Abstract

The purpose of the article is to recognize the moderating effect of customer knowledge on perceived service quality and customer satisfaction through customer value evaluation in the Indian banking sector. This knowledge can considerably streamline the effort banks invest in acquiring the right kind of customers. The results of the study indicated that perceptions of service quality positively impacted customer value evaluation. Moreover, customer knowledge strengthened the relationship that the empathy and responsiveness dimensions of service quality had with customer value evaluation and moderated the relationship that reliability and tangibility dimensions had with customer value evaluation.

Keywords

Introduction

The key to any business growth, customer satisfaction serves as a benchmark for any business organization to achieve success. In the fiercely competitive banking sector, acquiring customers, serving them and maintaining relations with them to attain the maximum satisfaction is the greatest challenge. This upsurge of competition in the retail banking domain, coupled with customers’ demands for augmented service quality, is forcing banks to understand the customers’ buying behaviour up to every possible extent. Banks are compelled to transform themselves into profit-oriented businesses in addition to their integral role in developing the lives of people and the economy on the whole. To become profit-oriented, banks have to be increasingly customer-oriented. However, a mere understanding of the needs of the customer and efforts to achieve their obligation to the banks alone are no longer a priority for the bank. On the contrary, maintaining and retaining relationships with the existing customers is the major concern for banks today (Ghazizadeh, 2010). Banks that develop an intimate relationship with customers gain advantages such as repeat purchase, customer commitment, emotional attachment to the bank and trust and liking towards the bank (Ragins & Alan, 2003).

Banks use successful business models such as service quality and customer relationship management to identify, serve and satisfy their customers. However, exploring ‘customer value contribution’ as a strategy enhances banks’ competitive edge with their ability to meet needs of customers and to deliver higher levels of customer satisfaction. Previous literature in banking identified aspects such as service quality (Chen, Chang, & Chang, 2005), self-service technology (Ho & Ko, 2008), operational quality, convenience and access, safety and soundness, monetary cost (Parente, Costa, & Leocadio, 2015), reduced waiting time and transaction cost (Dauda & Lee, 2016) affecting customer value contribution. A small yet growing number of businesses, however, gains marketplace advantage by drawing on knowledge regarding customer value contribution over their less knowledgeable competitors. These data-driven customer value assessments, measured in monetary terms, validated the efforts business invest in their customers (Anderson, 1998). Hence, customer knowledge and customer value evaluation are becoming one of the most sustainable business models in the retail banking sector.

With the passage of time, banks have realized the significance of maintaining relationships that are beneficial and needed to improve their satisfaction levels for business to grow over a longer period of time. As customers draw a value perception based on the activities conducted by the bank, the inability of bank employees to assess accurately their perception of service quality may lead to dissatisfaction with the service experienced. It is vital for banks to understand that customers bring profit and in return have to be provided with quality services.

The prime challenge for banks in managing customer relations is not to obtain information regarding customers and their needs alone but also to use this data and determine the best time to offer the relevant product/solution to these customers. It is found that the convenience of bank’s location, price/charges, the recommendation from other account holders and promotional activities are no more criteria for customers to select a bank. Instead, factors such as transaction accuracy, carefulness of employees, and efficiency in correcting mistakes and the friendliness and helpfulness of employees (Zineldin, 2005) are used by customers to select the banks. The existing literature on marketing practices of banks offers plenty of scope for exploring the relationship between service quality and customer value evaluation and the influence of customer knowledge on the mentioned relationship. In this context, the present article looks into the impact service quality has on customer value evaluation with the intermediating effect of customer knowledge. This exercise will help in identifying valuable and beneficial customers with much more clarity.

Background of the Study

A bank has to create customer relationships that deliver value beyond the core product. This is derived by measuring and controlling quality through effective implementation of customer relationship management practices, quality service and appropriate differentiation strategy (Zineldin, 2005). CRM is a top priority for banks as they are rated and rewarded based on customer relationships managed (Swartz, 2000). The customer’s perception of service quality is achieved by consistently anticipating and meeting their needs and expectations. The relationship between service quality and employee–customer interpersonal skill is pertinent to get a relationship stronger. A high-quality service gives credibility to the employees. It encourages favourable word-of-mouth communications, enhances customers’ perception of value and boosts the morale and loyalty of employees and customers’ alike (Parasuraman, Zeithaml, & Berry, 1988).

A successful CRM implementation requires a committed company-wide focus on key customers in their one-to-one marketing efforts. It will further gain traction if the customers’ needs are interpreted and demands are met on an enduring basis. A comparative study of the human encounter vis-à-vis technology encounters in a banking environment especially when remote technological interventions are frequent, found that technology increases the overall satisfaction of customers, but the human interface is also equally indispensable (Simmer, Burman, & Haytko, 2008). Contradicting the above interpretation is a finding that even though perceived service quality is a global judgement of superiority of a service, the customer’s satisfaction is specific to encounters or transactions (Parasuraman et al., 1988). It is observed that researchers and practitioners often assume that CRM is a technical centric practice as banks have been using different software tools to perform it (CRMnext, Oracle, Salesforce, etc.).

CRM is not only a technical centric practice but also a strategic function of the organization. PwC, on the contrary, states that technology is a critical part of managing existing customers; otherwise, it is not easy to build more meaningful engagement, a differentiated value proposition and a consistent experience across a complex new array of channels. Five leading issues that shaped challenges while implementing a CRM approach are intelligence, usability, customer experience, multichannel strategy and customer data integration (DeGarmo & Hurley, 2011). According to an Accenture report, banks have the most immediate challenges as eroding customer trust and satisfaction. These challenges can be overcome by getting the following basics right-branch network optimization, basic multichannel integration, proactive and reactive management, operational customer segmentation, sales force effectiveness, simple and clear communication and performance management (Terrizzano, Pesaresi, & Naja, 2012). Interestingly, this corresponds to bank’s service quality dimensions of empathy, assurance, reliability, tangibility and responsi-veness (Parasuraman et al., 1988). These perceptions of service quality determine the degree of CRM implementation. Implementing CRM contains five dimensions: customer acquisition, customer knowledge, customer information system, customer value evaluation and customer response (Lu & Shang, 2007). Understanding the perceptions of these dimensions helps banks to anticipate their expectation in the future and create superior customer experience so that they do not churn.

Banks usually confront complex difficulties on numerous fronts such as marginal product differentiation, rigid and inflexible operating guidelines, rising customer expectation, proliferating solutions available. The real differentiation in banking can occur when banks provide customer-centric offerings. To build such offering, banks need to gain deeper insight into customer value. This customer value is the ‘overall assessment of the offering’s utility on perceptions of what is received and what is given’ (Zeithaml, 1988). It can be measured by collecting customer-related data, and customer knowledge is gained pertaining to perceptions on tangibility, service assurance, employee responsiveness, empathy and service reliability dimensions of service quality. Thus, customer value is assessed and influences banks to pay attention to calculating the resources expended on acquiring the customer. The acquired customer then is a satisfied customer who is always emotionally linked with a service provider for its favourable perceptions. If the banks have a good CRM strategy contained by comprehensive customer knowledge of service quality perceptions, understanding customer value evaluation and eventually invest resources in value-based customer acquisition, then customer satisfaction will automatically be increased.

The present study attempts to explore ways in which banks can cultivate and implement an effective CRM. The process can be devised in understanding the relationship between the customer’s perceptions of bank’s service quality and the bank’s efforts to acquire new customers, evaluating the customer value and building customer knowledge, eventually leads to satisfied customers. The relationship reveals the intermediary effect of customer knowledge between service quality perceptions and customer value evaluation and then acquiring the customer. The study validates that right acquisition results in heightened satisfaction and more loyalty.

The layout of the article is such that it begins with a review of the literature, hypothesis formulation, and conceptual model, research methodology, analysis and interpretation, discussion on the congruence or nonconformity of the hypothesis with previous studies and concludes with business and research implication.

Theoretical Background and Conceptual Framework

CRM ensures acquiring the right customer with the right needs so that banks provide more value and have a positive impact on customer satisfaction levels. CRM has defined dimensions as customer acquisition, customer knowledge and customer value evaluation. Customer acquisition covers the bank’s flexibility in measuring customers’ urgent requirements and using customer information in developing different marketing mix for targeting customers and identifying newer markets. Customer knowledge comprises the bank being knowledgeable about obtaining key customers and understanding their service requirements. Customer value evaluation covers the bank to analyse the individual customer’s profit contribution and analyse customer types and behaviours to identify customer value (Lu & Shang, 2007).

Quality in the service sector has been a topic of discussion for both practitioners and academics. Service quality is a multidimensional concept with which the quality is measured, and it is also known as the service quality exterminator or SERVQUAL. It consists of five indicators: reliability, responsiveness, assurance, empathy and tangibility in services.

Each of these dimensions is important for customers; however, in certain contexts, some are more needed over others (Parasuraman at al., 1988).

Customer satisfaction is paramount to a favourable perception of service quality and a successful execution of CRM, especially in financial services. Since customers are unable to evaluate services prior to the service experience, service encounter, explained as the interaction between the service provider and the customers, is key in evaluating the service performance (Gil, Berenguer, & Cervera, 2008). During these encounters, the customer is able to get an impression of the way the organizations provide their services. It is a triumvirate of the interaction between the organization, processes and employees. Experience during the service encounter, the interaction between the triumvirate and the customer, determines the level of customer satisfaction. In banks, customer satisfaction, hence, is a multidimensional construct. The list of bank service attributes used for the measurement of satisfaction comprises elements such as the appearance of the bank, behaviour of bank employees, layout and atmospherics, operating hours, interest rate and waiting time (Manrai & Manrai, 2007). These elements are found in the earlier mentioned CRM constructs such as customer knowledge, customer value evaluation and customer acquisition and service quality dimensions. Bank customers may regard some of these elements as being not equally important as the others.

The constructs used in this study are mentioned in Table 1 as follows:

List of Constructs

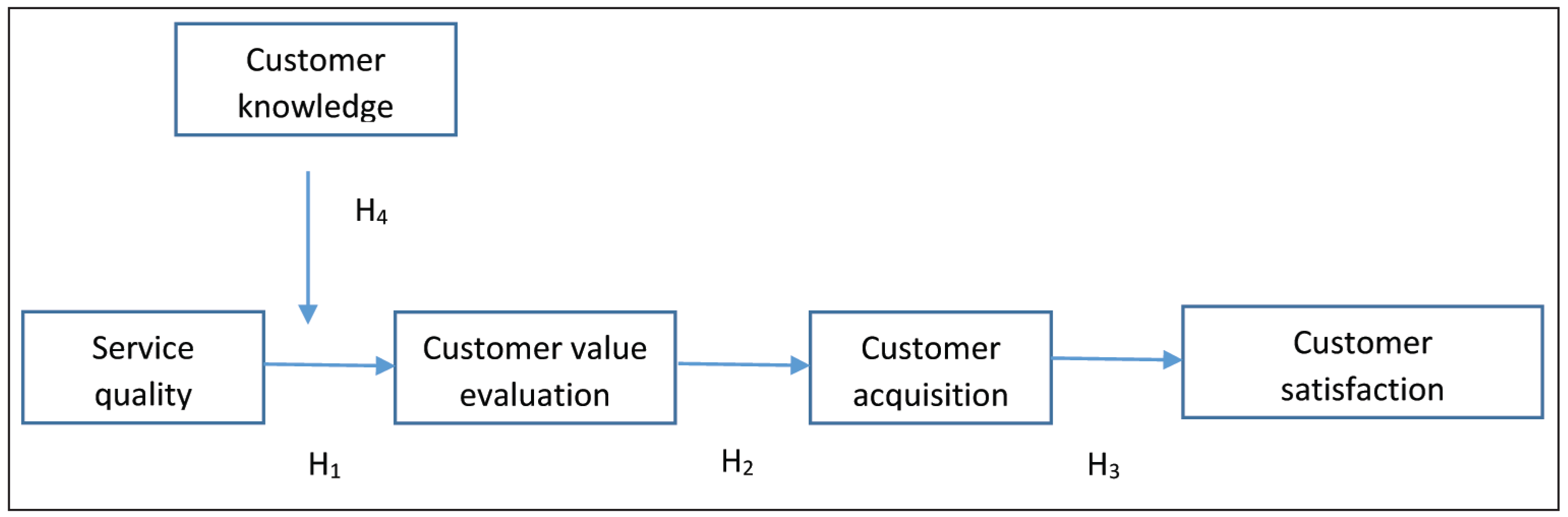

Within the above conceptual, structural and theoretical background, this article presents a framework illustrated in Figure 1, showing the CRM practices of customer value evaluation, customer knowledge and customer acquisition adopted by banks and the customer’s perception of bank’s service quality and the above-stated CRM practices.

Drawing from the aforementioned literature review and research framework, the accompanying hypotheses were proposed (refer to Table 2).

Service Quality and Customer Value Evaluation

Service quality of service firms has demonstrated the positive relationship between increased customer satisfaction and future purchase intentions (Zairi, 2000). In the modern customer-centred era, customer value is a strategic weapon in attracting and retaining customers. Delivering superior customer value has become a matter of ongoing concern in the building and sustaining competitive advantage by driving CRM performance (Wang, Lo Po, Chi, & Yang, 2004).

List of Hypothesis Statements

Customer value evaluation covers the bank to analyse an individual customer’s profit contribution and analyse customer types and behaviours to identify customer value (Lu and Shang, 2007). Customer value has a significant role to play in the bank’s operational decision-making. Creating customer value is a major source of competitive advantage for organizations. The more the customers perceive to receive, the more value gets derived from their total experience. In this scenario, customers are not buying goods or services alone, but specific benefits, which solve problems. They contribute value when the service is offered to match their perception of bank’s ability to solve their problem (Knox, 2003). On the aforementioned discussion, hypothesis 1(H1) is formulated as:

H1: There is a positive relationship between service quality perception and customer value evaluation.

Customer Value Evaluation and Customer Acquisition

Organizations have given immense importance to acquiring and retaining profitable customers. For effective customer management, it is important to gather information on the customer’s value contribution. The value is assessed, and customers are segmented based on their value (Hyunseok Hwang, 2004). Customer value, however, is a dual concept. First, in order to be successful, firms create perceived value for the customers. Customer perceived value is measured, and those perceptions are provided/altered through the marketing-mix elements. Second, customers, in return, contribute value through multiple forms of engagement to the firm. Organizations need to measure and manage this value of the customer(s) and incorporate this knowledge back into real-time marketing decisions (Reinartz, 2016). The lifetime value of the customer considers customer profitability to have a significant role in service provider’s customer acquisition activities and customer acquisition/retention trade-off activities (Berger & Nasr, 1998). On the aforementioned discussion, hypothesis 2 (H2) is formulated as:

H2: There is a positive relationship between customer value evaluation and customer acquisition.

Customer Acquisition and Customer Satisfaction

In today’s arena, success in the marketplace necessitates building customer relationship and not just creating products. This building of customer relationship means delivering superior value over competitors to the target customers (Kotler, 2002). Doing so leads to satisfied customers. Recognizing and anticipating customers’ needs results in customer satisfaction. Organizations that are able to rapidly understand and satisfy customers’ needs make greater profits than those which fail to understand and satisfy them (Barsky & Nash, 2003). By acquiring the right customer with the right value contribution and favourable perception regarding the service quality, the benefits become twofold. First, the acquisition cost for such customers is low and second, customer satisfaction is guaranteed as the customer is understood well ahead of implementing acquisition activities. On the aforementioned discussion, hypothesis 3 (H3) is formulated as:

H3: There is a positive relationship between customer acquisition and customer satisfaction.

Moderation Effect of Customer Knowledge Between Service Quality and Customer Value Evaluation

Enterprises realize customers as their most important asset and recognize that a high level of customer satisfaction can only be achieved by enhancing service quality. Thus, acquiring customer knowledge to initiate and maintain customer relationships, to enhance service quality has become an important issue for these enterprises (Tseng & Wu, 2009). On the aforementioned discussion, hypothesis 4 (H4) is formulated as

H4: Customer knowledge moderates the relationship between service quality perceptions and customer value evaluation

Research Methodology

The study started as an exploratory in nature at the first phase of research. A comprehensive review of literature helped on exploring the gap in the existing literature and introducing the role of customer knowledge as a moderator variable between service quality and customer acquisition. To initiate the nobility of the concept, with experts with practical banking experience, academicians performing research on the same field were consulted and brought under one umbrella to deliberate through focus group discussion. The focus group was organized by a group of 10 academicians as well as senior-level banking professionals working in India. This exercise helped researchers to gain greater insights into the usage of banking services and their perceptions of the bank’s activities meeting their expectations.

In the subsequent phase of the survey, a descriptive research was taken, and this fell into a conclusive design. This study utilized, apart from self-developed items, items from the validated questionnaires of earlier research like items from the SERVQUAL/RATER instrument from Parasuraman et al. (1988) and CRM items from Lu and Shang (2007). The obtained data on fundamental variables of service quality dimensions, customer knowledge, customer value evaluation and customer acquisition dimensions of customer relationship management and customer satisfaction in retail banking.

Subsequently, the hypotheses framed in the study are tested using the questionnaire as a tool to survey research. Data thus collected were analysed with IBM SPSS and AMOS (Version 20*). The respondents were also asked regarding the level of satisfaction based on the overall banking experience and the likelihood action taken eventually. In all the statements in section B, a format of a five-point ordinal Likert scale was used with the response continuum ranging from 1 to 5, where 1 = strongly disagree; 2 = disagree; 3= neutral; 4 = agree and 5 = strongly agree.

The prepared questionnaire, then, was tested through a pilot study on 200 respondents prior to being used for the study. The survey was conducted using multicriteria sampling on customers who had bank accounts in various private (old generation and new generation) and public sector banks in India. Public sector banks—State Bank of India and its associates which include State Bank of India (SBI) and State Bank of Travancore (SBT) and Nationalized banks which include Union Bank of India (UBI) and Canara Bank; Old generation banks—South Indian Bank (SIB) and Federal Bank; New generation banks—ICICI Bank and HDFC Bank. Initially, a sample size of 838 was estimated as adequate, but it was decided to distribute 860 questionnaires of these, and 846 responses were found suitable to conduct the analysis further.

Research Results

The data were normally distributed and passed the reliability test with above the acceptable limit (Cronbach’s coefficient Alpha was found above 0.70). It is observed that the relationship between tangibility, reliability, responsiveness and empathy dimensions of service quality with customer value evaluation dimension is significant. ‘Customer Value Evaluation’ was the dependent variable, and Tangibility, Reliability, Responsiveness, Empathy dimen-sions of the service quality were the independent variables used to conduct path analysis and analysis of interaction effects. The independent variables were Tangibility, Reliability, Responsiveness, Empathy dimensions of the service quality (see Figure 2). Impact of service quality dimensions also checked in relation to the mediation of ‘Customer Knowledge’ on customer value evaluation. The assurance was not included in the model since in banking, service providers are expected to be delivering products and services as per the guidelines of regulatory bodies. Therefore, there is no perceived differentiation between banking institutions on the basis of assurance.

The regression coefficient and the standard regression coefficient depicted that the relationship between empathy and customer value evaluation dimension has the highest strength (regression coefficient 0.604 and standard regression coefficient 0.055) followed by tangibility (regression coefficient 0.238 and standard regression coefficient 0.057) and responsiveness (regression coefficient 0.233 and standard regression coefficient 0.077). Reliability dimension has the least influence on the customer value evaluation (regression coefficient 0.043 and standard coefficient regression 0.175).

Service Quality and Customer Value Evaluation

The empirical data as analysed and summarized were shown in Table 3:

Empirical Results on Service Quality and Customer Value Evaluation

It can thus be interpreted that customers would bank more and invest more if banks express empathy. Empathizing with the customer’s concerns would lead to an increase in profit contribution of customers. Banks are to be designed providing right solutions to customers on time with no delay. Banks fundamental business model has evolved from a ‘product push’ siloed approach to a customer-centric fully integrated self-service mode of operations (Veenstra, 2014). Self-service technology is becoming a new norm for the retail banking industry. Hence, the dimensions responsiveness and reliability are gradually experiencing technology intervention reducing the human interface. Newer ways of assessing these service quality dimensions emerge as financial institutions are realigning their business to incorporate technology (Iberahim, 2016). Hence, it is becoming a challenge for banks to maintain responsiveness and reliability as promised to customers even with the lesser human interventions.

Customer Value Evaluation, Customer Acquisition and Customer Satisfaction

The empirical data as analysed and summarized were shown in Table 4.

The results show that the relationship between customer value evaluation and customer acquisition dimensions of customer relationship management is significant. The regression coefficient and the standard regression coefficient depict that the relationship between customer value evaluation and customer acquisition is 0.033 and 0.385. It can thus be concluded that any change in the customer value evaluation dimension of customer relationship management would have its effect on customer acquisition. This argument holds true, especially in banking. To obtain the desired result of customer satisfaction and banks’ profitability, profiling of the customers with proper determination of customer value leads to quality customer acquisitions. This profile mapping helps banks to assess the requirements of the customers prior to acquiring them. As customer acquisition involves a cost to the bank, it is imperative for banks to assess the profitability of the customers and then decide the type of offering and the level of service to be offered. This emphasizes the core philosophy of CRM as each customer is different in value, banks need to efficiently allocate resource among customers. Customer value evaluation uses the customer knowledge that would drive customer purchase to optimize the resent and future value of customers.

Customer Value Evaluation, Customer Acquisition and Customer Satisfaction

The effect of customer acquisition dimension of customer relationship management on the level of customer satisfaction is significant from the survey results. The regression coefficient and the standard regression coefficient depict that the relationship between customer acquisition dimension of customer relationship management and the level of customer satisfaction is strong (regression coefficient 0.036 and standard regression coefficient 0.152). Thus, it can be concluded that any change in the customer acquisition dimension will have its significant effect on the level of customer satisfaction. Acquiring right customers and matching service offering with the requirements of the customers leads to exceeded customer satisfaction, Doing so, customer commitment increases, and there is increased value to banks. Banks must adopt appropriate acquisition strategy to convert potential customers into paying customers, and the customer base gets expanded. Measuring the costs, comparing it with customer’s potential and later with the profits generated by them helps banks to balance acquisition cost and cost of keeping the customers satisfied. The success of banks thus would lie in reducing the marketing cost to acquire new customers and increase overall customer response rates, which is an evidence of a satisfied customer (Kumar, Kee, & Charles, 2010).

Moderation Effect of Customer Knowledge Between Service Quality and Customer Value Evaluation

The moderating behaviour of customer knowledge in the relationship between service quality and customer value evaluation of CRM dimension is tried in this part of the analysis. The empirical data as analysed and summarized are shown in this section taking each service quality dimension over customer value evaluation with the moderating customer knowledge dimension.

Moderation One

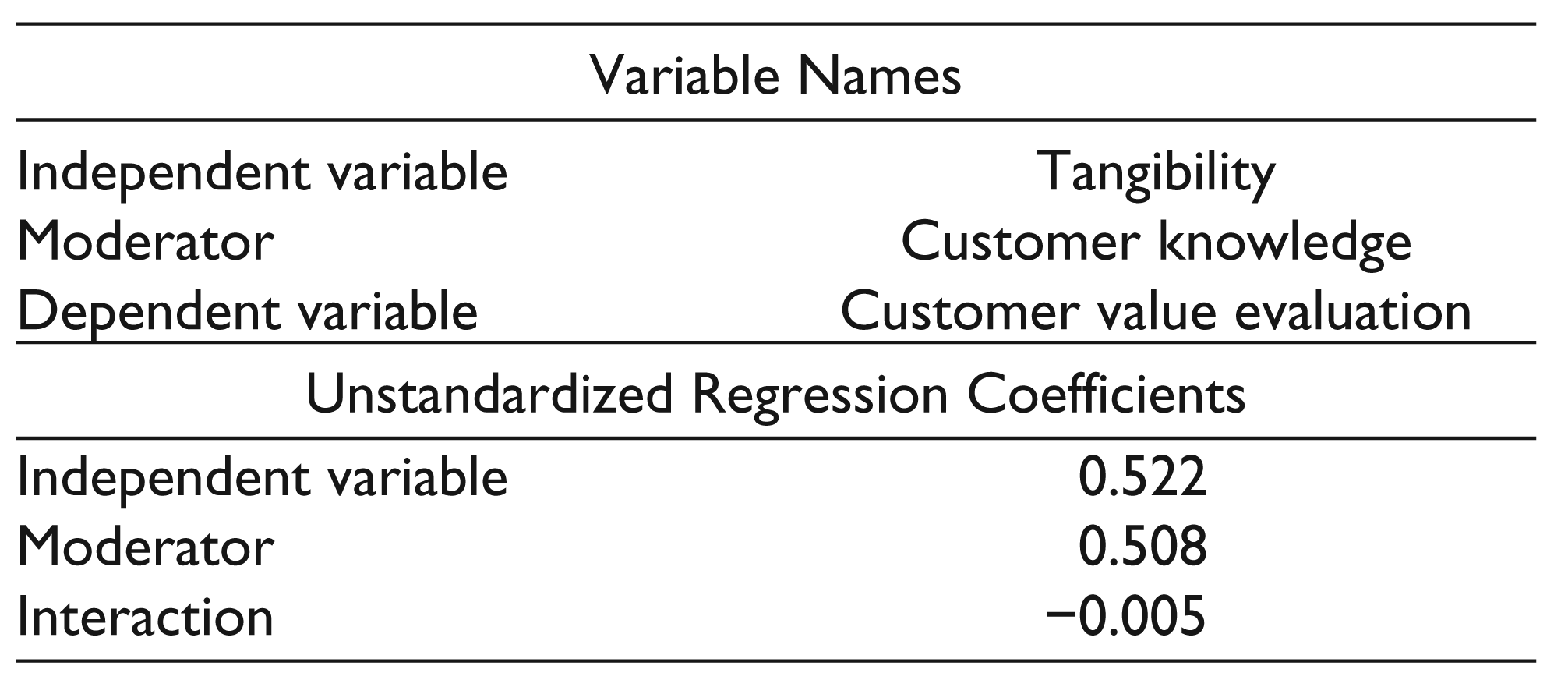

Customer knowledge acting as the moderator between tangibility and customer value evaluation is shown in Table 5.

Tangibility is the appearance of physical facilities, equipment, personnel and communication materials (Zeithaml, 2006). From the Table 5 and Figure 3, the regression results show that the relationship between tangibility and customer value evaluation is moderated by customer knowledge, and this moderating variable weakens the strength of the relationship (interaction, −0.005). In other words, although the tangibility dimension of service quality has a positive influence on customer value evaluation (Table 3), it is weakened by the moderating customer knowledge variable. Symbolizing (Table 5, Figure 3) there is an impactful relation between upgraded technologies in banks, the operational hours of banks, visually appealing facilities and materials used and the professional appearance of the employees, with measuring profit contribution of various customer groups and analysing the customer types and behaviour to identify their value. However, customer knowledge, which is the banks’ effort on obtaining knowledge on their key customers, understanding their service requirements and insisting them to use more and more of the banks’ services and products, weakens the strength of the relationship between tangibility and customer value evaluation. Hence, the hypothesis is accepted. It may be interpreted as more customers are aware of the terms and conditions, the operations standard of the banks, very few customers would rely on the tangibles offered by banks. The more technology is implemented in delivering services, and less would have tangible influence on the profit contribution of the customers.

Regression Coefficients for Two-way Interaction—Levels of Tangibility

Moderation Two

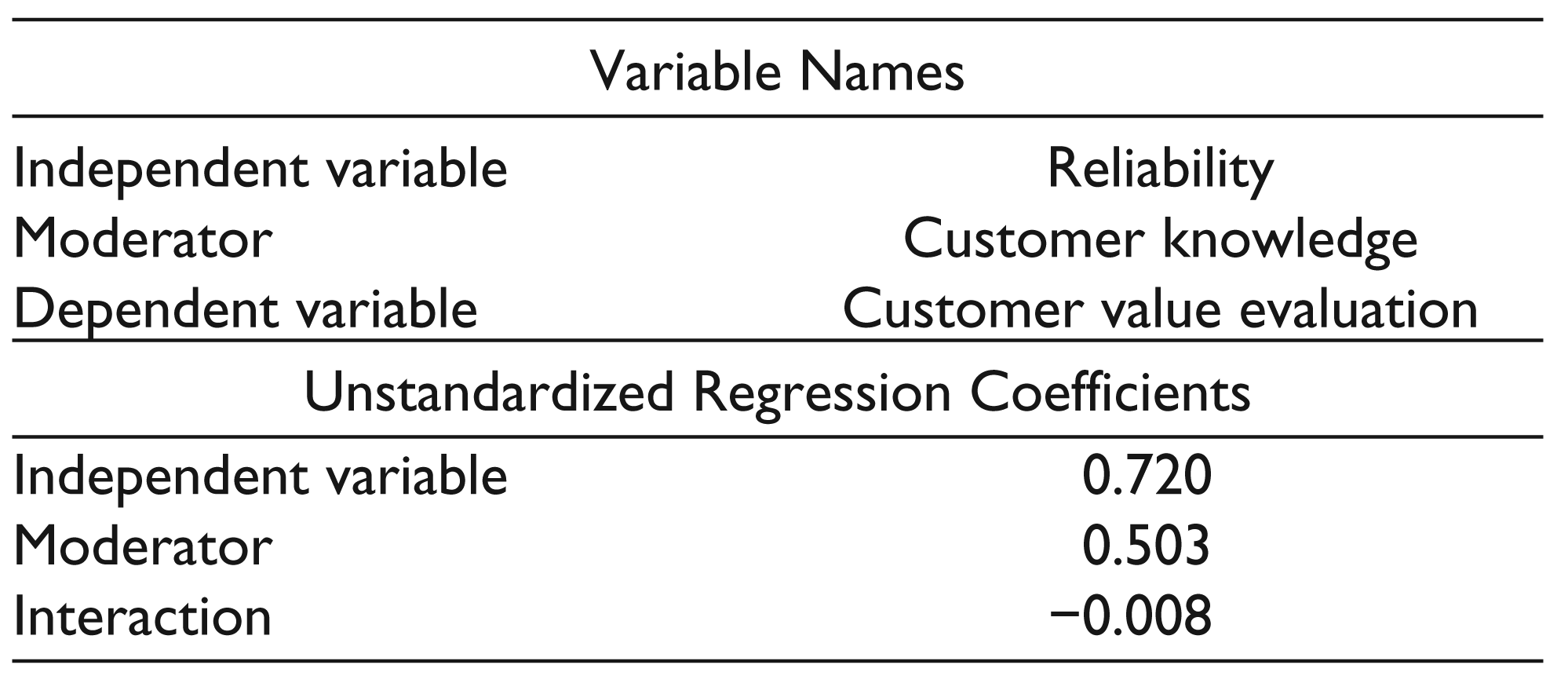

Customer knowledge acting as the moderator between reliability and customer value evaluation is shown in Table 6 and Figure 4:

Regression Coefficients for Two-way Interaction—Levels of Reliability

It is the judgement of customers/clients regarding an overall performance of the organization and its services (Zeithaml, 2006). In banks, reliability measurement is established by testing consistency and stability. The major reason for customers to choose banks is dependability. Banks always promise customers a high level of security during transactions. Banking service can increase customers’ confidence and trust if employees are able to provide appropriate service to each customer (Iwaarden, Wiele, Ball, & Millen, 2003). The regression results show that although the reliability dimension of service quality has a positive influence on customer value evaluation (Table 3), it is weakened by the moderating customer knowledge variable (interaction, −0.008). Results depicted that customer’s knowledge can dampen the strength of the relationship between the perception of stability and consistency of banking services with the bank’s comprehension of the customer’s profit contribution. Banks knowledge of key customers and their requirements moderates dependability over accuracy and consistency in delivery of services leading to the bank’s examining value contribution.

Moderation Three

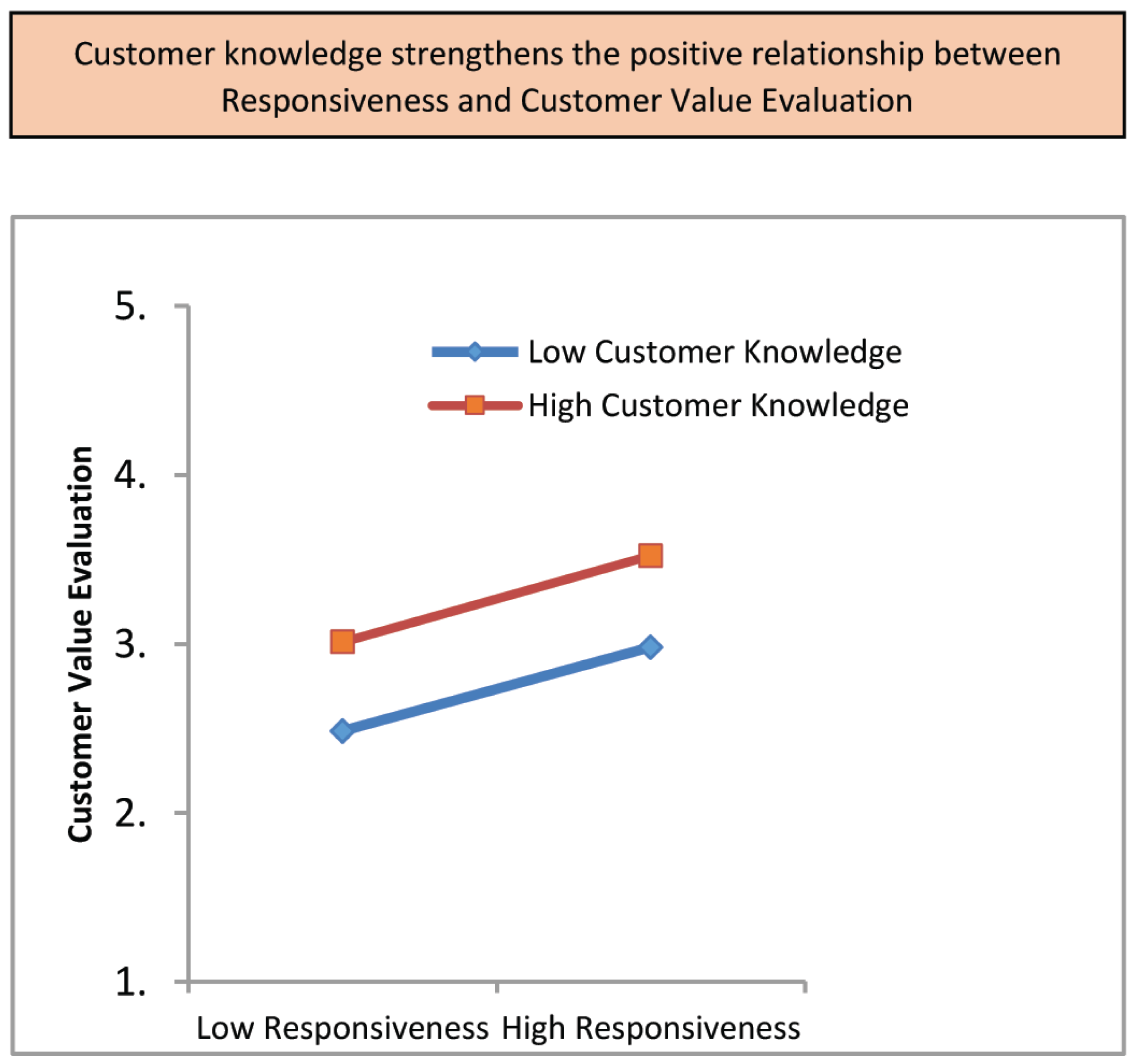

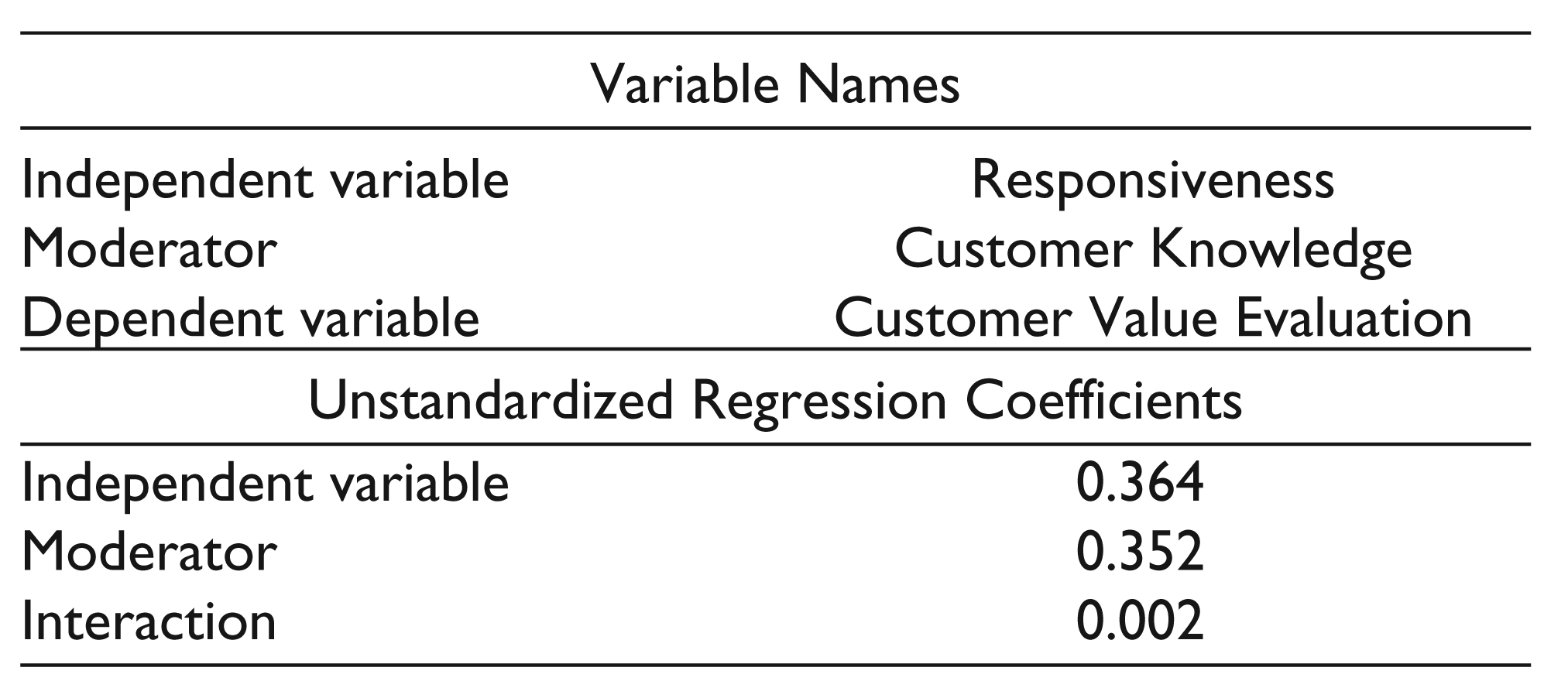

Customer knowledge acting as the moderator between responsiveness and customer value evaluation is shown in Figure 5.

Responsiveness is defined as the willingness to help customers and provide prompt service (Zeithaml, 2006). The future of banking is responsive, and banks need to design and fold the banking experience around their customers by providing them with the right product or service at the right time. Banking experiences that are dissatisfactory are discussed twice above good ones. Likewise, customers dissatisfied with the bank’s attempt to resolve a problem or answer a query confide to 16 more people. Customers who complain and have their complaints resolved are more brand loyal than customers who have no complaints (Lynn, 2000). From Table 7 and Figure 5, it is seen that customer knowledge moderates the relationship by strengthening it (interaction 0.002). Responsiveness deals with the process of banking, and this dimension of service quality ensures customers not having any problem while dealing with banks. Knowledge of customers helps banks in providing services performed to expected standards, correctly, promptly and timely leading to more valuable contribution.

Regression Coefficients for Two-way Interaction—Levels of Responsiveness

Moderation Four

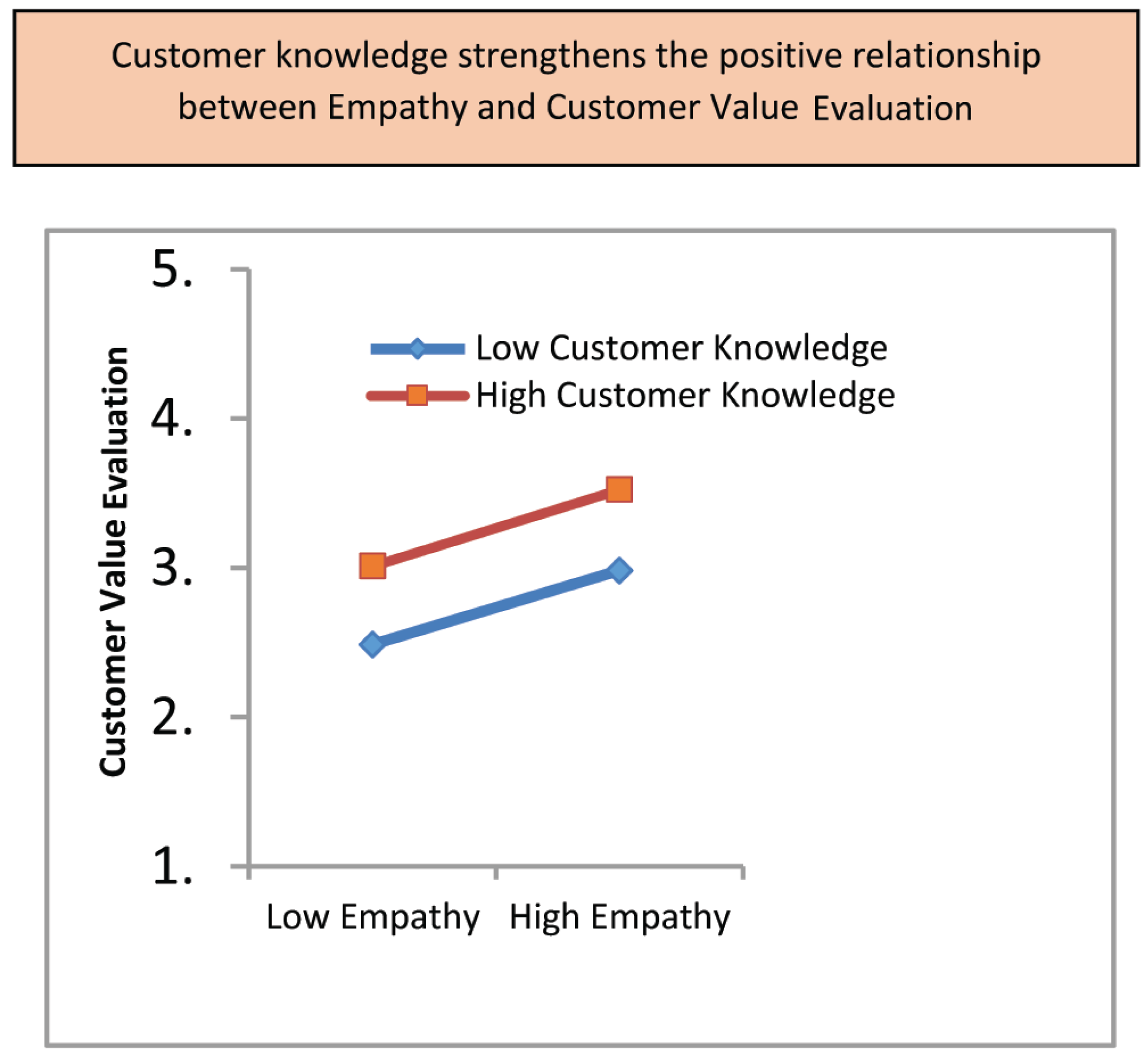

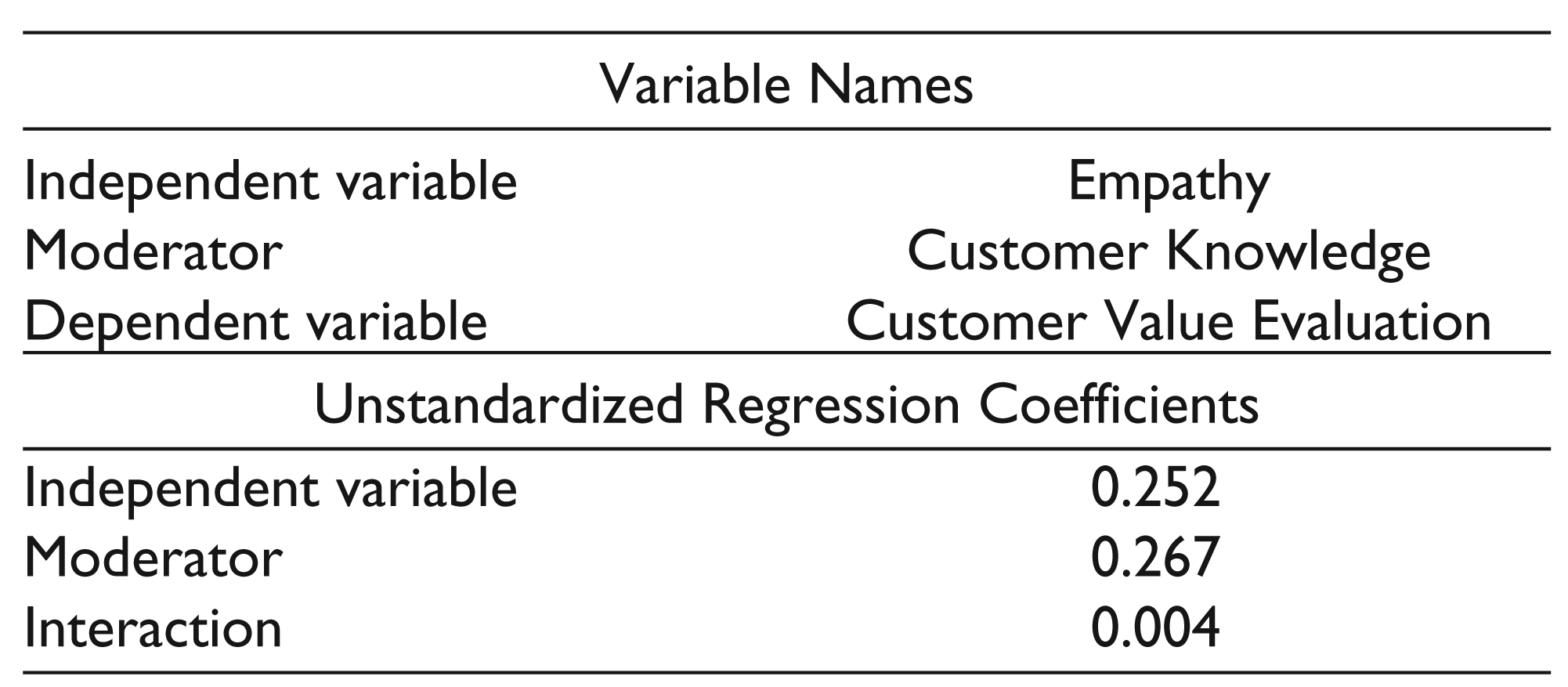

Customer knowledge acting as the moderator between empathy and customer value evaluation is shown in Figure 6.

Empathy is the caring and individualized attention the firm provides its customers. Empathy as a dimension of service quality primarily drives customer satisfaction. Banks are trying to divert their customers from bank offices to ATMs, and the internet may undermine the importance of human contact, which is essential for successful customer service. Therefore, bank managers should bear in mind while striving to improve the service quality that the problem is genuine empathy and interest that cannot be put into a script (Ica, 2010). From the aforementioned table and figure, the regression results show that although the empathy dimension of service quality has a positive influence on customer value evaluation (Table 3), it is strengthened by the moderating customer knowledge variable (interaction, 0.004). The above data (Table 8, Figure 6) is interpreted as the customer’s knowledge can strengthen the relationship between the perception of caring and empathy. The firm provides its customers with the bank’s comprehension of customer’s profit contribution. Banks knowledge of key customers and their requirements moderates employees empathizing with the customers while delivering services and bank’s identifying and utilizing the customer’s value contribution.

Regression Coefficients for Two-way Interaction—Levels of Empathy

Discussion

Today, organizations are obliged to render more services apart from their product offerings. Service as a component is an integral part of customer satisfaction. Experts have demonstrated that service quality is identified with customer satisfaction. Service quality enhancements and building strong and fruitful relationships with customers is the prime concern for organizations, specifically banks (Khare, 2010). Improving service quality has become the tool that banks utilize to retain customers (Gradener, 1999). Banks are facing a tremendous competition and the demand of the customers for better service quality is in the upsurge. Consequently, banks are forced to identify customers as an important asset that needs to be protected and nurtured (Bowman & Narayandas, 2001).

By paying attention to service quality, banks gain a competitive advantage in the undifferentiated marketplace. A higher perception of service quality provided by banks can lead to increased revenue, satisfied customer base and an improved rate of customer retention (Kumar et al., 2010). Thus, to survive the prevailing intense competition, banks attempt to create convenient banking. Banks provide services such as ATM, ready cash service, money transfers, national electronic fund transfer and the real-time gross settlement, banking via mobile phone, and so on are insufficient as they can be easily replicated by other banks. Customer relationship management is the centre of all activities as banks have moved from being transactional to the relationship oriented. For building a long-term relationship with customers, banks should look into the customers’ satisfaction from the customer’s perspective instead of bank’s perspective (Peppers & Rogers, 2004). While maintaining the relationship with customers, banks focus on identifying customer needs and providing services exactly matching with those needs. Service quality has a positive influence on customer satisfaction (Thaichon, Quach, Bavalur, & Nair, 2017), and using CRM effectively provides a comprehensive view of the customer groups obtained and it increases the chances of repeat business enhancing the net growth of the business.

As banking deals with financial needs, this study found four dimensions positively impacting the value customers contribute to the bank name, tangibility, responsiveness, empathy and reliability. Assurance dimension does not influence value contribution. In other words, social interactions between employees and customers classified as empathy will make the customers contribute more to value. Perception of service performance called reliability will also have a positive impact on the customer’s value contribution. The visual images which help customers to form impressions regarding the quality of service called tangibles will have a positive effect on the customer’s contribution to profit. On the contrary, altering assurance dimensions has no effect on the customer value evaluation. In other words, the customer’s value contribution is not increased or decreased due to the enhanced perceptions of assurance regarding the service provider, as these dimensions are a problem-/grievance-specific and do not directly lead to more purchase. In other words, trust and confidence gained from skilful employees do not influence customer’s value contribution. Customer value evaluation and customer acquisition indicate that banks are making progress in analysing the customer’s contribution to profit, assessing their behaviour in identifying value and accordingly are developing new products and services enhancing personalized approaches. All of this will all have its influence on activities implemented and approaches used by banks to meet the needs of the customers and attract large customers. This realization will improve the manner in which customer information is utilized to attract new customers, customize products and services and fulfil promises on time. In addition to this, information on customer value would help to acquire them providing a total financial solution through knowledgeable/trained employees who have a sincere interest in the benefit of those customers. Banks take up approaches, that can attract customers, utilizing the right information to customize products and services, fulfil promises on time and provide complete end-to-end financial solution through trained and competent employees who are pleasing and have a sincere interest in the benefit of the customer. This will all lead to a more satisfied customer reaping greater benefits to the banks in the long run.

Implications of the Study

This study can be extended to find the influence of four dimensions of service quality and three dimensions of customer relationship management on customer satisfaction. It can also be advantageous to study in detail the perceptions of customer relationship management of different segments of respondents. Considering the diverse application possibilities and the value provided to banks, the study can be extended to further delving into comparisons between old and new generation banks, and perceptions on service quality dimensions. The study provides actionable information to banks with which they can design and implement marketing programmes catering to the diverse requirements of the customers.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.