Abstract

This study examines the impact of board gender diversity on corporate risk-taking, moderated by the firm life cycle stages. Data from 200 non-financial firms listed on the Pakistan Stock Exchange (2018–2022) were analyzed using the system generalized method of moments. Corporate risk-taking, the dependent, was measured using systematic risk and total-risk proxies. Results showed that board gender diversity had an insignificant effect, firm life cycle had a negative significant impact, while the interaction term (board gender diversity and firm life cycle) showed a positively significant impact on risk-taking measured by total risk. In contrast, both factors, along with their interaction, positively influenced risk-taking when assessed through systematic risk. The study further segmented the firm life cycle into five distinct stages, finding that the impact of board gender diversity on risk-taking varied across stages. For instance, at the introduction and maturity stages, board gender diversity positively affected risk-taking for both proxies. However, at the growth and decline stages, its impact was insignificant. These findings suggest variability in the relationship between board gender diversity and risk-taking, potentially influenced by the choice of risk proxies. Theoretically, this study contributes to the body of knowledge on how a firm’s life cycle and board gender diversity influence corporate risk-taking. This study’s insight also holds significant implications for corporate governance and policymaking because, contrary to popular belief, the findings suggest that board gender diversity does not uniformly reduce risk-taking; instead, its impact varies with the firm’s life cycle stage.

Highlights

Board gender diversity (BGD)’s varied impact: The study reveals that BGD’s effect on corporate risk-taking (CRT) is not uniform but varies significantly with the firm’s life cycle stage (FLC).

Significance of FLC: It plays a crucial moderating role, with the interaction between BGD and FLC showing a positively significant impact on CRT. This underscores the importance of considering contextual factors like FLC in governance studies.

Implications for corporate governance: Contrary to common beliefs that gender diversity on boards universally reduces risk, findings suggest that the influence of gender diversity is more nuanced and dependent on FLC context. This has significant implications for policymaking and the structuring of corporate boards.

Introduction

Today’s business environment is highly turbulent, unpredictable and constantly changing, posing a risk to a company’s survival, growth and sustainability (Chen et al., 2015; Yasser, 2012). Corporate risk-taking (CRT hereafter) is an essential value-adding activity as it influences a firm’s decision-making regarding planning, budgeting, control and other key business areas (Baghdadi et al., 2023). While a well-calculated risk may lead to increased shareholders’ wealth and competitive advantage, excessive risk-taking can be disastrous (Muhammad et al., 2023).

Several factors, such as the firm’s risk policy, board gender diversity (BGD hereafter), system operational efficiency and competitive environment, can affect CRT behaviour (Firdaus & Adhariani, 2017; Sila et al., 2016; Teodosio et al., 2021). Gul et al. (2011) stated that BGD can help enhance risk management and, subsequently, higher performance. Critics of BGD argue that women are less likely to take risks, less confident and less emotionally stable than their counterparts (Barber & Odean, 2001; Dowling & Aribi, 2013; Levi et al., 2014). An increase in BGD may lead to poorer performance and growth, delays in decision-making and less competitiveness (Eckel & Grossman, 2008; Perryman et al., 2016). Sila et al. (2016) concluded that firms with less BGD outperformed those with higher levels of BGD in terms of profitability, market share and growth. Moreover, the firms differ significantly in their critical financial decision regarding capital structure, operations and mergers and acquisitions (Jianakoplos & Bernasek, 1998).

Advocates of BGD have a different perspective; they argue that the thinking, objectivity, behaviour and risk assessment of working women can be much different from housewives (Arnardottir & Sigurjonsson, 2018; Elomäki, 2018). BGD can help firms efficiently manage risk, make prudent and intelligent decisions, better manage information, improve firm performance and positively contribute to boardroom meetings (Firdaus & Adhariani, 2017; Nadeem et al., 2019). However, BGD may not produce benefits in a ‘patriarchal’ society (Low et al., 2015). Several researchers have termed Pakistani society a patriarchal society (Yasser, 2012).

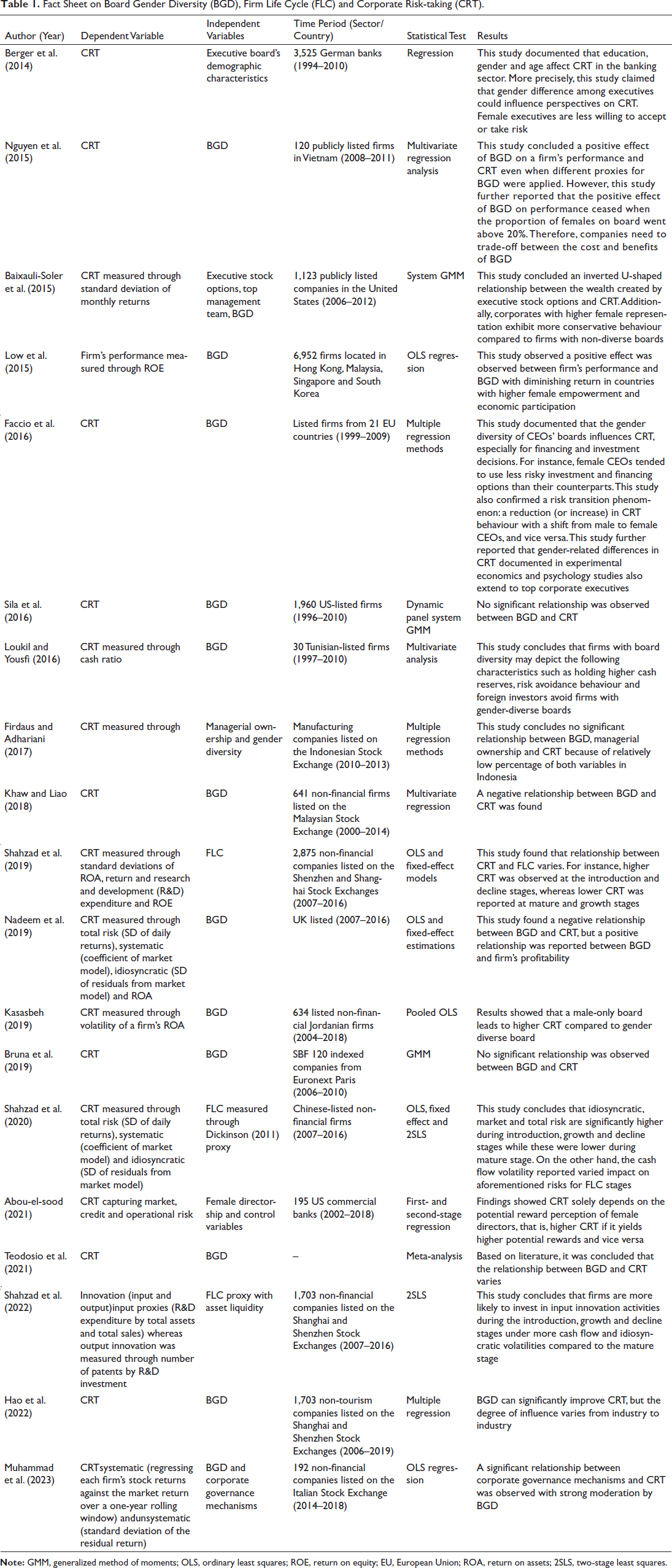

The literature indicated that BGD and CRT are important, yet to be explored, areas of research from diverse perspectives (Bannier & Neubert, 2016; Faccio et al., 2016; Harjoto et al., 2018). Most of the existing research up to now (see Table 1) has tended to examine either the impact of BGD on CRT (Teodosio et al., 2021) or the impact of CRT on firm’s life cycle (Habib & Hasan, 2015). Research has identified that a firm life cycle (FLC hereafter) can have multiple implications for its financial position, growth, size, information disclosure, board structure and CRT (Faff et al., 2016; Miller & Friesen, 1984). Anthony and Ramesh (1992) were the pioneers to introduce the term ‘FLC’, and Dickinson (2011) later proposed a new FLC model based on a firm’s cash flows.

Fact Sheet on Board Gender Diversity (BGD), Firm Life Cycle (FLC) and Corporate Risk-taking (CRT).

Fact Sheet on Board Gender Diversity (BGD), Firm Life Cycle (FLC) and Corporate Risk-taking (CRT).

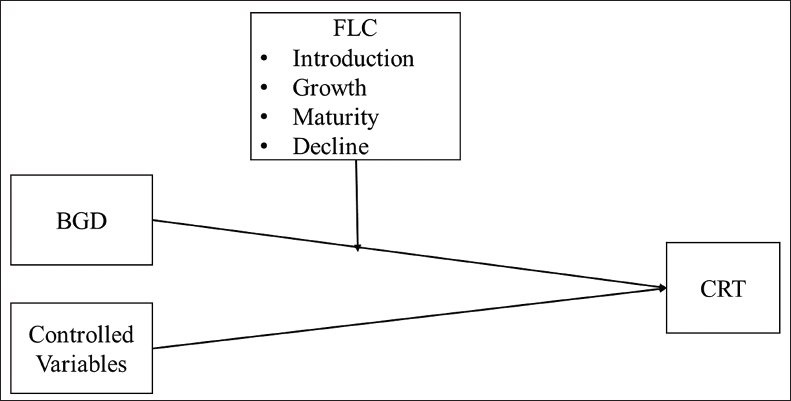

Miller and Friesen (1980) argued, as postulated in FLC theory, that an enterprise will go through several predictable stages, and the enterprise’s operationality, board structures, policies, resources and CRT will differ significantly. However, prima facie the relationship between BGD and CRT at distinctive firm life stages has not yet been thoroughly explored. This may lead to several research questions: (1) How does BGD affect CRT at different stages of FLC? (2) Are the findings consistent across different CRT proxies? (3) Are the theoretical foundations, BGD improves CRT, supported in the context of Pakistani listed firms? The search for an answer to these questions is the aim of the present investigation.

Therefore, the present research is novel in two key aspects. First, past studies, such as Hasan and Habib (2017), argued that CRT varies significantly for the distinctive stages of the FLC. This study would have been more useful and interesting if it had examined the moderation of BGD for FLC and CRT. Because Aghaei et al. (2018) argued that a firm’s structure, board composition, strategy and risk-taking behaviour will change at different life cycle stages. Although Hasan and Habib (2017) examined the impact of CRT on the FLC; however, firm’s structural element, especially BGD, was not taken into account. This study will address the shortcoming of present literature by considering the moderation of BGD at distinctive stages of FLC and CRT.

Second, representation of women on boards has increased significantly in recent years, albeit still lower than that of their counterparts. Volunteering and legislative quotas contributed to the growth of BGD (Adams & Ferreira, 2004). For instance, Norway has implemented a 40% compulsory quota system for females on the board of listed companies (Ahern & Dittmar, 2012). Despite considerable efforts to increase BGD, there is still a long way to go, particularly in developing countries like Pakistan (Yasser, 2012). For instance, although the number of directors in Pakistani listed companies has increased from 351 to 430 in recent years, Pakistan ranks 151 out of 153 countries in terms of gender parity and equality (Pakistan Stock Exchange, 2023). Additionally, Asghar (2021) and Asghar et al. (2022) reported that out of 9.07% of female directors, only 0.83% are non-executive while 8.25% were executive directors, mostly linked to the family, with little to no role in managing the company’s affairs. Considering this, it is important to investigate whether BGD, in the Pakistani context, truly contributes to improved CRT at different stages of the FLC.

This study works on the lines of agency theory coupled with corporate life cycle and behavioural decision-making theories to investigate the moderation of BGD at distinctive stages of FLC and CRT. Behavioural decision theory describes how individuals make decisions rather than how they ought to be, highlighting that men and women quite substantively differ in their decision-making, especially when confronting risk (Paul et al., 1984). Past studies referred to females as less emotionally stable, more risk-averse, less confident and more subjective decision-makers compared to their counterparts (Croson & Gneezy, 2009; Powell & Ansic, 1997). On the other hand, Shahzad et al. (2019) reported that men overestimate their decision-making abilities, underestimate risk and uncertainty and resources to cope with such risks and uncertainties. Hence, it is typically believed that females are less likely to take risk compared to males. This perspective is supported by agency theory, which suggests that such risk aversion can lead to underinvestment.

The traditional view on risk and return advocates that high risk would yield higher returns and vice versa (Dempster, 2002; Ganzach, 2001). The literature has found contradictory evidence regarding the traditional view of risk and return. For instance, firms reported a low or negative return for introductory and decline stages, while these stages posit a greater risk to the firms (Habib & Hasan, 2015). As per the corporate life cycle theory, an enterprise will go through several predictable stages, and the enterprise’s operationality, structures, policies, risk-taking and resources would differ substantively. As applied to this study, the theories mentioned earlier hold that board structure (proportion of females on board) could significantly impact CRT at different FLC stages (see Figure 1). Literature on CRT, BGD and FLC is summarized in Table 1.

H1: BGD has a significant impact on CRT.

H2: FLC has a significant impact on CRT.

H3: BGD has a significant impact on CRT with moderation of FLC.

H3a: BGD has a significant impact on CRT with moderation of FLC (introduction stage).

H3b: BGD has a significant impact on CRT with moderation of FLC (growth stage).

H3c: BGD has a significant impact on CRT with moderation of FLC (maturity stage).

H3d: BGD has a significant impact on CRT with moderation of FLC (decline stage).

The non-financial firms listed on the Pakistan Stock Exchange (PSX) were selected for this study because the regulatory and governance mechanism for financial firms is very different from non-financial firms. For instance, financial firms are also subject to certain regulations (i.e., banking regulations), though distinct from those for non-financial firms. A total of 475 non-financial firms are registered at PSX. After synchronizing data and eliminating the companies with missing observations for BGD, the final sample size shrunk to 200 non-financial firms from 2018 to 2022.

To investigate the relationship between CRT, BGD and FLC as a moderator, we used the system generalized method of moments (SGMM). Past studies such as Baixauli-Soler et al. (2015), Bennouri et al. (2018) and Sila et al. (2016) used GMM to examine the impact of BGD, FLC and CRT. Authors like Hermalin and Weisbach (2001) and Sila et al. (2016) claimed that some aspects of the board are not exogenous. Therefore, there is always a potential possibility of weak instrument identification. Similarly, Wintoki et al. (2012) argued that not all the characteristics included in the board are genuinely exogenous; culture, regulations and other factors might significantly influence on firm’s board composition. Therefore, it is essential to make BGD exogenous first. Hence, increasing the lag in SGMM makes the variable more exogenous. With that help, we can better identify the weak instrument. We generate the following dynamic base regression model for our study:

where

In previous studies, researchers used different methods to calculate CRT. We used two proxies of risk, systematic risk and total risk as used by Harjoto et al. (2018), Khaw and Liao (2018) and Nadeem et al. (2019). We measured total risk as the standard deviation of daily stock returns and systematic risk was calculated through beta coefficient on stock market portfolio (Khaw & Liao, 2018; Nadeem et al., 2019). We regressed the following model:

where

Literature reported two key proxies such as proportion of female on board and dummy to capture impact of BGD (Carter et al., 2003; Loukil & Yousfi, 2016). Authors like Gyapong et al. (2019), Liu et al. (2014) and Sila et al. (2016) used proportion of female on board to better capture the impact of BGD on CRT, therefore, this study also used the same proxy for BGD. Dickinson (2011) life cycle model was used to measure FLC for this study. According to which,

(i) Introduction, if CFO < 0, CFI < 0 and CFF > 0;

(ii) Growth, if CFO > 0, CFI < 0 and CFF > 0;

(iii) Mature, if CFO > 0, CFI < 0 and CFF < 0;

(iv) Decline, if CFO < 0, CFI > 0 and CFF ≤ or ≥ 0;

(v) Shake-out: remaining firm years will be classified as shake-out stage;

where,

CFO = cash flow from operations,

CFI = cash flow from investment,

CFF = cash flow from financing.

Control variables such as firm size were measured as logarithm of total asset (Nguyen & Nguyen, 2017), leverage as total debt divided by total assets (Gebhardt & Lee, 2000; Li & Li, 2013), firm age as years since founding (Athene, 2006), and ROA as a ratio of operating profit to total assets.

Results and Discussions

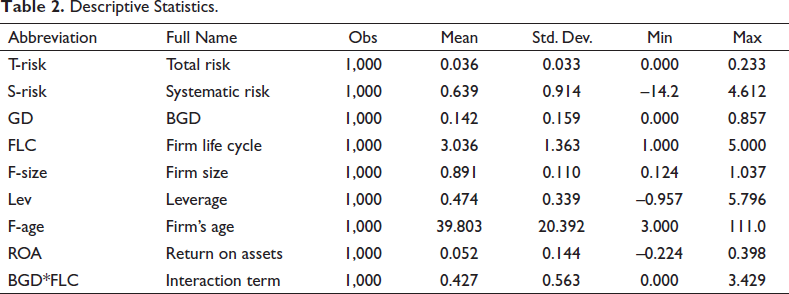

The descriptive statistics, such as total observations, mean, standard deviation, maximum and minimum values for the variables mentioned earlier, were calculated. These variables include CRT (measured through total and systematic risk), BGD, FLC, firm size, leverage, firm’s age and ROA. The results were reported in Table 2 to identify outliers and abnormal behaviour of variables in the data.

Descriptive Statistics.

Descriptive Statistics.

An interpretation was performed for crucial study variables such as total risk (T-risk hereafter), systematic risk (S-risk hereafter), BGD, FLC and the interaction term of BGD with the FLC. Descriptive statistics presented in Table 1 revealed that the mean value for T-risk was 0.036 with a standard deviation of 0.033. T-risk was measured through the standard deviation of daily returns for 200 indexed companies, with a higher standard deviation indicating a risky investment and vice versa. The maximum value for T-risk was 0.233, whereas the minimum was 0, suggesting that sample companies were moderately risky. Descriptive statistics also reported a mean value of 0.142 for BGD with a standard deviation of 0.159, BGD was calculated as the ratio of female directors to total board directors. The minimum value of 0 indicates that the board is not diversified, whereas the maximum value of 0.857 indicates that the firm has a diversified board. Descriptive statistics for the FLC reported a mean value of 3.036 with a standard deviation of 1.363. FLC was measured utilizing Shahzad et al. (2019) proxy. The minimum value of 1 indicates the firm was in the introductory phase, whereas the maximum value suggests a shake-out.

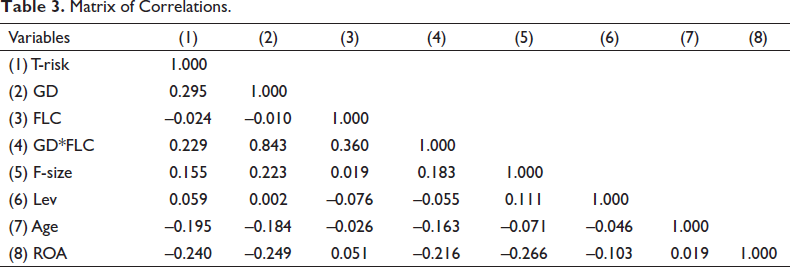

Bivariate correlation analysis was applied to examine the association between variables, and the results were presented in Table 3.

Matrix of Correlations.

Variable may posit no correlation, partial correlation or a perfectly positive or a negative correlation. The results of correlation analysis presented in Table 2 revealed a weak and a positive association between T-risk, BGD, firm size and leverage whereas variables such as FLC, firm age and ROA although reported a weak, however, a negative association with T-risk. Table 4 reports the results for one-step SGMM estimation estimated through robust command.

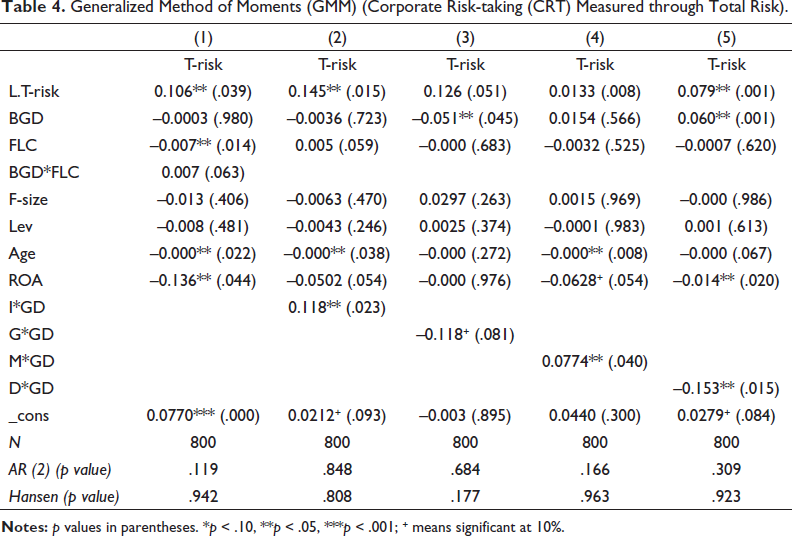

Generalized Method of Moments (GMM) (Corporate Risk-taking (CRT) Measured through Total Risk).

For all the estimates, number of groups was more remarkable than the number of instruments, and F-statistics were significant (less than 5%). Moreover, the p values for AR (2) and Hansen for all models were insignificant (greater than 5%), hence eliminating the possibility of second-order serial correlation and indicating the validity and accurate identification of instruments. The results for all GMM estimates also reported a significant lagged dependent variable (L.T-risk), suggesting that models are dynamic in nature and reversion behaviour where past risk-taking affects the current level of risk-taking.

The results of SGMM model 1 showed an insignificant impact of BGD (β-value –0.0003 and p value .980) on CRT (measured through T-risk), rejecting H1 that BGD has a significant impact on CRT. The negative sign of efficiency is consistent with the literature findings (Khaw & Liao, 2018; Nguyen, 2011), suggesting diversity might restrict risk-taking as conventionally believed that females are risk-averse. However, the relationship was statistically insignificant.

Further results revealed that FLC reported a negatively significant (β-value –0.007 and p value .014) impact on CRT (measured through T-risk), supporting H2 that FLC has a significant impact on CRT for the sampled companies during the 2018–2022 period. In other words, 1% change in FLC will reduce the CRT by 0.007, a negligible but statistically significant impact. Results also reported a positively significant (indicating a 10% significance level) impact of FLC*BGD (β-value 0.00754 and p value .063) on CRT, supporting H3. In other words, 1% change in BGD in FLC may increase CRT by 0.00754 at a 10% significance level. Past studies such as Perryman et al. (2016) concluded that a gender-diverse board might be risk-averse compared to a non-gender-diverse board. However, this study found that BGD may positively and negatively impact CRT at different FLCs. FLC comprises four distinctive stages: introduction, growth, maturity and decline. Therefore, it might be difficult to efficiently explain the impact of FLC on CRT. Hence, the impact of these distinctive stages was also examined. Control variables are generally consistent in terms of their significance and predicted direction. For example, large firms assume less risk, but firms with high growth opportunities take on more risk.

The results of SGMM model 2 again reported an insignificant impact of BGD (β-value –0.00361 and p value .723) on CRT, rejecting H1. However, the impact of FLC turned out to be positively significant (β-value 0.00558 and p value .059) on CRT, supporting H2 that FLC has a significant impact on CRT for the sampled companies during the 2018–2022 period. In other words, a percent change in FLC will increase the CRT by 0.00558, a negligible but statistically significant impact. Results also reported a significant positive impact of BGD*I (β-value 0.118 and p value .023) on CRT, supporting H3a, that is, ‘there is a significant impact of BGD on CRT with the moderation of FLC (introduction stage)’. In other words, a percent change in BGD at the introduction stage may increase CRT by 0.118. As mentioned earlier, no past study has examined the relationship between FLC and CRT with the moderation of BGD. Hence, directly comparing this study’s findings with the literature is difficult. However, findings were compared to the closest available literature. The positively significant impact of the introduction stage on CRT with the moderation of BGD is consistent with the findings of Hasan and Habib (2017), who also concluded a positively significant impact of the introduction stage on CRT. Although a negative sign was expected in the relationship between introduction and CRT with the moderation of BGD, a positive result was observed, considering females are risk-averse. The opposite sign was observed, possibly because of a patriarchal mindset, as identified by Low et al. (2015). Companies Act 2017 section 154 requires listed companies to have at least one female director on the board; otherwise, they may be penalized. To avoid penalties and to comply with a legal requirement, listed companies increased female board membership, but their role was symbolic instead of activity taking part in decision-making. Therefore, the interaction of BGD with the introduction stage yields the same sign as the impact of the introduction stage on CRT.

The results of SGMM model 3 reported a significantly negative impact of BGD (β-value –0.0514 and p value .045) on CRT, accepting H1. This result is consistent with the literature’s finding that increased BGD may reduce CRT (Barber & Odean, 2001; Dowling & Aribi, 2013). However, the impact of FLC was insignificant in model 3 (β-value –0.0009 and p value .683) on CRT. Results further revealed a negatively significant (at 10%) impact of BGD*G (β-value –0.118 and p value .081) on CRT, supporting H3b that ‘there is a significant impact of BGD on CRT with the moderation of FLC (growth stage)’. In other words, a percent change in BGD at the growth stage may reduce CRT by 0.118. The negatively significant impact of the growth stage on CRT with the moderation of BGD is consistent with the findings of Hasan and Habib (2017), who also concluded a negatively significant impact of the growth stage on CRT.

Past studies such as Al-hadi et al. (2015), Dickinson (2011) and Hasan and Habib (2017) argued that, at the growth stage, management has to undertake market or product expansion decision surrounding more significant uncertainties and risks. Considering this argument, a higher CRT was expected. However, the results showed a lower CRT at the growth stage with moderate BGD. This negatively significant relationship could be explained by agency theory. Management was expected to undertake a positive net present value project, requiring additional risk to increase shareholder wealth. However, management may forgo these positive net value projects if their interests are not well aligned with the interests of shareholders.

The results of SGMM model 4 reported a positive insignificant BGD (β-value 0.0154 and p value .566) impact on CRT, rejecting H1 that CRT has a significant impact on CRT. However, the result of FLC turned out to be insignificant (β-value –0.00325 and p value .525) impact on CRT. Further results revealed a significant positive impact of BGD*M (β-value 0.0774** and p value .040) on CRT, accepting H3c that ‘there is a significant impact of BGD on CRT with the moderation of FLC (maturity stage)’. In other words, a percent change in BGD at the maturity stage may increase CRT by 0.0774. The finding was compared with the closest available literature due to the unavailability of direct literature. The significant impact of the maturity stage on CRT with the moderation of BGD is consistent with the findings of Hasan and Habib (2017) and Shahzad et al. (2019), who also concluded that a positively significant impact of the maturity stage on CRT. In the initial phase, like at the maturity stage, firms like to take more risks and invest more to manage their assets (Shahzad et al., 2019).

The results of SGMM model 5 reported a significant positive BGD (β-value 0.0600 and p value .001) impact on CRT, accepting H1 that CRT has a significant impact on CRT. The result of FLC revealed a negative insignificant (β-value –0.00325 and p value .525) impact on CRT. Further results revealed a significant impact of BGD*D (β-value –0.153 and p value .015) on CRT, accepting H3d that ‘there is a significant impact of BGD on CRT with the moderation of FLC (decline stage)’. In other words, a percent change in BGD at the decline stage may decrease CRT by –0.153. As above mention, in the past, no study was examined, so this study faced difficulty while comparing directly with the literature, but the find was compared with the closest available literature. Shahzad et al. (2019) documented that at this stage, firms are associated with risk is given future performance. At this stage, firms sometimes invest in a negative NPV project because of their risk-avert approach. At this stage, firms must manage their assets and position in the market.

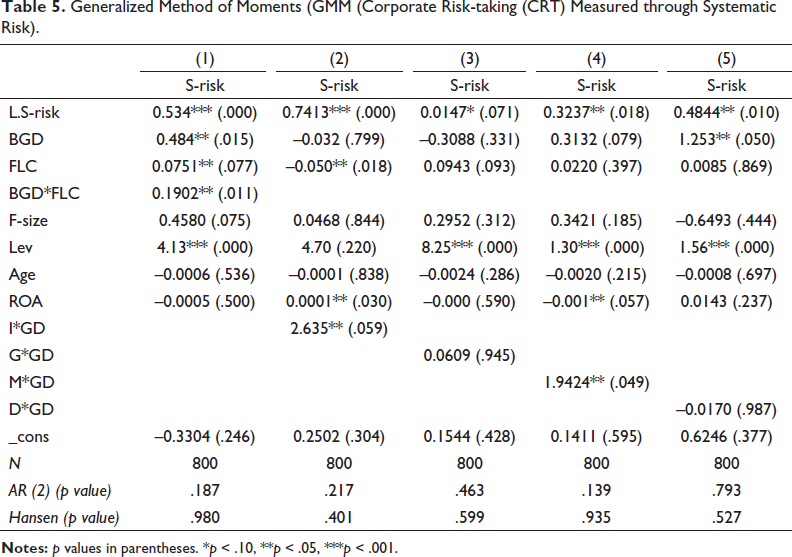

The literature identified that different proxies might yield contradictory results (Avram et al., 2010; Ciftcioglu & Bein, 2017; Din et al., 2020). This could be observed in this study as some results showed contradictory findings when CRT was measured through S-risk (see Table 5). For instance, BGD was positively insignificant under model 1 when CRT was measured through total risk, while BGD reported a negatively insignificant result. As total risk was measured through the standard deviation of daily returns and found an insignificant impact of BGD on risk-taking, one may conclude that firm’s specific characteristics (i.e., BGD) do not influence CRT. On the other hand, the systematic risk was measured through beta (a relative risk to the market) and found a significant positive impact of BGD on risk-taking. Therefore, market-specific characteristics (i.e., BGD) influence CRT. This phenomenon was reaffirmed in model 3 when the interaction term of BGD with the FLC (growth stage) was regressed. This inconsistency could be attributed to the proxy choice reported by literature (Avram et al., 2010; Ciftcioglu & Bein, 2017; Din et al., 2020).

Generalized Method of Moments (GMM (Corporate Risk-taking (CRT) Measured through Systematic Risk).

Result’s Summary.

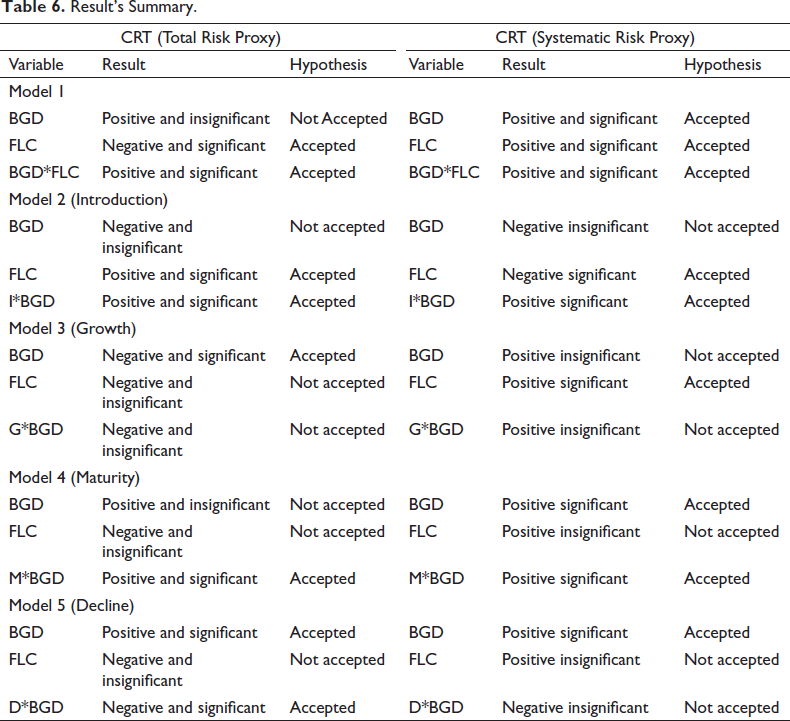

The results for the FLC also revealed that the impact of BGD on CRT varies (see Table 6). For example, BGD positively impacted CRT for both proxies at the introduction and maturity stages. On the other hand, BGD revealed an insignificant impact in the growth and decline stages.

Literature concluded that BGD could have significant impact on CRT, a higher board diversity may discourage risk-taking and vice versa. Past studies also suggest that several factors such as firm’s size, ownership type and board structure, past performances and investment experience, political and institutional powers, access to required resources, incentive plans, stakeholders, corporate governance and FLC may influence CRT decisions of the firm. Past studies although investigated the impact of BGD on CRT but have not considered the impact of other factors that might impact this relationship such as firm’s life cycle. Literature identified few studies that examine the impact of FLC on CRT but yet again BGD was not considered when investigating the said relationship. This study fills this literature gap by investigating the impact of BGD on CRT by moderating of firm’s life cycle.

Drawing on five years of data and almost 200 non-financial firms, our study contributes to this debate by investigating the relationship between BGD on CRT with moderation of FLC. SGMM was applied to investigate the relationship mentioned earlier. The dependent variable, CRT, was measured through two proxies, that is, total risk and systematic risk.

The findings for total risk revealed an insignificant impact of BGD on total risk-taking. In contrast, the proxy for systematic risk reported a significant impact of BGD on systematic risk. The FLC negatively impacted CRT measured through total risk, while the FLC reported a positively significant impact on CRT when measured through systematic risk. The results further showed that interaction term (BGD with FLC) reported a positively significant impact on CRT for both proxies, total and systematic risk. As the FLC has five distinctive stages and the combined results may not yield meaningful insights for decision-making purposes, the results for these distinctive stages were also estimated. The results for FLC stages revealed that the impact of BGD on CRT varies. For example, BGD reported a positively significant impact on CRT for both proxies at introduction and maturity stages. On the other hand, BGD revealed an insignificant impact at growth and decline stages. Few contradictory results were also observed when CRT was measured differently. The contradictory findings for total and systematic risk were mainly because of different proxy choices, measured differently. These findings have significant policy and theoretical implications.

No study is without limitation, this study also has several limitations, for example, sample period was small and only non-financial firms listed on PSX were used to examine the aforementioned relationship. Several other factors such as board characteristics, ownership structure, organization culture and structure, which could also impact on relationship between BGD and CRT, were not considered in this study. Therefore, future researchers may address aforementioned limitations.

Managerial Implications

Contrary to common beliefs, findings suggest that the influence of BGD is more nuanced and dependent on FLC context. This has significant implications for policymaking and the structuring of corporate boards.

Authors Contribution Statement

Sajid Mohy Ul Din: Conceived and organized the overarching research goals and framework. Led the data analysis and interpretation efforts, and was primarily responsible for drafting and revising the manuscript.

Ahmad Adeel: Played a critical role in idea generation and identifying the research gap. Actively addressed the comments from reviewers, significantly contributing to the refinement and finalization of the manuscript.

Sheheryar Khan: Focused on data cleaning and contributed to the data analysis and methodology section of the research. Their technical expertise ensured the integrity and accuracy of the data processing.

Parsa Rani: Was instrumental in the data collection process, focusing on gathering information from selected companies. Participated in brainstorming sessions that shaped the research’s development and execution.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.