Abstract

The purpose of the article is to study the impact of sustainable supply chain management (SSCM) on the financial performance of the firms in India. The empirical analysis used data from the top 100 listed companies by market capitalization on BSE. Content analysis is conducted to analyse the principle ‘life cycle sustainability of goods and services’. Hierarchical linear regression is used to test the hypotheses. The results reveal that sustainable sourcing and resource utilization are the two SSCM activities that have a significant positive impact on the financial performance of the firm. The article offers insights for focusing on the activities that increase the shareholder value. It is the initial study that has focused on the sustainable supply chain activities at the micro level as mandated by the regulators of sustainability reporting and studies the impact of such activities on the financial performance of the Indian firms.

Keywords

Introduction

It is a well-established fact that the adage ‘sustainable development’ has been popularized by ‘Brundtland Report’ published in 1987 by World Commission on Environment and Development. This report states that the sustainable development means to meet the present requirements without harming the abilities to meet the needs of the coming generations. In the case of a firm, meeting the present requirements means meeting the needs of the firm’s stakeholders, namely shareholders, customers, investors, suppliers, authorities, groups, communities and so on. Focusing only on the shareholder’s economic goals, which subsequently deteriorates the environment and affects the societal welfare, however, will not lead to the achievement of sustainability. Therefore, the need arises to balance all the three pillars, that is, the economic goals of the firm, the societal goals and the environment, which is also known as the triple bottom line (TBL or 3BL) approach (Colbert & Kurucz, 2007; Colman, 2004; Elkington, 1994; Garriga & Mele, 2004; Hedberg & Malmborg, 2003; Joyce & Paquin, 2016; Kolk, 2004; Rajeev, Pati, Padhi, & Govindan, 2017). Further, Spreckley (1981) clarifies that the TBL accounting broadens the conventional reporting framework by taking into account social and environmental performance in addition to the financial performance of the company.

The supply chain of a firm is an area of activity where major imbalances occur among the three indicators, that is, economic, social and environment. To study these imbalances, researchers have used the life cycle analysis. Life cycle analysis is a technique to measure the environmental impact related to all the stages a product passes through, right from raw material procurement to disposal and recycling of the product. It is also known as cradle-to-grave analysis. If a firm is to manage its business sustainability, the supply chain activities involved in sourcing, procurement, conversion and logistics activities are to be managed in such a way that a balance is maintained among the economic, social and environmental indicators.

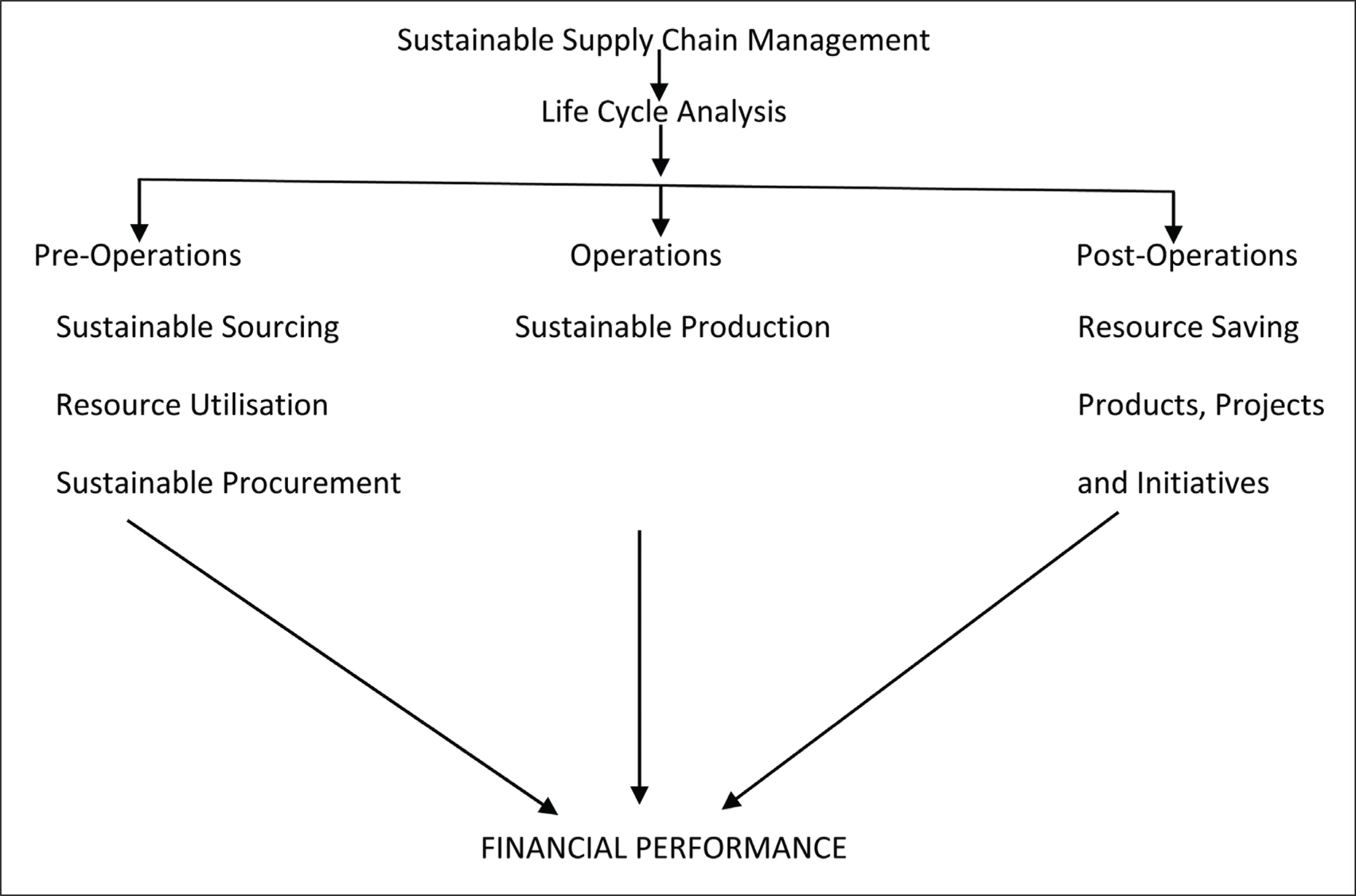

Based on the previous literature, at the macro level, the supply chain has been divided into three major sets of activities, that is, upstream activities (Ageron, Gunasekaran, & Spalanzani, 2012; Golicic & Smith, 2013; Li, Wu, Holsapple, & Goldsby, 2017; Morali & Searcy, 2013; Su et al., 2016; Vachon & Klassen, 2006; Wang & Sarkis, 2013; Wolf, 2011, 2014), downstream activities (Ageron et al., 2012; Golicic & Smith, 2013; Li et al., 2017; Morali & Searcy, 2013; Su et al., 2016; Vachon & Kalsen, 2006; Wang & Sarkis, 2013; Wolf, 2011) and production-related activities (Golicic & Smith, 2013; Su et al., 2016). Different names have been given to upstream activities, such as green procurement (Wolf, 2014), inbound logistics (Carter & Roger, 2008; Wang & Sarkis, 2013), green purchasing (Wang & Sarkis, 2013), green supplier development (Wang & Sarkis, 2013) and transport (Wang & Sarkis, 2013). Downstream activities are also known as outbound logistics (Carter & Roger, 2008; Wang & Sarkis, 2013) and green marketing (Wang & Sarkis, 2013). Production activities are also known as operations (Ageron et al., 2012; Wolf, 2014), internal integration (Wolf, 2011), internal operations (Vachon & Kalsen, 2006), internal business (Bhagwat & Sharma, 2007) and environment-conscious manufacturing (Wang & Sarkis, 2013). Deriving from the existing literature, these supply chain activities have been named as upstream activities, operations and downstream activities in the present article.

Abundant research has been conducted on evaluating the impact of sustainable supply chain management (SSCM) on the financial performance of the company. Sybertz (2017) asserts that sustainable supply chain activities have a positive impact on the three TBL dimensions. Wang and Sarkis (2013) find that structured SSCM that has both social and environmental initiatives is associated with increased return on assets and return on equity. Geng, Mansouri, and Aktas (2017) find that in the ‘emerging economies’ in Asia, there is a positive relationship between SSCM and TBL dimensions in manufacturing firms.

With reference to financial performance vis-à-vis SSCM, research has been conducted at the macro level. The existing research has a broader scope but is less specific. Over a period of time, the regulators of different countries have mandated the companies to report sustainability activities in detail. The researchers have somehow overlooked to evaluate the impact of these sustainable activities on financial performance, as mandated by the regulators of sustainability reporting. They have continued to evaluate the impact of SSCM on financial performance by dividing the supply chain activities into upstream, operations and downstream activities. However, as already stated, the reporting of these activities has changed. Therefore, there is a need to further breakdown each of these activities. In the present article, the impact of SSCM on the financial performance of the company has been undertaken by further dividing the upstream operations and downstream activities into micro activities so that the impact of these activities can be studied more comprehensively. The SSCM activities have been breakdown into various activities at the micro level on the basis of the proforma of Business Responsibility Report (BRR) given by Security Exchange Board of India (SEBI) and the existing literature (Carter & Roger, 2008; Golicic & Smith, 2013). Esfahbodi, Zhang, and Watson (2016) have assessed SSCM on the basis of sustainable procurement, sustainable distribution, sustainable production and reverse logistics. In other words, the supply chain is a com-bination of upstream, that is, supply-side, downstream, that is, customer side while the operations are in the centre (Jonsson, 2008). This will help in evaluating the SSCM activity/activities contributing more towards the financial performance of the firm.

Theory Building and Research Hypothesis

Stakeholder Theory as a Proponent of Sustainable Development

Stakeholders are the persons or the parties that have a direct or indirect interest in the organization. There are various direct and indirect stakeholders of an organization, namely shareholders, employees, clients, pressure groups, communities and so on (Dyllick & Hockerts, 2002). Stake-holder theory is particularly applicable to SSCM because stakeholders’ pressure may lead a firm to adopt some SSCM practices that are initially economically unfavourable (Sarkis, Zhu, & Lai, 2011). In the recent times, various international reporting agencies on sustainability such as the Global Reporting Index (GRI), non-governmental organizations, regulating bodies, press and media and the society are putting pressure on the organizations to pursue sustainability in their operations. Companies need to pursue responsible business practices to ensure equal importance being given to the interests of stakeholders because the stakeholder theory suggests that every individual or party (stakeholder) participates in the activities of a firm to obtain benefits (Morali & Searcy, 2013). The predominant stakeholder of the firm is the shareholder. Sometimes a firm may pursue strategies that maximize the wealth of shareholders at the cost of harming the interest of other stakeholders. However, companies cannot forego the interest of other stakeholders for the sake of wealth maximization of the shareholders. The reason being, the company will not be able to make profits if the society refuses or is unable to provide resources to the firm and also refuses or is unable to buy products manufactured by the firm. Hence, the organizations must balance the needs of all the stakeholders in order to sustain itself in the long run. In the present article, the stakeholder theory is studied with respect to local and small suppliers and society involved in a sustainable supply chain. The impact of sustainable practices, like procurement from local and small suppliers, and sustainable projects/products for society on the financial performance of the firm is studied in the present article. From the discussion, four hypotheses have been formulated regarding stakeholders:

Sustainable Sourcing

This activity highlights the methods in place for sustainable sourcing.

It basically refers to making sure that a company’s social and environmental performance extends to its supply chain. The company is supposed to list all the activities that it manages and all the processes it has established to promote its supply chain sustainability by sourcing from social and environmental certified suppliers, including transportation initiatives like using CNG vehicles for controlling pollution. Blome et al. (2014) concluded that sourcing from the sustainable supplier has a positive impact on the environmental, social and financial performance of the firm through the cost reduction for the organization. Kashmanian, Wells, and Keenan (2015) argue that check on the suppliers can help to map out suppliers, minimize risks associated with business and in bringing out inefficiencies, but are not capable of increasing market share. Carter and Jennings (2002) find that on the basis of social responsibility, there is a positive association between buyer–supplier relationships and it increases the operational performance of the firm. This may happen because strong relationships are built between purchasing managers and supplier who have the same values that are socially responsible values. Sustainable sourcing is related to sourcing of the resources from the nearest possible source, hence, it would result in cost reduction by reduction in the transportation costs. Therefore, sustainable sourcing might result in better financial performance. Hence, the following hypothesis has been formulated:

H1: Sustainable sourcing has a positive and significant impact on the financial performance of the company.

Sustainable Procurement

This activity refers to the steps to procure goods and services from local and small producers, including communities surrounding the place of work. According to BRR, ‘local’ means purchasing from the place as near as possible if the material of equivalent quality is available. ‘Small’ means sole proprietorship organizations where the owner is a worker, self-help groups or remote workers, that is, home-based workers. It also includes producer-owned entities, such as cooperatives, producer companies. Vachon and Mao (2008) assert that procurement from near possible community results in the betterment of local communities and fairness in the society and this leads to social sustainability. Chan and Wong (2012) confer that environmentally responsible purchasing results in better financial performance due to increase in net income through cost reduction for the organization. Further, sustainable procurement from the local and small organization will have a positive impact on the environment and the society as procurement from the locals may result in less transportation and therefore less pollution. Simultaneously, procurement from local vendors will generate employment for the local workers. Bag (2012) find that the sustainable procurement leads to better financial performance through an increase in sales and market share. From the above discussion, the following hypothesis has been framed:

H2: The sustainable procurement has a positive and significant impact on the financial performance of the company.

Sustainable Production

According to BRR, this activity highlights the methods to recycle the products and waste generated during operations. Sustainable production is about the procedures that the firms have in place to recycle their products after consumption by consumers including the packaging. Murray, Kotabe, and Wildt (1995) find that production innovation and process innovation have a positive impact on the financial performance of the company. Gallego-Alvarez et al. (2015) study the relationship between decreased greenhouse gas emissions in the sustainable supply chain and financial performance, and concluded that there is a positive and significant relationship between decreased greenhouse gas emissions and corporate financial performance. Aguilera-Caracuel and Ortiz-de-Mandojana (2013) confer that technological improvement saves energy and recycles waste material, thus, contributing to the sustainability and this has a positive impact on the financial performance of the company. The reason might be that energy saving and recycling can be used for other purposes in the production process, thus, leading to the cost reduction for the company. Therefore, the following hypothesis has been framed on the basis of the above discussion:

H3: Sustainable production has a positive and significant impact on the financial performance of the company.

Sustainable Product/Projects

This activity throws light on the projects and products developed by the firm that have positive effects on the society. These products and initiatives must be safe and contribute to the sustainability throughout their life cycle. Seuring and Muller (2008) have defined sustainable products as the products that have included all the environmental dimensions, such as ISO standards and social dimensions, such as no child labour. Wang, Chan, and Li (2015) suggest that green product design may not have a positive impact on the financial performance of the company as it adds to the cost of production. Walley and Whitehead (1994) confer that the firms investing in green products incur additional costs, thereby decreasing the financial performance of the company. Thus,

H4: Sustainable product/projects have a negative and significant impact on the financial performance of the company.

Resource-based View

A company can enjoy sustained competitive advantage if its resources are rare, unique and indispensable (Barney, 1991). Hart (1995) states that the efficient resource utilization is a challenge and the pressure is posed by the environmentalists regarding the degradation of the environment. Resources of the companies are the employees, processes, methods, finance and so on. These resources are needed to procure, manufacture and deliver the products and services to the end users. These resources must be used in a responsible manner so that all the stakeholder needs get sustainably fulfilled. Ruf, Muralidhar, Brown, Janney, and Paul (2001) proclaim that a company opting new design process may relish a sustainable competitive advantage over a company that only uses filtering equipment at the end of the process as a formality to meet the legal requirement. Vachon and Klassen (2006, 2008) state that the RBV has recently received support in research linking environmental sustainability practices related to the supply chain activities to improved economic, operational and market performance. These authors note that the supply chain processes have a direct impact on the natural environment, and the practices to manage and reduce this impact can develop capabilities to improve financial performance. In the present article, resource-related activities in the SSCM, such as resource utilization, sustainable production, sustainable sourcing and resource saving, are studied. Further, the impact of these sustainable practises on the financial performance of the firm is studied. Following two hypotheses have been framed regarding the resource-based view (RBV).

Resource Utilization

This activity highlights the reduction of resources (water, energy and raw material) emission reduction during the production, sourcing and distribution in the entire supply chain. Vachon and Wao (2008) conclude that saving of the resources with the help of recycling during production results in improved environmental performance. Hart and Ahuja (1996) find that emission reduction and efforts to prevent pollution result in better financial performance for high emission producing companies. The reason might be that saved resources directly translate into cost reduction and also reduce the environmental impact. Hanifan, Sharma, and Mehta (2012) resolve that supply chains of manufacturing companies incur more than half of the total expenses and greenhouses gas emissions. As the suppliers are more associated with environmental change, therefore, it is important to consider the cost and environment change analysis. We hypothesize that better utilization of resources will lead to better financial performance. Hence:

H5: Resource-utilization has a positive and significant impact on the financial performance of the company.

Resource Saving

Resource saving throws light on saving of resources (water and energy) by the consumers during the usage of the product. Vachon and Klassen (2006) assert that green co-operation with customers has a positive impact on the environmental performance. Geng et al. (2017) find that green customer collaboration is strongly linked with operational performance. However, the firms have to invest in training programmes to educate consumers about the resource saving. This might lead to receding financial performance. The firms might have to invest in advertisements to show resource saving benefits to their customers; these initiatives can result in higher costs. However, it might lead to cost reduction at the customer end. Hence:

H6: The resource saving has a negative and signifi-cant impact on the financial performance of the company.

On the basis of the above-discussed theories, it can be deduced that SSCM of the firms generate: First, better financial performance if the companies focus on the interest of all the stakeholders by fulfilling the varied demands of the stakeholders. Second, Sustainable resource utilization not only creates sustainable competitive advantage and helps in grasping the opportunities provided by environmentalists, society, pressure groups, government and regulating bodies for making the supply chain sustainable.

Research Question

There is inexactness in the literature regarding the impact of SSCM on the financial performance of the corporations because the results are mixed. One set of researchers shows a positive impact of SSCM on financial performance of the firms (D’Avanzo, von Lewinski, & van Wassenhove, 2003; Ellinger et al., 2011; Ellram & Liu, 2002; Golicic & Smith, 2013; Li et al., 2011; Nayar, 2005; Mitra & Singhal, 2008; Tan, Kannan, Handfield, & Ghosh, 1999). Whereas, another set of researchers confirms a negative impact (Jiang, Belohlav, & Young, 2007; Kotabe & Murray, 2004; Wieder, Booth, Matolcsy, & Ossimitz, 2006). Further, Ahi and Searcy (2015), Esfahbodi et al. (2016), Geng et al. (2017), and Vachon and Klassen (2006) find that upstream activities are strongly associated with better financial performance, while Gallego-Alvarez et al. (2015), Geng et al. (2017) and Golicic and Smith (2013) argue that operational activities are more strongly associated with economic performance. Mitra and Singhal (2008) and Seuring and Muller (2008) assert that downstream activities contribute to the improved financial performance. Further, most of the studies are confined to the emission of gases and pollutants, that is, only the environmental dimension of TBL (Buchholz, 1998; Epstein & Roy, 2001; Jose & Lee, 2007; Kolk, 1999, 2003). Rajeev et al. (2017) confer that studies focusing on the three pillars of SSCM, that is, economic, environmental and society are scarce. Therefore, there is a need to study all the three pillars of TBL that contribute to the higher financial performance of the corporations.

As discussed earlier, there is also ambiguity relating to the activities actually contributing to the financial performance as no research has been undertaken by breaking down the SSCM activities into micro activities based on the mandatory sustainability reporting. There is a need to undertake the research at the micro level to uncover the activities in SSCM that increase the financial performance of the company.

Further, most of the previous research is confined to the developed economies (Ameer & Othman, 2012; Gill, Dickinson, & Scharl, 2008; Jose & Lee, 2007; Kolk & Pinkse, 2007; Lo & Sheu, 2007; López, Garcia, & Rodriguez, 2007; Morhardt, 2010; Wagner, 2010). However, there has been an increase in sustainability disclosures after 2012 in India. SEBI has mandated the Regulation 34(2)(f) of SEBI (Listing Obligations and Disclosure Requirements) Regulations 2015 (SEBILODR) for the companies to disclose sustainability regarding activities in their annual reports. Furthermore, the findings of the researches in developed economies may or may not hold true in an emerging economy like India.

Thus, the present study focuses on the following objectives:

To study the impact of the sustainable supply chain on the financial performance of the firms in India. To evaluate the activities contributing to the financial performance of the firms based on the mandatory sustainability reporting.

Thus, the present study adds to the body of existing literature on the sustainable supply chain in an emerging economy like India.

Independent variables used are derived from previous literature and from the proforma of BRR. An explanation of the explanatory independent variables is derived from the proforma of BRR and previous literature. The hypo-theses discussed earlier are shown in Figure 1.

Database and Sample Selection

For achieving the above-mentioned objectives, the top 100 (market capitalization) BSE listed companies are selected. During the year 2012, SEBI made it mandatory for the top 100 (market capitalization) BSE listed companies to disclose BRR either in their annual reports or in the sustainability report. The report is divided into nine principles. One of the nine principles is named ‘Life cycle sustainability of goods and services’. Annual reports have been extracted from the BSE and the official websites of the companies. Further, the financial data has been collected from PROWESS software, the database owned by Centre for Monitoring Indian Economy.

Methodology

Life cycle sustainability assessment (LCSA) methodology as propounded by Finkbeiner, Schau, Lehmann, and Traverso (2010) is used in the present article. LCSA focuses on the three pillars of sustainability, that is, the social, the economic and the environment. Rajeev et al. (2017) has conferred that sustainable distribution, sustainable design, sustainable production, sustainable purchasing and sustainable development cover the three factors of sustainability. In the present study, in order to cover all the dimension of TBL, following Srivastava (2007), Seuring and Muller (2008) and Golicic and Smith (2013), the upstream activities are further broken down into smaller activities, namely sustainable sourcing, resource utilization and sustainable procurement. Similarly, the operations have been studied as sustainable production that includes reduction of waste and recycling activities. Downstream activities are further broken down into smaller activities such as sustainable products/projects and resource saving. Business responsibility has also listed sustainable products/projects and resource saving as two activities to be reported by the firms.

To achieve the objectives of the article, content analysis has been employed to analyse the principle ‘life cycle sustainability of goods and services’ from the BRR. Further, multiple regression analysis has been conducted to check the impact of SSCM activities on the financial performance of the companies.

Content Analysis

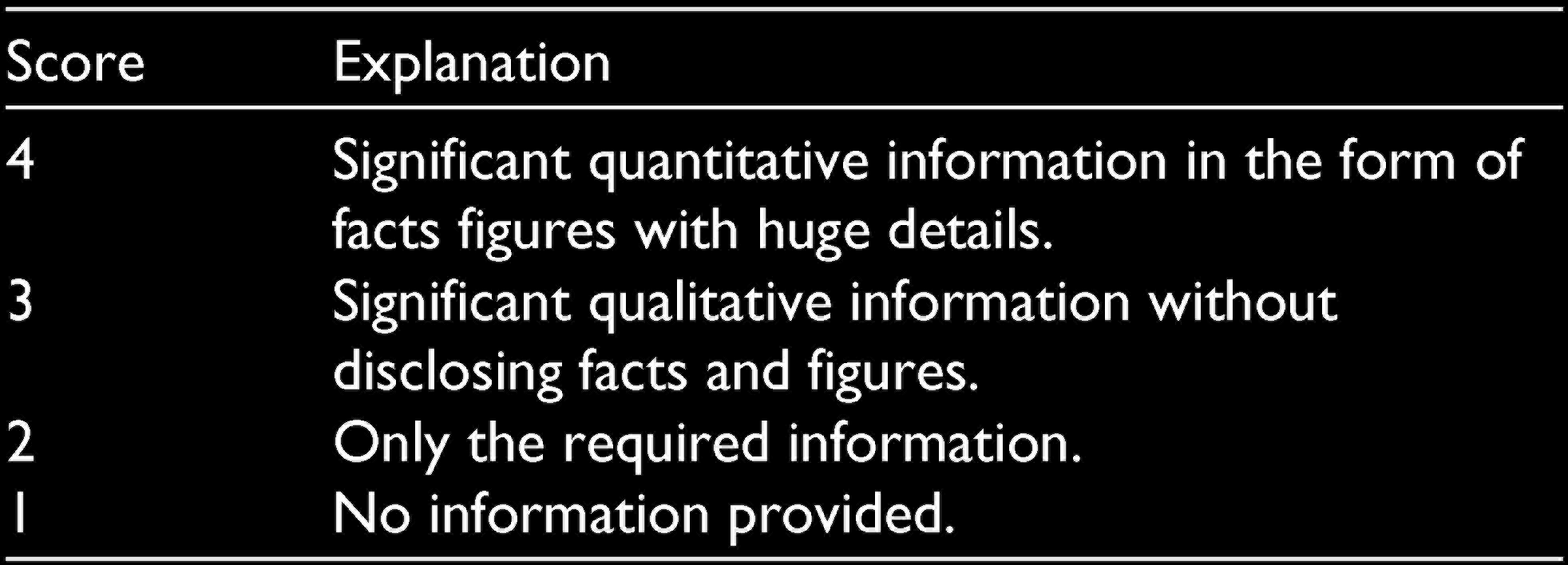

Content analysis is widely used in the sustainable supply chain literature (Ameer & Othman, 2012; Gill et al., 2008; Jose & Lee, 2007; Morhardt, 2010; Rondinelli & Berry, 2000). The two researchers separately content analysed ‘life cycle sustainability of goods and services’ principle from BRR. First, we generated the activities in the supply chain based on the previous research and the BRR. The activities identified are: (a) sustainable products/projects, (b) sustainable production, (c) resource utilization, (d) resource saving, (e) sustainable procurement and (f) sustainable sourcing. Second, each activity is assigned a score ranging from 4 to 1 based upon the content given in the BRR. Analysis of the content has been undertaken in the following manner: If a firm reported a significant quan-titative contribution to related activity, the firm gets a score of 4. Significant quantitative information means financial information, detailed contribution in the terms of numbers and so on. If a firm disclosed significant qualitative contribution to the related activity, we give it a score of 3. For example, detail of sustainable product but without disclosing the quantity of energy it saves and resources it uses. We give a score of 2 for the activities which reported the required information only and not much more. For instance, the firm that reports the activity in the form of yes and no only. And, the last score of 1 is given to the company that does not report any contribution related to that activity. Similar scoring is reported by Bart (2007) for the content analysis of mission statements. The score sheet is illustrated in Table 1.

The Score Sheet

Regression Analysis

Following López et al. (2007), Lo and Sheu (2007), Wagner (2010) and Ameer and Othman (2012) multiple regression analysis has been used in the present article. Tobin’s q has been taken as the dependent variable to measure the financial performance. Tobin’s q being the ratio between the value of the company’s assets and the replacement cost of the company’s asset (Kaldor, 1966) is a robust measure of financial performance. The expected signs for the explana-tory variables are given in Table 2.

Expected Signs of the Independent Variables for the Firms

Apart from the six explanatory independent variables and one dependent variable (Tobin’s q), an additional control variable has been included in the model on the basis of existing. The control variable included is sales growth, which is measured as a natural log of sales change.

Analysis and Interpretation

This section details the impact of sustainable supply chain activities on the financial performance of the company. The regression findings reveal that sustainable supply chain activities have a significant impact on Tobin’s q (R2=0.18, f-value 2.757 and p=0.012). Thus, the independent variables explain the 18 per cent variance in the dependent variable. Hence, the sustainable supply chain practices have a significant impact on the financial performance of the company.

Further, the results of the regression analysis show that some activities have a significant positive impact while other activities have a significant negative impact on Tobin’s q. Sustainable sourcing (β=1.999 and p<0.05) and resource utilization (β=1.996 and p<0.05) have a significant positive impact on the Tobin’s q such that Tobin’s q of a firm increases with the increase in sustainability in sourcing and resource utilization by the firm. Thus, H1 and H5 are supported, meaning thereby that sustainability in sourcing (Blome et al., 2014; Carter & Jennings, 2002; Kashmanian et al., 2015) and resource utilization (Hart & Ahuja, 1996; Vachon & Wao, 2008) activities have a significant positive impact on the financial performance of the firm. Resource saving (β=–2.623 and p<0.05) has a significant negative impact on Tobin’s q of the firm, that is, Tobin’s q decreases with the increase in sustainability in resource saving. Thus, H6 is supported meaning thereby that resource saving has a significant negative impact on the financial performance of the firm. Sustainable procurement, sustainable products/projects (Wang et al., 2015) and sustainable production have no significant impact on Tobin’s q (p>0.05) of the firm. Therefore, H2, H3 and H4 are not supported because they have no significant impact on the financial performance of the firm. The control variable sales growth (β=1.926 and p<0.05) has a significant positive impact on Tobin’s q.

From Table 3, it is clear that the two major activities that positively contribute to the financial performance of the companies are sustainable sourcing and resource utilization. These two activities are part of the upstream activities of the SSCM.

Results of Regression Analysis

Conclusion and Implications

From the results of the regression analysis, it can be concluded that the financial performance of the company is affected by sustainable activities in the supply chain. However, the results of the analysis have both positive and negative impact on the financial performance of the firm. Frost, Jones, Loftus, and Laan (2005) and Vijfvinkel, Nasser, and Jolanda (2011) have also found similar results. Hart (1995) and Vachon and Klassen (2006) have found a positive impact of upstream activities on the financial performance of the firm. Our research also shows that the two activities that have a significant positive impact are the upstream activities. The reason might be that in India, being a vast country, the resources are scattered, and transporting raw material from the nearest supplier may save resources, like energy, and may reduce pollution and the cost for the firm. Another interesting finding highlighted in the study is that resource saving by customers has a significant negative impact. The reason might be that the firms have to invest in training programmes to educate consumers about the resource saving. The firms might have to communicate the benefits of resource saving to the consumers.

Though firms have not been able to translate resource saving and sustainable products and projects into enhancement of financial performance but still, firms can benefit by positioning the product as a sustainable product. The positioning of the product discloses its benefits and sustainability that differentiate the product in the marketplace. There is a definite shift in consumer preferences for sustainable products. This is an opportunity that is not being exploited by the companies as yet and hence it is not getting translated into better financial performance. The managers need to target this segment.

The results of the study offer implications for the companies. First, managers of all companies should focus on sustainable activities in order to enjoy better financial performance because sustainability practices in activities increase Tobin’s q of the company. Second, companies must source material from suppliers who are certified to be compliant with environment standards so as to increase their company’s shareholder value. Third, companies must also focus on saving energy, water and raw material in order to enjoy the better financial performance. Fourth, transporting raw material from the nearest possible supplier is another activity that companies need to focus upon.

The study also adds value to the existing literature on SSCM. Our study extends the sustainable development theory to an emerging market like India. In fact, it is one of the initial studies that has focused on the sustainable supply chain activities at micro level as mandated by the regulators of sustainability reporting, and studies the impact of such activities on the financial performance of the Indian firms and tries to highlight the sustainable activities of the supply chain that actually contributes to the performance of the company.

Scope for Future Research

The present study focuses on the process-specific interventions like the life cycle analysis. Sybertz (2017) defines the process-specific interventions as the actions within the supply chain that are being applied to aim better environmental, social and economic performance (TBL dimensions). Further research can be conducted using issue-specific interventions such as usage of energy and fossil fuel, and carbon emission in the SSCM. According to Sybertz (2017), issue-specific interventions concentrate on issues that strike particular supply chains but are focused on important issues that can affect different activities within a supply chain. Addition of these variables in SSCM can make the future studies more robust.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.