Abstract

The objective of this article is to analyze if demographic characteristics influence user attitude towards mobile banking. The sample comprise of current users of online banking. Although earlier studies on technology adoption models have received considerable empirical validation, most of the studies did not consider moderating variables. Among those, which consider moderating variables, primarily explored are gender, age and income. By including other moderator variables in the model, we hope to lessen the inconsistencies found in past research studies. To test the moderating effect, two methods, viz. multiple linear regression and Fisher Z transformation are used. Results show that gender, age, qualification, experience, occupation, income and marital status were significant moderating variables. However, educational background did not show any moderating effect. Our results suggest that by extending the Technology Acceptance Model (TAM) and Diffusion of Innovations (DoI) theory, the research provide insights into the factors influencing consumers’ attitude to adopt mobile banking applications. Besides, the results of moderating effect improve our understanding of the demographic differences, which influence the degree of mobile banking adoption. This study will help researchers and practitioners to come up with improved mobile adoption frameworks and applications with greater understanding of the influence of demographic factors.

Introduction

A number of studies exist which have used Technology Acceptance Model (TAM) to explain user behaviour and intention to adoption technology innovation. The major components of TAM model are perceived ease of use, perceived usefulness, attitude and intention. Further, many research studies have been conducted to examine the moderating effect of demographic variables on the user attitude to adopt technology. Despite the fact that most Americans use the Internet, those who are older, less educated, minority and lower income have lower usage rates than younger, highly educated, white and wealthier individuals (Porter & Donthu, 2006).

The unified theory of acceptance and use of technology (UTAUT) as suggested by Venkatesh, Morris, G.B. Davis and F.D. Davis (2003) aims to explain user intentions to use an information system and subsequent usage behaviour. This model is based on a review and consolidation of eight models, which were used by previous researchers to explain information system usage behaviour. The model also includes the constructs of the TAM and Diffusion of Innovations (DoI) theory. Subsequently, the researchers have explained the relationship between the antecedents and intention using four moderating variables (gender, age, experience and voluntariness of use). Although the model explains a significant amount of variance in behavioural intention and actual usage, there seem other demographic variables which have not been considered in the model.

In the article, we have used the constructs as discussed by two models, that is, innovation diffusion theory and the TAM. While TAM looks at perceived ease of use and perceived usefulness as factors influencing attitude, the innovation diffusion theory uses perceived relative advantage, ease of use, compatibility, observability and trialability to explain attitude and intention. Both perceived usefulness and perceived relative advantage focus on the advantages that mobile banking offers, such as time and place independence, effort saving qualities (Mallat, Rossi & Tuunainen, 2004), ubiquity, flexibility and mobility (Sulaiman, Jaafar & Mohezar, 2007) as compared to other banking channels. Perceived usefulness is the belief that using a particular technology would increase the performance. Given that every individual has fixed number of hours in a day, from the mobile banking perspective, it is important that this offers enhanced the productivity with low effort and convenience. Extending the above logic, users are willing to use mobile banking when they perceive it to be useful and helpful for the efficiency of their work (Gu, Lee & Suh, 2009). Efficiency refer to the perceived benefits customers receive in relation to the sacrifice or costs and is perceived cognitively as the ratio of benefits and sacrifice (Laukkanen, 2007). Further, other than efficiency, convenience has also been discussed as an important factor which influences technology adoption. From the perspective of self-determination theory, convenience is that users believe that a technology or a system is helpful in their task completion (Chang, Yan & Tseng, 2012). Other than time utilization in case of mobile banking, accessibility, handiness and portability seem to provide convenience (Laukkanen, 2007). Berry, Seiders and Grewal (2002) have proposed five dimensions of service convenience, namely, decision convenience, transaction convenience, benefit convenience, access convenience and post-benefit convenience. Kaura, Prasad and Sharma (2013) in a study involving Indian banks found that private sector banks offered higher convenience on all the five dimensions as compared to their public sector counterparts.

Alongside the constructs of the two models, also used are various demographic variables to examine their moderating effect between the antecedents of mobile banking and user attitude. While consumer adoption of online banking has been studied extensively, few studies exist which explore the factors that influence mobile banking adoption in the Indian context. Further, the moderating effect of demographic variables on attitude to adopt mobile banking is limited to gender, age and income. This research study attempts to examine the moderating effect of various demographic variables, such as gender, age, qualification, educational background, experience, occupation, income and marital status. By including other moderator variables in the model, we hope to lessen the inconsistencies found in past research studies. The next section discusses a review of literature around moderating effect of various demographic variables discussed in earlier studies. This is followed by research gaps and objectives of the study. The following section discusses the rationale of the study and the research model. Thereafter, methodology is discussed which is followed by analysis of data and findings of the study. The penultimate section presents conclusion and implications of the study followed by limitations and scope for future work.

Review of Literature

Extensions of models influencing technology adoption have been used by researchers to explain adoption of various forms of technologies.

The Moderating Effect of Gender

Extensions of models influencing technology adoption have been used by researchers to explain adoption of various forms of technologies. Zhang and Prybutok (2003) have examined the effect of gender as a moderating variable on online shopping purchase intention and the results showed that gender is an important moderating variable in online commerce. Males are more inclined to adopt bank technology (Wan, Luk & Chow, 2005), Internet banking (Akinci, Aksoy & Atilgan, 2004) and mobile banking (Amin, Hamid, Tanakinjal & Lada, 2006) than females. Nysveen, Pedersen and Thorbjørnsen (2005) found a stronger proportion of perceived usefulness of mobile chat services among men than women. Demirci and Ersoy (2008) found that with respect to gender, innovativeness was found to be significantly higher in males than females. Shin (2009) found that the moderating effects of gender with respect to technology usage are significant. Lee et al. (2010) empirically demonstrated that demographic factors indirectly influence individual differences in the use of retail self-service checkouts through consumer traits and that difference in consumer traits arise from demographic factors. Further, they found that women tend to exhibit a higher level of technology anxiety while men are more likely to be innovative towards technology. Furthermore, the moderating effects of social norms are stronger in female group while the influence of enjoyment is stronger in male group (Hwang, 2010).

Cheung and Lee (2011) found perceived usefulness to influence attitude and behavioural intention to use an Internet-based learning medium more strongly for male students than it influences female students, while subjective norm is a more important factor determining female students’ intention than it is for male students. Suki (2011) in Malaysian context conducted a study to investigate whether gender, age and education really moderate online music acceptance. It was found that younger people less than 25 years, male and higher educated, were more strongly affected by perceived playfulness and perceived ease of use towards online music. Onyia and Tagg (2011) in a sample of Nigerian customers found gender to significantly influence the attitude of retail banking customers. Liu, Zhao, Chau and Tang (2015) in the context of mobile coupon application in China found personal innovativeness in information technology usage has more positive impact on behavioural intention for males than females. Falahati and Paim (2015) found significant differences in financial attitude, financial socialization and secondary socialization agents between male and female students in Malaysia.

Nysveen et al. (2005) found that no differences in moderating effect across gender were found between ease of use and attitudes. In Lee et al.’s (2010) study, it was found that the direct impact of gender on intention is statistically insignificant. Hernández, Jiménez and José Martín (2011) in a sample from Spain found that the factors related to the Internet (acceptance, frequency and satisfaction) are stable for men and women in case of experienced online shoppers. The moderating effect of gender is insignificant in case of experienced users. Jambulingam (2013) among Malaysian students found that the age and gender do not moderate the relationship between the determinants of mobile technology adoption and behavioural intention.

In the Indian scenario, the involvement of male and female gender in financial matters is different. While girls may not be so much involved with financial practices, their counterparts are encouraged to take financial decisions. This practice is more prevalent in rural India and small towns where men are considered responsible for earning money and women to look after the family. Since mobile banking is associated with financial transactions, the differences in degree of technology adoption in male and female attitude may be due to disparity in financial decision making. Wang, Sun, Cobb, Lawson and Sharples (2016) found that gender moderates the relationship between perceived ease of use, perceived enjoyment and intention to use. Further, gender is not found to have significant moderation effects on the relationship among perceived usefulness, perceived compatibility and intention to use.

Despite these gender differences, according to a recent report published by the Internet and Mobile Association of India (IAMAI) and IMRB International, overall 71 per cent male and 29 per cent female are Internet users in India. In urban India, the ratio between male to female is 62:38 while it is 88:12 in rural India. However, the important point is that the Internet usage among males has been growing at a rate of 50 per cent while it is growing at 46 per cent for female users which is comparable. It is expected that, in times to come, the technology gap between male and female will significantly reduce. This is more apparent in developed countries where men and women have similar access to technology.

The Moderating Effect of Age

Similarly, studies on technology adoption demonstrate that younger users behave differently as compared to their counterparts. Older users tend to be relatively laid back in terms of using technology for conducting transactions as they are sceptical about the technology and rely more on face-to-face transactions. A study by Im, Bayus, & Mason (2003) found that age to be a strong predictor of new product ownership in the consumer electronics category. Age has been identified to have a moderating effect between technology use and perceptions (Yi, Wu & Tung, 2005).

Technology anxiety seems to influence the degree of adoption differently among varying age groups with older consumers having more technology anxieties (Demirci & Ersoy, 2008; Lee et al., 2010; Morris and Venkatesh, 2000; Porter & Donthu, 2006). Age strengthens perceived usefulness, perceived cost and perceived system quality and in turn moderates attitude towards intention to adopt mobile banking (Riquelme & Rios, 2010). Faqih and Jaradat (2015) found that demographic variables of age and gender have considerable moderating influence on the adoption of mobile technologies in healthcare systems in Jordan.

Older individuals due to their limited exposure to computers, mobile handsets and Internet have lower perceptions of self-efficacy in learning Internet (Porter & Donthu, 2006). Wang, Wu and Wang (2009) in the context of mobile learning in Taiwan found age to have a moderation effect of effort expectancy and social influence on intention. With respect to age, insecurity and discomfort were found to be higher in older respondent as compared to younger ones (Demirci & Ersoy, 2008). Older people tend to have greater technology anxiety, and are less technologically innovative compared to young consumers. That is, younger people are relatively early adopters of new ideas, services and products (Lee et al., 2010).

However, there are studies which argue that the age of the user does not have a significant impact on their online behaviour. Most of the technologies today, computers Internet, mobile and so on irrespective of the age and social class are available and affordable to a larger population. According to Hernandez et al. (2011), in its initial stages of technology introduction, there was a clear bias in the profile of users but with passage of time the differences in terms of demographic profile are diminishing. Lee et al. (2010) in the context of retail self-checkouts found that age does not directly influence user’s intention. Chong (2013) in a sample involving Chinese respondents found that age has a significant relationship with m-commerce usage activities. Martins, Oliveira and Popovic (2014) in a sample of users from Portugal found that age explains behavioural intention of Internet banking adoption and that older respondents have more intention to use Internet banking.

In a more recent study by Wang and Sun (2016) involving elderly respondents found that older people are reluctant to adopt newer technologies. They found that age has a moderating effect on older people’s gameplay intention. The moderating effect of age on the association between motivational variables (perceived ease of use, usefulness, enjoyment and compatibility) and adoption of innovative three-dimensional (3D) printing in Chinese context was found to be true only in case of the variable ease of use (Wang et al., 2016).

The Moderating Effect of Qualification

Qualification is defined as the title, knowledge and skill gained through the process of formal education, which is recognized in the industry and makes someone eligible for a position or job. The decision to adopt a new technology is governed by the degree of knowledge or information one has on how to use it appropriately. India’s mobile phone subscriber base recently surpassed the one billion mark and a large chunk of this group comprises of students and young users in the age group of 20–35 years. Mobility has offered India’s young population a window to the world of opportunities which includes access to information and knowledge, education, employment and commerce.

Rogers (1983) believes that earlier adopters have more years of formal education than do it later adopters. Consumers who are early adopters of technology can be characterized by educational attainment (Im et al., 2003). Liebermann and Stashevsky (2002) found that users with low education level will perceive high barriers to Internet and e-commerce usage as compared to users with high education level. A higher educational level may give rise to a greater level of knowledge in new technologies, thereby accelerating the early adoption of a new technology. This is evident from a study by Rhee and Kim (2004) who found that people educated to a higher level were found to be more likely to use the Internet.

According to Porter and Donthu (2006), early adopters of new technologies tend to have higher educational levels while less-educated individuals feel more technology anxiety which impedes their ability to learn newer technologies. Weijters et al. (2007) suggest that people exposed to higher levels of education are likely to have had more exposure to technology, not only at their workplace but also in the course of their day-to-day activities. Onyia and Tagg (2011) empirically found that level of education significantly influences Nigerian banking customer’s attitude towards Internet banking. Chong (2013) showed that educational level has a significant relationship with m-commerce usage activities.

The Moderating Effect of Educational Background

Educational background refers to the area of prior education and the nature of degrees obtained. Background as a classification is important as some education streams are more technical in nature as compared to others. For example, in India, primarily two areas of education streams are popular; Engineering which is the application of mathematics and science knowledge to innovative, design, build and apply tools, systems, processes and organizations; and Arts and Humanities which consists of philosophy, history, literature, psychology, political science, etc.

Studies on the relationship between educational background and attitude and intention towards technology adoption are limited.

The Moderating Effect of Experience

Earlier research studies have cited experience as the amount of time the individual has been using a particular technology, such as Internet banking, online commerce, mobile banking, and so on. The concept of experience in previous studies refers to the same implied meaning: more familiar with and more knowledgeable about the technology of interest (Sun & Zhang, 2006). In our study, the experience is defined as the cumulative experience that the person gains while working on a specific job, role, position or project.

Experience in previous studies refers to the degree of familiarity and knowledge about the technology of interest (Sun & Zhang, 2006). Taylor and Todd (1995) confirmed that technology usage is more significant for experienced users than for inexperienced users. Prior studies confirmed that the effects of perceived ease of use, perceived usefulness and subjective norm on attitude and intention differ between experienced and inexperienced users (Venkatesh & Davis, 2000; Venkatesh et al., 2003).

The Moderating Effect of Occupation

Occupation is defined as the activity that serves as an individual source of livelihood. In our study, the sample comprises of both students as well as working professionals. Hence, we define occupation as the activity the mobile banking user is currently involved with, that is, either he is studying or working somewhere.

Compared with other potential demographic moderating factors, occupation received less attention in prior studies. In one such study involving Nigerian retail banking customers, employment status was cited as a major determinant of attitude towards Internet banking (Onyia & Tagg, 2011).

The Moderating Effect of Income

Income is defined as the money earned by individuals or businesses in exchange for providing products or services. Income levels influence user attitude and behaviour. Past research studies have examined how income may encourage or discourage user from technology adoption. Porter and Donthu’s (2006) study shows that lower income consumers are the consumers who are most concerned about cost and their perception is that the cost is high relative (device, access fee) to perceived usefulness. On the contrary, high income consumers are able to afford high quality of latest technology and Internet connection. This differential access to technology results in varying levels of anxieties among users, with low income users having high anxieties. Thus, income level influences the timing and the extent of technology adoption.

According to Hernandez et al. (2011), high income causes users to perceive lower risks while making online purchases, whereas low income discourages online transactions. It is logical to believe that with rising incomes, perceptions related to ease of use, efficiency, convenience and trust with technology adoption moderates user behaviour and intention. This is evident from the findings of a study by Lee et al. (2010) who found that technology anxiety decreases as income level increases. Users in the high-income group are usually active users of communication technologies and thus their level of comfort with using technologies is high. However, with falling prices of computer hardware and Internet, a large number of users from lower income group have also started using online services.

The Moderating Effect of Marital Status

Marital status is defined as the status on an individual where he is living as a single, married, divorced or widowed. For our study, the marital status is defined as either the person being single or married. Previous research studies have shown that married consumers prefer electronic banking transactions (Katz & Aspden, 1997; Stavins, 2001). However, another study by Gan, Clemes, Limsombunchai and Weng (2006) revealed that marital status has no impact on the adoption of electronic banking. Munnukka (2007) found significant association between marital status and levels of adoption of mobile communication services. Consumers in stable relationship tend to make less use of mobile communications as compared to those in less stable relationship or none.

Moderators Other than Demographic Variables

Im et al. (2008) in a sample comprising of US students examined perceived risk, technology type, user experience and gender as moderating variables. In addition to demographic variables, other variables like perceived image and perceived self-efficacy have been studied as variables which moderate the effect of factors of technology adoption on attitude. Perceived image is defined as the degree to which the technology enhances user’s image or social status and is found to have a positive effect on attitude (Mohammadi, 2015). Self-efficacy is defined as the degree of familiarity or comfort with using technology and it influences attitude towards mobile banking (Mohammadi, 2015).

Research Gaps and Objectives of the study

As evident from the review of literature, the antecedents of attitude towards mobile banking adoption are perceived ease of use, perceived convenience, perceived efficiency, perceived risk and privacy (trust) and perceived lifestyle compatibility. They influence the adoption positively. However, there are demographic variables, such as gender, age, educational qualification, educational background, occupation, income and marital status, which moderate the relationship between the above-mentioned antecedents and attitude. In this study, for a better understanding of perceived usefulness, two dimensions, namely, efficiency and convenience, have been used. The study improves the TAM by adding trust, convenience and efficiency as relevant factors. The article also integrates lifestyle to existing factors and focuses on both socio-technical aspects. There is no study conducted so far which have used all demographic variables to test their moderating effect between antecedents to mobile banking adoption and attitude towards mobile banking. Further, there is no study that employs more than one method to examine the moderation effect and draws a comparison of the results of the methods used.

While TAM, DoI and UTAUT have been used by numerous researchers, the primary purpose of the study is to extend the application of these models to determine the moderating effect of all demographic variables and to re-examine their effect between the antecedents and user attitude and behaviour towards mobile banking adoption.

In particular, the objectives of the study are to examine the impact of various antecedents to mobile banking on attitude towards mobile banking and to test the moderating effect of various demographic variables, namely, gender, age, qualification, educational background, experience, occupation, income and marital status, between antecedents to mobile banking and attitude towards mobile banking adoption.

Rationale of the Study and Research Model

Considerable amount of literature exists on factors which determine user acceptance of technological adoption including demographic variables. In order to identify cross-demographic differences between the antecedents to mobile adoption and attitude, we propose a model combining the TAM model and UTAUT model as a reference for explaining user attitude for mobile banking adoption. Our model contains a variety of antecedents taken from both the models along with demographic variables as moderator variables to explain the impact on user attitude towards technology adoption.

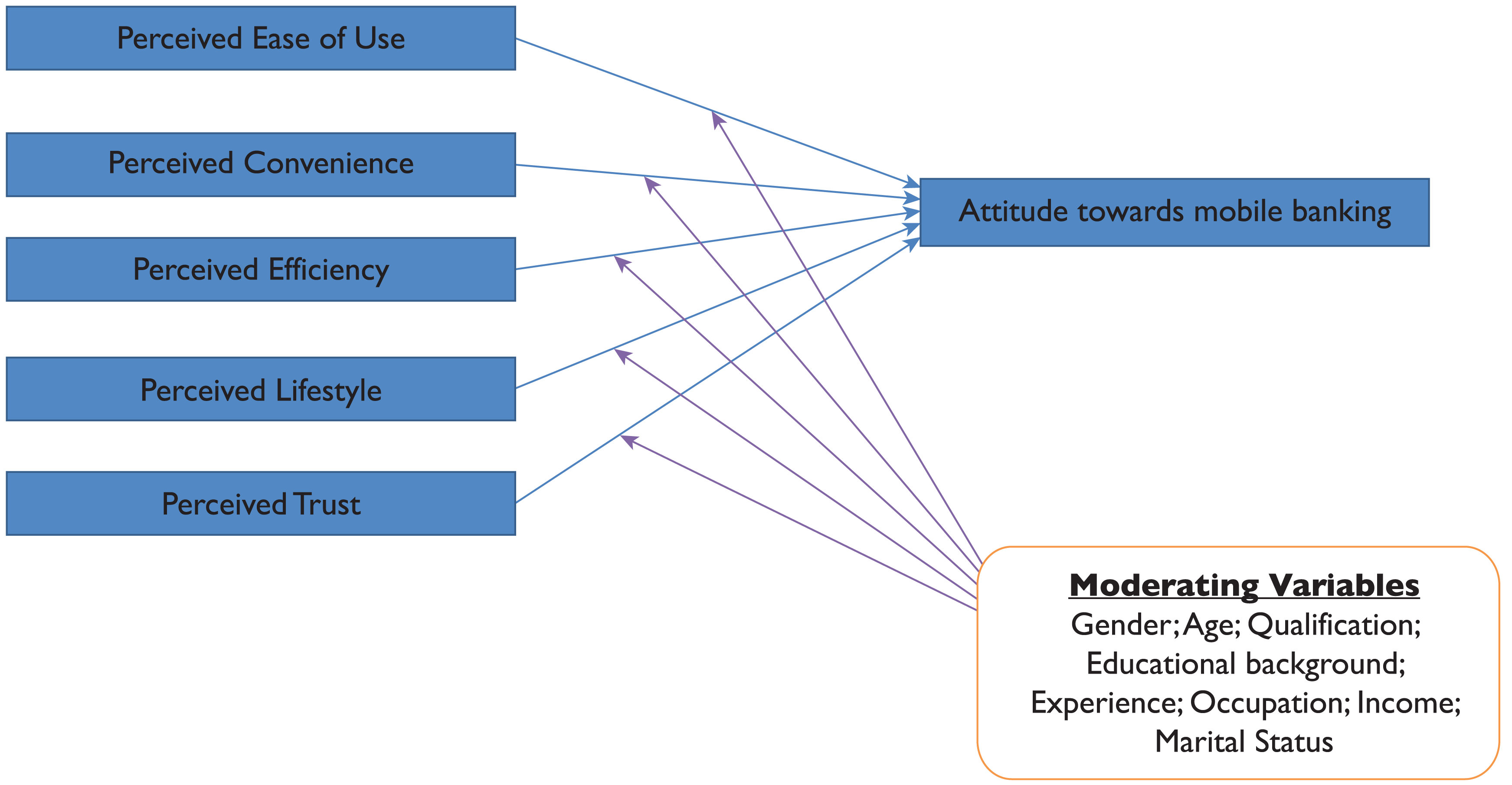

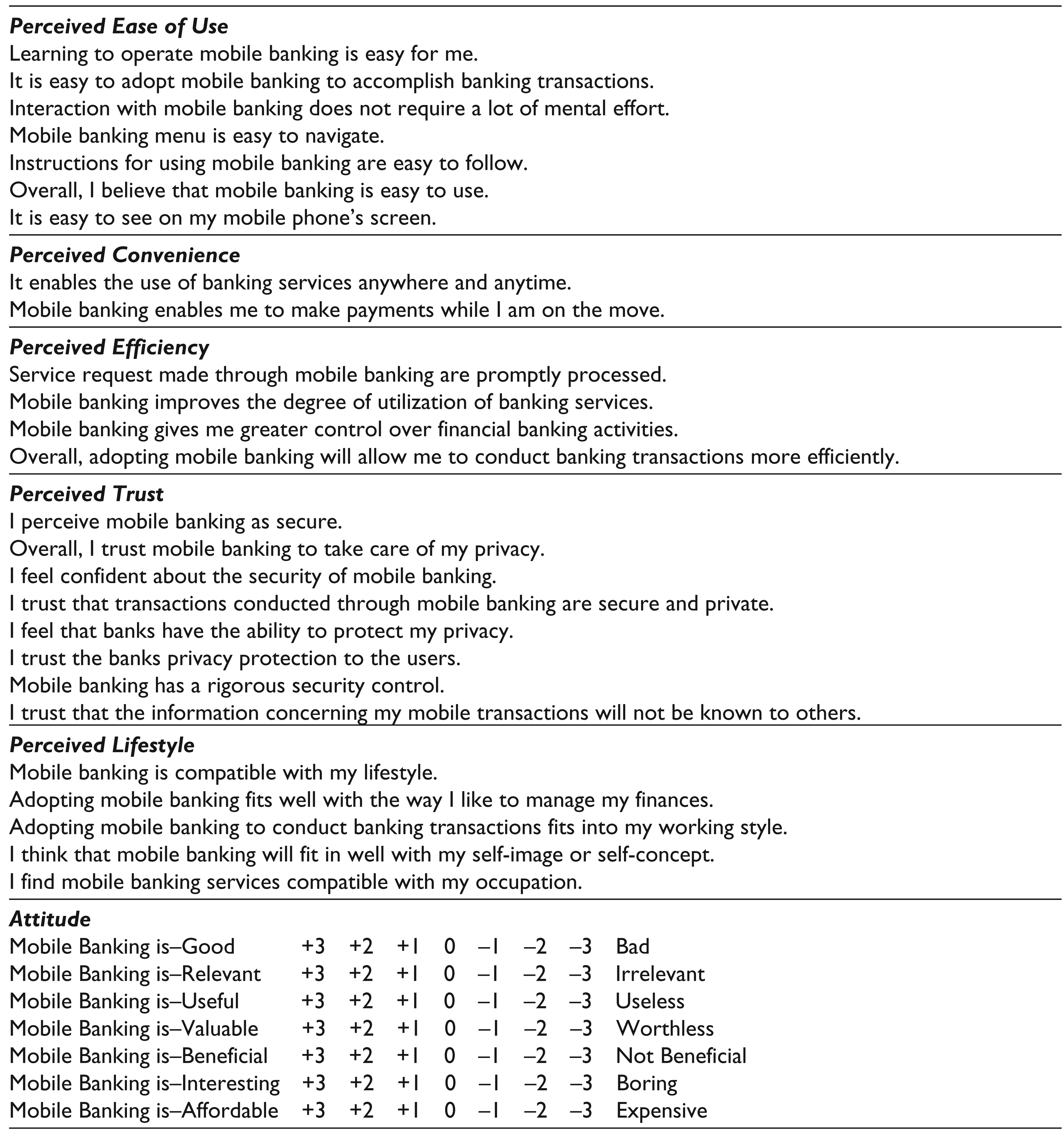

The five factors considered to influence attitude are perceived ease of use, perceived convenience, perceived efficiency, perceived lifestyle and perceived trust. The demographic variables considered are gender, age, qualification, educational background, experience, occupation, income and marital status. Perceived ease of use is the degree to which a technology is perceived easy to understand, learn or operate. Perceived convenience is the degree to which consumers can manage their finances anywhere, anytime in real-time. Perceived efficiency is the ability of users to derive more value from the transaction with similar or lower effort. Perceived lifestyle is explained in terms of consumer personality, innovativeness, degree of interactions and relationships. Perceived trust is defined as a critical component of a transaction and is associated with terms like security, privacy and perceived risk. This is depicted in Figure 1.

The five constructs are based on synthesis of the review of literature and the qualitative research (focus group discussion), details of which are discussed in the next section. Most of the scales are taken from earlier study and confirmed using confirmatory factor analysis.

Methodology

In review of literature, the results of a focus group discussion with eight senior managers of public sector banks resulted in 59 statements responsible for the adoption of mobile banking. These statements were vetted by external experts and they were of the opinion that 17 statements were capturing the same reasons for mobile banking adoption as some of the other statements. The 17 statements were removed and remaining 42 statements were subjected to an exploratory factor analysis with Varimax rotation. They satisfied the conditions for KMO being greater than 0.5 (KMO = 0.947) and Bartlett’s Test of Sphericity being significant as indicated by p-value less than 0.05. This resulted in emergence of seven factors which were labelled as Factor 1 = Behavioural Intention (BI); Factor 2 = Trust (TR); Factor 3 = Ease of Use (EOU); Factor 4 = Attitude (ATT); Factor 5 = Lifestyle (LS); Factor 6 = Efficiency (EFF) and Factor 7 = Convenience (CON), respectively, (refer Appendix 1). Together, they explained 76 per cent of the total variance.

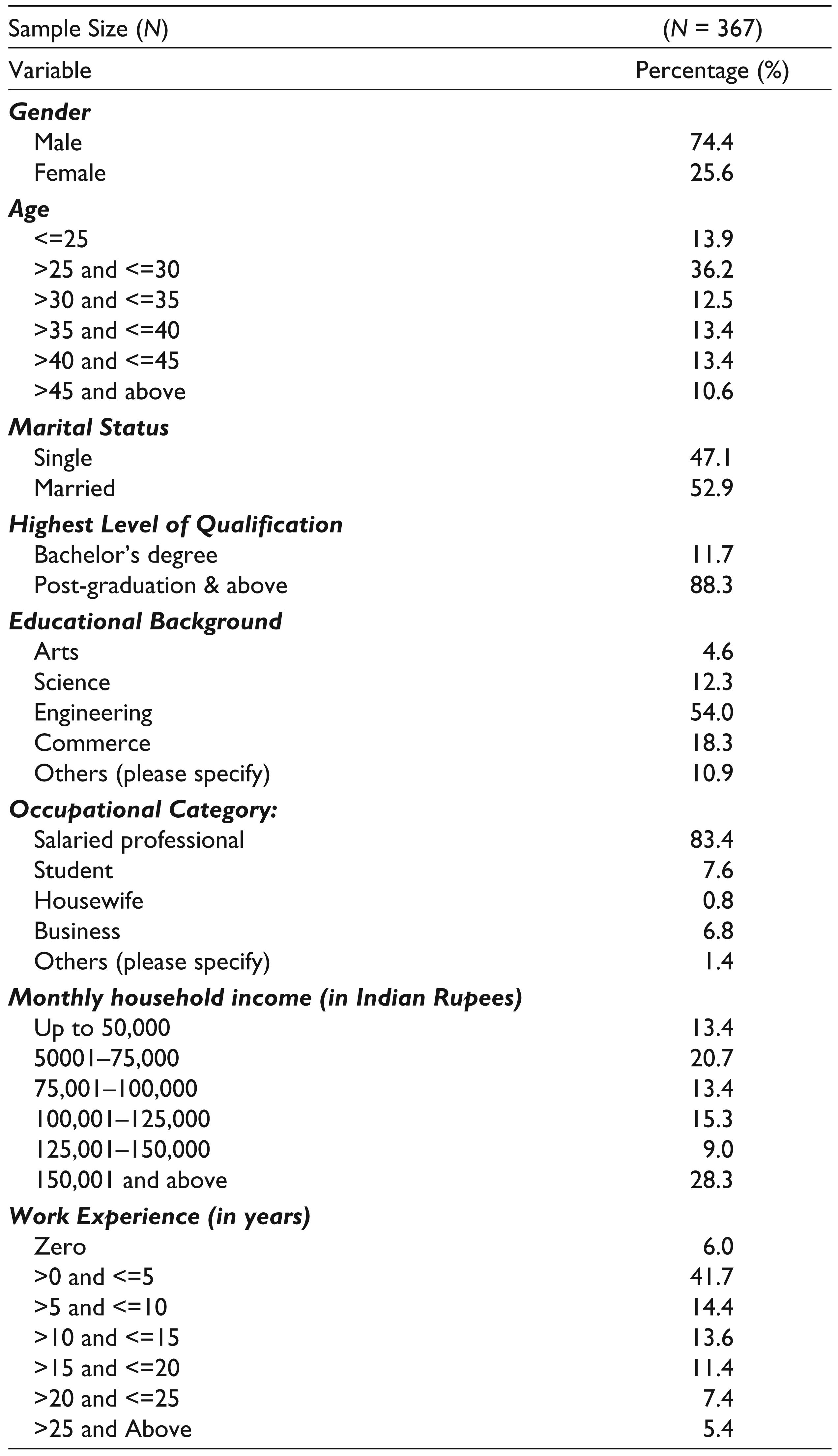

Another sample comparable to the one used for exploratory factor analysis was taken. The size of the sample was 367. Out of the 367 respondents, approximately 75 per cent of them were males, 55 per cent were engineering graduates, 88 per cent had acquired post-graduate degree as their highest qualification, 50 per cent were less than or equal to 30 years, 84 per cent were salaried professionals and 53 per cent were married. The demographic distribution is shown in Table 1.

Next, confirmatory factor analysis was conducted to confirm the factors as obtained in exploratory factor analysis. Both online and physical surveys were used to collect data. No financial incentives were given for filling the surveys. Cross-section survey was used for data collection over a period of 1 month. All the conditions needed for confirmatory factor analysis were met. Multivariate normality test using Mardia’s coefficient was satisfied. The values of normed chi-square = 2.047; CFI = 0.944; NFI = 0.896; TLI = 0.939 and RMSEA = 0.053 were found to be in acceptable range (Hu & Bentler, 1998). Further, the conditions of convergent and discriminant validity were well within the acceptable range.

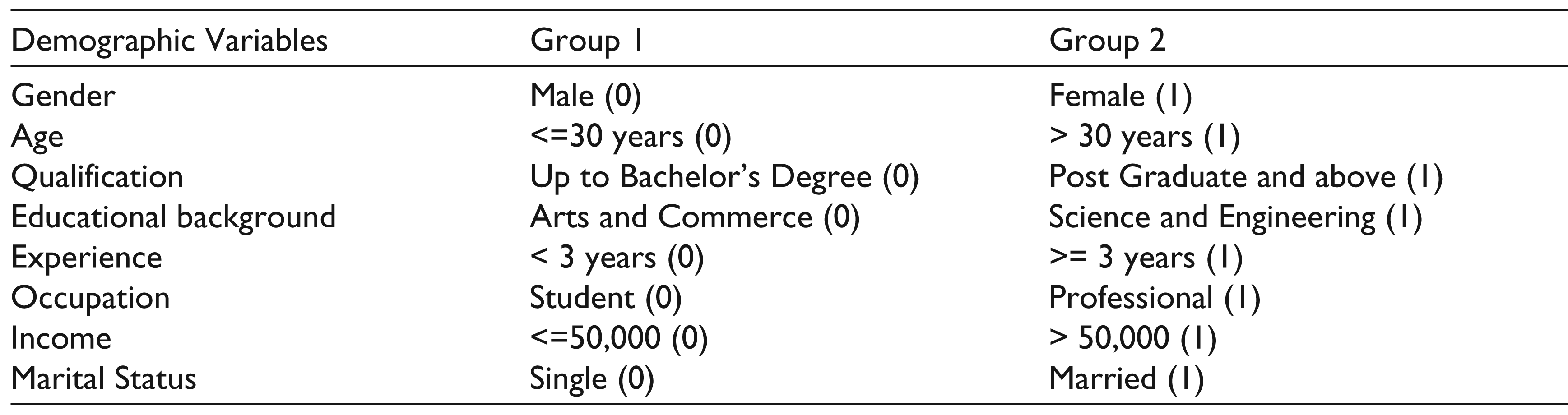

For examining the moderation effect of the demographic variables, such as gender, age, qualification, educational background, job experience, occupation, income and marital status, various antecedents of mobile banking adoption along with attitude were considered. Each of these demographic variables was divided into two groups. Group 1 comprises of male, respondents with age less than or equal to 30 years, educational qualification up to bachelor’s degree, education background being arts and commerce with a work experience of less than 3 years, occupation being student, with income less than or equal to ₹50,000 per month and marital status being single. Group 2 comprises of female, respondents with age greater than 30 years, with post-graduate and above qualification, with educational background being science and engineering, having experience of greater than or equal to 3 years, working as professional, having income of greater than ₹50,000 per month and marital status being married. The Group 1 was coded as 0 and Group 2 as 1. The above description of demographic profile is exhibited in Table 2.

To test the moderation effect of demographic variables, the following multiple regression is proposed (Sharma, Durand & Gurarie, 1981)

where Y = dependent variable (in the present case attitude towards mobile banking); H = independent variable (in the present case it is perceived lifestyle or perceived trust or perceived efficiency or perceived convenience or perceived ease of use); Z = dichotomous moderator variable having a value of 1 and 0 (e.g., Z = 1 for female and Z = 0 for male and similarly for other as shown in Table); and HZ = the interaction term between independent and moderator variable.

Descriptive Statistics of Survey Data (N = 367)

The Demographic Description of Two Groups

For Z to be a pure moderator variable, the coefficient d should be significant, whereas b and c should be statistically insignificant. Z is a quasi-moderator variable if both the coefficients c and d are statistically significant.

The second method to test for moderation is through Fisher’s Z-transformation. To determine the moderator effect using Fisher’s Z-transformations, the sample for each of the demographic variables is divided into two groups (Dailey, 1978). The correlation coefficient between the dependent variable and independent variable is computed for Group 1 and labelled as r1. Similarly the correlation coefficient between the dependent and the independent variable is computed for the Group 2 and denoted by r2. The hypothesis to be tested for examining the moderating effect is as follows:

H0: ρ1 = ρ2 (There is no moderation effect) H1: ρ1 ! ρ2 (There is a moderation effect)

where ρ1 and ρ2 denote the population correlation coefficients for Group 1 and Group 2, respectively.

Now as per the Fisher’s Z-transformation, we define

Now, Z1–Z2 follows a normal distribution with mean zero and variance =

Now, Z is defined as

For a given level of significance, if computed value of absolute Z is greater than the absolute tabulated value, null hypothesis is rejected that means there is a moderation effect.

In Fisher’s Z-test, the correlation coefficient between independent and dependent variables across the two groups are compared. In the case of regression method, we examine whether the regression coefficients are different in the two groups or in other words, interaction effect is significant or not.

Analysis of Data and Findings of the Study

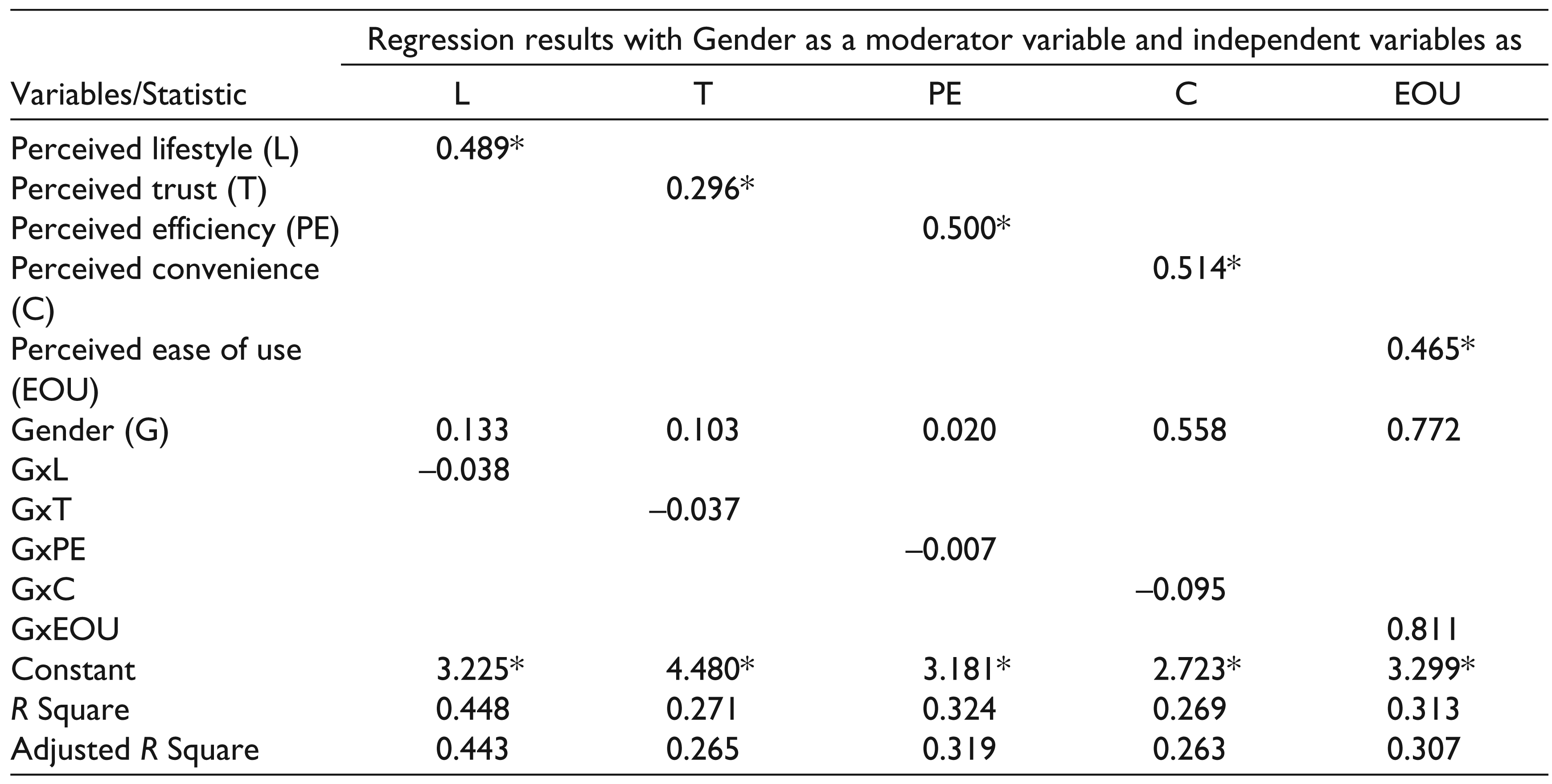

The regression results with gender as a moderator variable are presented in Table 3. The results indicate that gender does not moderate the relationship among each of the independent variables, namely, perceived lifestyle, perceived trust, perceived efficiency, perceived convenience and perceived ease of use, with the dependent variable attitude towards mobile banking. This is because the interaction effect in each of these cases is insignificant. The only conclusion that can be drawn is that each of these independent variables significantly affect attitude towards mobile banking.

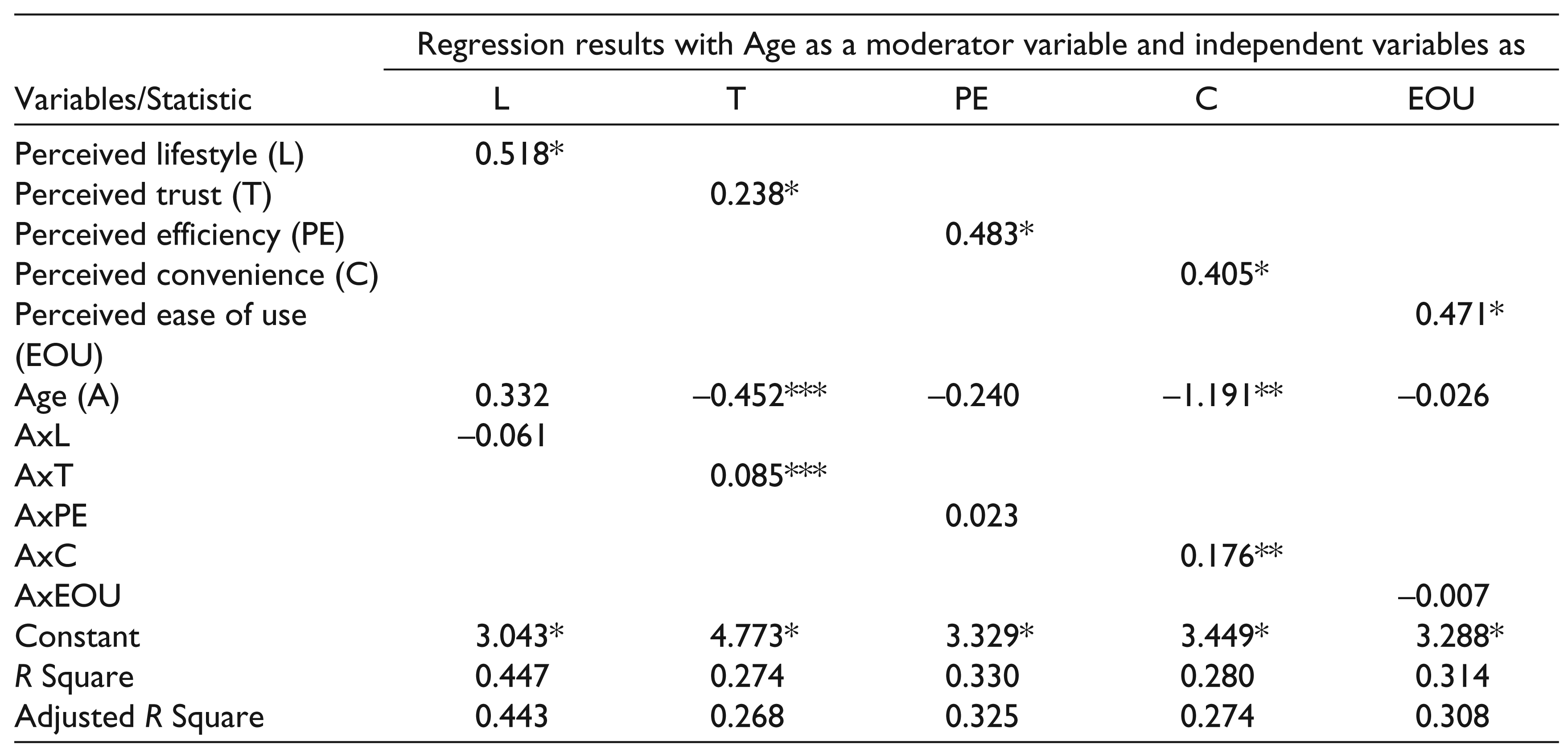

The second moderator variable that was considered is age. The results as shown in Table 4 indicate that age moderates the relationship between trust and attitude and also convenience and attitude. It is seen that for those respondents who are in the age group greater than 30, the influence of trust on attitude is higher as compared to those who are 30 years or below. One plausible reason for this could be that elderly customers might have been the user of the facility for a long time and their experience might be positive. Further, it is seen that for elderly respondents (above 30 years of age), this medium is found to be more convenient as compared to the one with younger age.

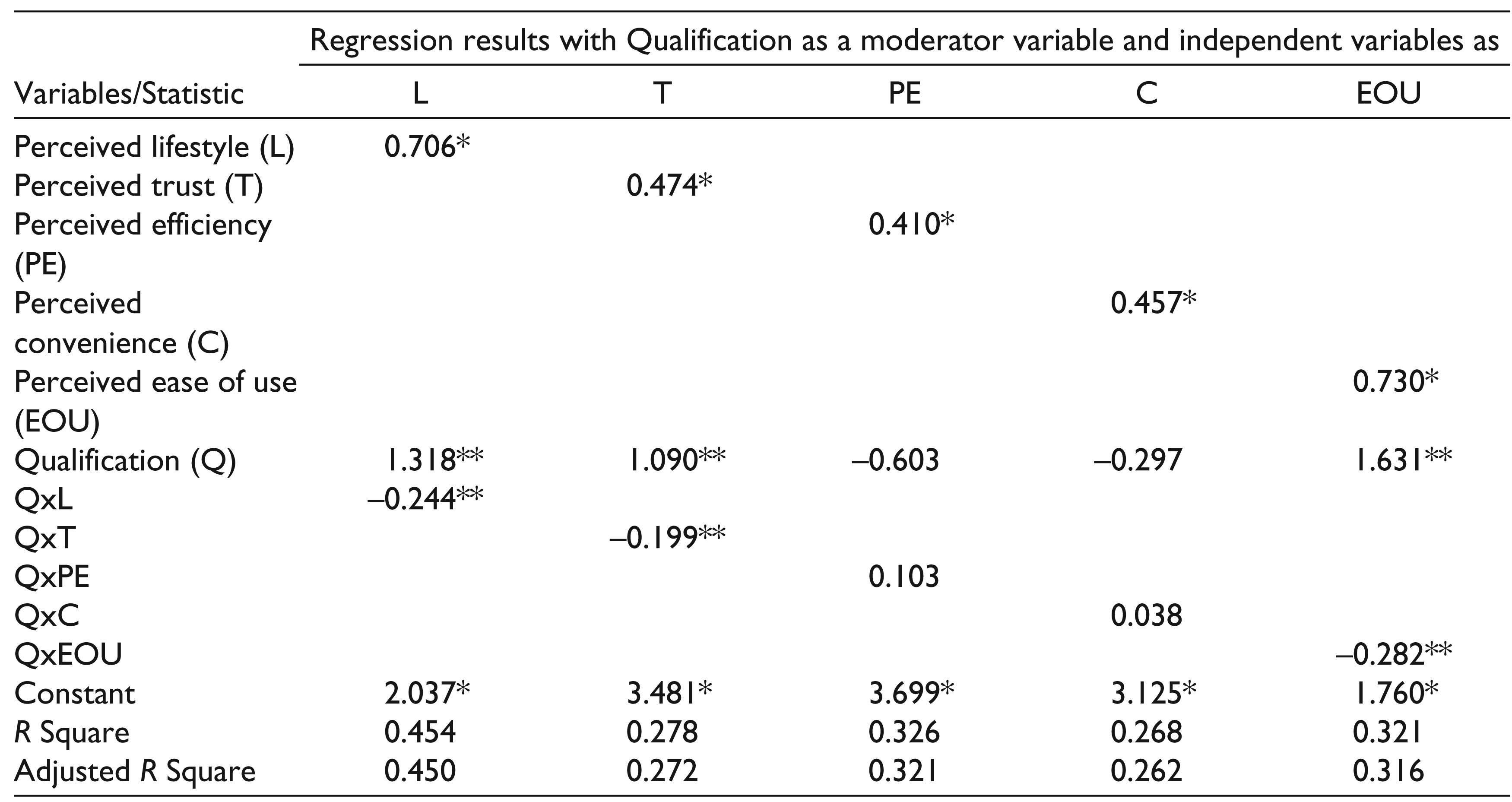

It is seen from Table 5 that qualification moderates the relationship between lifestyle, trust and ease of use with attitude towards mobile banking. In case of those who are post-graduate and above the impact of lifestyle on attitude is negative as compared to those who are having graduate and below qualification. The qualification moderates the relationship between trust and mobile banking attitude. This is higher for highly qualified people (post-graduate and above) as compared to those who are graduate and below. The effect of ease of use on attitude is found to be lower in case of post-graduates and above as compared to those whose qualification is up to graduation.

Gender as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

Age as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

Qualification as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

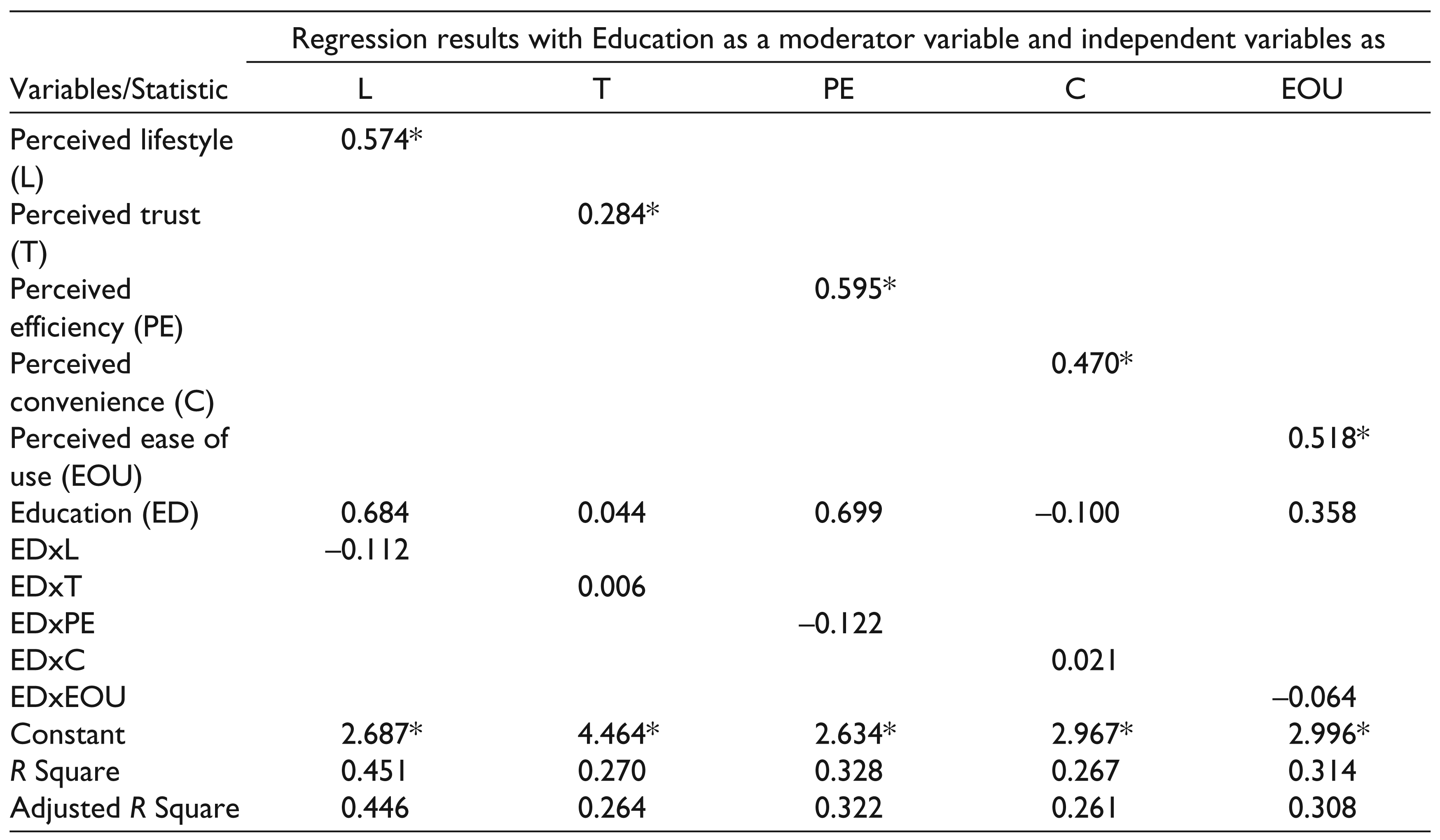

The results in Table 6 indicate that educational background does not moderate the relationship between any of the independent variables and attitude towards mobile banking. This means that the effect of each of the independent variables towards mobile banking is same irrespective of the educational background of the respondents.

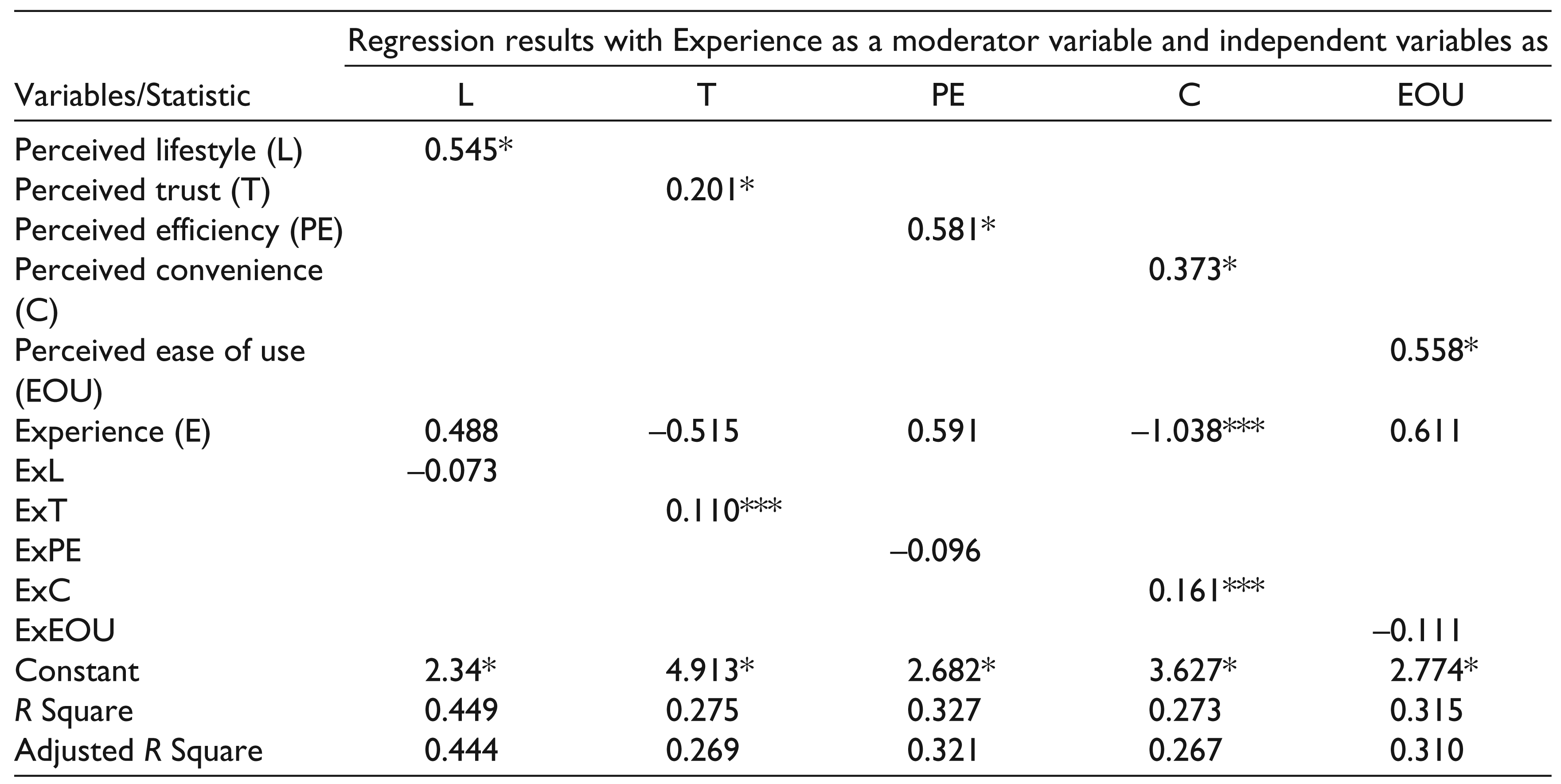

With respect to experience, it is observed that the impact of perceived trust on attitude towards mobile banking is more in case of people with more than 3 years of work experience in relation to those who have less than or equal or equal to 3 years of work experience. Similarly, respondents with more experience (> 3 years) find the impact of convenience on attitude towards mobile banking more than those with less than or equal to 3 years. The results are summarized in Table 7.

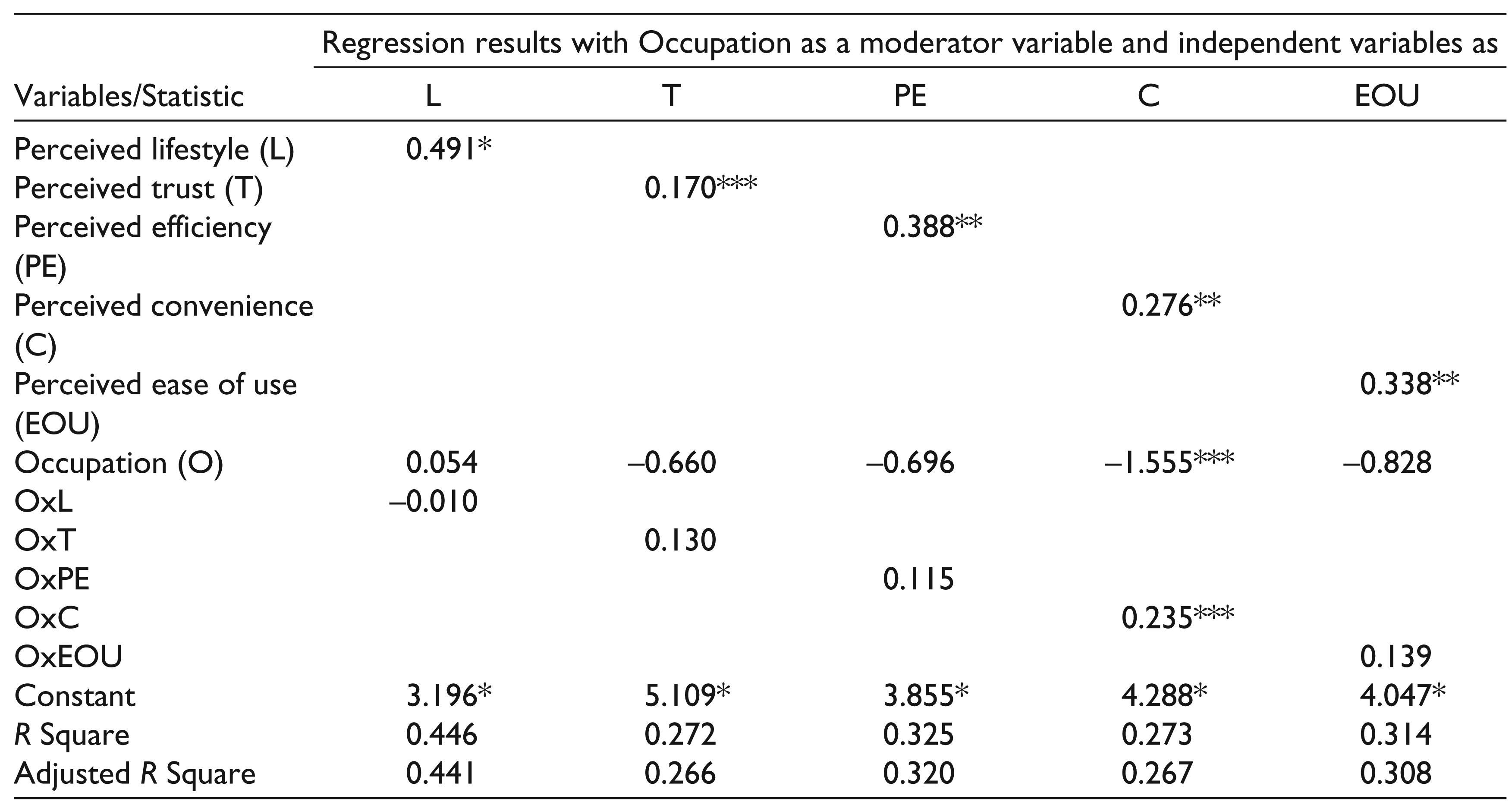

When occupation is used as a moderator variable, it is found (see Table 8) that professionals find the impact of convenience on attitude towards mobile banking more than that of students.

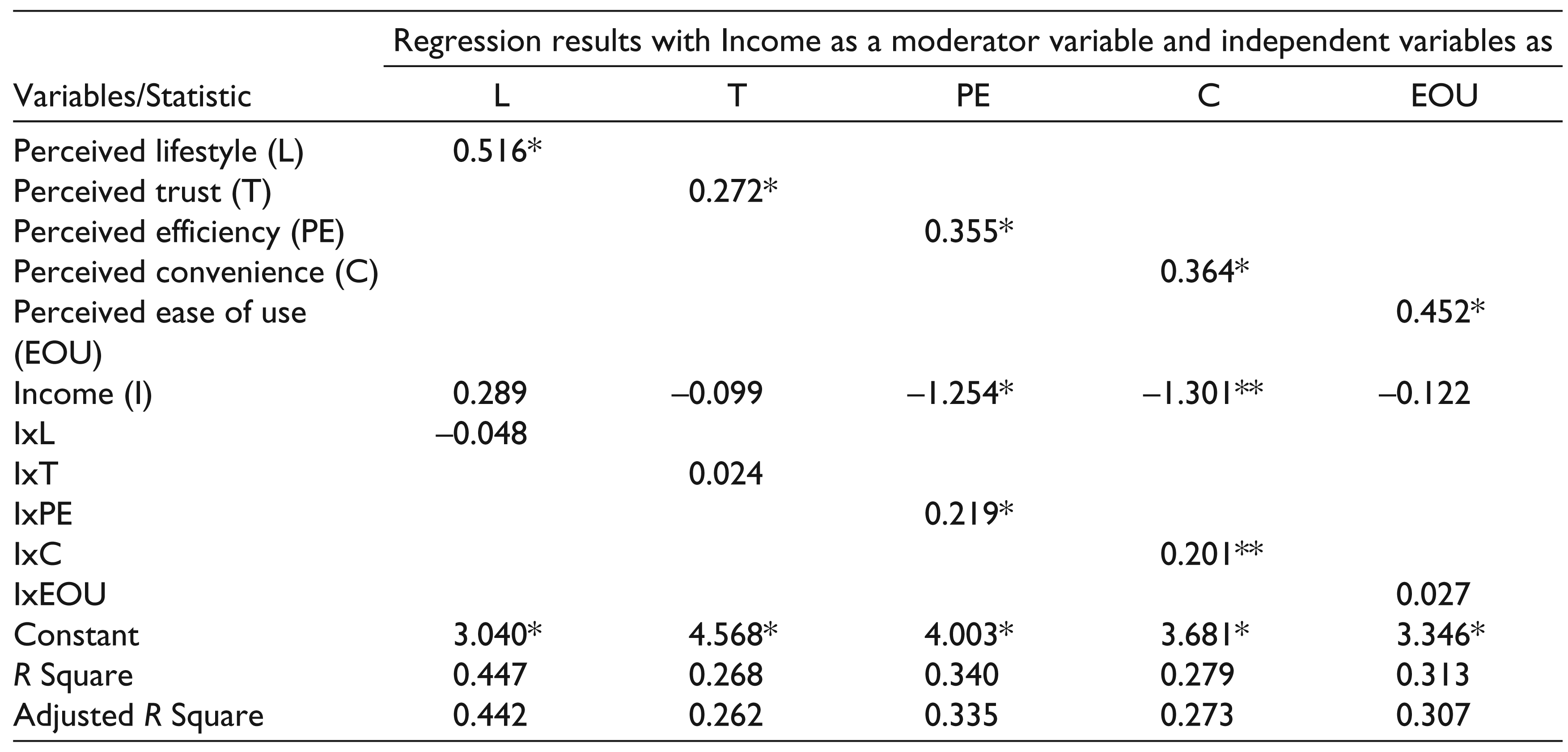

As evident from Table 9, in case of income as a moderator variable, the influence of perceived efficiency and convenience attitude towards mobile banking is more in case of higher income group (greater than 50,000 per month) than in case of low-income group (less than or equal to 50,000 per month).

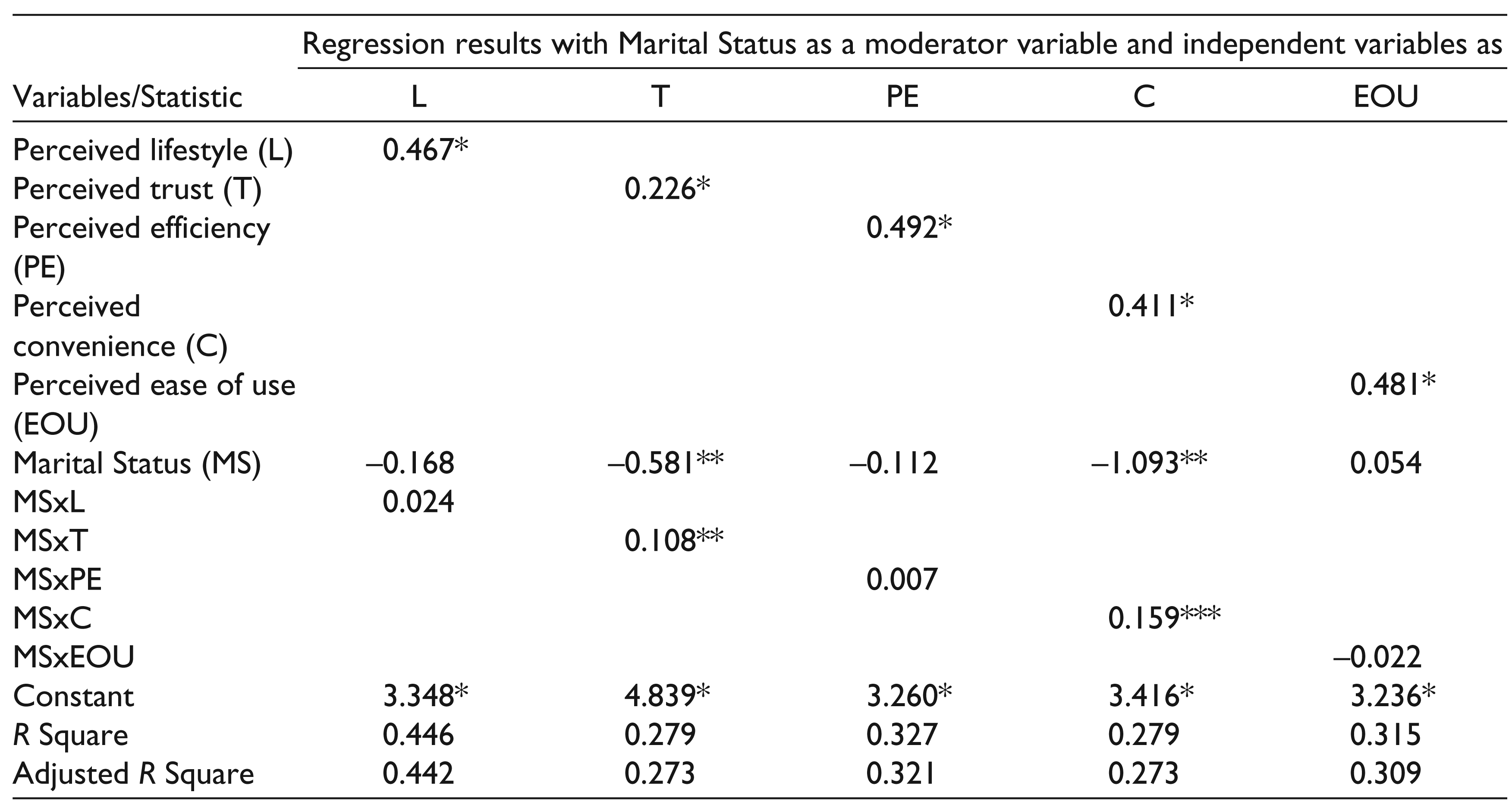

Next, marital status is taken as a moderator variable and the results are shown in Table 10. It is found that the impact of trust and convenience on attitude towards mobile banking is more in case of married respondents as compared to the single respondents.

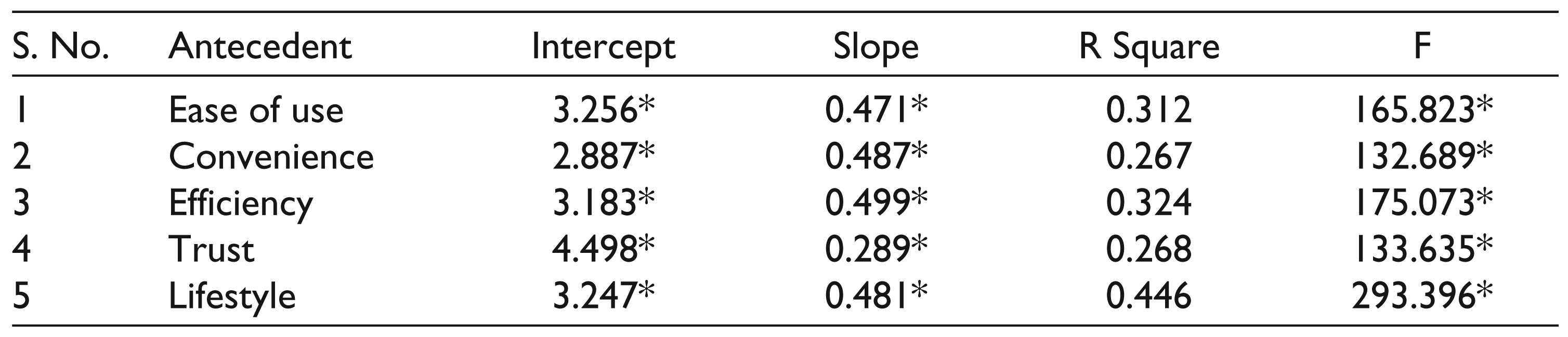

The results of the regression of attitude towards mobile banking on each of the independent variables are given in Table 11.

Education as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

Experience as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

Occupation as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

Income as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

Marital Status as a Moderator

ii.) ** is significant at 5 per cent.

iii.) *** is significant at 10 per cent.

Estimate Regression Results of Attitude on its Various Antecedents

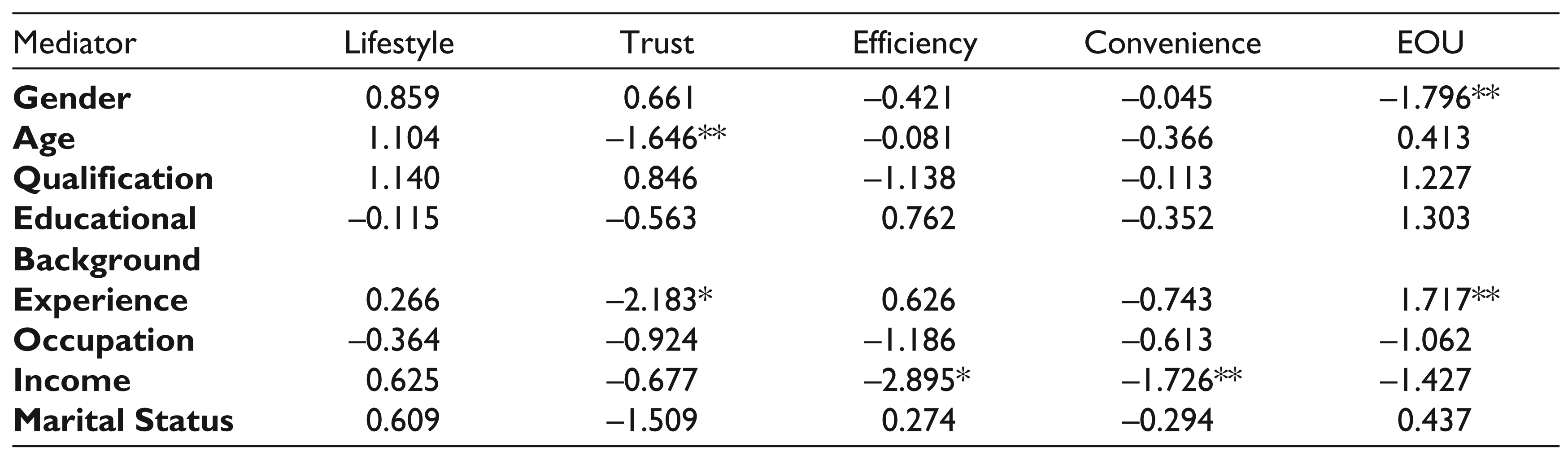

Results of Fisher Z-Statistics

ii.) ** indicates significance at 10 per cent level.

The results in the Table 11 indicate that each of the independent variables has a positive and significant influence on the attitude towards mobile banking. For example, the antecedent ease of use has a positive slope coefficient which implies that with increase in ease of use the attitude towards mobile banking would go up. Similarly, the results for the remaining four antecedents can be interpreted. The five regression equations have R square value ranging from 0.267 to 0.446. Although they are not very high, they are statistically significant as indicated by the F-statistic. This shows that these regressions have a significant goodness of fit.

Next, the moderation effect of demographic variables on the relationship between antecedents to technology adoption and attitude towards mobile banking is tested using Fisher’s Z-transformation. The results are summarized in Table 12.

Summary of Results

Gender has a moderating effect between the ease of use and attitude towards mobile banking. Further, the effect is higher in case of women than in case of men. This means that women have found that the effect of the ease of use for mobile banking is higher in case of women than men. This finding is consistent with earlier studies (Im, Kim & Han, 2008; Venkatesh & Morris, 2000; Wang et al., 2016) who found that the moderating effect of perceived ease of use on intention was slightly stronger for women versus males.

Trust has a positive impact on attitude towards mobile banking. However, age moderates this relationship and it is found that the effect of trust on attitude towards mobile banking is more in case of older respondents (above the age of 30) than younger respondents. This is consistent with suggestions from earlier studies that age has a moderating effect between technology use and perceptions (Demirci & Ersoy, 2008; Lee et al., 2010; Morris & Venkatesh, 2000; Porter & Donthu, 2006; Wang et al., 2009; Wang et al., 2016; Yi et al., 2005). Older users perceive higher risk associated with new technologies when compared to younger users (Liebermann & Stashevsky, 2002). Hence, it is important that new technology is perceived as trustworthy by older users.

It is found that experience moderates the relationship between trust and attitude towards mobile banking. The effect of trust on attitude is more in case of more experienced customers than less-experienced ones. A plausible reason for this could be that it takes time to build up the trust. The amount of time spent on using mobile banking capabilities lowers the risk perception associated with its adoption. The results indicate that experience also moderates the relationship between ease of use and attitude towards mobile banking. It is more in case of less-experienced customers than in case of more experienced customers. It is reasonable to assume that less-experienced customers would be young in age and hence more technology savvy as compared to their other counterparts. The finding contradicts the findings of earlier studies (Im et al., 2008), which suggest that experience does not moderate the relationship between the ease of use and intention.

The income has a moderating effect in measuring the relationship of perceived efficiency attitude towards mobile banking. It is seen that the efficiency in higher income group is more than in case of lower income group. A plausible reason could be that people in the higher income group are busy and do not have time to go to branch for banking. Further, they have enough financial resources to purchase latest smartphones and Internet packages for conducting banking transactions whenever required. Thus, they opt for mobile banking as a preferred way to do their banking transactions. Income moderates the effect of perceived convenience on the attitude towards mobile banking. The effect of perceived convenience is more in case of higher income group than lower income group. This is because people in higher income group are busy and thus have little time to physically visit bank branch. Thus, they perceived mobile banking as a convenient way to conduct mobile banking transactions.

The academic qualifications, educational background, occupation and marital status of the respondent do not have any moderation effect of antecedents of mobile banking adoption on the attitude towards mobile banking. With respect to educational level or qualification, our findings corroborates the finding of Wang et al. (2016) who found educational level not to be an important moderator of the key relationship with user intention. These findings contradict previous studies which support the hypothesis that highly educated people tend to adopt new technology more quickly than the less educated (Weinberg, 2005).

Conclusion and Implications of the Study

The study uses two well-established theories, TAM and DoI, to explain the impact of antecedent variables, such as ease of use, convenience, efficiency, trust and lifestyle, on attitude towards adoption of mobile banking. The study attempts to conceptualize a new model by incorporating additional demographic variables which have not been explored before. Further, the moderating effect of demographic variables on attitude towards mobile banking was tested using two methods (a) regression analysis and (b) Fisher’s Z-statistics.

The results of regression analysis show that each of the independent variables has a positive and significant influence on the attitude towards mobile banking as indicated by t-statistics. The explanatory power of the model as indicated by R square for various independent variables vary between 27 per cent and 45 per cent, which are significant as per F-statistics. This shows that each of the proposed variables influence user attitude towards mobile banking adoption. This corroborates previous research studies, which have found perceived ease of use (Deb & David, 2014; George & Kumar, 2013; Gu et al., 2009; Lin, 2011; Nasri & Charfeddine, 2012; Suh & Han, 2003); convenience (Agarwal, Rastogi & Mehrotra, 2009; Howcroft, Hamilton & Hewer, 2002; Liao & Wong, 2008; Suh & Han, 2003); efficiency (Deb & David, 2014; Lin, 2011; Mohammadi, 2015); trust (Agarwal et al., 2009; Hernandez & Mazzon, 2007; Lewis, Palmer & Moll, 2010; Lin, 2011; Nasri & Charfeddine, 2012) and lifestyle (Mohammadi, 2015; Riquelme & Rios, 2010; Tan & Teo, 2000) to positively and significantly influence attitude. In the Indian context, Kumar, Lall and Mane (2017) in a study involving management students found that perceived ease of use, perceived usefulness, social influence and trust propensity positively and significantly influence intention to use mobile banking services.

If we compare the results as obtained from the regression analysis and that of Fisher’s Z-transformation, the following conclusions emerge:

Gender does not moderate the relationship using regression analysis, whereas in case of Fisher’s Z-transformation, it is found to moderate the relationship between ease of use and attitude and the effect is more in case of females than males. Our study corroborates the findings of earlier studies (Amin et al., 2006, Riquelme & Rios, 2010). Ease of use has a stronger influence on female respondent than males (Riquelme & Rios, 2010; Wang et al., 2016). This suggests that perception of ease of use is more salient for females than males (Wang et al., 2016). However, the direction of the moderating effect is found to be opposite in comparison with findings by Amin et al.‘s (2006) who found that male undergraduate students were slightly more inclined to see mobile phones as a practical device for banking purposes.

Age moderates the relationship between trust and attitude in the same direction by both the methods. It is seen that the impact of trust on attitude is more for elder respondents than for younger respondents. Further, it is seen that age moderates the relationship between convenience and attitude where the younger respondent find it more convenient than the older ones.

Income moderates the impact of perceived convenience and efficiency on attitude towards mobile banking and in the same direction.

Experience moderates the relationship between trust and attitude in both the methods, whereas it acts as a moderator for ease of use to attitude using Fisher’s-Z test and convenience to attitude in regression analysis.

Occupation does not act as a moderator as per Fisher’s Z-transformation; however, it moderates the relationship between perceived convenience and attitude towards mobile banking.

The marital status does not moderate the relationship using Fisher’s Z-test, whereas it has impact in influencing relationship between trust and convenience on attitude.

Qualification does not moderate the relationship using Fisher’s Z-test, whereas it has impacted the relationship of three independent variables, namely, lifestyle, trust and ease of use on attitude towards mobile banking.

Educational background does not act a moderator using both the tests.

Many of the results using the two methods are similar. There are of course differences between the two in some cases which could probably be due to the nature of assumptions that two methods make in testing a moderator variable. The independent variables on which demographic variables have shown a moderating effect are trust, convenience and ease of use.

Considering the fact that the adoption rate of mobile banking is still marginal, this study reveals that gender, age, income, experience, occupation, qualification and marital status are the salient demographic variables, which moderate the impact of independent factors (ease of use, trust, lifestyle, convenience and efficiency) on user attitude towards mobile banking. High degree of competition among Indian banks has resulted in banks offering innovative customer tools, the latest being mobile applications to service customers in a better way. The first managerial and business implication which could be drawn from this study is that banks are advised to enhance the use of mobile banking usage, particularly through offering mobile banking applications which are easy to use, convenient, secure, efficient and match the lifestyle expectations of their users. The second implication is based on the finding that except educational background all other demographic variables moderate the relationship with user attitude. Thus, banks should make an attempt to increase and promote the features of mobile banking, such as ease of use, convenience and efficiency among female users. Similarly, with respect to age, banks should develop strategies to enhance confidence among old age consumers about the convenience and security of mobile banking channel. Beyond ease of use, trust and convenience, banks must also emphasize on the compatibility between the banking services offered and the working/lifestyle of their target customers. It may involve spending more time explaining the capabilities of mobile banking or simplifying the interface for older users. Another implication could be designing suitable services to meet the specific needs of different demographic segments.

Limitations and Scope for Future work

Despite the previous findings, the study has some limitations that should be addressed in the future. First, the current study is based on respondents mostly from North India. India, considering its large population, demographic and socio-economic differences exists between different regions (North, South, East and West). Further study needs to be carried out to apply the model used in this study across the four regions to identify similarities and differences. This will help banks and technology companies to devise specific strategies to address user expectations from these regions. Second, further studies can be carried out to apply the model to other developing countries and cross-cultural comparisons can be made. Finally, our study looks at the relationship between the antecedent variables and attitude towards mobile banking adoption and the moderation effect of various demographic variables. Further, studies may be carried out to test if there exist any causal relationships between the antecedent variables and whether the causal relationship is moderated by demographic variables.

Footnotes

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

An earlier version of this paper was presented as a full research paper entitled ‘Role of demographics as moderator in mobile banking adoption’ in Twenty-third Americas Conference on Information Systems, Boston in August 2017 and was published in their conference proceedings.

(Questionnaire)

>Read the following statements and indicate your level of agreement/disagreement for the following statements a seven-point scale as indicated below (1 = Strongly Disagree and 7 = Strongly Agree)

|

|

| Learning to operate mobile banking is easy for me. |

| It is easy to adopt mobile banking to accomplish banking transactions. |

| Interaction with mobile banking does not require a lot of mental effort. |

| Mobile banking menu is easy to navigate. |

| Instructions for using mobile banking are easy to follow. |

| Overall, I believe that mobile banking is easy to use. |

| It is easy to see on my mobile phone’s screen. |

|

|

| It enables the use of banking services anywhere and anytime. |

| Mobile banking enables me to make payments while I am on the move. |

|

|

| Service request made through mobile banking are promptly processed. |

| Mobile banking improves the degree of utilization of banking services. |

| Mobile banking gives me greater control over financial banking activities. |

| Overall, adopting mobile banking will allow me to conduct banking transactions more efficiently. |

|

|

| I perceive mobile banking as secure. |

| Overall, I trust mobile banking to take care of my privacy. |

| I feel confident about the security of mobile banking. |

| I trust that transactions conducted through mobile banking are secure and private. |

| I feel that banks have the ability to protect my privacy. |

| I trust the banks privacy protection to the users. |

| Mobile banking has a rigorous security control. |

| I trust that the information concerning my mobile transactions will not be known to others. |

|

|

| Mobile banking is compatible with my lifestyle. |

| Adopting mobile banking fits well with the way I like to manage my finances. |

| Adopting mobile banking to conduct banking transactions fits into my working style. |

| I think that mobile banking will fit in well with my self-image or self-concept. |

| I find mobile banking services compatible with my occupation. |

|

|

| Mobile Banking is–Good |

| Mobile Banking is–Relevant |

| Mobile Banking is–Useful |

| Mobile Banking is–Valuable |

| Mobile Banking is–Beneficial |

| Mobile Banking is–Interesting |

| Mobile Banking is–Affordable |