Abstract

The present study intends to investigate the impact of financial sector development on GDP growth in the four middle-income countries of South Asia over the period of 1990–2016. Using pooled mean group (PMG) estimation, this study tries to examine whether in these developing countries, GDP growth has been influenced by size of market capitalization and size of market turnover in the long run which are used as proxy for stock market development. Similarly, domestic credit to private sector is used as proxy for banking sector development while assessing its long-run impact on GDP growth. Furthermore, by incorporating a dummy variable for the global financial crisis (2007–2008), this study investigates whether these economies are vulnerable to external shocks or not. The outcomes of this study find that relatively, the impact of banking sector on GDP growth has remained low in the region. Nevertheless, the development in both sectors has positively influenced economic growth in the long run. The outcomes of this study suggest that both, i.e. stock market and banking sector, are vital determinants of long-run economic growth in the South Asian countries. Therefore, to achieve the sustainable growth, policymakers need to adopt the global approach which can be ensured by improving the quality and scope of financial services in these countries.

Keywords

Introduction

International linkages in the area of financial development and economic growth have acquired crucial importance in modern times. Due to the perfect mobility of capital across the world, the investors would try to invest in the asset in any country that yields the highest returns. This encourages the resource mobilization process, which may further lead to economic growth in the region. However, in the 1980s, especially in the middle-income countries of Asia, the situation was entirely different. Most of the Asian countries were struggling with the financial market imperfections such as illiquidity and other structural and institutional constraints (Claessens & Kose, 2013). The day-to-day working of stock markets in Asian countries was based on manual trading, which was guided by various kinds of stringent protections. In the same fashion, banking sector was suffering from the inadequacy of technological, transparency and governance issues. As a result, these countries were compelled to embrace the trade openness and encouraged the inflows of foreign investment to meet the investment requirements. After the Asian financial crisis of 1997–1998, financial sector consolidation was earmarked as thrust area for economic growth (Aghevli, 1999; Crockett, 1999; Le et al., 2015).

The revamping of stock markets and restructuring of banking sector have made the continent go to investment destination in the recent past. As a result, the stock markets of Asian countries have flooded with foreign investment. These financial sector reforms have changed the growth pattern of Asian countries within a span of 20 years (Krueger, 2006). However, while assessing the role of financial development, the contribution of stock markets has been underestimated across the region. Apparently, in a well-developed banking sector, stock markets have tendency to grow which may further lead to economic growth in the long run (Aghevli, 1999). The mounting literature provides insights only about the banking sector reforms and its impact on economic growth. Therefore, to bridge the research gap, in the present article, besides banking sector, the impact of stock market development has also been examined. In the middle-income countries of South Asia, which are committed to sustainable economic growth, assessing the contribution of stock market and banking sector development becomes vital. Indeed, without understanding the role of stock market and banking sector, the pattern of economic growth may not be easy to determine. Since both the sectors are intricately linked to each other, ignoring any one of them may invite the problems in financial front which may compel to initiate the stock market and banking sector reforms (Krueger, 2006). Therefore, the present research work has tried to analyse the impact of stock market and banking sector development on economic growth in the four middle-income countries of South Asia over the period of 1990–2016. The inclusion of financial crisis of 2007–2008 as an independent variable in this study may enable to understand that whether these countries are vulnerable to external financial effects. The selection of the comprised countries is based on the World Bank’s income criteria which portrays that these countries come in the middle-income segment. Moreover, in the selected countries (i.e. India, Pakistan, Sri Lanka and Bangladesh), GDP growth has witnessed an upward trend during the study period.

The present study is divided into five segments. The second segment ‘Review of Literature’ provides insight into the present state of literature pertaining to the economic growth and financial sector development and rationale of this study. The third segment ‘Research Methodology’ highlights the research methodology and framework. Thereafter, the fourth segment ‘Results and Discussion’ analyses and interprets the results of this study. Lastly, the fifth segment ‘Conclusion’ ends with conclusion and policy implications.

Review of Literature

The extant literature pertaining to the association between financial sector and GDP growth can be segregated into three groups: the first group tries to assess the impact of financial sector development on GDP growth which is known as supply-led group. The second group, which is termed as demand-led group, holds the view that economic growth leads to financial sector development in the long run. The third school of thought assumes that financial sector development and GDP growth are complementary to each other. In other words, both, i.e. financial development and GDP growth, have tendency to affect each other in the long run (Ahmad et al., 2016).

Following the supply-led outcomes, Levine (1997) and Ang (2008) have identified the role of quantitative and qualitative factors which may have long-run influence on GDP growth. The quantitative endeavours may help in enhancing credit facilities by improving the financial services which may further lead to fresh productive investment and economic growth. In the beginning, financial development reduces the infrastructural constraints and this induces the new investors for investment. On the other hand, qualitative measures ensure that whether the quality of credit facilities and services is user-friendly or not (Pereira, 2008). As a result, qualitative channels indirectly influence the level of investment. However, a countryspecific study carried by Jayarathe and Satrahan (1995) in the USA ascertains that inter-state and inter-bank relationship may have an impact on the quality of loan which means that the efficient financial system, i.e. quality of financial services is more important than the size of economic growth. Similarly, the outcomes of Hassan et al.’s (2011) study carried in 168 countries observed that in developing countries, financial development has a positive impact on economic growth over the study of 1980–2007. To assess the financial development, this study uses six determinants: (a) banking sector’s credit to domestic sector, (b) banking sector’s credit to private sector, (c) the ratio of M3 to GDP (liquid liabilities), (d) gross domestic savings, (e) trade and (f) government consumption expenditure. All the determinants are taken as the ratio to GDP. As far as the combined impact of banking sector and stock markets development is concerned, the study by Beck and Levine (2004) carried in 40 developed countries showed that both, over the period of 1976–1998, have positively influenced economic growth. For signifying the financial and banking sector development, the study used the ratio of stock market turnover and credit to the private sector by banking sector, respectively. Similarly, by using the determinants of financial sector and banking sector in 25 developing countries over the period of 1993–2000, Koivu (2002) observed that financial growth has a positive impact on economic growth, whereas the impact of banking sector determinants has been found negative. The negative impact of banking sector may be the outcome of banking crisis of 1990s and infrastructural inefficiencies. The outcomes of various studies suggested that in developing countries, financial sector has a positive impact on economic growth (Raddatz, 2006; Rousseau & Yilmazkuday, 2009).

Taking into consideration the demand-led approach, Wurgler (2000) perceived that availability of natural resource and state of economic development has an impact on financial sector development. Subsequently, developed financial market guides about the productive and unproductive investment ventures. Similarly, using the pre-independence and post-independence data of Central Asia, Djalilov and Piesse (2011) observed a bidirectional relationship between financial development and economic growth. However, the relationship between them varies across countries during the study period. The mixed-up results may be due to the institutional and infrastructural peculiarities among the countries. Furthermore, in transition economy, besides the development of financial sector, other macroeconomic determinants may also have a spillover impact on economic growth. The outcomes of De Haas (2001) study showed that in developing countries, asymmetric information and transaction costs may hamper the financial sector development which may lead to economic slowdown.

Compared with European countries, the process of financial sector development in Asia countries has been remained slow over the period. In the 1990s, inadequate infrastructure, non-performing assets (NPAs) and poor technology were the common features of financial sector in the region (Uyanik & Segni, 2001). The share of bank credit to private sector in India, Pakistan, Indonesia and Bangladesh was less than half in comparison with some major high-income countries of Asia. In addition, the same significant gap between developed and developing countries has been observed in capital markets. However, in terms of stock market capitalization, India has emerged as a leader after 2002 and performed better than many developing countries. Similarly, despite the infrastructural and administrative reforms, the development of Asian bond markets has been remained very slow in the recent past (Estrada et al., 2010). Nevertheless, in the recent past, due to the efforts of central banks of Asian countries, banking sector and stock markets have been restructured entirely. After the recent global financial crisis, in East and Southeast Asia, lending to private sector has increased significantly. Additionally, the stock and bond market capitalization have also showed upward movements (Adams, 2008). Apparently, most of the countries in the region have witnessed a significant economic growth during this period (Djalilov & Piesse, 2011). Ahmed and Ansari (1998) observed that financial sector development initiatives of 1990s have a positive impact on GDP growth in South Asian countries. The outcomes of the study confirmed the validity of supply-led hypothesis of economic growth. Ahmad and Malik (2009) perceived that in 35 developing countries of Asia and Africa, efficient resource allocation through banking system has broaden the scope of financial sector which has further led to per capita income increase. Furthermore, the study observed that compared with foreign investment, domestic investment has been remained instrumental in channelizing the financial resources. On the other hand, the study by Chee and Nair (2010) carried in 44 Asian and Oceania countries over the period of 1996–2005 observed that banking and stock market reforms have been decisive factors to attract the foreign direct investment (FDI) which has a positive impact on economic growth in the region. The study revealed that in the set of least developed countries, financial sector and FDI have remained complementary to each other. Assessing the nexus between financial sector and economic growth in the middle-income countries of South Asia for the period of 1980–2013, Murari observed that bank lending to domestic sector and GDP growth has a bidirectional association. Furthermore, the study found that stock market capitalization, liquidity and economic growth have tendency to influence each other in the long run. However, domestic credit to the private sector has an insignificant impact on economic growth which shows that the scope of banking sector needs to be improved. Contrarily, the outcomes of a time-series data-based study carried out by Hye and Wizarat (2013) in Pakistan observed that the short-run impact of financial reforms on economic growth has remained positive and significant, whereas in the long run it has an insignificant impact on economic growth. The long-run insignificant association between financial development and economic growth may be due to the slow growth of stock market capitalization in the Pakistan. Beside financial sector development, international macroeconomic fluctuations may have an influence on economic growth of a country. The study by Balboa and Mantaring (2011) observed that in Philippines, due to financial crisis, besides economic growth, financial markets have also observed the slowdown, especially in 2008–2009. Similarly, the study by Ali and Afzal (2012) conducted in Pakistan and India found that due to the financial crisis, the stock market returns in Pakistan and India have witnessed a downfall; however, in Indian case, its negative impact has remained stronger than Pakistan. The large size of market capitalization may be the reason for strong negative impact in India. Furthermore, the study concluded that the negative shocks are more significant than positive shocks.

Due to the growing trade links in the recent past, financial markets in the Asian region have come closer to each other which has enlarged the scope of investment through stock markets. Besides, the international presence of banks has strengthened the scope of trading endeavours. The existing stage of financial development and economic growth in the South Asian countries provides the scope of a panel study. Therefore, the study by creating a set of four middle-income countries of South Asia has intended to investigate that whether the development of financial sector has an impact on economic growth in the long run. At the same time, using financial crisis as a dummy variable this study tries to investigate that whether these countries are substantially vulnerable to international economic activities or not.

Need of the Study

Due to the rapid economic growth in the middle-income countries of Asia, the researchers and policymakers have tried to investigate the determinants of economic growth in the recent past. However, most of the studies have ignored the role of stock markets to determine economic growth in the region. The present study is distinct in three manners. (i) This study has included stock market and banking sector development to exhibit the financial sector growth. (ii) This study uses the pooled mean group (PMG) approach that allows the use of common coefficients in the long run, whereas across countries the short-run coefficients and error variances can be different. The long-run common coefficients would be identical provided the model holds the assumption of same technology (Solow, 1956). Apparently, the state of technology is similar in the identified countries of South Asia. (iii) Lastly, the gist of this study is to explain whether recent financial sector developments have contributed to increase the level of national income in the selected developing countries of South Asia. In the recent past, besides economic growth, the financial sector has witnessed a complete turnaround in the region. In this context, the studies in the past have ignored the association between GDP growth and financial sector development.

Research Methodology

Using the PMG approach, this study explores the long-run impact of financial development on economic growth in the four middle-income countries of South Asia over the period of 1990–2016. The definitions and sources of comprised annual data series are mentioned in Table 1. The literature provides proxies for financial sector development. However, due to the methodological differences, it is difficult to identify the common determinants of financial sector development. Nevertheless, the literature identifies three crucial proxies for financial sector, namely stock market capitalization, stock market turnover ratio and credit provided by banking sector to private or domestic sector (Beck & Levine, 2004). The stock market capitalization is calculated by dividing the value of listed shares to GDP of a country. Similarly, the ratio of value of traded shares to value of listed shares provides the stock market turnover ratio. The size and liquidity in the market is represented by stock market capitalization and turnover ratio, respectively. If these two indicators exhibit the high level, then it shows that stock market is developed. The development in banking sector is estimated by calculating the ratio in which numerator is lending by banks to domestic private sector and denominator is GDP of a country. This approach allows exclusion of lending by banks to government and public companies. Beck and Levine (2004) considered that exclusion of government sector borrowing provides the real picture of a market.

Data Sources and Definition of Variables

Furthermore, inflation, trade openness, investment, government consumption expenditure, real rate of interest and broad money are included as controlled variables in this study which are identified as crucial variables for economic growth (Murari, 2017; Saci & Holden, 2008). To detect the vulnerability and sensitivity in selected countries, this study uses a dummy variable for the financial crisis of 2007–2008 in which value 0 represents the absence of financial crisis and value 1 captures the impact of financial crisis through selected determinants. The real impact of financial crisis is felt after 2008; therefore, the year 2008 is considered as the beginning of financial crisis in the Asian markets. Table 1 shows the sources and definition of selected variables.

Framework

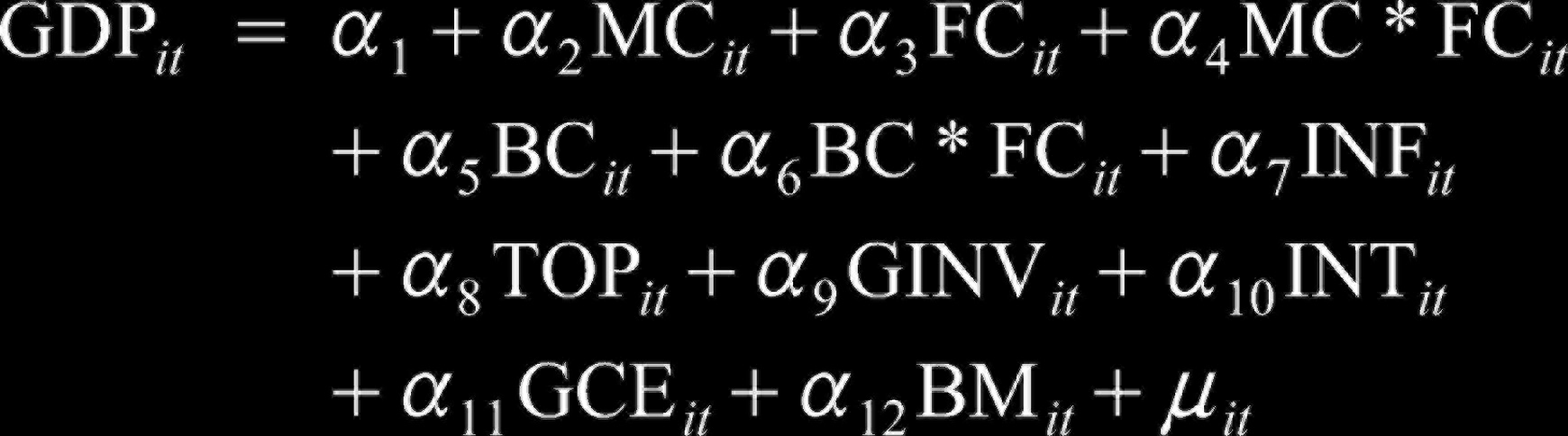

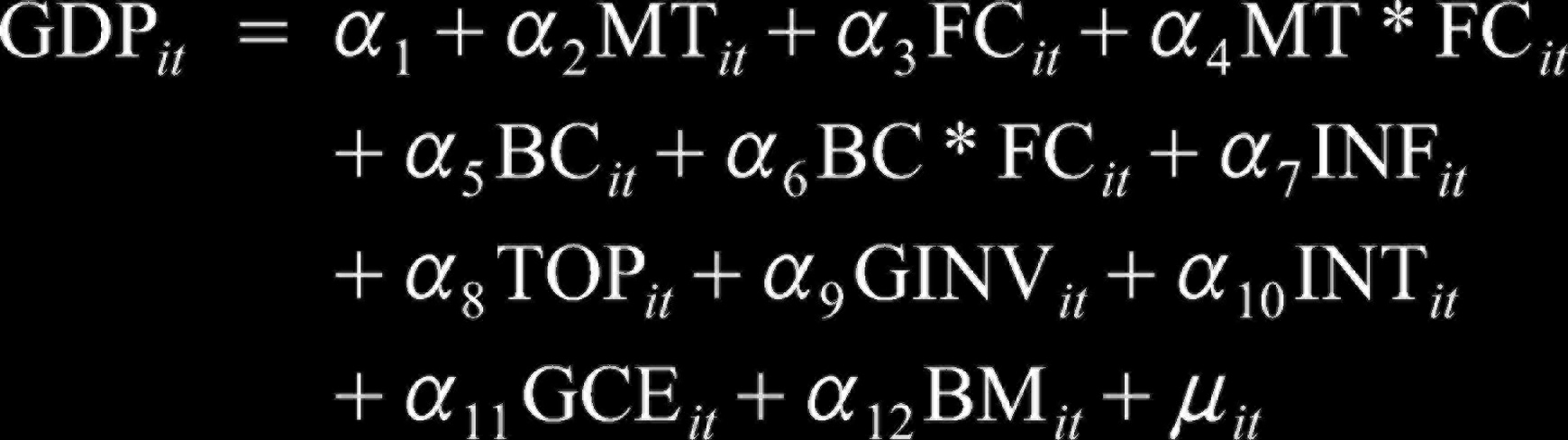

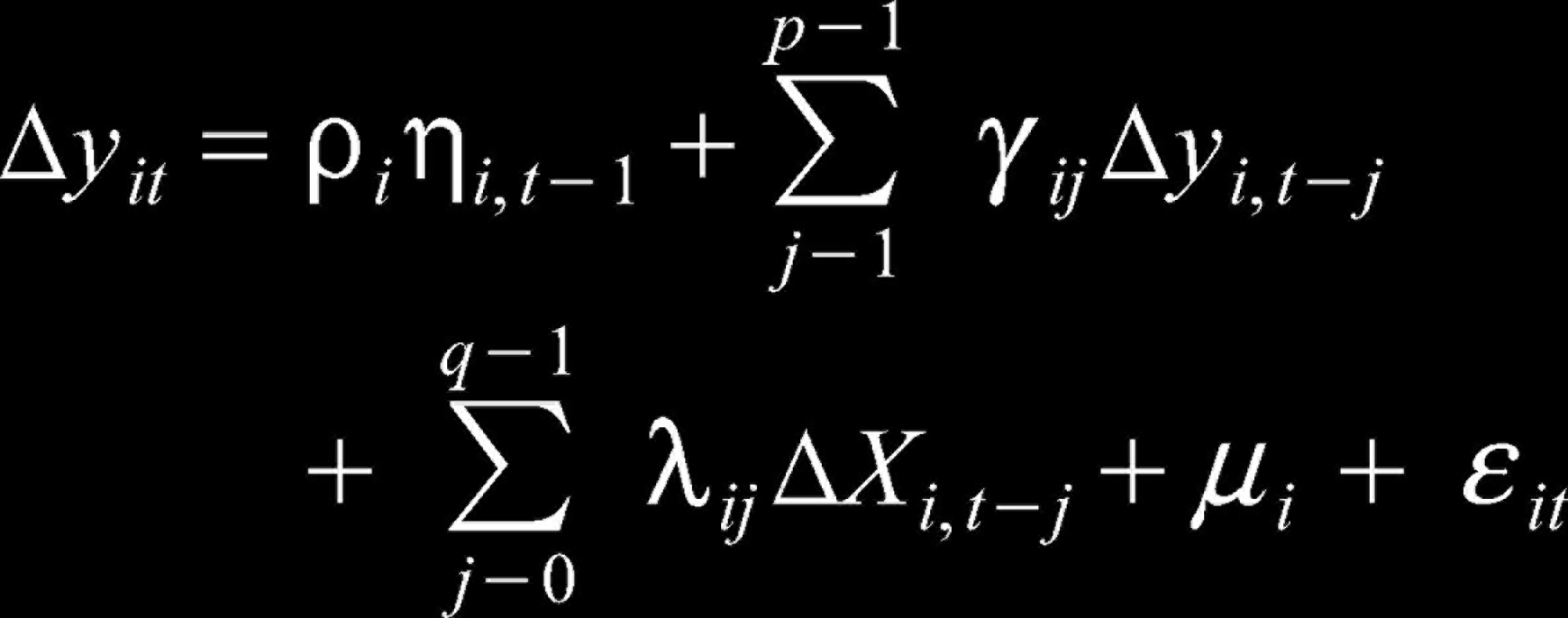

The present research work has applied the PMG estimation which is suitable for dynamic panel analysis (Pesaran et al., 1999). Using the heterogeneous dynamic adjustment procedure, this approach establishes the long-run equilibrium. The PMG approach ignores the assumption of common parameters across the countries, which is an important assumption in fixed and random effects approaches. In case of longer time period and small size of cross sections, the PMG approach is preferred than generalized method of moments (GMM). The PMG approach even works with I(0) and I(1) types of variables, which is most likely to happen in the large time-series data (Gujarati & Sangeetha, 2007; Pesaran et al., 1999; Sharma et al., 2018). In the present study, the numbers of selected countries are four and the period is 27 years. Thereby, the traditional panel approaches may provide the misleading results in dynamic panel model. Moreover, the slope coefficients are identical, if traditional approaches are to be followed. Whereas, PMG estimation assumes that the short-run coefficients, intercepts and error terms can differ across cross sections. Moreover, across cross section, the long-run coefficients are similar over the period (Das, 2011). Furthermore, by averaging the coefficients, PMG estimates the pooled data as a system and provides the common coefficients for the long run. Using per capita GDP growth as a dependent variable, equation (1a) and (1b) provide the baseline framework for this study (Ahmad et al., 2016; Murari, 2017; Sharma et al., 2018a):

In equation (1a) MC represents the stock market capitalization, and in equation (1b) MT represents the size of market turnover in the selected countries. The details pertaining to the other variables are mentioned in Table 1.

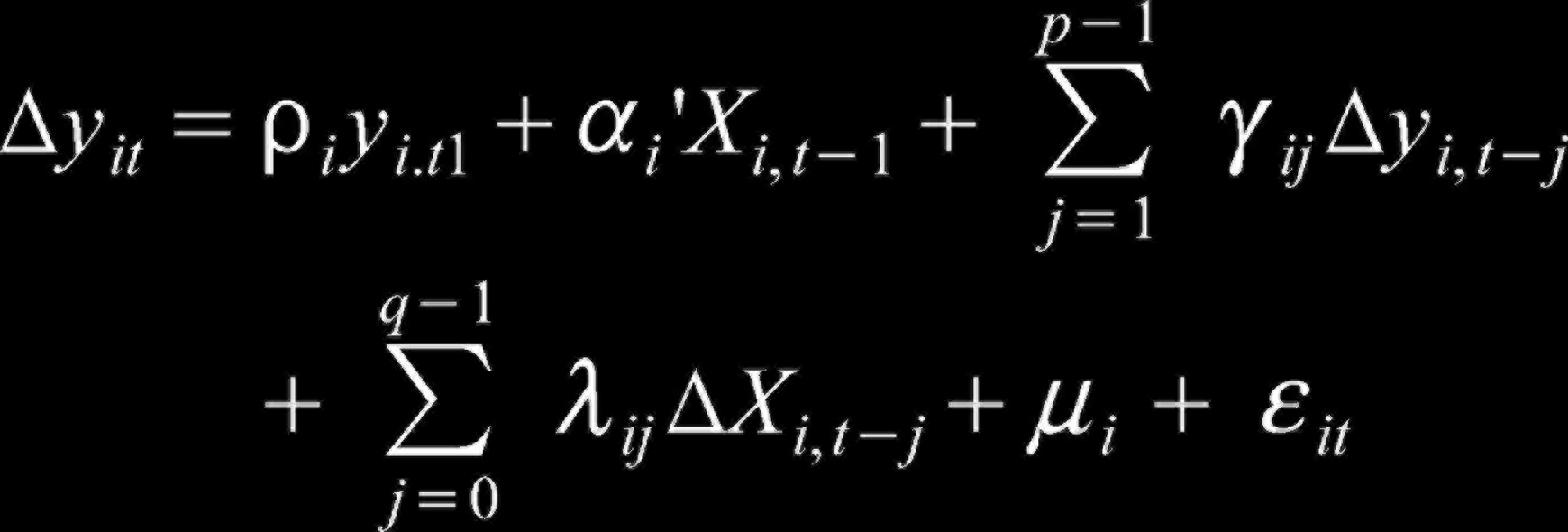

Thereafter, using the autoregressive distributed lag (ARDL) model, equation (2) provides the unrestricted specification, where GDP (y) is taken as dependent variable.

where i is number of countries and t is time period.

In equation (2), yit and Xit are taken as scalar dependent and independent variables (k × 1 vector), respectively. Furthermore, ρi and αi’s represent lagged dependent coefficient and independent variable coefficients, respectively. The lagged first differences coefficients of dependent variables are denoted by γij, and the lagged first differences coefficients of independent variables are represented by λij. Assuming the independent distribution of i and t across cross section, mean 0 and variances > 0, the error term is shown as εit. Furthermore, the assumption of ρi < 0 for all i provides a long-run relationship between dependent and independent variables.

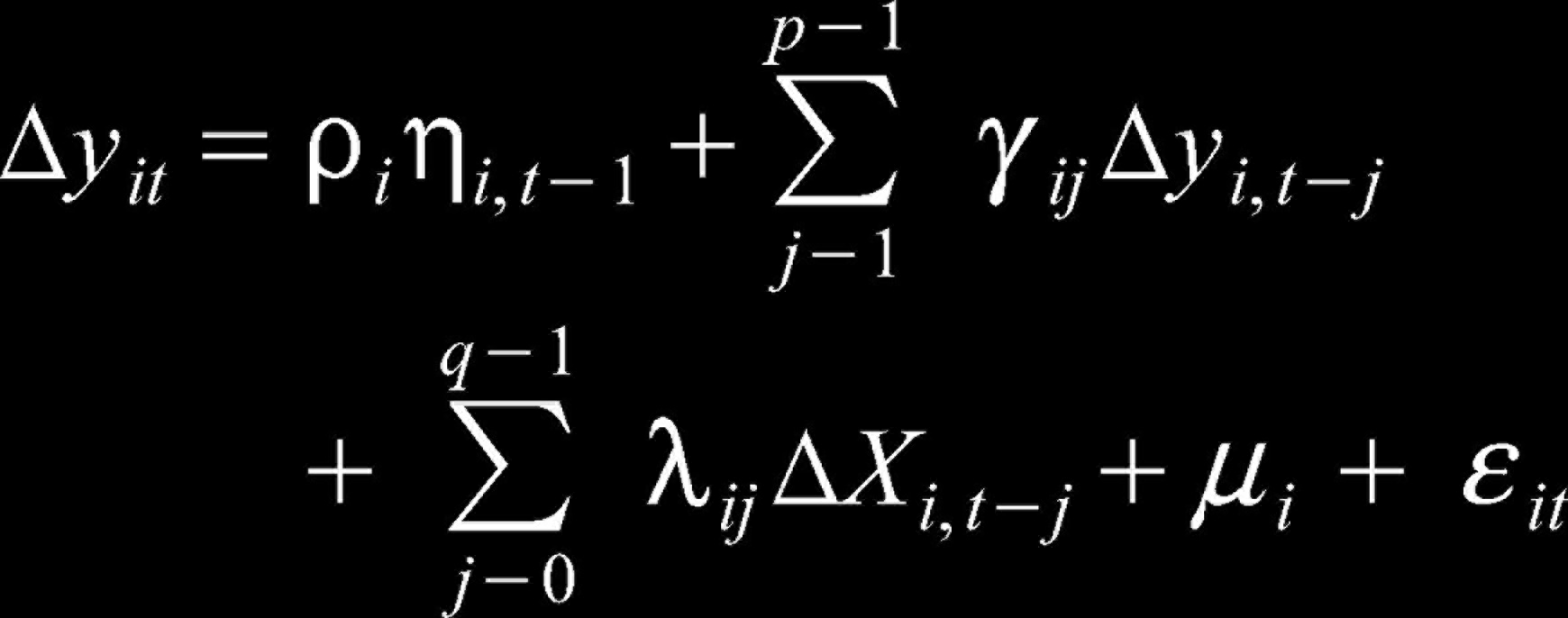

where ɸ = αi/ρi which represents the long-run coefficients of k × 1 vector and ƞit’s are assumed to be stationary with non-zero means. Equation (4) is the representation of equation (2), where error correction term given by equation (3) is being used.

Thereafter, equation (5) provides the error correction coefficient, i.e. θ, which represents the speed of adjustment for the long-run equilibrium. This system provides the common coefficients for long run, whereas the short coefficients and error correction terms are allowed to vary across cross section. Using the Hausman’s (1978) test directs that whether long-run homogeneity among parameters is available or not. After detecting the long-run homogeneity in the pooled data, PMG estimation can be applied. The pooled data-based PMG estimation is given as:

Results and Discussion

Panel Unit Root Test

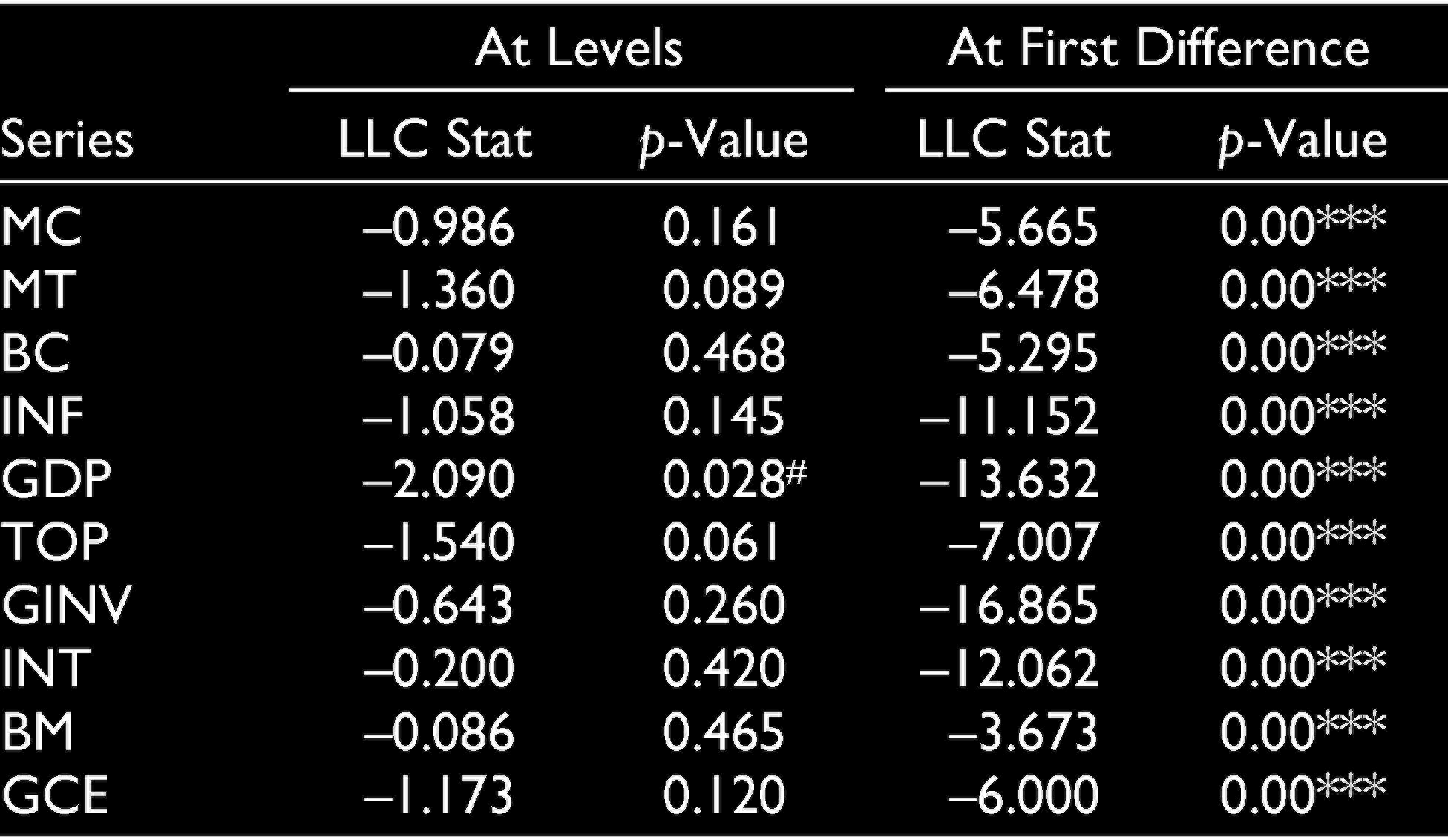

First, the stationarity of included data series using Levin et al.’s (2002) common unit root test is examined. This LLC test considers that the coefficients of the autocorrelation are identical across the countries. In other words, the LLC test assumes the common testing mechanism across cross sections and it is based on asymptotic normality while calculating the panel unit root test (Murari, 2017). This panel unit root test assumes the null hypothesis of non-stationary series at level. It is evident from the results of Table 2 that except GDP all other series are unable to reject the null hypothesis of unit root at level, whereas at first difference all the series are stationary.

LLC’s Panel Unit Root Test Assuming Common Unit Root Process (At Levels And First Difference)

On the other hand, Im et al.’s (2003), Madala and Wu’s (1999) and Phillips and Perron’s (1988) individual unit root tests considered the individuality assumption that allows the coefficients to change across the countries. While calculating the coefficients, Im et al.’s and Phillips and Perron’s tests considered the asymptotic normality assumption, whereas Madala and Wu’s (1999) test values are calculated using chi-squared dispersal. The results of Im et al.’s (2003), Madala and Wu’s (1999) and Phillips and Perron’s (1988) individual unit root tests showed that all the individual series are stationary at first difference and reject the null of hypothesis of non-stationarity. The results for these tests are mentioned in Table 3.

Thereafter, to measure the long-run co-integration between dependent and independent variables, Kao’s (1999) panel co-integration test is performed. This test is an extension of ADF stationarity test and uses the residuals for the long-run co-integration. Furthermore, it assumes the homogeneous slopes and dissimilar intercept across cross section.

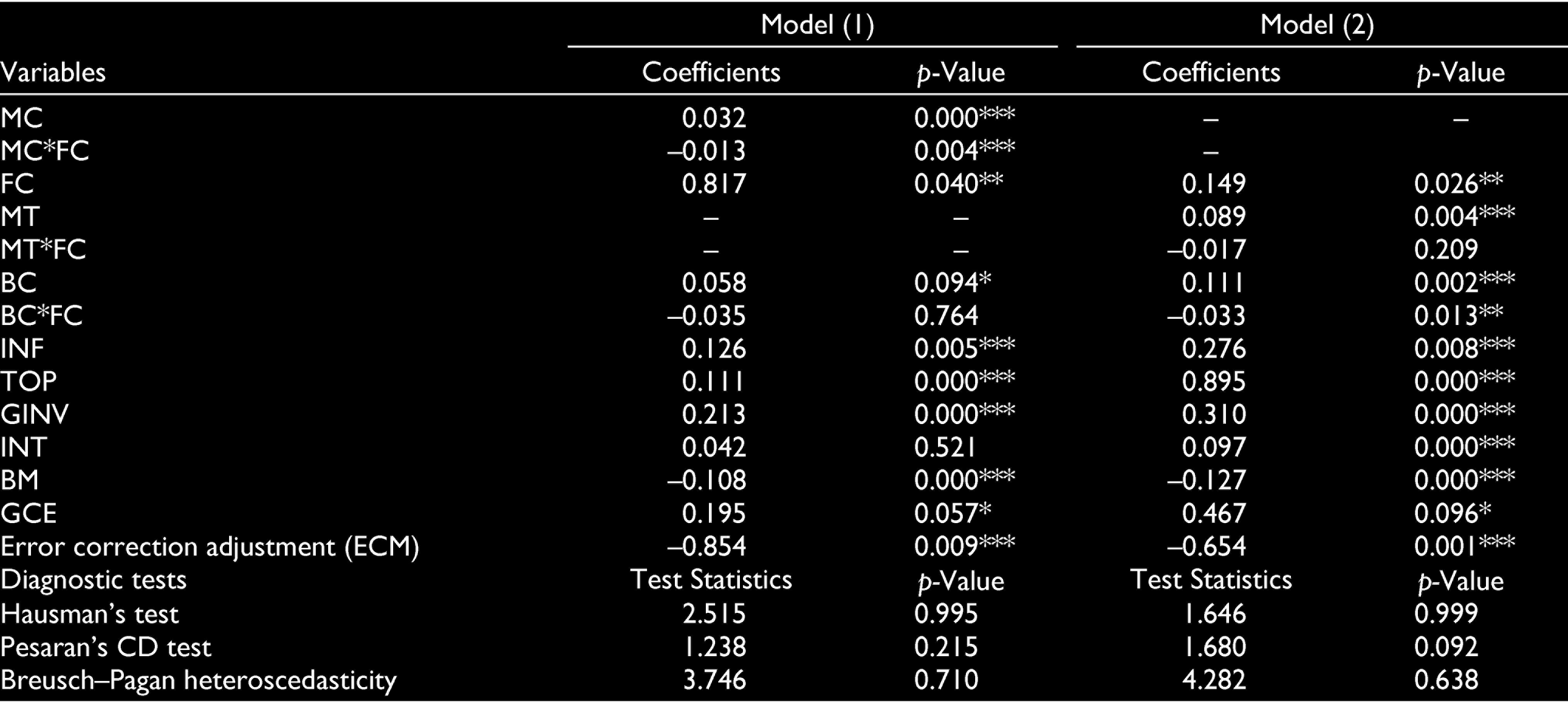

The outcomes of Kao’s panel co-integration test given in Table 4 reveal the association between dependent and independent variables over the study period. It is evident from the outcomes of Table 4 that all the dependent variables have either unidirectional or bidirectional association with independent variables. Therefore, the comprised proxies for financial sector development can be used to examine the PMG estimation in the developing countries of South Asia. Thereafter, using PMG estimation, the outcomes shown in Table 5 provide the long-run relationship of GDP growth and financial sector development in South Asian middle-income countries, which enables to assess the magnitude of coefficients and the direction of relationship between dependent and independent variables. In Table 5, market capitalization and stock market turnover are used as proxy for stock market development and domestic credit to private sector by banks is used as proxy for banking sector development.

Panel Unit Root Tests Assuming Individual Unit Root Process (At Levels and First Difference)

Kao’s Panel Co-integration Test

Results of Pooled Mean Group Estimation, Dependent Variable: GDP Growth (Four Countries, 1990–2016)

Outcomes of the PMG Model

The results shown in Table 5 reveal the long-run association between stock market, banking sector and GDP growth in the South Asian middle-income countries over the period of 1990–2016. The results of model (1) show that market capitalization has a positive and significant impact on GDP growth. On the other hand, the interaction of market capitalization with financial crisis (MC*FC) has negatively influenced the GDP growth in the long run. In other words, it can be perceived that in the middle-income countries of South Asia, due to the financial crisis, stock market capitalization has led to decline in GDP growth. Furthermore, the long-run impact of domestic credit to private sector by banks, which is used as a proxy for banking sector development, on GDP growth is found positive in the region. However, it is evident from the outcomes of model (1) that the coefficient of domestic credit to private sector by banks is statistically significant at 10 per cent level, which poses a question on the role of banking sector in the development of South Asian economies. Besides, its interaction with financial crisis has not significantly influenced the economic growth in the long run. The outcomes of the present study are consistent with the earlier studies, where stock market capitalization and banking sector development has a positive impact and their interaction with financial crisis has a negative impact on economic growth (Ahmad et al., 2016). Apparently, due to the lack of integration or openness of banking sector in South Asia, the negative impact of banking sectors’ interaction with financial crisis might have been reduced in the long run (Brunschwig et al., 2011).

The results of model (2), given in Table 5, suggest that the size of market turnover, which is also used as a proxy for stock market development, has a positive impact on GDP growth in the long run. However, the interaction of market turnover with financial crisis has a negative impact on GDP growth in the region. The positive impact of market turnover and market capitalization on GDP growth suggests that due to the growth in stock market, GDP growth in the middle-income countries has positively been influenced in the long run. On the other hand, global financial crisis has played a negative role in the development of stock market, which has further led to decline in GDP growth. Unlike model (1), the outcomes of model (2) suggest that the interaction of banking sector development with financial crisis has a negative and significant impact on GDP growth in the region.

Furthermore, the outcomes of models (1) and (2) suggest that inflation, trade openness, investment and government consumption expenditures have a positive effect on GDP growth in the long run. The positive and significance association of trade openness, investment and government consumption expenditure with GDP growth confirms the outcomes of earlier studies (Ahmad et al., 2016; Loayza & Ranciere, 2006).

Both models have been computed using lag one for the independent variables across cross section (Pesaran et al., 1999). To establish the long-run relationship, Hausman’s test assumes the null hypothesis of common coefficients across cross section. It is evident from the results of joint Hausman’s test that the null hypothesis cannot be rejected in both models. Therefore, the study confirmed the results of PMG estimation and provided common coefficients for independent variables, which have a long-run impact on dependent variable. Unlike mean group (MG) estimation, PMG estimation provides the common short-run and long-run coefficients, if the Hausman’s test statistics are unable to reject the null hypothesis of no common coefficient. Furthermore, the negative and statistically significant coefficients of speed of adjustment confirm that the models (1) and (2), if disequilibrium happens, automatically achieve the long-run equilibrium with a speed of (–0.854) and (–0.654), respectively. In other words, both models automatically adjust to the long-run equilibrium since sign of the error correction terms is negative and statistically significant in both models. Similarly, the outcomes of Pesaran’s cross-sectional dependence test confirm that both models have absence of cross-sectional dependency. Similarly, the p-values of Breusch–Pegan test confirm the absence of heteroscedasticity in both models.

Based on the outcomes of PMG models (1) and (2), it can be suggested that in the sample countries, GDP growth has positively been influenced by stock market and banking sector development in the long run. However, global financial crisis has negatively influenced the stock market and banking sector in the region, which has further led to decrease in GDP growth. The outcomes of Wolde-Rufael’s (2009) and Murari’s (2017) study also observed that financial and banking sector development has a positive impact on GDP growth in Kenya and South Asian developing countries, respectively. For examining the causal association between incorporated variables, the Granger causality test has been performed. The results of this test are given in Table 6.

Granger Causality Test Results

It is evident from the results of Table 6 that market capitalization (MC), capital formation (GINV), broad money (BM) and interest rate (INT) have Granger caused domestic production (GDP) in India. Conversely, GDP has driven market turnover (MT), inflation (INF), trade expansion (TOP), bank lending (BC) and financial crisis (FC), as the null hypothesis is not established by the calculated p-values.

Conclusion

Indeed, the coexistence of robust economic growth with fiscal and balance of payment (BoP) imbalance in the South Asian countries poses the question on the role of stock market and banking sector development since lack of integration and openness in stock market and banking sector may distort the growth endeavours and lead to unproductive distribution of resources. Therefore, the present study intends to investigate the impact of stock market capitalization and stock market turnover, which are proxy for stock market development, on GDP growth in the four middle-income countries of South Asia. Besides stock market, this study also tries to examine the influence of banking sector development on GDP growth in the region. In the past, various studies have tried to examine the impact of stock market and banking sector development on the economic growth in South Asia. However, most of the studies have neglected the role of financial crisis (2007–2008), which has shaken the world markets, while examining the impact of these developments. The present study using PMG estimation assesses that market capitalization and market turnover have positively influenced the economic growth in the South Asian countries. However, the interaction of stock market turnover and market capitalization with the dummy variable finds that global financial crisis has a negative effect on both the indicators, which has further led to decrease in GDP growth. Similarly, banking sector’s impact on GDP growth has remained positive and significant during the study period. Nevertheless, in comparison with financial sector, banking sector’s role has remained less significant in the region. Moreover, its interaction with the dummy variable of financial crisis has negatively influenced the economic growth. The results of PMG estimation given in both models confirm that for the present set of independent variables, common coefficients can be derived which provide the long-run stability in the model.

Policy Implications and Scope for Future Research

Referring to the outcomes of this study, it can be perceived that in the middle-income countries of South Asia, to achieve the sustainable economic growth, policymakers have to make the stock market and banking sector more growth-oriented, which can be ensured by infusing competitiveness while delivering the stock market and banking services. Furthermore, by enlarging the scope and quality of these services, governments of respective countries need to adopt the global outlook in the long run.

The present study has ignored the possibility of non-linear association between GDP and its determinants, which opens the scope for future research. Even, the economic fluctuations occurring in international markets may have an impact on domestic financial market. Therefore, while assessing the impact of financial sector development on GDP growth, the inclusion of international economic endeavours such as globalization may enable to provide better understanding about the phenomenon under study.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.