Abstract

This study examines how stock market sentiment in a Gulf Cooperation Council (GCC) stock market may spill over to affect sentiments in other markets in the region. Findings from dynamic conditional correlation models in a generalized autoregressive conditional heteroscedasticity (GARCH) framework, traditional Granger causality test and impulse response functions suggest that Kuwait and Qatar stock markets are segregated from other markets in the region. Saudi Arabia and the United Arab Emirates (UAE) markets are well integrated, and any shift in sentiment in either of the two affects the other. Bahrain and Oman are somewhat integrated with the UAE and Saudi stock market sentiments. Thus, when an investor has significant investments in both Saudi Arabia and the UAE, he must be aware of any contagion effect—especially in the case of a stock market panic.

Keywords

Introduction

Investors’ sentiment is their overall psychological attitude towards the financial market. In traditional finance theory, investor sentiment has no role in determining stock prices. But the idea of sentiment’s impact on stock returns is not new. For example, Black (1986) explains how market sentiment may influence noise traders to act irrationally. In two seminal studies, Baker and Wurgler (2006, 2007) show that sentiment is present in investors’ belief about a firm’s future cash flows and returns, which cannot be justified by the real facts they currently have in their hands. This article investigates: (a) the presence of stock market sentiment spillover among the Gulf Cooperation Council (GCC) stock markets; (b) the direction of sentiment spillover; and (c) the duration of spillover effect in case of any shock to sentiment. Empirical results of this study suggest that the Kuwait and Qatar stock market sentiments behave independently of other GCC markets’ sentiments. The stock market sentiments of Saudi Arabia and the United Arab Emirates (UAE) are significantly correlated and bi-directional, suggesting possible spillover of euphoria or panic between these two markets. Bahrain and Oman—the two smallest markets in the GCC—are weakly integrated with the UAE and Saudi market as far as sentiment is concerned.

The traditional view of finance suggests that arbitragers should be able to intervene in the market in time to drive away any mispricing. However, De Long et al. (1990) point out that arbitragers cannot influence stock price to go back to its fundamental value when noise traders create additional risk through their irrational behaviour. This finding is also supported by Ofek et al. (2004), Schmeling (2007) and Dumas et al. (2005). Baker and Wurgler (2007) reconfirm the previous conclusion by showing that those stocks that are most affected by sentiment are the ones most difficult to arbitrage. Stambaugh et al. (2012) are of the opinion that sentiment should be considered as an important market-wide risk factor. Hence, the risk that arises because of investor sentiment can be treated as undiversifiable market risk.

The initial evidence of market sentiment was in the context of developed markets. The presence and effects of sentiment on stock prices may be different for emerging and mature markets, because these two types of markets act dissimilarly in many ways. Studies show that the actions of an Asian and a Western investor may be different, which are related to perception (Ishii et al., 2009), process of reasoning (Buchtel & Norenzayan, 2008) and style of thinking (Nisbett & Masuda 2003). Thus, the effect of culture—which also belongs to investor psychology—on stock markets cannot be disregarded. Moreover, in comparison to mature markets, emerging and frontier markets are characterized by the presence of relatively low liquidity, infrequent trading, less-informed retail traders and limited access to reliable information (Hassan et al., 2003).

Several studies on emerging markets also report the presence of sentiment. For example, among many others, Chi et al. (2012) and Guo et al. (2017) report that investor sentiment has a strong impact on the Chinese stock market. The presence of sentiment in the Indian stock market has been detected by Jana (2016) and Dash and Maitra (2018). Sentiment–returns relationship in the Taiwan stock market is evident from the study by Chi et al. (2012). Rehman (2013) provides provides empirical evidence that stock returns of the retail-investor-dominated Karachi Stock Exchange are influenced by market sentiment. The findings of Anusakumar et al. (2012) indicate the presence of sentiment in the Asian emerging markets, and their result is valid across firms with respect to firm size, volume of trade, study period and proxy selection. Doukas and Milonas (2004) and Grigaliūnienė and Cibulskienė (2010) find an inverse relationship between stock market sentiment and future stock returns in the Greek and Scandinavian markets, respectively.

Although sentiment is recognized as a very important factor influencing stock returns around the world, only a few studies have examined this issue for the GCC stock markets. Altuwaijri (2016) predicts a positive relationship between sentiment and aggregate market returns. Białkowski et al. (2012) show that Ramadan (a month of fasting) exerts a significant positive impact on investor sentiment in 14 Muslim countries. Seyyed et al. (2005) have earlier reported a similar effect of Ramadan on the Saudi stock returns. Wasiuzzaman (2017) and Abbes and Abdelhédi-Zouch (2015) also provide evidence that the Hajj (annual Muslim pilgrimage)—through its impact on investors’ sentiment—significantly influences the Saudi stock market.

In a nutshell, the GCC regional market—with a combined market capitalization of close to US $1 trillion—has failed to motivate international researchers, academicians and foreign investors to pursue adequate research. In December 2019, Saudi Aramco went public, which increased the total market capitalization of the GCC markets to approximately US $2.7 trillion. The partial opening up of the Saudi market to foreign investors and its partial approval of short selling, the upgradation of Qatar, the UAE and the Saudi market to emerging status have played an important role to attract foreign investors. Moreover, the all-out effort of respective governments to diversify their sources of revenues has led to make policy changes required to allure foreign investors. Now, as the market has become open to foreign investors, these investors definitely need to recognize this regional market more thoroughly. In this regard, research on the behavioural aspects of this regional market are of prime interest, mainly due to the strong presence of retail investors.

As discussed above, the impact of sentiment on stock returns has become an overwhelming factor for all the markets around the world. Sharmin (2019) provides evidence of a strong presence of sentiment–returns relationship in the GCC markets. Keeping this phenomenon in mind, this study focuses only on the behavioural aspect (i.e., sentiment) of these markets, and its influence on the stock prices is avoided. Since these markets have geographical proximity, share a similar culture and are dominated by retail traders, spillover of sentiment is of high importance to a potential foreign investor. In this backdrop, this study predominantly investigates the spillover behaviour of investor sentiment between the GCC stock markets.

This study is expected to have a strong implication for investors, policymakers and academicians. First, this study is unique in the sense that it primarily focuses on the behavioural aspect of the GCC stock markets by only considering the spillover of the sentiment of one market to that of another market. On the contrary, previous studies have considered the spillover effect of sentiment on stock returns. In other words, this study examines the spillover of the mental states of investors between markets. The knowledge on sentiment spillover is of high importance in order to invest during episodes of panic and euphoria. Second, this study will surely help foreign investors make better investment strategies. For example, an investor can achieve better diversification benefits through avoiding investing in the financial assets of a particular market if its sentiment is found to be strongly contagious with another market in the region.

Third, sentiment has important implications for regulators. A quantifiable measure of sentiment can help regulators and policymakers make appropriate and timely interventions and policy changes. Especially, the knowledge of sentiment spillover helps regulators and policy makers intervene in the market in time to safeguard it from potentially harmful contagious trading behaviour. It is understandable that in a region of contagious financial markets a policy decision for a market cannot be taken in isolation. Finally, this study uses dynamic conditional correlation models in a bi-variate generalized autoregressive conditional heteroscedasticity (GARCH) framework, traditional Granger causality test and impulse response functions from vector autoregression (VAR) to detect the presence of spillover of sentiment, the direction of spillover and the duration of (a shock to sentiment on) spillover, respectively. Thus, this kind of unique use of three techniques allows this study to capture the complete phenomenon of spillover effects of sentiment in the GCC markets.

The rest of the article is organized as follows: the second section provides a brief review of studies related to spillover of sentiment. The third section gives information about the data and methodology used to address the spillover of sentiment in the GCC stock markets. Empirical results are discussed in the fourth section. The fifth section concludes the article.

Literature Review: Spillover Effects of Sentiment

Extant empirical studies provide strong evidence of the significant effect of investor sentiment on the US market returns (Baker & Wurgler, 2006, 2007; Baker et al., 2012; Brown & Cliff, 2004; Saade, 2015). Most of the non-US sentiment-related research focuses on other developed markets. However, only a few studies examine the impact of sentiment on emerging markets (e.g., Canbaş & Kandir, 2009; Chowdhury et al., 2014; Kling & Gao, 2008; Lux, 2011; Sayim & Rahman, 2015; Schmeling, 2009; Siriopoulos & Fassas, 2012). These studies also report the presence of sentiment in emerging markets.

Investors’ investment behaviour and their response to risk may differ across markets, even if the market conditions are similar (Apartsin et al., 2013). The presence of sentiment may be linked to the degree of collectivism that the concerned country inherently possesses. Another important behavioural aspect of investors is related to individualism. It is a behavioural trait that guides traders to focus on their own inherent abilities and internal attributes to make trading decisions. Collectivism, on the other hand, is related to the society. In fact, it is the degree to which people tend to follow the behaviour of other investors in the community (Chui et al., 2010). In comparison to the United States, Hofstede (2001) classifies Mexico as a highly collectivistic society. The presence of such behavioural traits suggests that investors may pursue similar investment strategies, which may ultimately contribute to the formation of an overall sentiment of the market. Schmeling (2009) argues in favour of this by showing that the so-called inverse relationship between sentiment and subsequent returns is stronger for countries that are culturally vulnerable to herd-like behaviour.

Many studies in the literature have documented the contagious behaviour of market sentiment (Baker et al., 2012; Lee et al., 2014; Sayim & Rahman, 2015). For example, Sayim and Rahman (2015) find that the sentiment of the US institutional investors’ spillovers affect Turkish stock returns. This spillover effect is so robust that authors suggest that investors use sentiment as a systemic risk factor for the Turkish market, although these two markets are located in two different continents. Berg and Vu (2019) study the spillover of the US financial market volatility on 17 development markets’ real economic activities. Their findings show that the performances of these markets are more linked to the United States than to their own financial market.

Verma and Soydemir (2006) examine the impact of both US institutional and individual sentiments on the UK, Brazil, Chile and Mexico stock markets. They find various levels of contagious relationships. They conclude that the spillover relationship between the sentiments of these markets is dictated by the level of each country’s trade relationship with the USA. Heath and Kopchak (2015) provide further evidence on the strong relationship between the Mexican and US economies and financial markets. In addition, they document that Mexican stock returns are influenced more by the US monetary innovations during economic downturns than during expansions. Liston-Perez et al. (2018) suggest a positive dynamic relationship between the Mexican stock market sentiment and its returns. Their results also indicate that the spillover of the US sentiment affects Mexican stock market returns.

The results of Cheuathonghua et al. (2019) suggest the presence of stronger tail cross-dependences between the US sentiment and 31 equity market indexes at the highest quantile, displaying the presence of asymmetric reactions to sentiment innovations. They also report that the tail dependences between the US sentiment and other foreign markets are stronger in bullish periods than in bearish periods. Concetto and Ravazzolo (2019) investigate the strength of sentiment to forecast the US and the European Union stock market returns. Confirming previous findings, their results show a strong impact of sentiment on the US stock returns. However, for the European stock markets, the impact is relatively weak. As far as the direction of causality is concerned, a one-way spillover effect from the USA to Europe is observed.

For the South African stock market, Rupande et al. (2019) show that there are movements in overall risk attitude that are influenced by the volatility perceived by sentiment-affected noise traders who are careless market fundamentals. This study also shows that there is a significant connection between investor sentiment and stock return volatility, which implies that behavioural finance is able to explain the volatility as well as stock returns on the South African market. Abdelhédi-Zouch et al. (2015) examine the role of the US investor sentiment in amplifying the financial crisis of 2008 by considering the volatility spillover between S&P 500 returns and investor sentiment. The findings of the study show that the investor sentiment was able to magnify the impact of sub-prime financial crisis through intense spillover of volatility (due to swings in investor sentiment) to equity returns.

Some recent studies look into the spillover of sentiment on real economic activities. ZarBabal and Evans (2018) show the presence of a positive contemporaneous relationship between investor sentiment and contemporaneous non-durable spending, whereas the relationship between sentiment and future spending turns negative. Zheng and Osmer (2019) report that median priced houses’ returns are typically higher when the sentiment is down. They also find evidence of a strong return spillover effect that only persists within the real estate industry. Finally, dynamic conditional correlation models show that correlations between the stock market sentiment and housing returns rise during economic recessions.

Some studies focus on the international transmission of sentiment. Yarovaya et al. (2017) investigate the transmission of positive and negative returns and volatility shocks across nine developed and 11 emerging futures markets in a pair-wise manner. Their results suggest that there is an asymmetry in returns and volatility spillovers across markets. Rehman et al. (2017) examine the impact of the sentiments of Germany and Japan on those of Turkey and Pakistan. They observe a significant impact of sentiments of developed markets on those of young, emerging markets. El Abed et al. (2019) use a dynamic conditional correlation (DCC) framework which takes into account both long memory as well as time-varying correlation. Their findings exhibit a pattern of ups and downs in correlation during the occurrence of the Eurozone sovereign debt problems, suggesting the presence of spillover effect between the credit default swaps index and other financial instruments.

Data and Methodology

Data

There are seven stock markets in the GCC region. The markets are Abu Dhabi, Bahrain, Dubai, Kuwait, Oman, Qatar and Saudi Arabia. The UAE consists of two stock markets—Abu Dhabi and Dubai. In this study, both the markets are combined to form a single UAE stock market. So, this study has used six stock markets in the sample. The sample period for this study is from January 2004 to December 2017. Changes in sentiment may or may not be justifiable by existing facts. This study is interested in the latter—that is, when sentiment changes without any logical change in market fundamentals. Macroeconomic data—interest rates, industrial production, consumer price index and crude oil prices—are used to find residual (or unjustifiable) sentiment for each market. Monthly macroeconomic data for individual countries are collected from International Financial Statistics. Monthly oil prices data are collected from the website investing.com. DataStream provides monthly stock return index and other financial data necessary to create sentiment proxies.

As DataStream data are not clean (Ince & Porter, 2006), this study employs some caution while choosing and cleaning data. Since this study involves monthly data of six markets, the visual method is first applied to check for data integrity. Dead firms have been dropped from the sample. Cleaner data are preferred over the presence of survivorship bias. If any stock is not traded for more than 24 months, it is dropped from the sample, in order to avoid autocorrelation arising from non-synchronous trading. Some columns of ‘#ERROR’ are present in the raw dataset, which have also been deleted. Only equity is considered in the sample. Any observation that shows a monthly return over 300 per cent in absolute value is also deleted. However, only in a few cases has this study noticed such extreme values. Finally, every stock must possess returns data for at least 24 months.

The Construction of Sentiment Proxies

An overall sentiment index for each of the six GCC markets has been estimated from five indirect sentiment proxies. The first proxy is the number of IPOs per month. The second indicator for sentiment is the average trading volume. It is simply the arithmetic mean of logged individual firm’s value of shares traded. The third one is the aggregate market turnover. Turnover of an individual firm is computed as the total number of shares of a firm traded on the last trading day in a given month divided by the total number of shares outstanding on the same day. Overall market turnover is the aggregate of turnovers of individual firms on the last trading day of the month. The fourth measure is the moving average ratio, which is slightly tricky to estimate. First, it needs one to compute the 4-month moving average of every stock and then calculate how many companies’ shares are traded above and below their own 4-month moving average. Next, the ratio of these two is taken and then aggregated cross-section-wise to compute a monthly sentiment indicator for the market. The last proxy to be used is TRIN (Trading Index). TRIN is calculated as (DECVOLt/#DECt)/(ADVVOLt/#ADVt), which is basically the ratio of average volume of declining stocks to average volume of advancing stocks. This measure is considered to be one of the most widely used sentiment proxies in the finance literature.

The Construction of a Unified Sentiment Proxy

The effect of macroeconomic variables on the sentiment proxies has been taken out, and residual sentiment proxies are created using the following regression:

where SENTit is the sentiment of the market I in the GCC region and IP, INF, INT and OIL indicate monthly industrial production growth, inflation, interest rates and oil price growth rate, respectively. These error terms represent sentiment, which is not explained by macroeconomic factors or systematic risk. In other words, errors or residual sentiment proxies only exhibit the current irrational sentiments in the markets.

Finally, using principal component analysis (PCA), a unified (composite) sentiment index is constructed for each market that captures the common component in the five proxies. Since the first principal component explains reasonably well the sample variance, a single sentiment factor should capture much of the common variations. Baker and Wurglar (2007) describe how to construct a unified sentiment index for a stock market of interest. Thus, each of the GCC markets possesses a sentiment index. Therefore, the six markets in the GCC region have six separate sentiment indexes. This article tests the sentiment spillover from one market to another using these six sentiment indexes.

The Conditional Correlation Between Individual Stock Market Sentiments

In order to investigate the dynamic correlation among the sentiments of individual markets, this study uses the bi-variate GARCH model with a dynamic conditional correlation framework. It allows for dynamic volatility to be incorporated in the model to estimate dynamic correlation. Thus, it gives a better estimation of correlation coefficients. Pairwise (bi-variate) estimation provides the correlation structure between the sentiments of two markets that evolve through time. The GARCH-DCC model of Engle (2002) can be written as follows:

where

In the DCC framework, conditional correlation can be expressed as:

where

The Effect of Innovations in Market Sentiment on Other Markets’ Sentiments

The VAR framework is able to show how an innovation in sentiment in one of the markets is going to have an impact on the sentiment of other markets. The VAR framework to be used in this context can be expressed as follows:

where

The Granger Causality Between Individual Market Sentiments

Although Granger causality does not determine the causality between two variables, it can provide a correlation between the current value of one variable and the past values of others. Obviously, it does not mean that movements of one variable cause movements of another. However, this test can show the direction of sentiment spillover across the markets in the GCC region. Granger causality test can be estimated by using a VAR framework that could be written out to express the individual equations as follows:

In this study, y and x are any two of the six GCC stock markets. Respective coefficients and chi-square statistics are able to show if the relationship between sentiments of individual markets is absent, unidirectional or bidirectional.

Empirical Results

Descriptive Statistics of Sentiment Proxies

Table 1 shows the descriptive statistics for six individual GCC stock markets’ sentiments. It is noticeable that over time, ups and downs in individual GCC stock market sentiments cancel out each other, resulting in almost an absence of sentiment. However, the respective standard deviations of sentiment show a different picture for individual stock market sentiments. Qatar has the largest (SD = 1.50) variation in sentiment, whereas the UAE has the lowest (SD = 1.12). Thus, the market sentiment of Qatar is the most volatile, although average sentiments of all the markets are close to zero. Since these markets have almost zero sentiment, with standard deviation slightly higher than one, a dynamic framework such as GARCH should be able to better capture the volatility of these market sentiments.

Table 2 presents the correlation matrix for the sentiments of all the stock markets in the region. A strong presence of correlation between sentiments in individual markets is clearly evident. Only Kuwait has a negative correlation with other markets in the region. Saudi Arabia—the largest market in the region—has a strong correlation (significant at the 5% level) with other markets. Thus, the results indicate that these markets are reasonably correlated, which make them vulnerable to any contagious shock to sentiment. However, such correlations cannot tell exactly how market sentiments are correlated over time in the presence of changes in conditional volatility across the markets. Neither do they show the direction of sentiment spillover.

Descriptive Statistics for the Sentiment of Individual GCC Stock Markets

Correlation Matrix for the Sentiment of Individual GCC Stock Markets

Dynamic Conditional Correlation Between Individual GCC Market Sentiments

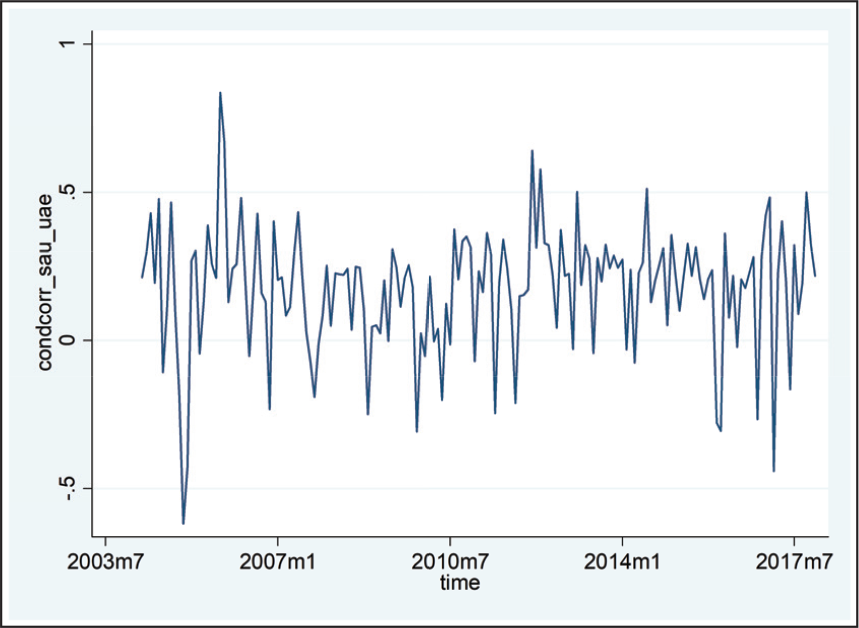

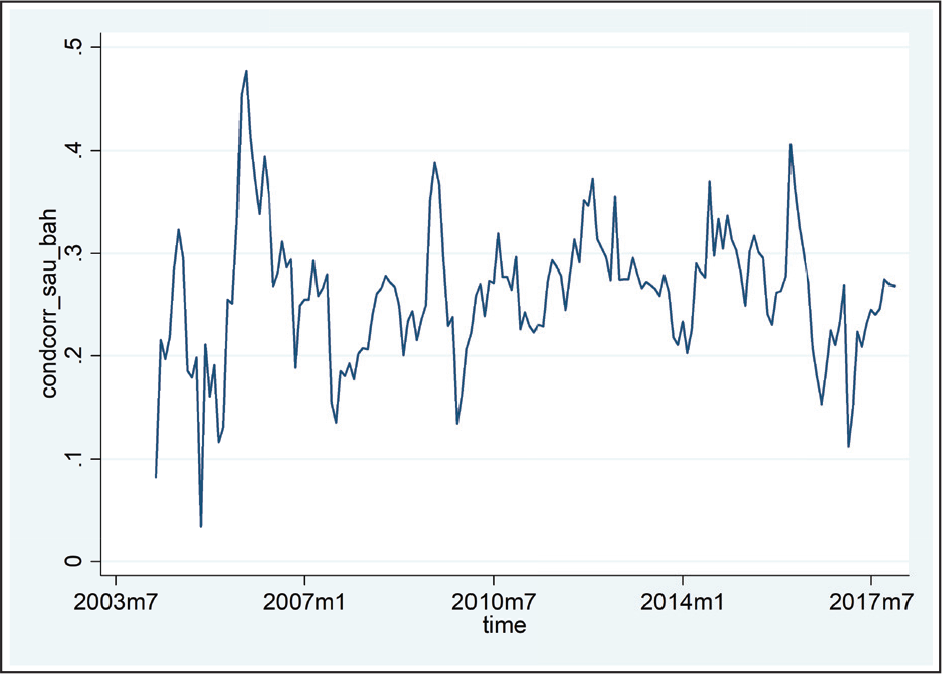

Figures 1(a)–1(m) show how the correlation of a pair of individual GCC stock market sentiments changes over time. The spillovers of sentiment between Kuwait and Qatar and between Kuwait and Oman cannot be estimated due to non-convergence of the model estimation process. Saudi Arabia and the UAE are the two biggest markets in the region. Interestingly, Figure 1(a) exhibits that the correlation between the sentiments of these two stock markets is extremely volatile. Usually, the correlation is positive and is in the range of 0.00–0.40. However, such a volatile correlation between the Saudi and UAE sentiments is an obstacle for portfolio diversification. Obviously, a dramatic rise or decline in Saudi sentiment can potentially sweep through the UAE market, even though the latter’s market fundamentals do not change at all. A reverse effect is also possible, but the direction of causality is not yet known.

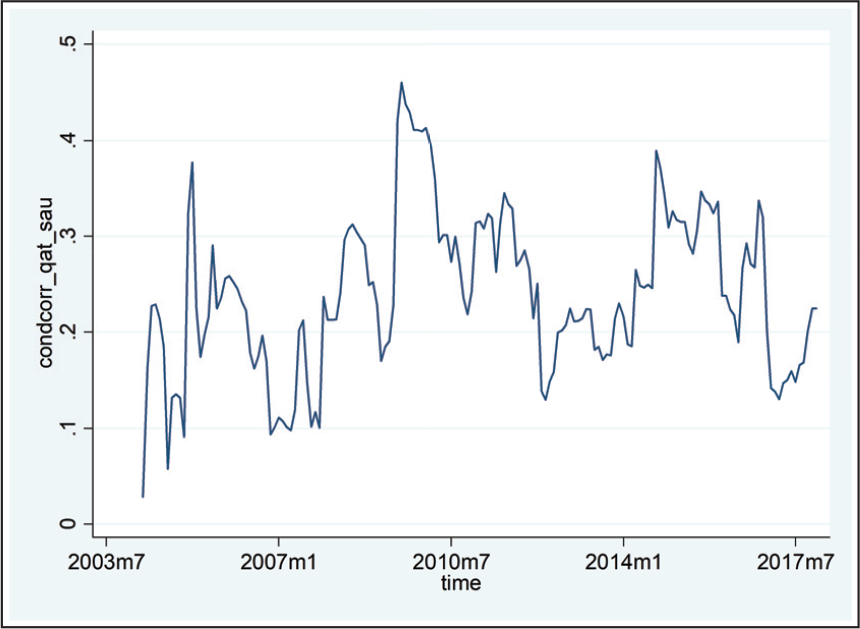

As shown by Figure 1(b), investor sentiments of the Qatar and Saudi markets are always positively related. The magnitude of correlation is not that strong. However, Saudi Arabia shut down the diplomatic and economic ties with Qatar in June 2017. The effect of this event is also visualized in the sudden drop in correlation approximately around the same period.

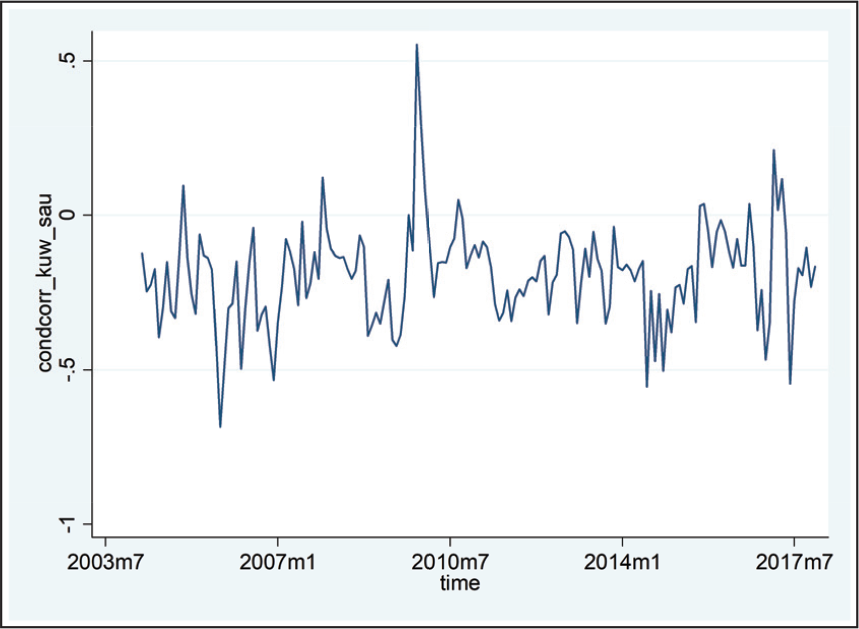

Figure 1(c) shows that the conditional correlation between the Saudi and Kuwait market sentiments has usually been negative, except for a big spike in late 2009. Such a negative relationship is also found in Table 2. This historical negative relationship between sentiments gives an opportunity to an investor to diversify his/her portfolio by investing in these two markets. Moreover, despite some spikes, investors’ actions are not strongly contagious for the Kuwait and Saudi markets. Figure 1(d) tells us that the conditional correlation between the Saudi and Oman market sentiments was close to zero in 2007, and since then it had been on the rise until 2013, when it reached 0.20. The continuous rise in correlation shows that these two markets’ sentiments have been becoming more integrated over time. However, since 2013, the integration has been relatively stable.

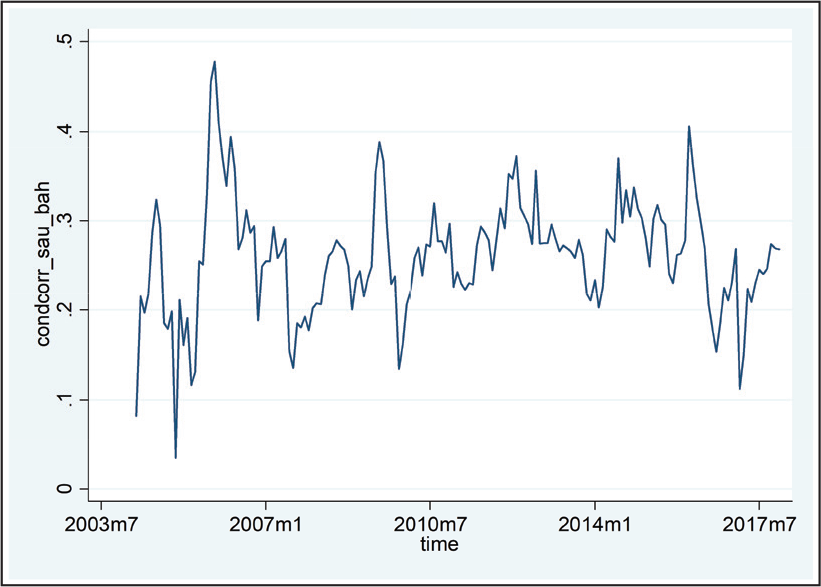

As shown in Figure 1(e), the Bahrain and Saudi market sentiments are not much integrated. This is a surprising finding, since these two countries are highly involved in trade and they also share a common border. Hence, this result suggests that investors in these markets are fundamentally different. The strong presence of non-synchronous trading in the Bahrain market may be the reason for its low integration with the Saudi market. The lack of trade suggests slow and less incorporation of dynamic information, which consequently leads Bahrain to be non-responsive to the events in Saudi Arabia. On the other hand, the Saudi market is well known for frequent trading and liquidity.

The conditional correlation between the sentiments of the Kuwait and UAE markets has almost always been negative throughout the study period. As shown earlier in Figure 1(c), there has been a persistent negative correlation between the sentiments of the Kuwait and Saudi markets. Thus, it is possible that investors in the Kuwait market behave in a fundamentally different way from those investing in the Saudi and UAE markets.

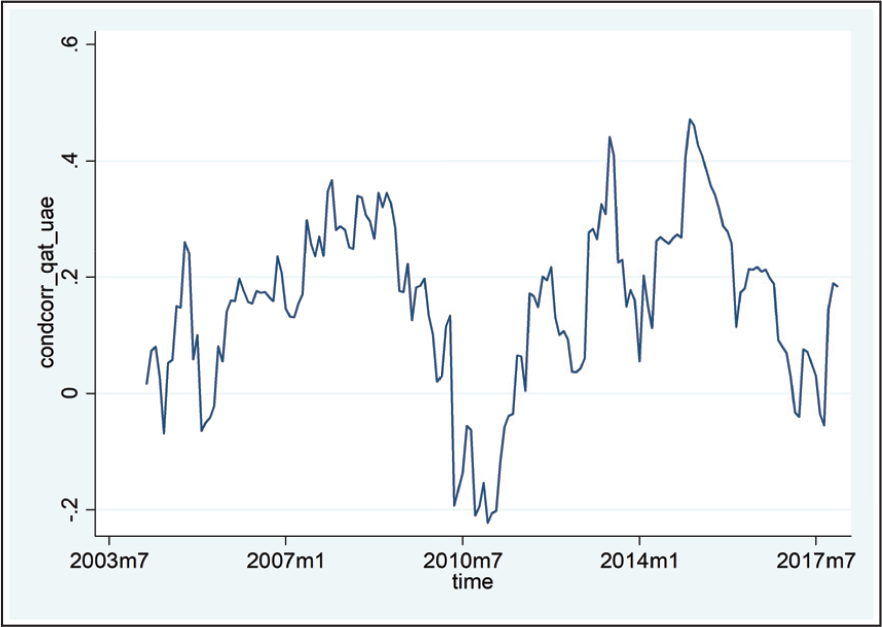

The conditional correlation between Qatar and the UAE market sentiments (Figure 1[g]) shows four distinguishable trends—an upward trend during the 2003–2008 period, a downward trend during the 2009–2010 period, an upward trend during the 2011–2013 period and a downward trend during the 2015–2017 period. However, the conditional correlation between investor sentiments in these two markets—albeit low in magnitude—has usually been positive. The impact of the Qatar embargo is also evident in 2017 through a sudden drop in correlation.

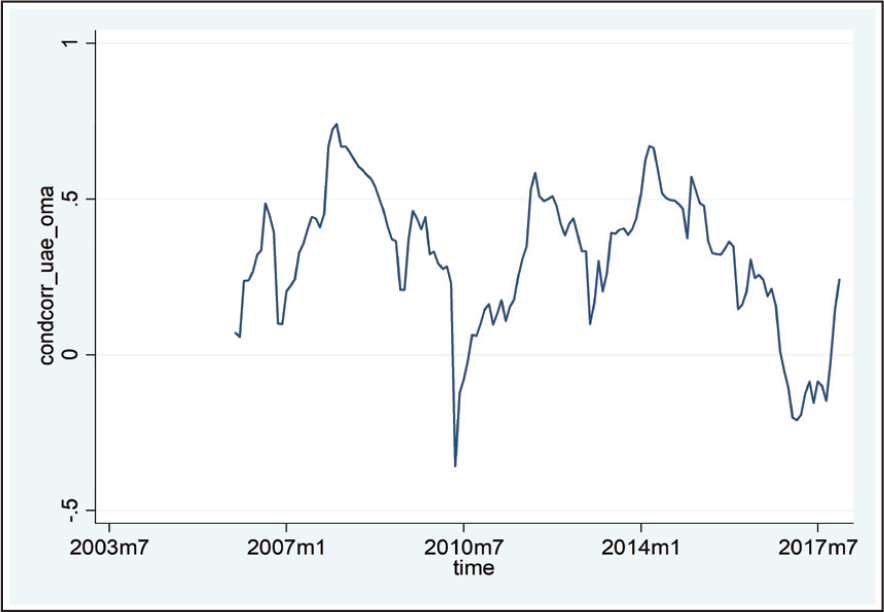

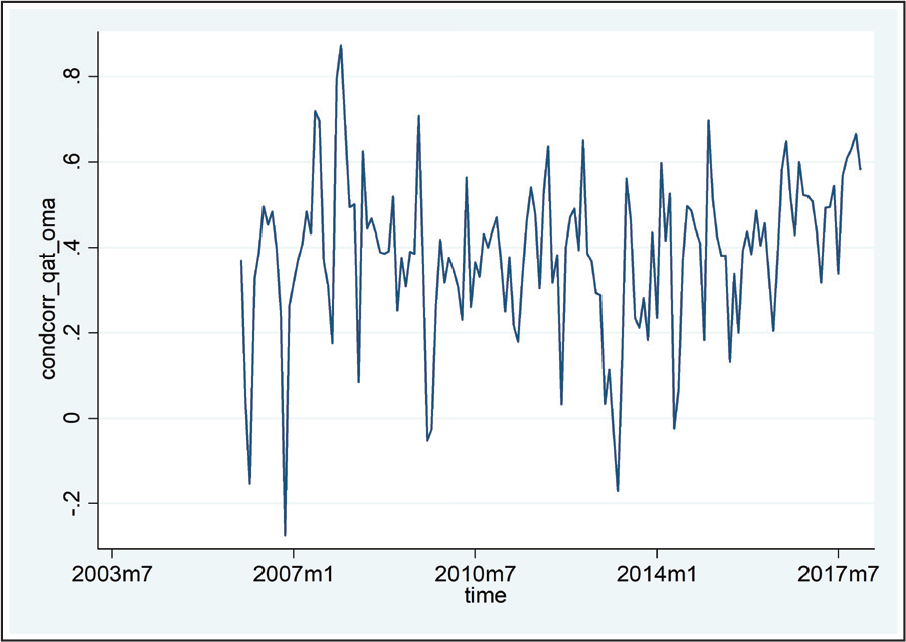

As shown in Figure 1(h), the correlation between the investor sentiments of the UAE and Oman markets sometimes has been extremely high during the study period. For example, it was approximately 0.70 in 2008. Strangely, the correlation dropped to −0.40 in July 2010. Due to such a variability in conditional coefficient, an investor must be cautious about investing in both the markets. Any behavioural bias in the UAE market may sweep though the Oman market. Since the UAE market is much larger than the Oman one, there is less possibility that it would happen the other way around.

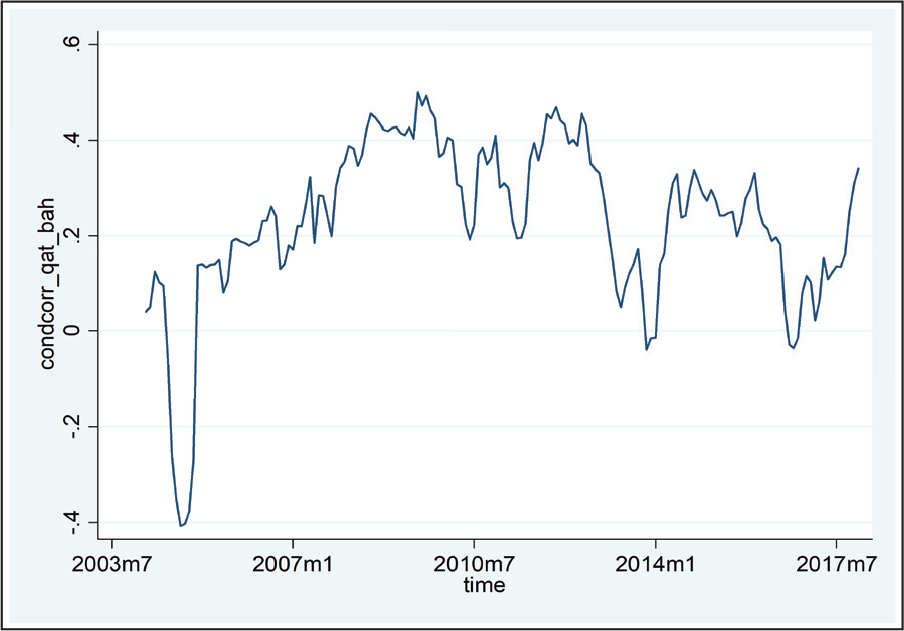

The conditional correlation between the sentiments of the UAE and Bahrain markets has been very smooth since 2007 (Figure 1[i]). During the period 2003–2006, the correlation jumped very sharply. Afterwards, the correlation has been usually modest in magnitude and has hovered approximately between 0.35 and 0.40. As per Figure 1(j), the correlation between Qatar and Oman is extremely volatile. In 2008, it reached over 0.80, which indicates that investors should be aware of a contagion effect in case of any potential negative shock to either of these two markets. Since Oman did not sever the diplomatic and economic ties with Qatar during the embargo, there is no sign of any change in the conditional correlation of sentiments. In fact, the conditional correlation slightly increased in 2017.

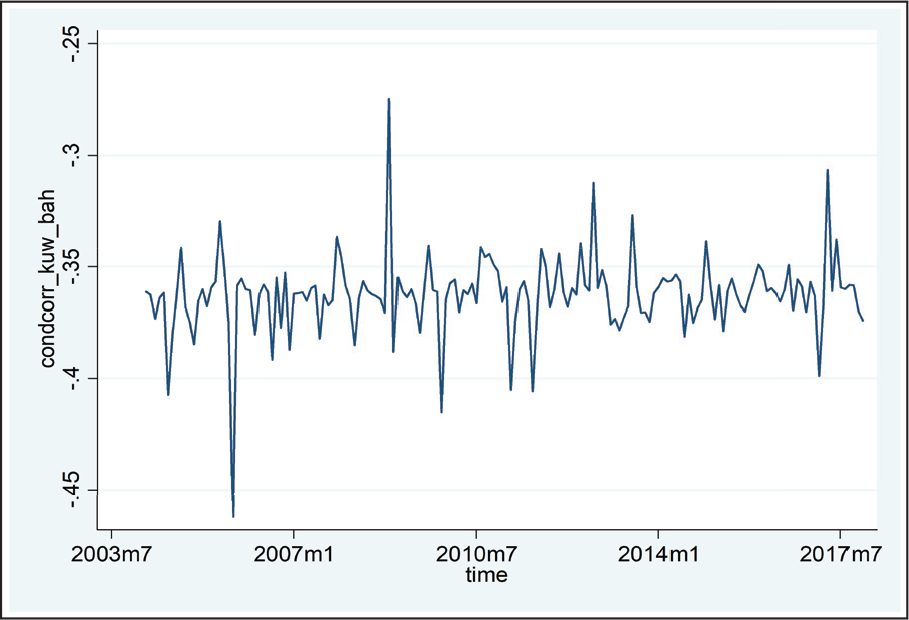

Figure 1(k) indicates that the correlation between Qatar and Bahrain has been moderate since 2006. A sudden drop in sentiment correlation is also visible just before the Qatar crisis in June 2017. Figure 1(l) shows that the correlation between Kuwait and Bahrain has always been negative. It is a strange finding, and the possible reason could be that Kuwait is a highly oil-based economy, whereas Bahrain is basically a financial hub of the region and its economy is less related to oil prices. Interestingly, Kuwait has been found to be isolated from all other markets in the region. Thus, investing in both markets may provide a strong opportunity to diversify risk as far as investor sentiment is concerned.

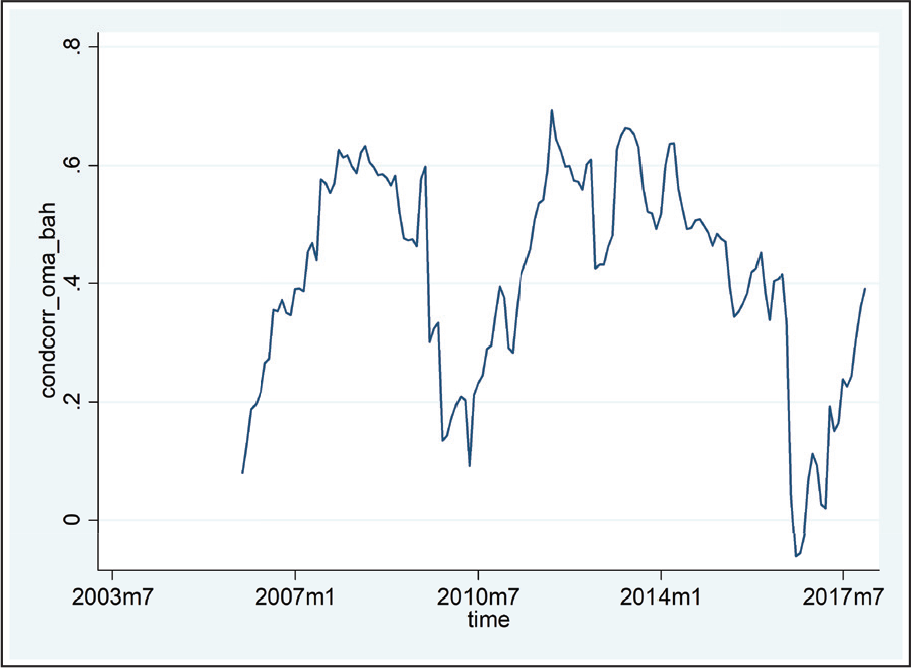

Finally, Figure 1(m) shows that the investor sentiments of Oman and Bahrain usually move in the same direction, although in mid-2016 the correlation suddenly dropped. At the end of 2017, it went up to about 0.40. This phenomenon coincided with the Qatar crisis, in which Oman did not take any side. Perhaps, it was an initial hiccup of the crisis and then markets normalized quickly. These two markets are the smallest in the region in terms of market capitalization. Both the markets also suffer from a strong presence of non-synchronous trading. Thus, in reality, the high correlation of investor sentiment in these markets may not have a strong impact on an investor with a well-diversified portfolio.

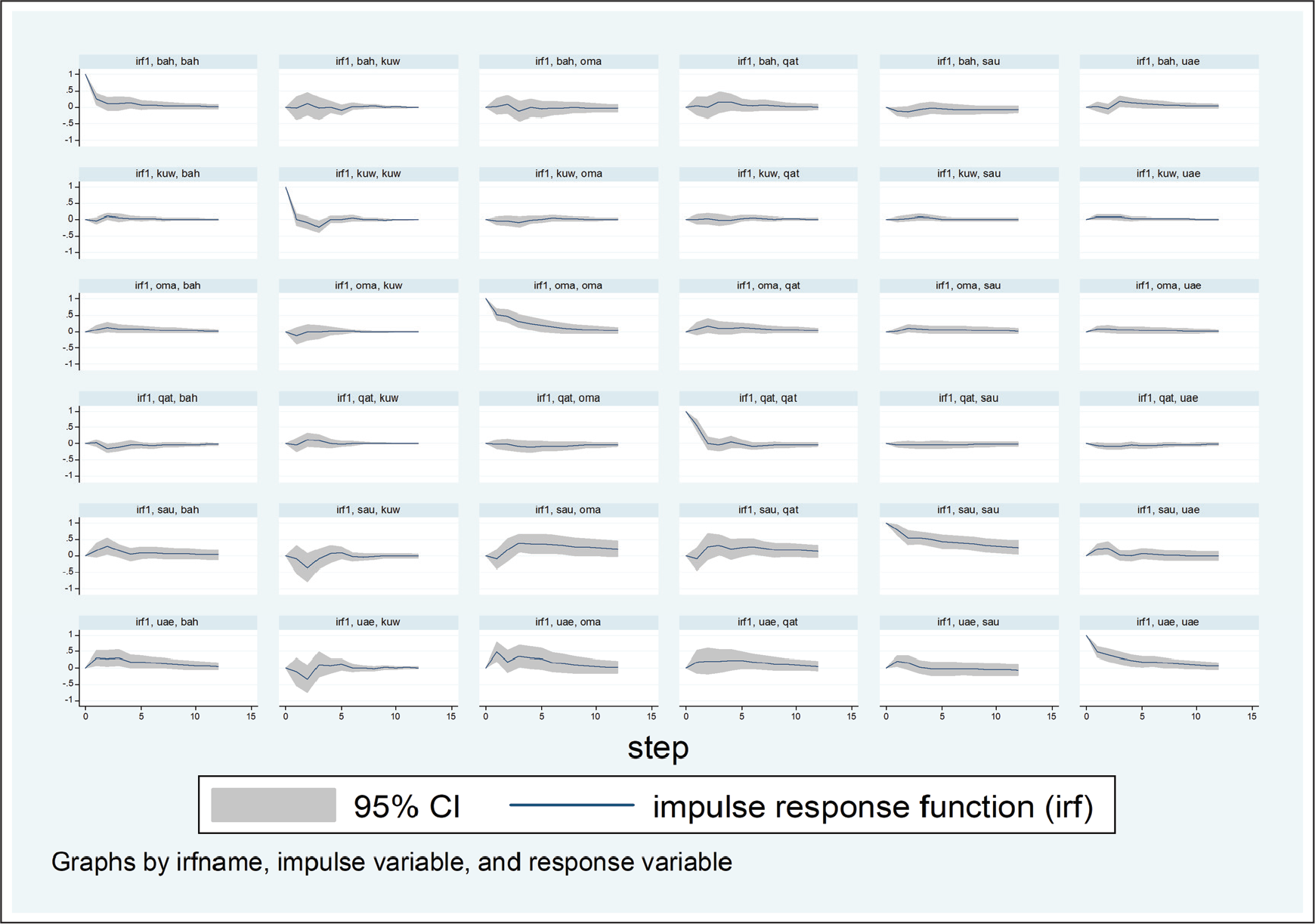

Response to Sentiment Shocks for the GCC Markets

Figure 2 provides impulse response functions (IRF) showing how the innovation in sentiment in any of the markets may have an impact on that of other countries (including its own). Diagonal graphs in Figure 2 show that the sentiments of these markets mainly react to the innovations in their own sentiment. The first column exhibits that Bahrain’s sentiment mainly reacts to the shocks to sentiments in the Saudi and the UAE markets. Especially, Bahrain takes a long time to absorb a sentiment shock in the UAE.

The sentiment in the Kuwait market responds to the shocks to the Saudi and UAE markets as well, but the effects are absorbed very quickly. The third column shows that shocks to the Saudi and UAE market sentiments in general have a strong impact on the sentiment in the Oman market, which takes a very long time to adjust to such shocks. The somewhat long-term effects of the Saudi and UAE market sentiments on the Qatar market sentiment are also evident. The reason could be the strong bilateral trade between Saudi Arabia and Qatar before the blockade. A shock to the UAE sentiment has a short-lived impact on the Saudi sentiment and vice versa (comparing the fifth and the last columns). Other than that, the UAE market does not respond to the shocks to other markets’ sentiment changes. Thus, these two markets are relatively strongly related. This finding is also corroborated by the findings from the dynamic conditional correlation analysis in the section

Direction of Sentiment Effects

Table 3 exhibits the pair-wise Granger causality test results for every pair of markets’ sentiments in the GCC. The results show that Qatar is completely isolated from the rest of the GCC as far as stock market sentiment is concerned. This finding, along with the discussion above, gives some indication that the Qatar market has always been isolated in the region and it is not just the outcome of the recent Qatar blockade. Qatar used to have a common border with Saudi Arabia, with a significant amount of trade. Even then, these stock markets are found to have been independent of each other. Kuwait is another country that is also isolated from the other markets in the region.

On the other hand, Saudi Arabia and the UAE have strong ties in terms of market sentiment. Since these two markets are the most liquid in the region, information goes back and forth much easily. There is a bidirectional Granger causality, meaning that any change in sentiment in either of these two may impact the other. Obviously, an investor involved in both Saudi Arabia and the UAE must be aware of the possible contagion effect. If there are a significant number of common investors, the impact could even get worse in case of any sudden change in the investor behaviour of either of these two markets. Bahrain and the UAE also have a strong bidirectional relationship. The UAE and Saudi Arabia have a unidirectional Granger causality towards Oman.

Pair-wise Granger Causality between the Individual GCC Market Sentiment

Conclusion

It has been found in the recent finance literature that sentiment has a strong influence on future stock returns. However, the spillover of sentiment across countries is not well-researched. This is especially true for the GCC markets. In this perspective, this study sheds light on how stock market sentiments in the GCC region may spill over to other markets in the region. This study uses GARCH-DCC, Granger causality and impulse response functions to detect the presence of spillover, the direction of spillover and the duration of shock to sentiment in the GCC markets, respectively.

The findings show that the Saudi and UAE markets are strongly related to each other. Any shock to either of these two markets affects the other and takes a long time to subside. The markets Qatar and Kuwait are completely isolated in the region. The recent blockade on Qatar cannot completely explain its isolation from the others. Kuwait’s isolation is a surprising finding, and this is not justifiable by any facts in hand. The other two markets—Bahrain and Oman—are the two smallest markets in the region, and they are somewhat related to the Saudi and UAE markets. Interestingly, the integration between the markets in the region did not increase by much throughout the study period.

Overall, it can be reasonably said that an investor involved in both the Saudi and UAE markets may face a contagion risk in the case of any behavioural shock. Obviously, the regulators of the Saudi and UAE markets should make regulatory frameworks and market monitoring in a coordinated manner. Because of their low correlation with the other markets, investors may be able to diversify their portfolio risk by investing in the Qatar and Kuwait markets. A regional investor can reduce overall portfolio risk by investing only in Kuwait in case Qatar is not investible due to its blockade imposed by Saudi Arabia, the UAE and Bahrain.

Footnotes

Acknowledgement

The author is grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.