Abstract

This study focusses on adopting a multi-level model for the organizational context within work groups and a functional perspective for socially responsible behaviours. This study developed a multi-level model for sustainable accounting practices within the work environment and tested it to illustrate some of the reasons that make organizations voluntarily participate in the green environmental behaviour. The quantitative (questionnaire survey) design was used to gather data from included 313 company workers in Iraq who were organized into 60 work groups. The results show that it was revealed that routine redesigning, legitimacy and functional affordance are related to sustainable accounting practices within the work environment for the leaders and members of the work groups. Furthermore, there was a direct relationship between routine redesigning, legitimacy, and functional affordance and sustainable accounting practices in addition to a mediation-mediated relationship by organizational sense-making within work groups. Theoretical effects and the revealed results highlighted psychological, social and organizational conditions that determine the sustainable work practices, and it was recommended that organizations should facilitate their social responsibility and environmental sustainability.

Keywords

Introduction

Routines are a fundamental concept in organizational strategy and research, and they play a significant role in coordinating the organization’s activities, widely contributing to constructing organizational abilities (Bapuji, Hora, Saeed, & Turner, 2018). While organizations derive significant value from routine stability, there is an increased concern about acquiring an insight into the value that would be gained or lost through routine redesigning (Feldman & Pentland, 2003). The classical organizational theory assumes that routine change, which is defined as numerous styles of related behaviours, is a fundamental thing for organization renewal (Bresman, 2013). Meanwhile, organizational and strategic scientists have realized that routine redesigning is often a complicated process that would have severe consequences due to its incompatibility with the previously approved organizational design (Helfat & Karim, 2014).

Routine is related to stability; but in recent years, due to the increased competition and advancements in technology, there is an increased need for capable and competent routine change (Al-Abrrow, Alnoor, & Abbas, 2019; Dittrich, Guérard, & Seidl, 2016). Other scientists offered evidences showing that routine redesigning would lead to beneficial results represented by renewing organizations. In short, despite the bad or inefficient effects of routine redesigning on organizations, it may still have several benefits (Bapuji et al., 2018). Hence, solid routine redesigning offers a potential motive to reinforce organizational performance through redesigning the pattern of procedures that constitute the routine and hence influencing its efficiency (Feldman, 2000; Peeters, Massini, & Lewin, 2014).

Routine change contributes not only internally but also externally when it achieves stakeholders’ interests (Pluye, Potvin, Denis, & Pelletier, 2004). This is confirmed by the institutional theory, which states that legitimacy has a significant influence on how an organization is constructed, how it is operated, how it is understood and how it is evaluated as a tool for supporting the organizational reputation (Drori & Honig, 2013). This may be exemplified by the oil companies operating in Brazil, which were victims of mismanagement and bad organizational change concerning rules and procedures, which led to tax fraud that contributed to the company’s legitimacy loss (Barros, 2014).

The Global Reporting Initiative (GRI, 2011) describes the process of reporting for sustainability by companies as ‘the practice of measuring, disclosing, and being accountable to internal and external stakeholders for organizational performance towards the goal of sustainable development’. In response to the social, cultural, and legislative increase, the aforementioned event demanded the expansion of companies’ responsibility to cover environmental concerns, and as a result of which, many organizations have become concerned about achieving legitimacy in assisting green transformations (Eneizan, Wahab, & Bustaman, 2015; Seidel, Recker, & Vom Brocke, 2013).

Routine redesigning contributes to achieving sustainability as employees’ behaviours can contribute to the dynamic capacities of sustainability (Strauss, Lepoutre, & Wood, 2017). In addition to routine redesigning, legitimacy stimulates sustainable accounting practices as stakeholders directly influence employees’ behaviour through the acquisition of social support ensuring that sustainability is guaranteed, and in turn, organization survival (Bäckstrand, 2006; Elg, Ghauri, Child, & Collinson, 2017; Hatch, 2013). Moreover, functional affordance has become the primary resource used to assist organizations in their efforts to become more sustainable and to support sustainable environmental processes. It is a kind of organizational change project that aims to limit consumption of the environmentally harmful resources and outputs through empowering organizations to understand the situation and implementing more sustainable practices.

The social, technical theory suggests that human and technological behaviours follow a coherent and interactive pattern and that any change occurring within technological behaviour will affect social relationships, emotions and work-related situations in addition to the effects on the new technological behaviour success or failure (Dauber, Fink, & Yolles, 2012; Geels, 2004). It is necessary for the work environment to be appropriate for human resources through the existence of the appropriate material characteristics within the organization (Seidel et al., 2013; Van Dijk, Berends, Jelinek, Romme, & Weggeman, 2011). However, during the last decades, many organizational scientists realized that lenses and concepts of systems have to view the organization as more than open systems, mainly because organizations face great difficulties due to the global changes, and this requires the need for new methods to understand work organizations as systems. This understanding is required to reinforce social sustainability within them based on contemporary work contexts (Kira & Eijnatten, 2013). Organizations’ behaviours and procedures related to social, economic and environmental sustainability have become a crucial issue (Eneizan, Abdulrahman, & Alabboodi, 2018; Enticott & Walker, 2008).

In the case of Iraq, which is a country that experienced many difficulties and crises similar to other countries and is currently experiencing the re-development stage, the infrastructure has collapsed in many sectors, including education, electricity and oil, because of all the malformations. Furthermore, practices of many organizations and companies operating in Iraq have resulted in social, economic and environmental problems—some of which are abnormal and others are more frequent but essential routines (e.g., local incidents of water pollution and discrimination in regulatory practices). For self-reestablishment, there must be a reconsideration for many procedures and rules in addition to the socio-technical elements within the organization and to achieving stakeholders’ interests with a pattern that leads to creating positive perspectives and organizational sense. This will eventually lead to facilitating human capital. In this way, companies will have a storage of knowledge and a pool of employees that facilitate the survival of the organization. However, there is a lack of studies investigating the relationship between routine redesigning, legitimacy, and functional affordance and sustainable work practices. Furthermore, the role of intermediation of organizational sense-making based on clear bases has been under-examined (Seidel et al., 2013).

Thus, the current study aims to investigate the influence of routine redesigning, legitimacy, and functional affordance on sustainable transformations with organizational sense-making as an intermediate variable, mainly because early studies indicated that a group of social, economic, and environmental procedures offer performance rewards while mitigating the adverse effects on organizational behaviours and practices (Enticott & Walker, 2008). Moreover better sustainability performance is related to sustainability accounting practices. However this is against the stance which legitimacy theory suggests that organizations tend to legitimize their efforts of being socially responsible through social or sustainable accounting (Clarkson, Li, Richardson, & Vasvari, 2008). In this regard, it is interesting to mention the study done by Dawkins and Fraas (2011). They found that companies with extreme environmental performance generally disclose more and the main argument by them is about the bad environmental performers who tend to legitimize themselves as socially responsible through sustainability reporting. Hence, this debate need to be further investigated and this study contributes in understanding the phenomena in a better way.

Theoretical Framework and Hypotheses Testing

Organizational Routine

Early literature indicates that organizational routine is the primary process for sustainability because routine activities are included in organizations’ budget as well as their operations by employees, as these activities go through a functional description and need storage of sources to be achieved (Pluye et al., 2004). Hence, organizational routine is viewed through two related factors: the first views organizational routine as an activity or a behaviour model, while the second views it as a group of rules and procedures, in regard to which, routine is considered as following a group of rules and procedures to perform a specific activity (Helfat & Karim, 2014). Organizational routine is regarded as a group of behaviours and acts engaging in the adaptive or previously acquired behaviour, and hence routine is a stored behavioural capacity where these capacities involve knowledge and memory (Becker et al., 2005). Moreover, organizational routine consists of a group of assumptions that are represented by the various behaviours that can be transferred from an organization to another by worker members, so organizational routine reflects the organizational memory that supports coordination among functional activities (Valieva, 2014). This occurs by using the pre-experience in achieving current activities depending on social networks, documented evidence, and computerized memory (Pluye et al., 2004). The work of organizational routine is a mechanism of informal control because of the apparent overlap in the understanding of participants in implementing the routine; thus, routine can also be understood as the combination of undocumented and documented rules that may be complementary or alternative to each other, to avoid contradiction (Feldman, 2000; Yang, 2017). Early literature indicates that organizational routine is a multi-dimensional construct (Loebel, 2012) consisting of organizational memory, adaptation, and rules (Pluye et al., 2004).

Organizational Legitimacy

The institutional perspective offers another view of relationships between organizations; it describes how organizations succeed through compatibility and environmental expectations. This is because the institutional environment consists of stakeholders’ standards and values, whereby this viewpoint argues that organizations adapt structures and processes that satisfy stakeholders. Organizational legitimacy is the general perception that the procedures of the organization are correct, desired, and appropriate within the environmental system of rules, values, and beliefs. In this regard, the institutional theory is concerned with a hurlow set of rules and values that shape behaviour versus concrete elements of technology and structure (Suchman, 1995; Woodward, Edwards, & Birkin, 1996). In addition, acquiring actual social support guarantees obtaining legitimacy, and this reinforces the organization’s survival. Contrastingly, legitimacy is not offered to the organization to gain more money or to offer better goods and services, but it is offered because it goes side by side with the widely accepted modern conventions and rules (Hatch, 2013).

Organizational legitimacy addresses how organizations can increase their ability to develop and to survive within a competitive environment through increasing acceptability and reliability and subjecting to stakeholders’ accountability. In contrast, many new organizations suffer and many of them cannot survive unless they can develop the necessary competencies for clients’ attraction and obtain sufficient resources (Jones, 2012). So, the best way for a new organization to obtain legitimacy is to imitate the goals, structures, and cultures of successful organizations within its environment (Rowan, 1982) to achieve organizational and social connection in order not to withdraw external agencies’ support, including governmental and legal authorities as well as clients (Blasio, 2007). This stems from the connection between the organizational legitimacy and the organizational reputation, as both concepts represent an evaluation of the organization by the social system (Deephouse & Carter, 2005).

In addition to what was discussed, organizational legitimacy is evaluated through examining the prevailing values and norms within the society, as obtaining scarce resources and commercial exchanges are not enough to judge the legitimacy of a particular organization (Dowling & Pfeffer, 1975). As a result, there are three types of legitimacy that are offered to organizations: pragmatic legitimacy, moral legitimacy and cognitive legitimacy. The first one, pragmatic legitimacy, is offered based on the audience benefit. The second one, moral legitimacy, is offered when an organization operates based on community moral interests and concerns and not on personal interests, while the third one, cognitive legitimacy, is offered to an organization when it works based on values and beliefs of stakeholders, in addition to its acceptability among audience (Colquhoun, 2013).

Functional Affordances

Functional affordance describes the ability to function and work in light of what the physical properties within the organization allow (Seidel et al., 2013). This is confirmed by other researchers who stated that functional affordance is related to physical characteristics (e.g., Hartson, 2003). This concept was suggested first by Gibson in environmental psychology by connecting it to the environment (Chemero, 2003). Gibson (1986) argued that animals and human beings do not initially view the physical properties of things, but instead, they view what they offer and thus, what we realize when viewing things are their qualifications rather than their qualities (Gibson, 1986). However, this realization does not necessarily mean that a human has to realize the possibility of the offered work (Stoffregen, 2003). Functional affordance thus describes the possibility of directed or instructed work towards the goal, which is offered to people and groups specializing in organizational fields (Seidel et al., 2013).

Functional affordance depends on the nature of the relationship between a user and a working system, as human and technological behaviours are directed through a coherent and interactive way. Besides, any change that occurs to the technological behaviour is reflected and consequently affects the social relationships, emotions and work-related situations in addition to the success or failure of the new technological behaviour (Dauber et al., 2012; Geels, 2004). Functional affordance determines the necessary tools to achieve the clear work goal (Mizelle, Kelly, & Wheaton, 2013), and this leads to achieving human resources interaction with the organization based on the goals, plans, values, beliefs and pre-experiences (Abdelqader Alsakarneh, Chao Hong, Mohammad Eneizan, & AL-kharabsheh, 2018; Alsakarneh, Hong, Eneizan, & AL-kharabsheh, 2018; Awaad, Kraetzschmar, & Hertzberg, 2015). Functional affordance is the primary factor of transformation towards sustainability through its useful contributions in changing the organizational practices that, in turn, represent green transformations (Seidel et al., 2013).

Organizational Sense-making

Individuals vary in the extent of playing an active role in affecting other organizational parties’ senses (Grimes, 2010), so there is no single agreed upon definition of sense-making. Despite this, there is an emerging consensus that sense-making indicates processes by which people rationally seek to understand vague or confusing issues or events (Brown, Colville, & Pye, 2015) as this represents a path that leads the ambiguous processes towards knowledge-based realities (Patriotta, 2003). Also, despite the similar use of apathy and ambiguity, there is no significant difference between them regarding senses. Reducing ambiguity lies in working to reach an answer for the question: what is happening (e.g., what is the story?), while minimizing indifference suggests that work does not make clear the lack of clarity, but this work illustrates the lack of clarity through what is done and what acts are performed to form what is happening. Therefore, organizations differ in realizing the market and technology, and some are more innovative because organizational sense-making is related to several organizational processes (Dougherty, Borrelli, Munir, & O’Sullivan, 2000). Strategic cognitive work models, in general, are based on the assumption that the rational thought is closely related to the selected procedures, so this process, through which what is going on is understood, has become very important for organization as it is linked to reducing uncertainty, which constitutes the primary factor in organizational attitudes (Maitlis & Christianson, 2014; Thomas, Clark, & Gioia, 1993).

Sense-making has become more central and intertwined in organizational concepts and theories, as senses and organization complete each other and organization emerges from a continuous process that is organized by people to understand the unclear inputs and bringing this sense back into the world to make it more organized (Weick, 2012). In other words, the organization is achieved to the limit with which senses are made, and thus an organization emerges from organization and senses. This explains the importance of organizational sense is making perspective within organizations (Colville, Brown, & Pye, 2012; Weick, Sutcliffe, & Obstfeld, 2005). Despite this sense-making, there are still some unresolved disputes regarding the concept, which suggest that the occurrence of sense on daily or instantaneous base in addition to its linkage to future may occur in the future. Many studies indicate that individuals who work on a single goal have the same sense, while other studies indicate that this does not necessarily ring true as senses may contrast (Brown et al., 2015).

There is increasing evidence that scientists seek to stimulate discourses focussed on sense-making as the organizational sense, making the process the primary factor for organizations’ success for its significant role in achieving consistent consensual cooperation among employers, employees, customers and other organizational components (Holt & Macpherson, 2010).

Sustainable Accounting Practices

In recent years, companies have begun to proactively integrate environmental strategies with their business and operations’ strategies and have moved beyond the organizational responses that involve costly investments in controlling pollutant waste and emissions (Eneizan & Obaid, 2016; Mohammad Eneizan, Abd. Wahab, & Ahmad Bustaman, 2015; Sharma & Henriques, 2005). These strategies facilitate the maintenance of resources and energy to contribute to directly decreasing costs by maintaining the natural environment for organizational sustainability (Al-Abrrow, Alnoor, & Abdullah, 2018). In relation to this, a perspective of the environmental destruction regarding risks was formulated in past literature; for instance, overexploitation and pollution may threaten access to a natural source; weak environmental performance may lead to lawsuits against organizations or may jeopardize their brands, and high levels of adverse climatic conditions may hinder production. Moreover, researchers suggest that such developments may create entrepreneurial opportunities to introduce innovative technologies (Ocampo, 2019). Wastes, for example, appear to be an environmental challenge but can be used to achieve better production and utilization of resources as efficiently as possible. This makes the environmental waste problem an ideal opportunity to use technologies that can utilize resources more efficiently either by recycling or reducing the amount of waste they leave (Bocken, Short, Rana, & Evans, 2014).

Natural environmental destruction is a prominent issue for our community, and business organizations are the main contributor to this challenge. As a response to the social, cultural and legislative stresses, 60 per cent of executive managers are committed to ‘Green Technology’ initiatives and the efforts of transforming into sustainability (Bhaumik & Banik, 2006; Seidel et al., 2013). This is possible by assisting the organizational context to form and understand sustainability interpretations by the organization members about sustainability practices within the organization, by legitimizing issues as part of organizational identity and integrating environmental indicators into employee performance assessment and employee’s knowledge of institutional sustainability policy (Abdulaali, Alnoor, & Eneizan, 2019; Linnenluecke, Russell, & Griffiths, 2009). The essence of sustainability, in particular, lies in the production of positive externalities and the avoidance of negative internal factors, which require the necessary existence of sustainable, dynamic capabilities that enable the organization to re-establish its resource base to deal with changes resulting from its proactive environmental or sustainability strategy. This requires the organization to achieve the balance between business objectives and external environmental processes (Augenstein & Palzkill, 2015; Bag, 2018; Strauss et al., 2017). The adoption of sustainable innovations is therefore influenced by many social and organizational factors, as the traditional view suggests that sustainable innovations occur and spread rapidly when there are mechanisms for market and organizational incentives, while recent evidence suggests that incentives are necessary to adopt standard innovations (Dyck & Silvestre, 2018).

Sustainable Transformations and the Role of Routine Redesigning, Organizational Legitimacy and Functional Affordance

Current studies in this field focus, in particular, on organizational motivational processes as an interpretation of how to form an organizational routine for sustainability, and this claim relies on dealing with memory, adaptation, values and rules as catalysts to influence sustainable accounting practices (Pluye et al., 2004). Empirical studies suggest that people, who think highly of a repetitive pattern, which can be distinguished from interrelated procedures tend to be concerned about others’ well-being and engage in more positive behaviours at work (Stiles et al., 2015). In line with the assertion that such processes may also influence sustainable accounting practices, results of earlier studies indicated that actual sustainability would require companies to fundamentally change the way they do business and commercial operations and the current status, as companies generally do not consider such changes.

Sharma and Henriques (2005) examined managers’ perceptions regarding to sustainability practices and found that the sustainability practices have moved beyond the early stages and more advanced practices are being adopted these days and focussing more on redesigning the routine processes to achieve better sustainability. Generally speaking, the analysis focusses on the company’s survival than on its sustainability (Shevchenko, Lévesque, & Pagell, 2016). It is possible therefore that routine redesigning contributes to achieving sustainability as employees’ behaviours can contribute to the dynamic capacities of sustainability (Strauss et al., 2017). To conclude, previous research and theories indicate that routine redesigning stimulates some employees to engage in an environment-friendly behaviour, as this represents an opportunity to achieve their moral motivations in order to maintain a desirable environment and society. Such dynamics are likely to influence supervisory and non-supervisory staff behaviour.

In addition to routine redesigning, legitimacy stimulates sustainable accounting practices as stakeholders directly influence employees’ behaviour through the acquisition of social support ensuring that sustainability is guaranteed, and in turn, organization survival (Bäckstrand, 2006; Elg et al., 2017; Hatch, 2013).

Recent research on sustainable accounting practices points out the role of social norms in developing sustainable projects, and previous studies suggest that sustainability emerges either within a supportive social environment frame that is characterized by the existence of social legitimacy or against a social environment that is characterized by the absence of social legitimacy. Both tracks depend on legitimacy as a stimulus to develop sustainability thoughts, acts, and reciprocal relations (Kibler, Fink, Lang, & Muñoz, 2015). Legitimacy, therefore, offers social acceptability for business or organizations, which assists companies to obtain a constant flow of resources and constant support that leads to increased sustainable accounting practices (Scherer, Palazzo, & Seidl, 2013).

Functional affordance is the main contributor towards sustainability through its useful contributions in changing the organizational context that in turn stimulates work behaviour, which forms green transformations (Seidel et al., 2013). Early studies indicate that functional affordance contributes to sustainability processes through relying on the concerned individuals and the organizational context; in other words, functional affordance assists in designing sustainable business (Seidel & Recker, 2012).

Functional affordance has become the primary resource used to assist organizations in their efforts to become more sustainable and to support sustainable environmental processes. It is a kind of organizational change project that aims to limit consumption of the environmentally harmful resources and outputs through empowering organizations to understand the situation and implementing more sustainable practices.

The role of organizational sense-making is influential and it can form sustainable accounting practices. Researchers argue that organizational work involves ambiguity and when the theme or meaning is ambiguous, people seek a way to reduce their confusion (Angus-Leppan, Benn, & Young, 2010). Organizational behaviours hence significantly affect the competency and efficiency of organizational practices and business (Cooper, Stokes, Liu, & Tarba, 2017). To maintain organizational sustainability, employees’ values should match those of their organization’s, and this requires changing the organizational sense-making (Onkila, Mäkelä, & Järvenpää, 2018). It is necessary for managers to communicate information to employees and to state that all are active contributors in achieving sustainable accounting practices (Brunton, Eweje, & Taskin, 2017). Organizational sense-making was chosen as a mediation variable because it represents a core of a dynamic and continuing stream of research in organization studies that are necessary to clarify how people in organizations, when confronted by discrepant events, seek processually to negotiate and sustain meanings that permit coordinated and rational action (Brown et al., 2015).

In recent years, researchers have increasingly approved that members of organizations suffer from organizational factors. Hence, when organizations systematically incorporate empathy in their organizational rules, values and routine, members within the organization positively respond and these feelings lead to positive organizational results such as increased commitment, decreased turning over rate, and enhanced social coherence and performance in achieving sustainability (Shahzad & Muller, 2016). Early studies suggest that organizational routine contributes to limiting organizational learning as it relies on clear, frequent work procedures and rules that contribute to influencing organizational sense-making, which, in turn, leads to decreasing sustainable accounting practices (Rice, 2008).

The unpleasant fact about business in official organizations, and even those with charitable functions and those that offer valued social contributions, is that sometimes these organizations might have awful work environments, which affect not only individuals’ behaviour but also the climate, performance and the sustainable accounting practices (Abdullah, Ahmad, Zainudin, & Rus, 2019; Jung, Bozeman, & Gaughan, 2018). Sense-making offers a way to understand how individuals understand their complex environments and thus, our understanding of events is a constant process that is influenced by factors that shape the way we are. Pre-experiences that shape how we understand what we experience, what occurs within our current environment, and our interaction with others, make legitimacy the primary factor and a great contributor in influencing organizational sense-making (Thurlow & Mills, 2015). Legitimacy then is related to organizational sense-making through its significant role in increasing untraditional communication among organizations and stakeholders and through decreasing unsurpassed communication, which significantly contributes to increasing social responsibility and hence assisting in achieving sustainable business practices (Schultz & Wehmeier, 2010). Legitimacy crisis emerges when the audience views the organization as no longer conforming to social standards and expectations. This may lead to undermining the legitimacy of the organization and to formal and informal restrictions on its activities, damaging its reputation and even threatening its survival through the negative influence on its organizational sense, which will ultimately negatively affect its sustainable accounting practices (Banik & Bhaumik, 2014; Zheng, 2010). Furthermore, there is a need to understand how harmony between social environment and new technology is essential for the success of implementing new systems and sustainable performance. Compatibility of social and technological systems encourages and increases organizational success.

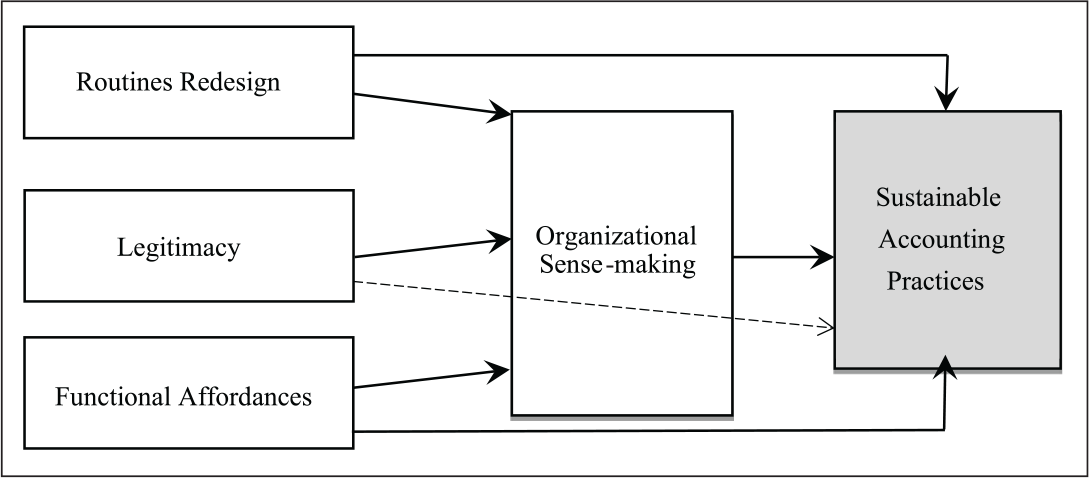

Organizational affordance achievement depends on each managerial intervention and user properties that allow reinterpreting of usage, as organization system functional talents emerge when the physical properties of functional systems are interpreted as those that offer vital work capacities that confirm the new work goals and objectives imposed on individuals. Moreover, these goals are instilled through new work goals that are determined by pointing out the target performance indicators and green action policies. To obtain sustainable work or business practices, business potentials that are offered by the organization systems should be available and this, in turn, depends on awareness, motive, and individuals’ attitudes in light of the business’s new goals prepared by the management (Seidel et al., 2013). Figure 1 shows the proposed conceptual model:

Methodology

Sample

Data obtained from 60 work groups’ leaders and 313 members working in oil, communication, and construction companies were analyzed. The group leaders were the group heads, while the members were at the middle management level. Before questionnaire copies administration, human resource managers were consulted about selecting the work groups. Following the methods utilized in previous researches, we designed a frame from a sample selection of 60 work groups that included 313 members from the companies. The selected work groups were formed a year earlier, and each group included more than three members including leaders and members that worked together for more than 1 year. Data were collected from both resources (groups’ members and leaders) at two points, at appropriate times. Human resource managers distributed questionnaires that required work groups’ leaders and members to provide demographic data, self-reports on personality traits, routine redesigning, legitimacy, functional affordance, organizational sense-making, and sustainable business practices. All participants responded and provided the required data. A mean of 4.02 employees for each group participated in this research, with a mean age of 43.06 years for leaders and 31.56 for members. Most respondents were males (61.47% leaders and 74.92% members).

Scales

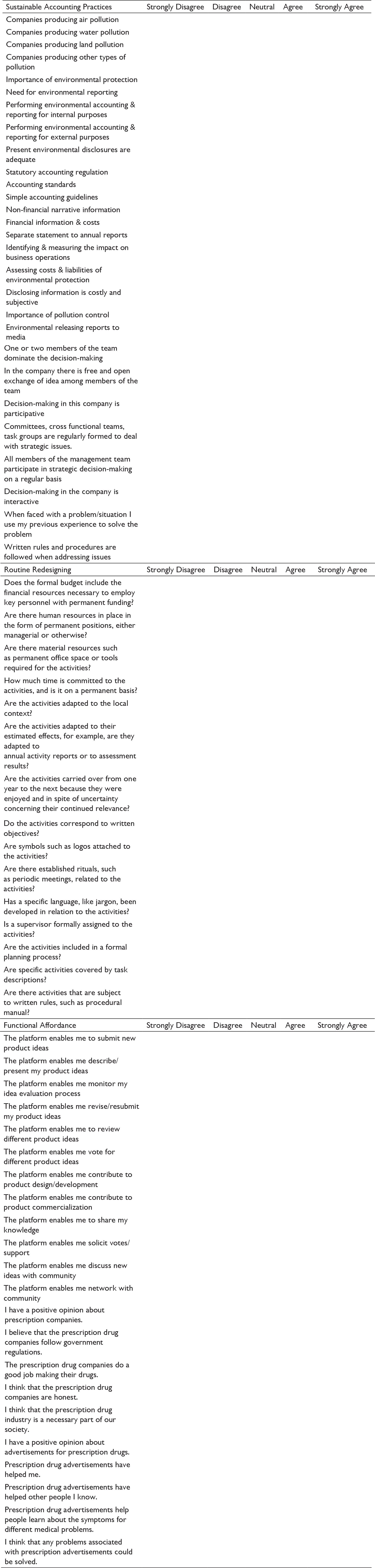

Routine redesigning: Pluye et al.’s (2004) 15-item routine redesigning scale was utilized.

Legitimacy: Chung’s (2010) 10-item legitimacy scale was used.

Functional affordance: Abhari et al.’s (2016) 12-item Functional Affordance scale was used.

Organizational sense-making: Carrington and Tayles’ (2011) 8-item Organizational Sense-making scale was used.

Sustainable accounting practices: Sharma and Henriques’ (2015) 20-item sustainable accounting practices scale was used.

The research framework included five variables: routine redesigning, legitimacy, and functional affordance as independent variables, organizational sense-making as an intermediate variable, and sustainable accounting practices as a dependent variable. These components were assessed using multi-element scales and the final questionnaire consisted of 65 items distributed on five variables gauged using a 5-point Likert scale (1 = completely do not agree, 2 = do not agree, 3 = somewhat agree, 4 = agree and 5 = completely agree). The questionnaire is attached in Appendix A.

Data Analysis

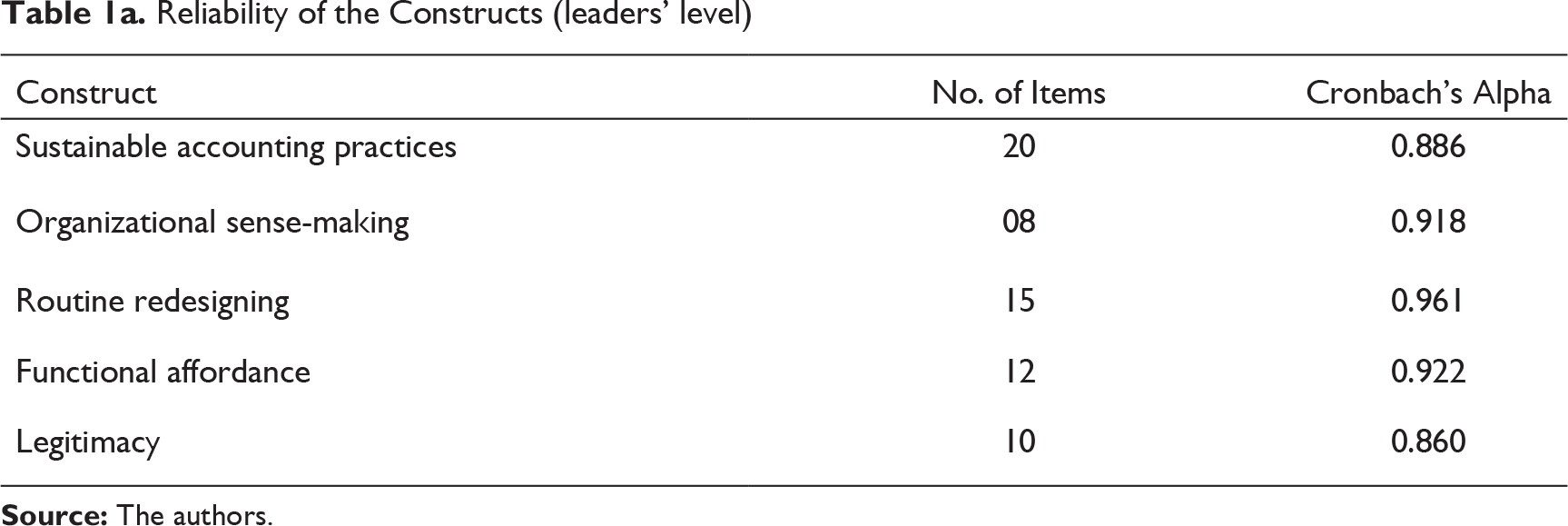

The aforementioned hypotheses were tested using SPSS version 22.0 before moving to the regression analysis certain preliminary statistics were performed to make sure the data is normally distributed and free from outliers and missing values. Moreover the scale reliability of the constructs was also examined. The results of the reliability are presented in Table 1a.

The data were collected from two different levels in organizations, that is, group leaders and members, to have an in-depth understanding of the phenomena. For this purpose, the analyses are presented for both levels.

Reliability of the Constructs (leaders’ level)

Reliability of the Constructs (members’ level)

Descriptive Statistics

Cronbach’s alpha values for leaders and members are not significantly different from each other. This is because those two samples may be more aware about the relationships between the main components of the study’s model. Also, the reliability is a stable property of tests themselves rather than a characteristic(s) of the responses of a given sample interacting with the items (Helms, Henze, Sass, & Mifsud, 2006).

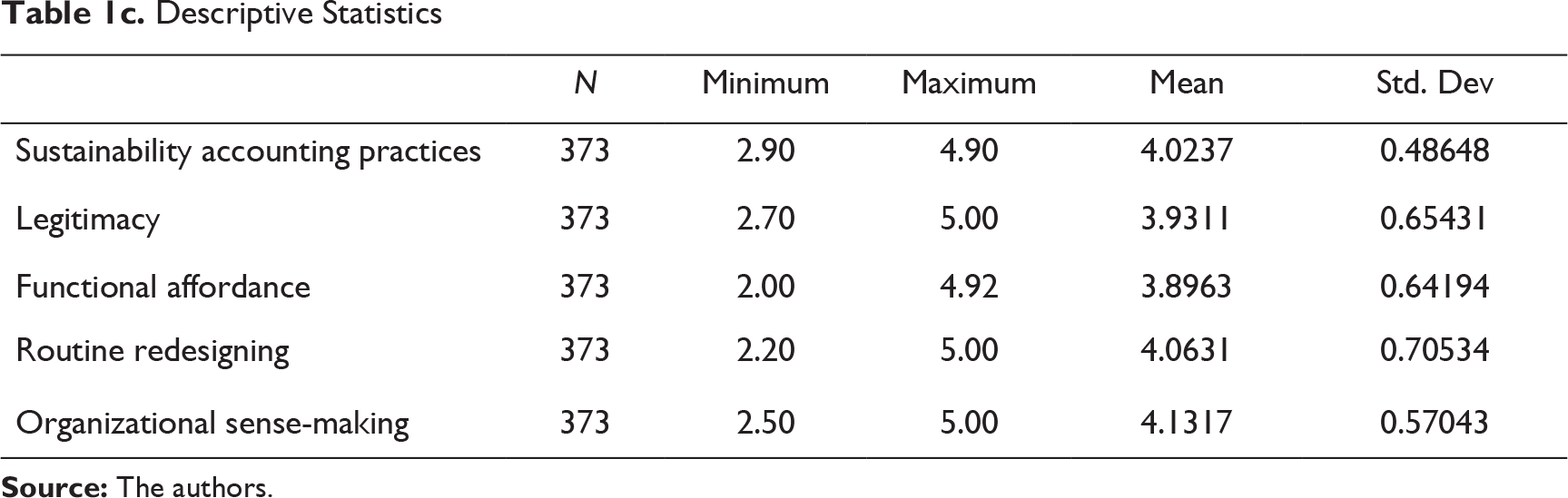

Table 1c shows the descriptive statistics of the constructs included in the study framework; the total responses were 373 including 313 members and 60 groups. The results show that sustainability accounting practices has a mean value of 4.02 with the standard deviation of 0.48 which mean that most of the respondents tend to agree with for the construct. The same is the case with legitimacy, functional affordance, routine redesigning and organizational sense-making, all of them having the mean values above 3 showing that on average the responses are towards agreement side. While the standard deviation in the responses is not high, this can also be seen in the minimum values which are not less than 2, showing that none of the respondents strongly disagreed.

Correlation Analysis (leaders)

* Correlation is significant at the 0.05 level (2-tailed).

Correlation Analysis (members)

The common method variance has a bias problem (Eichhorn, 2014). Therefore, to assure the independent variables free from bias and multicollinearity, the data was tested for tolerance and variance inflation factor (VIF). The results of tolerance and VIF are presented in Tables 3a and 3b.

Collinearity Statistics (leaders)

Collinearity Statistics (members)

Hypotheses Testing

Regression Results (leaders’ level)

Regression Results (members’ level)

Results of Hypotheses (Group Level)

Hypotheses H1a–H3a show the direct relationship (routine redesigning, legitimacy and functional affordance) with sustainable accounting practices. The results are shown in Table 4a under Step 2 below the results, showing that all three variables are significantly positively related to the sustainable accounting practices with p-value <0.05. Hence, supporting the hypotheses H1a, H2a and H3a.

The hypotheses H4a–H6a are regarding the mediating role of organizational sense-making in the relationship of (routine redesigning, legitimacy and functional affordance) with sustainable accounting practices. Mediating effect is evident if independent variable significantly predicts mediator (Step 1), independent variable significantly predicts dependent variable (Step 2) and in Step 3 as explained below, mediator significantly predicts outcome variable and direct relationship between predictor variable and outcome variable is lesser as calculated in Step 2. Here we can see in Table 4a the relationships of independent variables (routine redesigning, functional affordance and legitimacy) with mediator organizational sense-making are significant (Step 1). The independent variables (routine redesigning, functional affordance and legitimacy) with dependent variable sustainable accounting practice are also significant (Step 2) and the relationship of mediator organizational sense-making with the dependent variable sustainable accounting practices is also significant (Step 3) and the direct relationship of the independent variables have become lesser than Step 2. In Step 2 the coefficient for routine redesigning was 0.421 with p < 0.05 while in Step 3 it became 0.119 with p < 0.05; hence organizational sense-making mediates the relationship of routine redesigning and sustainable accounting practices. In the same way the coefficient for functional affordance was 0.347 with p < 0.05 in Step 2 while in Step 3 it became 0.098 with p < 0.05; hence organizational sense-making mediates the relationship of functional affordance and sustainable accounting practices. Moreover the coefficient for legitimacy was 0.287 with p < 0.05 in Step 2 while in Step 3 it became 0.081 with p < 0.05; hence organizational sense-making mediates the relationship of legitimacy and sustainable accounting practices. In a nut shell we can say that H4a, H5a and H6a were supported as there is significant mediating role of organizational sense-making.

Results of Hypotheses (Members’ Level)

Hypotheses H1b–H3b show the direct relationship (routine redesigning, legitimacy and functional affordance) with sustainable accounting practices. The results are shown in Table 4a under Step 2 below the results, showing that all three variables are significantly positively related to the sustainable accounting practices with p-value <0.05. Hence, supporting the hypotheses H1a, H2a and H3a.

Hypotheses H4b–H6b are regarding the mediating role of organizational sense-making in the relationship (routine redesigning, legitimacy and functional affordance) with sustainable accounting practices. Mediating effect is evident if independent variable significantly predicts mediator (Step 1), independent variable significantly predicts dependent variable (Step 2) and in Step 3 as explained below, mediator significantly predicts outcome variable and direct relationship between predictor variable and outcome variable is lesser as calculated in Step 2. Here we can see in Table 4a below the relationships of independent variables (routine redesigning, functional affordance and legitimacy) with mediator organizational sense-making are significant (Step 1). The independent variables (routine redesigning, functional affordance and legitimacy) with dependent variable sustainable accounting practice are also significant (Step 2) and the relationship of mediator organizational sense-making with the dependent variable sustainable accounting practices is also significant (Step 3) and the direct relationship of the independent variables have become lesser than Step 2. In Step 2 the coefficient for routine redesigning was 0.415 with p < 0.05 while in Step 3 it became 0.113 with p < 0.05 hence organizational sense-making mediates the relationship of routine redesigning and sustainable accounting practices, in the same way the coefficient for functional affordance was 0.345 with p < 0.05 in Step 2, while in Step 3 it became 0.094 with p < 0.05 hence organizational sense-making mediates the relationship of functional affordance and sustainable accounting practices; moreover, the coefficient for legitimacy was 0.292 with p < 0.05 in Step 2, while in Step 3 it became 0.079 with p < 0.05; hence organizational sense-making mediates the relationship of legitimacy and sustainable accounting practices. In a nut shell, we can say that H4b, H5b and H6b were supported as there is significant mediating role of organizational sense-making.

Discussions and Managerial Implication

The study aims to identify the influence of routine redesigning, functional affordance and legitimacy on sustainable accounting practices and to address the direct and mediation effects of the three independent variables on sustainable accounting practices, with the role of the intermediate variable (organizational sense-making) in oil, communication and construction companies operating in Iraq. The regression result indicates that routine redesigning, legitimacy and functional affordance significantly influence sustainable accounting practices, and that all three independent variables included in the model are necessary for obtaining a sustainable business performance for more extended periods as the organizational context is the way to sustainable performance for companies. Hence, it would have a positive influence on the economic growth of the country.

Realizing that organizational responses about related environmental issues do not follow official organizational policies and environmental management programmes, we developed and examined a multi-level model to explain the reason behind some employees’ voluntary participation in environmentally friendly behaviours within work, referred to as sustainable practices within companies included in the study. Employees were organized and distributed to small workgroups supervised by a leader. We found that organizational context had cumulative and inflated consequences because when they saw their leader engaged in sustainable work practices, group members increased their call for such behaviour, and this might be an attempt to achieve social value and relational motive.

Leader’s sustainable practices expose the work group to additional social stresses to engage in sustainable work practices. Our theory and evidence, in general, indicate multi-level influences that may stimulate some individual potential motives to achieve sustainable performance. Our multi-level study, which included 60 leaders and their subordinates composed of 313 members, completes and expands the results of Seidel et al. (2013) study, which indicated the significant role of functional affordance and organizational sense-making in sustainability.

This study found the company’s routine redesigning to be positively related to sustainable performance. The results of this study are in agreement with previous results, such as those of Bapuji et al. (2018) which indicated that routine redesigning based on understanding could improve routine efficiency through utilizing the participants-related plans. As employees obtain more knowledge about their roles in routine, they will be able to form more stable expectations than other participants. Furthermore, results indicated a significant influence that reduces uncertainty due to the outcomes of redesigning. In addition, recent research on sustainable accounting practices indicates the role of social norms in developing sustainable projects; early studies indicate that sustainability emerges either within a supportive social environment frame, that is characterized by social legitimacy, or against social environment, that is characterized by the absence of legitimacy (Kibler et al., 2015). Seidel et al. (2013) pointed out that achieving functional affordance depends on each of the current administrative intervention and the user properties that allow reinterpreting the utilized system in the organization as functional talents emerge. In this regard, when the physical properties of the functional systems are interpreted as offering significant work potentials that conform to the new work goals and objectives, which are determined through the target performance indicators imposed on individuals. These goals then are instilled through new work objectives that are determined through the target performance indicators and green work policies. In another related study, Carrington and Tyles (2011) found that sense-making, as a process, assists in giving meaning to environmental events through applying stored knowledge, values, experiences and beliefs on new situations in an attempt to understand these situations. Thus, as the organization’s workforce is more capable of significantly developing its effectiveness and its repositories of knowledge, individuals will be able to understand events more effectively, thereby helping to increase performance.

So far, the organizational sense-making has not attracted much interest from organizational researchers concerned about environmental sustainability. In studies that addressed organizational sense-making as predictors of socially and environmentally responsible work behaviours, particular environmental values, concerns, situations and beliefs have attracted greater interest (Carrington & Tayles, 2011) than the organizational properties also known as related to a larger group of work environment results. Also, despite the prominence of staff-based organizational structures, few studies highlighted the multi-level social dynamics’ combined influences that constitute sustainable practices at work. Our multi-level model is initiated with highlighting these dynamics and indicating the role of organizational sense-making in the relationship between routine redesigning and functional affordance on the current utilized sustainable performance.

Competition based on financial strength is not possible for a company; instead, companies should focus on their design and adopt it as a competitive advantage. Organizational context is viewed as a motivational factor to increase performance and thus, to facilitate countries’ environmental responsibilities in general, and Iraq in particular, companies should re-establish themselves, re-invest in human resources, and reduce their economic values at individual, managerial and general levels. This can be achieved by facilitating the organizational routine and by a commitment to stakeholders’ desires in addition to designing an appropriate environment for various cultures and creating a sense for environmental events by assisting human resources to apply and practise the stored knowledge, experiences, values and beliefs on new situations to understand them.

In doing so, companies will have a stock of knowledge and active employees able to assist the organization to survive, mainly since many studies have been conducted to investigate the relationship between routine and sustainability like Elg et al. (2017), legitimacy and sustainability like Kibler et al. (2015), and organizational sense-making and performance like Carrington and Tayles (2011); but there is no study on the topic of the current research, which is to identify the effect of the relationship between routine redesigning, legitimacy and functional affordance of sustainable accounting practices. Despite this, managers should refrain from merely adopting the results of this study for continuous routine redesigning, mainly because pre-studies results proved that organizational routine is a prominent type of organizational factors that assist in increasing sustainable practices (Elg et al., 2017). There are increased stresses on organizations to improve their environmental performance, and commercial media have been continuously publishing and categorizing the names of green companies and those that are not.

Organizations thus address environmental concerns through exclusively relying on organizational changes and they are concerned about obtaining a legitimacy in addition to increasing their human resources abilities and skills through achieving functional affordance for human resources to facilitate their environmental performance (Bapuji et al., 2018). However, we carefully offer these ideas as there is a need for more direct central interventions. Our results indicate the existence of organizational improvements represented by redesigning rules and procedures to achieve legitimacy for the organization in addition to the cognitive aspect, which will facilitate the efficiency of these interventions. Thus, as a result of the current work, the current study suggests that the Iraqi private-sector companies should exert more efforts to develop human resources in order to increase the ability to achieve sustainable accounting practice by reducing costs and eventually supporting economic development.

Moreover, organizations differ in realizing the market and technology, and some are more innovative because organizational sense-making is related to several organizational processes. Strategic cognitive work models, in general, are based on the assumption that the rational thought is closely related to the selected procedures and has become very important for organization as it is linked to reducing uncertainty, which constitutes the primary factor in organizational attitudes. Sense-making has become more central and intertwined in organizational concepts and theories, as senses and organization complete each other and organization emerges from a continuous process that is organized by people to understand the unclear inputs and bringing this sense back into the world to make it more organized Despite this sense-making, there are still some unresolved disputes regarding the concept, which suggest that the occurrence of sense on daily or instantaneous base in addition to its linkage to future may occur in the future.

The company’s knowledge-based climate should be developed in order to achieve a greater understanding of the situation and ultimately to contribute to performance enhancement. These efforts will assist entrepreneurs to invest more, and operating companies in Iraq will increase, which will lead to societal contributions and elimination of suffering brought by unemployment. This will also reduce costs, which in turn represents a motive for companies to increase their environmental responsibility towards society.

Limitations and Future Research

This study is merely a step forward in providing insight into how to encourage sustainable work practices. Due to the increased and various problems on environmental destruction, there is an urgent need for conducting more research.

First, among our suggestions for future research is the model generalization test and the results are indicated in Figure 1. In addition to environmental differences within cultural and organizational environments that vary in their influence on companies in different countries, research indicates that environmental beliefs, knowledge and situations vary across the world. Such differences may enhance or hinder organizational sense-making as shown in Figure 1.

Second, another limitation of the study is the fact that it relied on one single respondent from each company and thus bias data were questionable as there were more opportunities for the socially desired responses and not only honest feelings and opinions. However, this approach for data collection was utilized in many types of research. Besides, this study was limited to oil, communication, and construction companies operating in Iraq, with other significant companies excluded.

Third, the current study offered contributions regarding the influence of routine redesigning, legitimacy, and functional affordance through organizational sense-making, where the extent of sustainable accounting practices was identified in operating companies in Iraq. However, outstanding questions remain unanswered and underexplored (e.g., what is the influence of the properties of the executive manager on sustainable work practices among work groups? Moreover, do properties of other managers interact with those of working individuals in the same group in influencing sustainable practices?) With this, it is hoped that future studies will seek and address answers for such questions.

Fourth, we encourage future research to examine our results using other scales; for instance, our scales for organizational sense-making and sustainable accounting practices had a relatively limited scope, so there is a need for more large scales for sustainable accounting practices in order to improve the possible visions through future research.

Conclusion

On a final note, during our investigation of the influence of routine redesigning, legitimacy and functional affordance on sustainable accounting practices, we found that organizations should reconsider and review rules, procedures and conformance with environmental expectations by adopting structures and processes that satisfy stakeholders. They should also ensure workers’ goal-directed tasks through achieving confirmation with the user’s understanding of ambiguous issues or events. In turn, this represents a path that transforms ambiguous processes towards knowledge-based realities, and this is desirable in order to improve performance and achieve sustainable accounting practices by reducing costs. Managers should, therefore, work on these lines along with developing the organizational sense-making. Today’s private-sector companies are the backbone of the economy. In the same way, the private sector in Iraq needs to thrive by exerting efforts to develop a better workforce that can bring prosperity to Iraqi companies, leading to better economic performance.

Appendix A

Questionnaire

Gender: Male/Female

Footnotes

Acknowledgements

The authors would like to direct special thanks to the referees for their useful comments and suggestions to improve the quality of this article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.