Abstract

The COVID-19 pandemic represented an unexpected shock to the global economy, with a significant impact on business and consumer behaviour, particularly on spending and payments. This article aims to identify the drivers affecting consumers’ payment behaviour in Italy during the COVID-19 lockdown. We develop an empirical study, using structural equation modelling on data collected from 2,872 consumers in the period May 2020–June 2020 through the computer-assisted web interviewing methodology. A robustness check is run with an ordinary least squares (OLS) regression analysis. The findings highlight the positive and significant effect of COVID-19 worries on consumers’ payment behaviour. The uniqueness of this work derives from the creative approach with which it investigates the financial and social consequences of the COVID-19 crisis and focuses on possible solutions to encourage the adoption of innovative tools.

Introduction

In the last three years, consumer behaviour (Ardizzi et al., 2020) has changed markedly due to the COVID-19 pandemic and its dramatic consequences. The growth in the spread of smartphones and the usage of the internet due to the lockdown given the fear of contagion constituted an opportunity for the adoption of contactless and mobile payments, even for people with low financial knowledge and weak digital skills. In the most severe period of the pandemic, many individuals feared they could contract the virus through the exchange of cash, instead preferring to utilize payment instruments that would not expose them to dangerous situations (Ardizzi et al., 2020): during the lockdown, the amount of transactions through contactless cards increased from 35% to 55% (Perrazzelli, 2021). While previous works explore the impact of COVID-19 on consumer behaviour, in the literature, we could find no research on the role of the pandemic on payment behaviour. This article fills this gap by observing how the fear of COVID-19 contagion changed individuals’ payment behaviour in Italy. The Italian case deserves to be investigated because the use of cash is still widespread and the results may also be relevant for other countries with a similar culture (Ardizzi et al., 2021; Bank of Italy, 2020). Moreover, Italy is one of the countries that has been most affected by the pandemic, especially in the initial stages of the spread of COVID-19. By adopting a structural equation model (SEM), we find that concerns about the COVID-19 contagion and the change in purchasing behaviour that occurred during the lockdown pushed individuals to use mobile and contactless payment tools.

We believe that this article can contribute to the existing literature from several points of view. From a theoretical viewpoint, our research contributes to marketing and finance studies, increasing the knowledge on the link between emotions, consumers’ behaviour and m-payment adoption (Husain et al., 2020; Wisniewski et al., 2021). From an operational perspective, the new payment habits of Italians are pushing banks and financial operators to innovate their payment services. On the other hand, with the increase in mobile and contactless payment adoption, the costs of cash can be decreased, due to the decrease in cash usage: the advantage is being able to reallocate this saving to other sectors that need it. Finally, the results of this investigation are salient for regulators and policymakers interested in mobile and cashless payment users’ protection in relation to their financial knowledge level.

The remainder of this work is organized as follows. The first part presents the literature review regarding the relationship between payment behaviour and COVID-19, financial literacy, and the usage of information and communication technologies (ICT), highlighting the study’s hypotheses. The second section describes the research design, the survey construction and the econometrical procedures, followed by the presentation of the results. Finally, we discuss the outcomes, focusing on implications, limitations and future research avenues.

Literature Review

Payment Behaviour and COVID-19

Money is literally dirty. Passing cash from hand to hand makes it a receptacle for viruses and bacteria of all kinds and types (Jenkins, 2001; Maron, 2017; Tanglao, 2014; Thomas et al., 2008): after analysing bacterial survival, Vriesekoop et al. (2016) find a high microbial persistence on banknotes, polymer bills and coins.

The COVID-19 outbreak increased apprehension about handling potentially contaminated cash, and the idea that diseases can spread through coins and banknotes was emphasized, a view supported by the World Health Organization (WHO) (Abdillah, 2020; Cevik, 2020; Husain et al., 2020; Kakushadze & Liew, 2020; Pal & Bhadada, 2020). The costs and benefits of different payment methods were temporarily changed by this situation. The usage of cash, which became more expensive in terms of health risks, also became less convenient in comparison to the use of the debit card, the cost of which was reduced (Jonker et al., 2020).

Bhatia et al. (2023) analyse the intermittent continuous adoption behaviour of users of digital payment services (contactless, cashless and paperless forms of payment) during the COVID-19 pandemic, finding that an appropriate level of expectation leads to neutral satisfaction and intermittent continuous adoption behaviour by users. Via a structural equation modelling (SEM), Purohit et al. (2022) reveal that continuation intention in the digital payment use is influenced by subjective well-being, facilitating conditions, effort expectancy and satisfaction.

Ramos de Luna et al. (2023) show that perceived safety, perceived usefulness, perceived compatibility and subjective norms have a significant effect on the intention to adoption them and that subjective norms play a key role if the user has the opportunity to use mobile payment and receive adequate information.

Using two-stage least squares analysis, Cevik (2020) observes a reduction in the demand for cash due to the increase in the spread of infectious diseases, with the same macroeconomic financial and technological conditions. Collecting survey data on a representative panel of Dutch consumers during the first phase of the COVID-19 pandemic, Jonker et al. (2020) document a change in payment preferences. Examining habits regarding cash and cashless payments at the point of sale during the COVID-19, Wisniewski et al. (2021) highlight a preference for contactless transactions in the event of a high risk of infection, demonstrating the intention to move away from cash even after the end of the pandemic through the use of m-payment methods such as the QR code (Anderson et al., 2020; Kasab et al., 2020; Yan et al., 2021). According to Husain et al. (2020), safety is the motivation that pushes individuals towards cashless payments to safeguard against COVID-19. These arguments lead to Hypothesis 1:

H1: Individuals’ payment behaviours have changed due to the fear of COVID-19 infection.

Payment Behaviour and Financial Literacy

All national economies benefit from the financial inclusion of as many people as possible, for several social and economic reasons (Lusardi, 2019; Lusardi & Mitchell, 2011). According to Grohmann and Menkhoff (2017), financial literacy for the general population promotes financial inclusion, making individuals free and aware of their own choices: based on their level of financial knowledge, financial consumers are able to choose the services, tools, instruments and/or channels most in line with their characteristics.

Some scholars have considered the relationship between payment behaviour and financial literacy. The most literate individuals from an economic and financial point of view appear to demonstrate more capable debt management (Lusardi et al., 2015), better management of credit cards (Hamid & Loke, 2020; Klapper & Lusardi, 2019; Nicolini & Haupt, 2019; Shefrin & Nicols, 2014) and greater prudence in paying bills on time, tracking expenses and budgeting (Hilgert et al., 2003).

Interviewing a sample of Indonesian students, Gunawan (2023) shows that financial literacy and financial technology payments have a significant effect on consumption behaviour. Analysing the financial literacy score based on the standard financial literacy quiz conducted in India, Lahiri and Biswas (2022) find that less than 9% of individuals answered correctly the questions capturing all four aspects of financial literacy. Moreover, they find that financial literacy increases financial planning and that this, in turn, could improve financial behaviour.

Another literature branch examines the usage of payment instruments in relation to financial literacy (Arango et al., 2015; Marcotty-Dehm & Trütsch, 2021; van der Cruijsen et al., 2017). Financial literacy shows a significant and negative relationship to the use of m-payments (Kirana & Havidz, 2020; Liao & Chen, 2020), even for young users (Lusardi et al., 2018). However, there are no studies that consider how the lockdown has changed individuals’ payment habits, especially in those countries where the use of cash is still high.

These arguments lead to Hypothesis 2:

H2: During the COVID-19 pandemic, individuals used alternative payment instruments instead of cash, such as contactless cards and m-payments, independently of their level of financial literacy.

Payment Habits and ICT

Alternative payment instruments are considered on a par with new technologies, as innovation plays a crucial role in shaping user perceptions and decisions regarding technology adoption (Dahlberg et al., 2015; Liébana-Cabanillas et al., 2020; Shankar & Datta, 2018; Singh et al., 2017; Yi et al., 2006). With this motivation, the usage of alternative payment instruments is often investigated in relation to ICT adoption habits. Yi et al. (2006) demonstrate that innovativeness is a pivotal determinant of a user’s continuance intention to use alternative payment instruments. Liébana-Cabanillas et al. (2020) find that the innovativeness is positively and significantly related to the perceived usefulness of m-payments.

Administering a questionnaire to a sample of 288 people from February to May 2019, Dahab and Soudiè (2022) observe that perceived usefulness is verified as a mediating variable in the relationship between experience and intention to use m-payment. Zhang et al. (2022) find that a positive effect is attributed to the benefits of mobile payment in improving the financial inclusion and convenience of consumption activities in rural areas.

Another branch of studies identifies a small number of significant factors which are behind the increased usage of alternative payment instruments, such as high internet connectivity, the accessibility of mobile data, the existence of a strong wireless network and an inclination towards new and innovative technology (Kumar et al., 2021; Patil et al., 2017; Sinha et al., 2019). The analysis of the relationship between consumer spending behaviour, m-payment and the device used constitutes another field of literature (Dodini et al., 2016; Meyll & Walter, 2019; Shah et al., 2016).

During lockdown, sales of mobile devices have not only increased for study and work reasons, respectively, for young people and for several types of workers, but also to protect sociality, especially for the elderly. The growing number of mobile device owners, alongside other factors, could push traditional financial intermediaries to offer alternative payment services and instruments to attract new customers and open new markets. The proliferation of mobile devices could motivate users to use these devices for consumption needs as well, often coinciding with the adoption of alternative payment instruments.

These arguments lead to Hypothesis 3:

H3: During the COVID-19 lockdown, the usage of alternative payment instruments increased due to technological innovation and the proliferation of mobile devices.

Research Methods

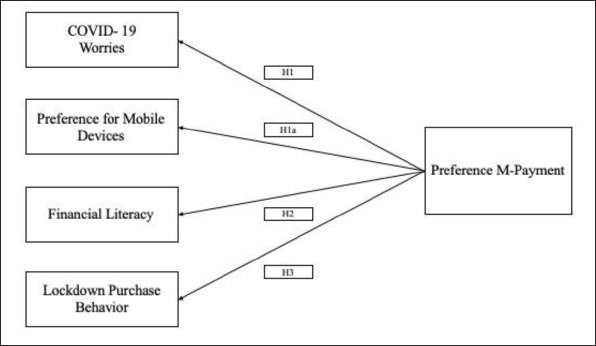

To obtain the information for the analysis, we administered a questionnaire that included questions about the COVID-19 worries and financial literacy of the respondents, their assessment of lockdown purchase behaviour, preference for m-payment and, in addition, mobile devices used for m-payment, sociodemographic characteristics—such as age, gender, marital status and education level—and socioeconomic features, including work status and income. A factor analysis was employed to define the main components of their COVID-19 worries, financial literacy, preference for m-payment and lockdown purchase behaviour. We utilized the Promax rotation criterion to treat the questions with the maximum likelihood method. We adopted the principal components resulting from the factor analysis for two purposes: (a) to construct a structural equation model (SEM) to test the hypotheses of our research (Figure 1), and (b) as dependent variables of a linear regression model employed in this research to strengthen the results obtained by the SEM.

Conceptual Model.

Construct Measures

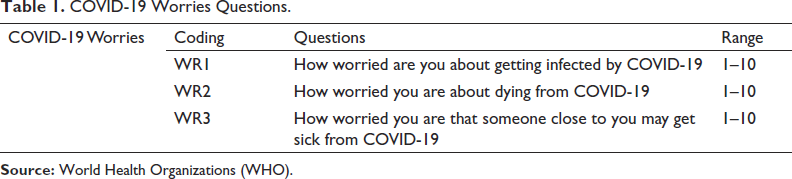

Based on the literature review about COVID-19 worries, m-payment behaviour, financial literacy and lockdown purchase behaviour, a survey instrument was developed as part of this study. Regarding COVID-19 worries, we adopted an official document published by WHO, titled ‘Survey Tool and Guidance: Behavioural Insights on COVID-19’ (first release). The variables and their related codes are described in Table 1. We summarized all the questions on a 10-point Likert scale, where 1 stands for not very worried and 10 for very worried.

COVID-19 Worries Questions.

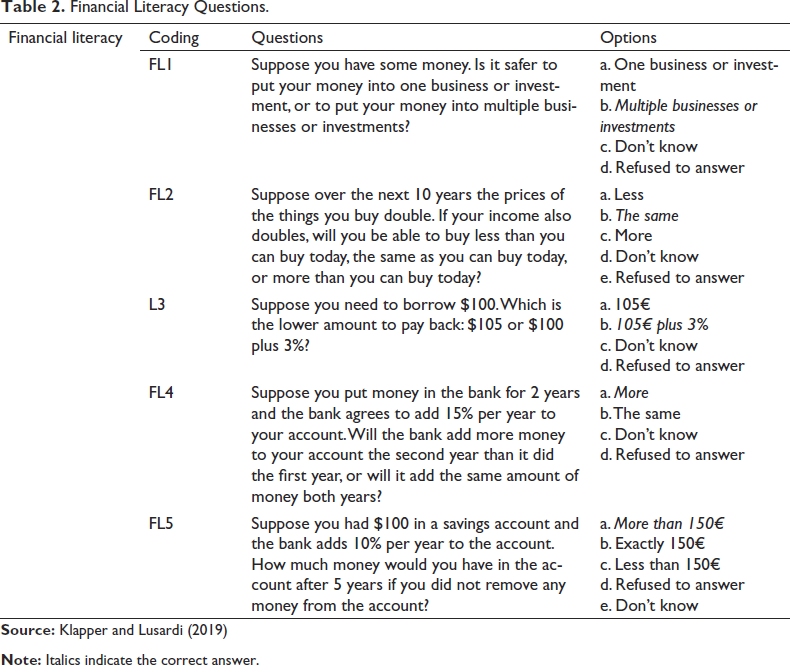

To measure financial literacy, we used Standard and Poor’s Global FinLit Survey (Klapper & Lusardi, 2019). The outcome of each question determined the knowledge of a specific financial theme (Table 2).

Financial Literacy Questions.

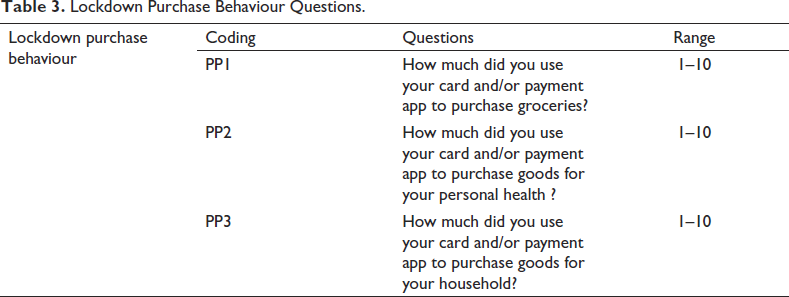

To analyse the effects of lockdown purchase behaviour, we created three questions. We summarized all the questions on a 10-point Likert scale, with 1 standing for not at all and 10 for very much (Table 3).

Lockdown Purchase Behaviour Questions.

To verify how and whether COVID-19 pandemic influences Italians’ purchase preferences, we developed three questions. We summarized all the questions on a 10-point Likert scale, with 1 standing for not at all and 10 for very much (Table 4).

Preference on M-payment.

The last session was about the preference for mobile devices, choosing between smartphones, tablet and desktop/laptop computers.

Data Collection

The data collection was carried out through the administration of questionnaires in Italy from the beginning of May 2020 until the end of June 2020, using computer-assisted web interviewing (CAWI). The adoption of the CAWI method was necessary given the lockdown restrictions imposed by the Italian government in the same period.

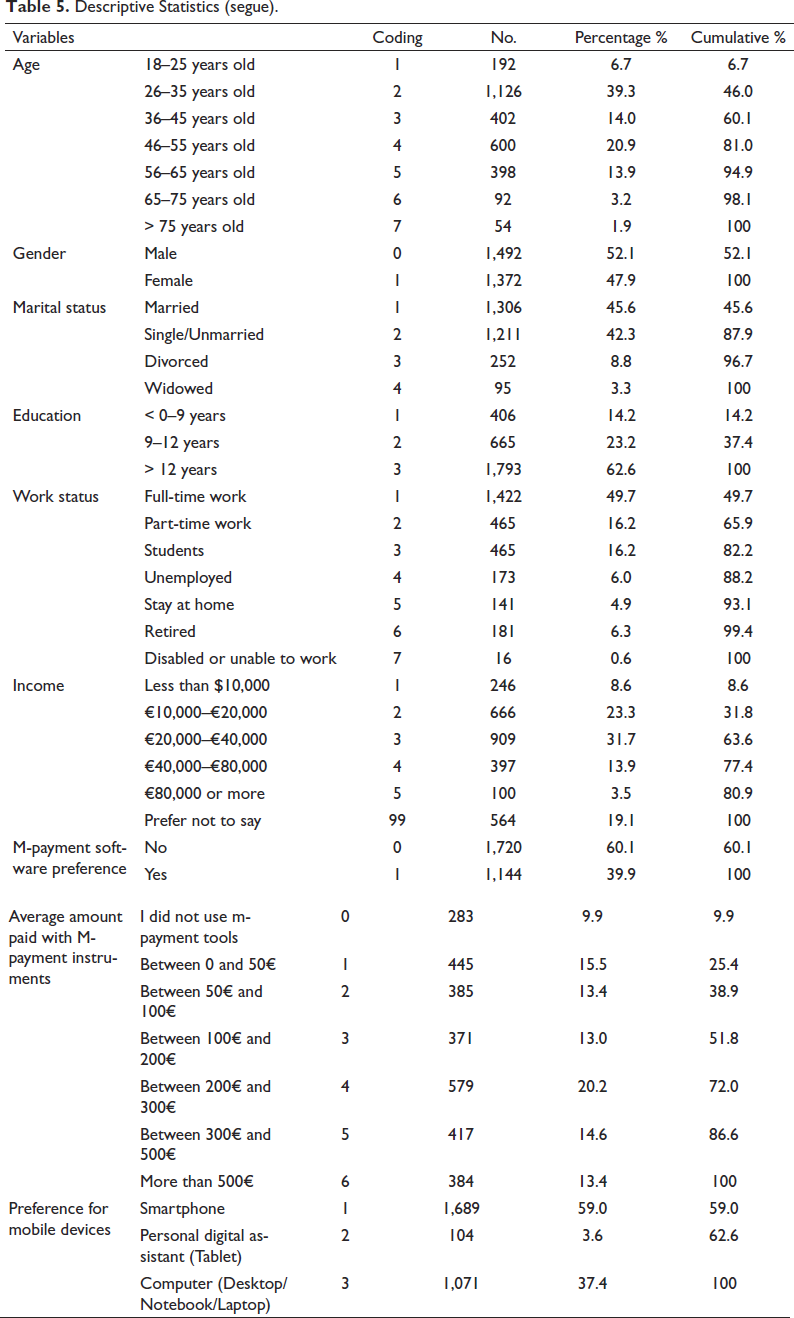

Through social media platforms such as Facebook, Twitter and LinkedIn, we invited approximately 3,000 randomly selected individuals to participate, collecting 2,950 questionnaires. After deleting those with missing values (Schlomer et al., 2010), the final sample was composed of 2,872 questionnaires. According to Dattalo (2008), the sample appeared to be representative of the Italian population. Table 5 presents the descriptive statistics.

Descriptive Statistics (segue).

Research Tool

To analyse the relationship between payment habits during the period of the March lockdown, the relationships between financial literacy and the adoption of mobile/electronic payments, we conducted a second-order SEM analysis.

A SEM is a recent statistical data analysis technique that allows the direct or indirect effect of causal factors on the evolution of an accident scenario to be estimated and its relationships assessed (Faraci & Musso, 2013; Jain et al., 2016; Khan et al., 2019; Shankar & Datta, 2018). One of the main objectives of this model is to understand whether, given a theoretical model, its reliability and accuracy can be verified with real data (Raykov & du Toit, 2005): goodness indices are used by strictly setting reference values. The SEM is well structured and suitable for empirically explaining what is claimed in the theoretical model if the goodness indices are confirmed.

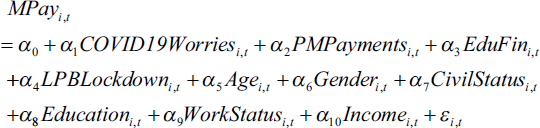

As a robustness check, we ran an OLS regression model, as follows:

where subscripts i and t, respectively, denote the cross-sectional dimension and temporal dimension of the analysis, preference for m-payment (MPay it ) is the dependent variable describing Italians’ use of m-payments, COVID-19 worries (COVID19Worriesit) represents concerns about COVID-19, preference for mobile devices (PMPayments it ) describes Italians’ purchasing behaviours during lockdown, financial literacy (Edufinit) identifies the level of financial literacy, and lockdown purchase behaviour (LPBLockdown it ) describes Italians’ behaviour during lockdown. Age, gender, civil status, education, work status and income are the control variables.

Data Analysis

Validity and Reliability of the Scale

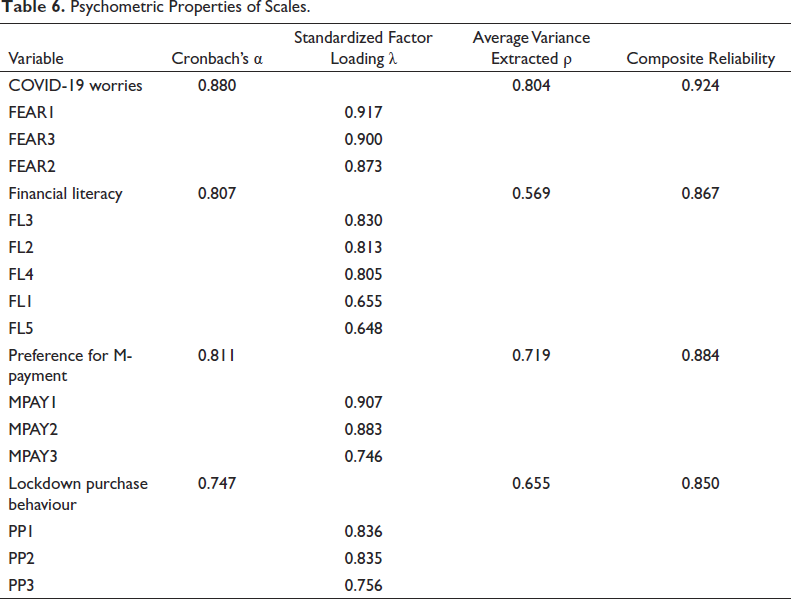

To ascertain whether and in what manner the elements of preference for m-payment can be clustered into primary components, we performed a principal components analysis (PCA), employing Promax rotations. Following the recommendations given by MacCallum et al. (1999) and Raubenheimer (2004), a minimum of three questions have been designated to the constructs of COVID-19 worries, financial literacy and lockdown purchase. In line with the insights of Jolliffe and Cadima (2016), a PCA facilitates an accurate interpretation of data culled from substantial datasets by mitigating the problem linked to eigenvalues/eigenvectors. With respect to the rotation method used in tandem with a PCA, Russel (2002) posits that the Promax method seems more suitable, particularly in cases like this study where the measurement scales appear to exhibit correlation with one another. Utilizing the Cronbach’s alpha value to test the validity of model, we found a value greater than the minimum acceptable value of 0.7 (Taber, 2018). All constructs showed an average variance extracted (AVE) value higher than 0.50 (Diamantopoulos & Siguaw, 2000; Fornell & Larcker, 1981; Hair et al., 2010). Finally, all constructs demonstrated composite reliability (CR) values greater than 0.80 (Netemeyer et al., 2003) and lower than 0.95 (Hair et al., 2017) (Table 6).

Psychometric Properties of Scales.

Findings from the SEM Analysis

The expected results predicted that financial literacy level, COVID-19 worries, lockdown purchase behaviour and preference for mobile devices determine the latent variable preference for m-payment. Based on the suggestions provided by Hu and Bentler (1999), the SEM fit indices showed a very good model fit (

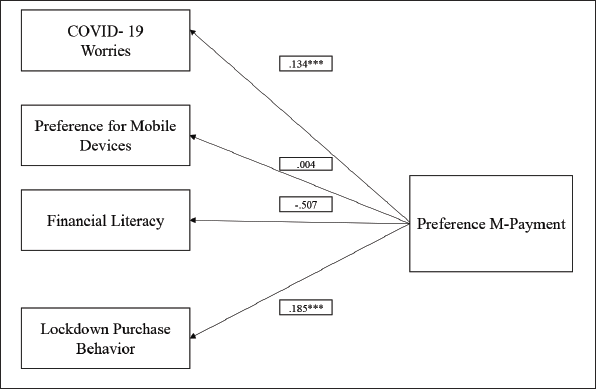

Figure 2 displays the findings. Financial literacy level and COVID-19 fear, lockdown purchase behaviour and preference for mobile devices jointly contribute to preference for m-payment. COVID-19 worries (standardized path coefficient [SPC] = 0.134; p < .000) and lockdown purchase behaviour (SPC = 0.185; p < .000) have a positive and statistically significant impact on preference on m-payment, confirming H1 (Cevik, 2020; Husain et al., 2020; Yan et al., 2021).

Structural Model.

Contrary to previous studies (Dahlberg et al., 2015; Liao & Chen, 2020; Lusardi et al., 2018; Meyll & Walter, 2019), financial literacy shows a negative and statistically unsignificant relationship with preference for m-payment (SPC = –0.507; p > .01). Due to the lockdown, individuals were forced to use m-payments to meet their basic needs, regardless of their level of financial knowledge.

Contracting previous studies (Dahlberg et al., 2008, 2015; Liébana-Cabanillas et al., 2020; Singh & Sinha, 2020), preference for mobile devices has a positive and unsignificant relation with m-payment (SPC = 0.002; p > .01), highlighting that the propensity to use m-payments is not conditioned by the device utilized to make the purchase.

Robustness Test

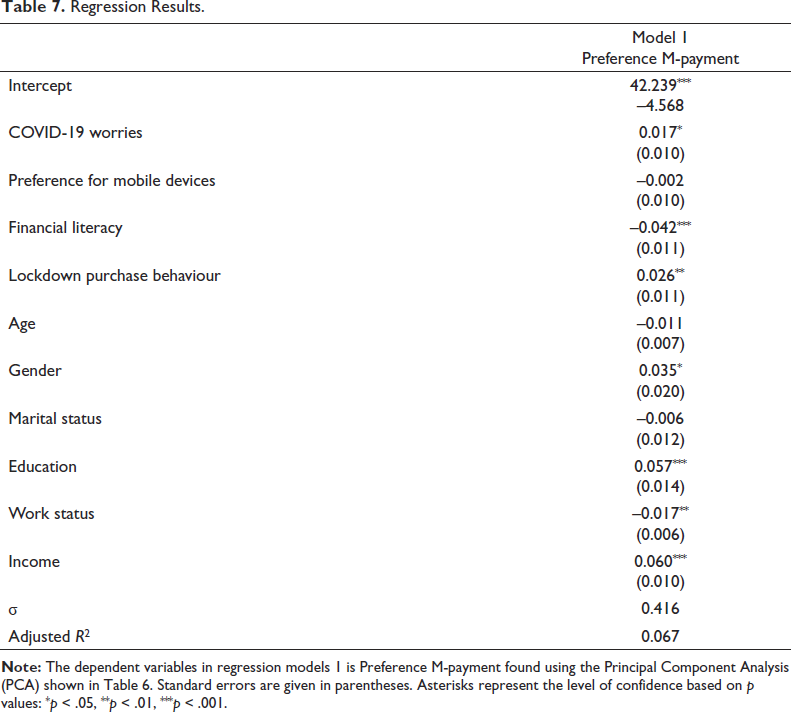

Table 7 shows the results of robustness check run with the OLS regression.

Regression Results.

m-payment is a function of COVID-19 worries, financial literacy and lockdown purchase behaviour. Compared with the previously proposed model, financial literacy, which was not significant in the previous model, has a negative and significant relationship with preference for m-payment in the regression model. The results establish how individuals with low financial literacy will be the most likely to prefer m-payment instruments to make payments. By extending the analysis to socioeconomic and sociodemographic variables, it is possible to show that higher levels of education and income are associated with a greater preference for m-payment instruments. Furthermore, with regard to gender, men seem to be more likely to prefer m-payment instruments for the purchase of goods and services than women. Employment status in our regression model is also an interesting variable in determining preference towards m-payment instruments. In fact, on our baseline sample, respondents who reported having more stable employment contracts are the most likely to use m-payment tools. Therefore, the linear regression model allowed us to confirm and extend the results expressed in the structural equation model (Figure 2).

Discussion

Due the COVID-19 pandemic and new technologies, consumers’ behaviours have changed dramatically. Due to the lockdown, the Italian government promoted several initiatives and strategies, such as e-commerce and digitization, to allow consumers to avoid direct physical contact, increasing the adoption of m-payment. Our study aimed to investigate the drivers of Italian m-payment usage during the lockdown, underlining the main implications. Using a SEM technique on data collected from 2,872 consumers in the period May 2020–June 2020 collected through the CAWI methodology and verifying the robustness of the results with an OLS regression, we found a positive and significant relationship between COVID-19 worries and consumers’ payment behaviour, while financial literacy and the spread of mobile devices do not seem to particularly influence consumer payment behaviour.

From a theoretical point of view, our research enriches the literature on consumers’ payment behaviour. Consumption habits are central in payment behaviour: when consumers buy goods or services, the importance they give to the purchasing experience and the preference for the use of cash linked to the conviction of greater control of expenses have long conditioned the diffusion and the usage of non-contact payment tools, such as contactless payment cards and apps. Existing studies (Abdillah, 2020; Cevik, 2020; Husain et al., 2020; Kakushadze & Liew, 2020) have shown how hand-to-hand money swapping could be a transmission vehicle for the COVID-19 virus. The fear of contagion on the one hand and the lockdown that has forced families and individuals into their homes for long periods of time on the other have proved stronger than the preference for the use of cash and resistance to the utilization of m-payments among Italians. For this reason, it is believed that this article also has implications for the behavioural literature, contributing to an enrichment of the literature relating to the influence of emotions on the payment behaviour of individuals (Guha et al., 2013; Risqiani, 2015).

From an operational and managerial point of view, Italians’ new payment behaviours and the ‘open banking’ model begun by Payment Service Directive 2 represent a revolution for Italian financial intermediaries, which are being driven to innovate. The possibility of moving towards the ‘unbundling’ of banking services opens competition in specific segments of the payment services value chain where aggressive pricing policies tend to capture market share from traditional operators.

From the policymakers’ point of view, the increased usage of m-payments could expose consumers to more fraud and data abuse. This topic confirms the critical nature of customer profiling and the effort that should be made to protect personal data in compliance with EU Regulation 2016/679 (General Data Protection Regulation), especially because the use of non-contact payments greatly increased during the pandemic. Given the changed Italian payment habits, regulators are also interested in fairness and transparency in the relationship between intermediaries and clients, as well as through policies aimed at increasing consumer awareness. Although the results of this research do not provide significant results, financial education programmes are of the utmost importance in making clients (users and merchants) aware of the differences between the various payment services as well as the opportunities, costs and risks associated with each one.

Despite its contributions, this study is certainly not without limitations, which suggest directions for future research. First, the data collection took place using an online survey and was limited to the Italian context, due to the lockdown period in which the questionnaire was administered. Future works could conduct both online and offline surveys with larger and more representative samples. Repeating the analysis in other countries will allow for a generalization of the results.

Second, the data collection was concentrated during the first Italian lockdown, in the period between March and May 2020. Unfortunately, Italy experienced other periods of generalized and partial lockdown in the following months linked to the second and third waves of the spread of COVID-19. Moreover, in December 2020, to incentivize the use cashless payments, a state cashback programme was launched in Italy. The change in the payment habits of Italians will be monitored to ascertain whether it persists in the long term. Future research will therefore have to consider a temporal extension of the analysis that considers these events to produce more reliable results and to estimate new variables, such as that relating to the state cashback programme, which are believed to influence the use of mobile and contactless payments in Italy.

Third, although this study does not show statistically significant results, the degree of the financial literacy of consumers and the proliferation of mobile devices are believed to affect their payment choices in the same way as investment decisions. Consumers with a higher level of financial education and knowledge will be able to choose the payment instrument that best suits their needs. Individuals who use mobile devices the most are more likely to make more use of m-payments because they are more familiar with the tool and because they are more likely to turn to e-commerce services. Future lines of research can take into consideration these aspects related to financial literacy and proliferation of mobile devices at a time not affected by the pandemic.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.