Abstract

A leading concern in client and vender relations is that the rising new situation of influence deploying of the credit card market. This situation is accountable for compulsive buying, which has disapprovingly exaggerated consumers, leading to impossible debt levels. Financial counsellors search for why and how individuals get themselves into financial debt. Compulsive buying behaviour and credit card could have a powerful effect on consumers’ financial stability. Further, in place of comprehending credit card usage and compulsive buying, this study correlates them with wealth attitudes such as power-prestige, financial knowledge and retention time. A cross-sectional descriptive research design using convenience sampling and non-probability sampling with quota samples of 313 credit cardholders was surveyed. The outcome showed that those with power-prestige money attitudes are likely to have free usage of credit cards through compulsive spending. Results also showed that those with a higher financial understanding have lower compulsive spending off the credit card.

Introduction

In the current scenario of innovation, market opportunities are available in the globalized market’s postmodern trade. The marketers of competitive products manufacture and supply assortment of products with numeral brands to decide. These products are embattled and targeted to the consumers in all feasible ways of marketer’s push strategy. Philosophy of consumerism is purchase at this instant and pay later. Under these circumstances, there is an essential linkage between the retail segment and the credit card market. People deny as they are inspired, compelled to devour or compulsive buying. In the past few years, consumer behaviour is the theme of concern for many academics, and select areas in many subjects among consumer actions are compulsive buying (Johnson & Attmann, 2009). The individuals passionate for shopping, engaged habitually in buying, are compulsive buyers (Boundy, 2000).

Furthermore, as an unusual outline of buying behaviour of consumer, it is identified as the mysterious elevation of consumption (Shiffman & Kanuk, 2000); a fascinating summit to consider concerning compulsive buyers who acquire merely the effect of the end user with a service or objective, but in addition for achieving satisfying emotion throughout the process of buying (O’Guinn & Faber, 1989). Money attitude plays an important role in consumer spending behaviour through credit cards. A positive money attitude leads to less compulsive buyers and less tendency to get involved with financial crisis than negative money attitudes. The person having a negative money attitude usually spends more money emotionally rather than rationally, which leads to improper money management of their financial resources. Leading to a debt problem, if not dealt with appropriately, can eventually result in bankruptcy among these types of consumers. The situation is made worse with the availability of credit cards, which enables consumers to spend more in advance before getting their pay. The phenomenon of using a credit card is increasing. The application is much easier as banks are competing aggressively in trying to expand their credit card market shares among the consumers. Consumers are encouraged to obtain more credit cards for usage, thus increasing credit availability for their spending. The financial choices a person makes when they begin adulthood will affect whether they become one of the many. Spending habits are healthy as the use of credit cards can affect a person’s financial stability throughout their lifetime. Therefore, individuals need to learn good spending choices before becoming adults and entering into the realm of credit.

Leclerc concluded in her 2012 article that individuals are especially inclined to acquire significant amounts of credit card debt due to ‘easy access’ (Leclerc, 2012). There is a connection between debt due to a credit card and compulsive buying (Joireman et al., 2010). Financial solidity is very significant, particularly for those who are presently opening out on their own. Compulsive buying with the usage of credit cards could have a powerful effect on a person’s financial stability. In the process to further understand compulsive buying behaviour along with credit card usage, this study correlates them with money attitudes and fiscal knowledge. As power-prestige relates to usage of funds for power and status, financial education relates to individual financial matters: in banking, interest rates, insurance, and retirement funds. Retention-time is careful planning and saving of money.

Within lieu of literature, the focal objective of the study is to observe attitudes scale by Yamauchi and Templar (1982) for retention time, power-prestige and financial knowledge in comparison with compulsive buying of credit card use.

Theoretical Background

Credit Card Market and Compulsive Buying

In the course of globalization from the past 15 years, literature is mainly Western, for Indian retail upbringing provides a comparable picture. Retail sales in India account for 10–11 per cent and amount to US$180 billion of GDP. Almost with approximately 12 million outlets, the Indian retail markets are leading retail outlet compactness around the globe having brighter prospects, propelled with the rapid changes in lifestyle within the Indian domestic scenario. Indian shoppers are progressively focusing on value, variety, convenience along with enhanced experience of shopping. Increase quality, diversity and accessibility of products have resulted in high spending power, employing supermarkets for their shopping (Gupta, 2015). According to the research by KSA Techno Park in the consumer outlook magazine 2014 shows that as compared to elders, expenses of youth has increased over three years, and teenagers are getting more affluent with each short year.

According to a recent research survey of global management consultant McKinsey, the credit card user market is anticipated at 18–20 million in India. Leading the credit card user youth, ICICI Bank with standard spends annually of Rs. 32,000 as per card (similar to that of more advanced markets such as Malaysia and Taiwan). ICICI Bank (Sharma & Abraham, 2012), with the highest promotions in the current structure, claims to attach 100,000 fresh customers each month, whereas Citibank connects 70,000–80,000 along with SBI adding 70,000–75,000 cards users every month. Further, the other forms of the marketplace where credit is required are housing loans, automotive loans, personal loans and education loans. Improving service quality has become the tool that banks utilize to retain customers (Nambiar et al., 2019).

The credit card users in India are hiking rapidly, and expanding affluence is likely to erode Indians’ persistent indisposition to expend on credit as they have valued thrift and frugality. According to a survey by MasterCard International, the Indian credit card diligence is in the nascent stage relatively as compared with the economics in West Asia. The results of the report indicate the highly increasing potential growth for the credit card market in the Indian economy. Very less research considering the Indian consumers exists. Therefore, this study gains importance for examining factors influencing the compulsive buying actions.

Compulsive Buying and Credit Card Usage

Compulsive buying behaviour is motionless mystified by impulse buying, even though these are two different concepts. Impulsive buying behaviour is aggravated as an external activate, whereas compulsive buying is motivated by an internal activate. Habitual buying behaviour may build addictive buying after converting into an always spending habit to lessen anxiety. Those shoppers who consistently capitulate to compulsive buying can be assigned as psychographic attributes such as depression, low self-esteem, impulsiveness and small emotional stability (Johnson & Attman, 2009). Credit card convention habit is recommended among money attitudes (power, anxiety and distrust as independent variables) and compulsive buying as dependent variable (Roberts & Jones, 2001).

Psychological Traits and Compulsive Buying

The mishandling of credit card further plays the same role (moderating variable) between psychological traits of consumers as power-prestige, self-esteem, risk-taking and compulsive buying. The general profile of credit card users is educated, active, mobile and socially engaged individuals from higher income groups. Furthermore, it describes credit card users as graduates, having managerial or professional occupations.

Money Attitude and Credit Behaviour

The money attitude scale developed by Hayhoe et al. (1999) initiated a significant difference within the money attitude of individuals who have a credit card and who were not using a credit card. The base of money attitude is the responses to behavioural questions, feeling, knowledge linked with a credit card and circling debt. It relates a valid credit attitude score relating to happiness from carrying credit cards. Pahlevan and Yeoh (2018) instigated a positive association between money attitude towards credit and probability of taking credit card balance. Robb (2011) found financial knowledge on a higher level positively associated among the individuals carrying credit card balance.

Financial Knowledge

Superior financial information might consequence a lot of positive behavior, just as long as education doesn’t ensure improvement. It is not adequate that the programmes would improve the commercial experience if the influence of augmented financial knowledge on consumer behaviour is not entirely implicit. Recent research by Robb and Sharpe (2009) initiated higher levels of financial expertise that ultimately linked with carrying the credit card balance among individuals.

Further Literature Review

The pasture of consumer behaviour has been borrowed traditionally from behavioural sciences, mainly cognitive psychology, in emergent models of the consumer decision cycle. Consumer behavioural studies clarify that persons and the environment are stimuli according to the consumer behaviour model (Schiffman & Kanuk, 2004). The replica covers the individual aspects of motivation, perception or desire, personality, learning, emotions and attitudes. They hope that to emerge and be alleged well by others can also be a stimulus. This incentive pressures persons to fulfil it. A person’s cognitive functioning acts as a regulator in determining the direction taken to address the stimulus. Cognitive psychology seems to be inappropriate for explaining the low involvement of consumers’ behaviour. The behavioural theory of learning has used to describe small participation cases where consumers put modest thought into decision-making (Rothschild & Gaidis, 1981). According to philosophy of behavioural science, the reasoned action by Martin Fishbein in 1960 with the focal point on the importance of pre-existing attitude is responsible in the decision-making process. The foundation theory posits that act of consumers’ behaviour is caused by retention to receive or create a particular outcome. Consumers retain the ability and capability to change minds and then decide on the various cause of action purchases without any instructions to be learned from reasoned action theory. Starting with selling the product to consumers, marketers have to correlate purchases with a positive result. The market’s particular result must be explicit.

The second part of the theory highlights the significance of moving customers throughout the sales pipeline. The demand must comprehend the long lags involving initial intent. Completing the action allows the consumers ample time to talk themselves out of purchase or about outcome of the purchase. Consumer psychology of debt and savings are not addressed in literature as the distinctiveness of consumers with a prospective accumulates extreme debt from studies of credit card usage. Dessart and Kuylen (1996) concludes the probability to possess disproportionate liability are renters, having children between seven to eighteen, and exceptional several balances with dissimilar firms or other family relations.

Further research suggests that the factors which contribute to the crisis of debt include (a) lack of insightful consequences of financial dealings and (b) lack of money management skills. Livingstone (1992) classifies distinctiveness of consumers’ debt and demographic and economic factors that rank debtors and non-debtors.

In literature, the compulsive buying concept was derived from the purchase decision of consumers. In general, it is described as chronic, disproportionate and cyclic purchasing, resulting in adverse life events, negative feelings or inner deficiencies and, therefore, carries robust compensatory components (Faber & Christenson, 1996). Owing to such compulsive buying behaviour, not only the society but the individual’s family is harmed as well, resulting in excessive spending, bankruptcy and extreme indebtedness (McElroy, 1991). Compared to older people, younger inhabitants are expected to use money as a way of power (Faber & Christenson, 1996). The utilization of credit cards when compulsively buying is a recipe for high levels of debt. Another downside to compulsive buying is that a large portion of society is habitual to buying tendencies that would be detrimental to the economy (Roberts, 1998). Numerous factors may persuade credit card debt as a significant amount of research has examined these factors. According to Norvilitis (2006), the strongest predictors of debt are financial knowledge, and there is more research that states that financial education has a more robust relationship with credit card use. Financial planning practices are associated with positive credit habits (Moore & Carpenter, 2009). Lai (2010) initiated that opting for a financial planning course decreases the likelihood of impulse buying. Robb (2011) also found that persons who engaged in more accountable credit card use were more likely to have superior scores on personal financial knowledge. Financial knowledge does not have to be learnt through a course in personal finance (Gupta & Sharma, 2014). Those who were mentored by parents using a ‘hands-on’ technique of financial skills are related to miniature credit card debt in evaluating those who were not mentored (Norvilitis & MacLean, 2010).

Not all research regarding financial knowledge found a link to credit card use or spending. Hancock et al. (2013) found a significant correlation with the possession of more than one credit card, but it was not significant in the final regression analysis. The study with the aim of financial awareness was not linked with inferior levels of compulsive buying. The business education schemes were encouraged practically with the lack of financial knowledge, although specific issues privileged and target audience have varied significantly. These programmes were able to assist researchers in developing a better understanding of the relationship which exists between financial knowledge scores and business education. The initial abundance of education programme has criticized for failing to gather data that have more specific outcomes in nature. Norvilitis and Santa Maria (2002) suggested that the important factors of financial education are skills, like balancing a chequebook and creating a budget. It is not just knowledge but also financial literacy which is crucial in decreasing credit card debt. Money attitude was another factor that was associated with credit card use and compulsive buying behaviour. Attitudes towards possession, compulsive spending and materialism were essential indicators of debt (Norvilitis et al., 2006). Norvilitis et al. (2006) showed no association between attitudes towards behaviour and money. The first dimension, power-prestige, refers to those who have great discernment on cash as a means of power evaluation of success. These communities tend to relate some money as a way to influence and impress themselves. Users who have an authority or position are expected to have developed a power-prestige money attitude (Yamauchi & Templar, 1982). Roberts and Jones (2001) found that compulsive buying behaviour considerably correlates with credit card usage, and power-prestige money attitude is located high in those persons. Hoon and Lim (2001) found individuals acquire objects belongings that confer symbolic respect and power-prestige standing assertively that in revolve might guide to a compulsive aspiration to hold on and make a case for their achievements to develop respect in society. The time-retention factor describes behaviour intended in the future, which requires full plan research (Yamauchi & Temple, 1982). Personages with time-retention attitudes to money are placing great prominence on planning for a protected financial future. In other words, they are more careful about monitoring their financial situations. Such individuals plan their utilization choices and behaviour carefully in expectation of anticipated financial security (Bonsu, 2008). Individual approaches to credit were considered by Xiao et al. (1995), where they developed a Likert rating scale poised with a sequence of statements linking to the credit card.

There is an increasing effect on the usage of credit cards due to technological advancement, as online shopping builds a convenient channel in favour of shopping with services which requires to fulfil their needs (Kushwaha et al., 2017). Previous studies signify that having a credit card in the wallet while shopping point are spending more on the purchase with shorter decision-making period for purchase.

Hypothesis Development

In support of the primary hypothesis, H1 that involved beginning the review of previous research to facilitate power-prestige money attitudes will positively be correlated with high compulsive buying of the credit card. Persons who purchase for status will be more likely to spend more without planning when they see something they think will make them look better—compulsive buying. They may also employ credit cards for these necessary purchases since they may live higher than their means. It hypothesized H2 that retention-time would negatively correlate with top credit card use compared to the compulsive buying of the credit card. The thought behind H2 is that those who have retention-time money attitude will be fewer to employ credit cards since they are careful with their money. The rationale for H3 is that persons with retention-time and money attitudes plan their budget to spend money. Hence, they are less likely to spend compulsively. There was some contradictory research that foresees that financial knowledge will have a negative correlation with a credit card utilization as well as compulsive buying.

The researchers developed a hypothesis for testing based on relevant secondary data and the relationship between variables as follows:

H1: There is a statistically significant linear relationship between power-prestige money attitudes and compulsive spending of credit cards. H2: There is a statistically significant linear relationship between financial knowledge and compulsive spending of the credit card. H3: There is a statistically significant linear relationship between retention-time money attitudes and compulsive spending of a credit card.

Research Methodology

Research Design

Descriptive research design opted for this study. The cross-sectional research method in descriptive research was adapted to address the outlined objectives above.

Sampling Method

Convenience sampling was collected using a non-probability sampling method.

Research Area

The location of this study was Ahmednagar city in Maharashtra, India. Ahmednagar is the largest district, area-wise, in the state of Maharashtra.

Sample Size

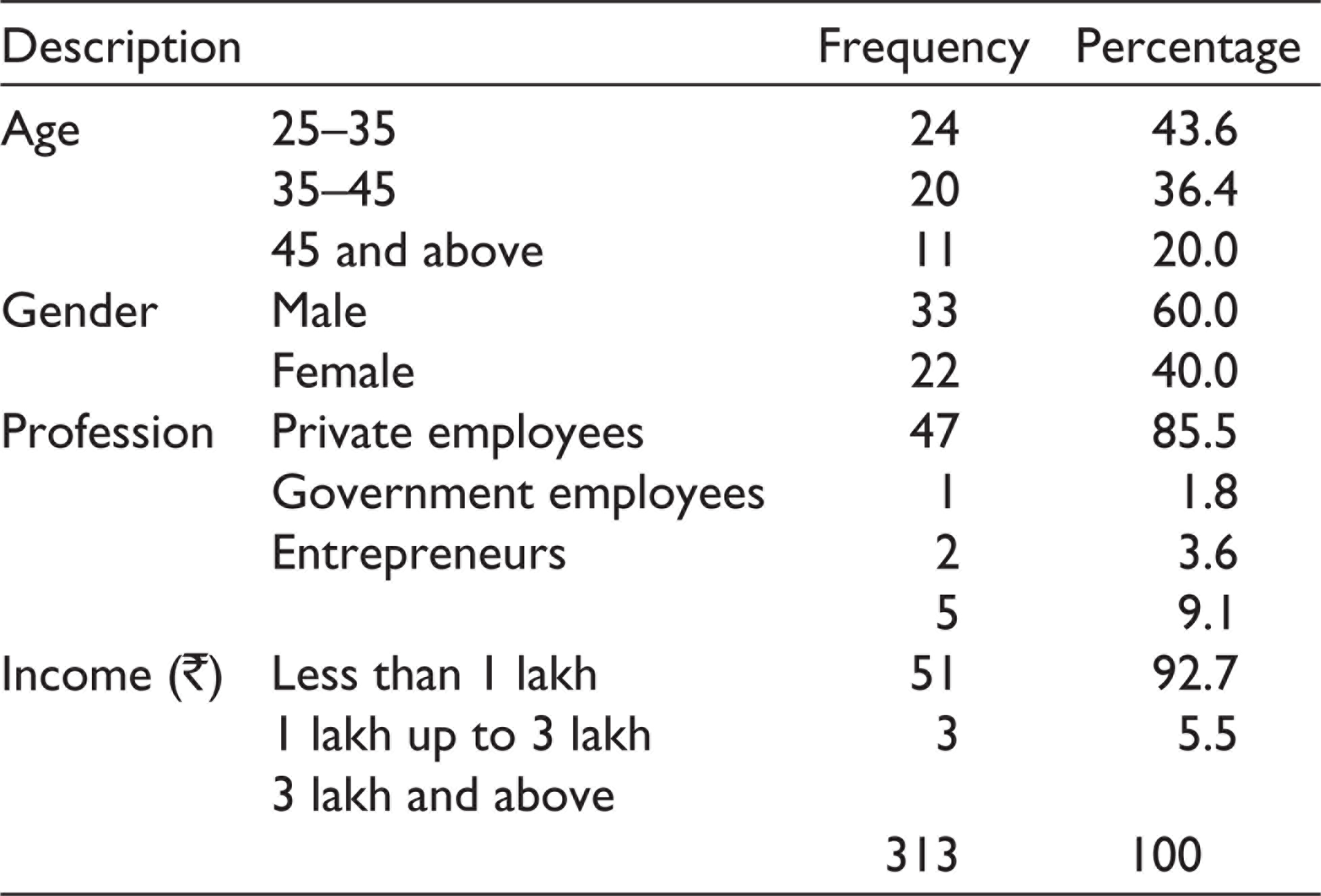

For the current research, 341 respondents were selected for final data collection and who possessed the credit card of the different financial institutes. Data cleaning reduced the participants to 313.

Data Collection Instrument

A well-structured questionnaire was constructed for the collection of primary data. The survey consisted of demographic profiles, including the participant age, gender class, occupation and current income. A better way to collect data was to manage the questionnaire individually. It investigated the influence of prestige, retention time, financial knowledge and using the habit of a credit card on compulsive buying of consumers. Journals, books, newspapers and other published sources were used for secondary data collection to understand the business environment better.

Measures

Questions comprised of scale for money attitude (Yamauchi & Templar, 1982), scale for credit card usage developed by Robert and Jones (2001), Jumpstart Coalition review of individual financial literacy amongst college student (Norvilitis et al., 2006) and scale of compulsive buying behaviour (Valence et al., 1988)

This study questions from the money attitude scale developed by Yamauchi and Templar (1982) that pertained to power-prestige money attitude and retention-time money attitude. The Likert scale on 7 points from ‘never’ to ‘always’ was measured. Power-prestige money attitude is the use of money for power or status. An example of a statement for power-prestige is as follows: ‘Though I must judge the success of inhabitants by their performance, I am more prejudiced with the sum of money they comprise.’ Someone who has a retention-time money attitude thinks it is imperative to save money to be financially stable and create a stable future. One statement involving retention- time money attitudes is as follows: ‘I pursue a cautious financial budget.’

A portion of the Jumpstart Coalition investigation of individual financial literacy among students (Norvilitis et al., 2006) used to enumerate participants’ financial knowledge. Twenty-three questions from this survey were used. Questions were multiple choices that asked about saving, spending and credit cards. Those with more correct answers were considered to have elevated financial knowledge, whereas those with less accurate responses found to have deep business experience. Questions from the scale of compulsive buying (Valence et al., 1988) were used in this study. This scale used a 5-point Likert scale rating from ‘strongly agree’ to ‘strongly disagree’ statements. One of the comments in the range was as follows: ‘When I possess money, I cannot help but spend parts or all of it.’ High scores indicated compulsive buying.

This research used questions regarding credit card usage (Roberts & Jones, 2001). This scale was also a 5-point Likert scale rating statements from ‘strongly agree’ to ‘strongly disagree’.

The statement from the scale was as follows: ‘I regularly use accessible credit on one credit card to compose a payment on another credit card.’ High scores indicated high credit card usage.

Demographic Characteristics of Sample

Data Analysis

Descriptive statistics are shown in Table 2. Correlations tests were used by using the SPSS to determine if there were relationship between financial knowledge, power-prestige, credit card use and impulse spending.

Descriptive Statistics

Correlations Results

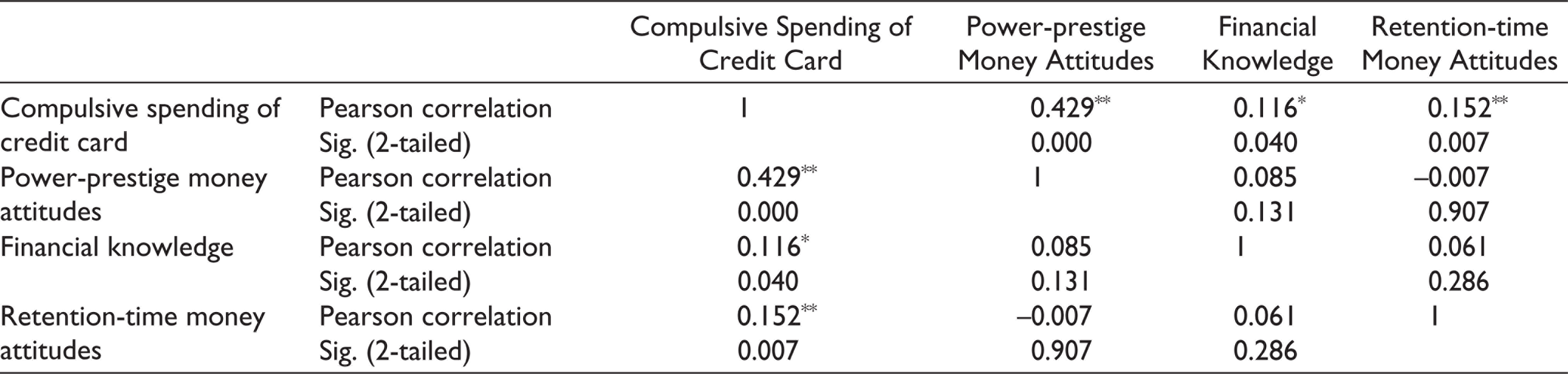

Perhaps, we would have to test H1 for whether there is a statically significant linear association linking power-prestige money attitudes and compulsive spending with a credit card. Correlation of power-prestige money attitudes and compulsive spending credit card (r = 0.429), based on n = 313 observations with pairwise non-missing values, is presented in Table 3. Pearson correlation coefficient is significant for p ≤ .05, two-tailed test. H1 supported our proposition. Similarly, we would have to test H2 for whether there is a statically significant linear association between a financial acquaintance and compulsive spending credit card. There is a correlation between financial knowledge and compulsive spending of credit card (r = 0.116), based on n = 313 observations with pairwise no missing values. Pearson correlation coefficient is significant for p ≤ .05, two-tailed test. H1 supported our proposition.

Correlationsa

* Correlation is significant at the 0.05 level (2-tailed).

a. Listwise N = 313.

At last, we would have to test H3 for whether there is a statically significant linear affiliation between retention-time money attitudes and compulsive spending with a credit card. There is correlation of retention-time money attitudes and compulsive spending using credit card (r = .152), based on n = 313 observations with pairwise no missing values. Pearson correlation coefficient is significant for p ≤ .05, two-tailed test. H3 did not support our proposition.

Conclusion and Discussion

The current study analysis concludes with (correlation) indicating each money attitude proportions have a relationship with compulsive buying, those who exhibit Power-Prestige money attitude incline to have free credit card usage resulting in higher compulsive spending. Roberts and Jones (2001) stated that compulsive buyers are anticipated to be associated with buying for a social category in addition (Phau & Woo, 2008) has revealed the relationship among the vision of money as an instrument of power and prestige and compulsive buying was acceptable and vindicated. The present research establishes that credit cardholders in a recreation of personality discovery are predisposed to correlate money as a method of achieving a preferred prominent and well-known image. For these persons, status is regarded through the possession of class products rather than through family reputation or personally. It is this approach that indicates the significance of status-seeking, acquisition, external recognition and competition.

Credit Card Usage and Compulsive Buying

This study confirms previous research by Lai (2010), Norvilitis et al. (2006), and Roberts and Jones (2001) recommending that credit card practice exaggerate the difficulty of persuasive buying. Credit card practice happens more momentous and implies to facilitate credit cardholders to be inclined to boost their money attitudes. However, they have access to credit cards, resulting in increasing their compulsive buying behaviour (Vieira et al., 2016). The improvement in internet technology may affect the increase of credit card usage as technology provides consumers with a suitable channel to shop for services and goods (Sharma, 2008). Further, it can be assumed that frequent credit card usage may add to compulsive buying, mainly when credit card holders are not capable of managing their purchasing behaviour. Analysing credit card usage and money attitude revels a transparent picture of how youth perceives money addition how this financial knowledge of money sense towards themselves and a variety of services or product. This research study reinforces the judgement that credit card habits may stimulate expenditure and strengthen the association among attitude towards compulsive buying and money.

Financial Literacy and Compulsive Buying

Financial knowledge was found to be connected with lower levels of compulsive buying in research conducted by (Brougham et al., 2011). This research clarifies that those with high financial literacy tend to have lower credit card employ and lower compulsive buying tendency. The research advocates the research by Potrich and Vieira (2018): The impact of financial literacy on compulsive buying behaviour and other behavioural aspects.

Retention Time and compulsive Buying

The present study justifies the previous research (Simanjuntak & Ambar, 2016) finding a negative correlation between retention-time money attitudes, credit card debt and compulsive buying. The present study did not find that those with retention-time money attitude had lower credit card use and lower compulsive spending. One factor that could affect retention-time money attitude and credit card use could be that people can use credit cards responsibly to build their credit (Veludo-de-Oliveira et al., 2014). Therefore, the use of credit cards is not always wrong.

Importance/Contribution of Study

This study contributes to two components that can significantly affect the cardholder’s debt (credit card usage and compulsive buying) and their relationship with two other ingredients, that is, financial knowledge and money attitude.

Suggestions

Giving people more opportunities to gain financial literacy could help them stay financially stable and avoid debt, but more research is needed before reaching this conclusion. The objective of consumer protection is to focus on the problem of debt to empower consumers through education. Requiring a personal finance class in schools and colleges could also increase the cardholder’s financial literacy. Many consumers get themselves into trouble simply because they have little or no idea where their money goes. Avoid cash advances and exceeding the credit limit—the information provided by government authorities and agencies, credit card industry and credit counselling entities. It becomes essential to address the temporal perspective that covers consumer’s perception of their spending and saving behaviour. Banks must counsel customers to avoid debt and from filing for bankruptcy, thereby making it difficult for the banks to collect. At the macroscopic level, the government can and must do more to stop many of the abuses in the credit card industry. For example, columnist Michael Schrage has an interesting suggestion: a sin tax of 2 per cent on credit and charge card purchases. The imposed tax would elevate income for the government and help restrict credit card expenditures and debt. The government can also restrain the marketing efforts of credit card companies. Smoking causes harm to people’s physical health. Likewise, excessive credit card debt also lowers their financial health. Credit card marketers should coordinate credit limits on all cards in possession of an individual so that it is impossible to run up a total debt far beyond the individual’s ability to pay. They should straight away increase efforts to engage young college going youth. Make it even more apparent that all the money borrowed and all the interest accrued must eventually be paid. Limit the number of any one type of credit card that a person can hold. For example, Visa might consider a policy that no person may hold more than one of the credit cards and limitations on the profits from credit cards. Another possibility would be to restrict mail and telephonic campaigns offering various inducements to accept new credit card. The credit card industry must take the aforementioned steps to reduce the burden of the credit card debt among the individuals. Consumers may enhance their financial decisions as they are aware of the impact of the current prospect dichotomy on their behaviour.

Limitations of This Study

Respondents were selected from Ahmednagar district only. The result of this study may vary with the change in location of the respondent. Since the study was carried in Ahmednagar city, the results cannot be applied to other geographical areas.

Information for Future Research

Present research findings, along with prior investigations, propose that credit cards do assist compulsive buying behaviour. Conversely, results cannot be seen as specific. Further cautious experiments and research studies are desirable to help improve understanding of the role of credit cards in compulsive buying. There was a limited amount of research regarding retention-time money attitudes with compulsive buying and credit card usage. Advanced investigation in this area is highly recommended. Another prospect is to explore the different delivery mechanisms relating to financial knowledge that individuals would instead prefer. It is equally essential to understand the developmental influences on the acquirement of money-management skills with specific consumption patterns. Primarily, the procedure by which youth are acculturated into a modern market economy in which debt and saving play a significant role must be investigated (Lewis, 1999). Likewise, the collision of early utilization of dysfunctional buying behaviour should be examined. Norvilitis et al. (2003) hearsay that, for instance, in adolescents, the pattern of compulsive buying begins to emerge a variety of independent consumption decisions with some financial responsibility acquired at the age when students are in college. Understanding the forces that shape such decisions can help to examine a lot of these adult compulsive behaviors. Future research should also explore consumption behaviour, for instance, (Lunt, 2000) dispute that savings afford present income drawn from past returns and borrowing provides current resources strained from future income. Inhabitants with different temporal orientations, likely to plan purchases or buy on impulse behaviour, must be investigated.

To conclude, the overuse and interrelationship between compulsive buying and impulsive buying must be investigated in a chronological direction. Based on current research on compulsive buying, other functions such as price, anxiety, sensitivity, and conspicuous consumption and usage of credit card positioned as possible moderators must be studied for future study.

Footnotes

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.