Abstract

Bid-ask spread, along with profit, also encompass the impact of asymmetric information cost and order processing cost. Asymmetric information influences stock prices with varying degree of investors’ perception. Estimation of asymmetric information cost and its determinants have been explored significantly under low-frequency trading. The literature hardly attempts to study asymmetric information cost under high-frequency trading (HFT). Asymmetric information cost significantly influences bid-ask spread, and hence the nature of its impact under different market conditions needs to be analyzed under HFT. The study attempts to estimate asymmetric information cost in HFT and analyze its determinants under different industry sectors and market conditions. The study followed Affleck-Graves et al. (1994, The Journal of Finance, 49(4), 1471–1488) model to estimate the asymmetric information cost using 5 minutes interval data for a period of 82 trading days. Information gets reflected in equity through the movement in price, variation in trading volume, and return volatility. The study has found share price, traded volume, return volatility and trading frequency as the major determinants of asymmetric information cost in different market conditions. The findings of the study have significant implications for market microstructure for trading, lowering information asymmetry in market and enhancing market quality.

Introduction

In recent years, upgradation of technology for large-scale data processing brings the concepts of algorithmic and high-frequency trading (HFT) in an electronic trading system. Researchers (Rojcek & Ziegler, 2016 ; Brogaard, 2010) argued that the introduction of HFT improves market quality, reduces spreads, increases market depth and enhances price discovery. In HFT, traders’ decisions to buy or sell depend on different transaction costs such as processing fees, exchange fees and liquidity costs. Bid-ask spread, price impact and opportunity cost are influenced by factors like traders’ expectation, market movements and information asymmetry in market among traders.

HFT has thrown light on an important aspect of financial market price movement, which are largely due to microstructure forces. Where some traders in market can avail privileged information about the values of assets, others may be trading merely on the basis of public news or information. The risk faced by an uninformed trader from an informed counterparty in the market can be an important determinant of asset prices (Easley, Hvidkjaer, & O’Hara, 2002). Hence, measuring asymmetric information cost can play an important role in improving the market quality as well as enhancing the liquidity in market, which will in turn allow a trader to correctly price a security (Easley & O’Hara, 1987). Market microstructure literatures define bid-ask spread as a price need to be paid for immediacy. In an order-driven market, traders execute trades by submitting market or limit orders. Bid price is the price that an investor is willing to pay for an order and ask price is the price that an investor is willing to receive from an order. The difference between the bid and the ask prices is known as the bid-ask spread, which is the compensation for immediacy. Spreads are very pertinent to HFT traders, as higher spread may generate higher profit. But spread also implies greater risk sometimes when traders are unable to exit their positions at their desired price. The theoretical literatures isolated and identified three main factors that determine spread: inventory carrying costs (Amihud & Mendelson, 1980; Ho & Stoll, 1983), adverse selection costs (Easley & O’Hara, 1992; Glosten & Milgrom, 1985) and order processing costs (Brock & Kleidon, 1992). Adverse selection cost is also known as asymmetric information cost. Jha, Murthy, Nagarajan, and Seth (1999) suggested order processing cost incurred from orders of different sizes and frequencies for the Indian market. Asymmetric information cost increases in presence of traders with rich information about the value of a security. But inventory holding cost is present whenever there is uncertainty for future payoffs from a security in an equally information distributed market. Each of the cost components depends on various factors, which call for analysis of the determinants.

Determinants of cost components have been extensively studied under low-frequency trading. Literature finds that asymmetric information cost strongly depends on the activity of informed and uninformed traders in the market. Easley, Kiefer, O’Hara, and Paperman (1996) argued that higher the trading volume, adverse selection cost reduces. Ahn, Cai, Hamao, and Ho (2002) found that adverse selection cost increases with more trading volume. Later, Riedl and Serafeim (2011) empirically found that higher information risk could lead to higher levels of information asymmetry, leading to increased bid-ask spread. With the above discussion, the study reviewed literature on asymmetric information cost and empirically analyzed various determinants, which explicitly describe it. The rest of this article is organized as follows. The second section presents a literature review on asymmetric information cost of bid-ask spread and its determinants. The third section briefly describes literatures gaps and research objectives of the study. The fourth section outlines the methodology for estimating asymmetric information cost of bid-ask spread using the models proposed by Affleck-Graves, Hegde, and Miller (1994) and George, Kaul, and Nimalendran (1991) based on serial covariance approach (Roll, 1984). The fifth section describes the empirical design for the computation of asymmetric information cost under high-frequency trading data with consideration of sectors. The study then describes the dataset used and stock selections in the sixth section. The seventh section presents the results of our regression models that relate estimated asymmetric information cost to firm-level characteristics. The eighth section concludes with a review of the rationale why the study considers this important in the context of Indian stock markets.

Literature Review

In an order-driven market, bid-ask spread not only represents immediacy of trading but also encompasses profit and transaction costs. Immediacy of trading represents the level of market liquidity whose absence impact the buyer and seller to settle their position. The bid-ask spread encompasses profit and transaction costs. Spread indirectly measures the liquidity. An investor may face difficulty in buying or selling a security in absence of significant number of trades. Less liquid stocks, like small-cap stocks, generally have a high spread compared to large-cap (index) stocks.

Bessembinder and Venkataraman (2010) computed quoted spread as difference between ask price and bid price. Empirical research (Stoll, 1989) suggests spread has three defined cost components, viz. order processing cost, inventory holding cost and asymmetric information cost. Stoll (1989) decomposed the bid-ask spread into three cost components under following assumptions:

Market is informationally efficient; expected price changes are independent of information. Bid-ask spread are constant over time; all transactions occur at best bid or best ask. Proportions of bid-ask spread components are same for all securities.

Asymmetric information cost, suggested by Bagehot (1971), computed by Copeland and Galai (1983), Easley and O’Hara (1987), and Glosten and Milgrom (1985) for liquidity suppliers, when they trade with informed traders. Copeland and Galai (1983) put forward a model of bid-ask spread with adverse information cost, where information carrying cost is measured in terms of various levels of precision. Limit order traders in the order-driven market face the risk of trading with a better-informed trader (Singh & Pandey, 2013). Buying undervalued stock or selling overvalued stock by an informed trader will create the risk for liquidity providers. Thus, liquidity providers demand some compensation for expected asymmetric information in the bid-ask spread. Glosten and Milgrom (1985) showed that asymmetric information leads to a positive bid-ask spread even in the absence of order processing costs and inventory holding costs. Empirical research works (Bollen, Smith, & Whaley, 2004; Brogaard, Hendershott, & Riordan, 2019) confirmed the importance of adverse selection cost as a determinant of spread. Number of shares held by a trader has been used as proxy for adverse selection by Branch and Freed (1977). Easley et al. (1996) argued that, with higher trading volume, the activity of uninformed traders relative to informed traders will be high, which in turn lowers the adverse selection cost. Stoll (1978) suggested that with higher rate of turnover, the adverse selection cost increases. Glosten (1994) shows that asymmetric information cost generates positive bid-ask spreads in an order-driven trading environment. Ahn et al. (2002) empirically justified that adverse selection cost component increases with the trade size. For computation of asymmetric information cost, Roll (1984) derived a simple measure of the spread based on the negative autocovariance of security returns. This measure has been extensively used for computation of asymmetric information cost by various researchers (Affleck-Graves et al., 1994; George et al., 1991). Glosten and Harris (1988) decomposed bid-ask spread into a transitory component and an adverse-selection component. The model was estimated using transaction price, in a cross-sectional regression, where spread is a function of trade size. The results suggest that the adverse-selection component is, at least, one of the determinants of the total spread. Bid-ask spread decomposition model of Huang and Stoll (1997) provides a detailed picture of setting prices and bid-ask spread in market.

A scan of the literature reveals use of diverse set of variables as determinants of asymmetric information cost. Minardi et al. (2006) found negative relationship between spread and stock price. Huang (2004) discussed about determinants of information asymmetry cost in comparative analysis of Singapore and Taiwan stock exchanges. The author confirmed positive relation of price level and return volatility with asymmetric information cost component of bid-ask spread. Kuo (2017) provided an interesting insight in the impact of change in tick size over different cost components of bid-ask spread in emerging market of Taiwan. The study performed analysis on models proposed by George et al. (1991), Huang and Stoll (1997) and Madhavan, Richardson, and Roomans (1997). Following Huang and Stoll (1997), Luo (2017) found that order processing cost is significantly higher compared to asymmetric information cost in London Stock Exchange (LSE) and New York Stock Exchange (NYSE) markets. The study also found that higher proportion of the bid-ask spread is directly related to the information inefficiency in LSE rather than in NYSE, which is consistent with findings from Hasbrouck, Sofianos, and Sosebee (1993).

Literature Gaps and Research Objectives

The above discussed literature presents an in-depth review of asymmetric information cost of bid-ask spread and its determinants. Under high-frequency trading data, the asymmetric information cost needs to be re-examined as it is not priced in all markets. Literature suggests volatility, number of trades, share price and trading volume as primary determinants of asymmetric information cost. Majority of the studies are performed on developed markets. However, in the Indian market, Singh and Pandey (2013) found higher proportion of adverse selection cost in bid-ask spread, but the authors could not distinguish the state of market, where adverse selection is high. Singh and Pandey (2013) also considered a few stocks and limited time period in their study.

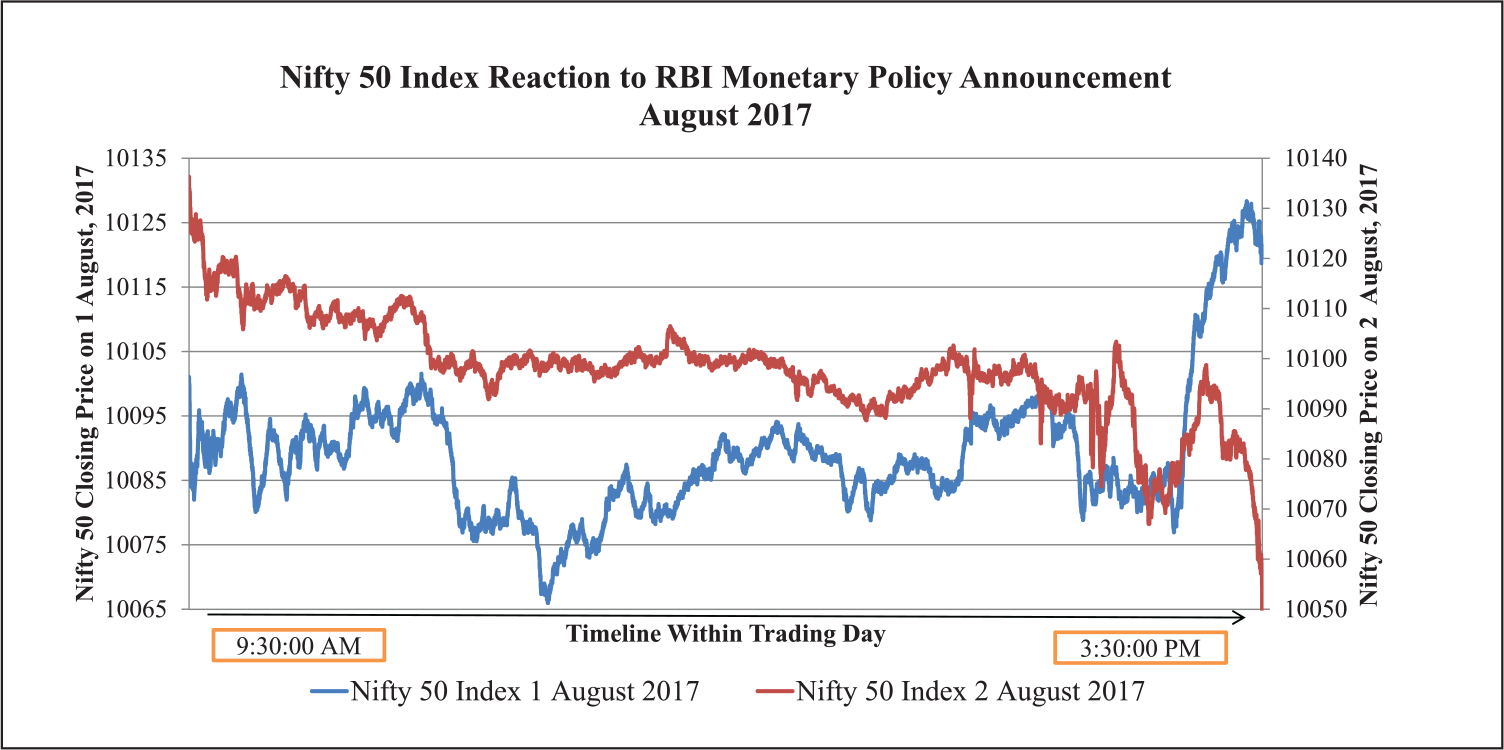

Study period of the article is selected with consideration of presence of public and private information in market. To understand this, Figure 1 is showing movement of Nifty 50 index before and after arrival of new information in market.

Figure 1 depicts the Nifty 50 index movement on the day before Reserve Bank of India (RBI) Third Bi-monthly Monetary Policy Statement for 2017–2018. The announcement was made on 2 August 2017. The study tries to accumulate information asymmetry (in terms of asymmetric information cost) in market within traders. The plotting of index on 1 August 2017 shows up rise towards the end of the day due to information asymmetry among traders before the RBI announcement. But on 2 August 2017, price goes down from the beginning. This clearly shows the asymmetry in information, which in turn affects the asymmetric information cost among various group of traders in the market and its impact on market behaviour.

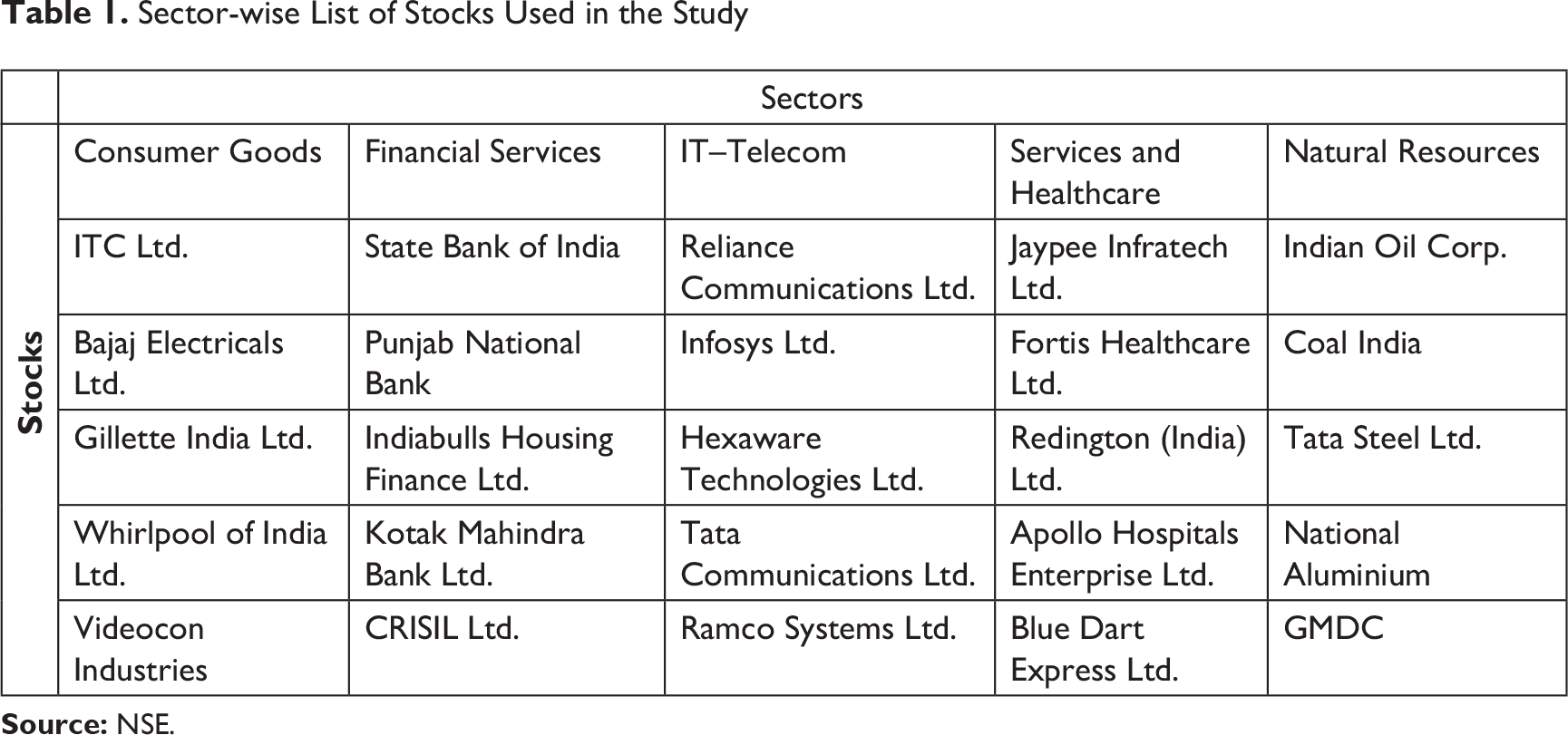

The article considers stocks from five dominating sectors of the Nifty (i.e., consumer goods, financial services, IT and telecom services, services and healthcare, and natural resources) belonging to different industry groups to analyze impact of sector specific determinants on asymmetric information cost. The article extends its analysis to different market conditions to articulate the changing nature of determinants of asymmetric information cost.

Methodology Review

Computation of Asymmetric Information Cost Component

Bid-ask spread can be measured in terms of quoted spread as follows (Bessembinder & Venkataraman, 2010):

where

The methodological discussions of the article are confined to segregation of bid-ask spread into different cost components and analyzing various determinants of asymmetric information cost. The methodological review outlined the pioneering literatures on asymmetric information cost provided by Glosten and Harris (1988) and George et al. (1991).

Affleck-Graves et al. (1994) proposed the model based on earlier study by George et al. (1991) model

where

where

Now,

where

Following measures from studies by Glosten (1987) and Roll (1984), George et al. (1991) computed continuous compound transaction return of a security i at t from equations 5 and 6:

where

The bid price subsequent to transaction t is interpreted as

Now the difference between

The serial covariance of

Implicit measure of spread is

Serial covariance of

Determinants of Asymmetric Information Cost Component

Determinants of cost components are computed based on study by Giouvris & Philippatos (2008). The study examines the effects of Quote Return, number of trades and trading volume on asymmetric information cost component (AI) and order processing cost component (OP) based on all available trades. The study proposes following panel regression models:

where

Empirical Design

Over the years, multiple models are proposed to estimate asymmetric information cost of bid-ask spread. Most popular among them are models proposed by Stoll (1989), George et al. (1991) based on work by Roll (1984) and Stoll (1989), Glosten and Milgrom (1985), Glosten and Harris (1988), Hagströmer et al. (2016), De Jong et al. (1996) and Madhavan et al. (1997). Later, many researchers such as Kim and Ogden (1996), Huang (2000), Menyah and Paudyal (2000) and Singh and Pandey (2013) followed empirical models to establish their works. Roll (1984) proposed the model to estimate bid-ask spread from transaction prices, which is indeed an implicit measure of bid-ask spread. Roll’s measure depends on multiple assumptions like symmetry of information in the market, order executions at best quotes, probability of execution is same at both buyer and seller side, and presence of only order processing cost in bid-ask spread. This study formulates empirical design to compute asymmetric information cost of bid-ask spread under high-frequency trading.

Computation of Quoted Spread

As per Stoll (1989) and Bessembinder and Venkataraman (2010), quoted spread is computed using the following equation:

where

Implicit Measure of Bid-Ask Spread

Implicit measure of percentage spread is computed based on study by Roll (1984). Roll’s measure of spread follows directly from equation, which depends on serial covariance of changes in returns.

where

Computation of Asymmetric Information Cost

Computation of asymmetric information cost is estimated for each stock on trading day basis within the timeline of 9:30 AM to 3:30 PM. Each trading day is divided into 5-min interval counted to 72 intervals. For each interval, asymmetric information cost is computed using extended models based on studies by Affleck-Graves et al. (1994) and Roll (1984). Data for the study have the properties of big data related to volume, variety, velocity, veracity, variability, visualization and value. This study considers flow of information in the market throughout the whole trading day. Thus, for each trading day, computation of asymmetric information cost will be done stock-wise.

where i is the stock, T is the trading day, t is the time interval for each computation, which has length of 5 min, r is the number of intervals in each trading day to compute asymmetric information cost, LOB is the asymmetric information cost measured in Tth trading day for stock i, E is the interval specific measurement and C is the measurement within each interval.

Within

After timestamp changes, matching happens within Bid and Trade (transaction) points based on

Within each

RDit is the difference between return calculated from transaction price of stock

Within each

where

Determinants of cost components are computed based on study by Giouvris (2008). The study examines the effects of return volatility, share price, number of trades and trading volume on asymmetric information cost component (AI) based on all available trades. The study proposes following panel regression models:

where AI is the asymmetric information cost,

The study has used five different models for five different sectors. Sector specific models are mentioned here:

In the above equation (21),

Based on the above discussion, the study proposed following hypotheses to be validated. As different sectors possess different level of information, asymmetric information cost will have different behaviour across sectors. Study of impact of determinants for various sectors on asymmetric information cost is necessary to understand behaviour of explanatory variables and accordingly formulate strategy.

Up and down markets have different properties based on the dominance of buyer and sellers, respectively. Capturing the impact of factors impacting asymmetric information cost under these two completely different market environments is also one of the objectives of the study.

The study assumes that asymmetric information has no impact on price discovery under high-frequency trading. A bidirectional causality test can put some light on the relation between asymmetric information cost and share price.

Data and Period of Study

Tick by tick data for the selected stocks listed on NSE CNX500 covering the period of April to July 2017 are collected from Bloomberg servers and processed under large-scale databases. Data cover major stocks from dominating sectors, such as consumer goods, financial services, IT and telecom services, services and healthcare and natural resources. A sample of total 25 stocks was considered for the study consisting five unique stocks from each sector of the market. As each sector has a unique information absorption rate, the study tried to analyze asymmetric information in different sectors and compare them with each other. The period also consists of both bullish and bearish market conditions. Continuous trend in the upward and downward movements have been considered as bullish and bearish periods, respectively. Both trade and quote data including algorithmic and non-algorithmic trading data, collected from Bloomberg servers, have more than 49 million ticks in total. After the cleaning process, 45 million data points are available for processing. Besides using pooled dataset, the study also includes datasets under different market conditions for analysis. Sector-wise analysis has been carried out to capture the behaviour and information absorption capacity of different sectors.

Table 1 depicts sector-wise detail information on stocks. Stocks were selected based on different categories of trading volume and share price, such that the bucket covers various categories of stocks, trading volume and market capitalization.

Sector-wise List of Stocks Used in the Study

Results and Discussion

The study used Affleck-Graves et al. (1994) and Roll (1984) models to compute asymmetric information cost component of bid-ask spread. Empirical design of Giouvris & Philippatos (2008) was implemented in the study to analyze the determinants of asymmetric information cost of bid-ask spread. Asymmetric information cost components have been considered as dependent variable and it is regressed against return volatility, share price, traded volume and number of trades as the independent variables. Correlations between covariates do not face issue of multicollinearity. A correlation plot is shown in Figure 2.

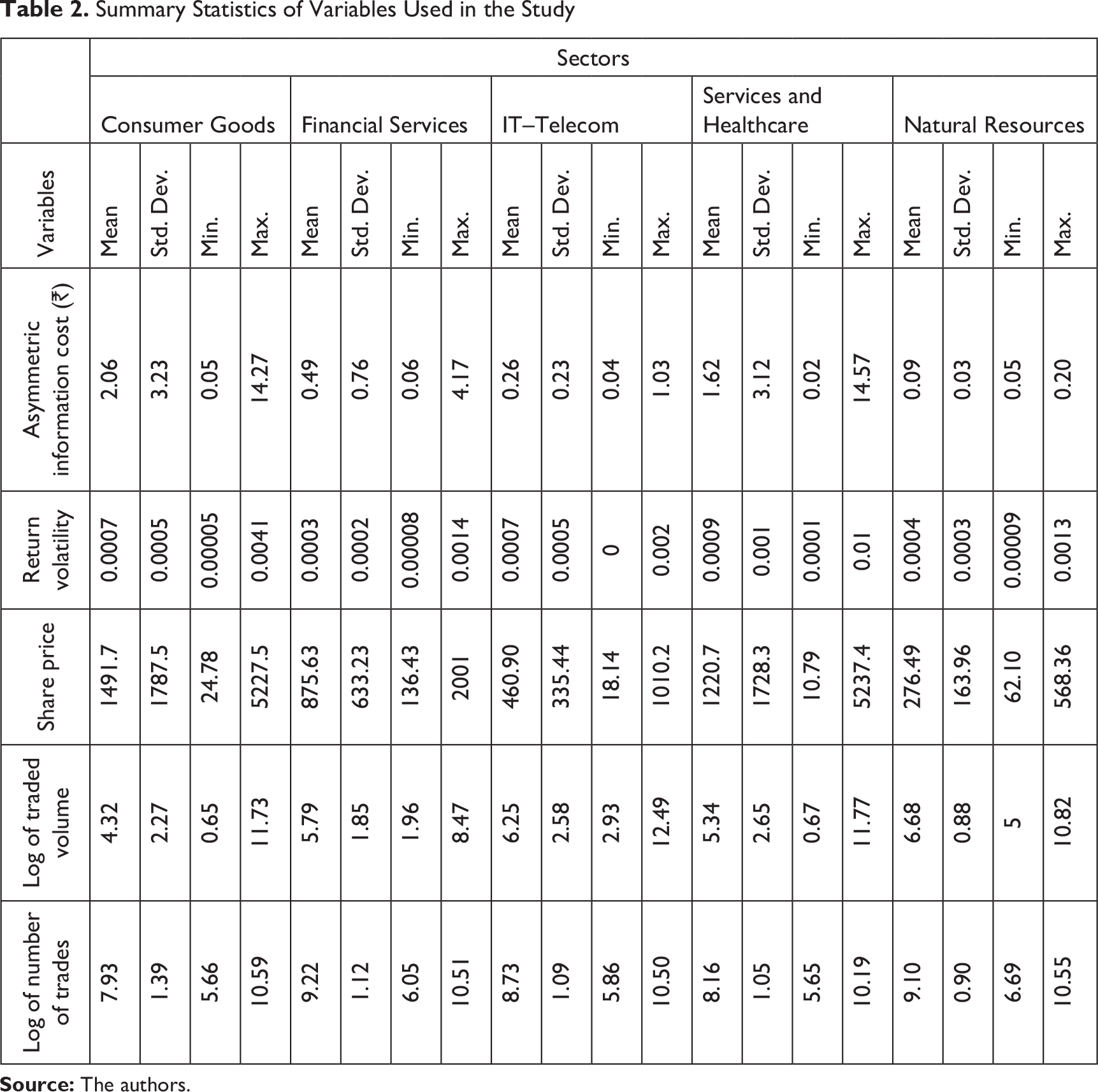

Asymmetric information cost is estimated, stock-wise, as per equation (17), which is reported in Table 2. Sector-wise average of asymmetric information cost indicates consumer goods having the highest asymmetric information cost and natural resources having the lowest average. Summary statistics of various determinants of asymmetric information cost are also provided in Table 2.

Analysis of Determinants of Asymmetric Information Cost

Analysis of determinants of asymmetric information cost was carried out sector-wise to capture the impact of sector specific information and behaviour. The study conducted analysis for each sector, namely, consumer goods, financial services, IT–telecom, services and healthcare, natural resources, where each sector has five identified stocks having a larger market share in that group. Literatures have identified that traded volume, return volatility, share price and a number of trades as the primary explanatory variables for the analysis of asymmetric information cost (Ahn et al., 2002; Copeland & Galai, 1983; George et al., 1991; Huang, 2004; Kim & Ogden, 1996). However, literatures have not provided conclusive evidence for the expected relationship of asymmetric information cost with each of the above-mentioned explanatory variables.

Summary Statistics of Variables Used in the Study

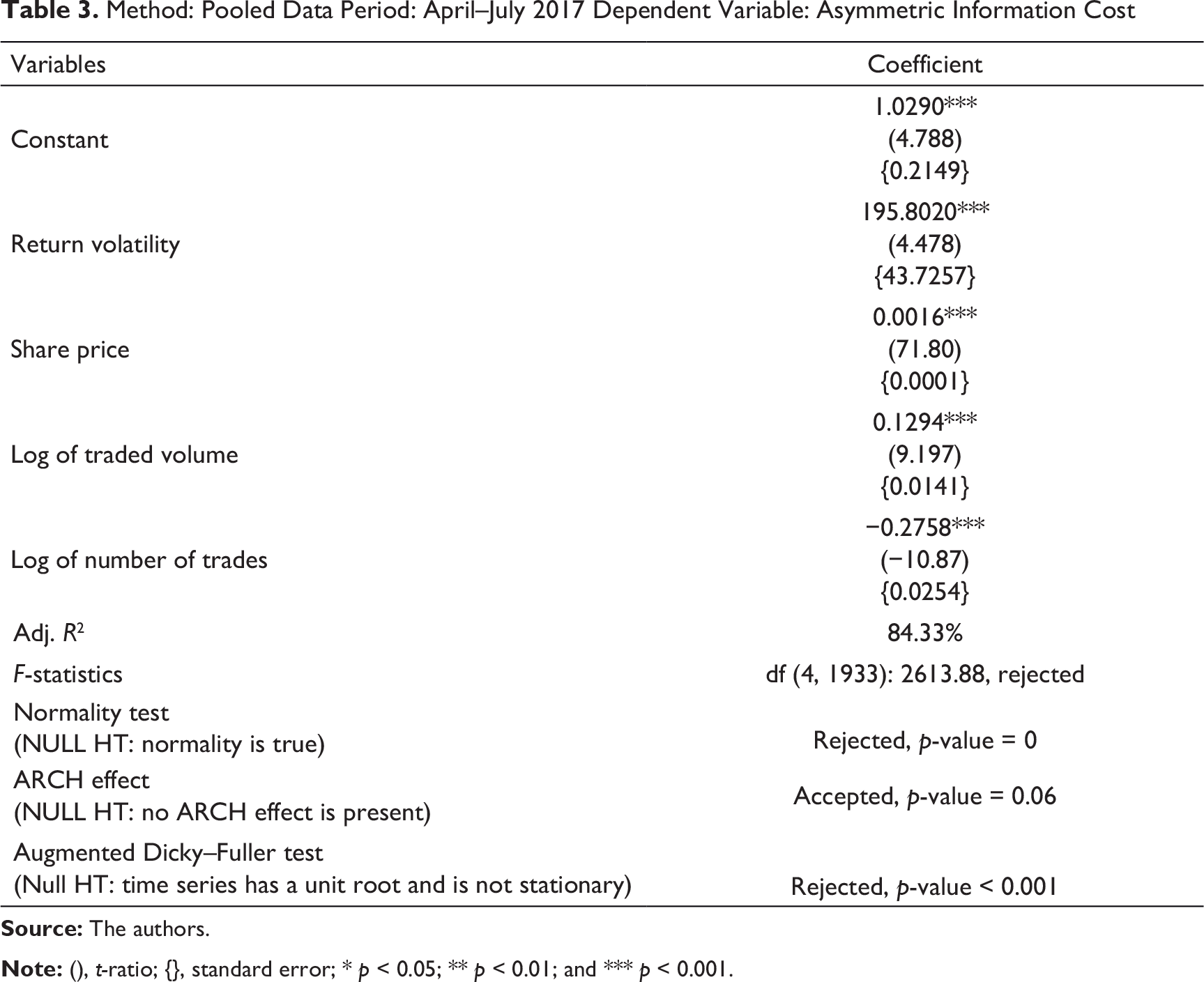

Method: Pooled Data Period: April–July 2017 Dependent Variable: Asymmetric Information Cost

Table 3 represents a pooled data analysis of asymmetric information cost and its determinants. Except log of number of trades, all other variables are found to be in a positive direct relation with asymmetric information cost. Adjusted R-Square is also very high.

All explanatory variables are statistically significant. Except number of trades, rest of the variables have a positive relation with asymmetric information cost. From the analysis, it can be inferred that with a greater number of trades, information asymmetry declines. At the same time, with more return volatility, asymmetric information cost rises, which may be due to the variability of stock prices with respect to variety of information. Volume shows a positive relation with asymmetric information cost, which is supported by the market microstructure theory that higher trading volume contains superior information (Nolte, Salmon, & Adcock, 2016; Wang, 1994).

Asymmetric Information Cost and Share Price—A Causal Analysis

The study also investigates causal relationship between asymmetric information cost and share price to understand the directional relation between them.

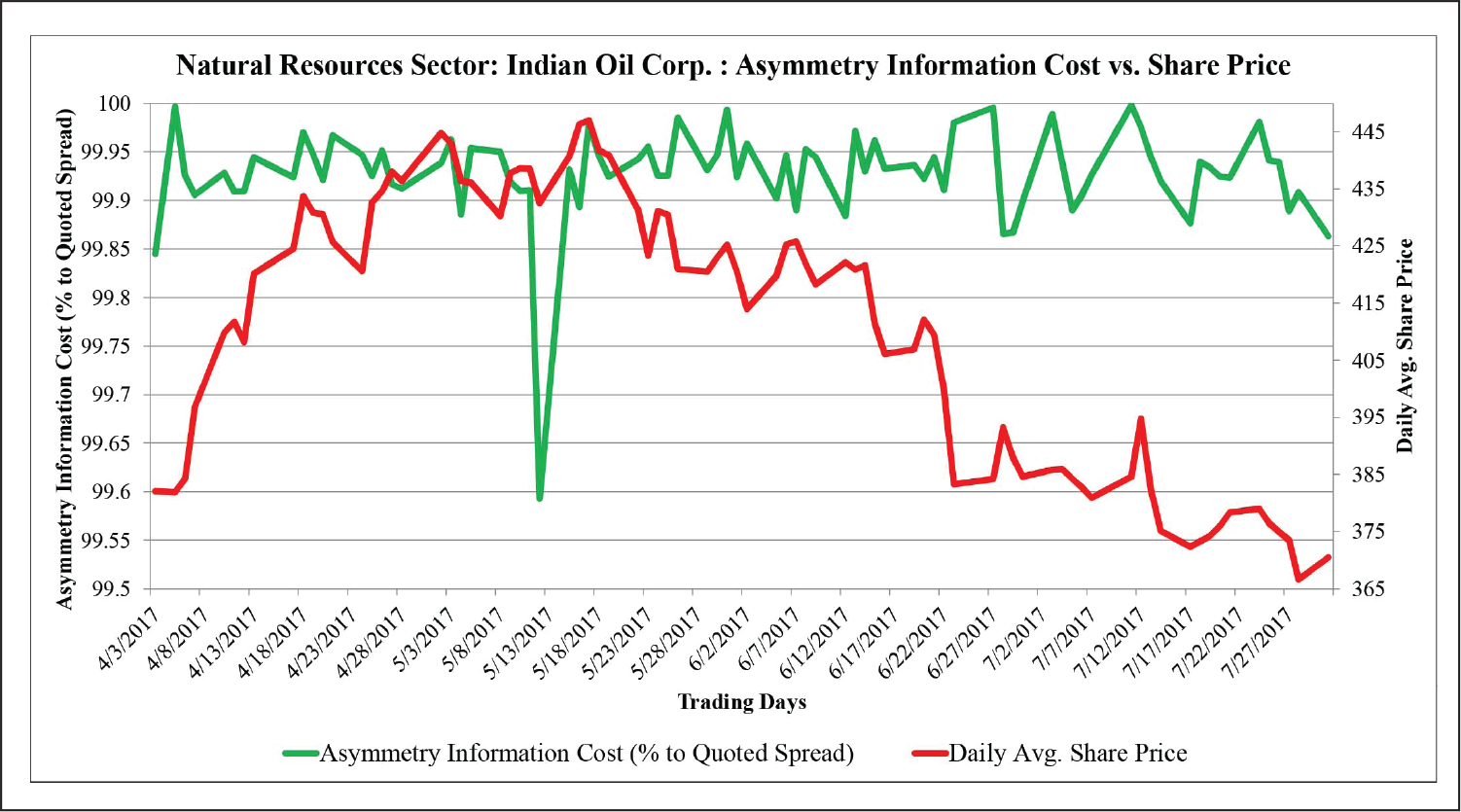

Figure 3 depicts the asymmetric information cost and share price of the stock of ITC Ltd., which belongs to consumer goods sector. Overall, share price and asymmetric information cost are in a direct relationship.

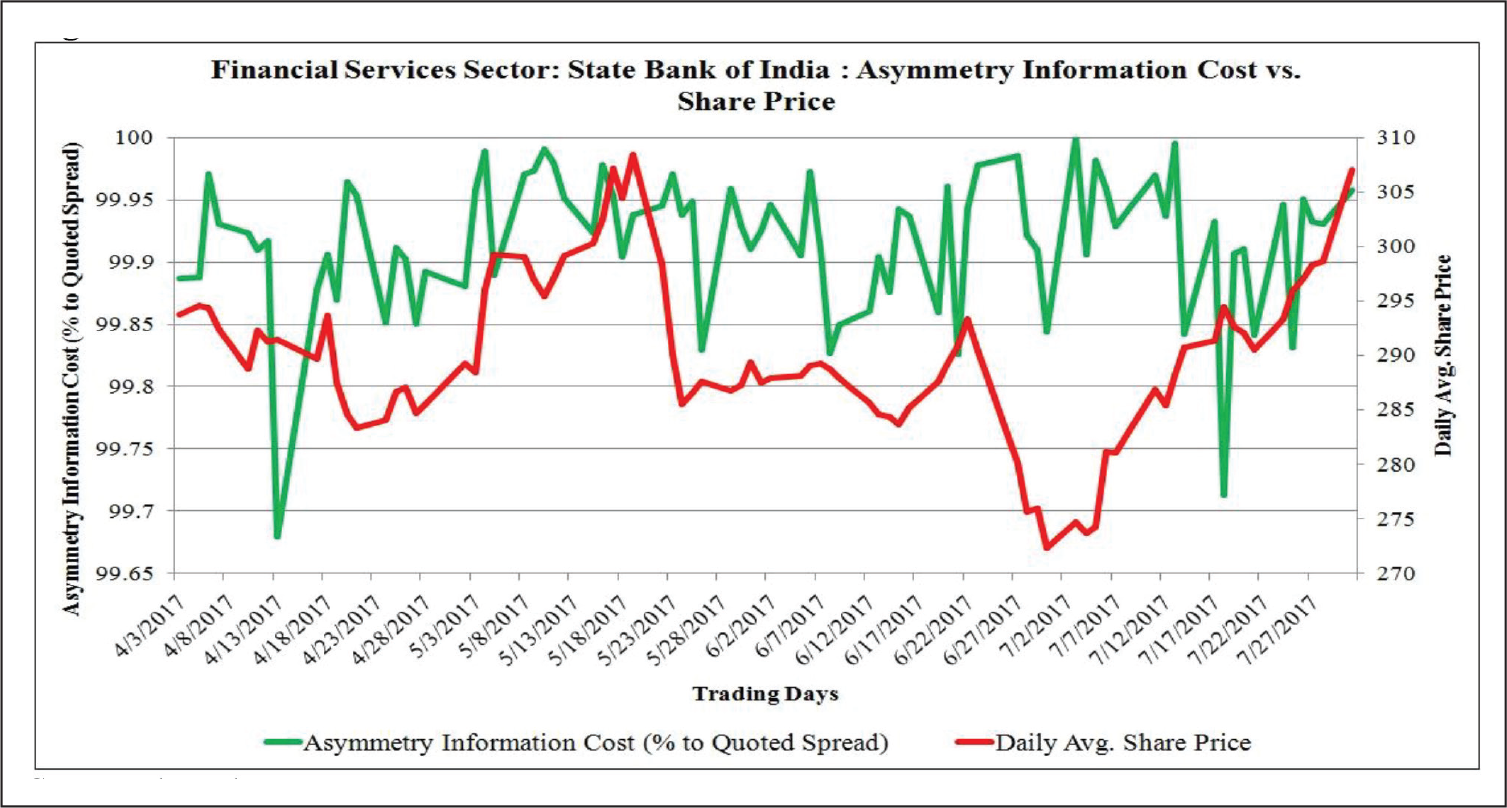

Similarly, Figure 4 represents the same relationship for State Bank of India (financial services sector) stock, where share price and asymmetric information cost both move in the same direction.

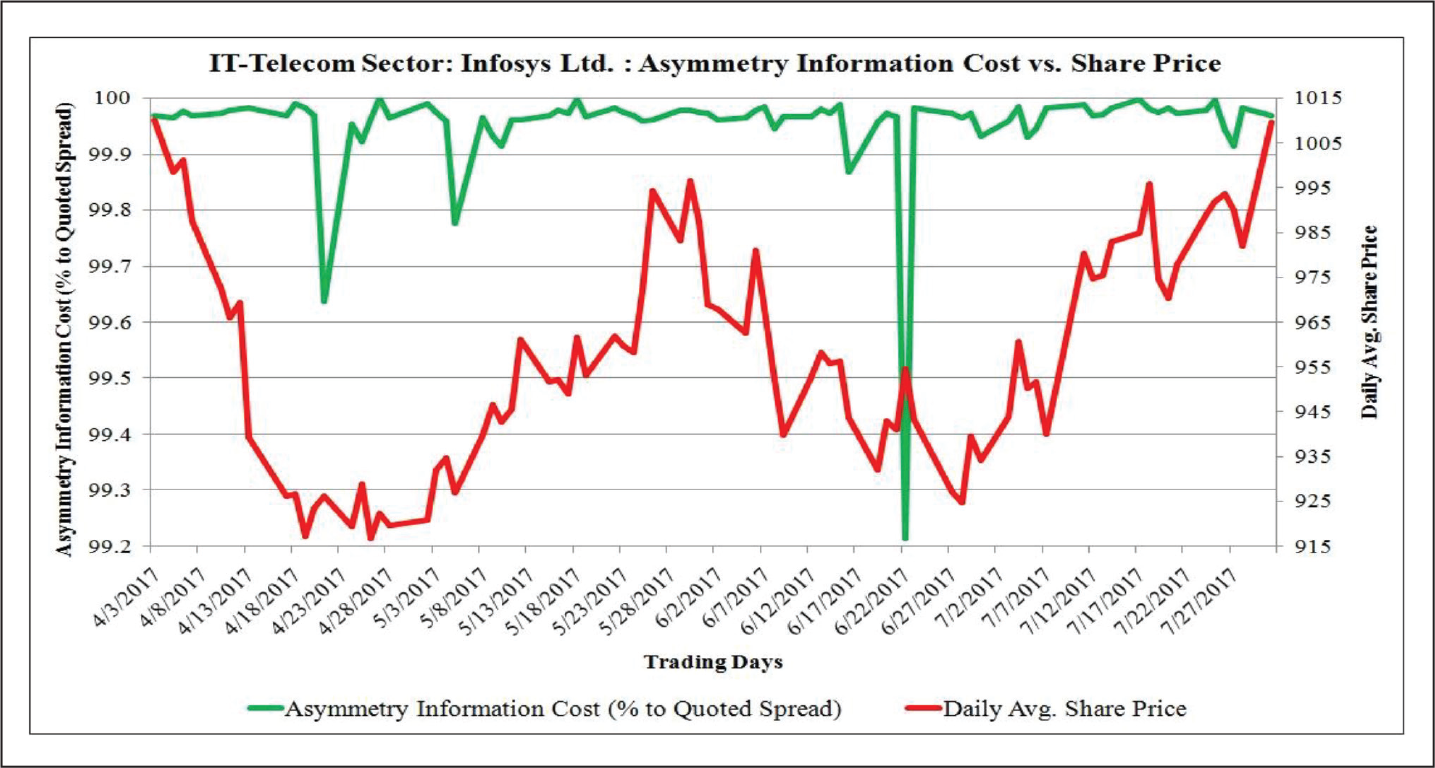

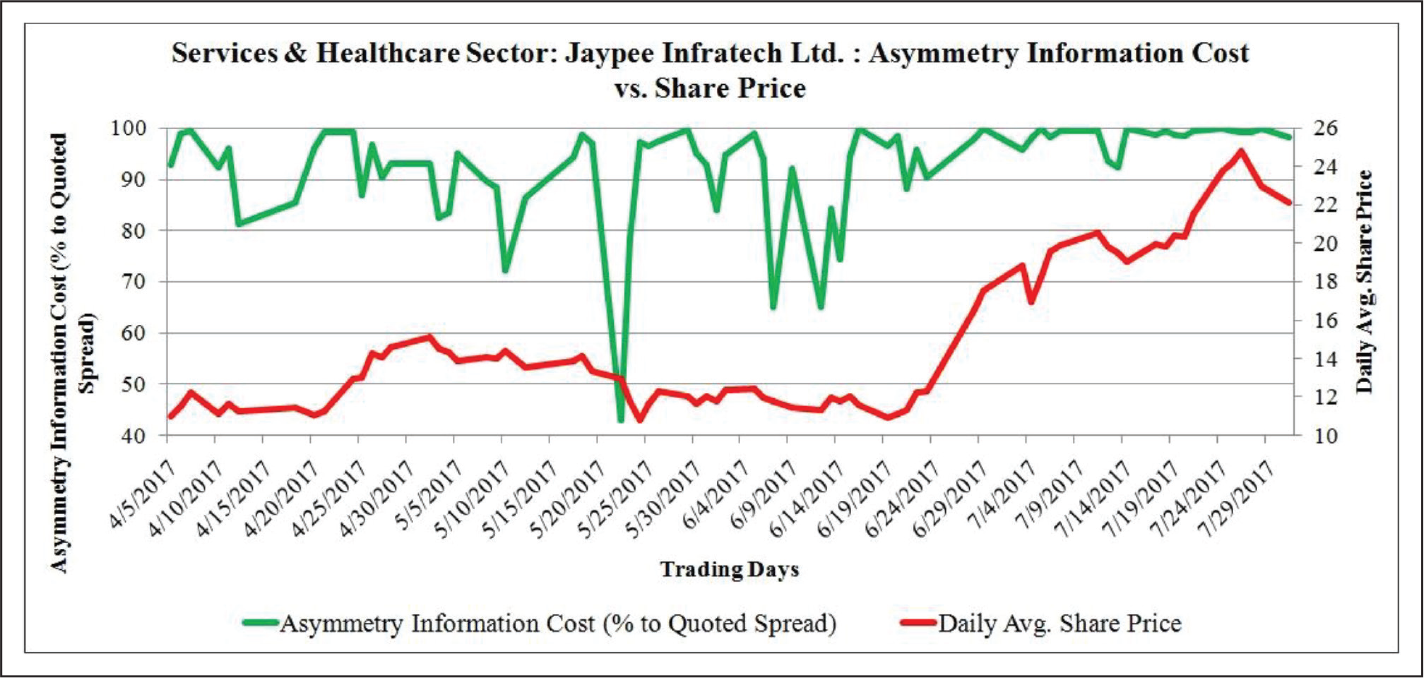

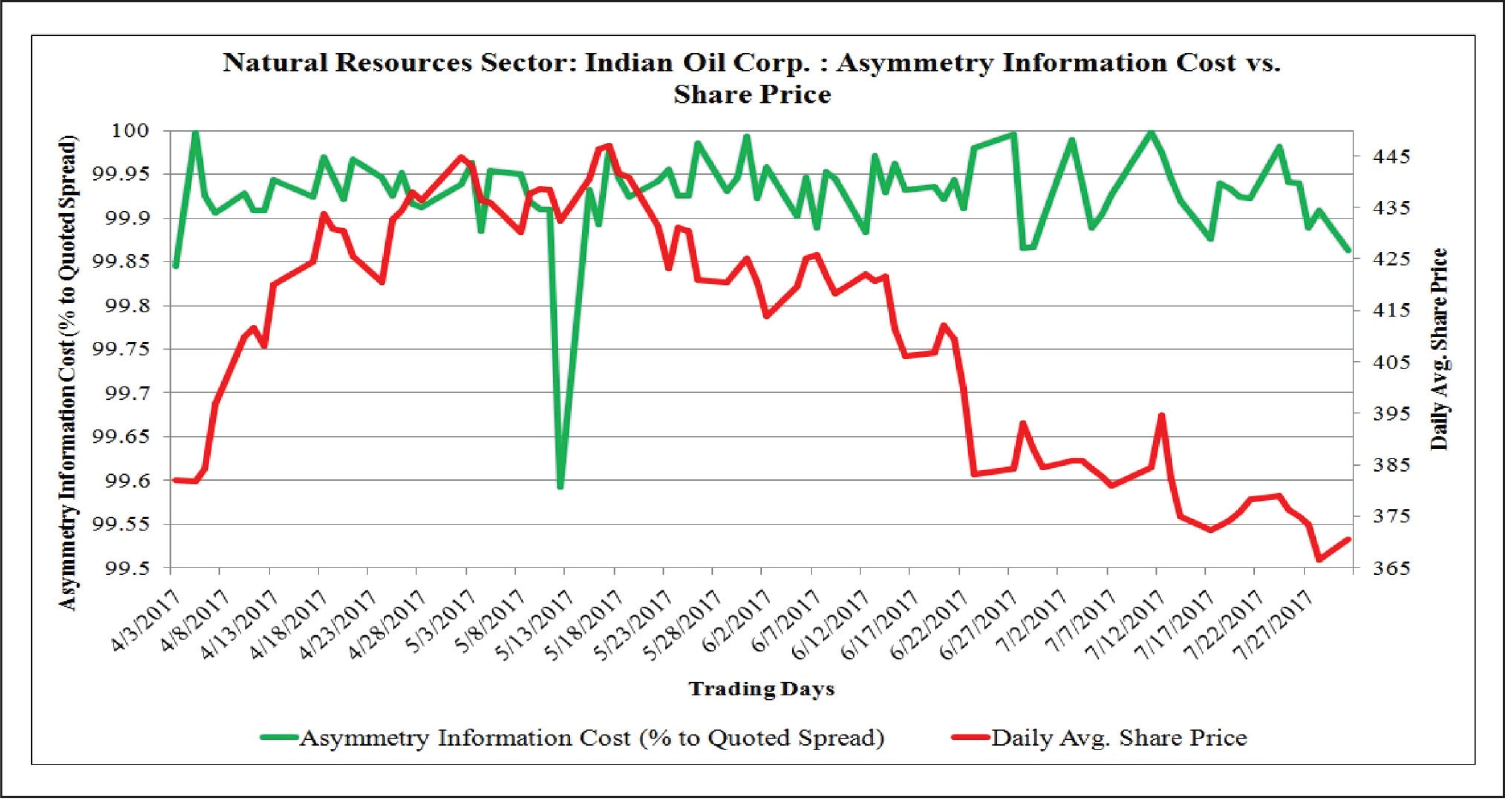

In case of selected stocks from other sectors (Figures 5–7), the study finds similar relation between asymmetric information cost and share price. However, the impact of asymmetric information cost on share price is much higher in case of ITC Ltd. (consumer goods sector) and Jaypee Infratech Ltd. (services and healthcare sector) than others.

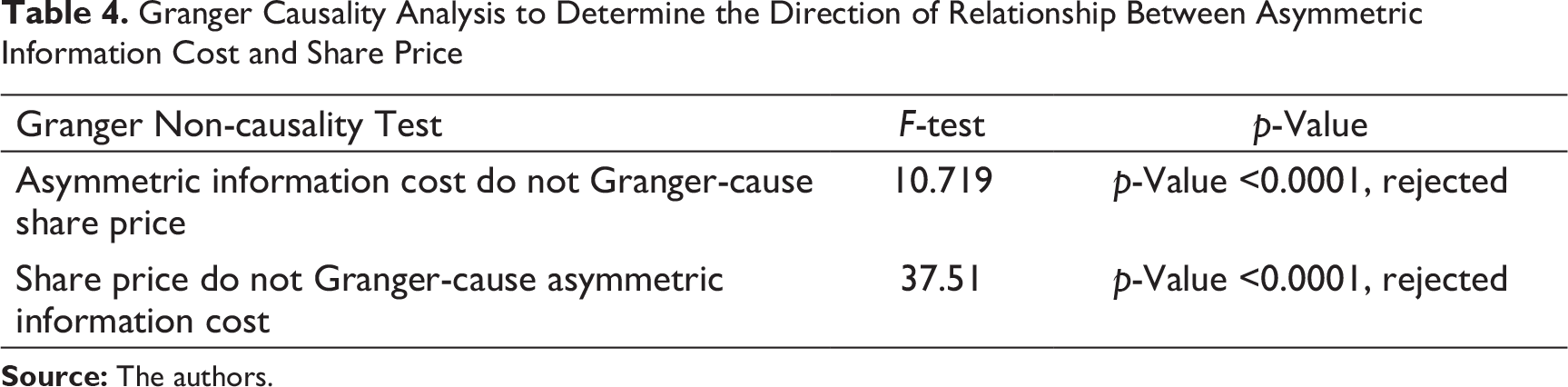

To analyze the causal relationship between asymmetric information cost and share price, the study performs Granger non-causality test.

Granger Causality Analysis to Determine the Direction of Relationship Between Asymmetric Information Cost and Share Price

From the Table 4, it can be seen that the Granger non-causality test rejects NULL hypothesis in both cases. So, the Granger non-causality test reveals a bidirectional causality between asymmetric information cost and share price, which implies that price and asymmetric information cost can influence each other. The study rejects hypothesis 4 and concludes share price and asymmetric information cost can influence each other.

Sector-wise Analysis of Determinants of Asymmetric Information Cost of Bid-Ask Spread

Sector-wise Analysis of Determinants for Asymmetric Information Cost. Almost All the Explanatory Variables Are Found to Be in Significant Relation with Asymmetric Information Cost Across the Sectors

In the literature on the subject, share price, trading volume, return volatility and number of ticks are considered as explanatory variables for the analysis of asymmetric information cost (Ahn et al., 2002; Brockman & Chung, 1999; Copeland & Galai, 1983; Demsetz, 1968; George et al., 1991; Glosten & Harris, 1988; Hasbrouck, 2007; Huang, 2004; Kim & Ogden, 1996; Wang, 1999). However, literature does not provide conclusive evidence for the expected relationship of asymmetric information cost with each of the above-mentioned explanatory variable. The results satisfy basic requirements of robustness test.

Empirical relationships between explanatory variables and asymmetric information cost are in accordance with recent literature (Ahn et al., 2002; Copeland & Galai, 1983; George et al., 1991; Huang, 2004; Kim & Ogden, 1996) in majority of the sectors. Volatility has significant positive relation with asymmetric information cost in all the sectors, which can be implied that, more the volatility more will be the adverse selection cost. This is consistent with studies by Huang (2004), and Kim and Ogden (1996). However, volume has a positive relation with asymmetric information cost in all the sectors except IT–telecom and natural resources sectors. For these two sectors, with increasing traded volume, more information is available to all traders, which lead to decrease in asymmetric information cost. Significant positive relation between asymmetric information cost and volume is consistent with findings from Kim and Ogden (1996), Ahn et al. (2002) and George et al. (1991), which implies with more volume being traded, asymmetric information cost increases. Number of trades has a significant negative relation with asymmetric information cost in all the sectors. Negative relation between trading frequency and asymmetric information cost is consistent with study by Kim and Ogden (1996), Huang (2004) and Giouvris & Philippatos (2008). This implies with more trading, scope of asymmetry in information for traders decreases, which subsequently decreases the adverse selection cost. However, share price has a significant positive relation with adverse selection cost in all the sectors. This implies with increasing share price, adverse selection cost increases. High priced stocks have less impact on information asymmetry. The above results reject the hypothesis 1: determinants have different impact on asymmetric information cost for different sectors. The difference is in terms of relation direction, significance and strength.

Sector-wise Analysis of Determinants of Asymmetric Information Cost of Bid-Ask Spread in Up-market

The study performs a sector-wise analysis of up-market dataset to capture the impact of buyers’ market on asymmetric information (Table 6). The study considered a continuous upward movement for consecutive trading days as an up-market trend. During the up-market, more information is coming to market and this information may be available to all traders, which are factor into the prices. The results satisfy basic requirements of robustness test.

Sector-wise Analysis of Determinants for Asymmetric Information Cost in Up-market. Almost All the Explanatory Variables Are Found to Be in Significant Relation with Asymmetric Information Cost Across the Sectors

The above results reject hypothesis 2 stating determinants have different impact on asymmetric information cost for different sectors in terms of relation direction, significance and strength.

Sector-wise Analysis of Determinants of Asymmetric Information Cost of Bid-Ask Spread in Down Market

Sector-wise Analysis of Determinants for Asymmetric Information Cost in Down-market. Almost All the Explanatory Variables Are Found to Be in Significant Relation with Asymmetric Information Cost Across the Sectors

Volatility has a significant positive relation with asymmetric information cost in all the sectors. Volume has significant negative relation with asymmetric information cost in IT–telecom and natural resources sectors, which implies different behaviour of traded volume in down market due to change in market dominance. Number of trades has significant inverse relation with asymmetric information cost in all sectors except in consumer goods, which can be due to seller dominated market changes behaviour of trading frequency on adverse selection cost. Hence, increase in the trading frequency will cause in less asymmetric information cost in major sectors. Share price has a positive relation with asymmetric information cost in all sectors. The above results reject hypothesis 3 stating determinants have different impact on asymmetric information cost for different sectors in terms of relation direction, significance and strength.

Conclusion and Policy Implication

The study reports the asymmetric information cost of bid-ask spread in different market conditions of Indian market (NSE) under high-frequency trading. The study used the model of Affleck-Graves et al. (1994) as a base model to build an empirical model to analyze the determinants of adverse selection cost under high-frequency trading. Empirical analysis reveals that share price, traded volume, return volatility and trading frequency have a significant impact on asymmetric information cost. The study found that asymmetric information cost has a positive relation with return volatility, traded volume and share price, while it has a negative relation with the trading frequency. The policy measures emanating from the analysis are that exchange should take steps to increase frequency of trading with low trading volume contracted. The market conditions-wise analysis, on pooled dataset, reveals that some of the explanatory variables have different impact on asymmetric information cost under different market conditions and thereby indicating determinants’ impact on asymmetric information cost is not uniform across various market conditions. The results of sector-wise pooled regression are similar across sectors, which indicates that sector-specific information behaves similarly.

The estimation of asymmetric information cost and analysis of its determinants would help stock exchange to design the market-microstructure for trading under different level of information asymmetry in market. The findings of the study suggest reduction of asymmetric information cost in case of consumer goods sector, which is relatively higher, compared to other sectors. The empirical findings reveal that volatility positively contributes to asymmetry information cost and hence increase adverse selection cost. Exchange should take steps to increase the trading volume and reduce return volatility to contain information asymmetry. Exchange should design stock specific volatility control policy to reduce the adverse selection cost. Improving disclosures norms and seamless information disclosures at Exchange could be the policy of the exchange to reduce information asymmetry. The empirical findings indicate that with more trading, information asymmetry decrease, which subsequently reduce adverse selection cost and, hence, the strategy of exchange should be to improve trading volume, which, in turn, will reduce information asymmetry. As the study has found lower information asymmetry with high volume trading and, hence, traders should initiate LOB during higher trading volume period to reduce the adverse selection cost. The findings of the study on NSE listed sample stocks reveal that exchange needs to reduce information asymmetry to decrease the spread and increase market quality. Since bid-ask spread indicates the level of trading and liquidity in the market, exchange needs to closely monitor privately held information to reduce asymmetry cost, which could significantly impact the bid-ask spread.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.