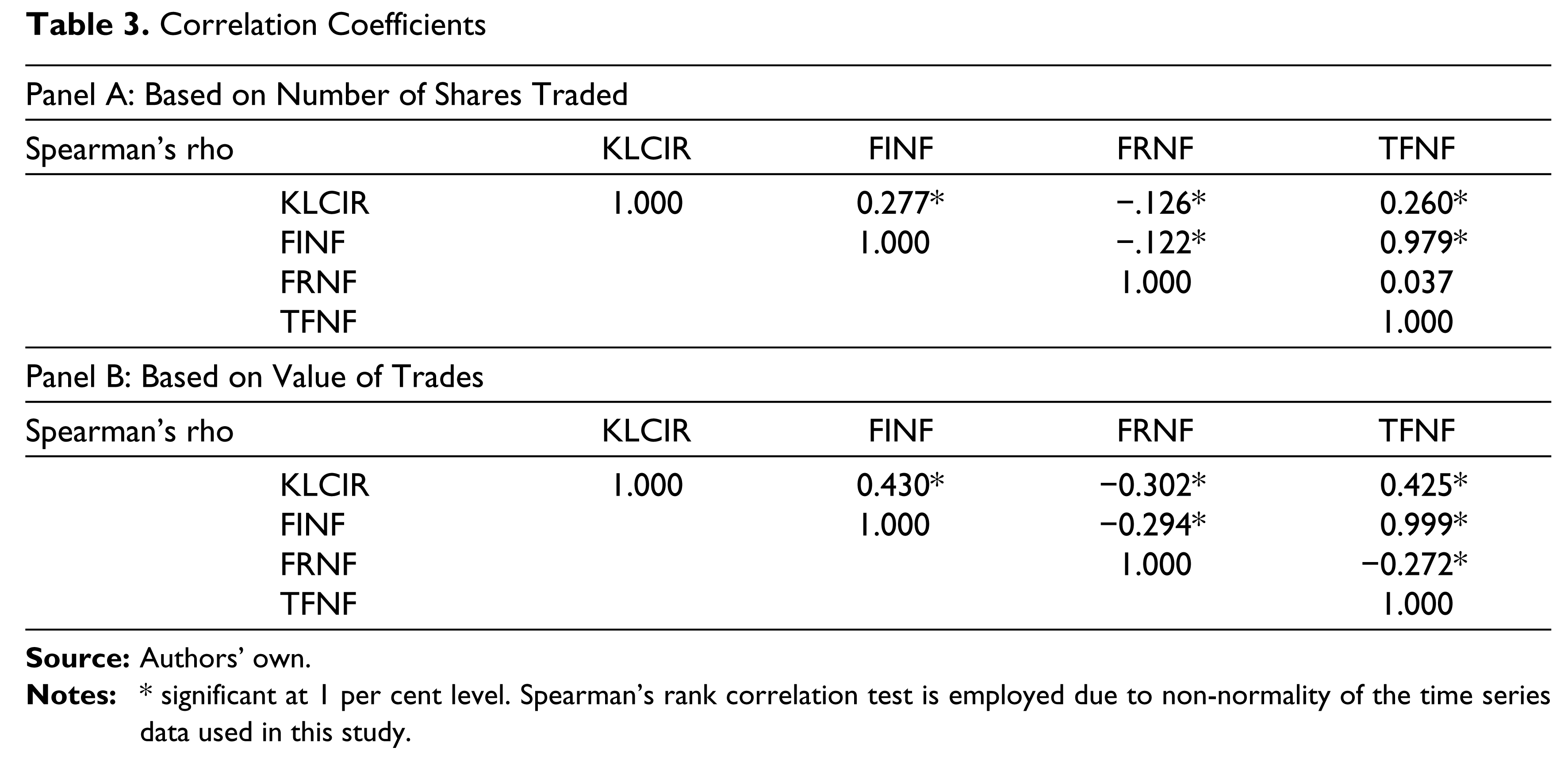

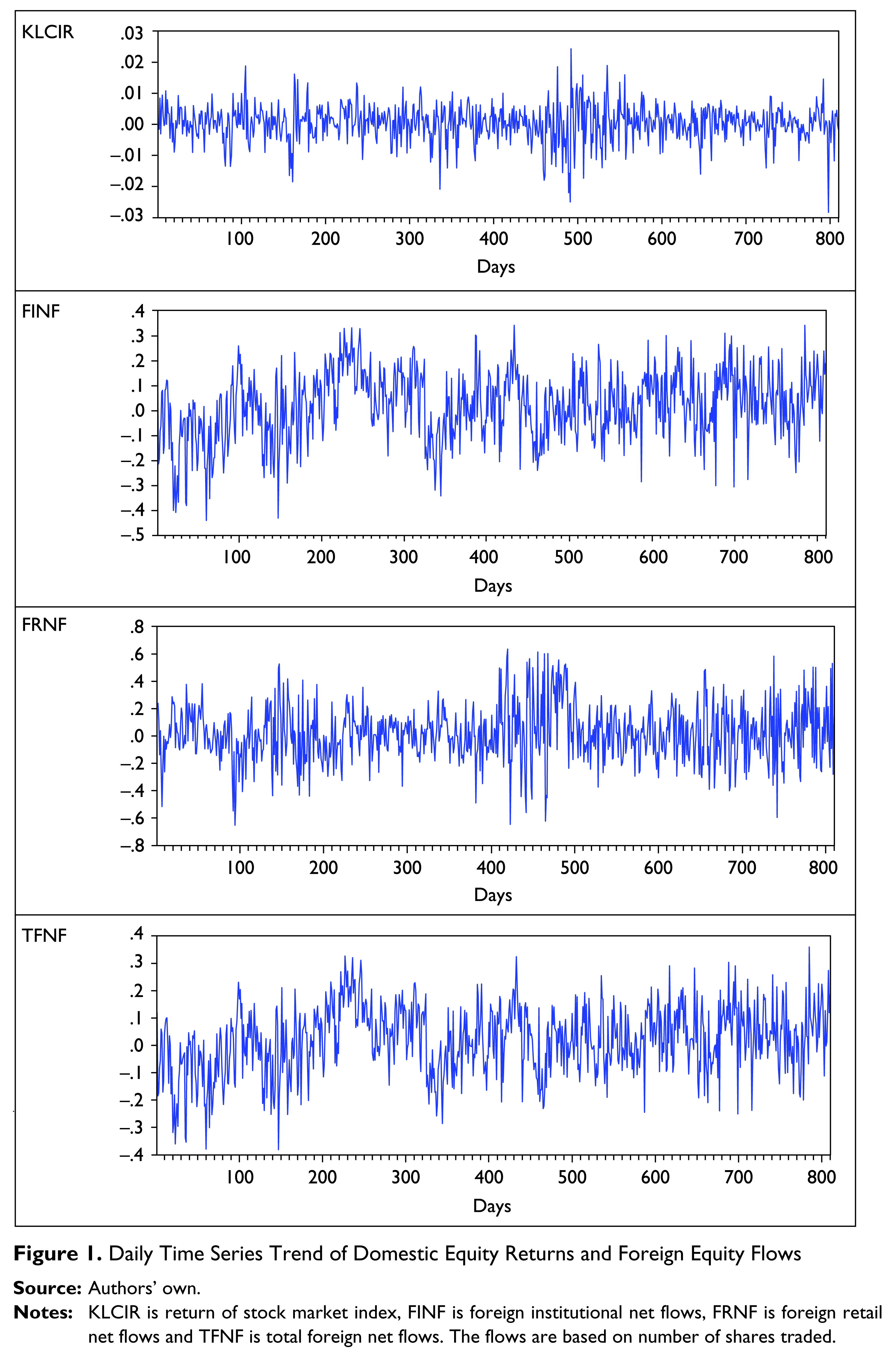

The correlation coefficients among local stock return and six measures of foreign equity flows are presented in Table 3. The cross correlation between domestic equity returns and foreign NF of fund provides preliminary insights about the relationships between returns and foreign NF into local equity market. The findings of this study show that domestic equity returns and foreign institutional equity flows are significantly positively correlated at 1 per cent level. Meanwhile, the correlation coefficients between domestic equity returns and foreign retail equity flows are negative and significant at 1 per cent level. This suggests that the domestic stock returns are positively and negatively associated with foreign institutional fund flows and foreign retail fund flows, respectively. The results in Table 3 imply that foreign institutional investors trade in opposite directions as compared to foreign retail investors in relation to the performance of local stock market returns. These findings apply both to the results in Panel A and Panel B of Table 3. The behavioural differences in trading activities between foreign institutional and retail investors in relation to the performance of local stock market are supported by the graph in Figure 1.

Correlation Coefficients

Vector Autoregressive Estimates

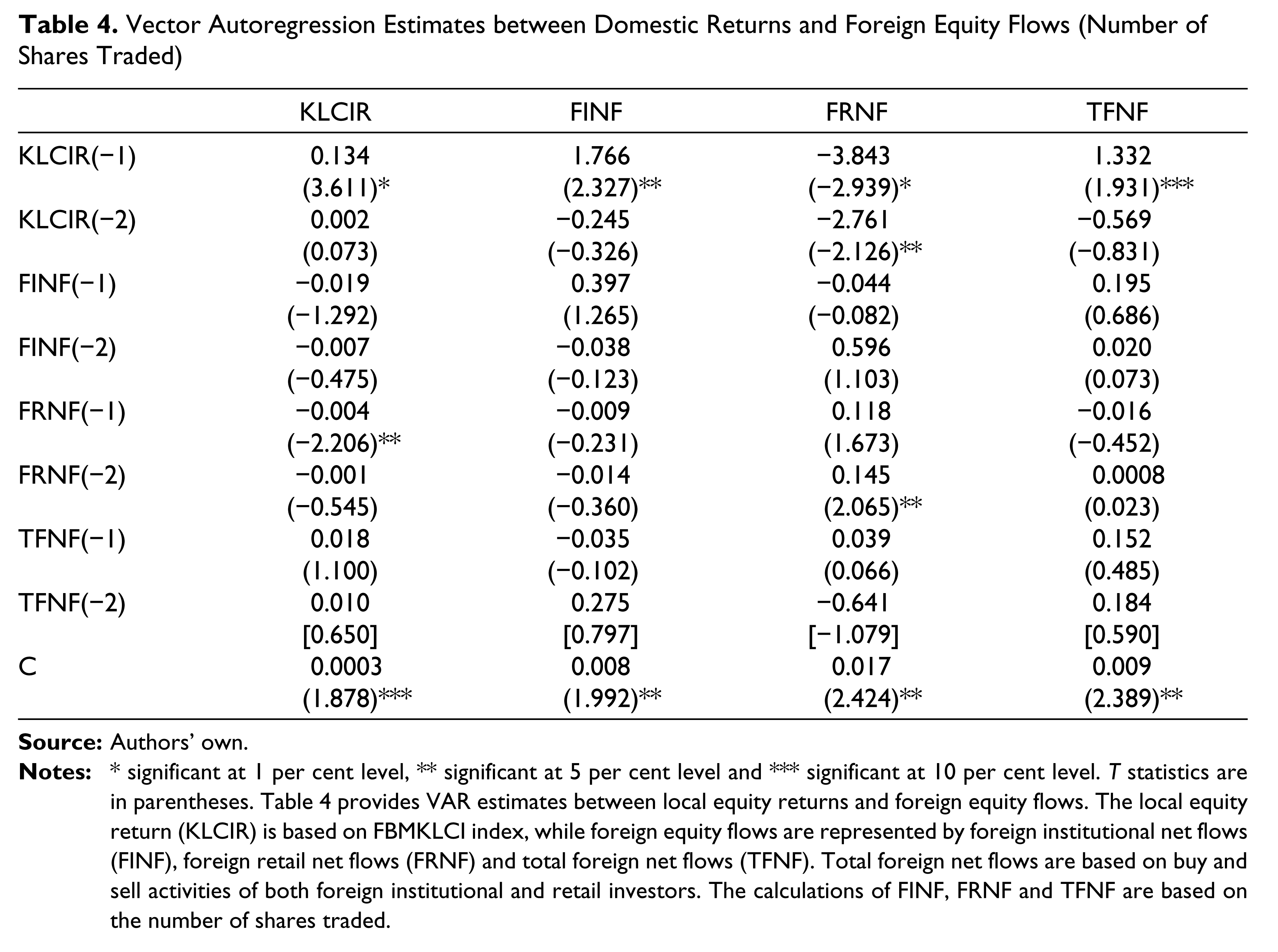

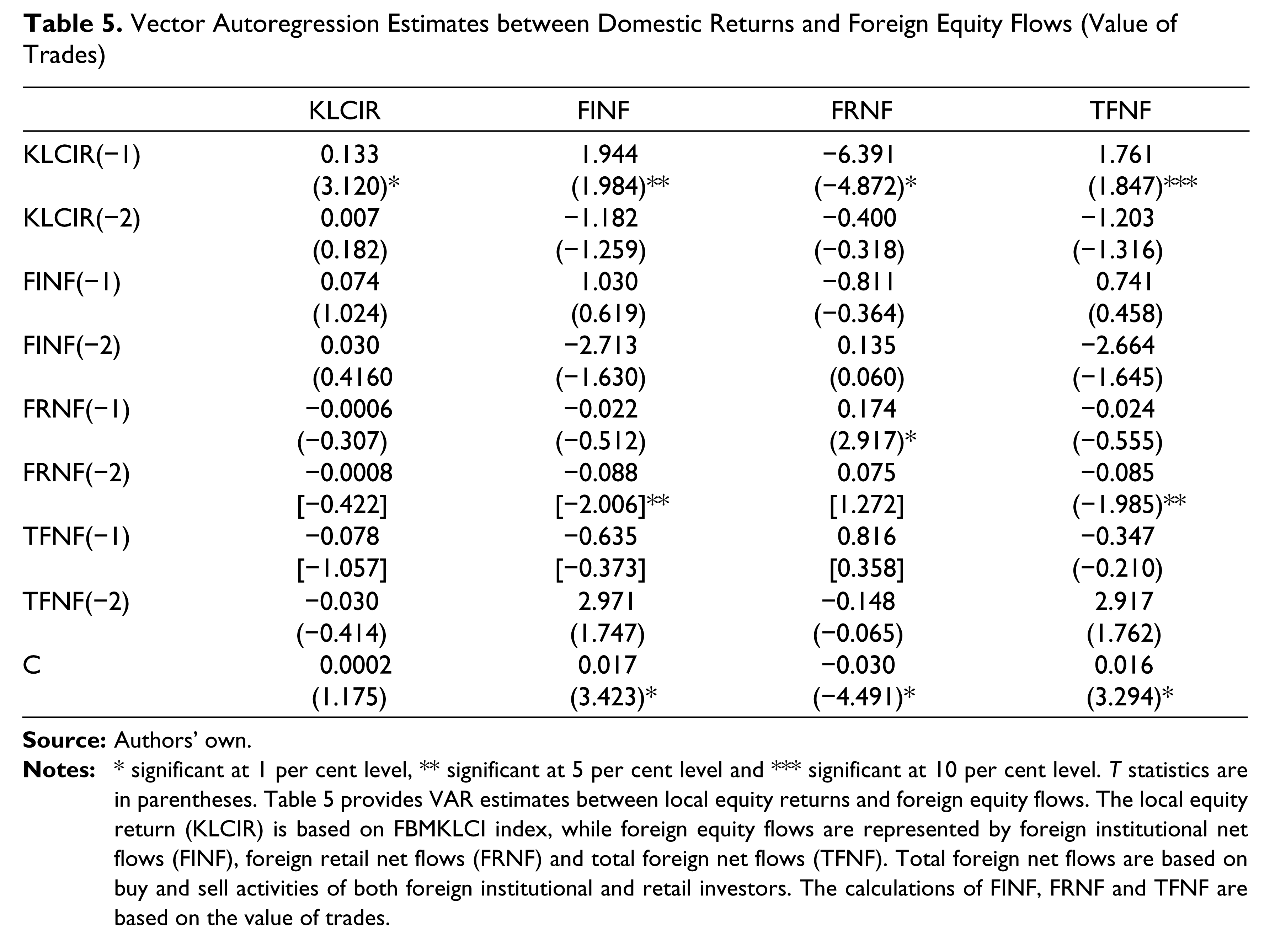

Tables 4 and 5 report the coefficients’ estimates based on VAR model between domestic equity returns and foreign equity flows. The results in both Tables 4 and 5 reveal several remarkable findings.

Vector Autoregression Estimates between Domestic Returns and Foreign Equity Flows (Number of Shares Traded)

Vector Autoregression Estimates between Domestic Returns and Foreign Equity Flows (Value of Trades)

First, current domestic equity returns are significantly and positively related to the previous day’s returns. Second, NF of foreign institutional investors also have significant positive relationships with lagged domestic equity returns. These findings are consistent with the findings of Brennan and Cao (1997) which document that the trading behaviour of US investors is positively linked with the return of emerging markets either in contemporaneous or in lagged form. They claimed that the US investors being at an informational disadvantage compared to domestic investors of emerging markets thus utilize stock returns as information signal in their trading activities.

Third, NF of foreign retail investors also are associated with lagged domestic equity returns. However, the relationship is negative. This finding is consistent with the findings of Chiang et al. (2012) and Ülkü and İkizlerli (2012) and this signifies that the investors tend to trade in the opposite direction to past market returns.

The above findings demonstrate that both institutional and retail foreign investors behave differently in relation to domestic equity returns. The results of this study are consistent with the findings of Hong and Lee (2011) using the data of Korean stock market. Moreover, other studies, such as, Barber, Odean and Zhu (2009) and Bae, Yamada and Ita (2008), document similar findings. They assert that the behaviour of institutional and retail investors is quite different in their reactions to stock return changes. Grinblatt and Keloharju (2000) provide further evidence on the behaviour of retail and institutional investors in relation to stock market returns. Among the findings of their study is that the trading of retail investors exhibits a stronger return–volume relation as compared to the trading of institutional investors. This phenomenon portrays that institutional and retail investors have different interpretations on the information related to past movement of stock prices. In addition, the findings of this study suggest that foreign institutional investors and foreign retail investors demonstrate a positive and negative feedback trading strategies, respectively. Therefore, it can be concluded that foreign institutional investors are momentum traders, while foreign retail investors are contrarian traders with regard to the return of Malaysian equity market. This study provides evidence consistent with that of Lin and Swanson (2004) with respect to investors positive feedback trading strategies involving Malaysian equity market. Since the findings of this study also reveal that foreign retail investors follow negative feedback trading, then positive feedback trading cannot be considered as a universal occurrence. A study by Ülkü and İkizlerli (2012) documents evidence of negative feedback trading for ISM. They relate the negative feedback trading to foreign investors’ perceptions on valuation.

Fourth, unlike foreign institutional investors, there is a linkage between lagged net fund flows of foreign retail investors with current domestic equity returns. Contrary to the previous studies (Lin & Swanson, 2004; Samarakoon, 2009), the relationship is negative. The negative linkages between foreign retail net purchases on domestic return are not consistent with the findings of Froot and Ramadorai (2008), Froot et al. (2001) and Lin and Swanson (2004). Their studies show that there are positive relationships between Malaysian equity market returns and current or past foreign equity flows. Lin and Swanson (2004) associate the positive relations between local equity return and foreign equity flow with information dissemination hypothesis.

Fifth, the current net fund flows of foreign retail investors are strongly related to their past trading behaviour for the estimation of foreign NF based on both the number of shares traded and the value of trades. Sixth, there is a significant association between the trading activities of foreign retail and institutional investors. However, the association is negative and is applicable for the calculation of foreign NF based on the value of trades.

In summary, there are linkages between foreign equity flows and return of Malaysian equity market. The relationship is a bidirectional involving foreign retail fund flows; meanwhile, there is a unidirectional relationship involving foreign institutional fund flows. The causal relation runs from past local stock market returns towards foreign institutional fund flows.

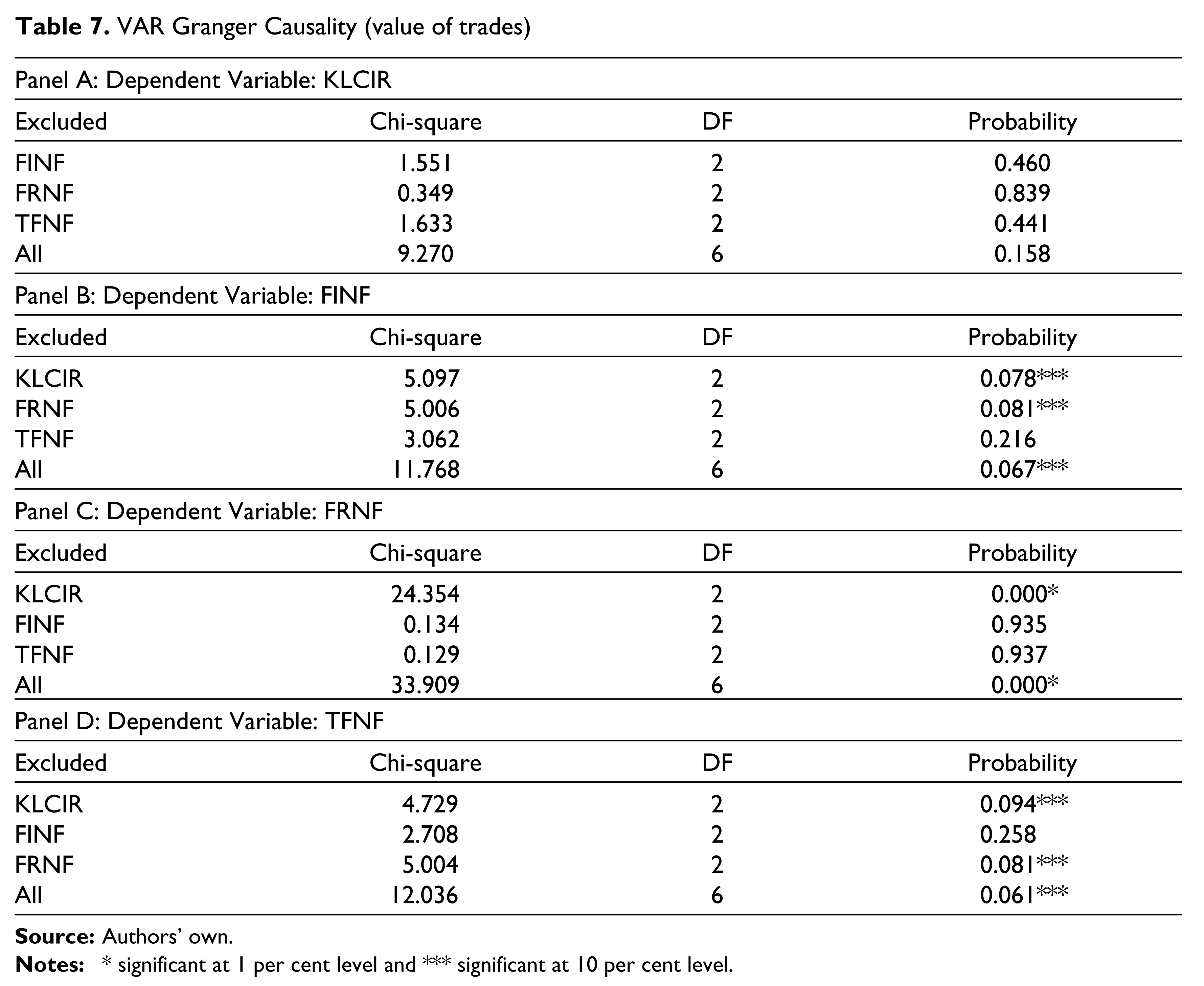

VAR Granger Causality

Regression results of VAR analyses in Tables 4 and 5 reveal that there are linkages between past equity returns and net foreign equity flows of institutional and retail investors. Results in Table 4 also show that there is a relationship between past trading activities of foreign retail investors and local equity returns. To investigate the causal directions between equity returns and foreign equity flows, this study employs VAR Granger causality test and the results are reported in Tables 6 and 7, respectively. The results of Panel C in both Tables 6 and 7 demonstrate that causality runs from domestic equity returns towards foreign equity flows of retail investors. The finding of this study, which indicates domestic returns have an impact on foreign fund flows, is consistent with previous studies on emerging equity market, such as, Bekaert et al. (2002), Bohn and Tesar (1996), Brennan and Cao (1997), French and Li (2012), French and Vishwakarma (2013), Ülkü and İkizlerli (2012) and Samarakoon (2009).

VAR Granger Causality (number of shares traded)

VAR Granger Causality (value of trades)

In addition, the results of Panel A in Table 6 demonstrate that foreign retail fund flows have prediction ability for future domestic market return. This finding is consistent with the results of past studies, for instance, Bekaert et al. (2002), Chandra (2012), Dahlquist and Robertsson (2004), French and Li (2012), Froot and Ramadorai (2008), Froot et al. (2001), Lin and Swanson (2008) and Ülkü and İkizlerli (2012). Thus, these imply that there is a bilateral relationship between local equity returns and trading activities of foreign retail investor in the short term and these are consistent with the studies of Chandra (2012), French and Li (2012) and Froot et al. (2001). The results in Tables 6 and 7 derived from VAR Granger causality technique revalidated the results reported in Tables 4 and 5. The results in Panel B of Tables 6 and 7 also reveal that foreign institutional fund flows are affected by domestic equity returns. As revealed by the results in Tables 4 and 5, the coefficients for the linkages between lagged domestic equity return and foreign institutional fund flows are positive. In this respect, foreign institutional investors are said to be at an informational disadvantage compared to local equity investors, and they trade on new information with a lag.

Conclusions

This article investigates the dynamic relation between domestic equity returns and foreign investors’ fund flows into local stock market. The domestic equity returns are calculated based on FBMKLCI index, while foreign investors’ fund flows are based on activities buy and sell of both foreign institutional and retail investors. The main focus of this study is to examine the association between domestic equity returns and fund flows of foreign investors as well as the causal direction between these two main variables. This enables us to explore the behavioural pattern of foreign investors both institutional and retail in relation to local equity market performance; they follow either a momentum or a contrarian trading strategy with regard to equity investments. The main findings of this study include: (i) there is a bilateral causal relation between local stock returns and foreign retail fund flows, (ii) causality runs from local stock returns towards foreign institutional fund flows and (iii) foreign institutional investors are momentum traders and foreign retail investors are contrarian traders with regard to the return of Malaysian equity market.

Footnotes

Acknowledgements

This research is conducted under Young Researcher Incentive Grants Scheme awarded by the National University of Malaysia (Grant no: GGPM-2013-003).