Abstract

The aim of this study is to explore the relationship between corporate social responsibility (CSR) (defined through multi-stakeholder’s framework) and financial performance in the context of Rajasthan small and medium enterprises (SMEs). To achieve this objective, an exploratory study was conducted and data were collected using structured questionnaire based on pretested scale items from 384 SMEs and structural equation modelling (second order) was employed. The statistics shows the overall model fit, and the findings indicate a significant but a weak positive relationship between CSR and financial performance. The results are in conformance with previous research works (Weber, 2008). It is also evident from the findings that although SMEs are socially responsible towards their different stakeholders, CSR is not a part of their strategy; rather, it is more an informal and self-driven approach. For them, CSR is not meant for economic imperatives; rather, they associate it with religious spirit. Due to constraints that they face in terms of resource and personal that can be deployed for CSR activities, the notion of CSR among them is still philanthropic and non-institutionalized.

Introduction

Over the past 15 years, debate about corporate social responsibility (CSR) and its implementation in practice has increased in both variety and volume. Bowen (1953) was the first who introduced the idea of CSR, defining it as an obligation for companies to consider certain factors during the course of their business activities. The traditional concept of social responsibility (SR) of business states that an enterprise is socially accountable if it produces goods and renders services for profit maximization (Agatiello, 2008; Cochran & Wood, 1984; Greenwood, 2001). There has been a shift from this classical view of CSR towards a more modern philanthropic one. The modern concept of CSR states that the business enterprises in their usual process of business decision-making should pay due attention to the social interests of the people in the community (Sarkar, 2005) because it is not just an economic entity; it is a social entity too. Friedman (1970) was the stern critic of this emerging concept of CSR and strongly asserted that ‘the sole social responsibility of business is to increase its profits only’. He justified this argument by strongly advocating that only human beings have a moral responsibility for their actions; business managers’ duty is towards shareholders, and social issues are the domain of the state, not the corporation. Despite this dominant ideology that publicizes business as an economic entity, the argument itself has been criticized for not considering the role that corporations actually do play in society.

In fact, the stress on ethical business conduct actually originated from businesses themselves, as revealed by actions of corporate philanthropy, social initiatives and codes of conduct by many companies (Frederick, 2006). Moreover, social contract theory proposed corporations as a ‘social enterprise’. This emphasized the fundamental principle that the collective well-being ahead (Dahl, 1972). Moreover, increased global interdependence, privatization, liberalization, environmentalism and the rise in strategic importance of stakeholder relationships make CSR a global phenomenon and perceived as being relevant to corporations all over the world (Aras & Crowther, 2008). All these have contributed significantly to the modern concept of SR of business enterprises, to rethink and alter their goal of profit maximization, to create benefits for society and the environment and in return receive social appreciation and an increase in the sustainability of their business. From that point on, CSR came to be considered as the introduction and implementation of sustainable development within the sphere of management. Later on, in 2001, European Commission defines CSR as ‘A concept whereby companies integrate social and environment concerns in their business operations and interaction with their stakeholders on a voluntary basis, as they are increasingly aware that responsible behavior leads to sustainable business success.’

Corporate social responsibility has gradually emerged from Western countries in large multinational enterprises that have adequate resources. Later on, global appeal and collective effort of government and companies have standardized and promoted CSR. Gradually, CSR has seeped into all levels, from large firms to small, in both developed and developing countries. Although it has been reported that businesses in developed countries are viewing CSR as legal responsibility, businesses in developing countries consider CSR as philanthropic responsibility before legal responsibility (Visser, 2008). Since then, a radical change in the relationship between business and society is witnessed by the world. This makes CSR ubiquitous, and it creates higher demands on managers to take a positive stance on issues regarding SR and ethical behaviour (Carroll & Gannon, 1997; Schwartz & Gibb, 1999). Consequently, the relationship between business and society has moved on from paternalistic philanthropy to a re-examination of the roles, rights and responsibilities of business in society. While there is a growth in the demand for companies to demonstrate accountability with regard to their business actions (Feltus & Petit, 2009) and the corporate endeavours to engage in socially responsible behaviour, the questions in front of them were: To whom we are responsible? What are the benefits?

To address these questions, two different perspectives on the CSR concept have emerged which lead to the ‘stakeholder–shareholder’ debate. Freeman (1984) discarded the shareholder perspective (classical view) and defined CSR through the lens of the stakeholder theory. Stakeholders are defined as ‘those communities or groups which can affect and can be affected by the deeds of an organization as they share certain demands or expectations with them’. Literature inherently accepted the stakeholder’s perspective and recommended that if firms are able to manage their SR appropriately, then it will not only reduce risk but also improve their sustainability and overall performance (Agle & Mitchell, 2008; Prado-Lorenzo, Gallego-Alvarez, Garcia-Sanchez & Rodriguez Dominguez, 2008; Vaaland, Heide & Gronhaug, 2008; Wang, 2008). This proposition gave rise to a new notion that CSR can be a viable antecedent to sustainable superior firm performance. This has induced much interest among researchers and academicians to research on the link between CSR and financial performance (FP).

All these theoretical and empirical developments are made exclusively in the context of large firms where CSR practices are well formalized and publicized (Aupperle, Carroll & Hatfield, 1985; Pinkston & Carroll, 1994), but the research on CSR in small and medium enterprises (SMEs) context always remains a neglected area and demands a substantial attention (Lapointe & Gendron, 2004; Spence, Schmidpeter & Habisch, 2003). The research has been particularly scarce on SMEs in developing economies (Burton & Goldsby, 2007; Hammann, Habisch & Pechnaler, 2009; Jamali, 2008; Luken & Stares, 2005; Mankelow, 2008; Morsing & Perrini, 2009; Sweeney, 2007; Yu & Bell, 2007).

Conceptual Background

Characteristics of Small and Medium Enterprises

Small and medium enterprises are not like the large firms; there are significant characteristic differences (Bridge, O’neill & Cromie, 1998; Longenecker et al., 1996). Large firms are characterized by formal and well-defined controlled systems and organized structures, whereas SMEs are characterized by the informal structures, looser control systems, less documentation and fewer procedural hurdles (Beaver, 2002; Longenecker, McKinney & Moore, 1989). Moreover, in small firms, ownership and management are quite inseparable, unlike the large firms. They have their own beliefs, ideologies, concepts and practices. Small and medium enterprises behaviours are implicit in terms of the values, character, attitude, educational background, entrepreneurial orientation and leadership style (Chaudhry & Krishnan, 2007) of the owners, which can be a decisive factor for strategies and policies in them (Cambra-Fierro, Hart & Polo-Redondo, 2008; Fitzgerald, Haynes, Schrank & Danes, 2010; Longenecker, Carlos, William, Leslie & Joseph, 2006; Preuss & Perschke, 2010). Thus, in SMEs, control remains in the hands of the owners, potentially enabling him or her to make personal choices about the allocation of resources (Spence & Rutherfoord, 2001). Therefore, researchers proposed that concepts like CSR may be a different approach when applied to SMEs because of their idiosyncrasies as compared to large firms (Russo & Perrini, 2010; Spence et al., 2003).

Corporate Social Responsibility in Small and Medium Enterprises

It was argued that the term ‘CSR’ applies only to corporate structures or, more specifically, large corporations with shareholders. Small businesses are not part of this bandwagon because they simply are not made for this challenge due to their small size, different ideologies and peculiar characteristics. However, the SMEs contribution in terms of economic, environmental and social development in the growth of economies has turned the global attention towards discussion and analysis of the principles and practices in them. As a result, this sector no longer remains outside from the CSR movement (Jenkins, 2009; Murillo & Lozano, 2009; Spence, 1999; Spence et al., 2003). However, Schoenberger and McKie (2005) argued that in CSR, the word ‘corporation’ implies that size is a prerequisite and therefore the term is not fit for smaller firms. So they proposed the concept of business for social responsibility (BSR). Ortiz and Kühne (2008) use the term ‘responsible business behaviour’ (RBB) instead of CSR to describe a strategic concept that should help SMEs to discover what constitutes their real economic, social and environmental responsibilities. Although the above arguments recognize similarities in the nature of the approaches, the need is for adapting the global CSR concept to the specificities of the SMEs. Since SMEs are not just smaller versions of larger-scale businesses (Jenkins, 2004), they have different structures and management styles (Perez-Sanchez, 2003; Tilley, 2000) that affect the magnitude and scale of their CSR activities.

‘Silent CSR’ or ‘sunken CSR’ practices are reported in SMEs, which reflects that SMEs are often unknowingly socially responsible in their own special ways. It has also been stated that this attitude is intuitive rather than formalized, and despite many SMEs leaders not even knowing the term ‘CSR’, their behaviour corresponds in practice to the philosophy of CSR (Murillo & Lozano, 2006). Most of the SMEs are having family-owned firms, or are privately held by a small group of shareholders. Such organization structure leads to a close relationship between management and ownership and makes it easier to align the objectives of both. Therefore, CSR in SMEs needs a specific approach adapted to the informal and entrepreneurial characteristics.

In congruence to the above-stated views, Lepoutre and Heene (2006) proposed an elaborated definition of small business SR and advocated that a responsible entrepreneur is the one who not only incorporates fairness and honesty in their dealings with customers, business partners and competitors but also who, along with these motives, shows a caring attitude towards the welfare of the customers and generates an equal developmental opportunities for their employees by engaging them in various skill-enhancing training and workshops. In this way, they can be represented as ‘responsible citizens’ who respect the environment and use the natural resources rationally.

Agle and Mitchell (2008) state that SMEs acumen towards CSR can be better understood through stakeholder’s concept (Gupta, 2012). Similar arguments are proposed by Toyne (2003) and Jenkins (2006) in their studies, who found that all SMEs implicitly or explicitly described their CSR efforts along the lines of stakeholder’s theory only. Although it has been reported that SMEs’ definitions of stakeholders are as heterogeneous in nature as they are themselves, they talk about those who have an interest, stake or connection in the company and those who influence, affect or depend on the company (Jenkins, 2006), yet the identification of key stakeholders is consistent. They are employees, customers, environment and local community (Jenkins, 2004; Thompson & Smith, 1993). In the case of SMEs most commonly employed, CSR activities that are widely reported in literature are described in following paragraphs.

Vives (2006) studied the CSR measures implemented by SMEs and explored that they primarily segregate their responsibilities into three categories: first, internal social obligation in terms of health and social security measures, improvement of working conditions and development of talent; second, external social measures in the form of development of network link with the local economy through social integration; and finally, environmental measures, which include the reduction of energy consumption and wastes recycling (Russo & Tencati, 2009).

This is in line with recent literature (Roche, 2002; Saulquin & Schier, 2010), which examined CSR activities in SMEs and reported that great sensitivity is shown by SMEs in relation to the well-being of their employees and their community links. As SMEs have relatively few employees, many of them are known to owners, which lead to more tangible concerns for them. Similar results are proposed by Juwaheer and Kassean (2009), who state that for most of the SMEs, CSR activities are towards community projects and environmental and social initiatives. Common activities included making charitable donations, recycling initiatives, health and safety programmes and contribution to educational institutions (Blomback & Wigren, 2009).

It is also reported that SMEs have good links with the community as they are involved in sponsorship deals and back-to-work/employability schemes (Berger-Douce, 2008). The local community therefore would seem to be an important stakeholder for the majority of SMEs studied. The reason is that SMEs by their nature are local institutions, and most of their workforce comes from the same community. The same picture emerges in relation to employees who appear to be well treated within the majority of SMEs (Hammann et al., 2009). Therefore, CSR in SMEs means the likelihood to improve work climate and productivity, and to provide a source for differentiation and visibility in increasingly complex and dynamic markets (Murillo & Lozano, 2006).

Small and medium enterprises also share a high degree of interrelation with their environment or communities in which they often act as benefactors or local activists. They are more oriented towards solving day-to-day problems, and sharing informal relations and communication; for them, interpersonal relationships are very important (Spence & Lozano, 2000). Issues such as support of diversity, employee participation and benefits have been found to be of major importance in SMEs (Albinger & Freeman, 2000). Further examples of CSR activities towards employees in SMEs are fair wages, a clean and safe working environment, training opportunities, health and education benefits for workers and their families, provision of childcare facilities, flexible work hours and job sharing (Branco & Rodrigues, 2007). Based on case study evidence from seven European countries, Mandl and Dorr (2007) pointed out that particularly high employee satisfaction and publicity attributed to CSR activities can have a beneficial outcome in terms of customer loyalty. Although SMEs are quite heterogeneous in nature, customer relationships are very important for them, and they viewed it as their primary SR (Wilson, 1980).

Regarding environmental practices in SMEs, Cassells, Lewis and Findlater (2011) examined New Zealand-based SMEs, and results suggested that most of the firms have set measurable targets to reduce fuel and energy costs and reduce air and water polluting emissions and had a recycling programme (Collins, Lawrence, Pavlovich & Ryan, 2007). Moreover, firms are using reusable packaging. This emphasis on waste management is consistent with the findings of other studies that have also found that this is an area of environmental improvement where SMEs do engage due to the perceived ease of doing so (Tilley, 2000).

Specifically, existing research works highlight the trust and dependency of SMEs on the interpersonal relationships with the different stakeholder groups (Spence et al., 2003). It has been reported that such social initiatives and activities are not knotted to any particular revenue or business purpose. They are generally engaged to minimize certain harmful effects on society and to fulfil social obligations, in order to delimit environmental pollution, to enhance employee morale or pursue favourable legislative or governmental support (Dean, 2004). Because for SMEs, socially responsible behaviour is quite a sensitive matter as they might feel the immediate negative effects of irresponsible actions (Chrisman & Archer, 1984) being their standing and involvement in direct surroundings (Jenkins, 2004).

Corporate Social Responsibility and Financial Performance

For the past few years, the concept of SR has been the subject of intense, philosophically influenced debates (Carroll, 1979; Freeman, 1984; Friedman, 1962). For some, CSR is about ethical behaviour; for some, it is more or less a legal responsibility; for others, it is merely a cost; and for rest, it is about making profits (Friedman, 1970). Such diverse arguments lead to a substantial increase in the number of studies to articulate the relationship of CSR with firms’ FP. In order to investigate the nature of this link, researchers have used different instruments, reflecting an absence of conceptual and operational homogeneity. The proposed results contradict and mixed views were emerged in the available literature that suggests a positive relationship (Kapoor & Sandhu, 2010) between the two, negative as well as no relationship, while some reports only a tenuous link (Van Beurden & Tobias, 2008).

A large body of literature based on the social impact hypothesis (Cornell & Shapiro, 1987) supports the notion that CSR has a positive effect on FP in the long run (Clarkson, 1995; Ruf, Muralidhar, Brown, Janney & Paul, 2001; Stanwick & Stanwick, 1998). The underlying asset of this hypothesis is stakeholder’s theory (Carroll, 2000; Cooper et al., 2001; Davenport, 2000; Freeman, 1984; Smith, 2003), which states that the firm can satisfy its stakeholders through the alignment of firm’s business interests or resources with appropriate CSR initiatives (Waddock & Graves, 1997). This in turn will improve the image and reputation (Lewis, 2003; Vives & Peinado-Vara, 2003) of the firm and can improve employee morale (Brammer & Pavelin, 2006), which leads to improved productivity and ultimately improved performance (Basu & Palazzo, 2008; Husted, 2003; Orlitzky, Schmidt & Rynes, 2003; Pirsch, Gupta & Grau, 2007; Vander, Gerwin & Arjen, 2008). The most contemporary research addressing the CSR–CFP link has largely employed the Kinder, Lydenberg, Domini (KLD) rating to evaluate corporate social performance (Graves & Waddock, 1994; Turban & Greening, 1997). The KLD instrument rates firm behaviour on several stakeholder dimensions, including employee relations, community involvement, environmental management, customers, minorities and women, international stakeholders and product quality to gauge their social strengths and weaknesses. Studies that have used the KLD have generally concluded that CSR positively contributes to firm’s performance (Berman et al., 1999; Waddock & Graves, 1997).

Contrary to this, Friedman (1970) proposes trade-off hypothesis and advocates that maximizing the profits is the only sole SR of a company. According to this, those firms that are engaged in CSR are in fact at an economic disadvantage as they incur costs to implement such activities (Ullmann, 1985). Salzmann, Ionescu-Somers and Steger (2005) further stated that those firms that are actively involved in such social events are at the detrimental position comparatively to those firms that are not, because to fulfil the social obligations, firms need to spend the resources and money, which accelerate their expenses and, as a result, reduce their profitability. Therefore, FP of the firm is negatively related to the CSR (Moore, 2001; Vance, 1975).

Second, the managerial opportunism hypothesis states that managers have their own objectives, and these may contradict with the objectives of shareholders and other stakeholders (Williamson, 1985). Preston and O’Bannon (1997) believed that managers can only generate maximum returns by ignoring stakeholders’ interests when FP is high. Conversely, if the financial results are inadequate, managers will tend to cash themselves by investing more in social activities. Therefore, it can be suggested that poor FP leads to improved social performance.

According to supply and demand theory, which was introduced by McWilliams and Siegel (2000), the demand for the involvement of a firm in social activities may be unlike; it depends upon the market conditions that might maximize the profit, or it might remain unchanged. However, as soon as the market reaches an equilibrium, it annuls both the costs and the profits generated by CSR. This leads to a neutral relationship between CSR and FP. This theory finds support in the empirical findings of the literature too (Aras et al., 2010; Mahoney & Roberts, 2007; Nelling & Webb, 2009; Seifert, Morris & Bartkus, 2003), which states no relationship between CSR and FP.

Literature Review

Unlike the CSR literature centring on large corporations, there have been few studies exploring the relationship between CSR and FP in SMEs (Thompson & Smith, 1991). A brief literature review of such studies is as follows.

Nair and Sodhi (2012) studied CSR practices in Indian SMEs and found that adoption of such practices provides an edge to them in the form of winning and retaining consumers and business customers; commitment of employees; image and reputation with internal and external stakeholders; networking opportunities; creativity and innovation in business; and even costs savings from environmental measures. Further, they reported that most of the SMEs agreed that these competitive advantages in the long run will help them in responding to new demands and access to new information and markets, and will later materialize in the form of enhancement of their business scale. In this way, CSR positively influenced FP of the firms.

Torugsa, O’Donohue and Hecker (2012) studied the relationship between specified capabilities of Australian SMEs (which are defined in terms of shared vision, stakeholder management and strategic proactivity) and FP. For this purpose, proactive CSR is employed as a mediating variable and defined through economic growth and prosperity, social cohesion and equity and environmental integrity and protection. Findings revealed that proactive CSR fully mediates the relationship. Moreover, it is also reported that all the specified capabilities share a positive association with proactive CSR, which in turn improves the firm’s FP. Further, they concluded that SMEs can maximize their financial returns while proactively making progress towards CSR.

Bnouni (2011) studied the relationship between CSR and FP in French SMEs. Results of the study revealed that social responsible strategy cannot be sustainable in the SMEs context if a certain level of profitability has not been reached (Berger-Douce, 2008). Therefore, they suggested the existence of a positive but marginal relationship between the various components of the CSR and FP.

Sawyer and Evans (2010) studied the key CSR activities of small business owners of South Australian region with regard to the key stakeholders. It was found that the SMEs were supportive of their stakeholders, especially the local community. They viewed CSR as a source of competitive advantage, which in turn improves the image of the business, saves costs and generates profit in the long run. Similar findings are reported by Wilson (1980), who conducted in-depth interviews with 180 owners/managers of SMEs and found that the appearance of social concern is often related to profit motives, as socially responsible behaviour appears to be necessary for the long-term survival of the SMEs.

Liu and Fong (2010) studied the CSR orientation in Chinese SMEs. For this purpose, they studied the impact of their internal activities, which are related to environmental sustainability, job creation, training for their employees and quality assurance to their customers on FP of the firms. Results revealed that no significant positive relationship exists between such CSR-oriented internal activities and firm’s FP.

Hammann et al. (2009) studied the relationship between SMEs’ SR and the value creation of a firm in the context of German SMEs. It was found that socially responsible management practices towards employees, customers and, to a lesser extent, society have a positive impact on the firm and its performance. These practices in turn were assumed to result in perceived positive reactions of the respective stakeholders and subsequently to positively influence the firm’s FP, that is, cost reductions and increase in profits.

Cristina, Cristina, Lorea and Asuncion (2009) studied whether SR can be a source of business value generation in the SMEs. They concluded that SR can be a source of value for the business only when it is akin to certain conditions; that is, the firm must have a strong conviction towards responsible behaviour rather than a mere economic and legal perspective; second, such activities must be focused on the critical issues that heavily condition business competitiveness; and finally, the SR must be embedded in the firm’s business strategy.

Jamali, Zanhour and Keshishian (2008) studied the SMEs’ uniqueness and relational attributes towards social activities and responsibilities in the context of developing countries. Empirical findings suggest that SMEs are found to be voluntarily engaged in several activities that can be called as CSR. However, such activities are not carried on in the context of FP, whereas these are related to deeply ingrained values and principles that correspond to responsible business conduct.

Avram and Sven (2008) studied the responsible business behaviour of the Austrian SMEs from a strategic management point of view. They first provide a thorough review of literature on CSR, elaborating on how the SMEs could generate social capital. Further, they concluded that SMEs usually have to face a lot of problems while implementing business activities, especially those related to external environment as compared to larger firms because of difficulties in accessing financial and personal resources.

Murillo and Lozano (2006) found that most of the Spanish SMEs share a strong persuasion that there exists a strong positive association between CSR and FP of the firms. Similar results of positive relationship between CSR and FP in SMEs were reported by Besser and Miller (2000).

Lahdesmaki (2005), Matten and Moon (2008) and Aragon-Correa, Hurtado-Torres, Sharma and Garcia-Morales (2008) reported that in the case of SMEs, CSR is derived from informal positive relationships that engender trust and reciprocity in network interactions between SMEs and their employees and local communities, which pay them in the long run in the form of enhancement in the scale of their business.

Longo, Mura and Bonoli (2005) studied Italian SMEs to identify their principal managerial instruments used for the creation of social value. The majority of SMEs perceived the SR concept and welcomed it not only because they have moral or ethical reasons for doing so but also because they believed that this contributes to the growth of the company’s own value, by means of an improvement in company image, ensuring the fidelity of customers and an improvement in relationships with employees and with the local community.

It is evident from the above literature review that the majority of CSR studies in SMEs are contextual in their nature and broadly focus on the developed economies (Raman, 2006). There is a relative paucity of information in the literature with regard to such studies in SMEs of developing economies (Arora & Puranik, 2004; Balasubramanian, Kimber & Siemensma, 2005; Baskin, 2006; Narwal & Sharma, 2008). Through this exploratory research, we seek to partially fill this lacuna by defining the CSR through stakeholder’s lens and its impact on FP of SMEs.

Theoretical Framework and Research Objective

Small and medium enterprises play an indispensable role in triggering economic growth and equitable development, particularly in developing countries. Their business activity is generally performed closer to the stakeholders, allowing them to be the first-hand recipients of expressed needs (UNIDO 1 Survey Report, 2008). Therefore, by sheer proximity, SMEs are continuously confronted to participate actively in the development of their environment and act ethically. Indian SMEs represent the socio-economic model of government, and their contribution to the economic growth of a nation is well recognized. They are the indispensable part of the economy as they constitute 6 per cent of GDP (Government of India, 2013), 34 per cent of national exports, 80 per cent of employment and nearly contributing 40 per cent to the entire output of the country. Currently, there are over 11 million SME units in India that produce more than 8,000 products. They are creators of entrepreneurial spirit and are crucial for fostering competitiveness and employment.

In brief, SMEs are important for a healthy and dynamic market economy (Hillary, 2000). Thus, a focus on large firms far from represents the entire story (Spence et al., 2001), and to ignore this sector when studying CSR is to ignore an important slice of business activity (Quinn, 1997). Therefore, the need of the hour is to focus on the CSR orientation of SMEs and its financial implications. As this can be very rewarding for a country because when a CSR-oriented SME grows into a large enterprise, and with its continuing stance, local social issues may become increasingly influential.

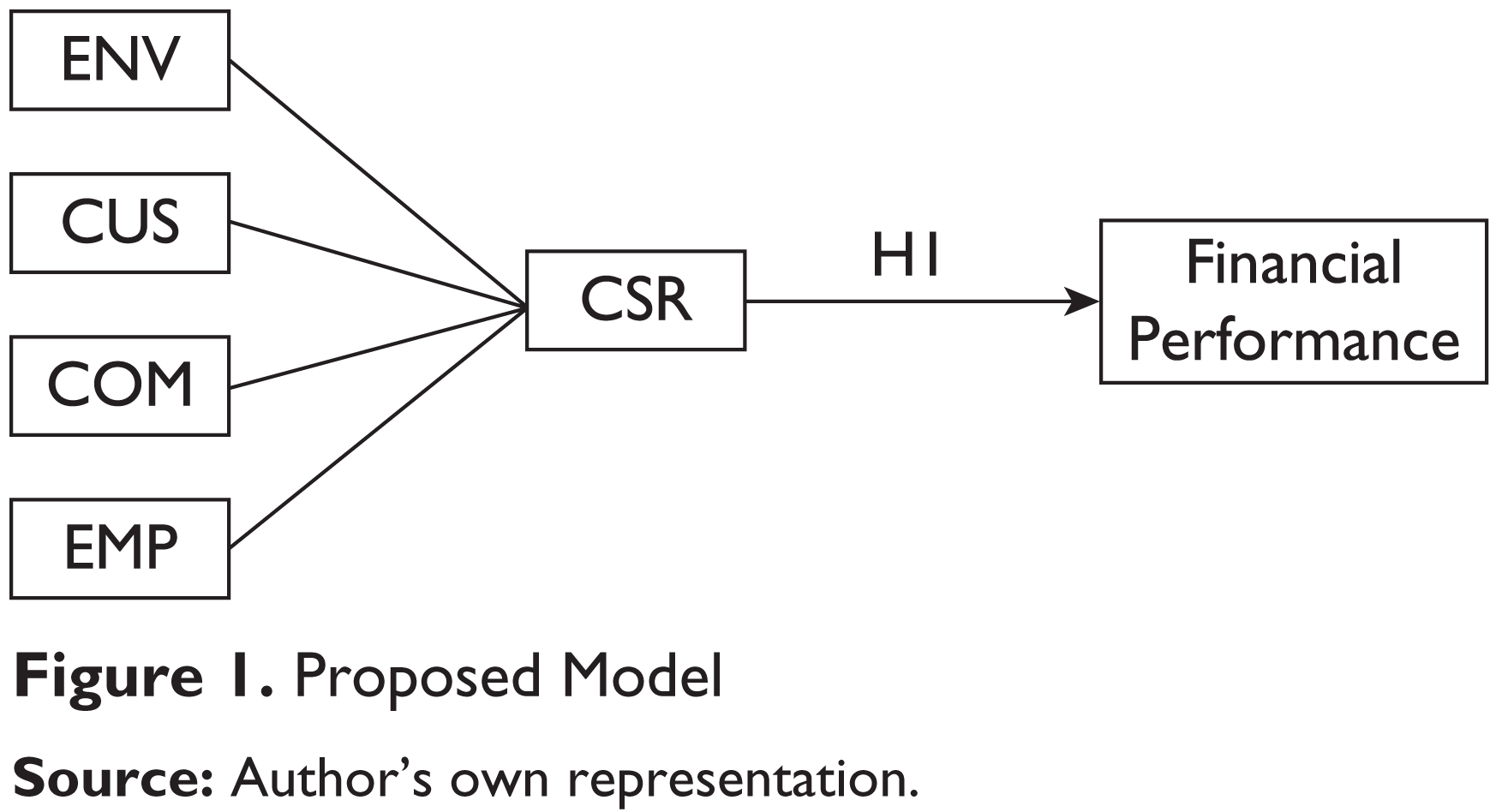

Although the previous studies in this context give us a framework to proceed in the direction to assess and explore the nature of the relationship between CSR activities of SMEs through multi-stakeholder’s framework and its impact on their FP, the mixed or confounded results in this area motivated the authors to pursue with more fine-grained approach and radical research methodology. Hence, in this context, authors have proposed the hypothetical model (Figure 1) and have employed structural equation modelling (SEM) to explore the extent of CSR activities of SMEs in the state of Rajasthan (India) towards their different stakeholders and their impact on their FP. The study proposes the following hypothesis that there is a significant relationship between CSR and FP of SMEs.

Sample and Data Collection

A total of 384 SMEs belonging to different sectors like ceramics (18.8 per cent), carpet (18.0 per cent), wool (14.1 per cent), gems and jewellery (16.1 per cent), machine tools (10.2 per cent), textile and other manufacturing industries (11 per cent) distributed all over the Rajasthan state were approached to take part in the study. A structured questionnaire was used for the survey, and data were collected either through electronic mail or through the telephonic interview that were conducted with the owner– managers of the companies. The questionnaires were complete in all respect and hence included for the purpose of the analysis. On the basis of general demographical characteristics, all firms were classified for further study, and the details of these classifications have been mentioned in Table 1, capturing the different demographic dimensions of the SMEs. Table 1 showed that there were 343 (89.3 per cent) males and 41(10.7 per cent) females. In addition, 73 (19.0 per cent) of the respondents were of age group under 30 years, 156 (40.6 per cent) were of age between 30 and 45 years, 109 (28.4 per cent) were of age between 45 and 55 years, while 46 (11.9 per cent) were of age above 55 years. The demographic result also shows that most of the entrepreneurs/owners are graduates (29.2 per cent) and postgraduates (27.3 per cent). Table 1 also showed that 121 (31.5 per cent) of the respondents indicated 15–20 years of business establishment, while 97 (25.3 per cent) indicated 10–15 years of establishment, respectively. Table 1 showed most of the respondents were running family-owned business, 153 (39.8 per cent). The majority of the firms in the sample were having annual sales between ₹25 lakhs and ₹50 lakhs (30.5 per cent). The percentage distributions of number of employees in various firms were as follows: 117 (30.4 per cent) were having less than or equal to 50 employees, 137 (35.7 per cent) were having employees between 51 and 100, and 130 (33.9 per cent) firms were having more than 101 employees.

Demographic Characteristics of the Sample

Research Design and Methodology

To explore the relationship between CSR and FP in SMEs’ context, authors adopted a more fine-grained approach and progressive research methodology that is quite novel in this area. Moreover, according to Berman and Wicks (1999) and Preston and Sapienza (1990), studies on the relationship between stakeholder’s management and FP are the deserted area of research in literature. To fulfil these lacunae, this research viewed CSR through the lens of multi-stakeholder’s framework (McKee & Boaytzis, 2005; Smith, 2003). In order to achieve the objective, CSR activities of SMEs are classified under four stakeholder’s headings, that is, customers, community, employees and environment, which is in congruence with the literature and interview findings of Agle and Mitchell (2008), Sweeney (2007) and Vaaland et al. (2008). The scales used for this study are adapted from previous research works in this domain (Bhattacharya & Sen, 2004; Gildea, 2001; Hopkins, 2003; Judge & Douglas, 1998; Stanwick & Stanwick, 1998). After this, each item (total 22) has been measured using a Likert scale of five points, ranging from ‘Not at all’ to ‘A great extent’. This is the proposed number of points according to Netemeyer, Boles and McMurriam (1996) and includes a mid-point, which is required, as with some items, a neutral response is a valid answer. Table 2 shows the scale used for the purpose of the present study.

Research Tool

As recommended by Anderson and Gerbing (1988), a two-step SEM procedure is employed in this study for estimating parameters: a measurement model followed by a structural model. The measurement model is a confirmatory factor analysis (CFA). The purpose of the measurement model is to specify the relationships between observed variables and latent variables. In the study, second-order CFA has been used so as to provide a more parsimonious account for the correlations among the lower order factors. Moreover, to explore the kind of relationships between multiple dependent and independent variables (Smith, 2004), a multivariate technique (i.e., SEM) has been employed.

Scale Items

Results of Data Analysis

Measurement Model

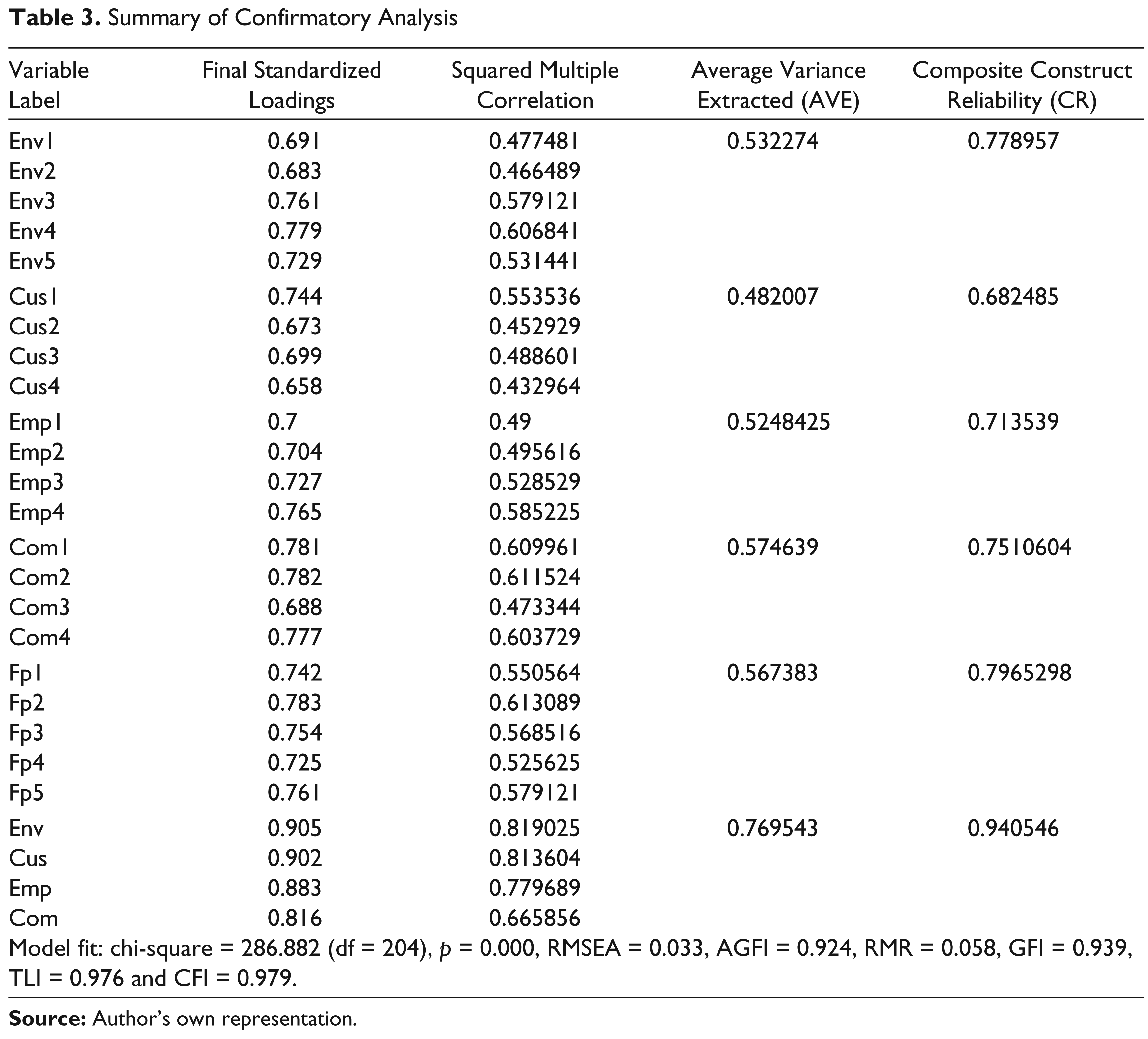

IBM AMOS 19 software was used to perform CFA. The analysis focused on one second-order latent variable, that is, CSR; five first-order latent variables, namely, environment (Env), customers (Cus), employees (Emp), community (Com) and financial performance (FP); and 22 observed variables. Confirmatory factor analysis (CFA) provides an assessment of the reliability and validity of the observed variables for each latent (first- and second-order) variable (Jöreskog & Sörbom, 1989). Under the assumptions of multivariate normality, maximum likelihood estimation (MLE) is considered most appropriate with large samples (Jöreskog & Sörbom, 1982). As the data satisfied the assumptions of univariate and multivariate normality, MLE was used. The constructs under consideration (CSR and FP) are jointly analyzed in a measurement model.

In the measurement model, degree of variance (of construct) is measured by squared factor loadings. Observed variables are considered to have higher explanatory power when the squared factor loading for each one is more than 0.50, moderate if between 0.30 and 0.50 and poor if below 0.30 (Holmes, 2001).

The model fit was assessed using chi-square value to degree of freedom ratio (CMIN/df), goodness-of-fit index (GFI; Jöreskog & Sörbom, 1989), the comparative fit index (CFI; Bentler, 1990), root-mean-square error of approximation (RMSEA; Browne & Cudeck, 1993), Tucker–Lewis index (TLI; Bollen, 1989), adjusted goodness-of-fit index (AGFI) and root-mean-square residual (RMR). The threshold for CMIN/df should be less than 3.0 (Hu & Bentler, 1999) or less than 2.0 in a more restrictive sense (Byrne, 1989). However, CMIN is affected by the sample size and normality of the data (Schumacker & Lomax, 2004; Tabachnick & Fidell, 2001). Therefore, the CMIN test should be used in combination with other indices. Values of GFI, AGFI, TLI and CFI should be over 0.90. Moreover, RMSEA should be lower than 0.05 to indicate a close fit of the model in relation to the DF. These fit statistics are evaluated to determine whether or not the predetermined model best explain the relationships between the observed and latent variables.

The proposed measurement model showed that all regression weights are significant (p < 0.001). The absolute fit statistics showed a chi-square of 286.882 with 204 (df) is significant (p = 0.000) [CMIN/ df = 1.406] with RMSEA = 0.033, RMR = 0.058, CFI = 0.979 and TLI = 0.976. This suggested that the model is acceptable; moreover, other fit indices, namely, GFI = 0.939 and AGFI = 0.924, are also supportive. The results suggested that the model fitted adequately to the data.

All items factor loadings are statistically significant and are greater than 0.60, which confirmed the convergent validity of the model. Moreover, covariance among the factors (FP and CSR) is significant (p < 0.001). Given that the model fitted the data adequately, respecification is not required. However, composite reliability (CR) and average variance extracted (AVE) are calculated to test the convergent validity. AVE should be either greater than or equal to 0.50 and CR should be greater than or equal to 0.60 (Bagozzi & Yi, 1988). Although CR is high, AVE is marginally lower in one of the constructs. The CR and AVE calculated for the second-order construct is satisfying the minimum cut-off set in theory. Hence, it could be concluded that the measures used within this research are within the acceptable levels, supporting the reliability of the constructs. Additionally, constructs’ factor loadings are statistically significant. Hence, convergent validity of the constructs is established. After evaluating the reliability, unidimensionality, constructs validity and convergent validity of the measurement model, the next stage is to perform the analysis of the structural model. Table 3 displays the summary results of CFA.

Summary of Confirmatory Analysis

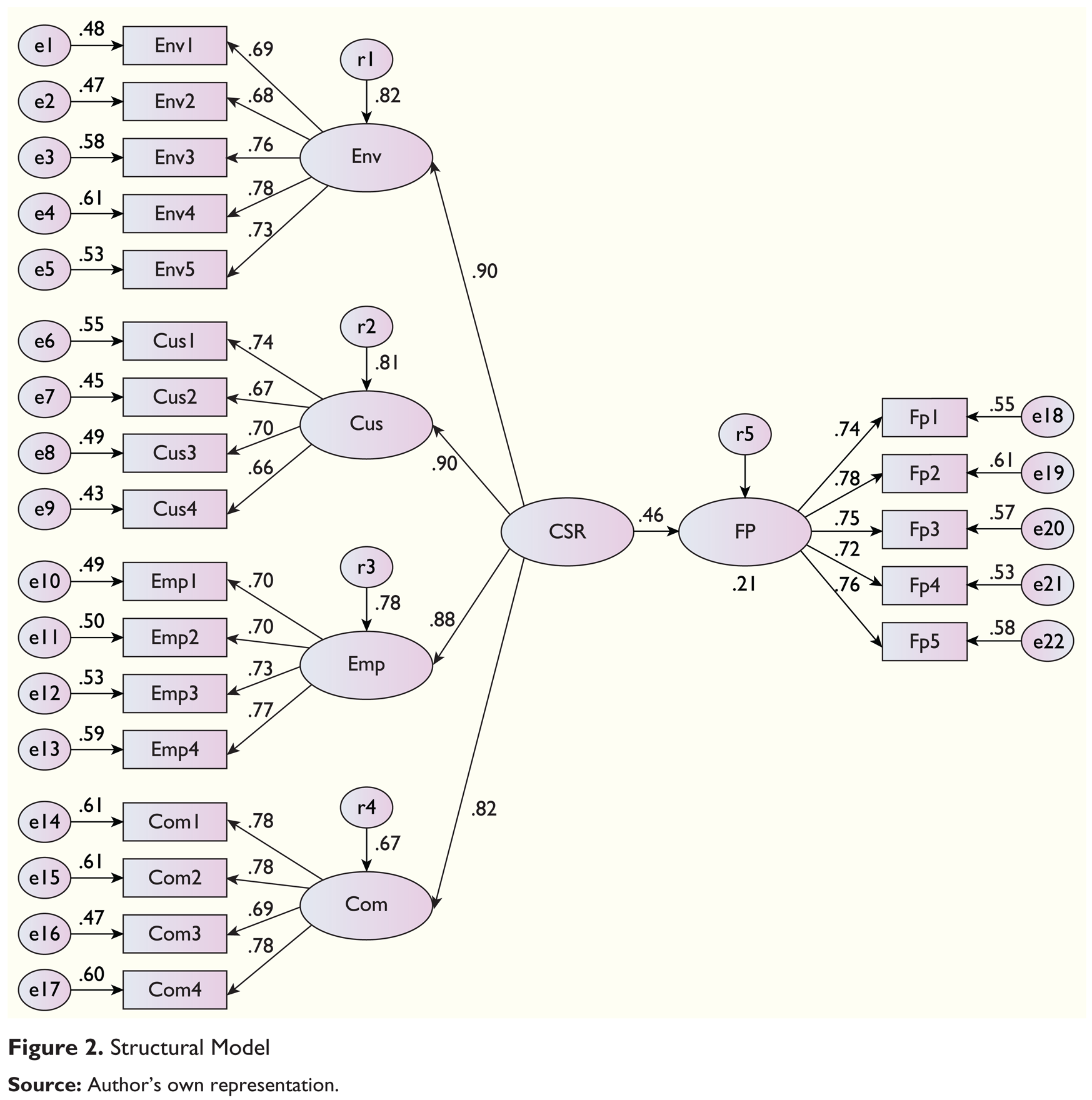

Structural Model

Structural equation modelling, a multivariate technique, is employed in this research to study the relationship between CSR and FP. Goodness-of-fit indices are analyzed to evaluate the fitness of hypothesized structural model. As the assumptions underlying SEM are met, overall model fit indices along with the various coefficient parameters are estimated to test the relationship between the two latent constructs (CSR and FP). The indices for goodness-of-fit demonstrate that this model fits the data adequately (chi-square = 286.882, df = 204 and p = 0.000), and the values of GFI = 0.939, AGFI = 0.924, RMSEA = 0.033, CFI = 0.979, TLI = 0.976, RMR = 0.058 and CMIN/df = 1.406. The R2 for the model came to 0.21 (Table 4). The structural model is depicted in Figure 2.

Structural Equation Results: Direct Relationship

The result of the study indicates a significant but a weak positive relationship between CSR and FP, which is similar with the findings of Orlitzky et al., (2003). The model explained 81 per cent of the variance in customers (Cus), 78 per cent of the variance in employees (Emp), 82 per cent of the variance in environment (Env) and 67 per cent of the variance in community (Com). This showed that CSR contributed positively towards different stakeholders. Moreover, the relationship is statistically significant (at 0.001 probability level) and in the hypothesized direction.

Findings

The research aimed to determine the extent of CSR activities of SMEs towards their different stakeholders and its impact on their FP. In this context, SMEs’ perception has been measured regarding the various CSR activities that are being undertaken by them to enrich their relationship with society and the environment. The owner/managers are asked whether their business is actively involved in the local community in any way, such as by donating goods or services to local organizations, supporting a local charity or sponsoring local events; whether they assess and manage the impact of their business on the environment; whether they provide clear and accurate information and value to their customers; what steps they take to resolve the grievances and how they conserve energy and minimize waste; and whether they find any tangible change in their sales revenue or in profit margins as a result of being responsible in their deeds towards the stakeholders.

In reply to the above statements, most of the SMEs stated that although they are socially responsible towards their different stakeholders, CSR is not a part of their strategy; rather, it is more an informal and self-driven approach. For them, CSR is not meant for economic imperatives; rather, they associate it with religious spirit. Due to constraints that they face in terms of resource and personal that can be deployed for CSR activities, the notion of CSR among them remains philanthropic and non-institutionalized. The following paragraphs explain the reported CSR activities of SMEs towards their stakeholders.

Environment

The SME owners/managers are asked up to what extent does their organizations implement specific CSR strategies that focus on maintaining the environmental integrity, eco-efficiency, pollution reduction, energy conservation, recyclability and environmental protection that goes beyond regulatory compliance, with the aim of minimizing a firm’s ecological impact.

Results revealed that most of the SMEs are quite sensitive towards the environmental protection and resource conservation not only to meet the legal compliances as specified under The Environment Protection Act, 2 1986, but also to save the financial obligations. Common activities manifested are environmental-friendly packaging (loadings = 78 per cent), for that they are using biodegradable cardboard boxes, bales made up of hays in cloth material, high-density polyvinyl (HDP) cloth, jute packaging and reusable fibre coils (Jenkins, 2006; Longo et al., 2005; Sweeney, 2007); regarding recycling initiatives and waste management (loadings = 76 per cent), they have mentioned that even the solid waste generated are properly staked, and some of the dump are used for the maintenance of roads and remaining are backfilled in excavated areas. Along with this, most of them are having ISO certification (loadings = 73 per cent) that emphasize on environmental management and provide assurance to the external stakeholders that environmental impact is being measured and improved. To conserve energy and reduce costs (loadings = 68 per cent), they have employed some simple measures such as using energy-efficient compact fluorescent light bulbs. Many firms turned off their lights at night, or used only security lighting. Moreover, at the daytime, to reduce the power consumption and for proper lightning and ventilation, they have incorporated transparent sheets in their roofs. In this way, efficient use of lighting is a common initiative undertaken by the firms in conserving energy. Most of the manufacturing firms (ceramics factories) not only have filtered chimneys to reduce the air pollution (loadings = 69 per cent) but also have incorporated the respirable dust samplers (common in woollen and carpet factories) inside their factories to maintain a safe and healthy working environment. These respirable dust samplers are widely used for air quality monitoring. It effectively detects the presence of inorganic gases in the environment. Even some of the medium-sized firms reported that they have high-volume air sampler, used to monitor the air to determine the extent of pollution and to identify the source of emission at regular interval of time. To reduce water pollution, many textile firms have installed chemical oxygen demand (COD) digesters and biological oxygen demand (BOD) incubators system to detect the effluent quality.

Customers

When the SME owners/managers are asked about their specific CSR deeds towards the customers, most of them reported that providing clear and accurate information to customers about products contents, labelling and after-sales obligations (loadings = 74 per cent) are their prime activities. As the market of their product is purchasers or buyers driven and being the integrated part of supply chain of large firms, it is essential for them to value their customers (loadings = 70 per cent) by ensuring honesty and impartiality in all of their contracts, dealings and advertising (e.g., a fair purchasing policy, provisions for consumer protection). To assure the customers about the quality criteria (loadings = 67 per cent), they send samples to them with the utmost promise of maintaining the same standards in their future transactions. To keep their customers happy and loyal and to develop a long-term relationship and a good rapport with them, SMEs are also giving an ear to resolve their complaints in a timely manner (loadings = 66 per cent).

Employees

Most of the SMEs agreed that employees are the lifeline of their organizations and they are indispensable for their success and growth. Further, they shared that in the market, there is a scarcity of competent labours and employees. Therefore, the biggest challenge in front of them is to retain them. Due to this reason, employees are in a central position within the firms, and firms are implementing specific CSR strategies in terms of opportunities to improve and multiply their skills and health and safety programmes. They are actively involved in the activities for employee benefits (loadings = 77 per cent) like encouraging employees to enhance and develop skills and long-term career paths (loadings = 73 per cent). For this purpose, they send their employees to the training centres. For example, most of the owners of the carpet manufacturing firms are sending their employees to the Carpet City ‘Bhadohi’ to enhance and make them learn the new techniques of handmade carpet weaving; likewise, in gems and jewellery industry, they organize not only certified programmes in collaboration with the national-level institutes for their workers to make them proficient with technical skills but also training camps, workshops and meditation camps in collaboration with social workers and NGOs to maintain the work–life balance of their employees (loadings = 70 per cent). They are also committed towards their health and safety (loadings = 70 per cent), as they provide them hygienic food and pure drinking water at subsidized rates in their canteens that are collectively run by the group of SMEs in that particular area. If in case accident occurs on the site, then they not only take labours to the hospital but also bear the whole expenditure, and in some cases, they are also paying them in advance to meet any contingent situations of their family. Apart from these activities, some SMEs mentioned that they also provide accommodation to those labours who belong to other places and also get admitted their wards in the nearby school for the purpose of elementary education. Moreover, on occasions such as Diwali, they give bonuses to their employees. Some SMEs also mentioned that they are also having a provision of provident funds for those employees who have been associated with them for a long period.

Community

It is often stated that community-oriented CSR activities of SMEs are shaped through their embeddedness in social ties and local interdependences (Murillo & Lozano, 2006). This belief found almost true as most of the SMEs revealed that they are actively involved in such activities that are in the proximity to the community. For this purpose, companies frame their recruitment and purchasing policies in such a manner that favours the local communities (loadings = 78 per cent). They further mentioned that such policies not only help them to create a good rapport in the society but also help them in developing a congenial and cohesive relationship with the local people. Apart from this, they are also actively involved in sponsoring the local events (loadings = 78 per cent), and donating some percentage of profits to charity (loadings = 77 per cent), such as at the time of social and religious ceremonies (e.g., Ramdevra Mela, Punrasarji Mela), they offer tea, water, snacks, medicines and other food material free of cost to the pilgrimages. They often correlate such social activities to religious spirit because they believe if they will do well to the society, then God will do good to them. Moreover, their employees also volunteer (loadings = 69 per cent) in the social events along with the social workers and local NGOs such as volunteering in blood donation camps, free health check-up camps and other social awareness activities. They also mentioned that, sometimes, due to political and social pressures, they have to get involved in local events through sponsorships and charity to please the affluent people of the society with this anticipation that in near future they would help them out in fulfilling their future aspirations.

Financial Performance

Although the SME entrepreneurs are satisfied with the FP of the firm in terms of change in profit margin (loadings = 75 per cent) and change in sales revenue (loadings = 73 per cent), they do not perceive them as a direct result of their CSR activities. Conversely, they correlate profit margin (loadings = 78 per cent) and sales revenue (loadings = 76 per cent) changes with their strong commitment towards the quality of their products, availability of raw materials, skills of their employees and prevailing market conditions. They believed that although CSR is a viable investment, its financial implications are experienced in the long term (loadings = 74 per cent). The reason is that CSR is neither a strategic commitment for most of them nor a legal obligation, whereas it is the moral persuasion of the owners that is reflected in their willingness and financial capability.

Conclusion and Implications

Deeper analysis of the small and medium firms operating in Rajasthan in relation to their CSR activities towards their stakeholders and its financial implication indicates a weak positive relationship. Results suggested that CSR in SMEs is still philanthropic and non-instrumental in nature. Although they have shown an inclination towards such activities, their FP is not as such enhanced through it. Other insights gained as a result of this study are explained subsequently.

The results support the notion that employees, customers and environment are the most vital stakeholders for SMEs. This is consistent with the existing literature. In particular, respondents agreed that the value orientation towards employees is very important as they are the purveyors of their viability (Clarkson, 1995). That is why in most of the cases, they are seen at the central position and being considered as an important firm resource (Pfeffer & Salancik, 1978). Moreover, the firms are focusing more on activities benefiting the employees and have employed a caring attitude towards them. It is also evident from this study that the management of the relationship with a firm’s another key stakeholder, particularly customers, is again very crucial for them as satisfied customers will ultimately lead to a better economic performance of the firm, and the SMEs of the state are well aware of the same. Therefore, to attain a symbiotic relationship with the customers, most of the SMEs show their full commitment and responsible behaviour in all their consignments and transactions. Being the responsible citizens, most of them are also maintaining the ecological balance through the wise allocation and optimum utilization of the natural resources. Moreover, involvement of the firm in the form of employment generation and purchasing policy favouring local enterprises, and undertaking community projects, give them a unique identity. This in turn augments firm’s image, goodwill or reputation, which are non-economic benefits that the firms are reaping as a consequence of being socially responsible. This long-term association in the term of intangible benefits would be materialized and help the firm in improving their FP in the long run.

Thus, despite the forces of globalization and resulting increase in competition and the pressure to be profitable, SMEs still view CSR primarily from a caring or value-driven mentality. In particular, owner’s attitude, willingness and social pressures are the main driving forces in shaping the status of SMEs in terms of their actual behaviour with regard to their CSR involvement. Therefore, the need of the hour is the adoption of more focused and strategic approach of CSR by SMEs in order to be economically sustainable, that is, more efficient and profitable in the long run. To accomplish this vision, the requirement is to maximize the stakeholder value by focusing on the ‘triple bottom line’ approach.

Limitations

The study is mainly based on the personal disposition of the SMEs situated in a particular geographical area (i.e., Rajasthan) towards CSR as expressed in the survey. Hence, bias may occur both as a result of the particular image key informants wish to portray and due to inevitable idiosyncrasies in individual perceptions of the concepts. Although some SMEs expressed difficulty in understanding the concept of CSR, all could define what it meant specifically in the context of their company. Corporate social responsibility was seen as an ‘all embracing’ idea that concerns having an awareness of the impacts of the business, and wanting to have a positive impact on a wide range of stakeholders through the business decisions that are made.

Footnotes

Acknowledgements

The authors are indebted to the anonymous referees of the journal for their useful recommendations in improvising the quality of the article.