Abstract

The common conclusion presented in a large number of scientific publications is that the COVID-19 pandemic has had a substantial negative impact on human health and businesses. The main aim of this article is to present the results of research on the impact of the COVID-19 pandemic on leading ICT enterprises’ financial performance. The research covered the three leading ICT enterprises: International Business Machines (IBM), Samsung Electronics Co. Ltd. (Samsung) and Canon Kabushiki Kaisha (Canon). The research covered the 15-year period from 2007 to 2021, which included the pandemic period of 2020–2021. This allowed for the evaluation of the dynamic rate of change over time and more precise comparison of the changes in the financial performance indicators during the pandemic period. The main conclusions are that despite significant restrictions, lockdowns and many infections, the COVID-19 pandemic has had no significant impact on the financial performance of the enterprises studied in the research. The research provides new knowledge about the impact of the COVID-19 pandemic on leading companies in the ICT industry. Further research on the impact of this pandemic may reveal details about more factors that influenced the business activities in other sectors of the economy.

Keywords

Introduction

The spread of COVID-19 has had a profound impact on countries around the world. It necessitated the mobilization of resources on an unprecedented scale to address the virus. Consequently, the economy has changed significantly over the past 2 years due to the impact of the COVID-19 pandemic on almost every aspect of socio-economic life. The rapid spread of the virus has led to every continent and country in the world being affected by the pandemic. The changes resulting from COVID-19 have become very important subjects of many scientific studies, and the number of publications is growing constantly. The changes have been caused by the threats posed by the spread of COVID-19 and their impact on human health. The outbreak and very rapid spread of the virus was unexpected for the whole world. Therefore, there is no doubt that it should be considered a crisis situation for most countries around the world. Both citizens and governments are involved in counteracting the threats through the issued regulations. These regulations sought to find the best ways to deal with the crisis situation. The extensive literature on this subject focuses first on prevention and then on diagnostics and treatment options. It describes the measures that can be taken to detect infections early and prevent their spread (Ting et al., 2020). New technologies and diagnostic devices have been developed, and artificial intelligence is now being used to diagnose COVID-19 (Liang et al., 2022; Wang et al., 2022a). Furthermore, the ways of doing business and the ways people work are changing (Kaushik & Guleria, 2020; Kudyba, 2020; Narayanamurthy & Tortorella, 2021; Neeley, 2021). Interest in remote work has grown rapidly and, as a result, the interest in digital transformation has also increased. Consequently, ICT is now most widely used for business activities and education, as well as in institutions such as hospitals, banks and science laboratories (Busulwa et al., 2022; Erskine et al., 2022; Kaputa et al., 2022; Konopik et al., 2022; Wenzel, 2022). The literature presents new concepts and models for running businesses and measuring results while subject to the restrictions that countries affected by the COVID-19 pandemic imposed (Matraeva et al., 2022; Saputra et al., 2022; Stalmachova et al., 2022; Troise et al., 2022). Many publications perform comparative analyses and estimate the financial impact of the pandemic on various industries, economies and societies around the world (Das et al., 2022; Estrada et al., 2020; Khan, 2022; Khlystova et al., 2022; Quan et al., 2022; Shen et al., 2020). The majority of scientific studies indicate that the imposed restrictions (e.g., lockdowns) have had a significant negative impact on the results achieved by enterprises, sectors and economies (Ashraf, 2020; Francesco et al., 2022; Salisu et al., 2022; Umar, 2022; Wang et al., 2022b; Yarovaya et al., 2022).

To determine the impact of the COVID-19 pandemic on business operations, two main limitations must be considered. The first limitation is the large number of employees infected by the virus. The second limitation is the lockdowns that governments imposed in countries affected by COVID-19. In the context of these limitations, two key negative effects on the business activities of enterprises can be identified. The first and most fundamental effect of the limitations is the significant reduction in the value of both revenue and gross profit. The pandemic began approximately 2 years ago—not long ago. Changes to revenue and gross profit are observed on a yearly basis. Furthermore, these indicators allow for the calculation of the gross profit margin. When considering the impact of the pandemic on the performance of the selected enterprises, gross profit margin is one of most accurate financial performance indicators. If a significant value reduction occurs in at least one of these indicators or in the gross profit margin, managers will look for short-term solutions in less visible or less significant long-term activities. These could include saving money on research and development (R&D) expenditure, investments or training schedules (Kaplan & Norton, 2004). In particular, R&D expenditure is a primary visible indicator for the long-term development of enterprises. Therefore, over a relatively short period of time (approximately 2 years), the limitations may result in a significant reduction in R&D expenditure to improve the current situation. After the short-term difficulties are over, it is possible to return to the previous level of R&D expenditure. Therefore, R&D expenditure is the third most important indicator when identifying the impact of the COVID-19 pandemic.

The literature on the subject also indicates that the most common effect of the imposed restrictions is a significant acceleration of the use of ICT. It applies to almost every aspect of human life, particularly in enterprises’ economic activities. The use of the latest ICT technologies allows people to work remotely from wherever possible. It has also accelerated the development of technologies for protection against infection, remote diagnostics and the treatment of people suffering from COVID-19. The values of the specified financial indicators can be observed in a time series. The remaining requirement is choosing the leading companies in the ICT sector. Taking into account a period of time significantly longer than the COVID-19 pandemic, leading ICT enterprises should be characterized by the continuity of their R&D activities and systematic achievement of their best effects. R&D expenditure was selected as one of the most important indicators used in this research when identifying the influence of the COVID-19 pandemic. One of the most widely recognized results of R&D activity is the number of obtained patents (Chen et al., 2021; Dernis, 2007; Dong et al., 2021; Florida et al., 2008; Griliches, 1990; He et al., 2022; Sagasti, 2004). A distinctive feature of the number of obtained patents is the lag between obtaining them and R&D expenditure. Lag between input and output variables of R&D activities is an important and distinctive feature of the innovation process. Therefore, such delays must be always taken into account. Lag is related to many factors. One factor is the time necessary for the United States Patent and Trademark Office (USPTO) to process a patent application, which varies from 18 months to 36 months (Lim & Kim, 2022; Popp et al., 2003; The United States Patent and Trademark Office [USPTO], 2021). Consequently, obtaining the largest number of patents over a period of many years requires continuous R&D expenditure. Therefore, the number of patents obtained over a period longer than the period during which the effects of the COVID-19 pandemic have existed is a justified criterion for determining which companies have a well-established leading position in a given sector. Moreover, the number of obtained patents is not a good indicator in the research on the impact of COVID-19 over a 2-year period. For over two decades, enterprises that belong to the ICT sector have continuously obtained the highest number of patents in the USPTO (USPTO, 2021). This is another reason for choosing leading ICT enterprises for evaluation in this research rather than other enterprises and industries. Enterprises continuously run R&D activities and spend considerable funds on obtaining patents. The enterprises chosen for the comparative analysis and evaluation in this research are IBM, Samsung and Canon.

The reasons for choosing these enterprises are that they belong to the ICT sector and they have obtained the highest number of patents from the USPTO among all industries and enterprises over the last 20 years (USPTO, 2021). Such a long period indicates that their R&D activities have been conducted continuously over this period. Furthermore, IBM was the uninterrupted leader in the number of obtained patents from the USPTO for over 20 years (USPTO, 2021). This is why these enterprises, unquestionable global ICT leaders in obtaining patents, are the best examples to use for this research. Additionally, the number of patents they have acquired and the results of their R&D activities are confirmed in the source documentation. This documentation comprises annual reports that are published annually throughout the research period by all the selected enterprises (Canon, 2022; IBM, 2022; Samsung, 2022). To identify the impact of COVID-19 on these leading ICT enterprises in 2020 and 2021, a 15-year research period from 2007 to 2021 was selected. The reason for choosing this research period was the possibility of using statistical tools to evaluate the dynamic rate of change over time. It was also chosen to compare value changes in the selected financial indicators more precisely over a significantly longer period than the pandemic period.

The main aim of this article is to present the results of research on the impact of the COVID-19 pandemic on leading ICT enterprises’ financial performance. Both this aim and the above-mentioned issues led to the main research question: Have leading ICT enterprises experienced significant changes in revenue, gross profit and R&D expenditure during the pandemic? The method used to answer this research question is described in the next chapter.

Materials and Methods

The main aim of this research was to identify and evaluate the impact of COVID-19 on the business activities of three leading ICT enterprises—IBM, Samsung and Canon. The research question will be answered through a two-stage analysis and evaluation described below.

The biggest impact of the pandemic restrictions was on people’s health and their ability to work, travel and go shopping. Therefore, the impact on business activities should easily be identified by the significant changes in the revenue and gross profit of the selected enterprises. The input data are shown in a time series of the revenue, gross profit and R&D expenditure of the selected ICT enterprises. They cover a 15-year research period that includes the pandemic years of 2020 and 2021 (Annex 1). It may also be possible to observe a significant change in R&D expenditure. The above-mentioned changes are observable during the pandemic period (2020 and 2021). The first stage of the analysis and evaluation was dedicated to identifying and comparing significant changes between the values of indicators in two identical comparative periods—before the pandemic (2018–2019) and during the pandemic (2020–2021). The second stage of the analysis and evaluation was dedicated to calculating the dynamic rate of change in the values of the indicators over the 15-year period from 2007 to 2021, which includes the pandemic period. In both stages, values of the following indicators were used: revenue, gross profit, R&D expenditure and gross profit margin. To obtain results in both stages, the gross profit margin, percentage change index and dynamic rate of change were calculated according to Equations 1, 2 and 3, respectively.

The pandemic is considered to have had an impact on the financial performance of the selected enterprises. Gross profit margin is one of most accurate financial performance indicators. It was calculated according to Equation 1:

where:

t is the subsequent year in the time series of the 15-year research period;

i is an index ranging from 1 to 3 denoting the ICT enterprise covered by the research: 1—IBM, 2—Samsung and 3—Canon;

vr ti is the value of the revenue each ICT enterprise i covered by the research in year t;

gp ti is the value of the gross profit of each ICT enterprise i covered by the research in year t; and

gpm ti is the value of the gross profit margin of each ICT enterprise i covered by the research in year t.

The percentage value of the change index was calculated according to Equation 2:

where:

t is the subsequent year in the period 2018–2021 covering two comparable subperiods;

k is an index ranging from 1 to 4 denoting the financial variable: 1—revenue, 2—gross profit, 3—R&D expenditure, and 4—gross profit margin;

i is an index ranging from 1 to 3 denoting the ICT enterprise covered by the research: 1—IBM, 2—Samsung, and 3—Canon;

vkt is the value of the financial variable k in year t;

vkt−1 is the value of the financial variable k in the preceding year t; and

ckt is the percentage value of the change index for each financial variable k in the subsequent year t.

The dynamic rate of change in each financial variable and gross profit margin was calculated according to Equation 3:

where

t is the subsequent year in the time series of the 15-year period;

N is the number of annual observations in the time series of the subsequent financial indicator c over the entire research period;

c is an index ranging from 1 to 4 denoting the financial indicator: 1—revenue, 2—gross profit, 3—R&D expenditure, and 4—gross profit margin;

i is an index ranging from 1 to 3 denoting the ICT enterprise covered by the research: 1—IBM, 2—Samsung, and 3—Canon;

One of the limitations of the evaluation was that COVID-19 first appeared in December 2019 but the virus only began to spread to most countries in the world in March 2020 (World Health Organization [WHO], 2020). Therefore, it was assumed that the pandemic period started in March 2020. Consequently, there is a difference of 2 months for 2020 compared to 2018 and 2019, which were before the pandemic period; however, this difference is not significant due to two factors. First, COVID-19 first appeared in December 2019; therefore, March 2020 is not an absolute starting point for the pandemic period. Second, the input data used to analyse, compare and evaluate the impact of the pandemic are not bimonthly or quarterly but annual values of observation. This means that the margin of inaccuracy of the results is not significant. The results of the calculation and evaluation are presented in the next chapter.

Results and Discussion

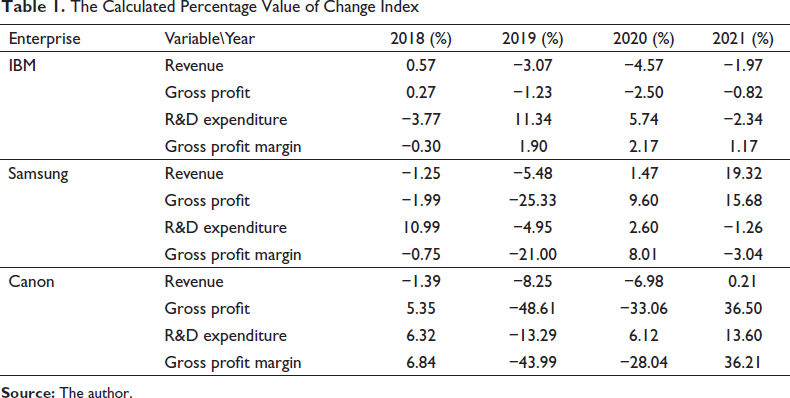

The first stage of the analysis and evaluation was dedicated to comparing the calculated values of the indicators between two periods of equal length—before the pandemic (2018–2019) and during the pandemic (2020–2021). The calculated percentage value of the change index is presented in Table 1.

The Calculated Percentage Value of Change Index

The comparative analysis of the results obtained for the period before the pandemic (2018–2019) and during the pandemic (2020–2021) indicates that IBM’s revenue increased by 0.57% from 2017 to 2018. In 2019, 2020 and 2021, however, it decreased marginally compared to each previous year. The same changes in value occurred with the gross profit. In 2018, IBM’s R&D expenditure decreased by 3.77% compared to the previous year. In 2019, before the pandemic started, and in 2020, after the start of COVID-19 pandemic, an increase in R&D expenditure was recorded. Conversely, in 2021, a 3.04% reduction in R&D expenditure was recorded. IBM’s gross profit margin decreased in 2018 compared to the previous year. In 2019, 2020 and 2021, its gross profit margin increased by 1.90%, 2.17% and 1.17%, respectively. The results of the comparative analysis indicate that there was no significant impact on the basic indicators of the financial performance of IBM during this period. Additionally, there were no significant changes in R&D expenditure during this period. This means that there has been no significant change in the corporate growth strategy of IBM due to the COVID-19 pandemic.

For Samsung, there were decreases in revenue, gross profit and gross profit margin (1.25%, 1.99% and 0.75%, respectively) in 2018 and in 2019 (5.48%, 25.33% and 21.00%, respectively), before the pandemic. Moreover, the value of R&D expenditure was 10.99% higher in 2018 and then decreased by 4.95% in the following year. Similarly, in 2020, during the pandemic, R&D expenditure increased by 2.60% and then decreased by 1.26% in 2021. The results of the comparative analysis for Samsung indicate that slight increases and decreases in the value of the indicators occurred in the periods before and during the COVID-19 pandemic. Therefore, it can be concluded that the pandemic had no significant impact on the values of the indicators that characterize Samsung’s financial performance. The results for its R&D expenditure also indicated that there was no significant change in its corporate growth strategy due to the pandemic.

Although there is no doubt that COVID-19 has had many negative effects on various businesses and a significant negative influence on workers’ health and the unemployment ratio and led to important changes in the workplaces of many enterprises, the financial results presented here indicate that the upward trajectory of the performance of IBM and Samsung was maintained (Barai & Dhar, 2021; Finstad et al., 2021).

The results for Canon show that its revenue decreased slightly during the pre-pandemic period and during the first year of the pandemic period in 2018, 2019 and 2020 by 1.39%, 8.25% and 6.98%, respectively. In 2021, however, there was an increase of 0.21% from the previous year. Canon’s gross profit during the pre-pandemic period increased by 5.35% in 2018 and then decreased significantly by 48.61% in 2019. During the pandemic period in 2020, a significant decrease of 33.06% was recorded, whereas in 2021, there was a significant increase of 36.50%. Regarding its R&D expenditure, there was a decrease in value of 13.28% in 2019 during the pre-pandemic period. In the remaining years of the research period, particularly during the pandemic period, there was an increase in Canon’s R&D expenditure. This could lead to the conclusion that the changes in its R&D expenditure are a result of the corporate growth strategy at Canon rather than the COVID-19 pandemic. Furthermore, there was a significant decrease of 43.99% in its gross profit margin in 2019 during the pre-pandemic period. Then in 2020, it decreased by 28.04% compared to the previous year. In 2021, during the pandemic period, there was a significant increase of 36.21% in its gross profit margin. Canon’s results show significant fluctuations in the values of the indicators covered by the research. However, these fluctuations apply both before and during the COVID-19 pandemic period. This means that the noted changes at Canon were due to causes other than the impact of the COVID-19 pandemic. Many factors influence the financial results of big enterprises. These factors include international factors related to financial conditions such as labour immobility, undue job loss, scarcity of employment opportunities, discontinuation of supply chain, uncertainty of investments and adverse clientele effect (Katoch & Sidhu, 2021; Lassoued & Khanchel, 2021). Such factors could have a significant influence on Canon’s financial results.

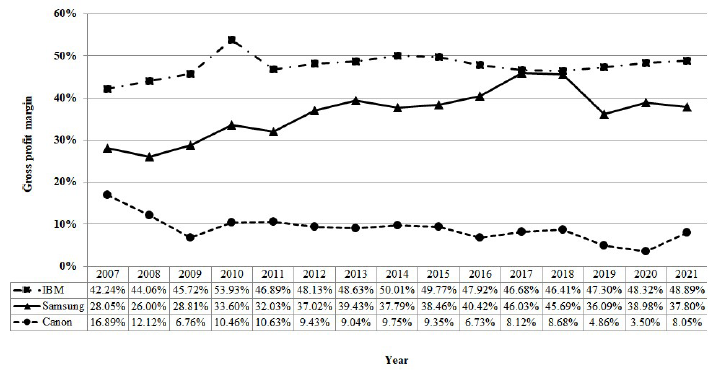

The results obtained in the second stage are presented below. The percentage value of the calculated gross profit margins for IBM, Samsung and Canon during the period from 2007 to 2021 are presented in Figure 1.

The highest gross profit margin of 51.93% was recorded for IBM in 2010, which means that for every USD 1 of revenue, a gross profit of 53.93 cents was generated. The lowest value of 46.31% was recorded for IBM in 2018, which means that for every USD1 of revenue, a gross profit of 46.31 cents was generated. For Samsung, the gross profit margin was also considerably high. Samsung’s highest gross profit margin was identified in 2017 at 46.03 cents of revenue per USD1. Its lowest gross profit margin was in 2008 with 26 cents of revenue per USD1. The lowest gross profit margin calculated in the entire period from 2007 to 2021 was for Canon. Its highest gross profit margin was obtained in 2007 at 16.89 cents of revenue per USD1, and its lowest was in 2020 at only 3.5 cents of revenue per USD1. Figure 1 also shows the gross profit margin values for the 2018–2019 subperiod immediately preceding the pandemic and for the 2020–2021 pandemic subperiod. The calculations indicate that IBM’s gross profit margin increased during both the subperiod preceding the pandemic and the pandemic subperiod. For Samsung and Canon, there was a decline in their gross profit margins in the 2018–2020 subperiod and a slight but important increase during the 2020–2021 pandemic subperiod. These results led to the conclusion that the COVID-19 pandemic had no significant impact on the gross profit margins of IBM, Samsung and Canon during this period.

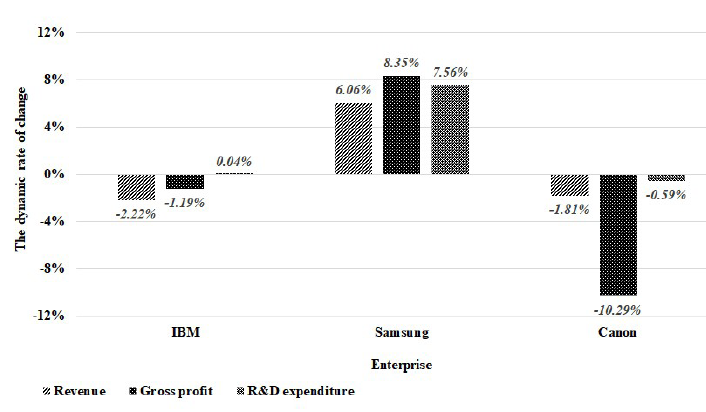

The values of the dynamic rate of change over the period from 2007 to 2021 are presented in Figure 2.

IBM’s results indicate that its revenue and gross profit margin decreased over time by an average of 2.22% and 1.19%, respectively, whereas its R&D expenditure increased marginally by an average of 0.04%. Therefore, for IBM, it can be concluded that its R&D expenditure remained at almost the same level, and it was its growth strategy that led to these results. For Samsung, its revenue, gross profit and R&D expenditure increased over time by an average of 6.06%, 8.35% and 7.56%, respectively each year. Canon’s revenue, gross profit and R&D expenditure decreased over time by an average of 1.81%, 10.29% and 0.59%, respectively in each year of the research period. It was also identified that IBM’s R&D expenditure remained at the same level, which also suggests that the results are a consequence of its growth strategy. It is also important to note that the results of the dynamic rate of change represent change over the 15-year period (2007–2021), where the last 2 years are the subperiod of the pandemic. Therefore, the results presented in Figure 2 should be interpreted in the context of this 15-year period and not based only on the 2-year pandemic subperiod. Canon’s significant decrease in gross profit margin compared to its small revenue decrease suggests that it experienced some internal problems during the period from 2017 to 2021. Additionally, the values of Canon’s and IBM’s R&D expenditure were similar, and Samsung’s R&D expenditure increased. This indicates that each enterprise implemented a growth strategy rather than suffering any impact of the pandemic, which would have caused a significant decrease in their expenditure.

In summary, the results of studies presented in the relevant literature definitely suggest that COVID-19 had a negative impact on various levels and fields of economic life and business activities, such as rising social and business isolation, and health and unemployment issues (Sawkat, 2021; Yahya et al., 2021). Research studies also highlighted that costs of business operations increased in many business activities and international cooperations, which resulted in the economic slowdown of domestic economies (Lassoued & Khanchel, 2021). However, based on the results of this research presented above, it can be concluded that the leading ICT enterprises—IBM, Samsung and Canon—coped remarkably well with the negative impacts of COVID-19. The research generally revealed that there was no significant negative impact of COVID-19 on the financial performance of enterprises covered by this research.

Conclusions

The main aim of this article was to present the results of research on the impact of the COVID-19 pandemic on the financial performance of three leading ICT enterprises—IBM, Samsung and Canon. The reasons for choosing these enterprises are that they belong to the ICT sector and they have obtained the highest number of patents from the USPTO among all industries and enterprises over the last 20 years (USPTO, 2021). Furthermore, IBM was the uninterrupted leader in the number of obtained patents from the USPTO for over 20 years (USPTO, 2021). The R&D expenditure is one of variables that describes the financial performance. The main research question was: Have leading ICT enterprises experienced significant changes in revenue, gross profit and R&D expenditure during the pandemic? This question was answered by the results obtained from a two-stage comparative analysis of two periods before and during the COVID-19 pandemic and dynamic changes in the values of financial indicators over the 15-year research period.

Comparative analysis and evaluation were carried out based on the most important financial indicators—revenue, gross profit, R&D expenditure and gross profit margin. All these indicators are important for the evaluation of an enterprise’s financial performance. The comparative analysis covered two periods—before and during the COVID-19 pandemic. The results obtained from the comparative analysis in terms of changes in the values of the above-mentioned indicators show that the smallest fluctuations (both in the period before the pandemic and in the period during the pandemic) were recorded for IBM, whereas the largest fluctuations were recorded for Canon. A decrease and an increase in the values of the indicators covered by the research were recorded in both periods. This proves that the COVID-19 pandemic had no significant impact on the financial indicators of IBM, Samsung and Canon during the research period. It also proves that the impact of the pandemic on business operations is not always negative. Achieving better results could be a result of taking advantage of emerging business opportunities where others only saw and highlighted threats and obstacles. Changes in the R&D expenditure of the enterprises covered by the research showed that there were no significant changes in the implementation of growth strategies due to the COVID-19 pandemic. The changes in the values of the indicators in both periods identified by the comparative analysis resulted from socio-economic and business conditions rather than a direct impact of the COVID-19 pandemic.

The results of the enterprises’ gross profit margins showed that the pandemic had no significant impact on their financial performance. The dynamic rate of change of their R&D expenditure during the period 2007–2021 suggested that it was a result of the growth strategy of each enterprise rather than a direct impact of the pandemic.

The results of the comparative analysis presented in this article led to the conclusion that the COVID-19 pandemic did not have a significant impact on the financial performance of the leading ICT enterprises that were subjects of this research—IBM, Samsung and Canon.

Future Research

Undoubtedly, the research conducted has provided new knowledge on the impact of the COVID-19 pandemic on leading companies in the ICT industry. However, it should be taken into account that the full impact of COVID-19 may not yet be measurable. Therefore, further research with an extended scope, more comprehensive financial performance indicators and beyond the ICT sector is important for both researchers and business specialists, as it can provide a new and more comprehensive understanding of the impact of COVID-19 on the business activities of global enterprises. New knowledge about the effects of such an unexpected phenomenon will allow us to gain a better understanding and prepare for similar phenomena in the future, as well as to integrate the identified issues into the growth strategies of global enterprises.

Limitation of This Study

This study covers basic and fundamentally important financial variables. Therefore, it cannot be treated as a comprehensive financial report related to the selected enterprises. The methods of calculating the results and performing the analysis and evaluation were adjusted to the duration of COVID-19. However, it must be considered that the effects of COVID-19 may also appear later and in the longer term. The negative effects of the pandemic initially affected human health, which is a factor that significantly changes over time and, in turn, affects the work performed and consequently the financial results achieved. The conclusions presented in this research may serve as indications for conducting in-depth research on the impact of COVID-19. The future research along with other methods used in analysis and evaluation can provide new and more comprehensive results about the impact of COVID-19 on global enterprises.

The Input Data Time Series

Footnotes

Acknowledgment

The author is grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.