Abstract

Capital structure is a very significant area in strategic financial decision making of firms. Several factors, both internal and external, influence a firm’s choices of capital structure. It is found that the research on this topic has mainly covered industrialized countries. Very little is known about the decision-making process on capital structure of firms in developing countries. The aim of this study is to investigate for the period 2000–2013, using panel data, the role of long-run effect of country-specific factors, such as prime lending rate, rate of inflation, gross domestic product (GDP) growth, size of capital market, corporate tax and civil unrest on capital structure choices among Sri Lankan firms listed in Colombo Stock Exchange (CSE).

Introduction

The choice of capital structure is perhaps one of the prime areas of attraction for many researchers in the area of finance. It deals with a firm’s choice of the types of securities to be issued. Myers (1984) rightly refers to capital structure as ‘the capital structure puzzle’. The determinants of optimal capital structure and its influence on a firm’s decision still remain unsolved, giving ample scope for further research. This decision can be influenced by several internal as well as external factors, termed determinants of capital structure. In fact, internal factors and their impact can be managed by a firm, while country-specific (macroeconomic) factors are beyond its control. Knowing the direction and impact of these factors will definitely help the mangers to make effective debt/equity decisions, which not only impact maximization of its returns but also ensure its survival in today’s turbulent environment. Available research in this area has mainly dealt with internal factors of firms, hardly going into the external factors, leaving a large space for research in the latter.

Literature Review

Capital structure theories have been widely documented and tested empirically in literature since the seminal work of Modigliani and Miller (1958). Different theories and hypotheses were presented by many researchers hoping to arrive at an optimal capital structure. These theories and hypotheses include net income (1959), net operational income (1959), traditional approach theory, Modigliani and Miller theory (1958, 1963), static trade-off theory (1973), pecking order theory (1984), signalling theory (1977), agency cost theory (1976), free cash flow hypothesis, dynamic trade-off theory (1984) and market timing theory (2002).

In the above-mentioned theories, two main theories, namely, pecking order theory and trade-off theory, are given importance. The first one is based on the information asymmetry between managers and other stakeholders of the company. It predicts that firms prefer to use internal financing when available and choose debt over equity only when external financing is required. An alternative to pecking order theory is the trade-off theory which grew out of the debate on the Modigliani–Miller theorem. According to this theorem, a company’s capital structure decision involves a trade-off between the tax benefits of debt financing and the costs of financial distress and, consequently, zeroes in on optimal capital structure, taking into consideration tax advantages, bankruptcy costs and agency costs. These theories help to understand the nature of corporate capital structure as well as to identify the potential internal and external factors. The inadequacy of literature on the influence of the macroeconomic environment on the corporate capital structure in an emerging market, thus, demands a structured theoretical and empirical analysis in order to identify the role of macroeconomy in the determination of corporate capital structure.

To be frank, the large number of studies addressing the determination of capital structure at firm and industry levels (Harris, 1991; Titman & Wessels, 1988) rarely considered the influence of country-specific factors on capital structure decisions. Even the few studies that did had no consistent conclusion. Furthermore, while literature is available in studies that examine the importance of firm-specific factors in determining a firm’s financing choice in the context of developing countries, empirical evidence on the influence of country-specific factors on this is very much limited. The objective of the present study is, therefore, to examine the role of long-run effect of country-specific factors on capital structure decisions of listed firms in Sri Lanka.

Fortunately, the capital structure is a well-developed topic in the corporate finance literature. The main approaches of the literature concentrate on the internal aspects of the firms that explain the level of the debt-to-equity ratio. The macroeconomic factors, hitherto treated as abstracts, are gaining importance in recent discussions. Thus, capital structure issues are getting concentrated on the individual firm level as well as the aggregate economy level. At the individual firm level, evidence has evolved into finding firm-specific determinants that influence its financing pattern (Claggett Jr, 1991; Frank, 2003; Rajan & Zingales, 1995; Titman & Wessels, 1988). Meanwhile, the empirical work at the macro level compares capital structure practices of firms between economies and regions (Bartholdy et al., 1997; Booth, Aivazian, Demirgüç-Kunt & Maksimovic, 2001; Haron, Ibrahim, Mat Nor & Ibrahim, 2013; Krishnan & Moyer, 1997; Rajan & Zingales, 1995). Further, from the research of Booth et al. (2001) and De Jong, Kabir and Nguyen (2007), it can be inferred that even though the capital structure in developing countries is affected by the same determinants as in developed countries, differences persist across countries, indicating that country-specific factors have a direct as well as indirect impact on firms’ capital structure.

The macroeconomic factors that are found to have a significant effect on the financing choice of a company are gross domestic product (GDP) growth rate (Bas et al., 2009; Dincergok & Yalciner, 2011; Gurcharan, 2010), rate of inflation (Camara, 2012; Demirguc-Kunt & Maksimovic, 1996; Frank, 2009; Gajurel, 2006; Gulati & Zantout, 1997; Hanousek & Shamshur, 2011; Mateus, 2006; Nakamura & Basso, 2009; Sett & Sarkhel, 2010), stock market development (Bopkin, 2009; Dincergok & Yalciner, 2011; Gajurel, 2006; Sett & Sarkhel, 2010), prime lending rate (Antoniou et al., 2002; Bas et al., 2009; Dincergok & Yalciner, 2011), corporate tax (Bartholdy & Mateus, 2008; De Angelo & Masulis, 1980; Graham, 2000; Gropp, 2002; Haugen & Senbet, 1986; Scholes et al., 1990) and civil unrest. 1

There are very few researches carried out in Sri Lanka with respect to capital structure to explore the determinants. Such studies (Buvanendra, 2010; Prahalathan, 2007; Smarakoon, 1999), which mainly focused on internal factors of capital structure on listed companies in Sri Lankan context, did not take into account the country-related factors. In light of the studies, a set of country-related factors selected for this study that are commonly used in the literature are GDP growth rate, rate of inflation, stock market development, prime lending rate, corporate tax and civil unrest. The area of capital structure is relatively unexplored in Sri Lanka as well as other emerging economies. Limited research work, though done, mainly dealt with firm-specific factors. The present study tries to fill this void to some extent by providing empirical evidence from a developing country’s perspective.

Methodology

Data and Sample

This research covered 50 companies selected from the listed companies of the Colombo Stock Exchange (CSE), based on highest market capitalization. The changes in their structure can reflect on the CSE as well as the economy. The companies under banking, finance and utilities sectors were eliminated due to their peculiar financial and business nature. The study analyzes the data covering a period of 14 years, that is, from 2000 to 2013. In firms which have their financial year ending on 31 March each year, data from the period 2000–2001 to 2013–2014 are considered, whereas in companies which have their financial year ending on 31 December each year, the data collection period is from 2000 to 2013. The information about the capital structure, profitability and size was obtained from the published annual reports of the respective companies in the CSE website as well the handbook of the CSE. The country-specific variables are obtained from a variety of sources. Gross domestic product growth and inflation are taken from World Bank World Development Indicators. Corporate tax rate is obtained from KPMG’s corporate tax rate survey. Remaining variables are collected from Sri Lanka Socio-economic Data 2013 and Economics and Social Statistics of Sri Lanka 2010, published by the Central Bank of Sri Lanka.

The variables used in this study and their measurement are largely adopted from existing literature (de Jong et al., 2007; Bopkin, 2009; Jõeveer, 2005). To examine the influence of country-level factors on capital structure, the following have been considered and their influences on capital structure have been analyzed. The selected country-specific factors, known as independent variables, are:

Prime lending rate (PLR): The average rate of interest charged on loans by commercial banks to private individuals and companies. Rate of inflation (INF): Annual inflation rate of growth in consumer price index (CPI), since the CPI is the official price index in Sri Lanka. The consumer prices are also more suited than wholesale prices to reflect pressures in demand. GDP growth rate (GDPG): The change in GDP in current market prices from a period to the next. Size of the capital market (SCM): The ratio of overall market capitalization to GDP. Corporate tax rate (TAX): The tax rate on the operating profits of the firms during a given taxable period, that is, the percentage at which Civil unrest (CUR): Dummy variable with a value of 1 during civil unrest and otherwise 0. (The 30-year civil war in Sri Lanka ended by 2009.)

a corporation is taxed.

In order to calculate the leverage (LEV) ratio 2 of a firm, we adopt the definition of capital structure as the ratio of total debt to total assets in book values.

Internal Factors

According to previous literature, there are some key internal factors, such as profitability, size, tangibility, growth, non-debt tax shield and other such factors, that have a significant effect on the financing choice of a company. However, in view of their relatively higher influence, profitability and size are commonly selected as internal factors of the study.

Theoretical predictions yield no consistent conclusions for the correlation between profitability and leverage. Trade-off models argue that profitable firms have greater needs than less profitable firms to shield income from corporate tax and that they should consequently borrow more. While pecking order theory suggests an inverse relationship between profitability and the level of debt, agency-based models give predictions upon this issue in the following ways: In the free cash flow theory, Jensen (1986) defines debt as a disciplining device to force managers to pay out profits and as a result, cash flow wasted in empire-building is mitigated. Therefore, a positive correlation between profitability and leverage is implied; in a signaling framework, profitable firms are assumed to use debt as a signal of the firm’s quality, thus this theory also predicts a positive relationship. However, most empirical studies confirm the negative correlation between profitability and leverage (Mukherjee & Mahakud, 2012; Rajan & Zingales, 1995; Titman & Wessels, 1988; Wald, 1999), while there is little positive relationship supported by empirical studies. The return on capital employed (ROCE) ratio, which is calculated by dividing the operating profit of the company by the capital employed (total assets – current liabilities), is used as a proxy of profitability (PROF).

As suggested by previous studies, it is generally agreed that size is positively associated with leverage. This positive relationship is verified by most studies with a few exceptions. For example, Rajan and Zingales (1995) found size to be positively associated with leverage in G-7 countries, except Germany, and this exception is hard to explain from the view of institutional differences. On the other hand, size may also be a proxy information asymmetry between insiders and outsiders. Large firms are thought to be associated with lower degree of information asymmetry when compared to smaller ones. Fama and Jensen (1983) argue that larger firms provide more information to outside investors than smaller firms. Benefiting from the low information asymmetry, larger firms are expected to have easier access to debt market and borrow at a lower cost. In prior studies, size of the firm is usually defined as the amount of assets or the value of total sales and most of the times the natural logarithm of these figures is taken in order to correct for non-normality of the sample. In this study, the natural logarithm of total asset is used as a proxy of size (SZ). 3

Model Specification

This study employed panel data procedures because the sample contained data across firms and over time. The use of panel data increases more informative data, more variability, less collinearity among variables, more degrees of freedom and more efficiency (Baltagi, 2005). Several techniques are available to deal with panel data analysis, but two panel econometric techniques, the fixed- and the random-effects models, are very important. The fixed-effects model takes into account the individuality of each firm or cross-sectional unit included in the sample by letting the intercept vary for each firm, but still assumes that the slope coefficients are constant across firms. The random-effects model estimates the coefficients under the assumption that the individual or group effects are uncorrelated with other explanatory variables and can be formulated (Mahalakshmi, Thiyagarajan & Naresh, 2012). Further, this study also employed the Hausman test (1978) to determine which estimation model, whether fixed- or random-effects model, best explains our empirical results.

The general form of the panel regression model can be stated as:

where i and t represent the firm and time, respectively. Y is the dependent variable which is a measure of capital structure. β0 is a scalar, β1 is K × 1 and Xit is the ith observation on K explanatory variables. Here, μit is a random term expressed as μit = αi + εit where αi is individual-specific effect or cross-section error component and εit is the remaining combined cross-section and time series error component. The expanded model for this study is stated as follows.

Fixed-effect model

Random-effect model

where

β0 is the constant term, β0i is the y-intercept of firm i, β1 – β6 are the coefficients of the independent macro variables, β7 and β8 are the coefficients of the independent internal factors, i is listed firm, t is time or year, LEV is leverage, PLR is the prime lending rate, INF is the rate of inflation, GDPG is the growth rate of GDP, SCM is the size of capital market, TAX is corporate tax rate, CUR is civil unrest, PRO is profitability, SZ is size and μit is the error term.

Results and Discussions

Tests for Data and Models

Correlation Analysis

To test the existence of multicollinearity among the key country-specific factors (independent variables), we perform correlation which examines the degree of association between any two variables. The results of correlation analysis are shown in Table 1.

Correlation Matrix

From Table 1, it can be seen that most cross-correlation terms for the explanatory variables are fairly small (less than or near to 0.5), thus giving no cause for concern about the problem of multicollinearity among the explanatory variables.

The Unit Root Test of Panel Data

Stationarity can be tested by finding out if the time series contains a unit root. There are various panel unit root tests. The tests proposed by Levin, Lin and Chu (LLC) (2002), Im, Pesaran and Shin (IPS) (2003) are used for this purpose. According to Baltagi (2005), it is advisable to analyze the outcome of both the LLC and IPS tests due to the fact that the limited power of LLC test assumption of unit root across cross sections is the same.

Table 2 presents the panel unit root tests. Based on the results, it can be concluded for all variables that the null of a unit root is strongly rejected in all cases. At 1 per cent significance level, both models confirmed that variables are stationary. Therefore, the data can be tested for both fixed- and random-effect regression.

Panel Unit Root Tests

Hausman Test

Hausman test (1978) is used to choose between a fixed-effects model and a random-effects model. The null hypothesis of the Hausman test states that there is no significant difference between the coefficients of fixed- and random-effects estimators (Gujarati & Sangeetha, 2007). The results of the Hausman specification test are reported in Table 3.

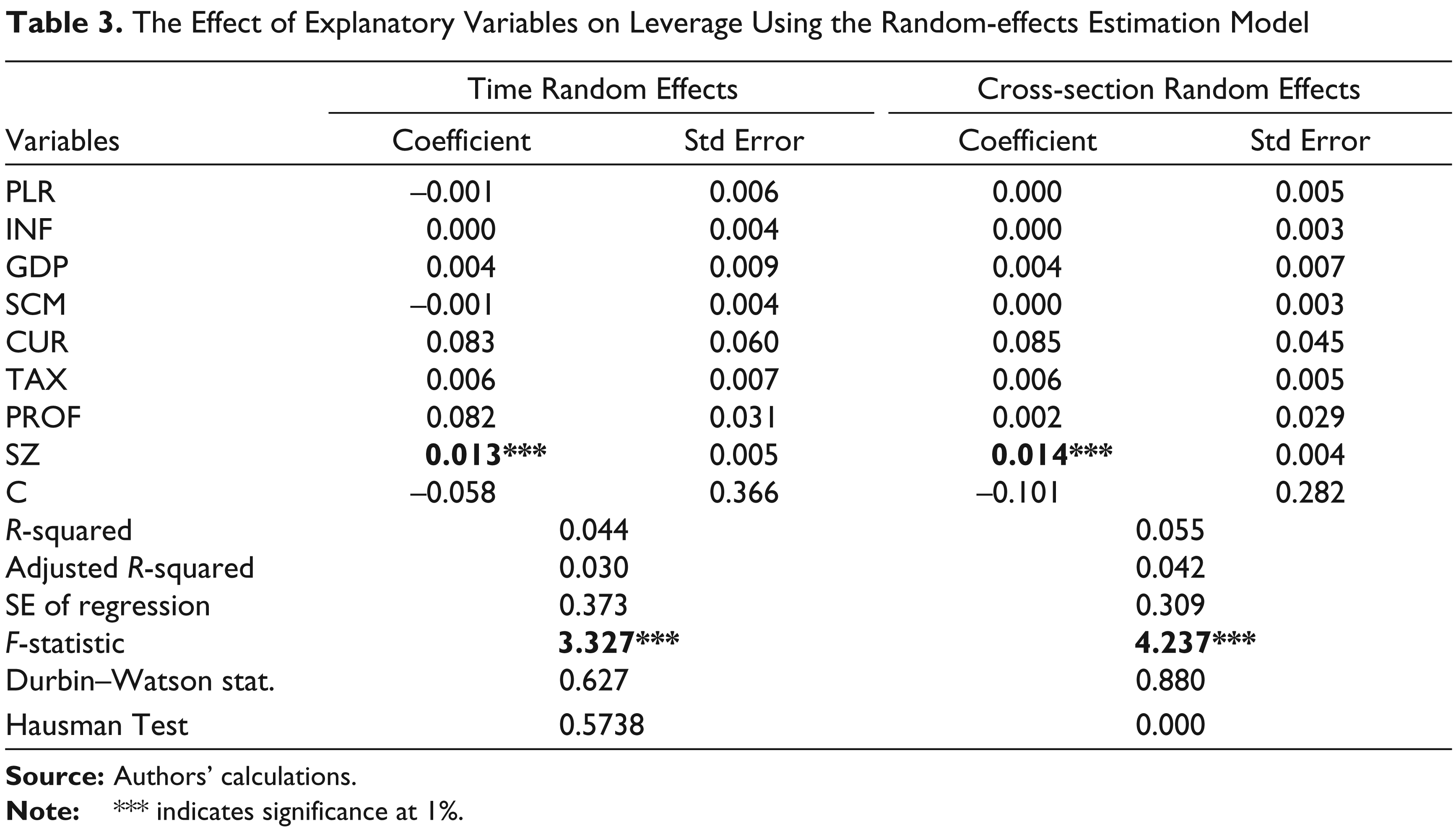

The Effect of Explanatory Variables on Leverage Using the Random-effects Estimation Model

Results indicate that the random-effect model is better than the fixed-effect model as the null hypothesis cannot be rejected at 10 per cent, since estimated chi-square value is statistically insignificant with leverage measure.

Results of Panel Data Analysis

The findings related to the impact of country-specific factors on the capital structure in the Sri Lankan scenario deviate from international findings in many ways. There is no concrete evidence from which we can state that there is a relationship between country factors and leverage. The results of the determinants of capital structure have been reported in Table 3.

The results are split into two parts, that is, time random effect and cross-section (across firms) random effect. The F-statistics show that the model is significant at 1 per cent, while adjusted R-squared values are very low. This implies that the selected macro variables have contributed nearly 4 per cent to the decision making on capital structure.

The country-specific factors do matter in determining and affecting the leverage choice around the world. The capital structure decision in the sample of Sri Lankan listed firms is unexpectedly insignificantly influenced by all country-specific factors, such as prime lending rate, rate of inflation, GDP growth, size of capital market, corporate tax rate and civil unrest. This is underwritten by the fact that the t-values of these variables become statistically insignificant, in both over time and across firms. It will be seen that the coefficients of the rate of inflation, GDP growth, corporate tax and civil unrest are positive, while those of prime lending rate and size of capital market are negative. The country characteristics, therefore, have no direct impact on the choice of capital structure. However, these do have indirect impact on firm-specific factors, which in turn predominantly influence the decision on firms’ capital structure. This view is reinforced by the findings of our previous study (Buvanendra et al., 2013).

In the Sri Lankan context, firm-specific factors are significant in predicting corporate financing decisions of the firms (Buvanendra, 2010; Prahalathan, 2007). The association between leverage and profitability of a firm is positive and apparently contrary to perceived wisdom. Though most empirical studies, such as Titman and Wessels (1988), Rajan and Zingales (1995), Michaelas et al. (1999), Booth et al. (2001) and Mukherjee and Mahakud (2012), reported a negative relationship between leverage and profitability, surprisingly, in this study, profitability is insignificant over time and cross-section. It could be due the type of measure used for profitability (ROCE) in this study. The fact that the sign of the coefficient is positive confirms the trade-off theory of capital structure, which says that more profitable firms have more debt-serving capacity and more taxable income to shield. One possible explanation for such counter-intuitive result could be a particular institutional feature of many developing countries including Sri Lanka, where strong government intervention in the credit allocation process allows profitable firms to receive preferential treatment in terms of access to credit as the lenders are confident that the companies will repay the loans. When granting loans, banks/lending institutions evaluate the financial performance of the company and they judge its repayment capacity.

The coefficient of the variable ‘size’ has a positive significant effect (at 1 per cent) on capital structure in both cases of time and cross-section random effects. Similar finding was reported by some earlier studies between firm size and leverage (Booth et al., 2001; Haron et al., 2013; Huang & Song, 2006; Rajan & Zingales, 1995; Wiwattanakantang, 1999; etc.). When the firms expand, they need funds for financing and when the internal funds are inadequate the companies tend to go for external financing (debt). This means, larger firms have more debt and these firms (sample represents the top larger firms) are usually more diversified and, therefore, have more stable cash flows. Consequently, they can afford higher levels of leverage. It is also rational that they have more assets for collateral to obtain debt. Thus, it is proved that the selected samples of larger firms of CSE have the opportunity to access bank credits easily in the Sri Lankan context. This is also supported by the samples selected for this study representing the larger listed firms. By virtue of the high value of their unpledged assets, they (larger firms) have a better opportunity vis-à-vis smaller firms to negotiate for loans on more favourable terms. The lending institutions consider them less risky compared to smaller ones.

It is underwritten by the fact that in the analysis in Table 3, once we used random-effect model with the inclusion of all selected variables (external and internal variables) of the study, the model revealed that out of the eight variables, size is the only significant one. Moreover, the researchers, due to the interest to see to what extent the significant variable, size, would by itself influence the capital structure decision, further analyzed this by using fixed and random models over time. Results are presented in Table 4.

Time Effect of Firm-specific Factor (significant variable only)

According to Table 4, there is no difference found between fixed- and random-effect models. Undoubtedly, the ‘size’ variable is positively significant under both random- and fixed-effect models. This is also supported by the samples selected for this study representing the larger firms of the CSE. They are able to use debt financing since they have more collateral than small companies and their earnings are also more stable. Clearly, size variable is the most consistent determinant of capital structure decision in Sri Lankan context.

Conclusion

This study presents an analysis of the country-specific determinants of capital structure choices of Sri Lankan firms, based on the data on top 50 Sri Lankan non-financial firms, listed in the CSE, for the period of 2000–2013 in a panel framework. This contributes to the empirical literature on capital structure in two ways. First, so far a very limited number of studies, which analyze, empirically, the country-specific factors and their influence on capital structure choices of firms in the Sri Lankan context, is found. The present study is, perhaps, the first one examining the long-run (14 years) effect of external factors on a firm’s capital structure decision. Second, the study uses panel data regression, such as fixed versus random-effect method of estimation, which is most appropriate for panel data analysis. In the Sri Lankan scenario, surprisingly, all selected country-specific variables, such as prime lending rate, rate of inflation, GDP growth, size of capital market, corporate tax rate and civil unrest, do not have any direct influence on the capital structure decision of firms. While the selected firm-specific variable, size, is a significant determinant of capital structure decision in Sri Lankan firms, it is useful to take into account the external factors appropriately in the analysis of firms’ capital structure decision, in view of the possible indirect impact of these factors, since a progressive trend in the economy is essential for the effective and sound decision making of a firm’s financial policies. This study focuses mainly on factors directly impinging upon decisions on capital structure. Delving into the external factors indirectly affecting these decisions demands an in-depth and extensive study, which therefore needs to be dealt with separately.

Footnotes

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.