Abstract

This study investigates the linkages between the antecedents of the extended unified theory of acceptance and use of technology (UTAUT2) model and an individual demographics in four developing countries in Southeast Europe. Three unexplored linkages are introduced, such as employment status, living settlement and financial experience. The article applies the partial least square and non-parametric methods to examine the proposed associations from a dataset of 959 individuals. Evidence reveals that those individuals who are employed, live in urban areas, and have financial experience scored higher in the UTAUT2 constructs. The article suggests the inclusion of additional moderating factors into the UTAUT2 model, which gives a better understanding of the individuals’ technology adaption to scholars and practitioners.

Keywords

Introduction

The rapid expansion of the Internet and smartphones enabled individuals to become a part of the financial digitalization and financial inclusion worldwide. In this regard, mobile banking is playing an imperative role apart from its primary functions (Asongu & Odhiambo, 2019; Fall et al., 2020; Myovella et al., 2020; Senou et al., 2019). Earlier, to access banking services, for example, to withdraw cash, a customer had to reach its location, and distance was a problem in typical traditional banking. The advent of information and communication technologies (ICTs), Internet, applications and smartphones made it easy for individuals to use digital financial and non-financial transactions in their day-to-day life, including developing countries (Lwoga & Sangeda, 2019; Mukerjee et al., 2020). Mobile banking provides fast, smooth and cost-effective services from the service provider. It is easy to reach the remotest customer, and bankers can use it as a competitive edge over competitors (Omotoso et al., 2012). Mobile banking supports the government to include every individual under the financial inclusion ambit to include them in its financial system (Mago & Chitokwindo, 2014). Therefore, one-way mobile banking plays a significant role in reaching the remotest customer through mobile banking and indirectly helping the government towards financial inclusion. Bankers are also using game dynamics and game machines to make the application attractive, fun-filled and engaging. It eventually makes usage attractive and easy for consumers to accept mobile banking and can position it as a more comfortable option to execute their daily financial transactions. The mobile banking system is based on four key components: smartphones, wireless Internet, banking applications and human behaviour. On one side, ICT innovations are continually improving Internet speed and security, smart and efficient devices, and bankers are continuously enhancing their banking applications to provide a wide range of banking services through the mobile interface (Ahmad et al., 2020; Alavi & Ahuja, 2016; Muñoz-Leiva et al., 2017; Tabetando & Matsumoto, 2020). On the other side, the unrelated component is human behaviour or precisely consumer behaviour. To make it smooth, efficient, safe and to serve consumers better, there is always a need to study what and how to influence consumers. Therefore, the most dynamic aspects of consumer behaviour to improve usage and acceptance of mobile banking are demographic factors, as it changes with time and places. This study will further investigate this area.

According to GSMA (2019), almost half of the population has access to mobile Internet. Growth in mobile Internet access is burgeoning, specifically in low- and middle-income countries because it is the cheapest way to access the Internet. The cost of the Internet is getting affordable, and the Internet is reaching rural areas. Therefore, mobile phone penetration and cheap Internet are what consumers need to access mobile banking. It reflects a strong reason to understand the potential of mobile banking. The report also indicates that there is a persistent gender gap regarding mobile Internet usage. As per the report, the two major demographic factors influencing mobile Internet usage are gender and income level. Another report from ITU (2019) also reveals interesting facts about digital development related to human being and reflects demographic differences. The report indicated that Europeans have the highest Internet usage and mobile phone ownership rates. Approximately, 97% of the world’s population lives within reach of the mobile cellular signal. People in Europe have easy access to basic requirements to use mobile banking, such as a mobile phone and Internet. Thus, if they have easy access to basic needs (ICT), then what else can affect, consequently, it can be human behaviour. Therefore, there is a logic to study mobile banking usage and adoption behaviour in the context of different countries and regions.

The most amazing fact is that the gender difference was not expected for Europe and American regions but all the world regions, but in fact, even Europe has more men than women using the Internet. Despite having the highest Internet usage and mobile ownership rates, still, gender differences can be traced. It raises an undeniable question, why the difference exists and how vast the difference is. Hence, gender is one factor the present study wants to link and understand why mobile banking usage behaviour and adoption differ in men and women. Based on this, the gender difference is still an issue. Moreover, the present study will cover the other demographic factors, such as employment and rural, urban people. The present study identified the critical demographic factors to understand human behaviour through the most accepted information technology model (unified theory of acceptance and use of technology [UTAUT]. Given by Venkatesh et al. (2012), many researchers applied mobile banking acceptance and usage studies (Baabdullah et al., 2019; Baptista & Oliveira, 2015).

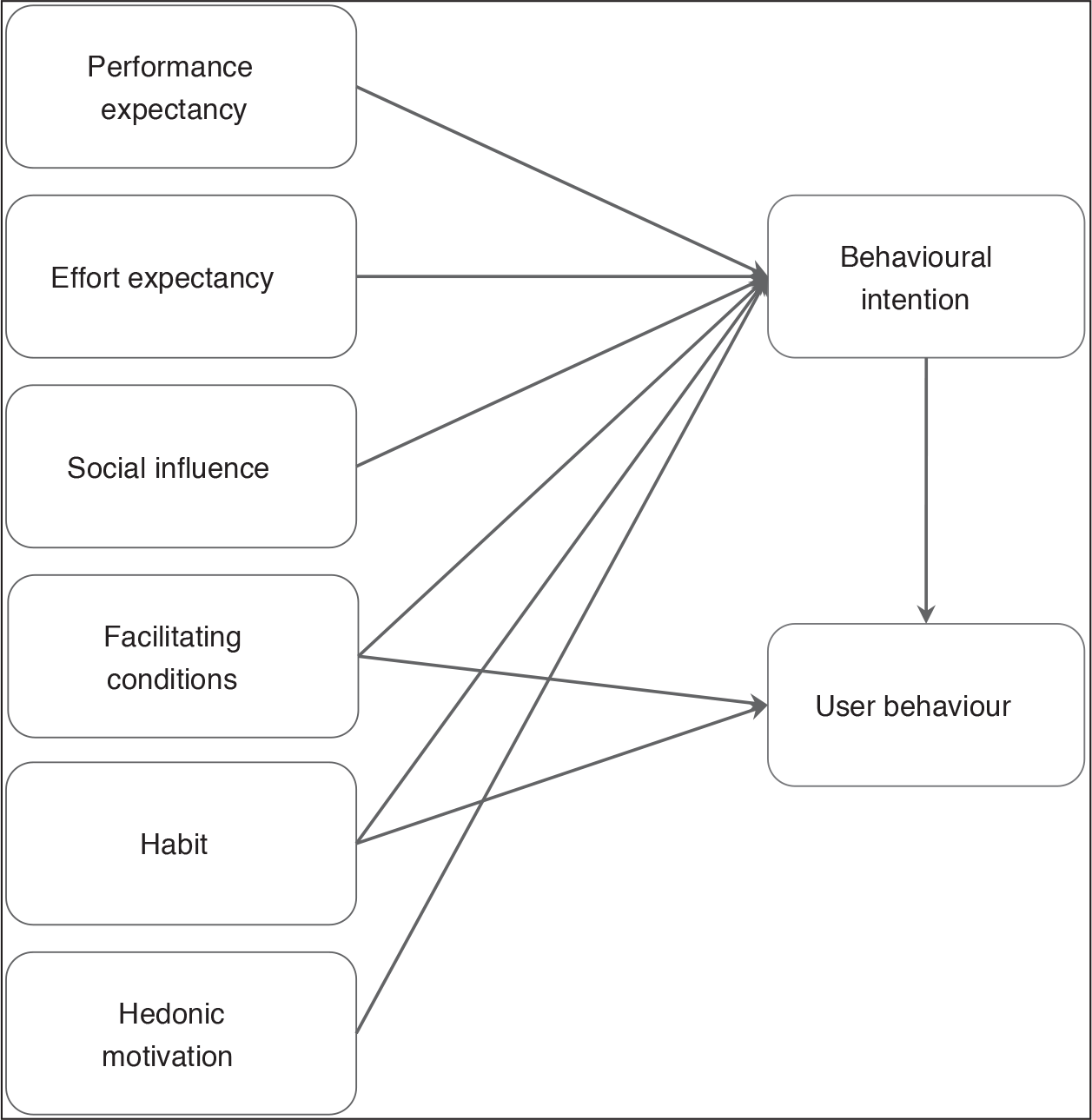

The UTAUT model was first recommended by Venkatesh et al. (2003) to determine the behavioural intention and use behaviour about the information system. That is why the current research’s theoretical support is based on two standpoints: UTAUT (Venkatesh et al., 2012) and the chosen demographic factors. The UTAUT model (Venkatesh et al., 2003) was established based on eight prominent and preceding theories: the theory of reasoned action (Fishbein & Ajzen, 1975), the technology acceptance model (Davis, 1989), the motivational model (Davis et al., 1992), the theory of planned behaviour (Ajzen, 1991), the personal computing utilization model (Thompson et al., 1991), the innovation diffusion theory (Rogers, 1995), the social cognitive theory (Compeau & Higgins, 1995) and the integrated model of technology acceptance and planned behaviour (Taylor & Todd, 1995; see Figure 1). On the other hand, many studies have covered various moderators to identify their impact on the antecedent of mobile banking usage behaviour. The models of UTAUT, and its extended version, itself applied a few demographic factors such as gender, age, experience and voluntariness of use. Subsequently, other authors also applied other demographic factors such as occupation, income, qualification, marital status (Chawla & Joshi, 2018), gender, education and user experience of ICT (Park et al., 2007). They found these factors do affect mobile banking acceptance to a certain extent. Therefore, based on the discussed literature, the present study has identified four demographic factors such as gender, employment, living settlement (location such as rural or urban) and financial experience. Living settlement and financial experience are not covered yet in any previous study to the extent of the author’s best knowledge. The same is the present article’s novelty to display how these two new demographic factors can influence the chosen antecedents regarding mobile banking usage.

The geographical focus of the present study is Southeast European nations. In the recent past, it has been noticed that the Southeast European countries are now taking adequate measures to grow and match with other western European nations (OECD, 2019; Tosheva & Dimeski, 2019). Another research in the Kosovo area suggests a need for training programmes for women, as they have shown a slower trend in adopting the technology. The bank can have online and mobile banking trial versions and must enhance the user-friendliness of the apps. The study indicates more studies and more comprehensive research with broader frameworks and more constructs need to be analysed to clarify the usage of online and mobile banking (Prenaj, 2017). Another study on mobile phone penetration and inequality reduction in Western Balkan states supports that mobile banking can be used extensively in developing countries to tackle prosperity, inequality and poverty (Vokshi et al., 2019). Mobile banking is positively associated with inclusive growth. Poverty and inequality in lower-middle-income countries, upper-middle-income countries and Central and Eastern European countries were negatively associated with the increased usage of cell phones to pay, send and receive bills (Asongu & Nwachukwu, 2018). These mentioned arguments support the country analysis.

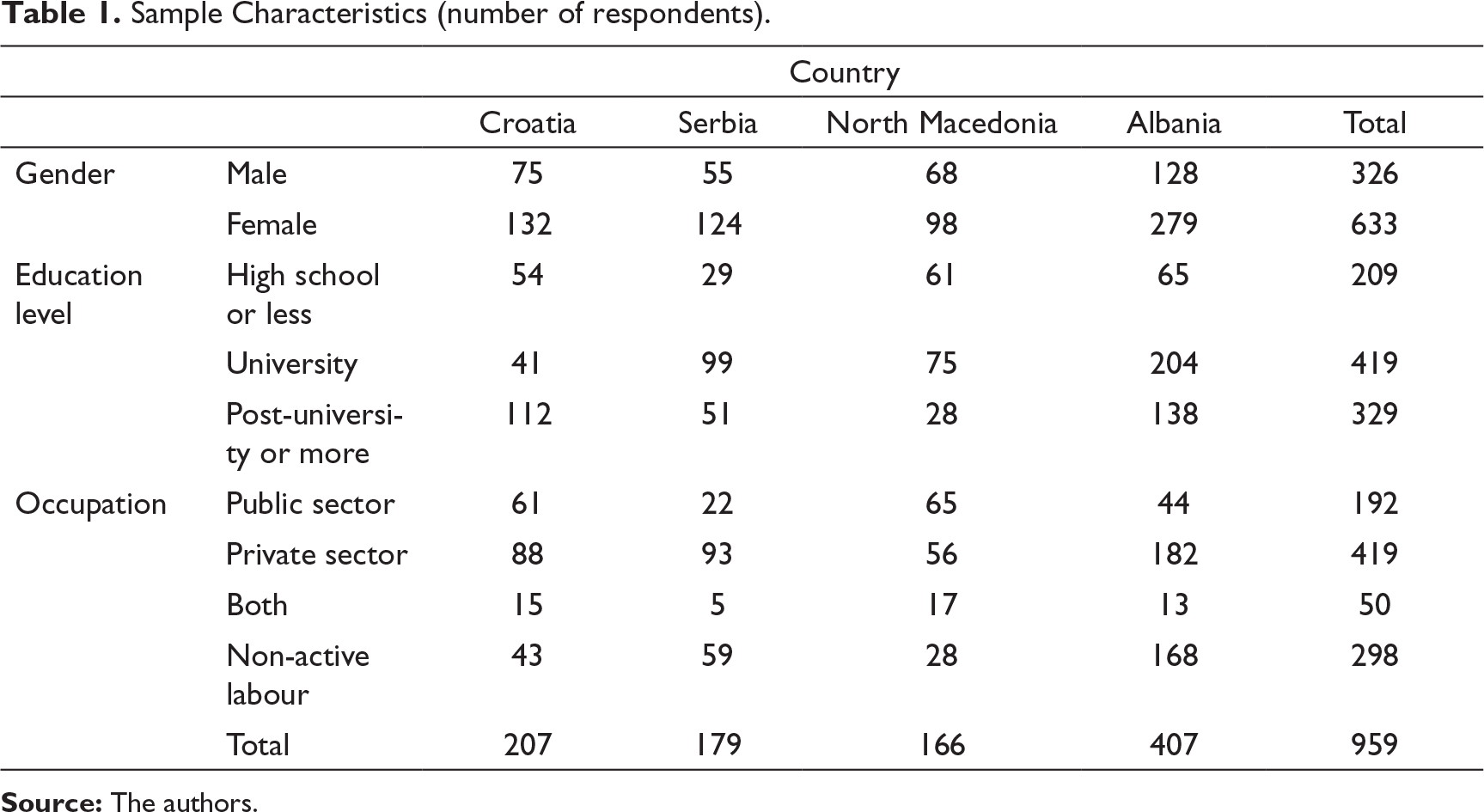

The present study was conducted over a wide geographical area covering Croatia, Serbia, North Macedonia, Albania and Kosovo. The chosen countries reflect similarities in their cultural aspects, for example, most southeast European countries have similar lingos, and they can comprehend each other, as it has many similarities (Vesnic-Alujevic, 2012). People of this region have witnessed many changes from the communist era to the republic regime. They desire to be a part of the European Union except for Croatia, which already has its membership. Western Balkan (located in Southeastern Europe) states are witnessing economic growth, reducing unemployment and increasing domestic labour demand. They are becoming a trustworthy partner of the European Union through their sustainable economic reforms and constant achievements of favourable results in many areas such as boosting digitalization, innovation, connectivity and economic growth and employment (Čeperković et al., 2018). Looking into the existing literature, it can be observed that very few studies have covered such a wide chosen area and also that the chosen phenomenon is not yet studied in this region. Most of the studies belong to strong economies in the European Union, Gulf countries, etc. Therefore, the chosen territory is still unexplored. The present study’s focus is to understand how the selected demographic factors influence mobile banking usage and acceptance (Chawla & Joshi, 2019). The gradual expansion of the Internet, mobile-based Internet usage, adoption of western European culture and lifestyle to be part of the European Union gives enough motivation to study how the peoples’ demographic factors affect usage of mobile banking in the chosen region (Zabukovšek et al., 2019; Vrček & Klačmer, 2014). Surprisingly, according to Kim et al. (2018), consumers’ demographic characteristics in developing countries tend to have a negative effect on the adoption of mobile financial services. A very strong argument forwarded by a study analysed location, age, gender and income on information communication and technology acceptance. Several studies encourage further in-depth analysis of location in future research and other socio-demographic variables (Petersen et al., 2020). Several other studies recommend further socio-demographic research in the related field (Niehaves & Plattfaut, 2014; Siregar et al., 2017). With this in mind, it is worth studying the relationships between UTAUT’s constructs and individuals’ characteristics in developing countries such as those in southeast Europe. The study’s outcome can help the policymakers and corporates towards strategy formulation to improve the acceptance and usage of mobile banking among the people of chosen states.

The present study has identified the key variables based on the UTAUT model (Venkatesh et al., 2012), such as performance expectancy, effort expectancy, social influence, facilitating conditions, habit, hedonic motivation, behavioural intention, user behaviour and demographic factors such as gender, employment, living settlement and financial experience to investigate the significant demographic factors influencing mobile banking acceptance and usage under the chosen theory in the context of the Western Balkan consumers’ mobile banking adaptability and acceptance. To the best of the authors’ knowledge, no other study has covered gender, employment, living settlement and financial experience extensively with UTAUT2 together, representing the present study’s core originality. From the managerial and practical implication point of view, the effect of demographic factors on behavioural intention and user behaviour in the context of developing countries provides useful insights. The study offers insights how the chosen demographic factors in each selected state related to the extended UTAUT model (Venkatesh et al., 2012) can help the chosen region to improve its mobile banking acceptance and usage. Adopting this framework would add substantially to the literature, and the outcome will contribute to practical implications. The necessity to understand and investigate the demographic factors that affect behavioural intention and user behaviour in referred transition countries motivated to conduct this research. Hence, this study seeks to examine the effect of demographic factors concerning the UTAUT2 model on the intention to use mobile banking in the context of post-communist transition countries of the Western Balkan states.

Literature Review

Various studies have been conducted to study the relationship of antecedents of UTAUT2 with demographic factors such as age, qualification, marital status and occupation but majorly focused as a moderator. The present study sheds light on the relationships between each component of UTAUT2 and the chosen demographic factors such as gender, employment, living settlement and financial experience. The study’s objective is to conclude the severity of selected demographic factors on each construct of UTAUT2 and recommend the policymakers and corporations to focus on those factors specifically to improve mobile banking acceptance and usage among the chosen regional states.

Unified Theory of Acceptance and Use of Technology

The UTAUT model was proposed by Venkatesh et al. (2003) and was developed as an interactive holistic model to understand better the consumers’ behavioural intention towards new technologies or systems’ acceptance and adoption. Further, (Venkatesh et al., 2012) UTAUT2, which is currently the latest model, has been increasingly adopted by researchers around the globe to explore the consumers’ behavioural intention for the adoption of various issues such as self-operative technology, adoption of smartphone devices and acceptance of learning management apps (Huang & Kao, 2015). UTAUT2 would efficiently illustrate and evaluate people’s technology adoption behaviours for new products in information technology (IT). That is the reason the present study implemented UTAUT2 as an analytical model. Looking at the context of UTAUT2, the first antecedent is performance expectancy, which implies the degree to which the use of new technology or the latest technological product will provide customers the benefits of conducting or using particular activities (Venkatesh et al., 2012). The present study considers the performance expectancy a significant antecedent to measure consumer behavioural intention using mobile banking, similar to the other studies (Baptista & Oliveira, 2017; Çera et al., 2020). The second one is effort expectancy, which relates to users’ level of convenience connected through a new technology service or product of a technology (Venkatesh et al., 2012). To determine the consumers’ behavioural intention, the performance and effort expectancies are among the most significant predictors of technology use and adoption (Baabdullah et al., 2019; Baptista & Oliveira, 2017; Çera et al., 2020). Another antecedent of UTUAT2 is the social influence; it means others acknowledge the extent of the significance of using new technology. The other three antecedents considered in the present framework are facilitating conditions, habits and hedonic motivation. Facilitating conditions refer to the individuals’ belief about the availability of organizational and technology infrastructure support in technology usage (Venkatesh et al., 2003, 2012). Habit, which is about individuals’ automatic behaviour of using technology, concerns the extent to which consumers use technologies. The last is the hedonic motivation. It is about the fun or enjoyment consumers derive from using a technology. It reflects that hedonic motivation plays a vital role in determining acceptance and using a particular technology (Magni et al., 2010; Venkatesh et al., 2012). Considering the objective of the present study, the antecedents of UTAUT2 are useful to determine the consumers’ behavioural intention of mobile banking usage like several studies did in the past around the globe (Baabdullah et al., 2019; Baptista & Oliveira, 2017; Çera et al., 2020; Huang & Kao, 2015). Hence, the UTAUT2 model has been adopted considering the relevance of the present study.

Linking Gender to UTAUT2 Constructs

The number of studies on gender states that males and females, to some extent, have different social roles and personal characteristics. This difference can be traced through their perceptions, information assessment and information technologies use such as computers, the Internet and mobile phones (Goh & Sun, 2014). Various studies reveal gender differences in the different related fields also. According to Zhang et al. (2014), there are significant gender differences in technology acceptance. A study by Todman (2000) confirms existence of gender differences regarding technology acceptance, as higher levels of computer anxiety and less positive attitude towards technology adoption were found in women than men. Another study supports this claim that women have greater technology anxiety than men (Lee et al., 2010). Hence, it means females might feel more stressed to use technology. Supporting the same argument, another study indicates that there is gender influence on purchase intentions, as women are more likely to be anxious about products with which they are personally attached (Wekeza & Sibanda, 2019). Several other studies also found gender differences in technology adoption and use. For example, computer and Internet use is lower in girls than in boys (Vekiri & Chronaki, 2008; Zhang et al., 2014). A study in Nigeria found gender significantly influences banking customers’ attitudes to Internet banking adoption (Onyia & Tagg, 2011).

On the other hand, anxiety is a behavioural state of humans (Steimer, 2002). Studies have exposed that females are usually less confident in technology usage than men (Goh & Sun, 2014). Having higher anxiety and less confidence, which forms behaviour, can affect purchase intentions. It has been found that fear, emotions etc., influence purchase intentions (Hutjens, 2014; Pappas et al., 2014). The theory of planned behaviour states that attitude is related to behavioural intentions (Ajzen, 1991), and the theory of reasoned action by Fishbein in 1967 states that intentions have a strong relation with behaviour and behavioural performance. It was found that the performance or non-performance of a given behaviour is determined by the strength of an individual’s intention to do it (Fishbein, 2008). In short, emotions impact purchase intentions, and several studies found gender difference using theory of planned behaviour to determine individuals purchase intentions (Pappas et al., 2014; Wekeza & Sibanda, 2019). Based on the consumer behaviour theories mentioned above, several variables like gender and employment status affect the consumer purchase intentions (Wekeza & Sibanda, 2019). Therefore, it can be summarized in simple words that anxiety, confidence, attitude, etc., influence females’ behavioural intention. The previous studies’ claims that there are significant gender differences towards acceptance of technology or Internet banking seem logical. Therefore, it is relevant to find the differences regarding mobile banking acceptance too. Based on this, the literature review further identifies the relationship between gender and UTAUT2 components. The study also related each component with gender differences found in related fields.

According to Venkatesh et al. (2003), the relationship between behavioural intention and performance expectancy, effort expectancy and social influence individually are moderately influenced by gender difference, and the designed model confirmed gender as an integral part of UTAUT. Social norms affect acceptance more powerfully among female respondents than male respondents (Riquelme & Rios, 2010), hence proving the relevance of gender to determine technology usage and acceptance. Similarly, other studies that adapted and applied UTAUT and/or UTAUT2 also confirmed that gender has a significant moderate influence on user adoption (Park et al., 2007) as well as on performance expectancy, effort expectancy and behavioural intention (Warsame & Ireri, 2018). Behavioural intention is more positively influenced by personal innovativeness for males than females (Liu et al., 2015). A study reflects users’ gender has a significant moderating impact on social media sites’ evaluation and usage behaviour (Lim et al., 2017). Another study concluded that hedonic shopping among female consumers is predominantly higher in comparison to men. Thus, hedonic shopping behaviour differs according to gender (Kirgiz, 2014).

Some research denied the moderate influence of gender between the elements of mobile technology adoption and behavioural intention. It also tested the moderate effect of gender between the relationship of facilitating conditions on behavioural intention (Jambulingam, 2013). Another study claims that there are no gender differences concerning mobile phone usage in the educational process (Ashour et al., 2012). Therefore, there are mixed result, where various authors found gender has a significant moderate impact, and few reject it. In this scenario, the present study tried to investigate the direct effect on the factors of the UTUAT2 model. Rowntree’s (2019) report reveals that the gender gap regarding mobile ownership and mobile Internet usage is lowest in Europe compared to 18 low- and middle-income countries worldwide. Hence, it also supports investigating the gender difference, especially towards mobile banking in selected eastern European countries. Pieces of evidence identify a lack of information on how gender influences the acceptance, adoption and usage of mobile banking, especially in the context of Balkans states. Studies also found that gender differences exist, especially in the use of mobile banking. The female intention to use mobile banking is significantly affected by perceived usefulness, which is a part of performance expectancy (Haider et al., 2016; Hyde-Clarke & Mnisi, 2015). Based on the above, the present article is intended to explore the gender differences related to the UTAUT2 model.

Linking Employment to UTAUT2 Constructs

Very few studies have considered employment a vital demographic variable, and it failed to attract the researcher’s attention. There is not much qualitative or quantitative research that analyse mobile banking acceptance from occupational perspectives such as full-time employees or full-time students (Bhatiasevi, 2016). It is probably the first time employment will be considered a potential factor to measure the effect antecedents of UTAUT2. The authors’ review of existing literature found only two relevant studies: Onyia and Tagg (2011) about Internet banking adoption where employment status reflected the significant impact on Nigerian customers’ attitude and intention towards Internet banking acceptance. Another study by Chawla and Joshi (2018) considered occupation as a moderator but included both professionals and students and found the occupation moderates between the antecedents and behavioural intention. Another study conducted a comparison between different occupations and found that occupation affects Internet banking usage. Some occupations have higher Internet usage, and some have less (Jayasiri et al., 2016). It becomes imperative to re-examine occupation as an independent variable to determine how employment affects consumers’ mobile banking usage behavioural intention. The present study considers only full-time employment status and will be a value addition in the literature, as it is not yet covered, and the same is the novelty of the present paper.

Linking Living Settlement to UTAUT2 Constructs

Another demographic factor included in this research is the living settlement which is chosen to determine the effect of living location (urban or rural) on the antecedents of mobile banking acceptance and usage. A study in Iran stated that the digital gap between urban and rural societies is alarming. As ICT plays a noteworthy role in rural growth processes, it must reach rural areas (Moghaddam & Khatoon-Abadi, 2013). To the extent of the authors’ knowledge, no prior study has covered the living location as a demographic factor. Neither the urban nor rural areas were covered in their research to measure its influence on the factors of UTAUT2 in terms of mobile banking usage and acceptance. Few countries witness the fast conversion of rural areas into urban or rapid migration of rural people towards the urban area. It becomes easy to adopt the urban style of living where the penetration of mobile ownership and Internet usage is better (GSMA, 2019). There are many studies related to ICT usage and acceptance, mobile ownership and Internet usage in rural and urban areas, but no study has ever covered living location as a factor affecting mobile banking usage and acceptance. Another study in South Africa by Ramavhona and Mokwena (2016) stated that in rural areas, people are reluctant to adopt Internet banking because of low awareness about its benefits, wrong perception about its conveniences, and fear of fraud. Also, poor infrastructure support regarding Internet access and computer availability are the reasons for not accepting Internet banking. In simple words, the acceptance and usage of Internet banking in rural areas of South Africa is low because of poor infrastructure and people’s wrong perceived intentions. The bank-led mobile banking model is seen as a useful and easy-to-use tool by people in unbanked and underbanked rural areas (Mtambalika et al., 2016). Therefore, there is a need to study in depth how location can impact the mobile banking usage intention. Based on these, it sounds logical to apply the rural and urban location factors to investigate the impact on the antecedents of mobile banking usage in the context of eastern European nations. It could be an exciting area, especially for policymakers and the business community.

Linking Financial Experience to UTAUT2 Constructs

According to Chawla and Joshi (2018), experience can be explained as the accumulated practical contact with and observation of facts or events that a person gains while working in a particular job, profession, place, or project. Another study stated that no precise definition of the experience is available; therefore, it will be useful to consider domain-specific conceptualization of experience and user experience related to technology, as the study was related to technology acceptance (Sun & Zhang, 2006). The experience represents the extent of familiarity with and knowledge about the technology of interest (Sun & Zhang, 2006). Earlier studies on technology acceptance have used the experience as a moderating factor (Venkatesh et al., 2003, 2012) and gave significant results and stated its importance as a moderator. Before the advent of UTAUT, Agarwal and Prasad (1999) stated that individual differences such as education level or the extent of prior experience have a substantial influence on TAM’s beliefs. No preliminary research about mobile banking usage and acceptance has ever considered financial experience effects. Mobile banking includes banking services provided through the Internet, based on an application and used through electronic devices. People who have financial work experience may find it easy to do a financial transaction online. Work experience may improve knowledge. OECD (2018) also stated that consumers with a lower level of financial knowledge should not be provided with a complicated or high worth transaction through online platforms. It is a risk as well as it can disengage the consumer from the usage.

There is an effect of experience, such as work experience, for example, individuals working in IT field or social media might have a different approach. Those users with experience in mobile applications, whether banking or any other, may have a different perception about the risks associated, improve their perception of utility and promote their usage overtime on an ongoing basis. Factors such as consumers’ personality, comparable experiences and individuals’ shopping orientation might reflect significant aspects of the technology acceptance model and online retailing (O’Cass & Fenech, 2003). The user-situational variables (training, experience and user involvement), attitude and demographics of users affect the acceptance of innovation (Alavi & Joachimsthaler, 1992). Personal experience continues to be a central factor in the usage of online retail (O’Cass & Fenech, 2003). Therefore, regarding mobile banking usage for the financial transaction’s it seems reasonable to investigate how experience in the financial domain can affect mobile banking use and acceptance. The present study investigates the influence of financial experience on mobile banking usage and acceptance, as scholars have not yet researched this area. The current research believed that the insight into how financial experience affects mobile banking usage antecedents would open a new research domain. Today, the financial market cannot work alone without ICT support. It makes it relevant and useful for policymakers and business houses.

Methods and Procedures

Data and Variables

To investigate possible linkages between the individuals’ demographics and UTAUT2 constructs, a questionnaire in the English language was designed and reviewed for content validity by academics of the field. It was then translated into the four local languages: Albanian, Serbian, Croatian and Macedonian. The questionnaire was selected as a data collection tool, as it was suggested by prior studies (Baptista & Oliveira, 2017). The questionnaire consists of two sections: the demographic profile of the respondents and the UTAUT2 constructs. Besides user behaviour, all other UTAUT2 constructs were adopted from Venkatesh et al. (2012). The scale of Martins et al. (2014) was used to measure user behaviour, pointing at the frequency of the use of mobile banking: 1 = ‘once a year’, 2 = ‘once in six months’, 3 = ‘once in three months’, 4 = ‘once a month’, 5 = ‘once a week’, 6 = ‘once in 4–5 days’, 7 = ‘once in 2–3 days’, 8 = ‘almost every day’, 9 = ‘every day’ and 10 = ‘several times a day’.

Sample Characteristics (number of respondents).

Data Analysis

Constructs and Their Items.

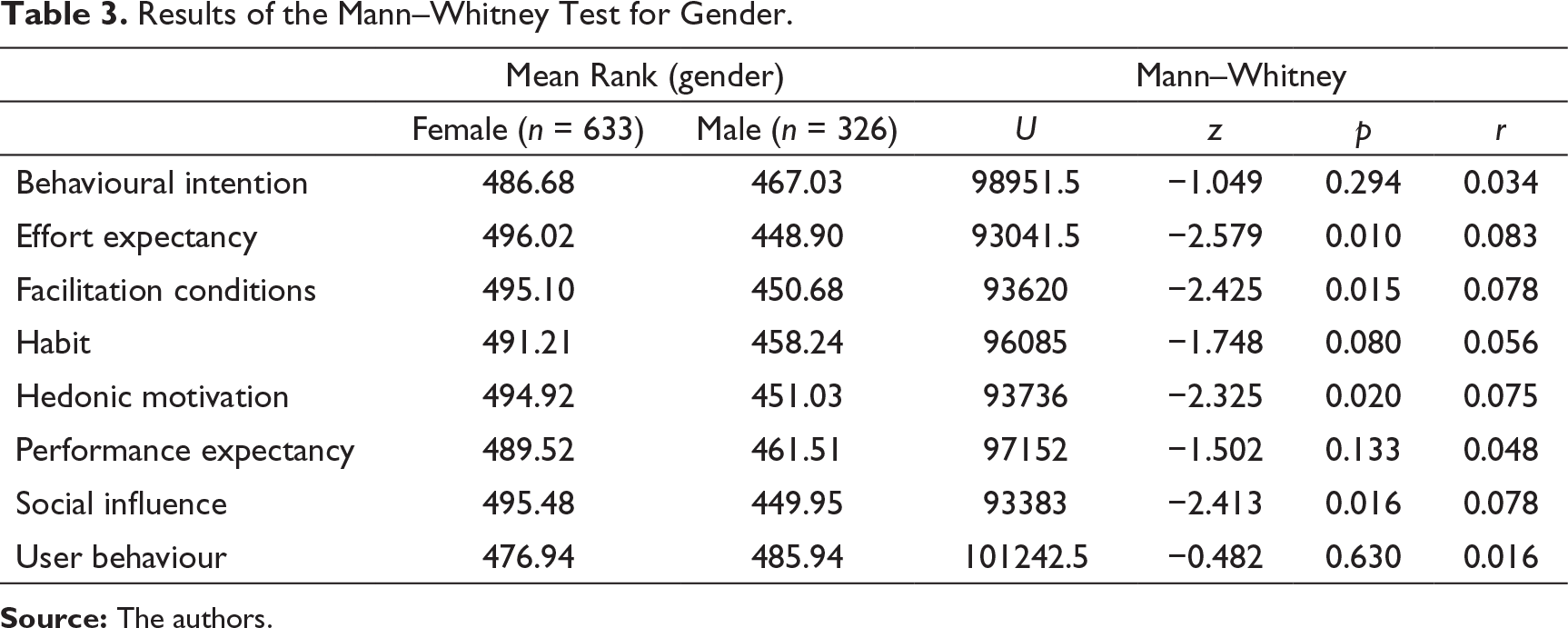

To investigate the linkages of the above constructs with the individuals’ demographics, a nonparametric test was used because the composed constructs were not normally distributed, as Kolmogorov–Smirnov and Shapiro–Wilk tests demonstrated (Meyers et al., 2013). As our demographic variables were dummy variables, the Mann–Whitney test was employed (Gravetter & Wallnau, 2017). The latter test analyses the difference only between the two groups. It converts the scores on the continuous variable to ranks across the two groups. It then evaluates whether the ranks for the two groups differ significantly (Pallant, 2016). Its effect size can be calculated as the z-score division with the square root of the sample size. The non-parametric tests were performed in SPSS 23.

Results

Results of the Mann–Whitney Test for Gender.

Results of the Mann–Whitney Test for Employment Status.

Results of the Mann–Whitney test for Living Settlement.

Results of the Mann–Whitney Test for Financial Experience.

Discussion

The present research has shown insights regarding the association between the UTAUT2 constructs and the individuals’ demographics (gender, employment status, living settlement and prior financial experience). The evidence showed that these constructs do significantly associate with individuals’ characteristics. However, these findings should be discussed a bit more carefully. Hence, in the following paragraphs, the above linkages are discussed in the context of the Western Balkan states.

The first tested relationship was the one that links the UTAUT2 constructs and gender. It was found that gender does associate with effort expectancy, facilitation conditions, hedonic motivation and social influence. Moreover, evidence showed that, compared to males, females scored higher on the latter constructs, consistent with prior studies conducted in a similar field (Goh & Sun, 2014; Lim et al., 2017; Sun & Zhang, 2006). However, the data showed that behavioural intention, habit, performance expectancy and user behaviour do not associate with gender (see Table 3), which goes in line with what previous studies have demonstrated (Baptista & Oliveira, 2017; Chawla & Joshi, 2018; Venkatesh et al., 2012). As a result, gender does not associate with all UTAUT2 model’s constructs. Therefore, considering the latter findings, technology acceptance and usage do not differ in terms of gender for Western Balkan people.

The second tested linkage was between the UTAUT2 model’s constructs and the employment status of the individuals. Evidence has supported the above associations stressing the importance of being employed in accepting and using technology, including mobile banking. As discussed in the literature review section, this study is among the first to consider employment status as a potential individual demographic linked to the UTAUT2 model’s constructs. In conducting the present research, existing literature and prior studies support the importance of employment status on an individual’s technology adaption (Elmi & Ngwenyama, 2020; Leppäniemi & Karjaluoto, 2008; Onyia & Tagg, 2011). However, the current research results contradict Moghaddam and Khatoon-Abadi’s (2013) finding regarding the association between living settlement and the UTAUT2 model’s construct.

The third tested association was between living settlement (the place where the individuals live: urban or rural area) and the UTAUT2’s construct. As in the employment status case, this article is among the first, which links living settlement to the UTAUT2 model’s constructs. Excluding hedonic motivation and social influence, all the other constructs reflected a significant relationship with the area where people live. Contrary to Moghaddam and Khatoon-Abadi (2013), the present study demonstrated substantial evidence supporting the above association. Thus, as expected, those who live in urban areas scored higher in the UTAUT2 constructs, which is in line with Ramavhona and Mokwena’s (2016) research. Hence, it can be concluded that people living in rural areas are reluctant to adopt Internet banking due to low awareness about its benefits, wrong perception about its conveniences, and fear of fraud.

The final investigated relationship in the current article is the one that links an individual’s financial experience to the UTAUT2 model’s constructs. Findings show that people who had prior experience working/internship in the financial sector, such as in a bank, exchange office, microfinance institution, pension funds, the insurance company, financial office, consultant, cashier, stock exchange, etc., scored higher in the habit, hedonic motivation and of course in the acceptance and usage of mobile banking. This lead to the fact that having experience working or doing the internship in a financial institution increases the chances to use mobile banking, which goes in line with Agarwal and Prasad’s (1999) claim, emphasizing that individual differences, including the extent of prior experience, have a substantial influence on TAM’s beliefs. To the best of the authors’ knowledge, this study is among the first few studies that link the individuals’ previous financial experience to the UTAUT2 model’s construct.

Research Implications and Limitations

Considering the benefits of technology usage, including mobile banking, for the society and financial industry, academicians, policymakers and managers have a constant interest in understanding the linkages between the individual demographics and technology adoption aspects. In this way, every effort to explain technology acceptance is motivated among scholars (Chaouali et al., 2017; Dahlberg et al., 2015; Ege Oruç & Tatar, 2017; Lwoga & Sangeda, 2019; Shaw & Kesharwani, 2019). In light of this need, the current article investigates how the individual demographics are linked to the UTAUT2 model’s constructs.

This study made an effort to explore whether the individual demographics are linked to the UTAUT2 model’s constructs or not in the context of four developing countries in the Western Balkan (Albania, Croatia, North Macedonia and Serbia). Although there are studies that investigated the associations of individual demographics and technology acceptance (Chawla & Joshi, 2018; Goularte & Zilber, 2018; Hoque et al., 2019), their relationships are not covered. The present research contributes in this regard by offering new insights by introducing new individual demographic variables such as employment status, living settlement and financial experience. To the best of the authors’ knowledge, this article is among the first which investigate the linkages between the latter variables and the UTAUT2 model’s constructs. Consequently, the study contributes to a better understanding of the technology acceptance puzzle. It suggests extending the number of moderating factors, which leads to a more comprehensive conceptual framework.

From the managerial point of view, bank managers are in favour of offering services remotely, as it reduces operational costs. For the financial sector, technological advancements create competitive advantages by allowing firms to focus on improving the services. Banks in transition countries like in the Western Balkan are advised to follow similar tendencies in advanced economies regarding mobile banking services, as it benefits both banks and clients. An enhanced bank strategy may need to be adjusted according to the individual demographics, as the current research emphasized. Following the suggestion of Hanafizadeh et al. (2019), while framing policies, it is also imperative to focus on local issues and concerns, as it might be supportive to governments to implement ICT plans.

Even though the objectives of the study were achieved, there are still some limitations. Although there are four countries included in the sample size, other developing countries from the Western Balkan, such as Bosnia and Hercegovina, Kosovo and Montenegro, were not a part of this project. However, based on the economic development level, they are in the same stage as those in the present analysis. Therefore, it is believed that findings are not affected, and the generalization of the results to other contexts is not limited. Nevertheless, the latter limitation can be overcome by further research. Another limitation deals with the distribution of the final sample. Even though non-parametric statistical methods were applied in this work, it would still be preferred to analyse a sample that satisfies the standard assumptions. The sample distribution is skewed regarding education and gender. This limitation can be overcome by applying restrictions in the sample design stage.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.