Abstract

Ever since the prominent work by Modigliani and Miller (1958), much research has been undertaken in trying to identify the factors affecting the capital structure. Lately, behavioural finance has begun to take hold of a more prominent position in trying to explain aspects of finance which traditional research has failed to clarify. In fact, a growing body of empirical evidence suggests that manager-specific characteristics significantly influence firms' financing decisions. The limited work carried out in lower-middle income countries drives us to thoroughly investigate the role played by CEOs’ characteristics in determining corporate financing decisions.

Employing a sample of 307 non-financial firms listed in Nifty 500 index, the panel regression results indicate that CEO tenure is significantly and positively associated to firm’s leverage for the possible reason that a long tenure of CEO reflects strong networks and alliances with important stakeholders that allow the CEO to compose, foster, and support risky initiatives like raising debt. Further, the level of leverage is higher at organizations where CEOs are younger on account of the fact that career and financial securities are imperative to a greater extent for older executives; therefore they may evade risky engagements that may interfere with their securities. The results also display that CEO share ownership has a significantly negative relationship to leverage because these executives have a large share of their personal wealth capitalized in the firm in the shape of firm-specific human capital and common stock holdings. This makes managerial insiders unwilling to use the optimum amount of debt funding for the firm for the reason that additional bankruptcy risk associated with higher levels of debt may arise.

The findings thus put forward that recurrent job changes among the senior officials should be discouraged because the subsequent short-term focus and dearth of firm-specific knowledge might promote risk evasion. It shows that elder executives desire a more conservative capital structure whereas younger executives endeavour to take more risk. So, there is a need to bring diversification in the management so as to take advantage from the skills and services of the young. The inverse association between CEO share ownership and firm leverage specifies that board of directors and the shareholders should be stringent in checking managers to make sure they perform as per the interests of shareholders. It seems that while making capital structure decisions risk seeking behaviour favouring high corporate leverage is important and should be encouraged.

Keywords

Introduction

A company’s capital structure remains a controversial matter in modern corporate finance. Ever since the prominent work by Modigliani and Miller (1958), much research has been undertaken in trying to identify the factors affecting the capital structure. Two central philosophies presently exist in context of decision on capital structure or corporate leverage: the trade-off model (TOT) and the pecking order model (POT; Myers & Majluf, 1984). TOT assumes that firms choose to allot their resources by comparing the tax advantages of debt with the costs of bankruptcy thereof, thus targeting an ideal debt ratio. POT challenges the preceding theory, contending that firms opt for a sequential choice over funding sources: they refrain from external financing if they have internal financing available and refrain from new equity financing when they can go in for new debt financing.

Capital structure has long been linked to the firm’s profitability and performance (Abor, 2005; Arbabiyan & Safari, 2009; Chakraborty, 2010). Researchers have undertaken research on leverage choices and studied the determinants of capital structure of firms (Céspedes et al., 2010; Deesomsak et al., 2004; Titman & Wessels, 1988). The focus of past research has been mostly on firm characteristics and corporate governance as determinants of capital structure. For example, Akdal (2010) examined various firm-level characteristics such as, profitability, size, growth opportunities, asset tangibility, non-debt tax shield, volatility and liquidity as predictors of capital structure. Yet various existing empirical papers could not slot in human elements in learning causes of companies’ financial leverage. Lately, behavioural finance has begun to take hold of a more prominent position in trying to explain aspects of finance which traditional research has failed to clarify. Researchers in accounting, economics and management agree that executive traits are critical in exercising strategic control, tougher monitoring and financial decision-making (such as capital structure) in firms. According to such scholars, executives have different characteristics such as age and gender which contribute to firms’ financing option among others. A prominent framework of financial literature regards rational behaviour and associated conduct of administrators as aspects of financial occurrences (Subrahmanyam, 2008). For instance, Oliver (2005) revealed that an individual executive’s traits may play a role in company’s financial leverage ratio. Therefore, it is crucial to examine whether these executive characteristics would enhance or weaken capital structure. This study therefore sought to fill this research gap by answering the research question: How do executive characteristics affect corporate leverage?

A number of notions also discuss the importance of executives in determining corporate tactics, which ultimately have a bearing on firm outcomes out of which the upper echelons theory (UET) needs a special mention here. The UET was established in an attempt to elucidate organizational behaviour, with the foundation of the idea being that organizational strategy originates as an outcome of the cognitive bases and values of upper management. But as information regarding cognitive bases and values can be difficult to acquire, Hambrick and Mason (1984) emphasize on using background characteristics, for example age, tenure, gender, socioeconomic background and experience as proxy because these are easily noticeable and can be considered as symbolic of the more ‘hard-to-obtain’ variables.

Despite important concerns against value creation by way of debt financing, debt happens to be an essential part of a typical organization’s capital structure through time and space. Executives do spend a substantial amount of time in planning their firms’ capital structure. Further, empirical evidence proposes that debt financing has devoted significantly to the growth and development of an economy (King & Levine, 1993). This is possibly the reason why the drift in resource distribution for the majority of lower-middle income and high-income countries shows a consistent upsurge in debt ratios with time. However, India stands as a special case where debt ratios of companies are consistently declining ever since the early 1990s, indicating the period of economic liberalization (Chauhan, 2017). On the other side, debt ratios in various other emerging markets displayed an increasing trend (Mitton, 2007). Therefore, it would be interesting to investigate deeper into the reasons that contribute significantly to the aforesaid anomaly. There are certain other competent aspects that make Indian firms worth being investigated. A majority of Indian listed firms are usually run by the family members and are family owned. It is predicted that the appointment of CEOs in countries where there is a concentrated ownership structure and where family-controlled firms are normally found is not the same from that in developed economies. Influential large family shareholders may take control to some extent in handling the CEO appointment mechanisms. It has been contended that such events might lead to substandard corporate governance because of an inadequate check and balance mechanisms on the part of board of directors.

This article adds to the previous works on CEO attributes and capital structure in quite a few aspects. First, an inclusive group of CEO traits and their influence on organization’s financial behaviours have been inspected to expand the work in economics and finance in addition to organizational theories. We investigate ideas suggested by the upper echelons model. Second, we inquire into CEO attributes of organizations in an evolving country where there exists concentrated shareholdings and this situation might be dissimilar from that in industrialized countries. Until now, there has hardly been any indication about the importance of CEO traits especially when confined to a growing country like India with respect to leverage decisions. Third, various studies have been executed on the UET, probing the association between managers’ demographical features and organizational results involving research and development spending (Barker & Mueller, 2002), technical innovativeness (Kitchell, 1997), financial disclosure (Bamber et al., 2010), cash holdings (Orens & Reheul, 2013) and corporate sustainable development (Huang, 2013). However, the practical implication of these studies continues to be basically unidentified especially in context of the link between CEO’s psychological and observable characteristics and firm leverage. Therefore, the present article tries to cover this gap via inquiring into CEOs’ traits and their possible repercussions on financing behaviour.

Literature Review and Hypotheses

A growing body of empirical evidence suggests that manager-specific characteristics significantly influence firms’ financing decisions (Bertrand & Schoar, 2003; Graham & Harvey, 2001; Schoar, 2003). Zwiebel (1996) expresses that the fact that the choice of capital structure is voluntarily chosen by the executive is undeniable. Similarly, Friend and Lang (1988) state that directors and officers have a personal inducement to lead the organization to employ less than the optimal quantity of debt into its financial structure. However, it is to be noted that research conducted in the developed countries (Berger et al., 1997; Faccio et al., 2016; Fosberg, 2004; Frank & Goyal, 2007; Friend & Lang, 1988; Serfling, 2014; Wen et al., 2002) outweighs the research carried out in developing countries (Abor, 2007; Sheikh & Wang, 2012; Ting et al., 2016). The limited work carried out in developing countries drives us to thoroughly investigate the role played by CEOs’ characteristics in determining corporate leverage decisions.

CEO Tenure

A CEO, who has continued with a firm for an extensive period, is likely to exhibit high proficiency as well as abilities (Hermalin & Weisbach, 1991). Hambrick and Fukutomi (1991) established a descriptive framework of the impact executive tenure has on performance with time, which came to be called as the seasons of a CEO’s tenure. The second season involves experimenting, which may mean that there is an increased level of risk-taking in the way of operating the firm. The executive is more comfortable with testing and experimenting because of the gained knowledge and accomplishment from the previous season. Therefore, this period is characterized by a more unsteady commitment to their paradigm because they are willing to experiment their wings as CEO. Moreover, CEOs with short tenancy may fall short of appropriate awareness to successfully observe and evaluate strategic risks. They are also untried, unfamiliar and devoid of legitimacy, which may bound their performance in progress (Simsek, 2007). Additionally, executives of the best-performing organizations engage in the utmost degree of territory building and attain increasing debt levels with the increase in their tenure (Zwiebel, 1994). Considering CEO tenure as a crucial characteristic, the study tries to approve the relationship and hypothesize the following.

H1: There exists a significant positive association concerning CEO tenure and firm’s leverage choice.

CEO Duality

The decision management and decision control should be distinct entities to effectively regulate the agency snags usually existing in the modern corporations (Fama & Jensen, 1983). However, Abor (2007), Mokarami et al. (2012) and Wellalage and Locke (2012) discover that CEO duality intensifies firm debt usage, signifying that according to stewardship model, CEO duality reduces communication conflicts and generates a clear sense of consolidated decision-making. Similarly, Faleye (2004) posit that the dual headship may reduce information asymmetry issues and lead to greater access to external debt. It suggests the relevance of avoiding conflict which may arise between a board chairman and a CEO, where the two characters are not the same. It could be described that the lack of this conflict allows the CEO in a one-tier structure to pursue a productive debt strategy built on the board’s advice. Despite the belief of direct relationship between CEO duality and corporate financing, it needs to be established in the Indian context, hence the following is hypothesized.

H2: There exists a significant positive connection between CEO duality and firm’s leverage decision.

CEO Education Level

Academicians have shown that managers’ inclination towards risk and decision-making styles varies by their education level. As per the UET, CEO education level is revealed in the traits of their corporations (Orens & Reheul, 2013). Finkelstein and Hambrick (1996) observe that executives with advanced education levels are eager to undertake risk to a greater extent. On an equal footing, Bertrand and Schoar (2003) report that executives holding MBA qualification are comparatively more aggressive and choose to involve higher level of capital expenditures besides holding more debt. They are not as much open to the accessibility of in-house sources of finance but more reactive to the existence of growth prospects or openings. In this research article, it is therefore anticipated that CEOs’ educational level is associated with greater debt financing by virtue of risk-taking attitude of CEOs with higher levels of education.

H3: CEO education level is significantly and positively related to financial leverage decision.

CEO Gender

Besides from the described variables, gender is additional chief variable to illustrate the traits of an executive. Faccio et al. (2016) documented that companies managed by female executives have less turbulent earnings, less leverage and a greater possibility of continued existence than otherwise alike companies managed by male CEOs. Above and beyond traditional clarifications such as agency and informational irregularities, potential economic reasons as to why CEO gender might affect risk-taking comprise (but are not restricted to) more prominent risk resistance in female CEOs (in comparison to male counterparts), divergence in job loss risk, less overconfidence, dissimilarities in incentive and compensation structures, and social standards. Similarly, Bertrand (2011) resolved that females are more antagonistic to risk than males in various situations. Therefore, it is well recognized that females are less risk tolerant as compared to men in general (Bernasek & Shwiff, 2001; Hudgens & Fatkin, 1985; Johnson & Powell, 1994). Based on the arguments, the nature of association between CEO gender and corporate financing the following is hypothesized.

H4: There exists a significant and negative relationship between female CEOs and financial leverage choice.

CEO Age

Founded on the UET, older CEOs stand more opposed to risk and are not as much assertive as younger or naive CEOs (Hambrick & Mason, 1984). Accordingly, these executives will wish to pick in-house funds in contrast to external funds. Older managers might be at a stage in their lives at which economic stability and career safety are vital. Their spending patterns, community circles and anticipations about retirement earnings are established. Any risky activity that might disrupt these usually are evaded (Carlsson & Karlsson, 1970). It was also established that older CEOs are inclined to be more economically vigilant as older age bracket of CEOs retained lesser cash holdings, interest coverage and financial leverage (Bertrand & Schoar, 2003). In addition to this, older executives sink a small amount of money into research and development, manage organizations with more varied operations, bring about more diversified acquisitions and uphold lesser operating leverage (Serfling, 2014). Founded on the above theoretical arguments the study anticipates the following.

H5: CEO age is significantly and negatively associated with financial leverage choice.

CEO Share Ownership

The association concerning ownership structure and capital structure is an important one because it reinforces the linkage between corporate governance and firm performance. Friend and Hasbrouck (1988) and Friend and Lang (1988) contend that a rise in managerial ownership drives organizations to lessen leverage in order to reduce default risk, thus supporting a negative link concerning managerial ownership and leverage. Fosberg (2004) also found an adverse association concerning capital structure and shares carried by the CEO, signifying that a CEO will keep their personal interests forward than those of the shareholders. Similarly, Bathala et al. (1994) stated a negative association concerning managerial ownership and debt ratio, suggesting that organizations trade-off executive ownership and debt so that the agency costs of the firm are controlled. Based on the examination of prior literature, the study assumes the following.

H6: CEO share ownership is significantly and negatively connected to firm’s leverage choice.

Research Methodology

Description of Data

The companies selected for this research work were those included in the list of Nifty 500 Index positioned by virtue of market capitalization as on 1 October 2016 after excluding banking and financial institutions, and firms for which whole time series data was unavailable. In the event of non-presence of CEO in a firm, person with an equivalent authority was selected, considering the individual’s signatures apparent on CEO/CFO credentials or on the statement concerning the code of behaviour for senior management and board according to Rule (17)5(a) of SEBI Regulations, 2015 which pertains to Listing Obligations & Disclosure Requirements. The ultimate sample for the study covered 307 non-financial firms. The duration for this research was five years commencing from 2012 to 2016. The data on CEO characteristics was gathered manually from the websites and the annual reports of the respective firms followed by Wikipedia, Bloomberg besides LinkedIn accounts of the corresponding officers. The firm-specific variables used in the research work were extracted from Ace Equity database.

Measurement of Variables

Operationalization of Variables of Interest

Research Framework

For scrutinizing the influence of CEOs’ attributes on financing decision, the following research model was constructed:

Leverageit = βit + α1CEOtenureit + α2CEOdualityit + α3CEOeducationlevelit + α4CEOageit + α5CEOgenderit + α6CEOShareownershipit + α7Boardsizeit + α8Boardindependenceit + α9Growthopportunitiesit + α10Firmsizeit + α11L(Firmage)it + α12Industryit + Ɛit

where α1–α12 stand for coefficients pertaining to the corresponding explanatory and control variables for this framework; i signify cross-sectional dimension or the individual firms and t represents time series dimension; and Ɛ is the error term.

Analysis and Findings

Descriptive Statistics

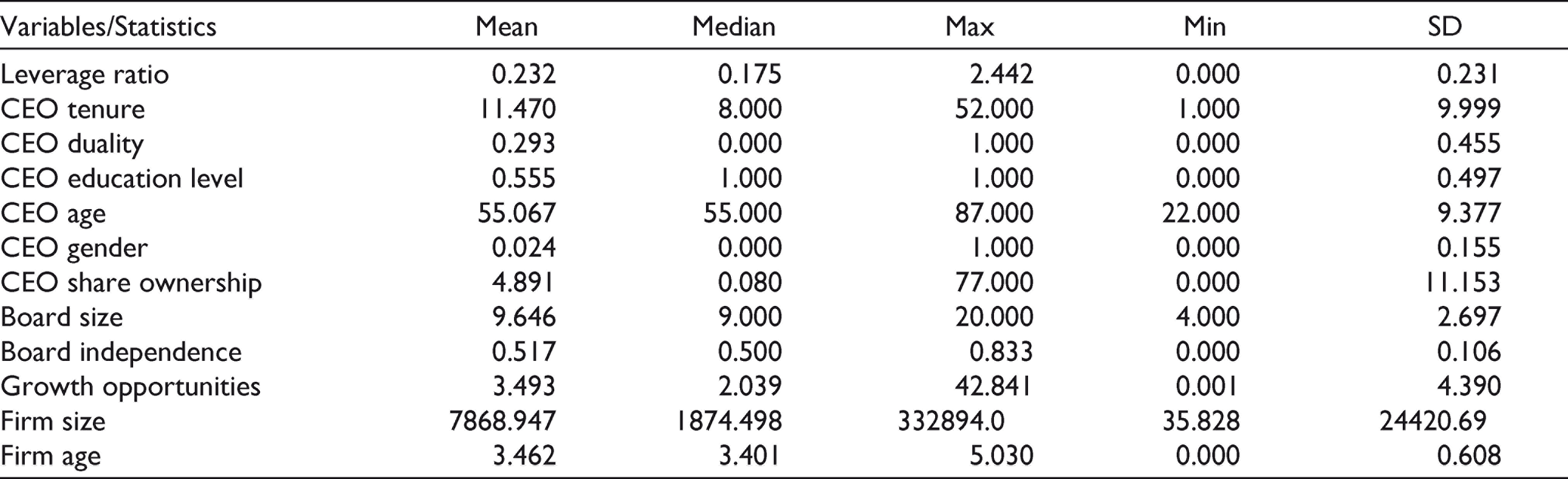

Table 2 furnishes the summary statistics of the parameters incorporated in the analysis. The average leverage ratio is 0.232 across the companies in our sample. This gives the impression that total debt seems to account for less than half of the capital of the organizations. In other words, 23 per cent of the total assets are backed or funded through debt capital. Average CEO tenure for the sample firms approaches 11.47 higher than the median value. Clearly, the variation in CEO tenure is quite extraordinary ranging between values of 1 and 52, backed by an inflated value of standard deviation (10). This means that a great portion of our sampled CEOs enjoy a relatively longer tenure. A longer CEO tenure implies that a company’s board has historically been inclined to retain this executive role. As can be perceived, CEOs have a median age of 55 years which shows that on an average Indian CEOs belong to the middle age category. It indicates that most of the CEOs fall in the period between early adulthood and old age, usually considered as the years from about 45 to 65 as per US census. Only 2 per cent of the studied CEOs are female, demonstrating that under representation of females on boards of directors as CEOs continues to be a subject of importance for researchers, shareholders, government and society. It shows that women continue to face unique challenges in their climb to the top of the corporate ladder. CEO duality is uncommon within the sample as its mean value is as little as 0.29, signifying that executives holding both the titles of CEO and chairperson is not a common feature of Indian firms. This implies that in a country like India, the separation of the positions of CEO and chairman is looked upon as a prudent move, taking into consideration the benefits of such separation. Besides this, about 55 per cent of the CEOs have postgraduate degrees signifying that they are well-educated professionals. The most prominent postgraduate degree came out to be MBA which demonstrates increasing professionalization in the Indian corporate sector. Lastly, the average CEOs’ share ownership is 4.8 per cent with a maximum shareholding of 77 per cent which implies concentrated shareholdings in the Indian corporate world. The ownership concentration reveals the fact that Indian listed companies are largely family owned.

Summary Statistics of Sample Variables (n = 1,535 observations)

Panel Regression Results Determining the Relationship Between CEOs’ Characteristics and Corporate Financing

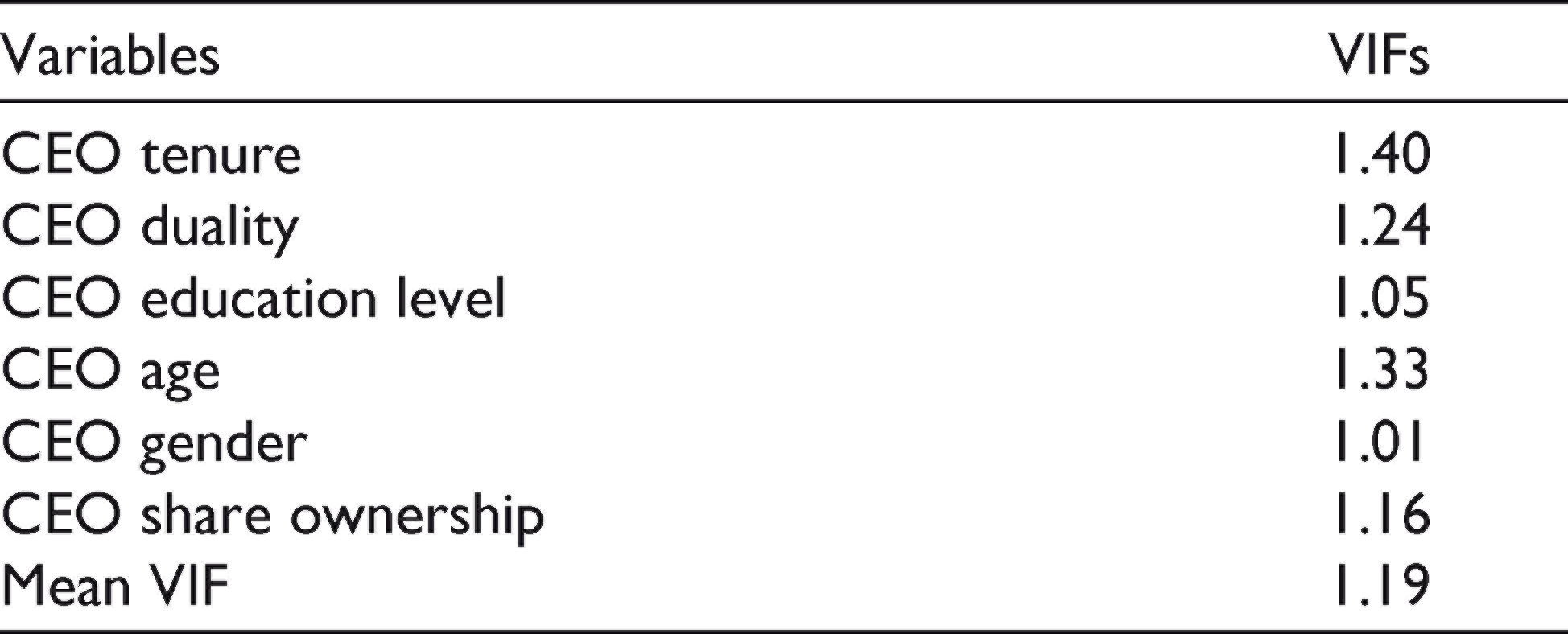

Before running regressions, the research framework is tested to confirm that it does not go through the problems of multicollinearity and heteroskedasticity. The issue of multicollinearity may arise if two or more independent variables are highly correlated. It may affect the estimation of the regression parameters (Hair et al., 2010). It can be detected either by examining the correlation matrix or by the variance inflation factor (VIF). The most common multicollinearity detection test is the variance inflation factor (VIF) for each independent variable. If the (VIF) is more than 10 for any independent variable, it indicates that this variable is highly explained by other variables and might be considered for exclusion from the model. For this study, the VIFs for all the independent variables was reported as shown in Table 3. The table depicts that the values are far lower than the cut off value of 10 as suggested by Hair et al. 2010 and thus confirm the absence of the multicollinearity issue. Second, an examination was undertaken with regard to heteroskedasticity of residuals and subsequently the findings have been stated using heteroskedasticity consistent standard errors as suggested by Arellano (2003).

Result of the Multicollinearity Test

Simple pooled OLS regression cannot adjust for firm-specific or time-specific effects. The fixed effect model (FEM) and random effect model (REM) can solve this problem. Various diagnostic tests are engaged to examine the suitability of one model over the other. The results of f statistics (which help examine the application of fixed effects model over pooled regression), Breusch-Pagan LM statistics (which help examine the appropriateness of random effects model over pooled regression) and Hausman test (to make a decision with regard to the application of fixed effects or random effects model) are shown in Table 4. The significant f and Breusch-Pagan LM statistics suggest application of fixed and random effects model respectively over pooled regression model. Further, the insignificant chi-square statistics for Hausman test recommends the application of random effects model over fixed effects model.

Panel Diagnostics

Thus, in order to validate the nature of relationship between CEOs’ characteristics and corporate financing, the study makes use of panel data regression by means of random effect model for a five-year period. The model indicates that the companies have a common mean value for the intercept. On the whole, the delivered results substantiate that the CEO traits may account for variation in company’s leverage. Panel regression results in Table 5 indicate that CEO tenure is significantly and positively associated to firm’s leverage (p value 0.02 < 0.05) and is consistent with the study conducted by Ting et al. (2016) for the possible reason that long-tenured CEOs mount up a track record, attain a profound knowledge of the firm’s settings, and acquire job- and firm-specific skills (Simsek, 2007). Moreover, a long tenure of CEO reflects strong networks and alliances with important stakeholders that allow the CEO to compose, foster and support risky initiatives like raising debt. Chen and Zheng (2014) also affirmed that the declining career concerns related with longer tenure intensifies the risk-taking capability of a CEO. Thus, the impression of a risk-prone CEO that appears from our results is not that of energetic and young, as is commonly existing in the literature, but instead, a matured and experienced individual with implicit knowledge of the organization and its environment. It seems that as our CEOs gather a track record and develop firm- and job-specific expertise as well as knowledge, they became more confident and competent in corporate financing. This finding may appear contradictory, as risk-taking propensity necessitates a willingness to welcome uncertainty and strategic change which would seem to support short tenure. The problems of short tenure, however, seem to exceed the advantages, whereas the benefits of extended tenure—firm-specific social and human capital, power and knowledge—seem to outweigh the liabilities of maintaining the status quo and rigidity.

Panel Regression Results of Influence of CEOs’ Characteristics on Corporate Financing

As portrayed in Table 5, the level of leverage is higher at organizations where CEOs are younger because age is significantly and negatively linked to corporate leverage with p value slightly above 0.05. It may be on account of the fact that career and financial securities are imperative to a greater extent for older executives, therefore they may evade risky engagements that may interfere with their securities (Carlsson & Karlsson, 1970). Similarly, executives coming from older age brackets are not as much aggressive or audacious as those coming from younger brackets because the elder executives favour and accept lower investment and leverage levels (Bertrand & Schoar, 2003). Longing for career success on the part of younger CEOs can also be one of the important factors. Therefore, younger CEOs have greater inducement for innovations and investment instead of maintaining an average, steady, long-term growth. They prefer lucrative financial strategy and thus involve in active financial activities. Hence, risk-taking level is substantial at firms where executives are younger.

The results also display that CEO share ownership has a significantly negative relationship to leverage at 10 per cent significance level supporting the theory of Friend and Hasbrouck (1988) who hypothesized that managerial insiders (directors and officers) have a personal motivation to cause the organization to use less than the ideal amount of debt in its capital mix. They suggest that this occurs because these executives have a large share of their personal wealth capitalized in the firm in the shape of firm-specific human capital and common stock holdings. This makes managerial insiders unwilling to use the optimum amount of debt funding for the firm for the reason that additional bankruptcy risk associated with higher levels of debt may arise. The negative relationship between CEO ownership and corporate financing indicates that increased share ownership brings into line the managers’ interests with the interests of external shareholders and minimizes the role of debt acting as a tool to alleviate the agency problems. Moreover, this finding approves that high leverage is less appealing to executives because it inflicts higher risk to them as compared to public investors.

However, CEO duality, education level and gender have no significant impact on corporate leverage as consistent with the findings of prior literature. CEO duality is found insignificantly positive with leverage ratio. The finding is consistent with Sheikh and Wang (2012) and Heng et al. (2012). The insignificant relationship between CEO education level and leverage is in line with the study conducted by Wang et al. (2016). Likewise, the insignificant impact of CEO gender is consistent with the findings as drawn by Coleman and Cohn (2000) who found that there seem to be no significant differences in debt usage between males and females, and gender is not an important predictor of financial leverage.

Table 5 also reveals that the control variable growth opportunities as measured by Tobin’s q is significantly and negatively associated with firm’s leverage (p value 0.00 < 0.01). As maintained by the trade-off theory, there is an inverse correlation between growth opportunities and level of leverage because creditors and firms have a lower tendency to engage on new ventures with high costs and uncertainty linked (Rajan & Zingales, 1995; Titman & Wessels, 1988). However, it is suggested that corporations with high growth prospects must consider the usage of credit resources for the reason that cost of capital of such resources may be cheaper as compared to the internal financing. On the other side, firm size has a significantly positive impact on leverage at 10 per cent significance level as the greater the size of the organization, the higher the possibility to support more debt in its capital structure (Rajan & Zingales, 1995). It entails that the size of the organizations is material when the question is about debt financing. The listed firms therefore must be concerned more with the value added or the quality of the assets they are procuring. Table 5 also illustrates that the dummy variables for Industry 1 (office administrative and support activities), Industry 5 (electricity and gas industry), Industry 7 (manufacture of cement), Industry 10 (manufacture of textiles industry) and Industry 12 (telecommunications) are significantly and positively associated to firm’s leverage indicating the capital-intensive nature of these industries requiring significant financial resources. There may not be a single ideal industry capital structure given that there exists considerable variation in company’s financial structure within industry, although the study provides indication that industries are essential in determining a firm’s capital structure. This implies that there may be a number of optimal capital structures inside an industry taking into consideration the nature of the industry.

Our results are consistent with the findings of Berger et al. (1997) who found a negative association between board size and company’s gearing level. It is assumed that considerable number of directors on the panel pushes the managers to trace lower level of debt to raise organizational performance. The results of the analysis also demonstrate that the board independence through the appointment of more independent directors is positively linked to leverage. The positive association between board independence and leverage approves earlier findings by Berger et al. (1997) and Jensen (1986) that firms with greater leverage are likely to have more outside executives. It also supports the claim by Pfeffer and Salancik (1978) that when a company has more external executives, it enhances the firm’s capability to protect itself from the external environment that in turn increases the capability of the firm to rear funds or increase its worth. It must however be taken into account that board size and independence of the board are insignificant in interpreting the leverage ratio. Similarly, firm age exhibits a positive relationship with leverage ratio though the association is not statistically significant but is consistent with the results of Bokpin and Arko (2009).

Limitations and Future Research

A few limitations are required to be noted while comprehending the findings provided in this research article. First, the sample is confined to companies part of Nifty 500 Index and henceforth, the findings might not be pertinent for enterprises which are operating on a small scale or to concerns operating outside India. Forthcoming studies may perhaps also attempt to experiment with the same relationship by inculcating financial and unlisted companies which are not forming a part of this study. Second, in view of the fact that the data on CEO traits was gathered by hand, the time period for the sample is narrowed to five annual years only, and hereafter, prolonged impact of CEO traits on company’s leverage could not be investigated based on these statistics. Third, apart from the scrutinized attributes, other soft and psychological factors can have repercussions on firm’s leverage. Owing to unobtainability of information, further analysis using additional traits was not able to carry out in this article, nonetheless future studies may possibly study, the influence of executive remuneration, work experience, directorships, professional background or founder status while conducting studies on corporate growth, human capital investment and the determinants of risk-taking. An alternative avenue of interest would be to examine the relationship with different risk proxies and to make comparisons with the traditional options. Lastly, by exclusively focusing on the CEO, we built an implicit assumption concerning the power distribution in the upper levels of management. Yet various authors (e.g., Frank and Goyal, 2007) have contended that the chief financial officer (CFO) might also be imperative, especially in case of financial decisions which may serve as a base for future studies.

Conclusion and Implications

A unidirectional relationship of our discussion assumes that being over-leveraged is inherently superior to being under-leveraged which is supported by the previous literature. Ross (1977) suggested that the values of firms will increase with leverage because increasing leverage increases the market’s perception of value. According to Heinkel (1982), more valuable firms have larger volume of debt financing. Noe (1988) showed that the average quality of firms financing with debt is always greater than those opting for equity financing. Besides this, Hadlock and James (2002) concluded that companies favour debt (loan) financing as they anticipate a greater return. As stated by Champion (1999), use of leverage is one approach to improve the firm performance. Similarly, Roden and Lewellen (1995) established a significant positive association concerning profitability and total debt. Therefore, it seems that while making capital structure decisions risk-seeking behaviour favouring high corporate leverage is important and should be encouraged.

Our findings put forward that boards must endeavour to nurture an essence of commitment and risk-seeking amid their managers because whether or not the organization follows performance-intensifying business initiatives, these seem to be critically moulded by managerial risk-taking tendency. Although personal character traits are hard to modify, encouraging a risk-seeking attitude is viable and may perhaps be made a part of incentive systems and managerial training programmes. Moreover, recurrent job changes among the senior officials should be discouraged because the subsequent short-term focus, dearth of firm-specific knowledge and insufficient socialization might promote risk evasion.

CEO age is positively associated with the low-level choice of leverage which shows that elder executives desire a more conservative capital structure, whereas younger executives endeavour to take more risk. The managers thus employed need to be familiar with the dealings of the organization despite their young age and there is a need to bring diversification in the management so as to take advantage from the skills and services of the young.

The inverse association between the proportion of the company’s common stock carried by the CEO and firm’s leverage specifies that a high level of managerial ownership may entrench management and generate agency snags. Managers with considerable voting power are possibly to take actions beneficial to themselves at the cost of outside shareholders. Managerial entrenchment could give rise to less use of debt than is ideal because entrenched managers may wish to reduce firm risk in order to safeguard their under-diversified human capital. It can also be said that because managers have put in a large share of their wealth in the firm in terms of shareholdings and firm-specific human capital, they have higher incentives than average shareholders to retain low use of debt in the capital structure.

However, the observed managerial traits do not explain for a good deal of the variance in leverage. The difficulty in fully elucidating the relationship may itself plug to something deeper. Possibly the CEO is actually portraying more than its personality as the CEO does not manage an organization in isolation and several other people are also involved. For instance the Chief Financial Officer (CFO) might indeed be accountable for corporate financing or the firm’s leverage choices. Therefore it may not be wrong to say that greater attention to the top management team rather than confining to the CEO might show interesting results.

This study also has concrete implications. Companies may have an advantage from our research findings because we deliver evidence of variables which significantly affect a firm’s financial structure. For instance, external and internal stakeholders concerned in knowing a company’s capital structure may benefit from our investigation in evaluating the possible factors that influence this system and can use our results to support their analyses. The results can assist the organizational decision-makers such as shareholders and policymakers make policies pertaining to CEO retention and selection decisions. The findings are pertinent for investors and corporate managers of the company for whom the characteristics of CEOs may be regarded as an essential source of knowledge for formulating and implementing investment policy. For instance, firms who desire to pursue risky policies and investments while employing a CEO, should consider appointing a long-tenured and younger CEO in order to promote entrepreneurial events. The advantage of the study goes to the corporations’ management in improving optimum capital structure and to the policymakers to assist in policy building to govern organizations based on a profound understanding of the effect of CEOs’ characteristics on corporate financing. This study has important implications for investigators of corporate governance which need to be careful in applying theories which are developed in western settings to emerging market framework. Emerging markets are highly dissimilar from developed markets with regard to institutional development, social, cultural, political and historical aspects. Therefore, there is a need to look for mid-range theories or evolutionary theories to understand these relationships in a better way (Shen, 2003).

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.