Abstract

Productive employment and decent work are the key elements for achieving fair globalization and poverty reduction as indicated in the International Labour Organization (ILO) Decent work agenda. The ILO adopted core labour standards to examine the labour practices all over the world, with the aim of making a balance between procedural justice and social rights. Further, Global Reporting Initiative (GRI) framework provides guidelines for reporting labour practices and decent work (LA) performance in the sustainability reporting framework. The purpose of this study is to contribute to the empirical literature by providing information about quantity and quality of disclosure on LA of four Asian countries, namely Japan, South Korea, India and Indonesia, during the period 2009–2017. Using content analysis based on GRI framework, this study finds that Japanese firms disclose more information relating to quantity and quality of LA. On the other hand, firms from Indonesia disclose least information on LA in the annual reports as compared to others. Further, the gap between quantity and quality of LA disclosure is found to be the highest in Indonesia followed by India and South Korea. Regarding the components, our results indicate that firms from Indonesia and India provide less information about the quality aspects of ‘equal remuneration for women and men’ and ‘training and education’. On the other hand, the average quality disclosure on ‘diversity and equal opportunity’ is relatively less for all the four countries. However, our results of quantile regression reveal that the positive impact of LA performance increases as we move from the lower quantile to the upper quantile of corporate financial performance. However, we find insignificant impact of LA on financial performance of firms from Indonesia.

Keywords

Introduction

This article examines the disclosure of labour practices and decent work (LA) performance of some select non-financial firms operating from four Asian countries, namely Japan, South Korea, India and Indonesia, based on the Global reporting Initiative (GRI) guidelines. Workforce of a company is viewed as a ‘primary stakeholder’ (Freeman, 1984; Donaldson & Preston, 1995) and the companies that consider high degree of ethical behaviour towards employees are regarded as more socially responsible firms (Cohen, Taylor, & Muller-Camen, 2012; Parsa, Roper, Muller-Camen, & Szigetvari, 2018). Extant literature indicates that efficient management of human resources is the crux for creating source of competitive advantages and enhancing firm performance (Porter, 1985; Begin, 1991; Jackson & Schuler, 1995). The concern for workers’ welfare of a company, which was regarded as philanthropic in the nineteenth century was suppressed by more instrumentalist concerns about satisfying institutionalised forms of employee interest through collective bargaining (Parsa et al., 2018, p. 48). However, it is difficult for firms to maintain standardized labour-related practice in the absence of proper regulation and enforcement mechanism to protect workers’ rights and this is more pronounced in the case of developing economies as compared to developed economies (Crane & Matten, 2010).

The International Labour Organization (ILO) adopted core labour standards in 1998 to examine the labour practices all over the world. The objective of this standard is to create a balance between procedural justice and social rights (Alston, 2005), which is popularly known as decent work agenda. United Nation’s Sustainable Development Goals 2030 also give proper importance relating to decent work for all men and women. In the present economy, knowledge-based resources or intellectual capital (IC) are the crux for creating firms’ value and are replacing the traditional physical and financial resources (Ghosh & Maji, 2015). In the empirical literature, human capital, comprising knowledge, skill, experience, talent and effectiveness of employees of an organization, is regarded as the heart of creating intellectual resources and plays a dominant role in improving firm performance (Chen, Cheng, & Hawang, 2005; Maji & Goswami, 2016). Given the importance of intellectual resources for enhancing firm performance, several initiatives have been undertaken to disclose intellectual resources including human resources around the globe. Some of the notable guidelines are framework of Guthrie and Petty (2000), Bontis (2003), International Symposium on Measuring and Reporting Intellectual Capital co-sponsored by Organisation for Economic Co-operation and Development (OECD) (1999), Danish Agency for Trade and Industry (1998) and Work Life 2000 (1998). Empirically, researchers have observed a positive influence of IC disclosure on firm value (Orens, Aerts, & Lybaert, 2009; Anam, Fatima, & Majdi, 2011; Maji & Goswami, 2018). However, this dimension of research is associated with human capital, organizational capital and relation capital, and it provides less importance on the LA indicators of workforce.

A notable improvement in the field of labour practices is seen after the publication of GRI guidelines in 2000 encompassing economic, social and environmental responsibilities of firms. GRI is the most popular framework worldwide for reporting corporate sustainability and its three dimensions. Employing GRI guidelines, a plethora of empirical evidences shed light on the positive impact of corporate sustainability on firm performance (Lo & Sheu, 2007; Artiach, Lee, Nelson, & Walker, 2010; Hussain, 2015; Ortas, Gallego-Alvarez, & Etxeberria, 2015; Laskar & Maji, 2018); corporate social responsibility on performance (Stahle, Stahle, & Aho, 2011; Ahamed, Almsafir, & Arkan Walid, 2014; Laskar & Maji, 2016); and corporate environmental performance on firm performance (Plumlee, Brown, & Marshall, 2015). Extant literature indicates that by providing information relating to social and environmental responsibility, firms can build sound sustainable relationship with the stakeholders, can reduce the social risk by satisfying the ‘voice of society’, can attract socially responsible investor and can utilize inimitable and non-substitutable resources more efficiently, which ultimately enhances firms’ market value.

A myriad of empirical evidences support the positive influence of corporate social disclosure on market performance of firms. For instance, Preston and O’Bannon (1997) observed the positive impact of corporate social disclosure on financial performance of large USA firms. Likewise, Choi, Kwak, & Choe (2010) found a positive association between disclosure of corporate social responsibility and performance of South Korean firms. In India also, Gautam and Singh (2010) and Laskar and Maji (2016) observed a positive association between social reporting and firm performance. Similarly, the study of Ahamed et al. (2014) in the context of Malaysia concluded that firms can improve financial performance by disclosing more social-related information. However, a study conducted by Nag and Bhattacharyya (2016) on corporate social responsibility (CSR) reporting in India found an insignificant association between CSR reporting and financial performance in the short run. In another study, Morhardt (2009) observed that about 97 per cent of the large companies reported social information in the published report, which indicates the importance of social reporting by large firms. LA performance is an important integral part of CSR. By disclosing information about LA performance to the outsiders, firms can signal their competitive positions to the market and fulfil the societal expectations. It can, thus, be argued that by disclosing more information about LA in the published reports, firms may enhance their financial performance. Hence, a positive association between disclosure of LA and firms’ financial performance can be hypothesized. However, empirical evidence, exclusively on LA performance of firms, is scanty in the existing literature.

Against this backdrop, this article aims:

To study the disclosure pattern of LA performance indicators of select companies from four Asian countries and To investigate the impact of LA on firms’ financial performance.

Recently, a few studies focus on the human aspects of CSR (Brown, Tower, & Taplin, 2005; Branco & Rodrigues, 2009; Cahaya, Porter, Tower, & Brown, 2011; Dominguez, 2011). However, these studies concentrate on labour practices in a specific context and they use annual reports as the source of labour disclosure. The present study differs from the earlier as it provides information about the LA practices of four Asian countries, using sustainability reports as the basis. Further, earlier researchers used mean regression in a cross section or panel data set-up to estimate the impact of labour practice on firm performance, which provides only an average or partial view of the association as it specifies the conditional mean functions given a set of covariates. In this study, we use quantile regression, which is a location model that intends to obtain a complete picture of functional relations between variables for all portions of a probability distribution by describing how the conditional distribution of response variable depends on a set of covariates.

The rest of the article is organized as follows: the second section deals with disclosure pattern on LA, while the third section is devoted to the association between disclosure of LA and corporate financial performance; concluding remarks are presented in the fourth section.

Disclosure Pattern of LA

Sample and Study Period

The survey reports of KPMG (2013) and Carrots and Stick (2013) indicate that corporate sustainability practice is in a much advanced stage in the USA, Australia, the UK and other European countries. On the other hand, in the Asian context, the concept is well developed in Japan and South Korea, while it is in emerging stage in case of India, China, Indonesia and Malaysia. In this study, we have selected four Asian countries; of them two (Japan and South Korea) are advanced in publishing sustainability reports, while the other two (India and Indonesia) are in the emerging stage. 1

Initially, we selected other countries like China, Malaysia and Singapore based on the report of KPMG and Carrots and Stick (2013). However, due to non-availability of sustainability report of many companies over the period, we excluded these countries from the study.

The sample for this study consists of all listed non-financial firms who have been publishing sustainability reports or social responsibility reports in their respective websites in English language, continuously since 2009. Based on the above criteria, the sample of this study consists of 114 companies from Asia, comprising 36 companies from Japan, 29 from South Korea, 28 from India and 21 from Indonesia. The study period was 9 years (2008–2009 to 2016–2017). The first year 2008–2009 is considered in this study as the survey report of KPMG (2013) indicates that some Asian countries like India and Indonesia have started sustainability reporting from 2009 onwards.

Measurement of LA Disclosure

We use content analysis technique to compute the disclosure score of LA. It is a widely used research technique in the empirical literature to convert qualitative information into quantitative form by extracting relevant information from the published documents (Guthrie & Parker, 1990; Guthrie & Petty, 2000; Brennan, 2001; Abeysekera & Guthrie, 2005; Laskar & Maji, 2016). Three aspects are very important in content analysis—source of information, content of analysis and unit of analysis (i.e., basis of coding) (Guthrie & Parker, 1990; Guthrie & Petty, 2000). In this study, published sustainability report or social responsibility report is the source of information. GRI framework is used as the basis for content of analysis as it is widely used in the empirical research (Brown, De Jong, & Levy, 2009; Marimon, Alonso-Almeida, Rodriguez, & Cortez, 2012). Finally, we adopt uniform coding system to enhance reliability of the content analysis as suggested by Guthrie, Petty, and Yongvanich (2004). Earlier, researchers used sentences (Deegan & Gordon, 1996; Gray, Kouhy & Lavers, 1995), paragraphs (Guthrie, Petty, & Yongvanich, 2004), portions of pages (Unerman, 2000) and words (Zeghal & Ahmed, 1990) as the basis of coding. However, in recent times, the empirical literature on computing disclosure score can be divided into two streams: one uses the binary coding system (‘0’ for absence and ‘1’ for presence) (Jones, Frost, Loftus, & Van Der Laan, 2007; Burhan & Rahmanti, 2012; Hussain, 2015), while the second group places emphasis on scale (Shareef & Davey, 2005; Wang, Sharma, & Howard, 2016).

Following the recent empirical literature, we use both the binary coding system (i.e. 0 and 1) and a four-point scale (0 to 3) for computing LA disclosure score. While the binary coding system, that is, score of ‘1’ is given if the information is disclosed and ‘0’ if the information is not disclosed, is used to get quantity of LA disclosure, a four-point scale is used to obtain quality of disclosure score. Some researchers (Shareef & Davey, 2005; Wang et al. 2016) give maximum score if an item can be described in numerical form and lower score if only description is given. However, there are several items in LA disclosure that cannot be expressed in numerical terms. For instance, in case of ‘programs for skills management and lifelong learning that support the continued employability of employees and assist them in managing career endings’ (LA 10) the description of programmes is more important than merely the numbers. The same is true in case of LA 15 (significant and actual potential negative impacts for labour practices in the supply chain and action taken). Hence, the qualitative information or information relating to non-financial aspects is also essential for investors and other stakeholders. In this regard, allotting maximum scores to only financial information or quantitative information cannot be pondered to be an appropriate methodology of scoring. In this respect, Marston and Shrives (1991) argued that a number cannot be considered to be worth more than a comment. Similarly, Botosan (1997) states qualitative information is more useful as compared to quantitative information. Further, all the items of LA as per GRI framework can be subdivided. Hence, we assign the code as ‘1’ if the GRI specified item is partly disclosed in the published report, ‘2’ if the item is fully disclosed in descriptive form and ‘3’ for quantitative form or in terms of preciseness and clarity. 2

If any item in the GRI framework can be expressed in numerical terms, we assign code ‘3’. When it cannot be expressed in quantities form, we emphasises on the clarity and preciseness of the description to assign code ‘3’.

After obtaining the item-wise score based on quantity and quality, total disclosure score for LA and its components are computed by employing the following formula:

where, Nj is the maximum score for each category (or overall), j is the company, i is the items and t is the time. Xijt assumes the code 1 and 0 only for the quantity of LA disclosure. In the case of assessment of the disclosure quality, Xijt assumes the code 0–3. Here, the maximum score is computed by multiplying the number of items with 1 for quantity and with 3 for quality. Initially, we compute the score for each item for each year of a particular company. Finally, to compute the average score for a particular year with respect to a country, we use simple arithmetic mean.

Quantity and Quality of LA Disclosure Practices

Figure 1 shows the movement of average LA disclosure (quantity) of sample firms from four Asian countries for the period 2009–2017. We use arithmetic mean of the computed disclosure score of all firms in a year for computing average disclosure score over the years. A cursory look into the figure reveals upward movement of the quantity of LA disclosure for all the countries over the years during the study period. For instance, quantity of LA disclosure has increased from 0.918 in 2009 to 0.954 in 2017 in case of Japan, about 0.804 in 2009 to 0.928 in 2017 in case of South Korea and India, and 0.745 in 2009 to 0.818 for Indonesia. It is important to note here that in the case of Indonesia, disclosure score shows an increasing trend from 2009 to 2012 and slightly declines thereafter. Indeed, prior to 2012, publication of sustainability or social responsibility report was voluntary for Indonesian firms. However, after 2012, the Indonesian government made it compulsory to disclose their sustainability-related activities as a part of annual report, which limits the scope of disclosing all information as mentioned in the GRI framework. We find no notable difference in terms of quantity of LA disclosure in case of South Korea and India over the years. However, average disclosure score in case of Japan is found to be higher than the other three countries throughout the study period.

Figure 2 shows the quality of disclosure score of LA over the years. Like the quantity of LA disclosure, an upward movement of Quality disclosure of LA is noticed for all the cases except Indonesia. In this respect, also the disclosure score of Japan is higher than others over the years. Interestingly, unlike quantity disclosure, a considerable difference is noticed regarding quality of LA disclosure between Indian and South Korea over the years. This implies that Indian firms provide information, but the objectivity of that information is relatively less. However, at the end of 2017, the observed gap is relatively less. On the other hand, observed disclosure score (quality) is considerably less for Indonesian firms and the gap widens over the years. This clearly indicates the lack of objectivity in the disclosure of LA for Indonesian firms.

In order to obtain a clear picture about the gap between quantity and quality of LA disclosure over the years, we plot the values of each country separately in Figures 3–6, respectively, for Japan, South Korea, India and Indonesia. Figure 3 shows that the gap is negligible over the periods in case of Japan. This indicates that companies are providing quality information of LA to the stakeholders to facilitate proper decision making. The observed gap is also very less in case of South Korea over the years, specifically after 2014. On the other hand, in the Indian context, the gap is more pronounced when compared to Japan and South Korea. Although some improvement has been noticed in recent times, still there is much scope to reduce the gap and provide more objective information, regarding LA practices, to the stakeholders. On the contrary, a considerable gap between quantity and quality of LA disclosure is noticed in case of firms selected from Indonesia, while the gap has remained stable over the years.

Now, we look at the disclosure patterns of the components of LA. In the GRI framework, total items relating to LA are sub-divided into eight indicators. Table 1 represents the quantity and quality of average disclosure score with respect to each indicator of LA. As observed earlier, quantity and quality of disclosure score for all the components are higher in Japan as compared to other three countries. The results also indicate that although quantity of disclosure score is quite satisfactory for most of the cases, the quality of disclosure is found to be relatively very less for some components, specifically in case of India and Indonesia. For instance, only 55 per cent and 60 per cent of the firms from Indonesia and India, respectively, are disclosing the ratio of basic salary and remuneration of women and men by employee category and by different locations of operations. On the other hand, more than 80 per cent of Japanese and South Korean firms are disclosing such information in numerical terms. Likewise, only 55.6 per cent and 70.5 per cent of the firms from Indonesia and India, respectively, disclose information relating to training and development in terms of quality, while such score is considerably higher (90% or more) in case of South Korea and Japan. Indeed, very less number of firms from Indonesia and India provide numerical information about average hours of training per employee by gender and employee category. Similarly, firms are providing overall percentage of employees receiving regular performance and career development, but such information according to gender and employee category are very less. It is also imperative to note that only 55 per cent and 60 per cent of Indonesian firms disclose quality information with respect to employment category and occupational health and safety category. However, in case of diversity and equal opportunity, the quality of disclosure is relatively less for all the four countries. For other components, the disclosure of information is satisfactory.

Disclosure of LA and Corporate Financial Performance

Variables

Disclosure Score Relating to Different Components of LA

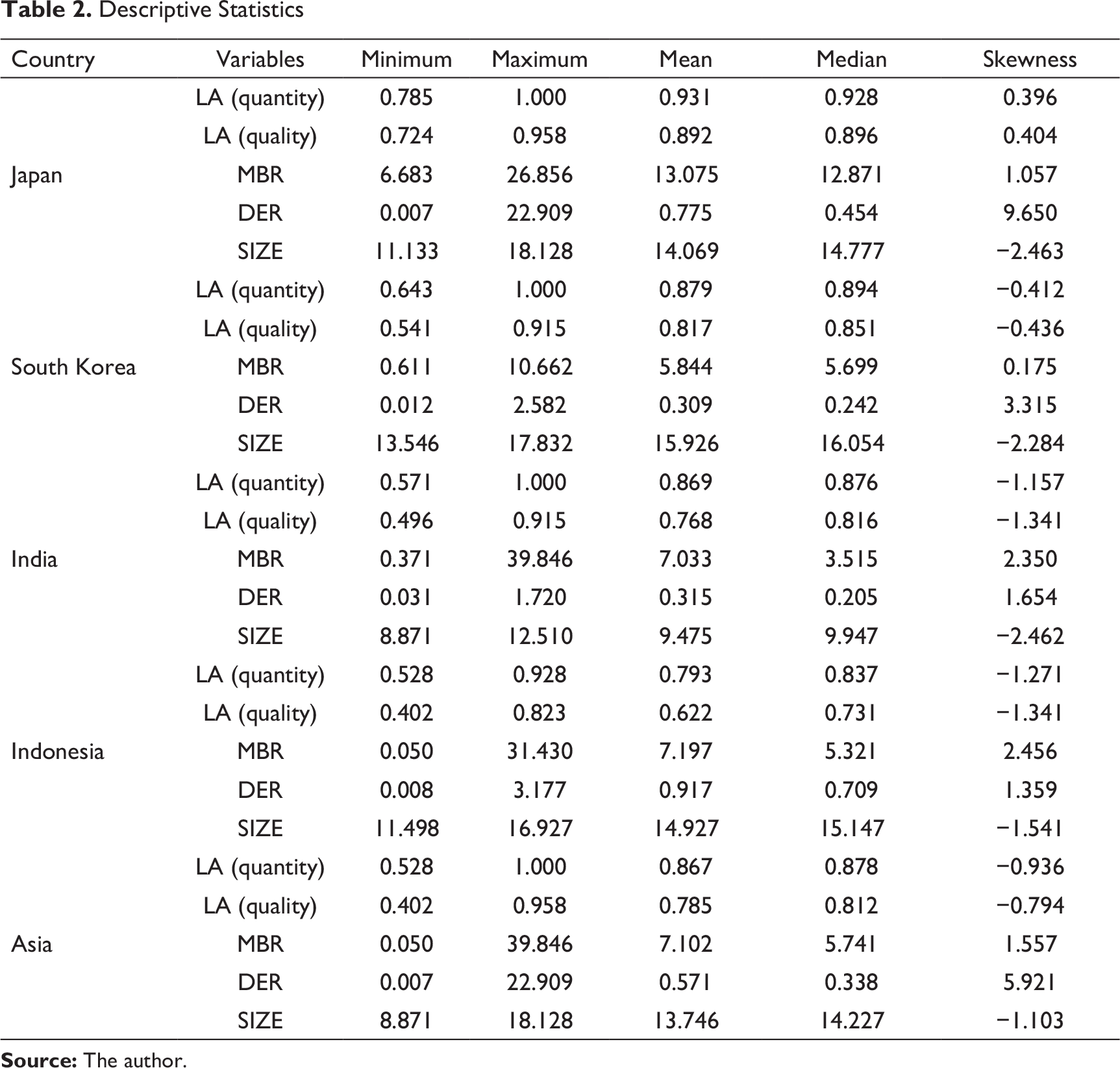

Descriptive Statistics

We compute univariate descriptive and robust statistics containing minimum, maximum, mean, median and skewness for all the variables under study and the results are shown in Table 2. As observed earlier, the average disclosure score both in terms of quality and quantity is higher in case of Japan as compared to other countries. While the mean difference between quantity and quality of LA disclosure is found to be approximately 4 per cent in case of Japan, it is about 6 per cent in South Korea. However, the difference is about 11 per cent in case of India followed by Indonesia (about 17%). The observed mean values of LA disclosure for all the countries during the year corroborate our findings as discussed in section ‘Disclosure Pattern of LA’. Regarding the distribution of the variable, the values of skewness show that the distribution of both quantity and quality of LA disclosure is not much skewed. Nevertheless, except in case of South Korea, the distribution of MBR is highly skewed. This indicates that the assumption of normality of the dependent variable is not tenable, barring South Korea in our study. Further, the mean value of MBR for firms from Japan is considerably higher than that of the other three countries. In case of debt–equity ratio (DER), the distribution is positively skewed for all the cases and the share of debt is relatively more for firms from Japan and Indonesia as compared to India and South Korea. On the contrary, firm size is negatively skewed, indicating the existence of firms with low sales. Thus, the results of descriptive statistics indicate that barring a few cases, the assumption of normality of variables under study is not tenable.

Descriptive Statistics

The Model

In the empirical literature on social responsibility, most of the researchers have used pooled ordinary least square (OLS) model or panel data regression model based on the assumption of normality. However, the dogma of normality, according to Hubber (1964), is largely attributable to a kind of wishful thinking. Indeed, there may exist nonlinear, or for that matter—biased, estimators superior to least squares for the non-Gaussian linear model is a well kept secret in most of the econometric literature (Koenker & Bassett, 1978, p. 35). It can, thus, be argued that if the distribution of the response variable is substantially skewed, we expect heterogeneity in the effect of study covariates in general, and at least at the extreme tails of the response distribution, in particular. Hence, if the distribution of the response variable is asymmetric and substantially non-normal, mean regression may not be useful to capture the differential effects of the potential covariates along the quantiles of the response distribution. In this study, we observe that in most of the cases, the distribution of variables is skewed. Hence, the use of classical linear regression model based on conditional mean may provide a biased view of the relationship. Further, the mean regression may provide only a partial view of the relationship, as it is a useful tool for summarizing the average relationship between the outcome variable of interest and a set of regressors, based on the conditional mean function

Assuming that the conditional quantile function is unique and that it is linear, a linear quantile regression specifies the conditional τ-quantile

Where Xji is the ith observation for regressor j = 1, …, k;

The specific quantile regression used in the present context is:

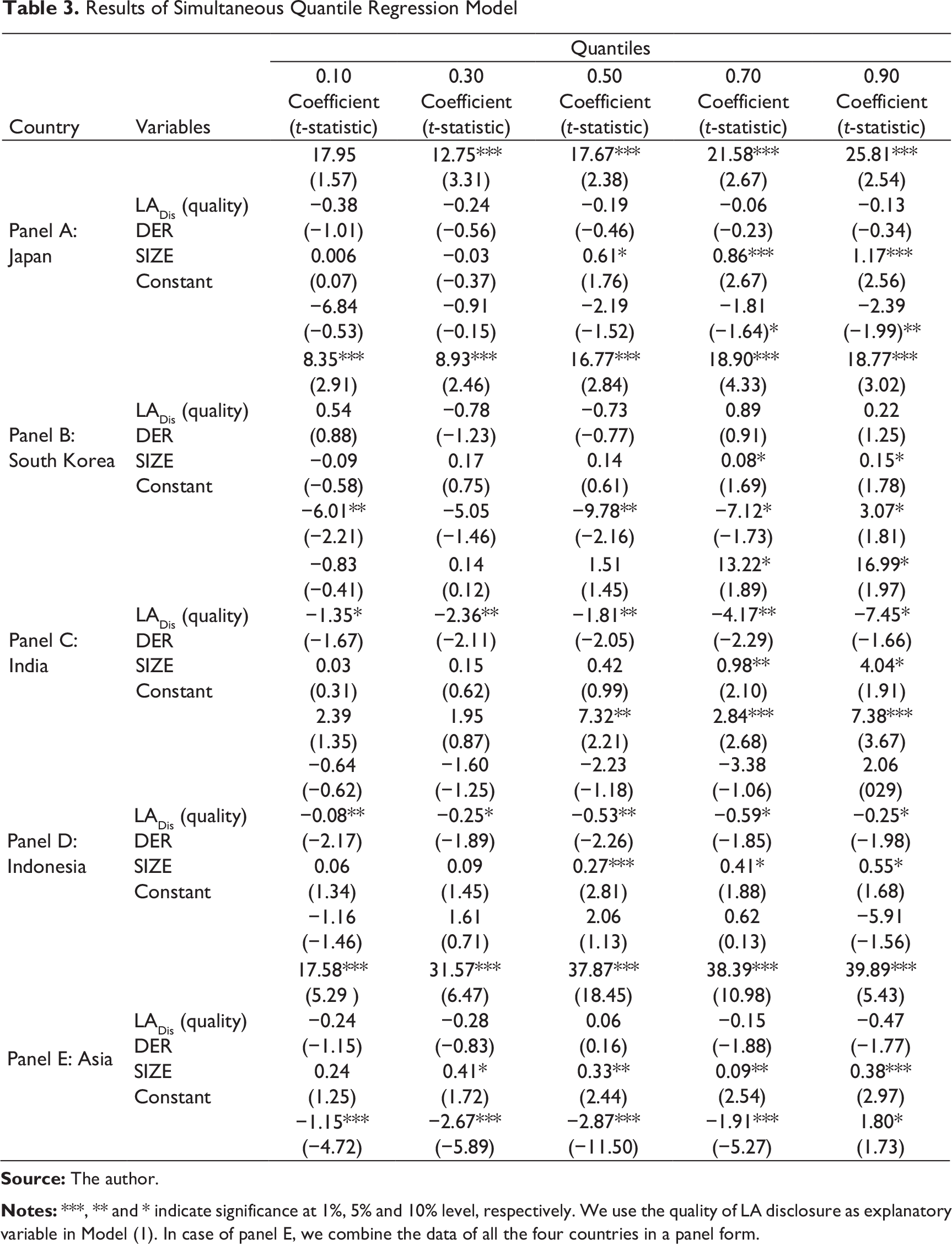

Results of Quantile Regression

Results of Simultaneous Quantile Regression Model

Further, the observed gap between quality and quantity of LA disclosure is found to be quite high in Indonesia as compared to other countries. The results, thus, corroborate that LA disclosure is a crucial factor for enhancing firm performance, but depends upon the efficiency of firms in utilizing human resources and disclosing the practice to the outsiders in order to create a positive signal in the market. The result of the present study is consistent with the findings of Cahaya et al. (2011), where the researchers empirically observe that the concern for labour disclosure is very less and the Indonesian companies are not clearly communicating labour responsibility to the external users to create a positive impact on firm performance. Finally, in case of Asia (panel E), the outcome of simultaneous quantile regression indicates that the impact of LA is positive and significant at all quantiles and the coefficients show an increasing trend as we move from the lower quantile to the upper quantile. This implies that LA disclosure plays a vital role in enhancing corporate financial performance and also segregating firms into out-performing and non-performing firms.

We find a positive impact of firm size on MBR, barring a few cases. This is true for each country as well as for the combined data; but, the results are significant at upper quantiles. This implies that large firms possess certain inherent advantages to acquire greater amount of financial resources and to use the economics of scale that helps to improve financial performance. On the other hand, the impact of DER is found to be insignificant for all the cases in case of Japan and South Korea. Nevertheless, in case of India and Indonesia, such association is found to be negative and significant. The negative impact of DER on firm performance advocates in favour of packing order hypothesis; but, for the combined data, no significant association between DER and MBR is observed.

Conclusion and Policy Implications

In an attempt to examine the disclosure pattern on LA of corporate firms from four Asian countries, this study finds that Japanese firms disclose more information relating to quantity and quality of LA. On the other hand, firms from Indonesia disclose least information on LA in the annual reports as compared to others. Further, the gap between quantity and quality of LA disclosure is found to be the highest in Indonesia followed by India and South Korea. However, it is the least among Japanese firms. The findings of the present study are consistent with the outcome of Laskar and Maji (2018), where the researchers observed similar results with respect to disclosure of corporate sustainability performance. Regarding the components of LA disclosure, we observe that firms from Indonesia and India provide less information about the quality aspects of ‘equal remuneration for women and men’ and ‘training and education’. On the other hand, the average quality disclosure on ‘diversity and equal opportunity’ is relatively less for all the four countries. In case of firms from Indonesia, Cahaya et al. (2011) also observed similar results and argued that the concern for labour disclosure is less for Indonesian companies. Thus, the present effort, along with earlier studies, indicates that there is a need to enhance the quality of disclosure about LA, specifically in case of India and Indonesia. It also provides a scope for further research, incorporating the labour laws in the respective countries, as a basis for analysing the causes of low disclosure of LA.

Finally, based on the outcome of quantile regression, our results indicate significant positive impact of LA disclosure on corporate financial performance, which is more pronounced at the upper quantiles of firm performance in case of Japan and South Korea. On the contrary, an insignificant association is found in case of Indonesia, which implies the inefficiency of firms in disclosing quality of LA practices. In case of India, the observed association is found to be positive only at the upper tails of the distribution. Earlier researchers (Stahle et al., 2011; Ahamed et al., 2014; Laskar & Maji, 2016) observed a positive association between CSR and firm performance. However, this study is exclusively on the disclosure of LA on firm performance. Further, unlike mean regression, the outcome of this study clearly indicates that the impact of LA disclosure of financial performance varies at different locations of the conditional distribution of firm performance.

The present effort is useful for policy implications. First, the outcome of the study indicates that by disclosing quality information about LA, a firm can improve financial performance. Hence, firms should disclosure more information on LA to provide positive signal to the market. Second, disclosure of LA plays a crucial role in segregating firms between out-performing and non-performing, ceteris paribus. Hence, firms should try to disclose more information on LA to achieve sustainable competitive advantages in the market. In this respect, special attention should be given to disclose numerical information about ‘salary and remuneration of women to men by employee category and by significant locations of operation’, information about various aspects ‘training and education’ in numerical terms and objective information on ‘diversity and equal opportunity’. Third, the observed gap between quality and quantity of LA disclosure, specifically in the context of Indonesia and India, advocates the need of the firms to disclosure more quality information in order to enhance their market value. Lastly, corporate sector cannot thrive in a world of poverty, inequality, unrest and environmental stress. Hence, it is the vital responsibility of every corporate firm to ensure the fulfilment of 2030 Agenda on Sustainable Development Goals (SDGs). Companies should provide quality of LA disclosure to the stakeholders to demonstrate their commitment towards the SDGs of gender equality (goal 5) and decent work and economic growth (goal 8). In this respect, further studies can be undertaken to link the disclosure of corporate sustainability and the SDGs.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.