Abstract

This article examines the existence of a bank-lending channel in Association of Southeast Asian Nations (ASEAN) using a sample of 328 banks from 2009 to 2015. The findings confirm that a bank-lending channel is effective. In particular, we find that consumer loans and commercial loans are sensitive to changes in monetary policy, but mortgage and corporate loans are not. We also find that commercial banks are vulnerable to monetary policy changes, but both investment and Islamic banks are not. On the contrary, special purpose banks are able to overcome the effect of monetary policy tightening by supplying more loans. The effectiveness of a bank-lending channel in ASEAN also holds when we control for the differences in governance structure of the countries. Policymakers need to take these into consideration in designing an effective monetary policy.

Introduction

Monetary policy is often used by central banks to influence the real economy. The major aim of this policy is to achieve low inflation, full employment and sustainable economic growth. The credit channel emphasizes on the role of bank credit in transmitting monetary policy changes to the real economy. A bank-lending channel is an example of credit channel. The conceptualization of the bank-lending channel is initialized by Bernanke and Blinder (1988). It focuses on the role of banks as financial intermediaries that have a competitive advantage in solving information asymmetry problem that exists between borrowers and lenders in the financial market. This model is based on the notion that some borrowers would only have access to credit market through the banks. Given that they are not able to substitute loans with other sources of credit, a decrease in bank loans will reduce investment and ultimately lead to a reduction in aggregate demand.

Banks play a very important role in providing credit in developing countries (Sufian, 2009). It is particularly true in the case of the ASEAN economy due to the underdevelopment of equity and bond market (Lee & Takagi, 2013). However, banks may face difficulties in extending credit facility to clients during a contractionary monetary policy because they are not able to replace the loss of deposits with other source of funds. This makes the bank-lending channel a crucial monetary policy transmission mechanism in the ASEAN economy. Nevertheless, the well-functioning of this channel can be influenced by various other factors in a country. The ASEAN economy differs widely in terms of its size, development stages and industrial structure. In line with this, considerable differences also exist in the development of financial sector in the region. Therefore, it is crucial to understand under what circumstances the bank-lending channel is effective so that necessary monetary policy decisions can be made to achieve a particular objective.

Different types of banking institutions exist in the ASEAN countries. Commercial banks have long dominated the financial services industry in the region by providing loans to individuals and businesses (Lee & Takagi, 2013). Investment banks, on the one hand, are mainly involved in fee-based transactions such as buying and selling of stocks, bonds and other investments as well as helping companies to go public with initial public offerings (IPO). Special purpose banks are government-linked institutions that are responsible for providing financing to a specific industry to facilitate its development (Asian Development Bank, 2013). Islamic banks engage in financing activities based on two principles: prohibition of interest and propagation of profit and loss sharing. Given the differences that exist in the type of financial institutions, the nature of competition within the banking sector may vary. This may give rise to different responses after monetary policy shocks. Similarly, differences also exist in the type of loans provided by these above-mentioned institutions. Hence, their sensitivities of monetary policy changes may also be different. In addition, the governance structure of the ASEAN countries also varies and may influence the effectiveness of the bank-lending channel.

Existing studies on a bank-lending channel in ASEAN have dwelt on issues related to the consolidation (Olivero, Li, & Jeon, 2011b) and competition (Khan, Ahmed, & Gee, 2016; Olivero, Li, & Jeon, 2011a). This study will contribute to the existing literature by analysing the effectiveness of the bank-lending channel by considering differences that exist in the type of banks, type of loans and governance structure. More specifically, this study will provide answers to the following questions: (a) which type of financial institutions is more sensitive to changes in monetary policy? (b) does the effectiveness of monetary policy transmission differ based on the type of loans? and (c) does governance influence the effectiveness of monetary policy?

The rest of the article is structured as follows. The second section provides the literature review. The third section describes the methodology. The fourth section presents an analysis of results and discussions, while the fifth section concludes the article.

Literature Review

In analysing the existence of a bank-lending channel, the existing literature has differentiated loan supply movement from the loan demand movement by emphasizing on the cross-sectional differences that exist between banks (Gambacorta, 2001). This is done on the basis that loan supply movements are influenced by bank-specific characteristics, whereas the same is not applicable in the case of loan demand movements. Earlier studies on the bank-lending channel have used aggregate data in identifying the existence of the bank-lending channel (Bernanke & Blinder, 1992; Kashyap, Stein, & Wilcox, 1993). Later studies have used bank-level data to test for the existence of the bank-lending channel (Ehrmann, Gambacorta, & Martínez-Pagés, 2001; Kashyap & Stein, 1995; Kishan & Opiela, 2000). Doing so takes into account the fact that the reactions of banks to monetary policy changes vary based on the characteristics of the banks.

Earlier studies have mainly analysed the effectiveness of bank-lending channel by focusing on the banks’ balance sheet strength (Altunbaş, Fazylov, & Molyneux, 2002; Ehrmann, Gambacorta, & Martínez-Pagés, 2001; Kashyap & Stein, 1995; Kishan & Opiela, 2000). Most of the earlier studies are based on banks in the USA. Later studies have confirmed the effectiveness of the bank-lending channel in Central and Eastern Europe (Matousek & Sarantis, 2009), India (Bhaduri & Goyal, 2015), China (Li & Lee, 2015), Russia (Ono, 2015), Turkey (Meral, 2015) and Malaysia (Asbeig & Kassim, 2015). Studies by Kakes and Sturm (2002), Zulkhibri (2013), Deng and Liu (2014) and Ferri, Kalmi, and Kerola (2014) have explored different aspects of the effectiveness of the bank-lending channel. Kakes and Sturm (2002) found effectiveness of bank-lending channel differs according to the type of banks. In particular, they found that credit cooperatives in Germany are more sensitive to monetary shocks. Zulkhibri (2013) observed that finance companies and banks that have higher exposure to corporate loans in Malaysia are more sensitive to monetary policy shocks. Deng and Liu (2014) found that the effectiveness of the bank-lending channel in the Australian banking sector varies based on the size of the bank and types of loans. A study by Ferri et al. (2014) on the European bank during the period 1999–2011 shows that stakeholder banks are less sensitive to monetary tightening compared to savings banks.

Theoretical model by Modigliani and Papademos (1980) illustrates that the effectiveness of monetary policy transmission depends on the structure of the financial market. Differences exist in the financial structure of the developed, emerging and low-income countries. Mishra, Montiel and Spilimbergo (2012) asserted that low-income countries are less integrated with the international financial market, less reliant on securities market, have less competitive banking sector and have central banks that intervene heavily in the foreign exchange market. As a result, the bank-lending channel should be more effective in these countries. However, the effectiveness of the bank-lending channel can be hindered by weaker institutional framework, highly concentrated banking sector and greater government ownership of banks in the low-income countries. Similarly, Cottarelli and Kourelis (1994) demonstrated that differences that exist in the structural policies of the financial system can influence the effectiveness of the bank-lending channel. On the other hand, Walsh (2010) asserted that a bank-lending channel works better in highly regulated financial markets compared to liberalized ones.

Most of the existing studies on banking sector mainly focus on developed countries (Sufian & Habibullah, 2009; Sufian & Noor Mohamad, 2012). In line with this, earlier studies on a bank-lending channel are based on banks in the USA and Europe. Recent studies by Matousek and Sarantis (2009), Bhaduri and Goyal (2015), Qiyue and Xian (2015) and Ono (2015) have analysed the effectiveness of a bank-lending channel in developing countries. However, existing studies on bank-lending channels in Asia have mainly focused on the effect of banking sector competition and consolidation on the effectiveness of bank-lending channels (Olivero et al., 2011a, 2011b). Based on the existing literature, we aim to analyse the effectiveness of bank-lending channels in the ASEAN countries by considering the different types of loans, banks and governance structure that exist in the region.

Methodology

The annual bank-level data used in this study are sourced from unconsolidated balance sheet and income statements from Orbis Bank Focus, a financial database maintained by Bureau van Dijk. The analyses of this study are carried out based on an unbalanced panel data of 398 banks from 2009 to 2015. The analyses include banks in Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam. In line with existing studies, the money market rate is considered as the measure of monetary policy. The Treasury bill rate or the discount rate is used when this rate is not available. The monetary policy data and the macroeconomic data are derived from the World Bank’s International Financial Statistics and the respective central banks’ website.

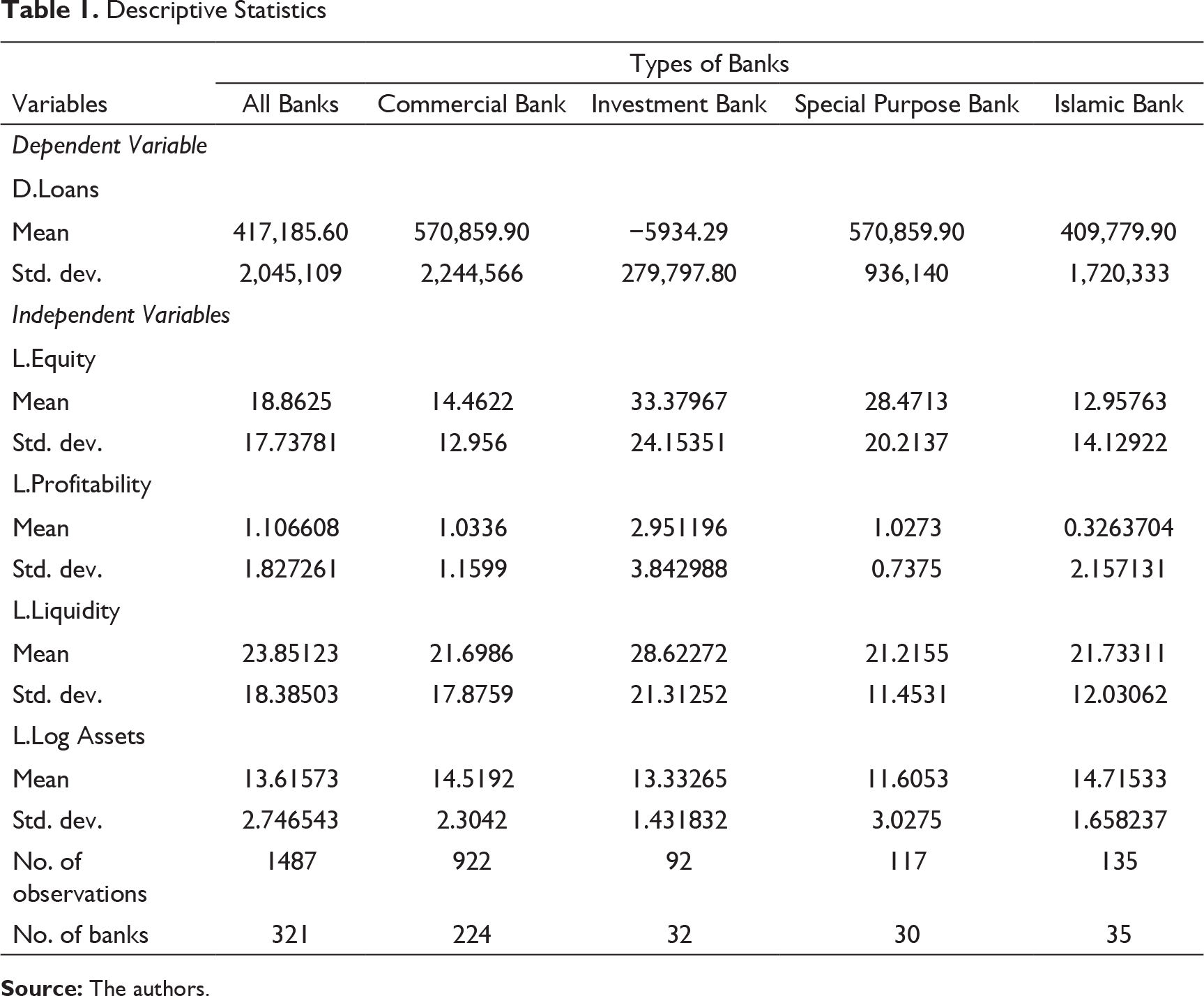

Descriptive Statistics

Based on the IS-LM model, a monetary contraction leads to a higher equilibrium interest rate in the money market, which, in turn, influences the real sector through lower investments. In understanding the role of banks in the monetary transmission mechanism, we used a bank-level fixed-effect panel data model to estimate the effect of monetary policy changes on banks’ loan growth. In line with Kashyap and Stein (1995, 2000), we used bank-level data to analyse the effectiveness of the bank-lending channel in ASEAN. Initially, the following model is estimated:

where i = 1, …, N; t = 1, …, T and j = 1, …, 10, where i represents the bank, t represents the time and j represents the country in which bank i operates. Loani,j,t denotes changes in lending activity for bank i in country j at time t, MP the measure of monetary policy changes for country j at time t. Bank Specifici,j,t represents bank specific control variables of bank i in country j at time t, respectively. Country Specificj,t represents country-level control variables at time t. MP is the monetary policy indicator and loan is the logarithm of total loans. In line with the literature, capital, profitability, liquidity and size are the bank-specific variables that will be controlled to account for the differences that exist in banks’ balance sheets. We used 1-year lag values of the bank-specific variables to reduce the potential endogeneity between loan growth and bank-specific variables. Country-specific variables include growth rate of GDP and consumer price index (CPI). These two variables are controlled to take into account the demand-side effects on loans. εi,j,t is a random error term.

In line with our earlier discussion, we aim to identify whether banks’ reaction to monetary policy differs according to types of loan. In doing so, we re-estimate the baseline model for different types of loans as follows:

where Type of Loansi,j,t represents mortgage, consumer loans, corporate loans and consumer loans. In our subsequent analyses, we focus on the differences in the reactions of different types of bank to monetary policy. In achieving this goal, we include the interaction term of monetary policy and types of bank in the model as follows:

where Bank Typei,j,t represents the dummy variable for the type of banks which include commercial banks, investment banks, special purpose banks and Islamic banks. The inclusion of the interaction terms allows us to isolate the indirect effect of monetary policy on loan growth that varies with bank types from the direct impact that is common across all banks (Ananchotikul & Dulani, 2015). Finally, we examine the effectiveness of bank lending in ASEAN by taking into account the differences that exist in the governance structure of the economies. This is done by re-estimating Equation (1) by including the governance variables in the model.

Panel data estimation method is used for analysing the data. This method considers the cross-sectional and time-series variations of the data. Based on the results of the Hausman tests, fixed-effects model is preferred. This method controls for unobserved heterogeneity when heterogeneity is constant over time and correlated with independent variables. The use of ordinary least square (OLS) method will be inconsistent and biased in this case. Robust standard errors are applied to control for autocorrelation and heteroscedasticity.

Analysis

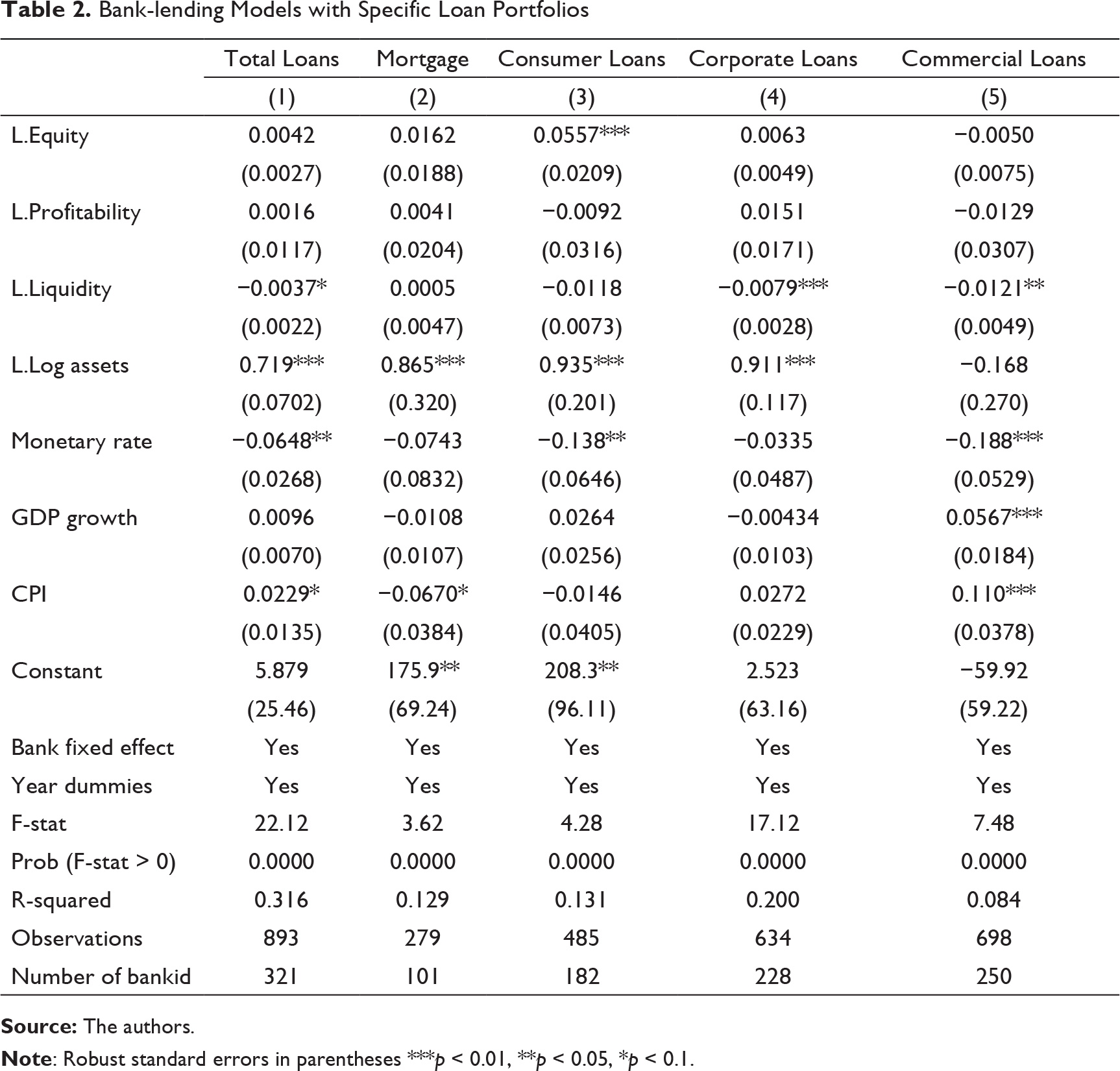

Table 2 reports the results of the effectiveness of the bank-lending channel in the ASEAN banking sector. 1

R-square is panel data that cannot be too high due to cross-sectional heterogeneity. R-square can be higher in the case where the data are more time dominant compared to cross-section dominant. In general, more related explanatory variables can be included to boost the R-square value. However, more focus should be given to the objective of the research (Wooldridge, 2010). Similar model used by Bhaumik, Dang and Kutan (2011), Ananchotikul and Dulani (2015) and Zulkhibri and Sukmana (2017) in identifying the effectiveness of monetary policy also obtained low R-square.

Bank-lending Models with Specific Loan Portfolios

Similar analysis is performed for different types of loan category to identify whether the sensitivity of bank loan supply to monetary policy changes vary depending on banks’ loan composition. 2

Data on type of loans is only available for ASEAN-5 countries (i.e., Indonesia, Malaysia, Philippines, Thailand and Singapore).

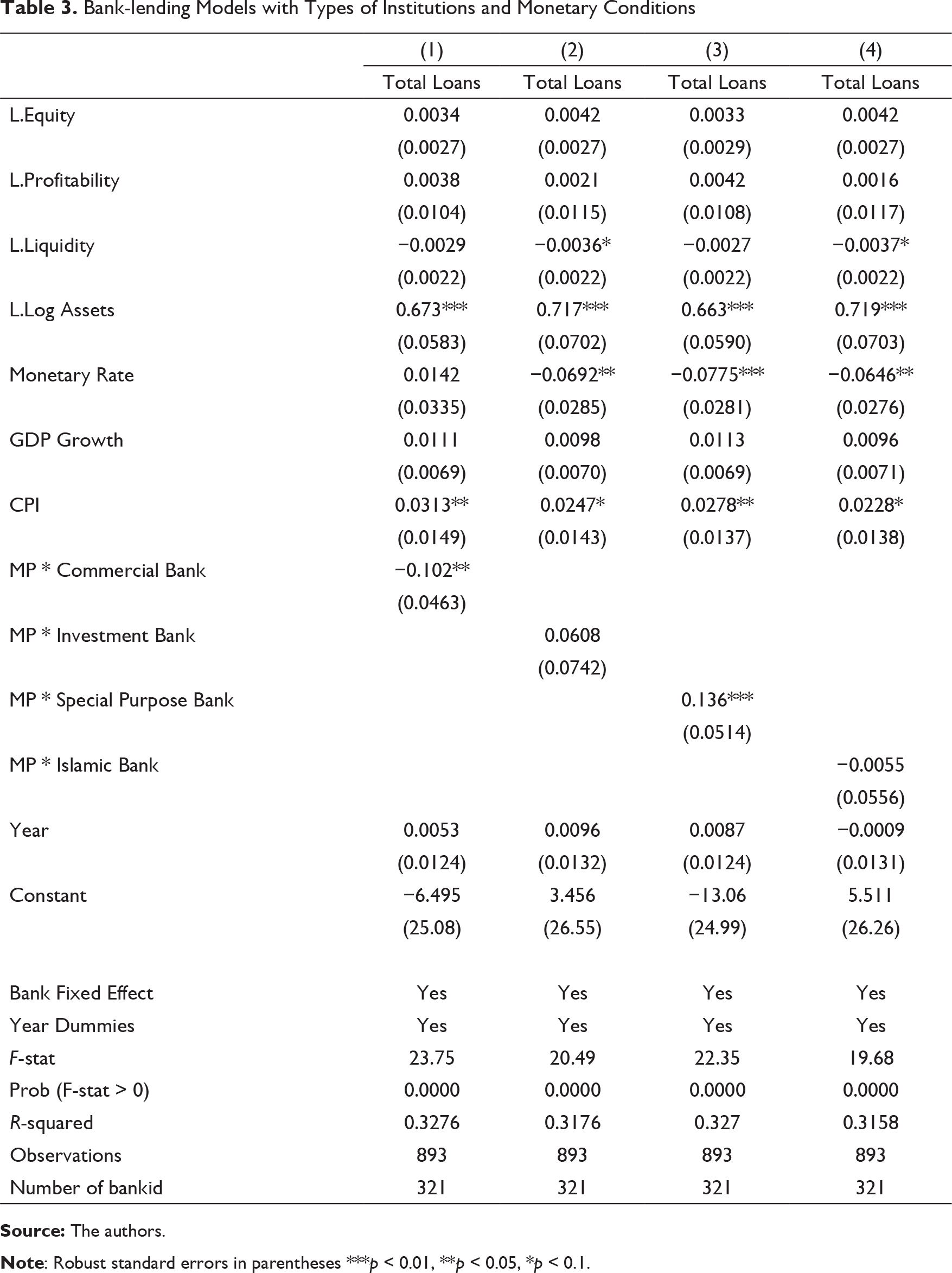

Further analysis on the effectiveness of the bank-lending channel is performed by distinguishing the type of financial institutions. The results in Table 3 confirm that the effectiveness of the bank-lending channel in ASEAN countries varies according to the type of financial institutions. We find that the coefficient for monetary policy rate is −0.102 for commercial banks, suggesting that a one-unit increase in the monetary policy rate leads to a reduction in commercial bank lending by 10.2. However, the results in Table 2 show that one-unit increase in the monetary policy rate reduces all banks’ lending by only 6.48 per cent. This suggests that commercial banks in the ASEAN countries are more vulnerable to changes in monetary policy compared to other banks. Similar findings have been observed by Ananchotikul and Dulani (2015) in the case of nine Asian countries which include ASEAN-5 countries, Hong Kong, India, Korea and Taiwan. Greater vulnerability of commercial banks to monetary policy changes may be due to their higher reliance on lending activities. Given that commercial banks adhere to strict capital and regulatory requirements, an increase in interest rate may result in capital loss on securities, thereby reducing banks’ capital holdings. Hence, banks may reduce their lending activities in the event that capital reserves drop below the statutory requirement level (Zulkhibri, 2013). In addition, greater vulnerability of commercial banks to monetary policy changes may also be due to greater competitiveness that is present within this banking segment in ASEAN (Hamid, 2017).

Bank-lending Models with Types of Institutions and Monetary Conditions

Bank-lending Models with Governance Structure

In addition, we find that investment banks are not sensitive to changes in monetary policy. The ability of investment banks to protect their credit may be due to the fact that these banks are mainly involved in fee-based income, and, as a result, they are less sensitive to changes in monetary policy. As far as the Islamic banks are concerned, we find that changes in the monetary policy have no significant impact on the level of financing extended by the Islamic banks. This suggests that the transmission of monetary policy through the Islamic segment of the banking sector in ASEAN is weak. The ability of Islamic banks to absorb the monetary policy shocks is due to the structural advantages that these institutions have compared to their conventional counterparts (Zulkhibri & Sukmana, 2017).

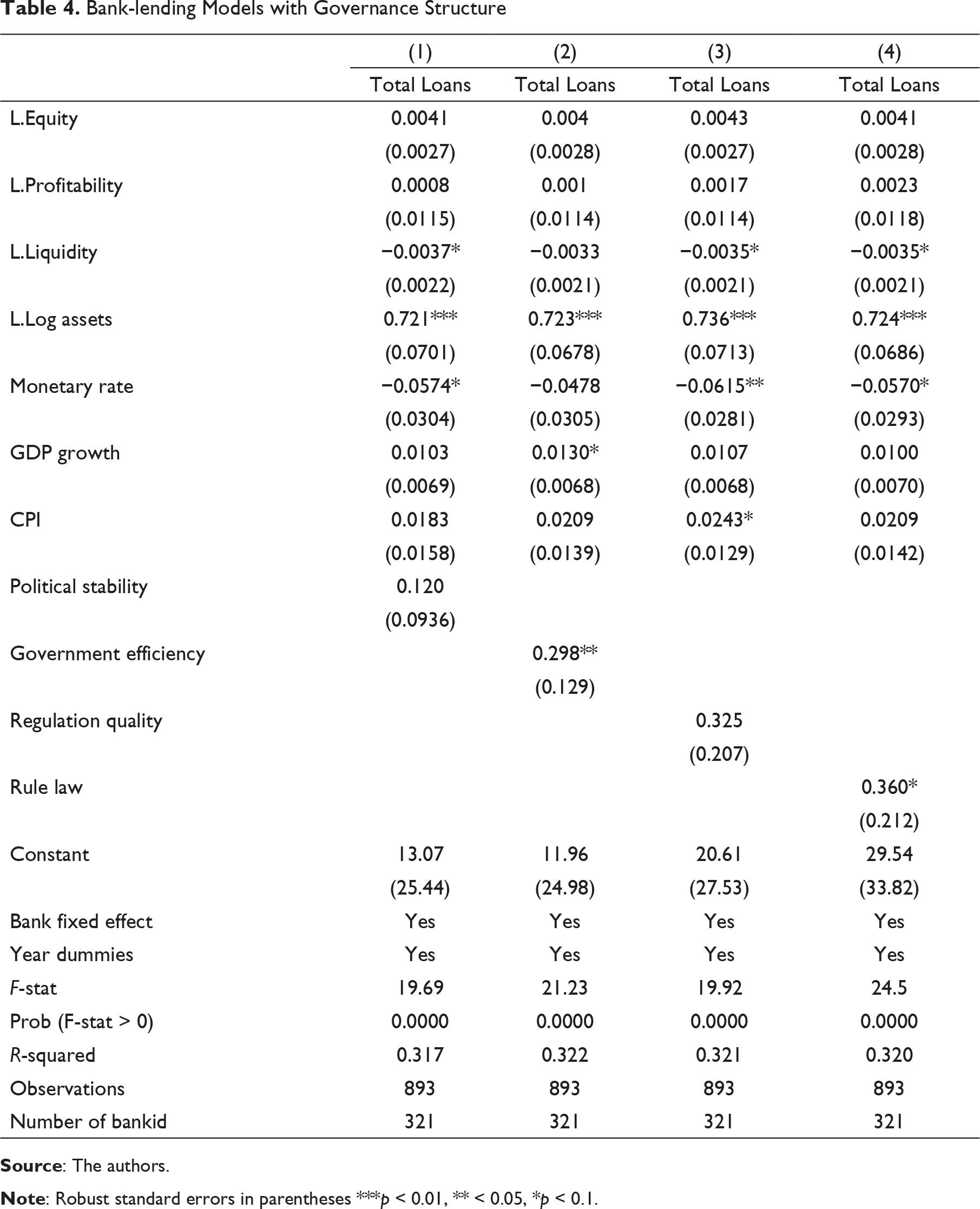

Further analysis on the effectiveness of the bank-lending channel in the ASEAN countries is performed by taking the governance structure into account. Studies by Demirgüç-Kunt; Laeven and Levine (2004); and Khan et al. (2016) showed that bank-lending behaviour can be influenced by the governance structure of a country. Four indicators used in the analysis are political stability, government effectiveness, regulatory quality and rule of law. These indicators are derived from the studies of Kaufmann, Kraay, and Mastruzzi (2017). Political stability index considers the likelihood that the government will face political instability, politically motivated violence and terrorism. Government effectiveness represents the quality of public and civic services, the absence of political pressures, the quality of policy formulation and implementation and the credibility of the government’s commitment to such policies. Regulation quality accounts for the government’s ability to design and implement sound policies and regulations that allow and promote private sector development. Rule of law considers the extent to which agents have confidence in and abide by the rules of society, particularly that which relates to the quality of contract enforcement, property rights, the police, the courts, as well as the likelihood of crime and violence. Higher values of the indicators relate to better governance, and as a result, they are expected to have a positive effect on banks’ lending behaviour.

The results reported in Table 4 show that the coefficients of monetary policy rate are negative and significant, ranging from −0.057 to −0.0615. This confirms that bank-lending channel is still effective in the ASEAN banking sector once when we consider the countries’ institutional characteristics and regulatory frameworks. We find that the coefficients on all four governance indices are positive. However, only government effectiveness and rule of law have a significant effect on banks’ lending activities. This implies that effective government and better rule of law encourage banks’ lending activities as observed by Khan et al. (2016).

Conclusion

The ASEAN banking sector has undergone many changes since the Asian financial crisis. Efforts have been taken to strengthen the equity market and develop the bond market in order to provide alternative source of funding to investors. Nevertheless, bank loans remain the primary financing source for many businesses and households. Given the importance of banking sector in the ASEAN economies, this article tries to provide evidence on the existence of a bank-lending channel in the ASEAN economy during the period after the global financial crisis. In doing so, we used an unbalanced bank level panel data to analyse the responses of bank loans to monetary policy changes in the ASEAN banking sector from 2009 to 2015.

First, we tested whether the effect of monetary policy changes on bank loans varies based on the types of loans. We find that a bank-lending channel is effective in the ASEAN economies. Nevertheless, additional analyses using different types of bank loans show that only consumer loans and commercial loans are vulnerable to changes in monetary policy, but mortgage and corporate loans are not. In addition, we also find that commercial banks are vulnerable to monetary policy shocks, but both investment banks and Islamic banks are not. On the other hand, we find that special purpose banks are able to supply more loans during the period of monetary policy tightening. Lastly, we find that the bank-lending channel is still effective in the ASEAN banking sector once we control for the differences in the governance structure of the countries.

Overall, we find that the effectiveness of a bank-lending channel in the ASEAN banking sector varies depending on the type of loan portfolio and banks. The findings of this study provide greater understanding about the effectiveness of a bank-lending channel in the context of emerging markets. This is an area that has not been well researched in the existing literature. The differences in the sensitivity of loans can be either due to supply or due to demand side effect. The latter implies that the demand elasticity for different types of loans may be different, while the former implies bank’s willingness to lend may vary according to the risk profile of the different types of loans. On the other hand, the differences in the sensitivity of different types of banks to monetary policy changes can be due to differences in the market structure, source of income and regulatory framework.

Policy Implications

The findings of this study present considerable policy relevance. First, we find that sectors of the economy are affected differently during monetary policy changes. This implies that policymakers need to be very careful when using monetary policy to achieve specific objectives. Given that households and small business are more vulnerable to monetary policy changes, policymakers need to ensure that they recalibrate interest rate decisions wisely so that they do not dampen consumers’ and small firms’ confidence. On the other hand, lack of vulnerability of mortgages and corporate loans to monetary policy changes suggests that policymakers need to use other supporting policy instruments to influence lending to these segments. Second, we find that certain types of banks are more sensitive to monetary policy changes, while others are not. Hence, policymakers need to internalize the effects of banking structure on monetary policy effectiveness. Given that government-owned banks are able to raise credit during monetary policy shock, policymakers may use public bank lending as an additional tool to stabilize credit during periods of economic slowdown.

Overall, our study shows that the effectiveness of monetary policy tool differs based on the heterogeneity that is present in the banking sector. Therefore, it is very crucial for policymakers to be aware of this when they formulate changes in monetary policy in order to achieve a specific objective. Going forward, policymakers also need to be aware of the various developments that are taking place in other sectors of the financial market that could possibly influence the effectiveness of monetary policy tools in the ASEAN economies.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

This work was supported by USM short-term grant No. 304/PJJAUH/6315001.